Market Overview

| Study Period | 2021 - 2031 |

|---|---|

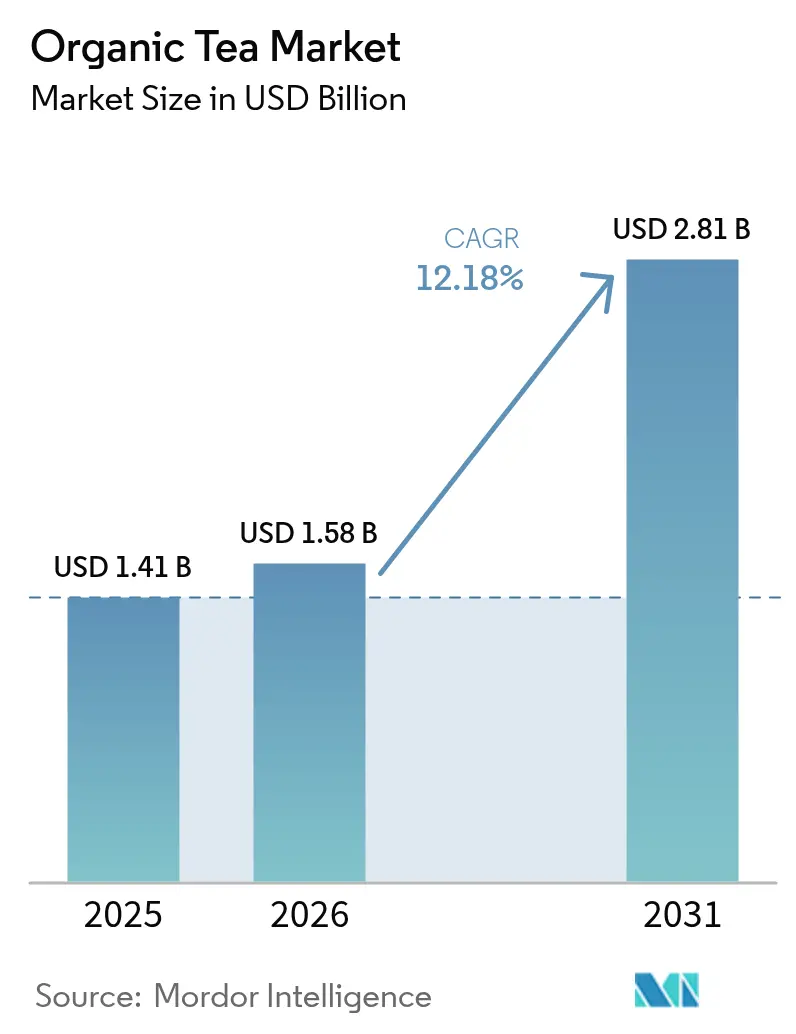

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Tea Market Analysis by Mordor Intelligence

The organic tea market size in 2026 is estimated at USD 1.58 billion, growing from 2025 value of USD 1.41 billion with 2031 projections showing USD 2.81 billion, growing at 12.18% CAGR over 2026-2031. Heightened health awareness, stringent organic-farming regulations, and a premium market positioning have reshaped consumer expectations for clean-label beverages. Supermarkets, cafés, and online platforms are increasingly dedicating shelf space to green, herbal, and functional tea blends. Moreover, sustainability credentials—such as carbon-neutral farms, regenerative practices, and recyclable packaging—have emerged as key differentiators. While Asia-Pacific leads in volume, bolstered by its agricultural expertise and a burgeoning middle class, Europe spearheads value growth, driven by established certification regimes and robust purchasing power. The organic tea market is witnessing a disciplined expansion phase, underscored by vertical integration, stricter enforcement of organic standards, and strategic acquisitions. In this evolving landscape, certified supply, brand authenticity, and an omni-channel presence are paramount.

Key Report Takeaways

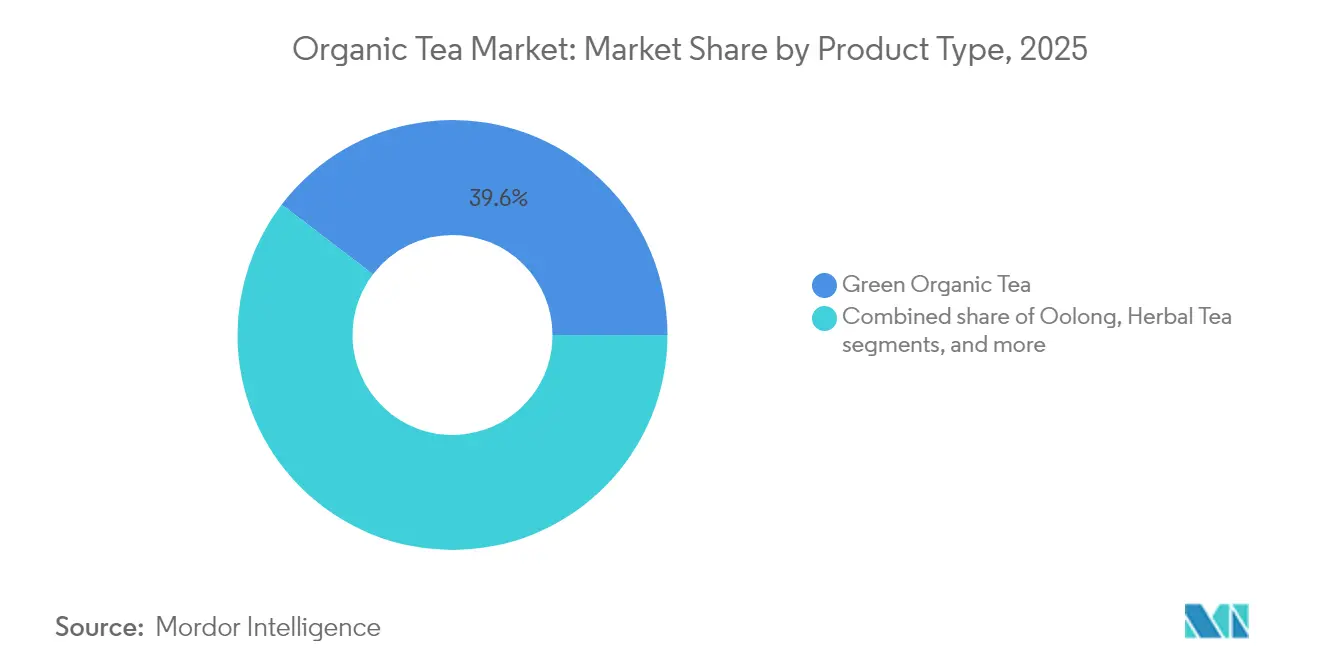

- By type, green tea led with 39.62% organic tea market share in 2025; herbal/fruit infusions are projected to advance at a 13.42% CAGR through 2031.

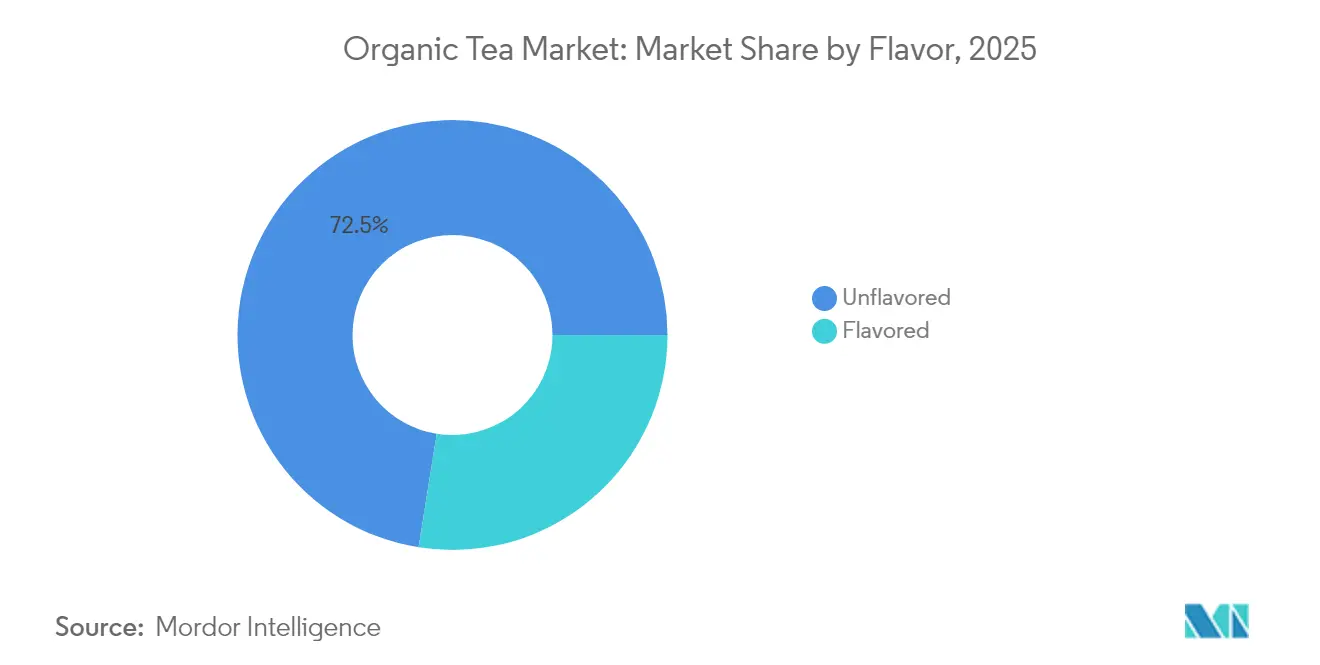

- By flavor, the unflavored segment accounted for 72.48% of the organic tea market size in 2025, while naturally flavored variants are set to expand at 12.76% CAGR between 2026-2031.

- By packaging, cartons held 34.62% revenue share in 2025; tins/cans are the fastest-growing format at 8.21% CAGR to 2031.

- By distribution channel, off-trade outlets controlled 51.74% of 2025 sales, but on-trade venues are expected to grow at 15.92% CAGR, reflecting strong café and restaurant demand.

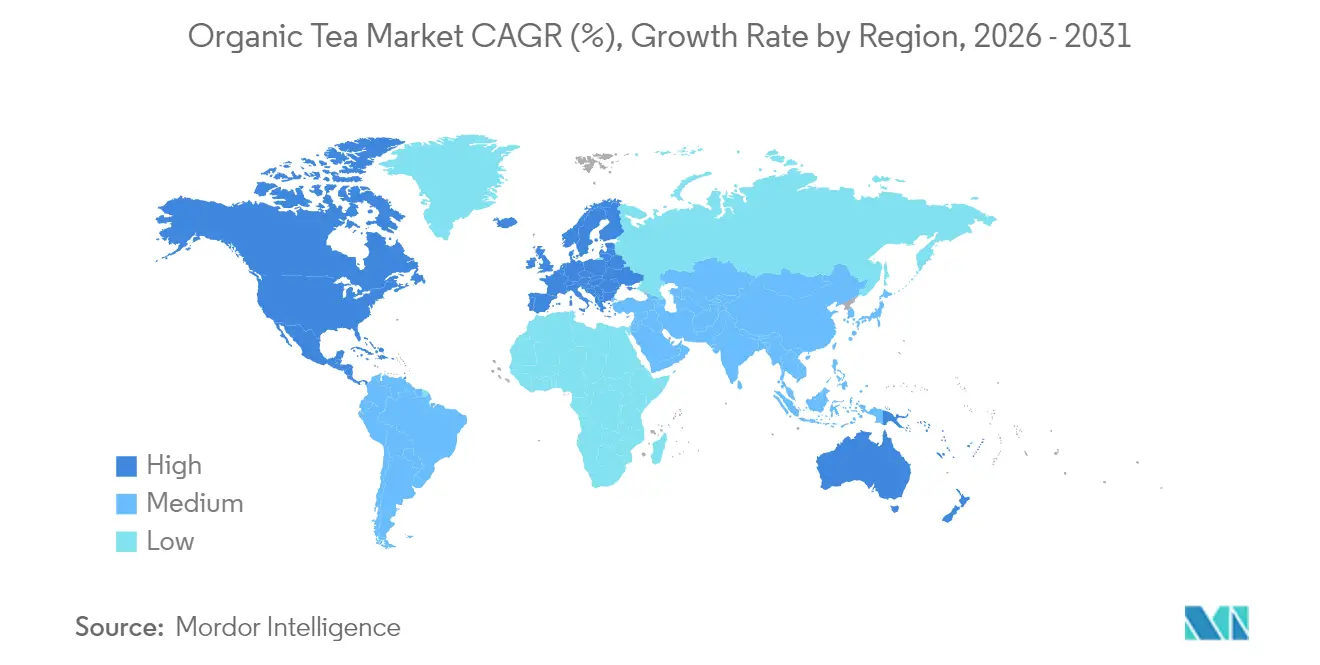

- By geography, Asia-Pacific dominated with 41.68% revenue share in 2025, whereas Europe is forecast to register the quickest regional CAGR at 12.49% from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Tea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Awareness Increases Demand for Chemical-Free Beverages | +3.20% | Global, with stronger impact in North America and Europe | Medium term (3-4 years) |

| Eco-Conscious Consumers Prefer Tea Sourced from Sustainable and Organic Farming Practices | +2.70% | Europe, North America, Urban APAC | Long term (≥ 5 years) |

| Government Incentives Boosts Growth by Promoting Organic Agriculture Adoption | +1.50% | Europe, North America, India | Medium term (3-4 years) |

| Premium Positioning of Organic Tea Appeals to Affluent Consumers | +2.10% | Global, with concentration in urban centers | Short term (≤ 2 years) |

| Functional Benefits Like Detox and Relaxation Drive Organic Tea Popularity | +2.40% | Global, with stronger impact in North America and Europe | Medium term (3-4 years) |

| Growth in E-Commerce Platforms Fueling the Market Growth | +1.90% | Global, with acceleration in APAC and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health Awareness Increases Demand for Chemical-Free Beverages

The rising health awareness among consumers has significantly increased the demand for chemical-free beverages, a key driver in the organic tea market. For instance, the United States Department of Agriculture (USDA) has reported a steady rise in organic product sales, including beverages, over the past decade. According to the USDA's 2023 Organic Survey, organic beverage sales accounted for a significant portion of the USD 63 billion organic market in the United States. Similarly, the Organic Trade Association (OTA) highlighted in its 2023 report that organic beverage sales grew by 8% year-over-year, driven by consumer preference for healthier alternatives. In Europe, the European Commission's "Farm to Fork" strategy has further encouraged the adoption of organic products, including tea, by promoting sustainable and chemical-free agricultural practices. Additionally, leading companies like Unilever, through its Lipton brand, have emphasized their commitment to offering organic and chemical-free tea options, as outlined in their latest annual report. Tata Consumer Products Limited, in its 2023 annual report, highlighted the expansion of its organic tea portfolio to cater to the growing consumer base seeking chemical-free options [1]Tata Consumer Products Limited, "Annual Report-2023", www.tataconsumer.com. These developments underscore the growing trend of health-conscious consumption, further propelling the organic tea market.

Eco-Conscious Consumers Prefer Tea Sourced from Sustainable and Organic Farming Practices

The growing preference for tea sourced from sustainable and organic farming practices is a significant driver of the Organic Tea Market. For instance, the United States Department of Agriculture (USDA) has established strict guidelines for organic certification, ensuring that tea producers adhere to sustainable farming methods [2]U.S. Department of Agriculture, "USDA Certified Organic: Understanding the Basics", www.ams.usda.gov. Similarly, the European Union's organic farming regulations promote environmentally friendly agricultural practices, further supporting the market's growth. According to the Food and Agriculture Organization (FAO), sustainable farming practices not only reduce environmental impact but also improve soil health, which is critical for tea cultivation. Additionally, companies like Unilever, through their Lipton brand, have committed to sourcing 100% of their tea sustainably, as highlighted in their annual sustainability reports. Companies like Tata Consumer Products and Unilever PLC, also emphasized its focus on sustainable sourcing and organic product offerings to meet evolving consumer preferences. Furthermore, initiatives like the Rainforest Alliance certification and Fair Trade certification are gaining traction, with many tea producers aligning their operations to meet these standards. These efforts reflect the increasing alignment of industry players with consumer demand for eco-conscious products, thereby driving the market forward.

Government Incentives Boosts Growth by Promoting Organic Agriculture Adoption

Government initiatives and incentives have significantly contributed to the growth of the organic tea market by promoting the adoption of organic agriculture practices. For instance, the United States Department of Agriculture (USDA) provides financial assistance through programs like the Organic Certification Cost Share Program (OCCSP), which helps farmers and processors offset the costs of organic certification. Similarly, the European Union has implemented the Common Agricultural Policy (CAP), which includes subsidies and grants to support organic farming. In India, the Paramparagat Krishi Vikas Yojana (PKVY) scheme encourages organic farming by offering financial aid and training to farmers [3]Ministry of Agriculture & Farmers Welfare, "PARAMPARAGAT KRISHI VIKAS YOJANA", www.pib.gov.in. According to the Food and Agriculture Organization (FAO), global organic farming land area increased by over 20% in the last decade, driven by such government initiatives. Additionally, companies such as Unilever and Tata Consumer Products have highlighted in their annual reports their commitment to sourcing organic tea, aligning with government policies and consumer demand for sustainable products. For example, Unilever reported a 15% increase in its procurement of organic tea in 2023, reflecting its alignment with sustainability goals. These efforts collectively drive the expansion of the organic tea market by fostering a supportive ecosystem for organic agriculture.

Premium Positioning of Organic Tea Appeals to Affluent Consumers

The premium positioning of organic tea serves as a significant driver for the organic tea market, particularly appealing to affluent consumers. For instance, according to the Organic Trade Association (OTA), the demand for organic beverages, including tea, has been steadily increasing, with a reported growth of over 5% in 2023. Additionally, government initiatives promoting organic farming practices, such as the USDA Organic Certification program, have further bolstered consumer trust in organic products. The European Union's Common Agricultural Policy (CAP) also supports organic farming through subsidies and incentives, further driving the market. Companies like Unilever, through their Lipton Organic Tea range, and Tata Consumer Products, as highlighted in their annual reports, have emphasized the rising preference for premium organic tea among high-income groups. Furthermore, the Tea Board of India has reported a notable increase in the production and export of organic tea, reflecting its growing demand globally. These factors collectively underscore the growing appeal of premium organic tea to affluent demographics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Costs Make Organic Tea Expensive for Many Consumers | -1.70% | Global, with stronger impact in price-sensitive markets | Medium term (3-4 years) |

| Supply Chain Limitations Hinder Consistent Organic Tea Availability | -0.40% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Strong Competition from Conventional and Flavored Teas Limits Organic Tea's Market Growth | -0.90% | Global, with stronger impact in traditional tea markets | Long term (≥ 5 years) |

| Lack of Knowledge on Organic Farming Hindering the Market Growth | -1.00% | APAC core, Africa, with spill-over to Latin America | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

High Production Costs Make Organic Tea Expensive for Many Consumers

High production costs remain a significant restraint for the global organic tea market, driven by labor-intensive farming practices, strict organic certification standards, and reliance on natural fertilizers and pest control methods, all of which elevate production expenses compared to conventional tea. The limited scale of organic tea farming further exacerbates costs, as achieving economies of scale is challenging, while lower yields due to the absence of synthetic inputs add to the financial strain. The certification process, requiring regular audits and compliance with stringent regulations, is both expensive and time-consuming, compounding the cost burden. Furthermore, the underdeveloped supply chain for organic tea compared to conventional tea leads to higher logistics and distribution expenses, resulting in a premium price point that restricts accessibility, particularly in price-sensitive markets. This pricing challenge continues to impede the global adoption of organic tea, despite increasing consumer awareness and demand for organic products, while also limiting producers' ability to compete with conventional tea manufacturers who benefit from lower production costs and established supply chains. Consequently, affordability remains a critical concern, posing significant barriers to the growth of the global organic tea market.

Supply Chain Limitations Hinder Consistent Organic Tea Availability

The global organic tea market is significantly restrained by supply chain limitations that disrupt the consistent availability of organic tea. These challenges arise from the complexity of sourcing certified organic raw materials, limited production capacities, and stringent regulatory requirements, with smaller-scale farming operations often unable to meet growing global demand. The time-consuming and costly certification process for organic products further complicates the supply chain, while transportation and storage issues, such as maintaining organic certifications during transit, exacerbate disruptions. Additionally, the market's reliance on specific geographic regions for organic tea cultivation creates vulnerabilities to climate change, natural disasters, and geopolitical tensions, which further destabilize supply chains. The lack of advanced infrastructure in key producing regions amplifies inefficiencies in processing, packaging, and distribution, ultimately hindering the market's ability to ensure a steady supply of organic tea and affecting its growth potential during the forecast period. As consumer demand for organic tea continues to rise, addressing these supply chain constraints will be critical for market players to achieve sustainable growth and meet evolving consumer expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Green Tea Leads, Herbal Infusion Tea Gain Momentum

In 2025, green organic tea holds a 39.62% market share, establishing itself as the leading segment. This leadership is attributed to its proven health benefits and increasing scientific validation of its functional properties. The shift toward healthier beverage options has significantly boosted its demand. Key benefits, including weight management, metabolism improvement, and antioxidant content, have driven its popularity among health-conscious consumers. Additionally, the rise in organic certifications and sustainable farming practices has strengthened consumer trust in green organic tea products.

The herbal and fruit infusion segment is projected to grow at a strong 13.42% CAGR from 2026 to 2031, outpacing other segments. This growth is driven by innovative flavor combinations and targeted functional claims, appealing to younger consumers seeking caffeine-free alternatives. The segment benefits from rising demand for natural and organic ingredients and increased awareness of the health benefits linked to herbal and fruit infusions. These beverages, often marketed as stress relievers, immunity boosters, and digestive aids, align with evolving consumer preferences. Furthermore, advancements in packaging and marketing strategies have enhanced the appeal of herbal and fruit infusions, solidifying their position in the global organic tea market.

By Packaging: Catons Reign Supreme, Tins Grow Rapidly

In 2025, cartons lead the global organic tea packaging market with a 34.62% share, driven by their cost-effectiveness, sustainability, and shelf stability. These features make cartons a preferred choice for manufacturers and retailers aiming to meet consumer demand for eco-friendly and practical packaging. Paper pouches, another significant segment, offer comparable sustainability benefits with added flexibility. Their lightweight design reduces transportation costs, making them particularly attractive to specialty retailers and e-commerce platforms that require adaptable packaging solutions.

Tins and cans, while currently holding a smaller share of the organic tea packaging market, are expected to grow at an 8.21% CAGR from 2026 to 2031. Their premium appeal resonates with consumers seeking high-quality organic tea products, while their ability to preserve freshness and aroma aligns with the quality standards expected by organic tea buyers. These attributes are likely to drive their increased adoption during the forecast period, particularly among brands targeting the premium segment.

By Distribution Channel: On-Trade Growth Transforms Market

In 2025, the off-trade segment held a 51.74% market share, with supermarkets and hypermarkets serving as key purchase points for mainstream organic tea buyers. These outlets meet the growing demand from health-conscious consumers by offering convenience and accessibility. Convenience and grocery stores also contribute significantly, attracting impulse buyers who make unplanned purchases during routine shopping. Online retail channels have gained traction, offering the widest product range and detailed information that appeals to informed organic tea consumers, enabling product comparisons and informed decisions, driving growth in the off-trade segment.

The on-trade segment, though smaller, is projected to grow at a strong CAGR of 15.92% from 2026 to 2031. This highlights the importance of cafes, restaurants, and hotels in the global organic tea market. These venues enhance brand visibility and encourage consumers to explore premium organic tea options. The shift toward premium and specialty organic teas is driving innovation, with brands developing exclusive blends and tailored packaging for food service applications. This trend is reshaping market competition as companies strive to differentiate and capture a larger share of this channel. Additionally, the segment benefits from the rising popularity of tea culture and the growing number of tea-focused establishments, which introduce consumers to a broader range of organic tea options.

By Flavor: Unflavored Leads, Flavored Gains Momentum

In 2025, the unflavored segment accounted for 72.48% of the global organic tea market, reflecting strong consumer demand for the authentic and pure qualities of natural organic tea. This preference stems from a focus on minimal processing and clean ingredients, aligning with wellness goals. The segment benefits from the growing demand for clean-label products, as consumers increasingly value transparency in sourcing and production. Additionally, its association with traditional tea-drinking cultures enhances its appeal among health-conscious and culturally aware buyers. In contrast, the flavored segment, while smaller, is projected to grow at a 12.76% CAGR from 2026 to 2031, driven by advancements in natural flavoring techniques that maintain organic standards while improving taste. The segment's growth is fueled by the popularity of innovative flavor combinations, such as fruit-infused, floral, and herbal blends, catering to diverse consumer preferences.

Younger consumers, particularly millennials and Gen Z, are driving this trend, seeking flavor exploration without compromising health benefits. These demographics view flavored organic teas as a balance of indulgence and wellness, creating opportunities for brands that can combine organic authenticity with appealing taste profiles. Companies investing in R&D to develop unique, naturally flavored teas are well-positioned to capture market share. The flavored segment's growth is further supported by the increasing availability of organic tea products across online and offline retail channels, expanding accessibility. As consumer preferences evolve, the global organic tea market is set for dynamic growth, with both unflavored and flavored segments shaping its trajectory.

Geography Analysis

In 2025, Asia-Pacific held a 41.68% share of the organic tea market, driven by its established role as a global tea production hub and rising domestic demand for premium organic teas. China leads with strong production capabilities and a growing middle class focused on health and wellness. In India, urban areas are reshaping tea consumption with specialized cafés boosting demand for premium organic options. Japan drives innovation in cultivation and processing, while Australia and South Korea see growth fueled by health-conscious urban populations. However, the region faces challenges in standardizing organic certifications due to varying regulatory frameworks. Europe is projected to grow at a 12.49% CAGR from 2026 to 2031, supported by increasing consumer awareness of sustainability and a robust organic certification system. Strict regulations enhance trust in certifications, while a shift toward premium, ethically sourced products drives demand. In Switzerland, specialized tea retailers are aligning with these trends, introducing innovative products and campaigns focused on quality and authenticity. North America, despite a smaller market share, shows significant growth potential. The U.S. organic tea market benefits from a health and wellness trend, with the ready-to-drink segment standing out as organic certification differentiates premium products. South America is emerging as an innovation hub, exemplified by Ecuador's Tippytea Blends, which supports fair trade, sources from local families, and uplifts around 250 households. Their unique Andean flavors are gaining global recognition. In the Middle East & Africa, markets like South Africa and the UAE are experiencing growing interest in organic teas. Premium positioning and health benefits appeal to affluent urban consumers, while traditional tea culture and rising sustainability awareness among younger demographics provide a strong foundation for market growth.

Competitive Landscape

The organic tea market is fragmented, fostering competition as established players contend with innovative entrants. Companies are increasingly adopting vertical integration to secure organic supply chains and strengthen their market position. For example, in January 2024, Tata Consumer Products acquired Organic India to expand its wellness portfolio and enhance distribution synergies. This reflects a broader consolidation trend, offering larger players advantages in certification compliance and distribution reach. Smaller players, however, face challenges due to limited resources and infrastructure.

Sustainability has become a critical differentiator in the market. Companies are moving beyond organic certification to implement initiatives like carbon neutrality, ethical sourcing, and eco-friendly packaging. These efforts align with consumer demand for environmentally responsible products, helping to build brand loyalty. Larger players, with greater resources, are better positioned to execute these strategies, intensifying competition.

Consumer preferences and regulatory requirements are also reshaping the market. Demand for transparency in sourcing and production is driving investments in traceability and supply chain management. Meanwhile, stricter regulations on organic certification and labeling are pushing companies to ensure compliance while managing costs. These factors, combined with consolidation and sustainability trends, are creating a challenging environment for smaller players. The market continues to evolve, driven by innovation, acquisitions, and a focus on sustainability.

Organic Tea Industry Leaders

-

Unilever Plc

-

Hain Celestial Group

-

Tata Consumer Products Ltd.

-

Associated British Foods plc

-

Harney & Sons Fine Teas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Wild Orchard Tea Company, a trailblazer in regenerative organic tea production, has debuted its Organic Certified® Everyday Green Tea, Everyday Black Tea, and Cinnamon Black Tea Bags at Wegmans Food Markets. Shoppers can find these products at 90 Wegmans locations throughout the Northeast. This launch underscores the company's dedication to regenerative organic farming and eco-friendly offerings.

- June 2024: Uncle Matt’s Organic® has introduced three new ready-to-drink refrigerated brewed black tea varieties to its product lineup: Brewed Unsweet Tea, Brewed Sweet Tea, and Half & Half Black Tea Lemonade. These offerings cater to diverse consumer preferences, providing both sweetened and unsweetened options, as well as a blend of black tea and lemonade.

- June 2024: Gujarat Cooperative Milk Marketing Federation (GCMMF) expanded its organic offerings with the launch of Amul Tea, Sugar, and Jaggery. This initiative aligns with the federation's strategy to cater to the growing demand for organic products. As part of this expansion, GCMMF aims to diversify its portfolio by introducing a total of 24 organic products, which will include essential staples such as wheat flour, rice, and pulses.

- March 2024: JUST ICE TEA, a brand owned by Eat the Change, launched a new lineup of organic teas packaged in cans. This innovative product range aims to cater to the growing demand for sustainable and healthier beverage options. The official unveiling of this product line took at the Natural Products Expo West trade show in Anaheim, CA, a prominent event showcasing natural and organic products.

Global Organic Tea Market Report Scope

Organic teas use no chemicals like pesticides, herbicides, fungicides, or chemical fertilizers, to grow or process the tea after it is harvested. Instead, farmers use natural processes to create a sustainable tea crop, like solar-powered or sticky bug catchers for preparing organic tea. The global organic tea market is segmented by the type of tea into black organic tea, green organic tea, oolong organic tea, and other organic teas. Based on the packaging into cartons, teabags, cans, paper pouches, and other mediums. By distribution channel into supermarket/ hypermarket, convenience stores, online stores, and other distribution channels. The market is also diversified based on geography into North America, Europe, Asia Pacific, South America, and the Middle East and Africa regions. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Black Organic Tea |

| Green Organic Tea |

| Oolong Organic Tea |

| Herbal/Fruit Infusion Organic Tea |

| Others |

By Flavor

| Unflavored |

| Flavored |

By Packaging

| Cartons |

| Paper Pouches |

| Tins/Cans |

| Sachets |

| Others |

By Distribution Channel

| Off-Trade | Supermarkets & Hypermarkets |

| Convinience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East & Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Black Organic Tea | |

| Green Organic Tea | ||

| Oolong Organic Tea | ||

| Herbal/Fruit Infusion Organic Tea | ||

| Others | ||

| By Flavor | Unflavored | |

| Flavored | ||

| By Packaging | Cartons | |

| Paper Pouches | ||

| Tins/Cans | ||

| Sachets | ||

| Others | ||

| By Distribution Channel | Off-Trade | Supermarkets & Hypermarkets |

| Convinience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East & Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global organic tea market?

The organic tea market is valued at USD 1.58 billion in 2026.

What compound annual growth rate (CAGR) is forecast for the organic tea market through 2031?

The market is projected to expand at a 12.18% CAGR between 2026 and 2031.

Which region holds the largest revenue share in the organic tea market?

Asia-Pacific leads with a 41.68% share as of 2025, supported by deep production expertise and rising middle-class demand.

Which organic tea category is growing the fastest?

Herbal and fruit infusion teas are expected to register the highest growth, advancing at a 13.42% CAGR from 2026 to 2031.

Page last updated on: