Fruit Beer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

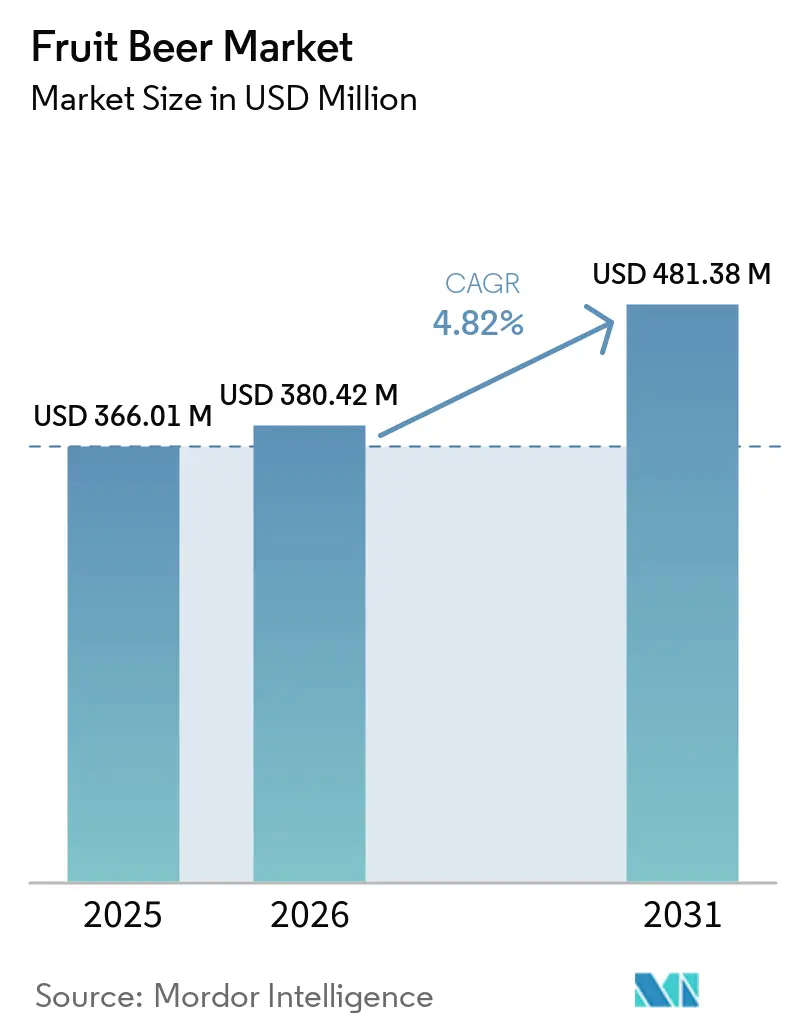

| Market Size (2026) | USD 380.42 Million |

| Market Size (2031) | USD 481.38 Million |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fruit Beer Market Analysis by Mordor Intelligence

The global fruit beer market was valued at USD 366.01 million in 2025 and is projected to grow to USD 380.42 million in 2026, reaching USD 481.38 million by 2031, with a CAGR of 4.82% during the forecast period of 2026–2031. This growth is primarily attributed to the rising consumer preference for flavorful, refreshing, and innovative alcoholic beverages that provide unique taste experiences beyond traditional beer. Shifting drinking preferences have driven demand for beverages with smoother flavor profiles, reduced bitterness, and enhanced sensory appeal through fruit-based formulations. Additionally, consumers are increasingly exploring variety and experimentation in their beverage choices, boosting the popularity of fruit-infused beers known for their distinctive aromas, sweetness, and balanced taste profiles.

Key Report Takeaways

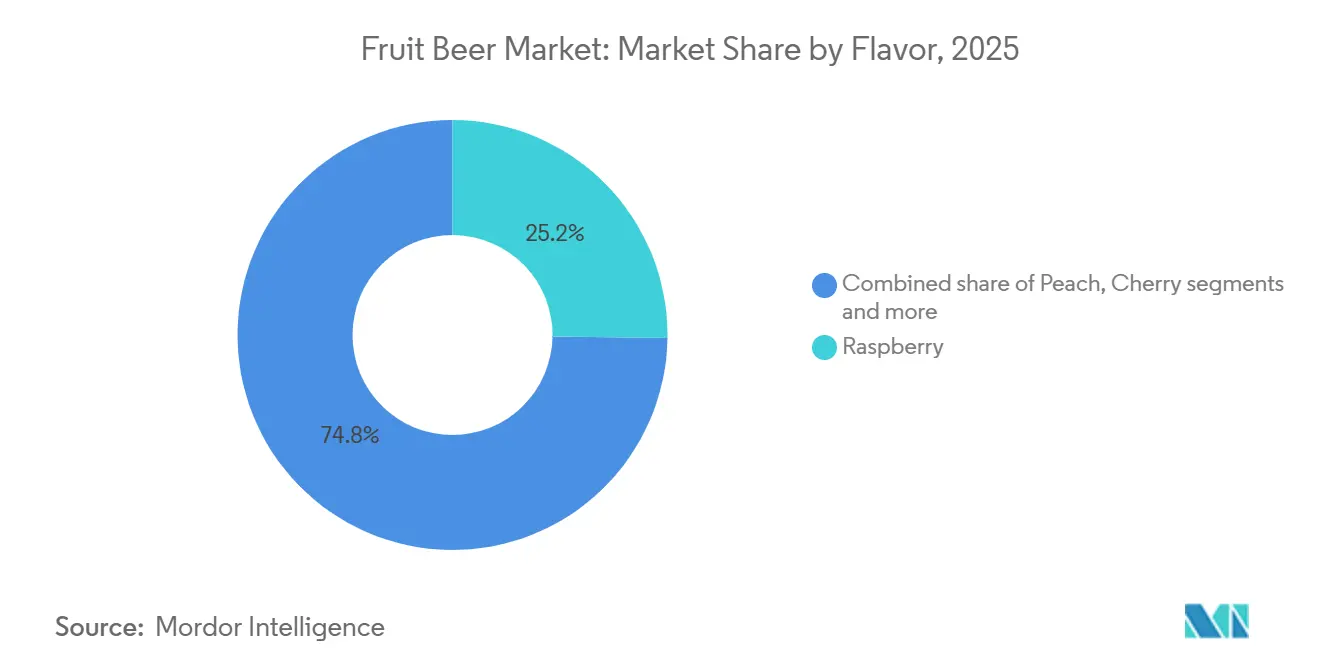

- By flavor, raspberry led with 25.22% revenue share in 2025, while peach is forecast to expand at a 5.45% CAGR through 2031.

- By alcohol content, non-alcoholic held 34.04% of revenue in 2025 and also recorded the highest projected CAGR at 6.13% through 2031.

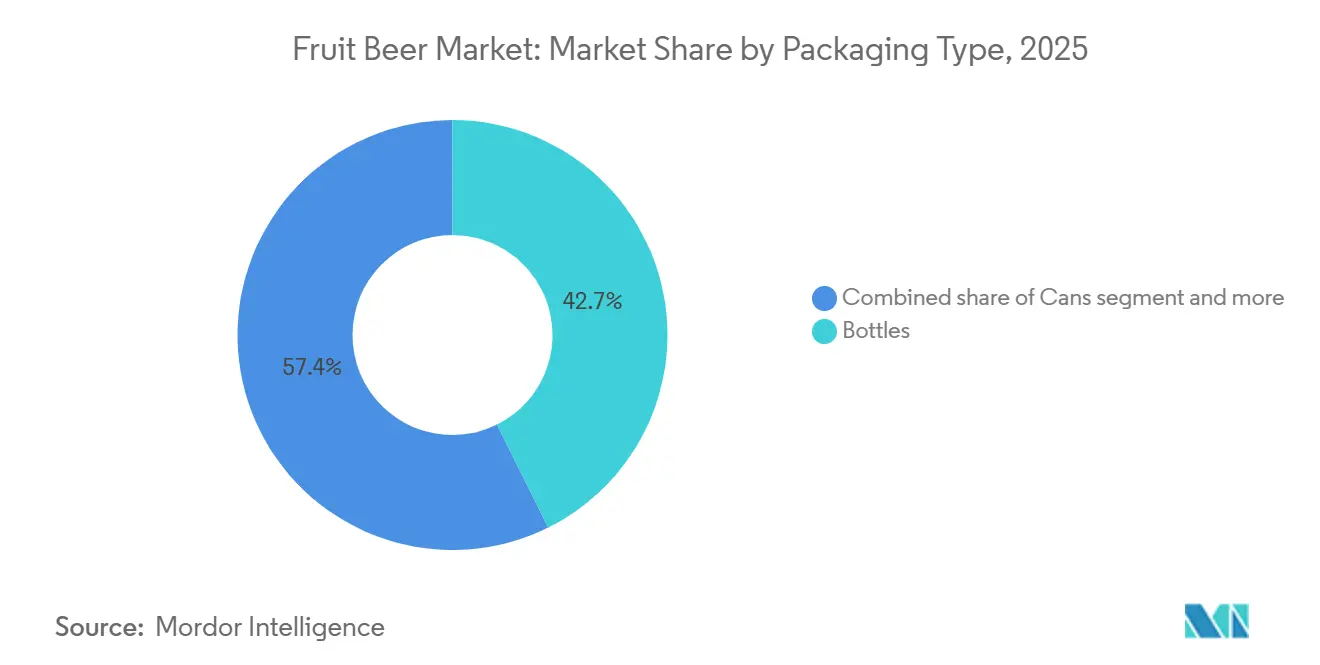

- By packaging type, bottles accounted for 42.65% of revenue in 2025, while cans are advancing at a 6.58% CAGR through 2031.

- By distribution channel, on-trade held 48.91% of revenue in 2025, while off-trade is forecast to expand at a 5.91% CAGR through 2031.

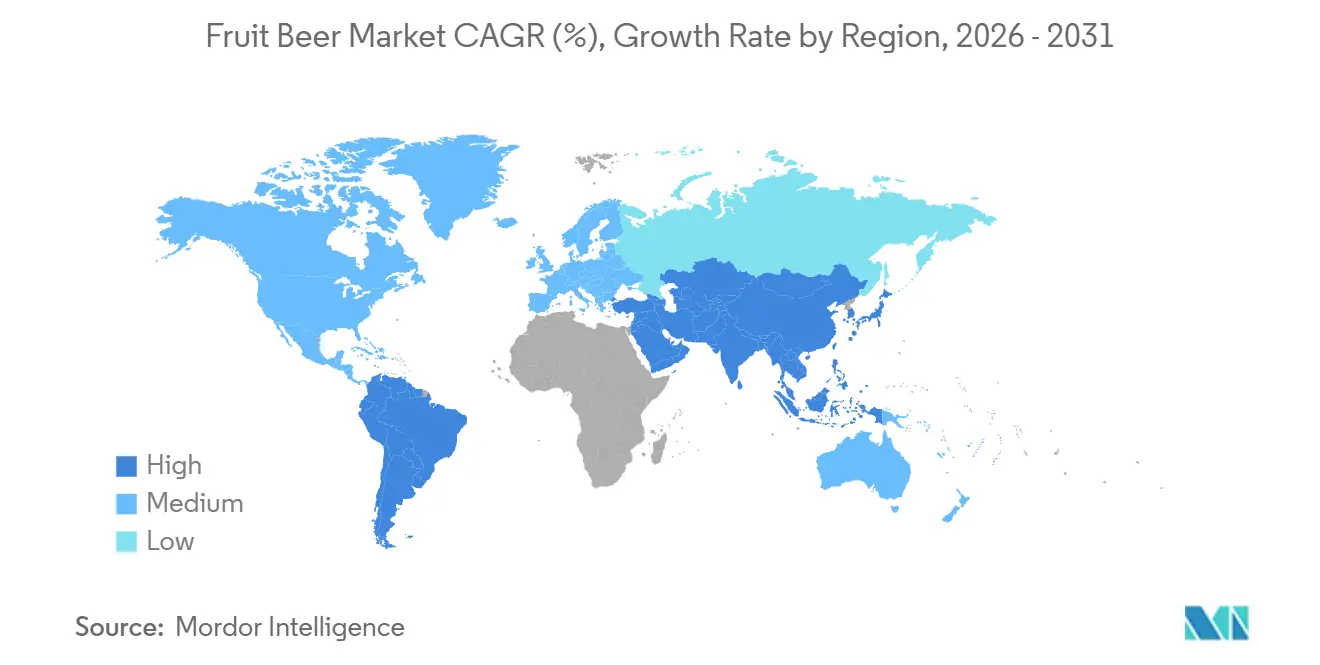

- By geography, Europe held 31.21% revenue share in 2025, while Asia-Pacific is projected to expand at a 6.89 CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fruit Beer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for flavored alcoholic beverages | +1.5% | Global, concentrated in North America, Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expansion of craft beer culture and microbreweries | +1.2% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Premiumization through flavor innovation and limited editions | +0.9% | Europe and North America, with growing uptake in Asia-Pacific premium outlets | Medium term (2-4 years) |

| Shift toward lighter, sessionable, and lower-ABV alcoholic beverages | +0.7% | Global, with strongest impact in United Kingdom, Germany, Australia, and United States | Short term (≤ 2 years) |

| Advancements in brewing and fermentation technologies | +0.3% | Global, with Research and Development concentration in Belgium, Germany, and the United States | Long term (≥ 4 years) |

| Influence of social media and marketing strategies | +0.3% | Global, amplified in Asia-Pacific and North America millennial/Gen Z segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer preference for flavored alcoholic beverages

Consumer preferences for flavored alcoholic beverages are shifting from traditional beer varieties to more refreshing and taste-focused options. Consumers increasingly seek beverages that offer a unique sensory experience, characterized by natural fruit notes, smoother taste profiles, reduced bitterness, and appealing aromas. This trend has made fruit beers appealing to both regular beer drinkers and those exploring alternative alcoholic beverages. Fruit flavors such as berries, tropical fruits, citrus, and mixed blends enhance the drinking experience by balancing sweetness, acidity, and freshness while retaining the core characteristics of beer. The rising demand for premium and craft-inspired beverages has encouraged brewers to experiment with new flavor combinations, seasonal offerings, and unique formulations. Furthermore, younger consumers' preference for variety, personalization, and visually appealing beverages has driven innovation within the fruit beer category.

Expansion of craft beer culture and microbreweries

The growth of craft beer culture and the increasing number of microbreweries are key factors significantly driving the fruit beer market. Craft brewers emphasize creativity, small-batch production, and unique flavor experiences, which differentiate them from traditional beer categories. This approach encourages extensive experimentation with fruit infusions, natural ingredients, seasonal varieties, and innovative flavor combinations, accelerating the development of fruit-based beer products. Consumers are increasingly drawn to craft-style beverages for their distinctive taste profiles, premium positioning, and diverse flavor options beyond conventional beer. For example, according to the Brewers of Europe, in 2024, there were 5,982 microbreweries across Europe. The ongoing expansion of independent brewing operations and their increased capacity for innovation continue to drive growth in the market. [1]Source: Brewers of Europe, "Number of microbreweries in Europe ", brewersofeurope.eu.

Premiumization through flavor innovation and limited editions

The fruit beer market is being driven by the increasing trend of premiumization through flavor innovation and limited-edition launches, as consumers seek unique, high-quality, and experience-oriented beverages beyond traditional beer options. Breweries are focusing on seasonal releases, exclusive fruit blends, innovative formulations, and craft-inspired products to differentiate their offerings and enhance consumer engagement. Limited-edition fruit beers encourage consumers to explore new taste experiences, while premium positioning through distinctive ingredients, creative flavor combinations, and advanced brewing techniques elevates perceptions of quality and exclusivity. For example, in June 2026, BERO, a premium non-alcoholic beer brand by Tom Holland, introduced a limited-edition seasonal release inspired by the British shandy tradition. This product was reimagined using BERO’s flavor-focused approach to beer craftsmanship and was crafted with 30% BERO Kingston Golden Pils and 70% lemonade, offering a refreshing, citrus-driven beer experience.

Shift toward lighter, sessionable, and lower-ABV alcoholic beverages

The growing preference for lighter, sessionable, and lower-ABV alcoholic beverages is driving the expansion of the fruit beer market. Consumers are increasingly seeking drinks that offer a balanced experience with reduced alcohol intensity. There is a noticeable shift away from stronger alcoholic beverages toward options that provide refreshment, flavor variety, and suitability for extended consumption occasions without high alcohol content. Fruit beers cater to this demand by offering moderate alcohol levels, appealing fruit flavors, smoother taste profiles, and lower bitterness compared to traditional beers. The demand for sessionable beverages has prompted brewers to create products that retain beer characteristics while enhancing drinkability through fruit infusions, controlled fermentation processes, and improved flavor balance. Furthermore, the growing emphasis on mindful consumption and moderation has heightened interest in beverages that support social drinking experiences while aligning with evolving lifestyle preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal fruit supply volatility affecting consistent input costs | -0.3% | Global; most acute in Europe (soft fruits) and Asia-Pacific (tropical fruit) | Short term (≤ 2 years) |

| Competition from alternative flavored alcoholic beverages | -0.3% | North America, Europe, Australia | Short term (≤ 2 years) |

| Short shelf life and quality drift in natural flavor formulations | -0.2% | Global, particularly affecting off-trade expansion in emerging markets | Medium term (2-4 years) |

| Advertising and alcohol tax constraints limiting mass-market scaling | -0.2% | South Asia, Middle East and North Africa, select Southeast Asian markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seasonal fruit supply volatility affecting consistent input costs

The seasonal volatility of fruit supply poses a significant challenge for the fruit beer market, as manufacturers depend on the steady availability and quality of fruits to uphold flavor, aroma, and product standards. Fruits commonly used in fruit beer production, such as berries, stone fruits, and tropical fruits, are subject to seasonal harvesting cycles, weather variations, crop yield fluctuations, and supply chain disruptions. These factors contribute to uncertainty in raw material availability. Changes in fruit supply often result in inconsistent pricing for fruit concentrates, purees, juices, and extracts, creating additional production challenges for breweries. Furthermore, maintaining a consistent taste profile throughout the year becomes difficult due to variations in the sweetness, acidity, and overall quality of natural fruit ingredients between harvest seasons. Such fluctuations affect formulation consistency, production planning, and inventory management, particularly for breweries specializing in natural and premium fruit-based products.

Competition from alternative flavored alcoholic beverages

The increasing competition from alternative flavored alcoholic beverages poses a significant challenge for the market, as consumers now have access to a variety of innovative drink options that provide similar refreshing and fruit-based experiences. Categories such as flavored ciders, ready-to-drink (RTD) cocktails, flavored spirits, and canned mixed beverages are gaining consumer attention due to their diverse flavors, convenient packaging, and contemporary brand positioning. These alternatives often compete directly with fruit beer by offering lighter taste profiles, lower-calorie options, and a broad range of fruit-inspired flavors, appealing to consumers who value experimentation and novelty. Furthermore, the rapid pace of product innovation in these competing categories makes it difficult for fruit beer manufacturers to sustain differentiation and retain consumer loyalty. Strong marketing strategies, premium packaging designs, and the growing retail presence of alternative flavored alcoholic beverages further intensify the competition for shelf space and consumer engagement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Raspberry Leads, while Peach Signals Emergent Premiumization

The raspberry flavor segment accounted for 25.22% of the fruit beer market share in 2025, driven by strong consumer acceptance, a distinctive sensory profile, and alignment with evolving taste preferences. Raspberry's balanced sweet-tart taste, refreshing aroma, natural fruit appeal, and compatibility with various beer styles make it a preferred choice for consumers seeking alternatives to traditional beer profiles. The growing preference for berry-based flavors has further solidified raspberry's position, supported by increased availability and consumption of raspberry ingredients. For example, UN Comtrade data indicates that Germany's raspberry imports rose significantly from approximately 10,197 metric tons in 2023 to around 41,780 metric tons in 2024, reflecting heightened demand and supply availability [2]Source: UN Comtrade, "Volume of raspberries imported into Germany", comtradeplus.un.org.

The peach flavor segment is projected to be the fastest-growing in the fruit beer market, with a CAGR of 5.45% during 2026–2031. This growth is attributed to increasing consumer preference for smooth, refreshing, and naturally sweet flavor experiences. Peach has gained traction due to its mild sweetness, juicy aroma, and balanced fruity profile, which effectively blends with beer while reducing the bitterness often associated with traditional variants. The flavor appeals to consumers seeking lighter, easy-to-drink beverages with a softer taste profile, driving its adoption across fruit beer varieties. Additionally, rising demand for unique and premium flavor profiles has spurred interest in peach-based formulations, as consumers continue to explore alternatives to conventional beer offerings.

By Alcohol Content: Non-Alcoholic Segment Drives Both Share and Growth

The non-alcoholic fruit beer segment accounted for 34.04% of the market in 2025 and is projected to grow at a CAGR of 6.13% during 2026–2031. This growth is driven by increasing consumer preference for mindful drinking, alcohol moderation, and flavorful alternatives to traditional alcoholic beverages. The segment is gaining traction as consumers seek options that provide the refreshing taste, aroma, and social experience of beer while minimizing alcohol consumption. Fruit-based variants further boost acceptance by offering natural sweetness, refreshing fruit flavors, and reduced bitterness, making non-alcoholic beer appealing to a broader audience. Additionally, advancements in brewing and alcohol-removal technologies support this growth by preserving authentic beer characteristics and improving taste quality.

The low-alcohol fruit beer segment is also experiencing significant growth within the fruit beer market. This trend is fueled by rising consumer demand for balanced alcohol consumption, lighter beverage options, and refreshing flavor profiles. Consumers are increasingly opting for beverages that allow extended consumption occasions while mitigating the effects of higher alcohol levels, positioning low-alcohol fruit beer as an attractive alternative to traditional beer. The combination of reduced alcohol content and fruit-based flavors enhances drinkability by delivering a smoother taste, lower bitterness, fruity aroma, and a refreshing sensory experience, appealing to both regular beer drinkers and new consumers.

By Packaging Type: Bottles Dominant as Cans Structurally Shift Occasion Access

The bottles segment accounted for 42.65% of revenue in the fruit beer market in 2025, driven by strong consumer preference for premium packaging, product quality preservation, and traditional beer consumption experiences. Bottles remain dominant as they effectively protect against external factors, preserving the flavor, carbonation, aroma, and freshness of fruit beer products. Glass bottles, in particular, are widely favored for their ability to enhance product appeal through premium presentation and support the visual attractiveness of fruit-based beers with vibrant colors and unique formulations. This segment also benefits from the consumer perception that bottled beverages offer higher quality and authenticity compared to other packaging formats. Additionally, bottles provide flexibility in packaging sizes, branding opportunities, and shelf differentiation, enabling fruit beer producers to emphasize flavor varieties and premium characteristics.

The cans segment is the fastest-growing packaging format in the market, registering a CAGR of 6.58% during 2026–2031, driven by increasing consumer preference for convenient, lightweight, portable, and sustainable packaging solutions. This format is particularly suitable for modern consumption patterns due to its ease of carrying, faster chilling capability, and suitability for outdoor and casual drinking occasions. The shift toward cans is further supported by breweries seeking packaging formats that improve logistics efficiency, reduce transportation weight, and align with recyclability goals. According to the Brewers Association, aluminum cans represented around 78% of packaged craft beer volume in 2025, underscoring the growing preference for canned formats across innovative beer categories [3]Source: Brewers Association, "Value Quest: 2025 Packaging Trends", brewersassociation.org.

By Distribution Channel: On-Trade Concentration Masks Structural Off-Trade Gains

On-trade channels accounted for the largest distribution revenue share at 48.91% in the market in 2025. This dominance is attributed to the growing consumer preference for experiential drinking environments, social consumption, and the discovery of premium beverages. Establishments such as bars, pubs, restaurants, and hospitality venues play a significant role in promoting fruit beer adoption by offering opportunities to explore various flavors, styles, and freshly served options. The segment benefits from the increasing demand for unique drinking experiences, where consumers are more inclined to experiment with innovative fruit-infused beer varieties compared to traditional retail purchases. Additionally, on-trade channels support premiumization, as professionally served beverages are often associated with superior taste, presentation, and overall experience.

The off-trade segment is the fastest-growing distribution channel in the fruit beer market, with a projected CAGR of 5.91% during 2026–2031. This growth is driven by rising consumer preference for convenient purchasing, at-home consumption, and access to a wider variety of beverage options. Supermarkets, hypermarkets, specialty liquor stores, convenience stores, and online retail platforms are contributing to the segment's momentum by offering a broader selection of fruit beer flavors, packaging formats, and premium varieties. Changing purchasing habits, such as a shift toward planned consumption and the increasing popularity of home-based social occasions, are further boosting demand through retail channels. Additionally, the expansion of digital alcohol retail, enhanced delivery services, promotional activities, and improved shelf visibility are strengthening consumer engagement in this segment.

Geography Analysis

Europe accounted for a 31.21% share of the fruit beer market in 2025, driven by the region's strong brewing heritage, established consumer preference for specialty beers, and extensive expertise in fruit-based beer production. The region benefits from a long-standing culture of experimenting with various brewing styles, fermentation methods, and fruit-infused formulations, which has fostered widespread consumer acceptance of fruit beer. The increasing preference for premium, craft-style, and flavorful beer experiences continues to strengthen demand, as consumers seek alternatives beyond conventional beer varieties. The growing popularity of low-alcohol and naturally flavored beverages, combined with continuous innovation in fruit combinations and brewing techniques, supports Europe’s leading position in the global fruit beer market.

Asia-Pacific is expected to be the fastest-growing region, registering a CAGR of 6.89% during 2026–2031. This growth is driven by changing consumer taste preferences, increasing acceptance of flavored alcoholic beverages, and growing interest in innovative beer formats. Consumers across the region are increasingly shifting toward lighter, refreshing, and less bitter beverages, supporting the adoption of fruit-infused beer varieties. Rising experimentation with tropical and exotic flavors, expanding craft brewing activities, and increasing demand for premium drinking experiences are accelerating market growth. Additionally, the growing preference for low-alcohol and approachable beer alternatives is expected to position Asia-Pacific as a key growth engine in the global fruit beer market.

North America holds a significant share of the fruit beer market, supported by its well-developed craft brewing ecosystem and growing moderation-driven consumer trends. Demand in the region is driven by strong consumer interest in innovative flavors, seasonal beer varieties, and premium fruit-based formulation. South America and the Middle East & Africa markets are at earlier stages of development but exhibit increasing growth potential. In South America, gradual adoption is being driven by growing exposure to craft and flavored alcoholic beverages. Meanwhile, the Middle East and Africa is experiencing growth through the expanding availability of non-alcoholic and low-alcohol fruit beer options. Product innovation, changing taste preferences, and increasing demand for differentiated beverage experiences are expected to support future growth across these emerging regions.

Competitive Landscape

The fruit beer market is fragmented, with global brewing companies, regional breweries, and craft beer producers competing through flavor innovation, product differentiation, and premium positioning. Key players in the market include Anheuser-Busch InBev SA/NV, Heineken N.V., Carlsberg Group, Molson Coors Beverage Company, and Boston Beer Company, Inc. These companies are enhancing their market presence by expanding fruit-flavored beer portfolios, introducing seasonal varieties, and catering to consumer preferences for refreshing, low-bitterness, and unique taste profiles. The growing competition has driven breweries to explore diverse fruit profiles, including berries, citrus, tropical fruits, and mixed fruit blends, to meet evolving consumer demands.

Technology and brewing innovation have become critical competitive factors, with manufacturers investing in advanced fermentation techniques, flavor stabilization processes, improved filtration, and alcohol-reduction technologies to enhance product quality. Companies are prioritizing authentic fruit taste, aroma retention, longer shelf stability, and consistent sensory characteristics while developing both alcoholic and non-alcoholic fruit beer options. Advancements in brewing processes are enabling producers to create fruit beers with enhanced freshness, natural flavor integration, and premium-quality profiles, helping brands differentiate themselves in a competitive market.

Product innovation remains a key strategy for fruit beer manufacturers, with companies regularly launching new flavors, limited-edition variants, and fruit-based blends to attract experimental consumers. The increasing preference for craft-inspired beverages has encouraged both large breweries and smaller players to develop unique formulations that combine traditional beer styles with modern fruit flavors. Additionally, companies are focusing on sustainable packaging, digital consumer engagement, and premium branding strategies to build customer loyalty and expand their market reach. As consumer demand shifts toward flavorful, convenient, and moderation-focused beverages, continuous innovation is expected to remain central to competition in the global fruit beer market.

Fruit Beer Industry Leaders

-

Anheuser-Busch InBev SA/NV

-

Heineken N.V.

-

Carlsberg Group

-

Molson Coors Beverage Company

-

Boston Beer Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: AB InBev introduced fruit-infused beers to the United Kingdom market, including Stella Artois Strawberries & Cream and Bud Light Lemon Squeeze. These products are designed to appeal to new demographic groups, particularly during the summer season.

- April 2025: Molson Coors Beverage Company introduced Madrí Excepcional Limón, a fruit beer available in 4x440ml can multipacks with an alcohol by volume (ABV) of 3.4%. This premium lager features a fresh, zesty lemon aroma and a flavor profile combining lemon and other naturally sweet and balanced citrus fruits.

- February 2025: Lindemans Brewery launched 8% ABV fruit beers, including Lindemans d'Or and Lindemans Noir. These high-quality brews maintain natural flavors and balanced sweetness without added sugars or coloring.

Global Fruit Beer Market Report Scope

Fruit beer is beer made with fruit added as an adjunct or flavouring. The fruit beer market is segmented by flavor, alcohol content, packaging type, distribution channel, and geography. Based on flavor, the market is segmented into raspberry, cherry, peach, apple, strawberry, blueberry, mango, mixed fruit blends, and other fruit flavors. Based on alcohol content, the market is segmented into non-alcoholic fruit beer, low-alcohol fruit beer, and high-alcohol fruit beer. Based on packaging type, the market is segmented into bottles, cans, and others. Based on distribution channel, the market is segmented into on-trade and off-trade channels. The off-trade segment is further categorized into supermarkets and hypermarkets, convenience stores, online retail stores, specialty/liquor stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market forecasts are provided in both value (USD) and volume (liters) for all the mentioned segments.

| Raspberry |

| Cherry |

| Peach |

| Apple |

| Strawberry |

| Blueberry |

| Mango |

| Mixed Fruit Blends |

| Other Fruit Flavors |

| Non-Alcoholic Fruit Beer |

| Low-Alcohol Fruit Beer |

| High-Alcohol Fruit Beer |

| Bottles |

| Cans |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Specialty/Liquor Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Flavor | Raspberry | |

| Cherry | ||

| Peach | ||

| Apple | ||

| Strawberry | ||

| Blueberry | ||

| Mango | ||

| Mixed Fruit Blends | ||

| Other Fruit Flavors | ||

| By Alcohol Content | Non-Alcoholic Fruit Beer | |

| Low-Alcohol Fruit Beer | ||

| High-Alcohol Fruit Beer | ||

| By Packaging Type | Bottles | |

| Cans | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Specialty/Liquor Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the fruit beer business?

The fruit beer market was valued at USD 366.01 million in 2025, stands at USD 380.42 million in 2026, and is forecast to reach USD 481.4 million by 2031 at a 4.8% CAGR.

Which region leads revenue and which region is growing the fastest?

Europe led with 31.21% of revenue in 2025, while Asia-Pacific is projected to post the fastest growth at a 6.89% CAGR through 2031.

Which product area is shaping future demand most clearly?

Non-alcoholic fruit beer is the clearest growth engine because it held 34.04% share in 2025 and is also forecast to expand at the fastest 6.13% CAGR through 2031.

What packaging trend matters most for suppliers and retailers?

Bottles still lead current revenue with 42.65% share, but cans are growing faster at 6.58% CAGR, helped by convenience, portability, and wider off-trade use.

Page last updated on: