Identity Resolution Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

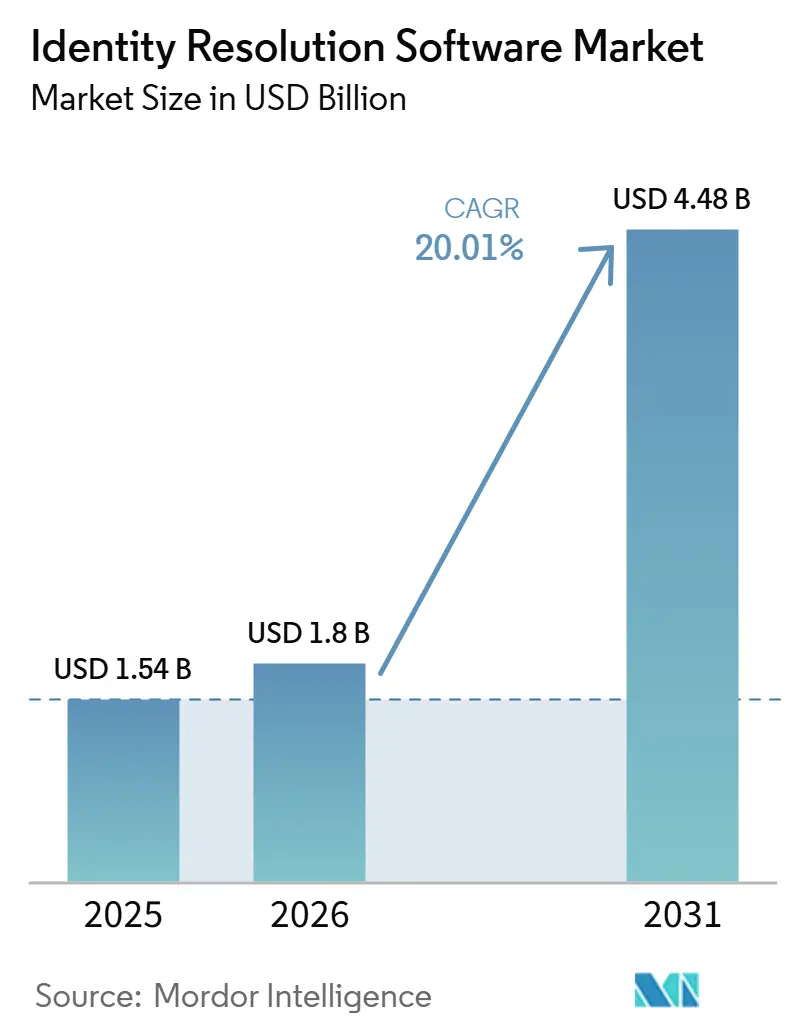

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 4.48 Billion |

| Growth Rate (2026 - 2031) | 20.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Identity Resolution Software Market Analysis by Mordor Intelligence

The identity resolution software market size was valued at USD 1.54 billion in 2025 and is forecast to reach USD 4.48 billion by 2031, growing at a CAGR of 20% from 2026 to 2031. The identity resolution software market is expanding as enterprises replace cookie-led targeting with first-party identity graphs that can support customer engagement across channels. The identity resolution software market is also benefiting from tighter privacy rules and the January 1, 2026, CCPA automated decision-making changes, which are pushing buyers toward deterministic and probabilistic matching systems that can work under stricter consent and governance requirements. The identity resolution software market is attracting interest from a broader set of decision-makers because AI agents, personalization tools, and next-best-action systems depend on accurate customer identity records to produce useful outputs. Competitive pressure is rising in the identity resolution software market as holding companies and platform providers fold identity capabilities into broader media, data, and AI stacks, highlighted by Publicis Groupe’s May 2026 agreement to acquire LiveRamp and its March 2025 acquisition of Lotame. The identity resolution software market still has room to expand through mid-market adoption, stronger interoperability, and privacy-safe activation models that enable enterprises to use identity data without relying on passive third-party collection.

Key Report Takeaways

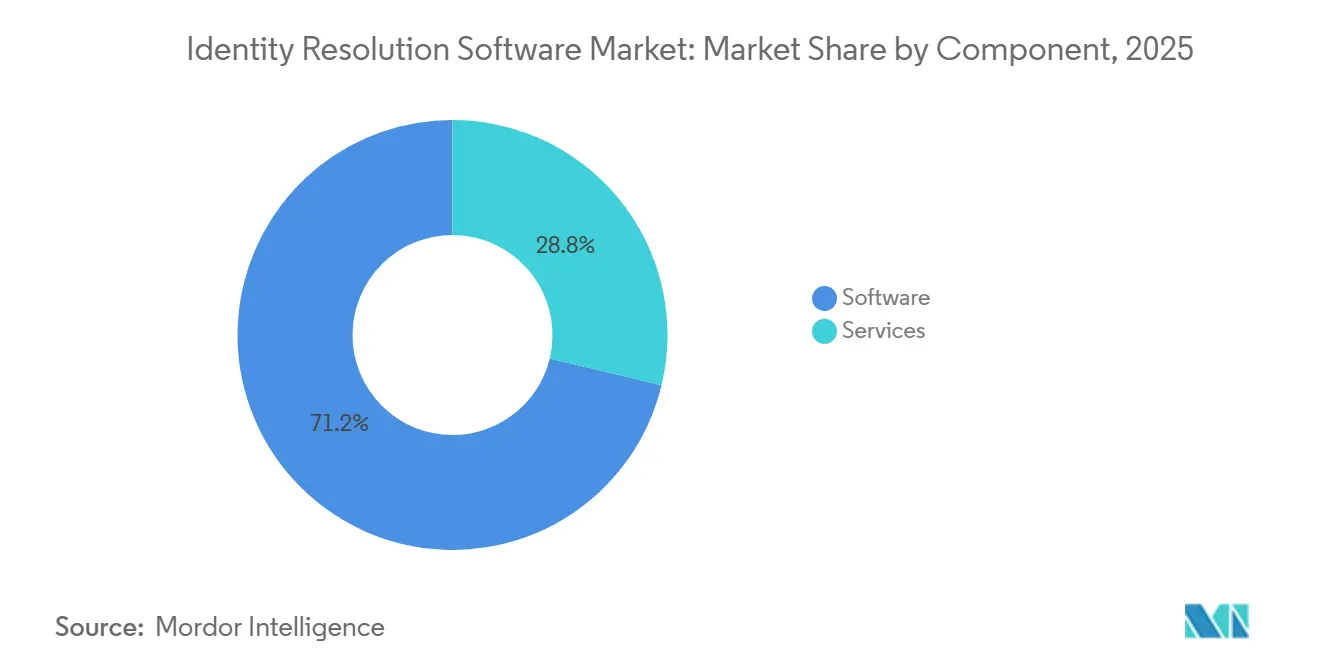

- By component, software held 71.24% of the identity resolution software market share in 2025, while services are projected to grow at a 22.83% CAGR through 2031.

- By deployment mode, cloud-based platforms accounted for 68.41% of the identity resolution software market size in 2025, while hybrid deployment is projected to expand at a 21.69% CAGR through 2031.

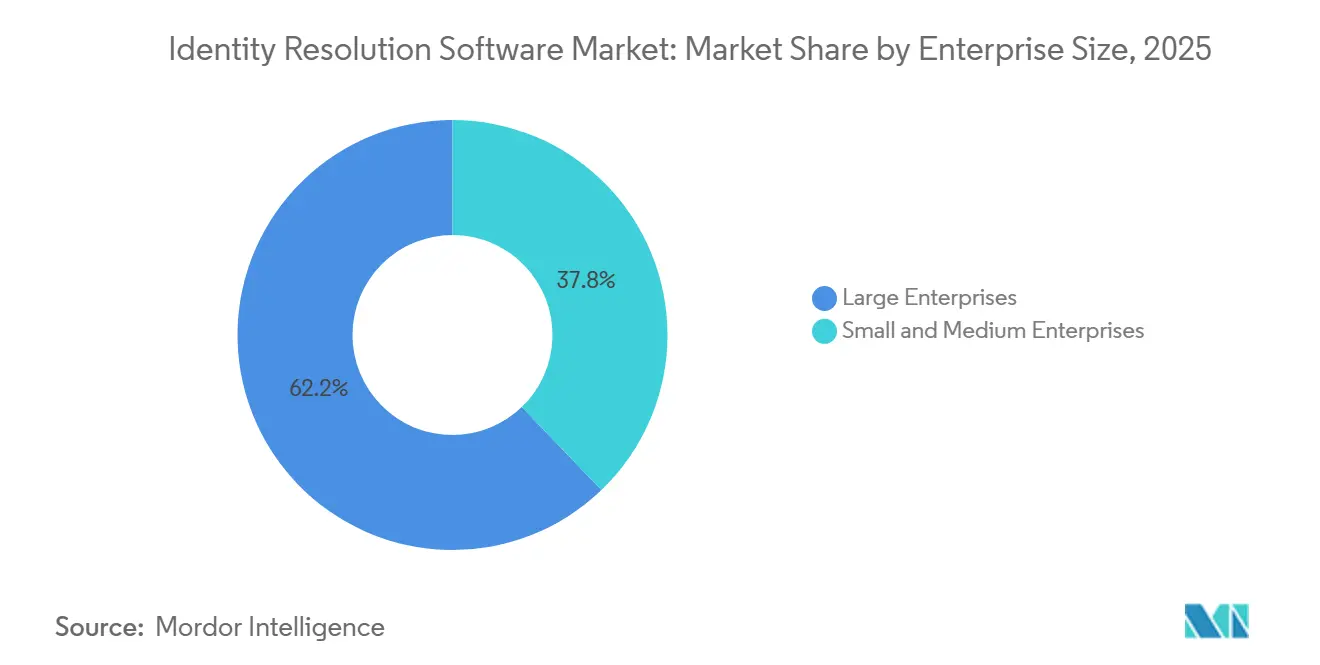

- By enterprise size, large enterprises held 62.18% revenue share in 2025, while small and medium enterprises are forecast to grow at a 23.74% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 24.86% revenue share in 2025, while healthcare and life sciences are expected to advance at a 21.42% CAGR through 2031.

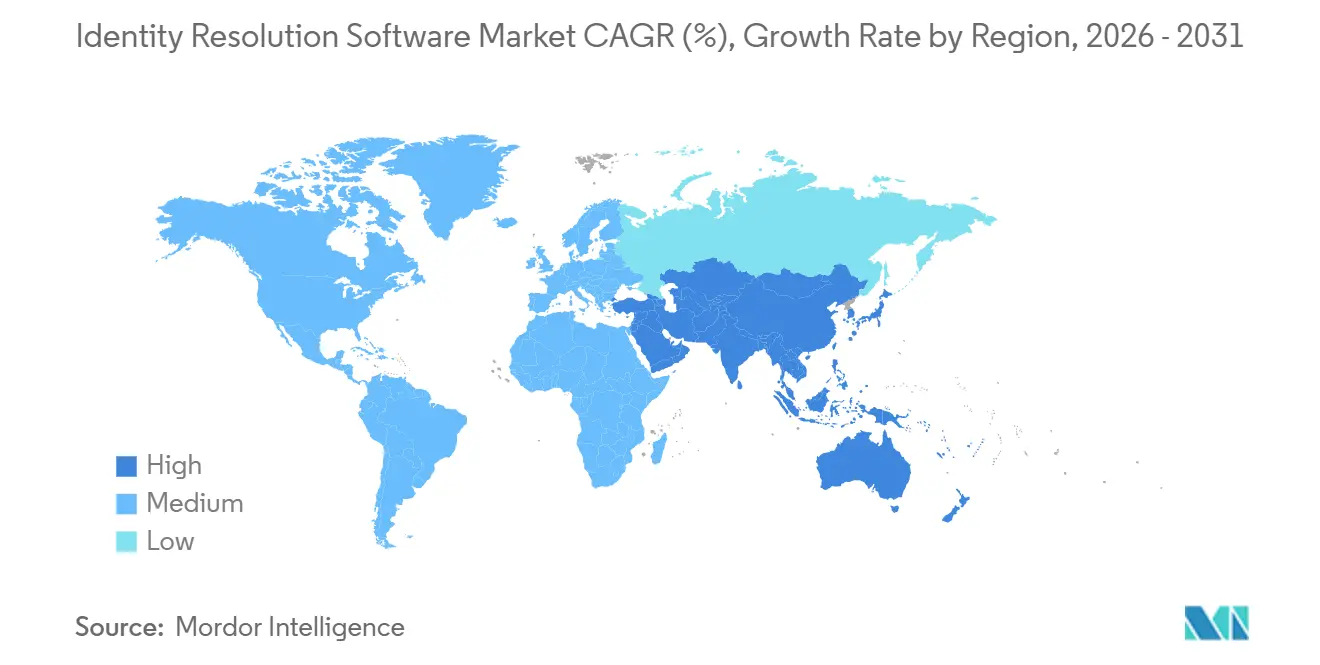

- By geography, North America accounted for 34.62% of revenue share in 2025, while Asia-Pacific recorded the highest projected CAGR of 24.19% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Identity Resolution Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cookieless digital advertising and first-party identity stitching | +4.8% | Global, with acute impact in North America and EU | Short term (≤ 2 years) |

| Unifying fragmented customer data across touchpoints | +3.5% | Global | Medium term (2-4 years) |

| Real-time personalization and next-best-action adoption | +3.2% | North America and EU, with rapid expansion into Asia-Pacific | Medium term (2-4 years) |

| Cross-device and cross-channel identity graph growth | +2.8% | Global | Long term (≥ 4 years) |

| Privacy-safe data collaboration and clean room workflow expansion | +2.1% | North America and EU | Medium term (2-4 years) |

| Fraud detection and duplicate record suppression use cases | +1.6% | BFSI-heavy markets, North America and core Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cookieless Digital Advertising Intensifies Demand for First-Party Identity Stitching

The identity resolution software market is seeing stronger demand as third-party cookies lose relevance across major browsers. Retail media networks now expect brands to match customer segments to deterministic identifiers rather than rely on third-party data brokers. That shift is moving more identity work into commerce and advertising infrastructure rather than leaving it with stand-alone tools. LiveRamp expanded RampID across Unity Exchange in April 2026, extending identity-based buying across 2.9 billion monthly active mobile devices globally and 256 million in the United States. The identity resolution software market is also being shaped by the need for sub-100 millisecond matching in programmatic environments, which is pushing vendors from batch processing toward streaming and edge-enabled architectures.

Rising Need to Unify Fragmented Customer Data Across Touchpoints

The identity resolution software market is benefiting from the growing burden of disconnected customer systems across CRM, loyalty, commerce, mobile, and offline channels. Many organizations still manage between 5 and 15 systems of record that assign different identifiers to the same person. Amperity’s April 2025 launch material, citing MIT Technology Review Insights, said 78% of global companies were not very ready to deploy AI agents, with disconnected and inaccurate customer data named as the main barrier. Identity resolution software addresses that issue by creating a persistent, privacy-safe identifier that supports a unified customer record across teams and applications. Amperity also said one large retailer uncovered 3.5 million previously unreachable customer email addresses after using its identity resolution capabilities, which shows why the identity resolution software market is gaining commercial support beyond marketing teams.[1]Amperity, “Amperity Unveils Industry’s First Identity Resolution Agent, Accelerating AI Readiness for Enterprise Brands,” Amperity, amperity.com

Enterprise Adoption of Real-Time Personalization and Next-Best-Action Engines

The identity resolution software market is moving toward real-time decisioning as enterprises seek to personalize offers while customers switch devices and channels. Buyers are moving away from overnight reconciliation and toward streaming architectures that can resolve a session within milliseconds. Oracle’s 2026 recognition in customer data platforms demonstrated that larger enterprise vendors are integrating identity resolution into broader CX environments, reducing integration friction for buyers.[2]Oracle, “Oracle Named a Leader in the 2026 Gartner Magic Quadrant for Customer Data Platforms,” Oracle, oracle.com TransUnion also expanded identity-led measurement on YouTube through its work with Google, extending real-time attribution into video environments where individual measurement had been harder to support. Amperity’s May 2026 update connected identity-resolved profiles to tools such as Microsoft Copilot, Braze AI, and Salesforce AgentForce, showing that the identity resolution software market is becoming part of the operating layer for agentic marketing workflows.[3]TransUnion, “TransUnion and Google Strengthen YouTube Measurement With Multi-Touch Attribution,” TransUnion Newsroom, newsroom.transunion.com

Growth of Identity Graphs for Cross-Device and Cross-Channel Resolution

The identity resolution software market is being shaped by identity graphs that now function as dynamic data structures rather than static lookup tables. These graphs map customer identifiers across devices, channels, and time periods, which increases their value as a long-term asset. Publicis acquired Lotame in March 2025 and added its 1.6 billion IDs, while WPP acquired InfoSum in April 2025 to strengthen access to privacy-safe cross-platform data.[4]WPP, “WPP Acquires InfoSum in Major Investment in Its AI-Driven Data Offer,” WPP, wpp.com TransUnion said joint customers processed billions of identity records on Snowflake within 12 months, indicating the scale now expected in cloud-native graph operations. The identity resolution software market is therefore moving toward cloud environments where embedded graphs can influence how pricing, data movement, and service delivery are structured.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy constraints on graph persistence and match rates | -4.2% | Global, with acute intensity in EU, US, and India | Long term (≥ 4 years) |

| Integration complexity across CRM, CDP, and ad tech stacks | -2.8% | Global | Medium term (2-4 years) |

| Poor legacy data quality and weaker resolution accuracy | -2.1% | North America and Europe | Medium term (2-4 years) |

| Dependency on third-party data and consent coverage | -1.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy Constraints Limit Graph Persistence and Match Rates

The identity resolution software market faces a structural limit because privacy regulations can reduce the amount of personal data available for matching and activation. Enterprises now have to delete, correct, or exclude data when consumers exercise those rights, which weakens graph persistence over time. California’s updated CCPA framework took effect on January 1, 2026, and added rules on automated decision-making, cybersecurity audits, and risk assessments. Those requirements raise the cost of building and maintaining large identity graphs and increase buyer focus on consent governance, audit readiness, and privacy-by-design controls. The identity resolution software market must therefore balance accuracy, scale, and lawful activation more carefully than it did when passive tracking was subject to fewer restrictions.

Integration Complexity Across CRM, CDP, and Ad Tech Stacks

The identity resolution software market is also constrained by the complexity of fitting new tools into fragmented enterprise stacks. A typical buyer may have a CRM platform, at least 1 CDP, a data warehouse, and several activation systems, each with different schemas, APIs, and latency needs. That makes identity reconciliation difficult without custom middleware, especially for mid-market organizations with limited internal engineering capacity. Acxiom addressed this problem in June 2026 by embedding Real ID into Databricks, so enterprises could work where their data already resides rather than moving it to an external service. IBM Consulting also expanded its Microsoft Security collaboration in June 2026, underscoring that the identity resolution software market now must account for multi-cloud tracing, remediation, and governance alongside core matching performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Software held a 71.24% revenue share in 2025, giving it the lead in the identity resolution software market and reflecting buyer preference for platform deployment over project-led engagement. Subscription pricing has supported that position because it gives enterprises more predictable spending patterns. Cloud-native software has also gained favor because it integrates more quickly with data lakes, CDPs, and activation platforms already used across the business. The identity resolution software market continues to reward platforms that can maintain auditable and consent-governed records for AI-driven use cases. Acxiom’s enhanced Real ID presence in Databricks and its role in the Databricks CustomerLake agentic CDP showed how software vendors are extending revenue potential through deeper platform integration.

Services are the fastest-growing component of the identity resolution software market and are projected to expand at a 22.83% CAGR through 2031. That pace reflects the implementation burden tied to graph design, probabilistic tuning, and consent framework setup. Many enterprises still need outside help to connect multiple clouds, business units, and jurisdictions into a usable identity layer. Managed services are gaining traction among healthcare and financial services users who need stronger oversight of data lineage, access controls, and audit trails. The faster growth of services does not weaken the software case; instead, it shows that the identity resolution software market is becoming more complex as deployments move from stand-alone matching to governed enterprise infrastructure.

By Deployment Mode: Cloud-Based Platforms Anchor Demand While Hybrid Gains Ground

Cloud-based deployment accounted for 68.41% of revenue in 2025, which made it the largest configuration in the identity resolution software market. Adoption has been strongest among digital-native retailers, media companies, and technology firms that already run cloud-first data environments. Cloud delivery supports real-time API access, which is critical for programmatic advertising and on-site personalization, where response times are tightly constrained. It also provides enterprises with elastic capacity during peak shopping periods, when identity queries can rise rapidly. LiveRamp’s March 2026 platform release extended native identity resolution across Snowflake and AWS, reinforcing the alignment of the identity resolution software market with in-environment graph management.

Hybrid deployment is projected to grow at a 21.69% CAGR through 2031 in the identity resolution software market. This model is gaining ground among regulated users who want to keep sensitive records in private environments while still using cloud links for lookup, enrichment, and activation. BFSI and healthcare buyers are particularly aligned with that approach because it helps them address residency and sovereignty requirements without giving up response speed. On-premise deployment still matters in legacy estates where external data transfer remains restricted by policy. Even so, the identity resolution software market is gradually shifting toward hybrid, cloud-based models as embedded cloud controls reduce the historical trade-off between control and flexibility.

By Enterprise Size: Large Enterprises Drive Baseline Revenue as SMEs Accelerate

Large enterprises accounted for 62.18% of revenue in 2025, which kept them at the center of the identity resolution software market. Their scale makes identity resolution a core operating need because they manage very large customer files across countries, languages, and business units. These buyers adopted earlier than most of the market and now focus less on tool availability and more on graph precision, latency, and governance. Oracle’s 2026 positioning in customer data platforms showed how large accounts increasingly buy identity functions as part of wider CX and enterprise suites. That pattern keeps the identity resolution software market closely tied to broader platform strategy in the upper end of demand.

Small and medium enterprises are the fastest-growing segment and are expected to expand at a 23.74% CAGR through 2031 in the identity resolution software market. Subscription pricing and cloud delivery have lowered the entry barrier from large infrastructure projects to manageable recurring software spend. That has made identity resolution more practical for firms without large data engineering teams. These buyers are using the software to improve marketing accuracy, reduce duplicate records, and connect growing sets of customer data across commerce and service channels. The identity resolution software market has a clear opening here, as many mid-market organizations are moving from basic CRM environments to more comprehensive data platforms and need an identity layer to enable those systems to work together.

By End-User Industry: Retail Anchors Demand, Healthcare Drives Growth Acceleration

Retail and e-commerce accounted for 24.86% of revenue in 2025, making it the largest end-user segment in the identity resolution software market. The driver is the number of identifiers a single customer creates as they move between apps, browsers, stores, returns, and loyalty programs. Retailers need those signals stitched into one profile if they want CRM, personalization, and measurement systems to work properly. Retail media networks have added another use case because they depend on reliable matching between advertiser files and retailer shopper profiles. That combination keeps the identity resolution software market closely linked to digital commerce and first-party monetization strategies.

The healthcare and life sciences industry is projected to grow at a 21.42% CAGR in the identity resolution software market through 2031. Growth is coming from both patient and consumer identity resolution, tied to digital health engagement. Hospitals and integrated systems use enterprise master person index tools to reduce duplicate records, billing errors, care gaps, and medication risks. Digital health businesses are also adopting identity resolution to support more personalized outreach while working within HIPAA-related limits on third-party data use. BFSI, IT and telecom, media and entertainment, industrial manufacturing, and government and public administration also contribute to the identity resolution software market through use cases such as KYC, fraud control, and benefits administration.

Geography Analysis

North America accounted for 34.62% of revenue in 2025, giving it the lead in the identity resolution software market and the largest regional market share. The region benefits from high enterprise software spending, deep advertising technology infrastructure, and a regulatory setting that weakens traditional tracking while increasing demand for compliant first-party identity tools. U.S. buyers also have access to established bureau and platform providers with large deterministic identity assets, which support faster adoption across marketing, analytics, and activation use cases. Canada and Mexico are also contributing to the identity resolution software market, as privacy modernization and data governance requirements drive greater demand for auditable matching systems.

Germany, the United Kingdom, and France represented the largest country markets in Europe for identity resolution software. Demand in the region remains centered on BFSI, retail, and media and entertainment, where firms must match data across channels while operating under tighter privacy expectations. Experian launched Identity Connect in the United Kingdom in July 2026, combining biometric verification, document checks, fraud intelligence, and bureau data through a single API in a compliance-led product design. South America is smaller, but Brazil and Argentina are adding demand to the identity resolution software market as financial data interoperability expands and consent-linked data use becomes more important.

Asia-Pacific is the fastest-growing region in the identity resolution software market and is projected to expand at a 24.19% CAGR through 2031, making it the strongest regional contributor to market growth. Mobile-first commerce and digital service growth are increasing the need for real-time identity matching across the region. China continues to support demand through broad real-name verification requirements across finance, telecom, e-commerce, and social platforms. Japan and South Korea are also raising the need for consent-governed identity systems through ongoing privacy and data governance changes. Trulioo reported 51% year-over-year growth in Asia-Pacific business verification volume in 2025, which signals the pace of identity-related adoption across the region. The Middle East and Africa remain smaller, but the identity resolution software market is gaining support there as the UAE and Saudi Arabia move ahead with national digital identity frameworks that will require compatible enterprise infrastructure.

Competitive Landscape

The identity resolution software market is moderately concentrated at the top and fragmented across the broader field. Credit bureau incumbents such as Experian, TransUnion, and Equifax compete with cloud-integrated vendors such as Oracle, Salesforce, Adobe, and SAP, as well as pure-play specialists including LiveRamp, Amperity, Acxiom, and Neustar. The main strategic divide in the identity resolution software market is between neutral identity graph operators and vendors that embed identity resolution inside a wider cloud or CX stack. Publicis Groupe’s agreement to acquire LiveRamp in May 2026 sharpened that divide by raising questions about how open a large, neutral identity network can remain once it sits within a broader media and data platform.

The identity resolution software market is also being reshaped by platform delivery models that reduce data movement and push identity functions closer to enterprise storage and compute layers. Acxiom’s June 2026 Databricks integration is a clear example because it made Real ID available as a native application inside the customer’s existing environment. Amperity’s Identity Resolution Agent launch in April 2025 and its May 2026 Model Context Protocol update showed another route to differentiation through AI-ready profile unification and governed connectivity to external tools. Oracle’s position in customer data platforms and Microsoft’s recognition in workforce identity security show that larger enterprise vendors are extending identity capabilities across adjacent categories. As a result, the identity resolution software market is no longer defined only by marketing use cases; it is increasingly tied to broader enterprise governance, security, and AI orchestration priorities.

There is still clear room in the identity resolution software market for vendors that can serve regulated buyers with strong precision, consent controls, and auditability. Healthcare, BFSI, and government users often need capabilities that general-purpose marketing tools do not prioritize. IBM Consulting’s June 2026 identity threat detection and remediation expansion with Microsoft Security showed that identity governance and remediation are becoming part of the broader competitive landscape. The identity resolution software market is therefore likely to remain active in partnerships, platform integrations, and selective consolidation as vendors compete on interoperability, privacy compliance, and graph utility.

Identity Resolution Software Industry Leaders

LiveRamp Holdings, Inc.

Experian plc

TransUnion LLC

Acxiom Holdings, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Experian launched Identity Connect, a new digital customer verification solution combining biometric verification, document checks, fraud intelligence, and bureau data through a single API. The product makes Experian the only Credit Reference Agency certified against the UK’s Digital Verification Services Trust Framework, positioning it for compliance-driven enterprise procurement under the UK’s evolving digital identity regulatory framework

- June 2026: Acxiom enhanced Real ID to deliver cloud-native identity resolution and interoperability across marketing and advertising technology, embedding identity management directly into brands’ own environments without data movement. The enhancement enables brands to own their customer identity graph as a proprietary asset, reducing reliance on third-party data intermediaries and maintaining resolution accuracy across online and offline data

- June 2026: Acxiom made Real ID available as a native Built-On application in Databricks and as a launch partner for the Databricks CustomerLake agentic CDP. The integration provides enterprise marketers access to Acxiom’s global identity graph of over 260 million addressable U.S. individuals directly within the Databricks environment, enabling identity resolution, data enrichment, and audience activation without PII movement

- June 2026: IBM Consulting extended its collaboration with Microsoft Security to deliver identity threat detection and remediation services at enterprise scale. The service adds identity-specific case management, AI-driven remediation recommendations, governed remediation workflows, and managed delivery aligned to NIST, ISO, SOC 2, and GDPR compliance frameworks

Global Identity Resolution Software Market Report Scope

The identity resolution software market refers to the ecosystem of software solutions and associated services designed to connect fragmented customer data across multiple devices, channels, and touchpoints to create a unified, persistent, and accurate customer profile. These platforms utilize advanced algorithms, including deterministic (data-based) and probabilistic (statistical) matching, to link disparate identifiers such as email addresses, cookies, mobile device IDs, and social media profiles. Deployed across cloud-based, on-premise, and hybrid environments, these tools cater to organizations of varying sizes across industries such as retail, BFSI, healthcare, and media. By enabling a holistic view of the customer journey, identity resolution software helps businesses enhance marketing personalization, improve audience targeting, ensure data privacy and regulatory compliance, and maximize overall return on investment by reducing duplicate records and minimizing wasted ad spend.

The Identity Resolution Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small And Medium Enterprises |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium Enterprises | |||

| By End-User Industry | Retail and E-Commerce | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Media and Entertainment | |||

| Industrial Manufacturing | |||

| Government and Public Administration | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2031 revenue outlook for identity resolution software?

The identity resolution software market is forecast to reach USD 4.48 billion by 2031, up from USD 1.54 billion in 2025, with a 20% CAGR over 2026 to 2031.

Why are enterprises investing more in identity resolution platforms?

Spending is rising because firms need first-party identity graphs, better customer data unification, and real-time support for personalization and AI-driven decisioning.

Which deployment model leads current demand?

Cloud-based deployment led with 68.41% of revenue in 2025 because it supports real-time API access, elastic scaling, and easier integration with modern data environments.

Which buyer group is expanding the fastest?

Small and medium enterprises are projected to grow at a 23.74% CAGR through 2031 as subscription pricing and cloud delivery lower adoption barriers.

Which end-user segment currently leads revenue?

Retail and e-commerce led with 24.86% revenue share in 2025 because omnichannel shopping and retail media both depend on accurate cross-channel identity matching.

Which region offers the fastest expansion opportunity?

Asia-Pacific is projected to grow at a 24.19% CAGR through 2031, supported by mobile-first commerce growth and rising demand for consent-governed identity systems.

Page last updated on: