Fortified Wine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.25 Billion |

| Market Size (2031) | USD 18.01 Billion |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fortified Wine Market Analysis by Mordor Intelligence

The fortified wine market size is expected to grow from USD 14.75 billion in 2025 to USD 15.25 billion in 2026 and is forecast to reach USD 18.01 billion by 2031 at 3.37% CAGR over 2026-2031. The growing demand for premium fortified wines is driving up average prices, even as traditional drinking habits change. This trend helps producers manage slower sales volumes in older, more established markets. Europe remains the largest market for fortified wines, owing to its strong cultural ties and the familiarity of consumers with these products. Meanwhile, the Asia-Pacific region is experiencing rapid growth due to urbanization, rising incomes, and the increasing influence of Western lifestyles. Innovations such as creative cocktail recipes, environmentally friendly wine production, and digital marketing are helping to create new opportunities for consumption and making brands more appealing to consumers. The market is fragmented, meaning there is significant potential for companies to merge or acquire others. Leading producers from countries like Portugal, Spain, and Italy are using their long-standing traditions, ownership of vineyards, and extensive global distribution networks to maintain their competitive edge and grow their presence in the market.

Key Report Takeaways

- By product type, port commanded 38.72% of the fortified wine market share in 2025; Vermouth is projected to advance at a 4.21% CAGR through 2031.

- By category, the mass segment held 58.01% of revenue in 2025, whereas the premium tier is on track for a 4.39% CAGR to 2031.

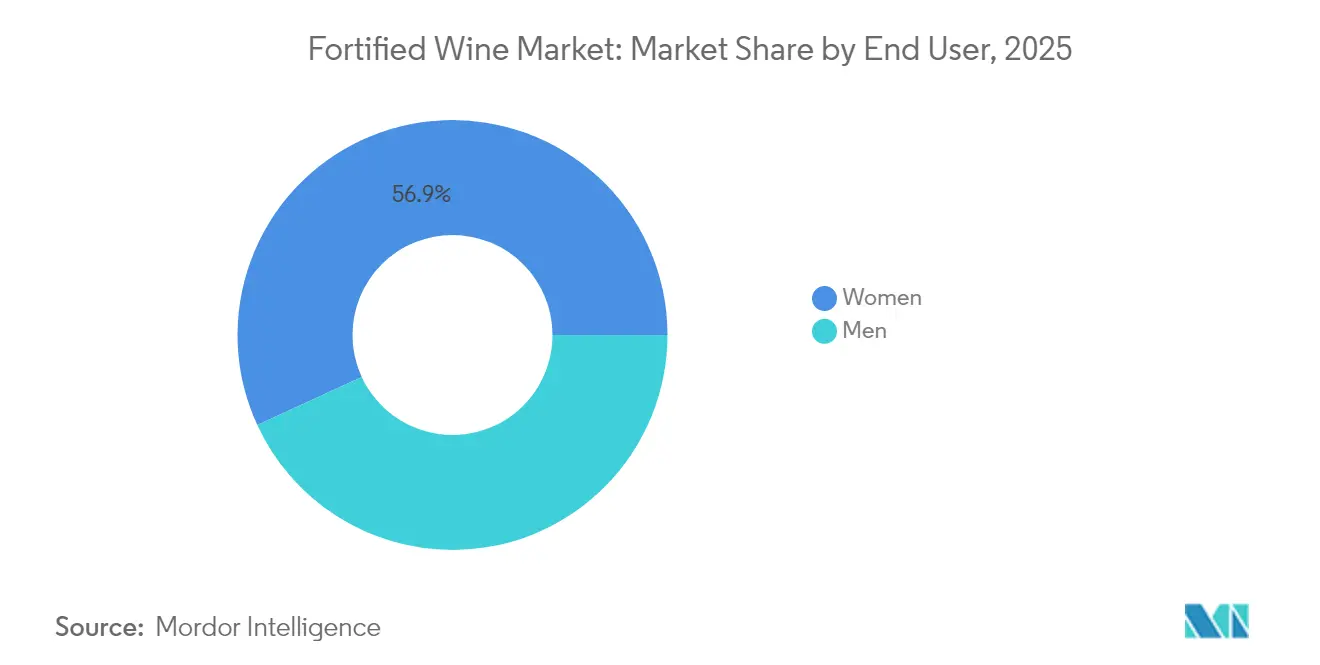

- By end user, women accounted for 56.88% of 2025 consumption, while the male segment is the fastest-growing at 4.72% CAGR to 2031.

- By distribution channel, off-trade captured 55.74% of sales in 2025; on-trade is recovering fastest at a 3.73% CAGR between 2026 and 2031.

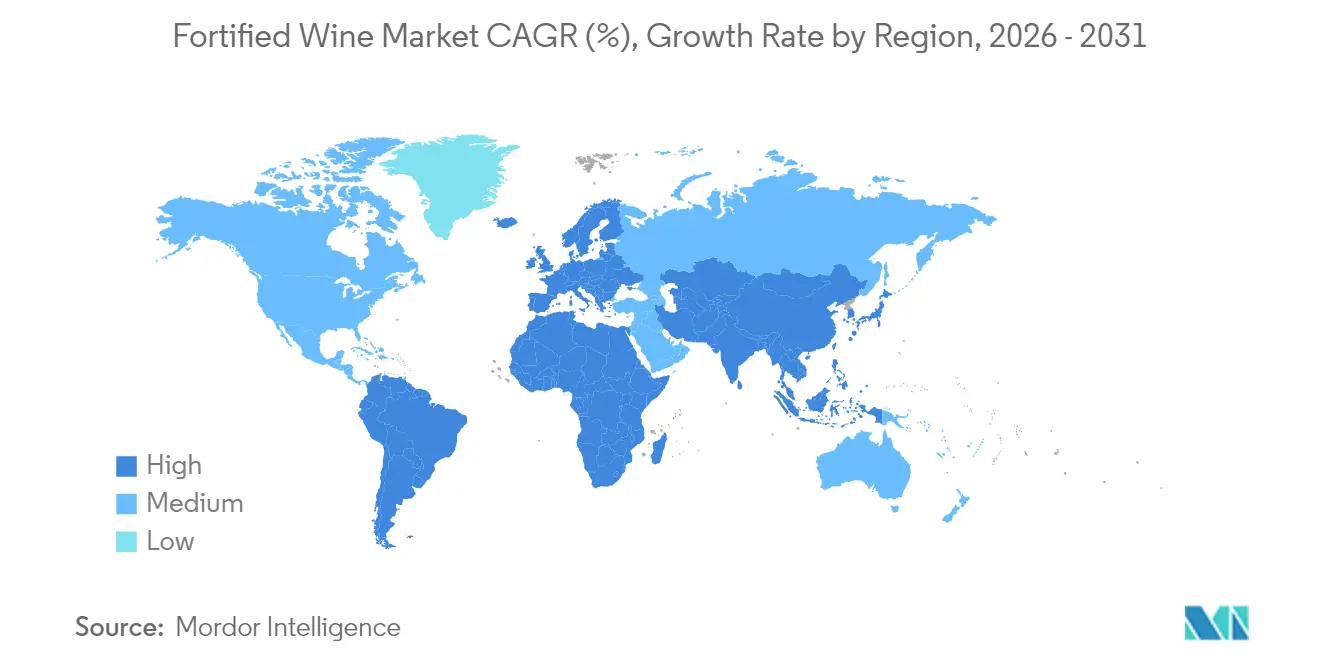

- By geography, Europe retained 57.02% regional share in 2025; Asia-Pacific is the fastest-growing region at a 5.05% CAGR for the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fortified Wine Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Technological advancement in terms of production | +0.8% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Surge in demand for premium wine | +1.2% | Europe, North America, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Product differentiation in terms of raw material | +0.6% | Europe, South America wine regions | Medium term (2-4 years) |

| Strong demand during festive seasons and social gatherings | +0.7% | Global, with peak impact in Europe and North America | Short term (≤ 2 years) |

| Growing use in mixology and cocktails | +0.9% | North America, Europe, Asia-Pacific urban markets | Medium term (2-4 years) |

| Growing interest in low-alcohol and digestif drinks | +0.5% | Europe, North America health-conscious segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for premium wine

The global fortified wine market is experiencing significant growth, driven by the increasing demand for premium products. Consumers, especially younger generations, are showing a preference for wines that emphasize quality, origin transparency, and sustainable practices. For example, Constellation Brands has shifted its focus to premium wines priced between USD 30–80 by selling off its mass-market labels. New EU regulations, as of 2024, requiring QR code-based ingredient and nutrition disclosures are helping to build trust and enhance product traceability [1]Source: European Union, "Food labelling in the EU – Consumers can get lost in the maze of labels," eca.europa.eu. Recent innovations in the market highlight this trend, such as Taylor’s limited-edition Historical Collection Reserve Tawny, launched in 2024, and Sandeman’s organic-certified Apitiv White Port. These products reflect a growing interest in heritage-rich and eco-friendly fortified wines. According to the International Organisation of Vine and Wine (OIV), the global wine export value in 2024 is estimated at EUR 35.9 billion, largely driven by the demand for premium wines in regions like Europe and North America [2]Source: Organisation of Vine and Wine, "State of the World Vine and Wine Sector in 2024," oiv.int.

Strong demand during festive seasons and social gatherings

Fortified wine sales see a significant rise during festive seasons and social gatherings, as these occasions encourage higher consumption in key markets. In Europe and North America, holidays like Christmas and New Year's consistently drive demand, while in China, the Lunar New Year celebrations lead to a noticeable increase in purchases. Similarly, weddings and other celebrations in South Asia contribute to seasonal spikes in demand. The hospitality sector's recovery after the pandemic has further fueled this trend, with consumers increasingly seeking premium and unique dining experiences. To meet this growing interest, many brands have introduced special promotions and limited-edition products. For instance, in December 2024, González Byass launched a holiday gift set featuring its Nectar Pedro Ximénez and Alfonso Oloroso sherries, catering to festive buyers. Symington Family Estates released a zodiac-themed collector’s edition of Graham’s Six Grapes Reserve Port for Lunar New Year 2025, appealing to tradition and cultural significance.

Growing use in mixology and cocktails

The use of fortified wines in cocktails and mixology is growing rapidly, especially among younger, city-dwelling consumers who are eager to explore new and creative drinking options. Classic cocktails like the Sherry Cobbler are making a strong comeback, while innovative drinks such as Port Highballs are becoming favorites in both upscale bars and casual lounges. Vermouth, in particular, has become a standout ingredient due to its complex botanical flavors and versatility, making it a popular choice for crafting unique cocktails across the globe. A 2024 survey by Drinks International found that nearly all (99%) of the bars surveyed included at least one Vermouth brand in their cocktail offerings [3]Source: Drinks International, "Brands Report 2024: Vermouth," drinksint.com. Bartenders are increasingly using fortified wines to create low-alcohol, flavorful drinks that cater to the evolving tastes of modern consumers. To support this trend, industry organizations and trade groups have stepped up by offering workshops and certification programs.

Growing interest in low-alcohol and digestif drinks

Fortified wines are becoming increasingly popular among health-conscious consumers and those seeking moderation in their drinking habits. These wines, such as dry sherries, semi-sweet ports, and vermouth-based aperitifs, are appealing due to their lower alcohol content and suitability for mindful consumption. Producers are innovating by using advanced winemaking techniques, like specialized yeast strains, to create reduced-alcohol fortified wines without sacrificing flavor or aroma. Additionally, regulatory changes are supporting this trend. In the United States, the proposed “Alcohol Facts” labeling rule by the FDA and TTB aims to provide clear nutritional information on packaging, helping consumers make informed decisions, as per the Federal Register[4]Source: Federal Register, "Alcohol Facts Statements in the Labeling of Wines, Distilled Spirits, and Malt Beverages," federalregister.gov. These developments are not only attracting new audiences but also redefining the role of fortified wines, making them a versatile choice for both pre-meal aperitifs and post-meal digestifs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent government regulations | -0.4% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Rising consumer inclination towards other alcoholic beverages | -0.6% | North America, Europe, Australia | Medium term (2-4 years) |

| Short shelf life after opening | -0.3% | Global, particularly affecting off-trade channels | Short term (≤ 2 years) |

| Limited consumer awareness and education | -0.5% | Asia-Pacific, emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations

Strict government regulations are creating significant hurdles for the fortified wine market, particularly for smaller and mid-sized producers. Regulatory authorities in major markets are enforcing tighter compliance measures, such as container size restrictions and new allergen disclosure requirements, as outlined by the Alcohol and Tobacco Tax and Trade Bureau. In the United States, California’s updated Bottle Bill has added further challenges by introducing Container Recycling Value (CRV) fees and specific labeling requirements. These changes are hitting boutique wineries and artisanal fortified wine producers the hardest. The increasing compliance demands are driving up production and packaging costs while complicating distribution processes. This could limit market access and reduce product variety, especially for niche producers focused on exports, making it harder for them to compete in an already challenging market environment.

Rising consumer inclination towards other alcoholic beverages

As consumer preferences increasingly lean towards alternative beverages, the fortified wine market faces mounting challenges, particularly with younger legal-age drinkers. Many younger consumers view fortified wines as antiquated or reserved for formal events, curtailing their everyday appeal. In response, producers are actively modernizing their offerings. They're rebranding, adopting sleek and modern packaging, and introducing convenient formats such as single-serve bottles and canned aperitifs. For example, certain brands are using bold designs and compact packaging to draw in urban millennials, while others are crafting ready-to-drink fortified wine cocktails tailored for casual social settings. These efforts aim to reposition fortified wines as versatile and appealing options for a broader range of occasions, bridging the gap between tradition and contemporary consumer demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Port Leads Heritage Appeal

Port remains the leading product type in 2025, which accounts for 38.72% of the market's total value. This dominance is largely attributed to Portugal’s protected designation of origin system, which ensures consistent quality and fosters consumer trust. Strong trade ties with the United Kingdom have historically supported steady demand. Port is widely available in both retail (off-trade) and hospitality (on-trade) channels, making it accessible to a broad audience. To appeal to premium consumers, producers are focusing on offerings like single-quinta bottlings and age-stated expressions, which emphasize the heritage and craftsmanship of their products.

Meanwhile, Vermouth is emerging as the fastest-growing segment, with a projected CAGR of 4.21% through 2031. This growth is fueled by Vermouth’s integral role in modern cocktail culture, particularly in major cities like Tokyo, New York, and London, where it has become a key ingredient in high-end bars. Producers are innovating by incorporating local botanicals to create terroir-driven products, which are gaining popularity in premium on-trade venues. The fortified wine industry is experimenting with hybrid styles that combine elements of aperitifs, digestifs, and cocktail ingredients, further expanding its appeal.

By Category: Premium Segment Drives Value Growth

In 2025, the mass segment is becoming the leading category in the fortified wine market, with a growth rate of 58.01%. This growth is mainly driven by the increasing demand from cost-conscious consumers who are looking for affordable wine options, especially in developing countries. Companies in the mass-market segment are taking advantage of this trend by offering attractive deals like multipacks, in-store discounts, and ensuring their products are widely available in supermarkets. Although these wines may not have the same level of craftsmanship or storytelling as premium wines, they are crucial for expanding the market and introducing new consumers to fortified wines.

On the other hand, premium wines are expected to grow at a steady CAGR of 4.39% through 2031. This growth reflects the strong demand for high-quality wines in wealthy urban areas across Asia and North America. Consumers in this segment are increasingly focusing on factors like quality, origin, and sustainability. They prefer wines that are vintage-dated, cask-finished, or have unique characteristics. To meet these preferences, producers are emphasizing features such as organic certifications, vineyard-specific labels, and eco-friendly packaging. Digital tools like virtual wine tastings and QR codes for product traceability are helping brands build trust and loyalty among consumers.

By End User: Women Lead Current Consumption

In 2025, female consumers made up 56.88% of fortified wine consumption, primarily due to the popularity of sweeter options like Port and Sherry during social events and as dessert pairings. To cater to this preference, brands have introduced smaller bottle sizes and highlighted approachable flavor profiles that pair well with various foods. On the other hand, male consumption is growing at a faster rate, fueled by an increasing interest in mixology and premium cask-strength variants. Educational campaigns aimed at simplifying the category and making it more appealing have further supported this growth, with the male consumer market projected to expand at a 4.72% CAGR through 2031.

Generational trends reveal that younger men are discovering fortified wines through their integration into cocktail culture, while women aged 30-50 are gravitating toward options that emphasize provenance and reduced sugar content. Marketing strategies have evolved to focus on inclusivity, moving away from outdated gender stereotypes. Instead, brands are now highlighting the heritage, versatility, and sustainability of their products.

By Distribution Channel: Off-Trade Dominance with On-Trade Recovery

In 2025, off-trade channels led fortified wine sales, contributing 55.74% of the total market share. This dominance is largely due to the continuation of home consumption habits established during lockdowns. Retailers, including specialty wine merchants and national chains, have increased their focus on fortified wine products by dedicating more shelf space and providing educational materials to help consumers make informed choices. E-commerce has also played a significant role in this growth, offering convenience and a broader selection of products. This has allowed smaller producers to reach niche audiences directly, further diversifying the market.

On-trade channels, such as bars and restaurants, are experiencing a steady recovery, with a projected growth rate of 3.73% CAGR. The revival of experiential dining and the return of tourism are key drivers of this growth. Sommeliers are introducing curated tasting experiences, such as flights featuring aged Tawny Port, Amontillado, and artisanal Vermouth, which encourage consumers to explore the category. Additionally, cocktail-focused bars are incorporating fortified wines into low-alcohol-by-volume (ABV) drinks, catering to the growing trend of mindful drinking. Producers are actively collaborating with mixology academies to provide training and resources, ensuring fortified wines gain prominence on menus and are effectively promoted by knowledgeable staff.

Geography Analysis

Europe accounted for 57.02% of the fortified wine market value in 2025, driven by the strong presence of PDO (Protected Designation of Origin) systems in countries like Portugal, Spain, and Italy. These systems ensure product authenticity and help maintain premium price points. Producers in the region are increasingly focusing on sustainability by converting vineyards to organic practices and adopting energy-efficient technologies in their cellars to comply with stricter EU environmental regulations. While household wine consumption in countries like Germany and France has seen slight declines, the region continues to benefit from high-margin sales through duty-free shops and fine dining establishments, supported by a steady influx of tourists.

The Asia-Pacific region is experiencing the fastest growth in the fortified wine market, with a projected CAGR of 5.05% through 2031. In China, the market shows a dual trend: ultra-premium imports are thriving in tier-one cities, while price sensitivity dominates in volume-driven provinces. Japan’s consumers, known for their appreciation of authenticity and tradition, continue to support steady imports of Sherry and Port. Emerging markets like India, South Korea, and Thailand are witnessing rapid growth, driven by rising disposable incomes and the increasing popularity of Western dining habits.

In North America, the fortified wine market faces challenges with declining volumes but shows resilience in the premium segment. The United States remains a significant market highlighting opportunities for recovery through targeted premium strategies. Recent regulatory changes in Ontario, Canada, allowing wine sales in grocery stores, have expanded retail access and created new opportunities for imported fortified wines. Meanwhile, the growing craft cocktail culture in cities like New York, Chicago, and Los Angeles has increased consumer awareness, with fortified wines like Port and Sherry being featured in innovative cocktails and tasting flights.

Competitive Landscape

The fortified wine market is highly fragmented. Leading producers from Portugal, Spain, and Italy dominate the market by leveraging their rich heritage, extensive estate holdings, and robust global distribution networks. Companies like Symington Family Estates are adopting modern technologies, such as advanced lagar systems, and focusing on organic vineyard conversions to meet the growing demand for sustainable products. Meanwhile, international spirits companies are streamlining their portfolios, with firms like Pernod Ricard and Constellation Brands divesting lower-margin wine products to concentrate on premium offerings.

Innovation is a key driver of competition in the fortified wine market, spanning both product development and production processes. For instance, new technologies like Pulsed Electric Field (PEF) extraction are being used to enhance color and tannin development, reducing production time for ruby-style wines. Smaller producers are differentiating themselves by restoring traditional casks and offering limited-barrel releases, which appeal to collectors and connoisseurs. Direct-to-consumer subscription clubs are gaining traction, providing steady revenue streams and valuable consumer data. Collaborations with mixologists and chefs are also helping brands create unique experiences, making their products stand out in a crowded retail environment.

Mergers and acquisitions are increasingly focused on expanding geographic reach and optimizing distribution channels. Companies are actively seeking established brands with strong Protected Designation of Origin (PDO) credentials and well-established market access in regions like Asia. Partnerships with technology firms are emerging as a new trend, with blockchain traceability and smart packaging being used to enhance authenticity and engage consumers more effectively. These strategies are helping brands build trust and maintain a competitive edge in the evolving market landscape.

Fortified Wine Industry Leaders

-

Symington Family Estates Vinhos S.A.

-

Caffo Group

-

Kopke Group Fine Wines, SA

-

E. & J. Gallo Winery

-

Bacardi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tri-Vin Imports launched the brand XXL, a high-alcohol, fruit-flavored fortified wine inspired by Moscato, positioned to appeal to younger and less traditional wine consumers. Initially produced in Moldova before shifting to California and France due to tariff issues, XXL offered 16–21% ABV and came in five distinct fruit flavors.

- August 2024: Waud Wines, a UK-based company, acquired Handford Wines to strengthen its retail footprint in London and expand its portfolio of fortified wines. This acquisition allows Waud Wines to tap into Handford Wines' established customer base and leverage its reputation in the market.

- February 2024: Sokol Blosser Winery, based in the United States, introduced its first-ever collection of fortified wines. The launch was strategically carried out through online direct-to-consumer channels, allowing the winery to reach its customers directly and offer a unique addition to its product portfolio.

Global Fortified Wine Market Report Scope

Fortified wine is a type of wine that contains distilled spirits and higher alcohol content than regular wine.

The market for fortified wine is segmented based on product type, distribution, and geography. Based on product type, the market is segmented into port wine, vermouth, sherry, and other product types. By distribution channel, the market is segmented into on-trade and off-trade. Off-trade is sug-segmented into supermarkets and hypermarkets, specialty stores, and other channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the report offers market sizes and forecasts in value (USD).

| Port |

| Vermouth |

| Sherry |

| Others |

| Mass |

| Premium |

| Men |

| Women |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Others Off Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Norway | |

| Russia | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Port | |

| Vermouth | ||

| Sherry | ||

| Others | ||

| By Category | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Others Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Norway | ||

| Russia | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the fortified wine market?

The fortified wine market is valued at USD 15.25 billion in 2026 and is projected to reach USD 18.01 billion by 2031.

Which product type holds the largest fortified wine market share?

Port leads with 38.72% share in 2025, underpinned by its protected designation of origin status and strong global recognition.

Why is Asia-Pacific the fastest-growing region?

Urbanization, income growth, and Western lifestyle adoption are propelling a 5.05% CAGR in Asia-Pacific through 2031, especially in China, Japan, India, and South Korea.

How is mixology influencing fortified wine demand?

Cocktail culture is boosting Vermouth and Sherry usage in urban bars, introducing fortified wines to younger consumers and expanding consumption occasions.

Page last updated on: