Sparkling Wine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 45.91 Billion |

| Market Size (2031) | USD 59.42 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

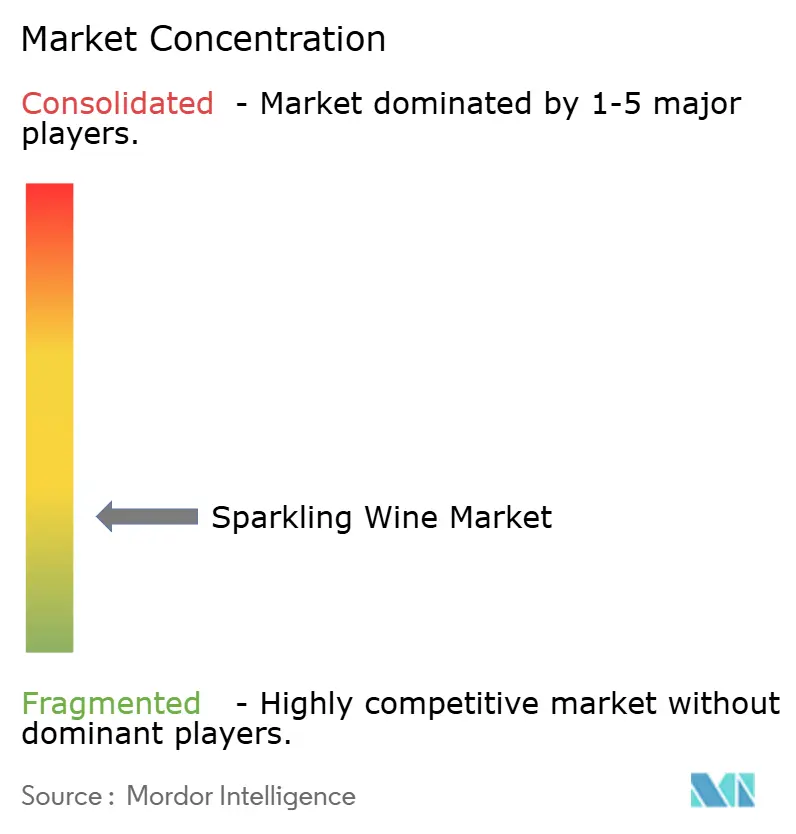

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sparkling Wine Market Analysis by Mordor Intelligence

The Sparkling Wine Market size was valued at USD 43.61 billion in 2025 and estimated to grow from USD 45.91 billion in 2026 to reach USD 59.42 billion by 2031, at a CAGR of 5.29% during the forecast period (2026-2031). Consumer preferences for premium products, combined with rising disposable incomes in developing economies, have transformed sparkling wine from a special occasion beverage to an everyday indulgence. The widespread adoption of e-commerce platforms and direct-to-consumer (DTC) business models has revolutionized distribution channels, making sparkling wines more accessible to consumers while improving profit margins for producers. Europe continues to dominate the market in terms of value, benefiting from its rich wine-making heritage and established consumer base. Meanwhile, the Asia-Pacific region demonstrates remarkable growth potential, driven by changing consumer preferences, the revival of international tourism, and the increasing popularity of sparkling wine as a gifting option. Wine producers are strengthening their market positions by emphasizing their historical legacy, implementing sustainable production methods, and investing in advanced quality control systems. However, they must navigate challenges including stricter labeling regulations and persistent supply chain disruptions that contribute to unpredictable freight costs.

Key Report Takeaways

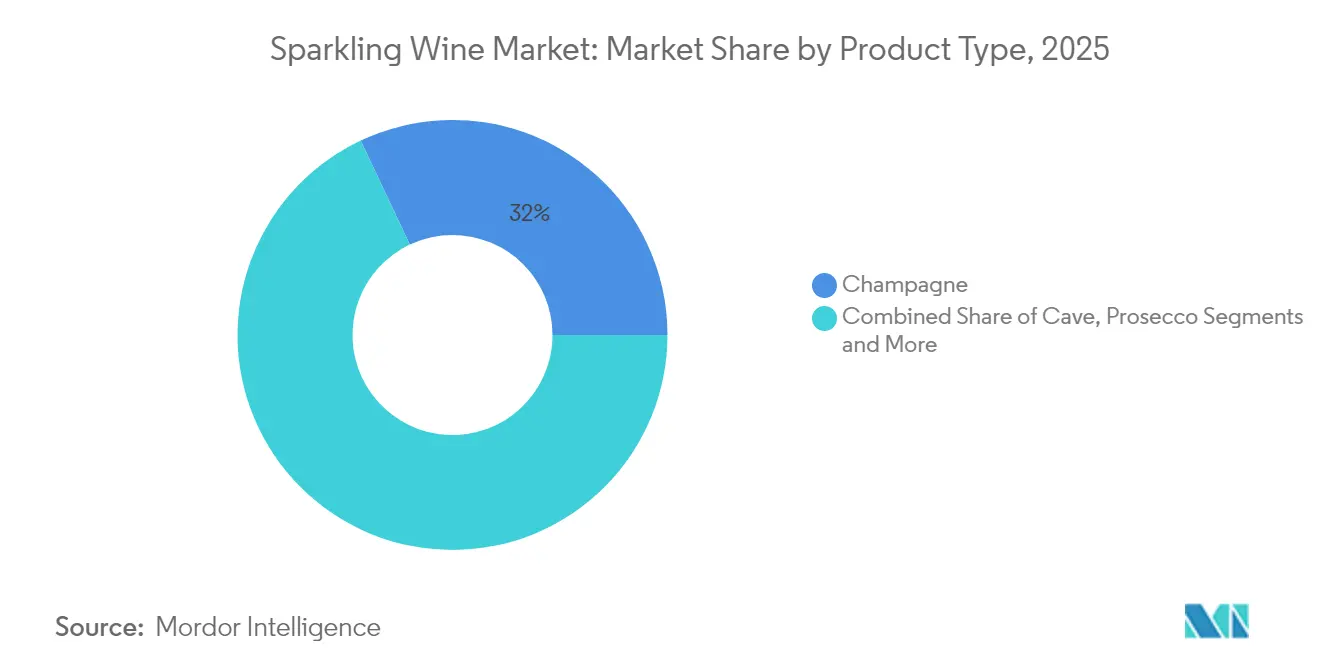

- By product type, champagne held 32.02% of sparkling wine market share in 2025, while prosecco is forecast to grow at a 6.52% CAGR to 2031.

- By category, premium offerings commanded 54.62% share of the sparkling wine market size in 2025 and are set to expand at a 6.58% CAGR between 2026-2031.

- By packaging, glass bottles accounted for 67.55% revenue in 2025; canned formats are projected to register a 6.55% CAGR through 2031.

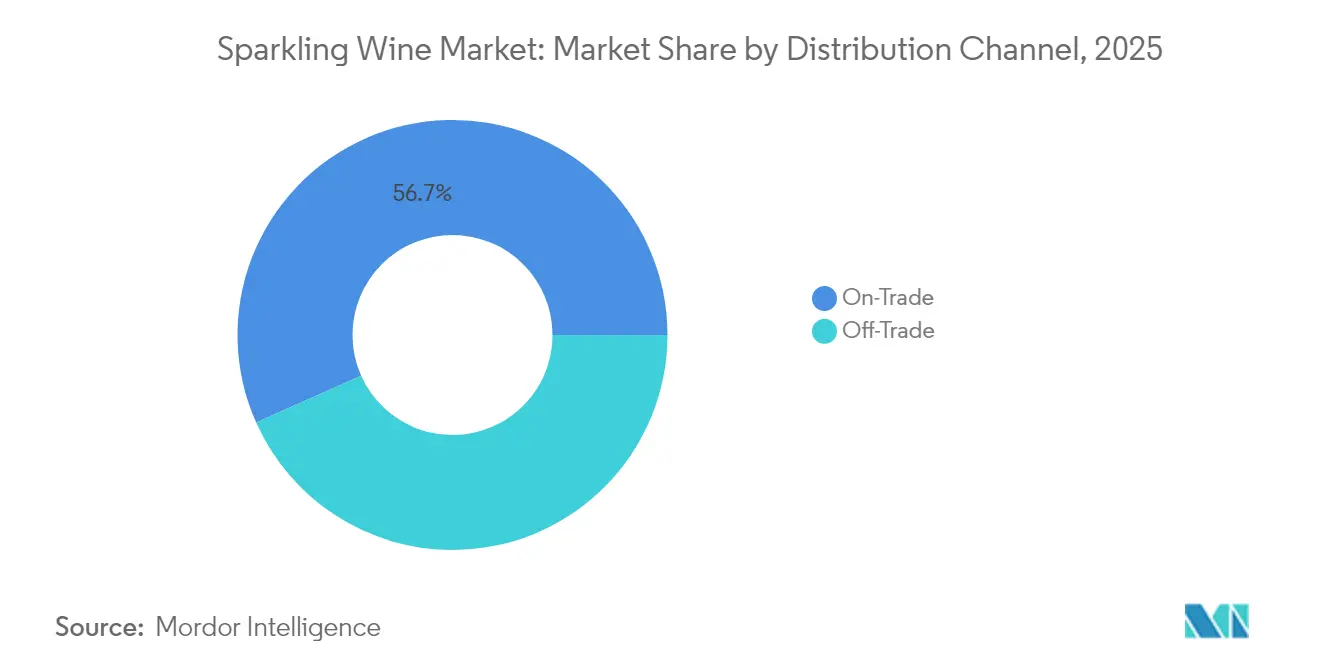

- By distribution channel, on-trade venues captured 56.68% of 2025 sales, whereas off-trade channels are poised for a 6.70% CAGR on the back of online retail and DTC platforms.

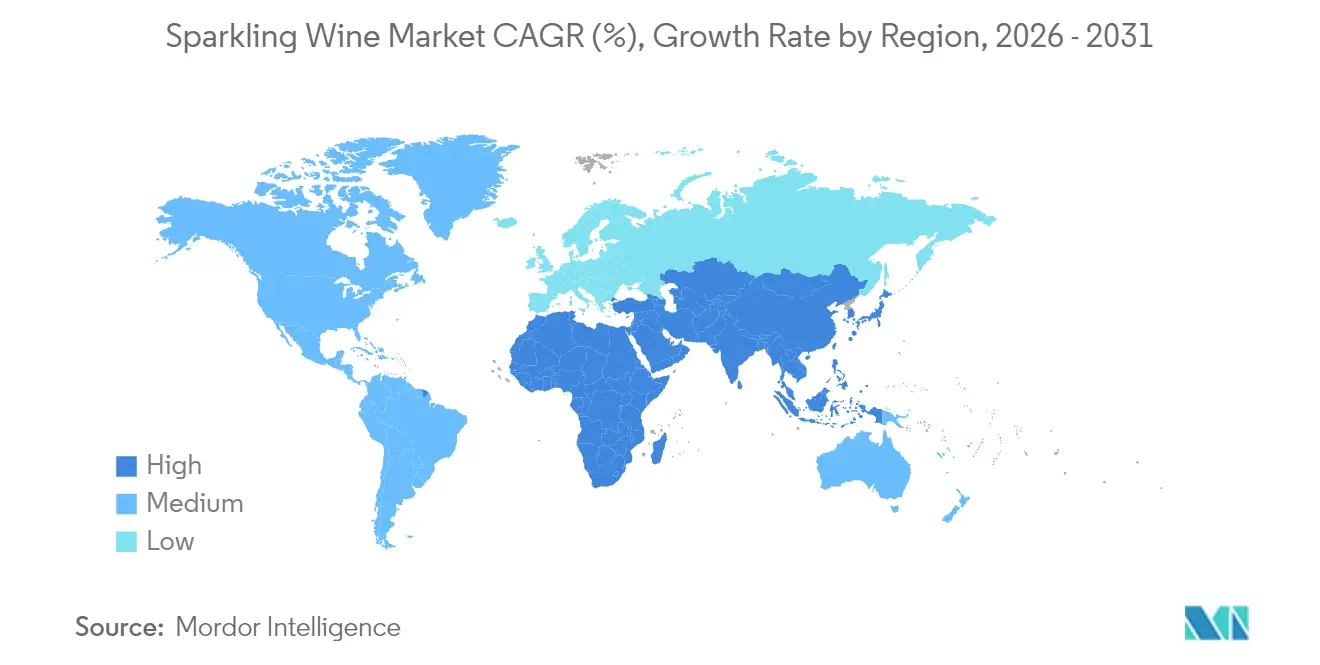

- By geography, Europe led with 33.86% value share in 2025, yet Asia-Pacific is expected to post a 6.79% CAGR to 2031 as income levels and wine literacy rise.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sparkling Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of sparkling wine offerings | +1.0% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Growth of wine tourism and vineyard experiences | +0.7% | Europe, North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Sustainability and eco-friendly production practices | +0.5% | Global, led by EU regulations and consumer demand | Long term (≥ 4 years) |

| Popularity of Italian and Spanish sparkling wines | +0.8% | Global, with particular strength in Asia-Pacific and Americas | Medium term (2-4 years) |

| Adoption of advanced winemaking technologies | +0.6% | Developed markets initially, expanding to emerging regions | Medium term (2-4 years) |

| Innovation in packaging and formats | +0.9% | Global, with strongest adoption in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization of Sparkling Wine Offerings

Consumer willingness to pay higher prices for sparkling wine is reshaping market dynamics, driven by evolving preferences and increased disposable income. The super-premium segment, where prosecco dominates sales growth, reflects changing consumer behavior as sparkling wine transitions from occasional indulgence to a regular luxury purchase. Premium pricing strategies now encompass sophisticated packaging innovations, with luxury brands investing in distinctive bottle designs and environmentally conscious materials to enhance perceived value. LVMH's champagne portfolio demonstrates the success of this approach, with Moët & Chandon achieving a valuation of USD 1.4 billion and Dom Pérignon reaching USD 799.8 million in 2024. Italian and Spanish producers have successfully capitalized on this premiumization trend by highlighting their centuries-old production techniques and unique regional characteristics, enabling them to command higher price points across international markets.

Growth of Wine Tourism and Vineyard Experiences

Wine tourism serves as a revenue diversification strategy, with successful micro-clusters attracting substantial visitor numbers annually and generating economic impact for rural communities. The combination of experiential offerings with sparkling wine production creates revenue streams beyond traditional sales, including tasting fees, accommodation, and merchandise. Consumer behavior shifts toward local experiences and authentic connections drive this growth, with virtual tastings becoming a permanent component of winery business models. The economic multiplier effect is significant in regions like the Peloponnese, Greece, where wine tourism supports numerous wineries and strengthens regional competitiveness through cooperative marketing initiatives.

Sustainability and Eco-Friendly Production Practices

Environmental consciousness has become a driving force in shaping consumer purchasing patterns, as customers increasingly prioritize sustainability practices when making buying decisions. The transition to sustainable production methods demands considerable initial financial investment but yields substantial returns through reduced material expenses and enhanced operational performance. California wineries that have obtained sustainable certifications consistently demonstrate that the financial advantages outweigh the costs of implementation, especially for established operations that can capitalize on their scale advantages. This strategic alignment between environmental stewardship and business operations in the wine industry generates value for both stakeholders and the environment while responding to evolving consumer preferences.

Popularity of Italian and Spanish Sparkling Wines

Italian sparkling wine exports continue to demonstrate remarkable market strength, with Prosecco emerging as the clear leader in EU sparkling wine exports. Holding a substantial 44% of total export volume in 2023, Prosecco significantly outperforms Champagne's 15% market share [1]Source: Eurostat, “Sparkling Wine Production and Exports,” ec.europa.eu. This success can be attributed to Prosecco's strategic market positioning as an accessible premium beverage, offering consumers the quality associated with traditional winemaking methods at price points that remain attractive to younger consumers. The Spanish sparkling wine market has undergone notable transformation, evolving into distinct classifications such as Conca del Riu Anoia and Corpinnat. This segmentation reflects a deliberate strategy by Spanish producers to establish unique market identities through emphasis on regional characteristics and elevated quality standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variability in raw material quality | -0.9% | Global, with particular impact in climate-sensitive regions | Short term (≤ 2 years) |

| Stricter labeling and health warning regulations | -0.6% | EU, North America, expanding globally | Medium term (2-4 years) |

| High costs of sustainable production | -0.4% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Supply chain disruptions and logistics challenges | -0.8% | Global, with particular impact on export-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Variability in Raw Material Quality

Climate variations, particularly unpredictable temperature patterns and irregular rainfall, continue to create significant operational challenges for wine producers, especially those focused on sparkling wine production where maintaining precise acidity and sugar levels is fundamental to product quality. The industry has observed that rising temperatures interfere with the natural relationship between sugar and anthocyanin development in grapes, which directly impacts the final wine quality and requires producers to implement advanced technical solutions to maintain their product standards. The inconsistency in grape ripeness during harvest periods has become a critical concern, as it substantially influences both the chemical properties and taste characteristics of the wine, with irregular ripening patterns resulting in elevated acetic acid levels and notable differences in flavor profiles. In response to these challenges, wine producers are making strategic investments in various adaptation measures, including the introduction of climate-resilient grape varieties, implementation of sophisticated irrigation systems, and adoption of precision agriculture technologies. However, these necessary adaptations require substantial capital expenditure and specialized technical expertise, presenting additional business considerations for industry stakeholders.

Stricter Labeling and Health Warning Regulations

The European Union's December 2023 mandate has fundamentally transformed wine labeling requirements, introducing comprehensive obligations for detailed nutritional information, ingredient lists, and allergen declarations [2]Source: European Commission, “Rules for Wine Labeling,” agriculture.ec.europa.eu. This regulatory shift has substantially increased compliance costs across the industry. The US Surgeon General's January 2025 advisory highlighting the relationship between alcohol consumption and cancer risk signals potential requirements for mandatory cancer warning labels, which would further increase compliance obligations and could influence consumer purchasing decisions [3]Source: U.S. Department of Health and Human Services, “Alcohol and Cancer Risk,” hhs.gov. Small wine producers, operating with limited financial and operational resources, find themselves particularly vulnerable to these complex compliance requirements, potentially driving them toward consolidation with larger entities. The diverse regulatory requirements across different countries create significant operational challenges for international wine producers, who must manage multiple label versions and absorb increased administrative expenses to maintain market access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Prosecco Drives Growth Despite Champagne Dominance

Champagne holds a dominant 32.02% market share in 2025, supported by its established heritage and protected designation of origin status, which enables premium pricing globally. Prosecco is expected to grow at a 6.52% CAGR through 2031, as it offers an accessible premium option that resonates with younger consumers. This market dynamic shows how traditional premium products maintain their value while more affordable alternatives drive volume growth.

Cava is improving its market position through new quality tier regulations, while English sparkling wines and other New World varieties gain market share through production innovations and effective marketing. The impact of climate change presents both risks and opportunities across the industry, with champagne producers adapting their vineyard management practices while prosecco benefits from new viable growing areas. The integration of precision viticulture and AI in quality control processes helps maintain consistent product quality while reducing operational costs and environmental effects.

By Category: Premium Segment Dominates Growth Trajectory

Premium sparkling wine holds a 54.62% market share in 2025 and is projected to grow at a 6.58% CAGR through 2031, indicating consumers' preference for higher-quality products and established brands. This market position shows sparkling wine's evolution from an occasional celebratory drink to a regular consumption choice. The economy segment experiences declining demand as consumers shift toward premium options that offer perceived higher value. Producers focus on differentiation through heritage, sustainability practices, and marketing experiences to support premium pricing strategies.

Established producers with strong brand recognition and distribution capabilities maintain competitive advantages in the premium segment. For example, LVMH's champagne division demonstrates successful premium market positioning with four of its brands ranked among the top global wine and champagne brands. Research shows that experienced consumers evaluate product quality attributes, while newer consumers consider factors such as price and packaging, indicating distinct market approaches for different price segments. Premium sparkling wine consumption grows significantly in emerging markets, driven by increasing disposable income and changing consumption preferences.

By Packaging Type: Canned Innovation Challenges Traditional Bottles

The wine packaging market continues to be dominated by traditional bottles, which maintain a 67.55% market share in 2025. Consumers strongly associate glass bottles with quality and celebration. However, canned formats are experiencing significant growth, with a projected CAGR of 6.55% through 2031. This growth is primarily driven by millennials who value portability and sustainability in their purchasing decisions. The evolution in packaging reflects the changing consumer lifestyle, where people increasingly seek convenient, single-serving options for outdoor activities and casual consumption.

European markets are leading the transition to canned wine, with companies like Winestar and The Uncommon successfully targeting younger consumers who prioritize new experiences and environmental responsibility . The sustainability aspect of aluminum cans has become a key selling point, as they offer superior recyclability compared to glass bottles while reducing transportation costs and carbon footprint. The industry's commitment to sustainable packaging extends beyond cans to include innovations such as lightweight glass bottles, alternative closures, and eco-friendly materials that address environmental concerns while maintaining product integrity.

By Distribution Channel: Off-Trade Acceleration Reshapes Market Access

On-trade channels hold a 56.68% market share in 2025, as sparkling wine remains closely tied to celebrations and social gatherings in restaurants, bars, and hospitality venues. Off-trade channels are growing at a 6.70% CAGR through 2031, supported by the expansion of e-commerce and direct-to-consumer sales models that doubled during the pandemic. This shift in distribution channels reflects increased home consumption and wider adoption of digital purchasing.

Within off-trade channels, supermarkets and hypermarkets benefit from consumers seeking premium products for home entertaining. Online retail enables producers to establish direct relationships with consumers, improving profit margins and customer retention. Convenience stores are expanding their wine selections to serve impulse buyers and regular consumers, while online platforms provide access to specialty products and international brands not found in local stores. This evolution in distribution benefits producers with strong digital capabilities and direct-to-consumer operations, while traditional wholesalers and distributors must enhance their value through improved logistics and market access services.

Geography Analysis

Europe dominates the market with a 33.86% share in 2025, building on its established production regions and traditional sparkling wine consumption culture. However, market maturity in the region indicates slower growth potential as consumer preferences stabilize and competition intensifies.

The Asia-Pacific region demonstrates exceptional growth potential, achieving a 6.79% CAGR through 2031. This growth stems from increasing disposable incomes among consumers and a deepening appreciation for wine culture, particularly in emerging economies where westernization influences consumption patterns.

North America maintains steady market development through premium product demand and established distribution networks, while South America benefits from its domestic production capabilities. The Middle East and Africa present growth opportunities through their expanding expatriate communities and tourism-driven premium beverage consumption. Regional preferences vary significantly, with Asian markets favoring lighter, fruit-forward wines, while European consumers maintain their affinity for traditional production methods. This diversity enables producers to tailor their offerings while managing cross-market operational risks.

Competitive Landscape

The sparkling wine market's fragmented nature creates significant potential for industry consolidation and market share growth. Companies are taking different paths to success - LVMH focuses on building its luxury brand portfolio while preserving heritage, while Constellation Brands has moved away from mainstream brands to develop its premium offerings above USD 15. Following a similar strategic direction, Pernod Ricard's decision to divest wine assets in favor of spirits demonstrates the industry-wide shift toward higher-margin segments.

Technology has become a significant factor in transforming wine production methods and market dynamics. Wine producers increasingly implement AI-driven precision viticulture to optimize grape cultivation, automated production systems to ensure consistent quality, and digital marketing tools to build and maintain strong customer relationships. The growing emphasis on sustainability continues to reshape market preferences, with consumers demonstrating a clear willingness to invest in environmentally responsible wines. This shift in consumer behavior aligns with regulatory requirements for increased transparency in production processes, creating a more environmentally conscious wine industry.

The market presents several untapped opportunities, particularly in emerging regions, alternative packaging solutions, and direct-to-consumer sales channels. These areas remain relatively unexplored by established players, creating openings for new entrants to establish themselves through innovative approaches and digital-first business models.

Sparkling Wine Industry Leaders

LVMH Moët Hennessy Louis Vuitton SE

Henkell Freixenet

E. & J. Gallo Winery

Constellation Brands Inc.

Pernod Ricard S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Belle Glos has expanded its portfolio by introducing two new sparkling wine varieties - Blanc de Blanc and Sparkling Rosé. This strategic expansion demonstrates the winery's commitment to diversifying its offerings while maintaining its reputation for quality winemaking in the premium wine market.

- April 2025: Constellation Brands announced a comprehensive repositioning of its wine and spirits business, divesting mainstream brands including J. Rogét sparkling wine to focus exclusively on premium products priced USD 15 and above, with retained portfolio featuring Robert Mondavi Winery and Kim Crawford alongside craft spirits collection

- August 2024: Pernod Ricard sold its international wine portfolio to Australian Wine Holdco Limited for over USD 1 billion. The sale included the Jacob's Creek and Campo Viejo brands. This transaction allows Pernod Ricard to focus on its premium spirits and champagne business, while Australian Wine Holdco Limited expands its global wine operations.

Global Sparkling Wine Market Report Scope

| Champagne |

| Prosecco |

| Cava |

| Other Sparkling Wine |

| Economy |

| Premium |

| Canned |

| Bottle |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Champagne | |

| Prosecco | ||

| Cava | ||

| Other Sparkling Wine | ||

| By Category | Economy | |

| Premium | ||

| By Packaging Type | Canned | |

| Bottle | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the sparkling wine market?

The sparkling wine market size is USD 45.91 billion in 2026.

Which product type is growing fastest?

Prosecco is projected to record a 6.52% CAGR between 2026-2031.

Why are canned sparkling wines gaining popularity?

Cans offer portability, single-serve convenience, and a lower carbon footprint than glass.

How will new labeling regulations affect producers?

Mandatory nutrition and ingredient disclosures in the EU and proposed US “Alcohol Facts” panels will raise compliance costs, especially for small wineries.

Which region will lead future demand?

Asia-Pacific is forecast to deliver the fastest regional growth at a 6.79% CAGR through 2031.

Page last updated on: