Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

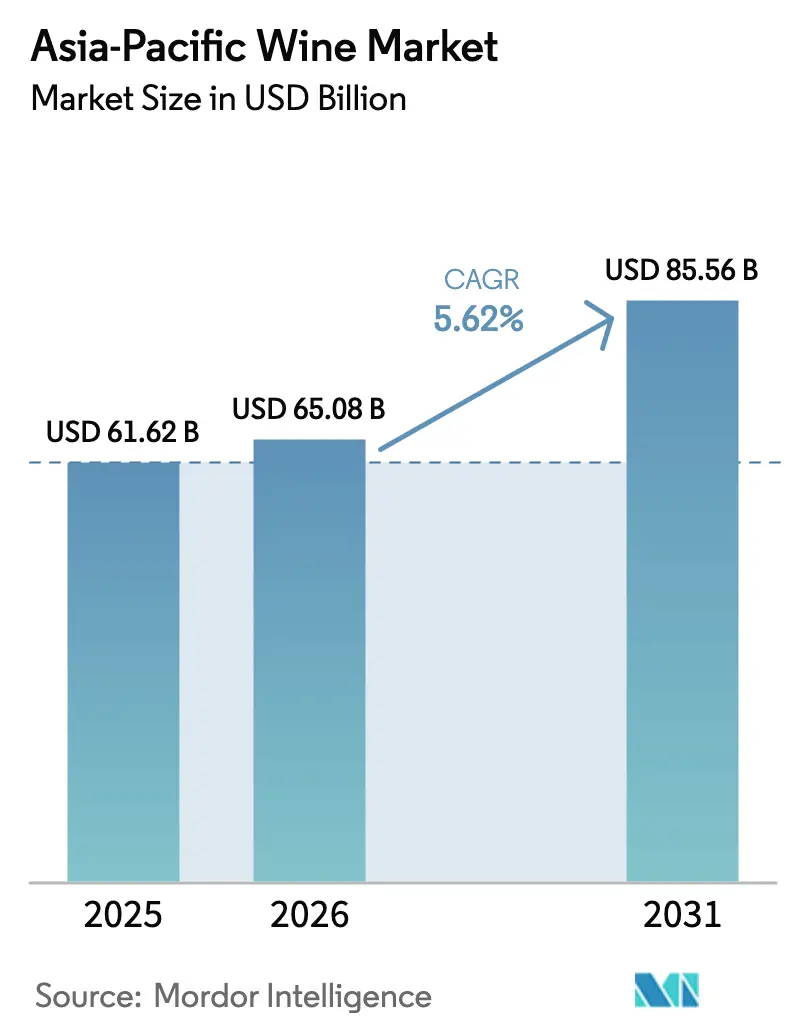

| Base Year Market Size (2025) | USD 61.62 Billion |

| Market Size (2026) | USD 65.08 Billion |

| Market Size (2031) | USD 85.56 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Wine Market Analysis by Mordor Intelligence

The Asia Pacific wine market size was valued at USD 61.62 billion in 2025 and estimated to grow from USD 65.08 billion in 2026 to reach USD 85.56 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). Steady volume gains and a pronounced shift toward premium offerings are underpinned by resilient household income, tariff liberalization in China and Thailand, and a sharp rise in omnichannel retail. Younger urban consumers, who prioritize authenticity, lower-alcohol alternatives, and climate-friendly production, are steering trends in favor of producers that can effectively combine terroir storytelling with ESG proof points. The sparkling sub-segment, buoyed by a culture of celebration and heightened visibility on social media, is managing to offset the volume pressures faced by still wine occasions. While challenges persist, ranging from competition with flavored RTDs and concerns over counterfeits to the complexities of uneven tax regimes, there are promising solutions. Technology-enabled traceability and climate-adaptive viticulture emerge as credible pathways to navigate these structural challenges.

Key Report Takeaways

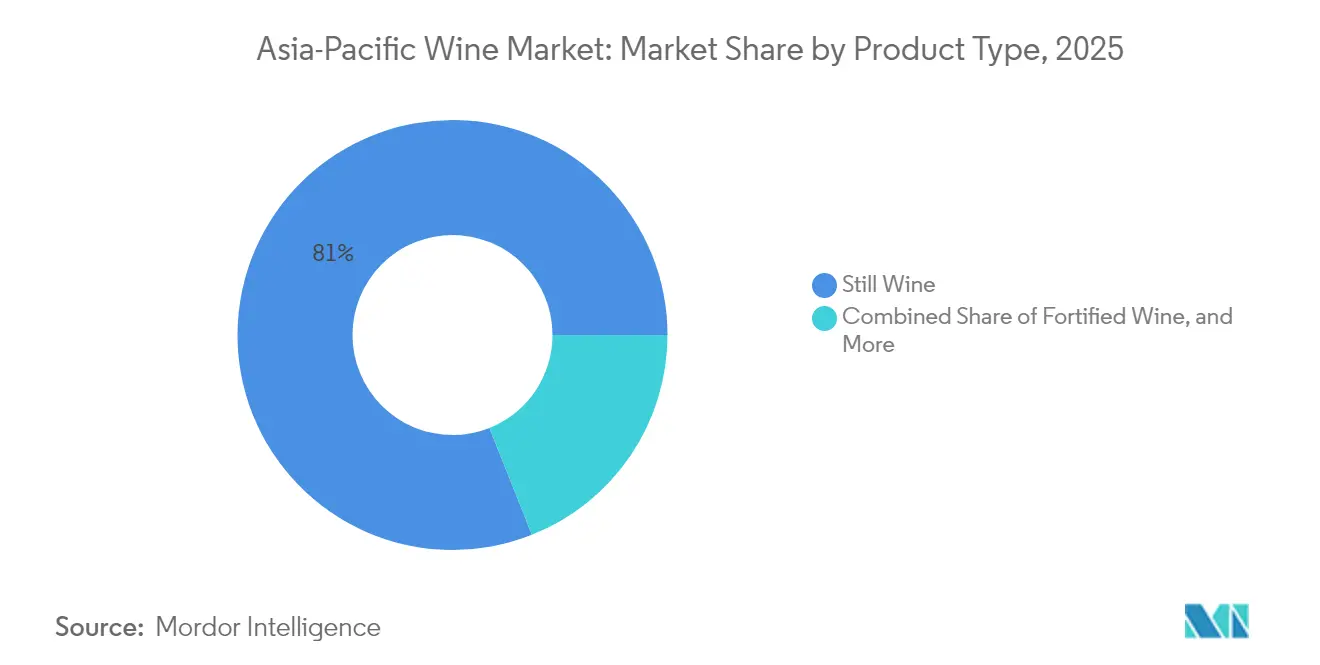

- By product type, still wine led with 81.02% of the Asia Pacific wine market share in 2025; sparkling wine is forecast to expand at a 6.21% CAGR through 2031.

- By colour, red wine accounted for 67.65% of the Asia Pacific wine market size in 2025, while rosé is advancing at a 7.55% CAGR through 2031.

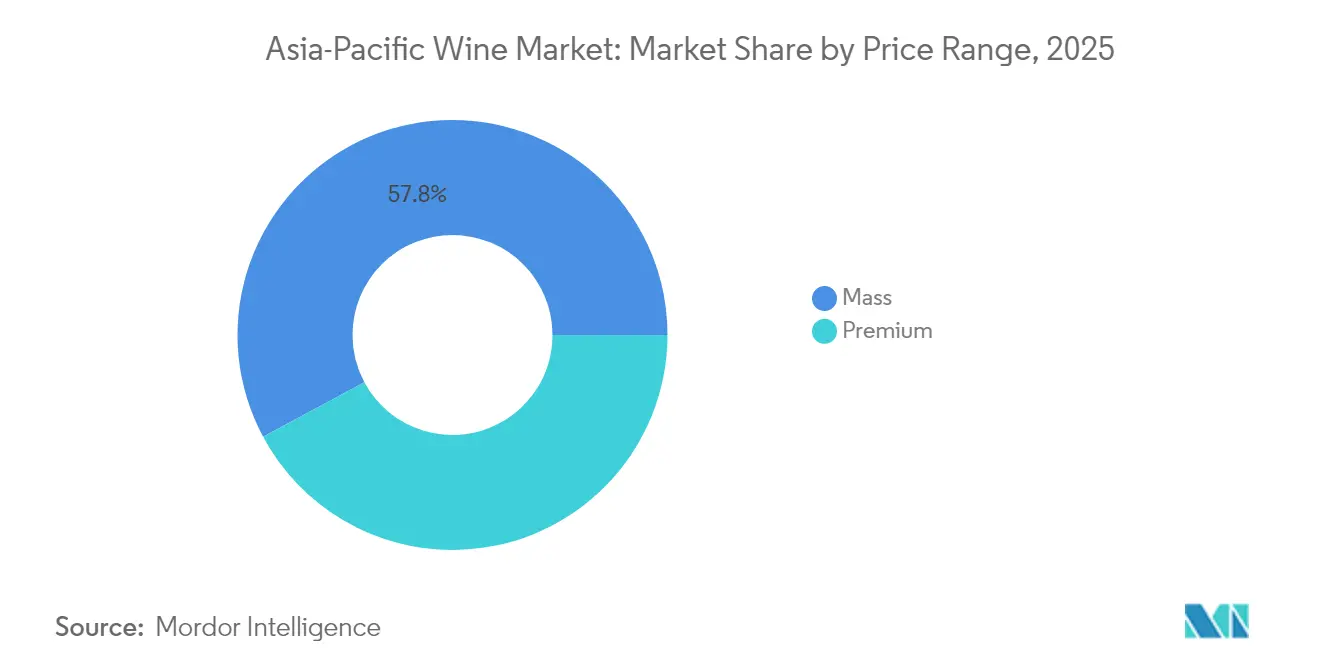

- By price range, mass-market labels held 57.84% revenue share in 2025; the premium tier is rising at a 6.93% CAGR to 2031.

- By end user, men represented 66.74% of consumption in 2025, whereas women showed the highest projected CAGR at 6.48% through 2031.

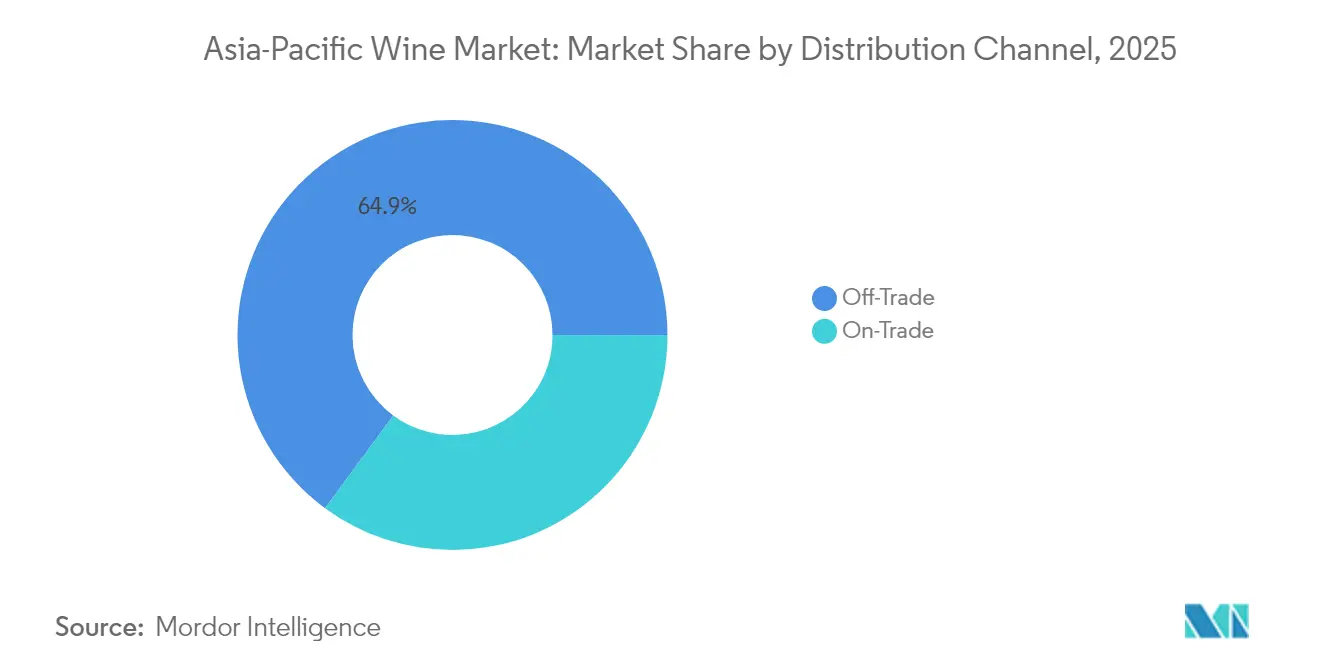

- By distribution channel, off-trade outlets captured 64.90% revenue in 2025 and are forecast to grow at a 6.60% CAGR on the back of e-commerce integration.

- By geography, China held a 62.95% share in 2025, whereas India remains the fastest-growing market at 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premiumization and gifting culture | +1.2% | China, Japan, South Korea, Singapore | Medium term (2-4 years) |

| Wine tourism and experiential marketing | +0.8% | Australia, New Zealand, China, India | Long term (≥ 4 years) |

| Exotic flavor exploration and new tastes | +0.7% | Southeast Asia, India, Vietnam | Short term (≤ 2 years) |

| Climate-adaptive grape R&D | +0.5% | Thailand, Vietnam, Indonesia, Malaysia | Long term (≥ 4 years) |

| Technological advances in winemaking | +0.4% | Australia, New Zealand, global spillovers | Medium term (2-4 years) |

| Celebration culture and social occasions | +0.6% | China, India, Philippines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Premiumization and Gifting Culture

As the middle class expands in the Asia Pacific, the demand for premium wine experiences is surging. McKinsey's 2024 consumer research highlights that younger Asian consumers are more inclined than their Western counterparts to opt for premium brands[1]Source: McKinsey & Company, “State of the Consumer 2024: What’s Now and What’s Next,” mckinsey.com. This shift presents lucrative opportunities for wine producers aiming at affluent buyers. China's grape wine production totaled 0.30 million kiloliters, generating a notable RMB 9.09 billion in sales revenue in 2024. This uptick underscores a robust value-per-liter trend, as noted by the Chinese Ministry of Commerce[2]Source: Ministry of Commerce of the People’s Republic of China, “酒类流通监测统计与管理,” mofcom.gov.cn. Despite economic fluctuations, traditions like corporate gifting during the Lunar New Year and business celebrations bolster the demand for premium imported wines. In 2024, Singapore's market saw a significant share attributed to its premium wine segment, which is characterized by bottles priced above SGD 70. Moreover, this premium consumption trend isn't confined to established markets. With Vietnam's middle class projected to swell by 23.2 million members by 2030, new opportunities for premium consumption are on the horizon, as highlighted by KPMG Vietnam.

Wine Tourism and Experiential Marketing

As Asia Pacific economies rebound from pandemic setbacks, wine tourism is emerging as a pivotal growth driver. The Asian Development Bank reports that tourist arrivals in Southeast Asia surged to 61.4 million in the first half of 2024, representing a 32% increase from the same period in 2023. In a bid to harness this recovery momentum, Wine Australia's Tourism Ready program, developed in collaboration with industry stakeholders, aims to attract international visitors and bolster the tourism sector. China's wine tourism infrastructure stands out for its sophistication, with studies indicating that the quality of winery services plays a crucial role in shaping brand equity at prominent destinations. The UN Tourism Global Conference on Wine Tourism 2024 spotlighted "Heritage in Every Bottle," underscoring the importance of genuine experiences and sustainable growth. This theme provides a blueprint for Asia-Pacific locales to create unique offerings. Meanwhile, Thailand's GranMonte winery is pushing the boundaries of tropical viticulture, successfully cultivating Syrah, Viognier, and Chenin Blanc in warmer climates. Despite facing regulatory hurdles, GranMonte is also enhancing its experiential tourism initiatives.

Exotic Flavor Exploration and New Taste Preferences

The Asia Pacific wine market demonstrates evolving consumer preferences toward distinct varietals and new wine styles. The recognition of Suntory's Tomi Koshu 2022 with Best in Show at the 2024 Decanter World Wine Awards marks significant progress for Japanese wines internationally, highlighting the potential of local grape varieties and winemaking methods. This recognition has increased interest in Asian wine production and climate-specific viticulture. Studies of wine consumption patterns in Taiwan and Malaysia show that taste characteristics and consumption occasions influence purchasing decisions. Malaysian consumers value pleasure and traditional aspects, while Taiwanese consumers focus on personal achievement and self-direction. The Southeast Asian market shows a preference for wines with pronounced fruit characteristics and lower alcohol content, which complement local cuisine and suit the tropical climate. Research into climate change adaptation has identified potential new grape varieties and rootstock combinations that can maintain wine quality while withstanding warmer conditions. Natural, biodynamic, and organic wines represent a small but growing segment, reflecting increased consumer awareness and environmental consciousness, particularly among younger consumers who seek sustainable products.

Climate-Adaptive Grape R&D Accelerating Vineyard Viability in Tropical Zones

Recent scientific developments in viticulture have enabled wine production to expand into tropical and subtropical regions of the Asia Pacific that were previously unsuitable. Research from Portugal demonstrates how high-resolution microclimate modeling supports vineyard adaptation through site-specific irrigation, canopy management, and climate-resilient cultivar selection. Australian studies have identified adaptation strategies, including varietal selection, rootstock breeding, irrigation management, and protective measures to maintain wine quality under higher temperatures and extreme weather. These advances are significant for Southeast Asian markets, where high humidity, heavy rainfall, and temperature extremes challenge traditional viticulture methods. Thailand's experience with tropical viticulture shows the practical implementation of climate-adaptive techniques, although regulatory restrictions constrain sector growth. The development of drought-tolerant and heat-resistant cultivars, along with precision irrigation systems and improved soil management, presents opportunities for domestic production growth in import-dependent markets. Disease-resistant varieties help reduce agrochemical use while maintaining quality standards, addressing both environmental and cost considerations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent counterfeit risk | -0.9% | China, Southeast Asia, India | Medium term (2-4 years) |

| High excise duties and complex taxes | -1.1% | India, Thailand, Malaysia, Indonesia | Short term (≤ 2 years) |

| Youth shift toward flavored RTDs | -0.8% | Urban centers region-wide | Long term (≥ 4 years) |

| Fragmented regulatory environment | -0.7% | Southeast Asia, India, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Counterfeit Risk Undermining Consumer Trust

The prevalence of counterfeit wine in the Asia Pacific markets impedes the growth of premium segments and undermines brand trust. Major enforcement operations in Shanghai and Yantai highlight the extent of this issue, with counterfeit Chateau Lafite production reportedly exceeding legitimate exports in some years. The Wine Origins Alliance implements traceability measures, including RFID tags, QR codes, blockchain verification, and government seals, to protect consumers and producers. However, small artisanal producers face difficulties adopting these solutions due to cost and technical limitations. Status-driven consumption patterns in premium segments further incentivize sophisticated counterfeiting operations. The market currently encompasses more than 1,000 different sustainability and authenticity certifications, leading to consumer confusion and opportunities for fraudulent claims. This situation requires unified certification standards and stronger enforcement protocols.

High Excise Duties and Complex Sub-National Taxes

The Asia Pacific region faces significant market access barriers due to complex taxation systems and high duty rates across multiple jurisdictions, which limit consumption growth and import competitiveness. In India, alcohol taxation remains under state control, resulting in 29 distinct excise markets with diverse duty structures and administrative requirements. Federal tariffs of 150% ad valorem on wines (50% basic customs duty plus 100% AIDF cess), combined with state-level excise regimes, result in duties and taxes comprising 60-75% of final consumer prices. Thailand's recent policy changes demonstrate the benefits of liberalization, as tariff elimination and excise reduction from 10% to 5% are expected to decrease retail prices by 35-40% and increase tourism-driven demand[3]Source: Dhruv Sood, “Distilled Spirits, Wine and Beer Market Update 2024,” fas.usda.gov. However, several markets maintain protective policies that support domestic spirits production or secure government revenue. Additional barriers include complex labeling requirements, import licensing procedures, and certification mandates, which increase administrative costs and create delays, particularly affecting smaller importers and premium wine segments. The diverse regulatory landscape requires market-specific compliance approaches and restricts the development of efficient regional distribution networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Wine Dominance Faces Sparkling Acceleration

Still wine held 81.02% market share in 2025, reflecting established consumption patterns and food pairing traditions across Asia Pacific cultures. Sparkling wine is expected to demonstrate the highest growth potential, with an estimated 6.21% CAGR through 2031, driven by the increasing celebration culture and premium consumption trends. Fortified wine maintains a specialized market presence, particularly in Australia and New Zealand, while the "Others" category, which includes ice wine, aromatized varieties, and low- or no-alcohol options, appeals to health-conscious consumers. In Japan, sparkling wine imports reflect the evolution of the market, with French and Spanish producers competing as Spanish Cava gains popularity due to its Champagne-method production and competitive pricing.

Market dynamics reflect changing consumer preferences, with younger consumers adopting sparkling wine for social occasions and lifestyle enhancement. Treasury Wine Estates demonstrates industry adaptation through initiatives like the Penfolds Evermore program, launched in April 2024 with AUD 1 million in grants over five years, combining environmental responsibility with product development. Low and no-alcohol wine variants show significant growth as consumers seek alternatives that preserve wine consumption traditions without alcohol content.

By Colour: Red Wine Leadership Challenged by Rosé Innovation

Red wine held a 67.65% market share in 2025, driven by traditional preferences and established food pairing practices across Asian cuisines. Rosé wine demonstrates the highest growth rate with a 7.55% CAGR, driven by premium positioning, social media visibility, and expanded consumption occasions. White wine shows varied performance across different regions and consumption occasions. In China's domestic production, red varieties account for approximately 80% of vineyard area, with Cabernet Sauvignon representing about 80% of red grape plantings, according to HAL Science.

Rosé's growth stems from marketing initiatives that expand its consumption beyond seasonal occasions by emphasizing lifestyle and wellness attributes. The category benefits from social media visibility, premium packaging developments, and celebrity partnerships that appeal to younger consumers. Research on climate change adaptation indicates that rosé production may improve through early harvest timing and temperature control methods that maintain wine acidity and freshness in warmer conditions. White wine performance varies across markets, with developed markets such as Japan showing strong demand for Chardonnay, while emerging markets prefer sweeter, fruit-forward varieties that match local taste preferences and warm climate consumption patterns.

By Price Range: Premium Segment Outpaces Mass Market Growth

In 2025, mass-market wines dominated with a 57.84% share, underscoring the price sensitivity and accessibility needs of the Asia Pacific's varied income levels. Meanwhile, the premium wine segment is on a growth trajectory and is expected to expand at a 6.93% CAGR through 2031. A burgeoning middle class, a culture of gifting, and a trend towards experiential consumption fuel this surge. Such trends highlight a broader consumer divide: some prioritize value, while others chase experiences. Take Singapore, for instance: in 2024, wines priced above SGD 70 per bottle accounted for a notable share of the market, highlighting the allure of the premium segment.

Positioned as a premium offering, the segment capitalizes on sustainability. Organic wines and those adhering to ESG standards fetch higher prices, appealing to eco-conscious buyers. Yet, there's a twist: while consumers tend to lean towards organic options when they are priced similarly to traditional wines, they often revert to conventional choices if the premium is substantial. On the other hand, the mass market grapples with competition from ready-to-drink alternatives and spirits. To counter this, there's a push for enhanced value propositions. Strategies include innovative packaging, compelling brand narratives, and a premium positioning that's accessible, all while ensuring quality perception remains intact.

By End User: Women's Consumption Growth Outpaces Male Dominance

In 2025, men account for 66.74% of wine consumption in the Asia Pacific markets, a trend rooted in traditional gender roles and a culture of business entertainment. Yet, women are emerging as the fastest-growing demographic, boasting an expected 6.48% CAGR through 2031. This surge is fueled by evolving social norms, greater economic participation, and a trend towards lifestyle premiumization. Such a transformation paves the way for tailored marketing, product innovation, and strategic channels that cater to women's preferences and consumption moments. Research from the USDA highlights that in India, women are not only more engaged in on-premise wine consumption but are also willing to pay a premium for quality experiences.

The uptick in female wine consumption reflects broader societal shifts, including urbanization, delayed marriages, and career advancements, which are all contributing to increased disposable incomes and more social consumption opportunities. Female consumers are particularly drawn to wine tourism and experiential marketing, valuing authentic, educational, and social experiences over mere alcohol consumption. This demographic shows a pronounced interest in sustainability, health-conscious choices, and alignment with brand values. Producers emphasizing environmental stewardship, social responsibility, and transparent practices stand to gain. Moreover, health-conscious women are gravitating towards lower-alcohol and organic wine variants, allowing them to enjoy wine while prioritizing wellness.

By Distribution Channel: Off-Trade Dominance Strengthens Through Digital Integration

In 2025, off-trade channels captured a 64.90% market share and projected a 6.60% CAGR through 2031, driven by the expansion of modern retail, the rise of e-commerce, and a shift towards convenience. Specialty liquor stores, bridging the gap between online and offline, lead the off-trade scene with their curated selections and expert advice. Supermarkets, hypermarkets, and convenience stores, as part of the broader off-trade landscape, are expanding their wine offerings, recognizing both the profitability of the category and the growing demand from consumers. While on-trade channels grapple with post-pandemic recovery, they find solace in a tourism rebound and a trend towards experiential consumption.

Digital transformation is propelling off-trade growth. KPMG research reveals that 45% of consumers in the Asia Pacific prefer omnichannel experiences, which blend online and physical retail. Channels like social commerce and live streaming are surging, particularly in regions such as China and Southeast Asia, as well as among Gen Z, who prioritize experiential marketing and influencer endorsements. In China, a 55% adoption rate of buy-now-pay-later schemes is paving the way for premium wine purchases, thanks to the allure of flexible payments. The e-commerce landscape for wine is diverse, with no single player dominating, urging businesses to adopt multi-platform strategies tailored to local payment preferences, logistics, and consumer tastes. Unlike traditional retail, wine-centric e-commerce platforms such as VineSpring, VinoShipper, and Vivino excel in inventory management, customer education, and direct-to-consumer sales.

Geography Analysis

In 2025, China held a dominant 62.95% market share. Following the lifting of tariffs on Australian wine in March 2025, shipments rebounded to AUD 1.03 billion within a year. While domestic output was a modest 0.30 million kiloliters, it raked in sales of RMB 9.09 billion, underscoring a strategic shift towards valuing sales over volume. In December 2024, Treasury Wine Estates showcased its commitment by acquiring 75% of Ningxia Stone & Moon Winery, navigating through challenges like anti-counterfeiting and economic fluctuations. E-commerce is boosting volumes, but trust concerns are pushing demand for blockchain-verified products. With beer and baijiu as cultural mainstays, wine's growth hinges on premium narratives and robust supply chains.

India, currently holding a mere 0.96% of the revenue pie, is the fastest-growing player, boasting a 7.18% CAGR projected through 2031. The Australia-India ECTA has slashed duties on premium wine brackets, spurring imports. However, state taxes still keep prices elevated, as highlighted by Wine Australia. While consumption is centered in five major metros, Tier-2 cities like Jaipur and Chandigarh are emerging, bolstered by visibility in modern trade. Though domestic production is in its infancy, it stands to gain from Maharashtra’s vineyard clusters and the burgeoning tourism in Nashik. Ongoing negotiations on bottled-in-origin rules could further amplify the category's potential.

Japan and South Korea showcase a discerning, quality-centric demand. Japan boasts 303 wineries under its “Japan Wine” label, yet local production satisfies only 4% of the nation's consumption, leaving ample room for imports. The EU's tariff removal in 2024 heightens competitive pressures, compounded by an aging vineyard workforce that hampers domestic growth. In South Korea, imports have favored U.S. suppliers, with shipments witnessing a 14% uptick in 2024, driven by premium positioning, as reported by the USDA. Both nations place a premium on sustainability and smaller, exclusive releases that appeal to their refined palates.

Southeast Asia offers a mixed bag of opportunities. Vietnam, buoyed by a 5.05% GDP growth in 2024 and benefitting from 16 FTAs, is witnessing a surge in imports. In Thailand, a duty cut in February 2024 slashed prices by up to 40%, spurring gains driven by tourists. Singapore stands out as a re-export powerhouse, with a USD 980 million market, merging robust domestic consumption with regional distribution. However, Malaysia and Indonesia face challenges due to religious constraints and steep duties, relegating wine to premium urban segments. The future of the region's wine market is contingent on tax reforms, enhancements in cold-chain infrastructure, and a rebound in tourism.

Competitive Landscape

The Asia Pacific wine market remains fragmented, offering both established multinationals and emerging regional players a chance to capture market share through unique positioning strategies. Yantai Changyu Pioneer Wine Co., Ltd, spearheads production in China, while Treasury Wine Estates, with its Penfolds brand, targets premium markets globally. This strategy is bolstered by acquisitions, notably the 75% stake in Ningxia Stone & Moon Winery secured in December 2024. In a nod to industry consolidation, April 2025 saw the birth of Vinarchy, a merger of Accolade Wines and Pernod Ricard's wine operations from Australia, New Zealand, and Spain. This new entity boasts an impressive production of over 32 million cases and net sales hitting AUD 1.5 billion annually.

Leading producers are increasingly adopting technology, with artificial intelligence now standard for vineyard monitoring, soil analytics, and personalized marketing. There's a growing emphasis on sustainability, digital-first distribution, and climate-adaptive viticulture. Initiatives like New Zealand Winegrowers' "Roadmap to Net Zero 2050" and the Sustainable Winegrowing New Zealand certification, which spans 98% of the vineyard area, highlight how sustainability can be a competitive edge in today's eco-conscious market.

New entrants are harnessing direct-to-consumer channels, social commerce, and influencer collaborations to navigate traditional distribution hurdles. This is especially evident in markets with stringent regulations or dominant incumbents. Wine-centric e-commerce platforms and subscription models are enabling smaller producers to connect directly with affluent urban consumers. Meanwhile, established brands are bolstering their market presence by investing in omnichannel strategies, blending physical retail, online platforms, and experiential marketing to adapt to shifting consumer preferences.

Asia-Pacific Wine Industry Leaders

Yantai Changyu Pioneer Wine Co Ltd

Constellation Brands, Inc

Treasury Wine Estates

Great Wall Wine (CoFCO)

Accolade Wines

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Pernod Ricard completed the sale of its wine portfolio to the owner of Accolade Wines, creating industry consolidation and repositioning Pernod toward spirits categories while strengthening Accolade's position in the Asia Pacific markets.

- April 2025: Vinarchy launched as a new global wine company through the combination of Accolade Wines with Pernod Ricard's Australian, New Zealand, and Spanish wine businesses, producing over 32 million cases annually with AUD 1.5 billion in net sales and targeting accelerated growth in emerging Asia Pacific markets, including China, Japan, Korea, and India.

- December 2024: Treasury Wine Estates acquired 75% of Ningxia Stone & Moon Winery, demonstrating a strategic commitment to Chinese market development and local production capabilities to serve premium domestic demand.

- August 2024: Penfolds confirmed plans to build vineyard and winery facilities in China, signaling major investment in local production capabilities to serve growing domestic premium wine demand and reduce import dependency.

Asia-Pacific Wine Market Report Scope

Wine is an alcoholic drink typically made from fermented grape juice. The wine market is segmented by product type, color, distribution channel, and geography. The Asia-Pacific wine market is segmented by product type into still wine, sparkling wine, Fortified Wine and Vermouth). The market is segmented by color into red wine, rose wine, and white wine. Based on the distribution channel, the market is classified as on-trade and off-trade channels, of which the off-trade channel is further classified into supermarkets/hypermarkets, specialty stores, online retail channels, and other distribution channels. In terms of Geography, the market is segmented into China, Japan, India, Australia, and the rest of the Asia-Pacific region. For each segment, the market sizing and forecasting have been done in value terms of USD million.

By Product Type

| Fortified Wine |

| Still Wine |

| Sparkling Wine |

| Others Wine Types (Ice, Aromatised, Low/No-Alc) |

By Colour

| Red Wine |

| White Wine |

| Rose Wine |

By Price Range

| Mass |

| Premium |

By End User

| Men |

| Women |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Others Off Trade Channels |

By Geography

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Vietnam |

| Thailand |

| Indonesia |

| Singapore |

| Malaysia |

| Rest of Asia-Pacific |

| By Product Type | Fortified Wine | |

| Still Wine | ||

| Sparkling Wine | ||

| Others Wine Types (Ice, Aromatised, Low/No-Alc) | ||

| By Colour | Red Wine | |

| White Wine | ||

| Rose Wine | ||

| By Price Range | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Others Off Trade Channels | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Thailand | ||

| Indonesia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia Pacific wine market?

The market is valued at USD 65.08 billion in 2026 and is forecast to reach USD 85.56 billion by 2031.

Which product segment is growing fastest?

Sparkling wine leads growth with a 6.21% CAGR, driven by celebration culture and premium positioning.

Why is India considered the fastest-growing country for wine in Asia Pacific?

A young demographic, urbanization, and tariff reductions under the Australia-India ECTA support a 7.18% CAGR through 2031.

What role does e-commerce play in regional wine sales?

Off-trade channels, powered by omnichannel retail and social-commerce live streams, account for 64.90% of revenue and grow at 6.60% CAGR.

Page last updated on: