IAM Security Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

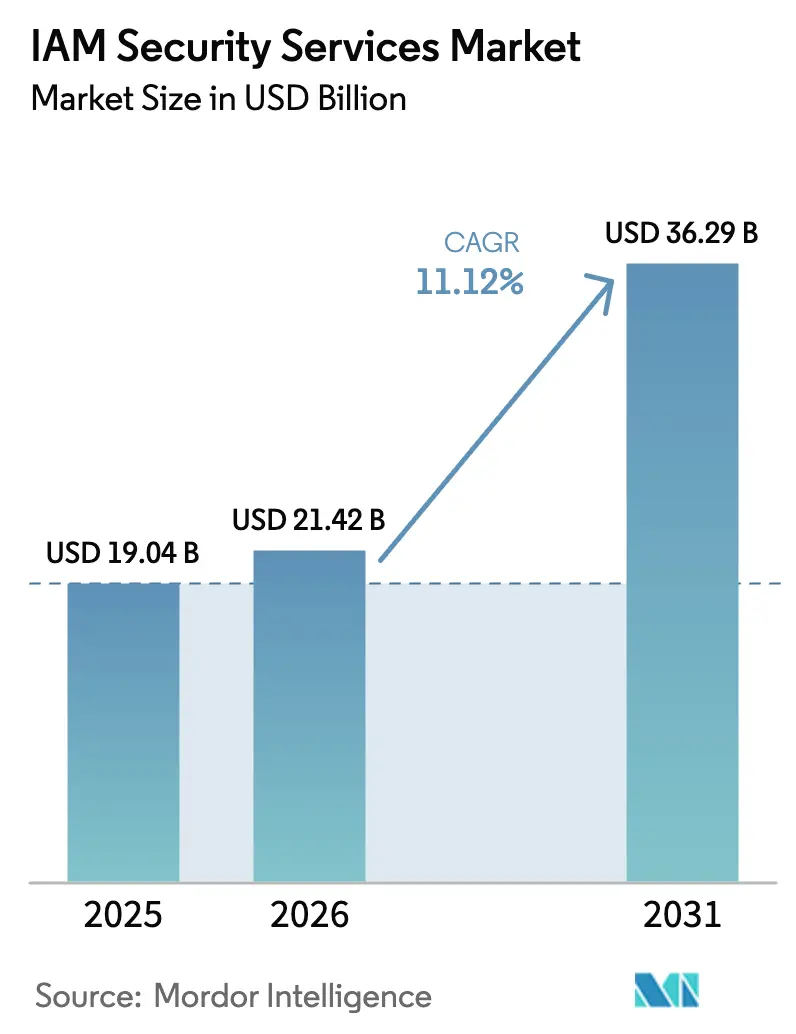

| Market Size (2026) | USD 21.42 Billion |

| Market Size (2031) | USD 36.29 Billion |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

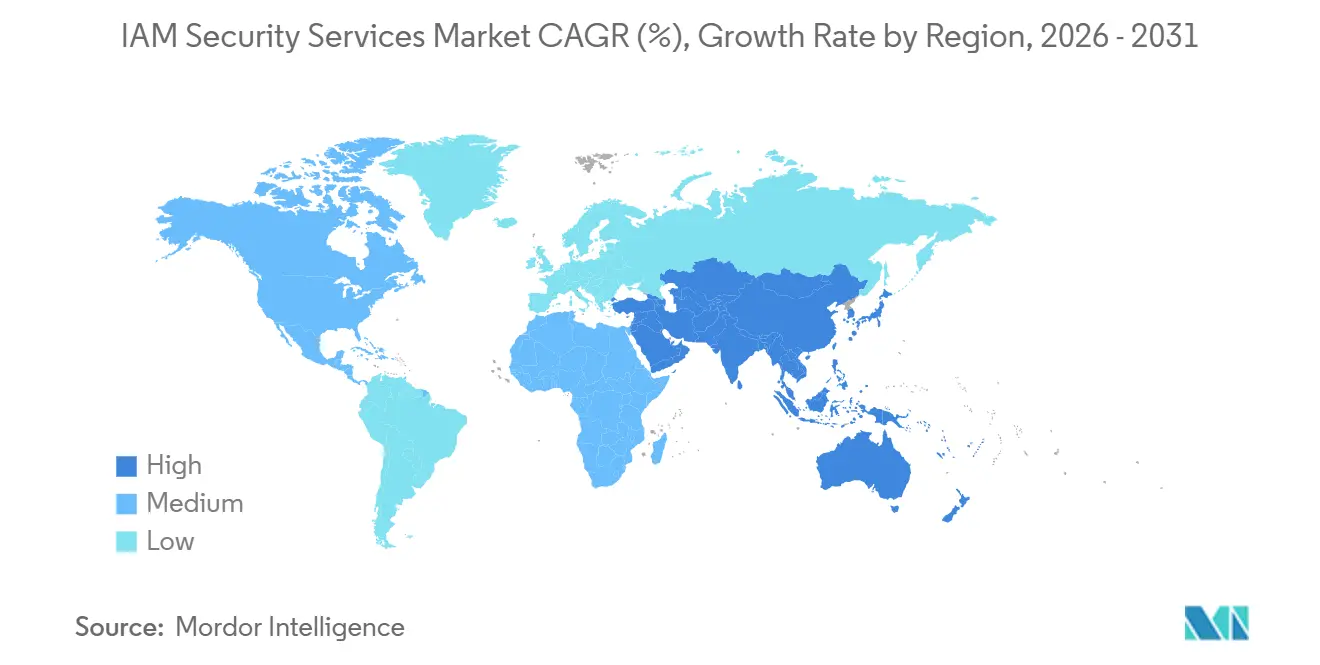

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

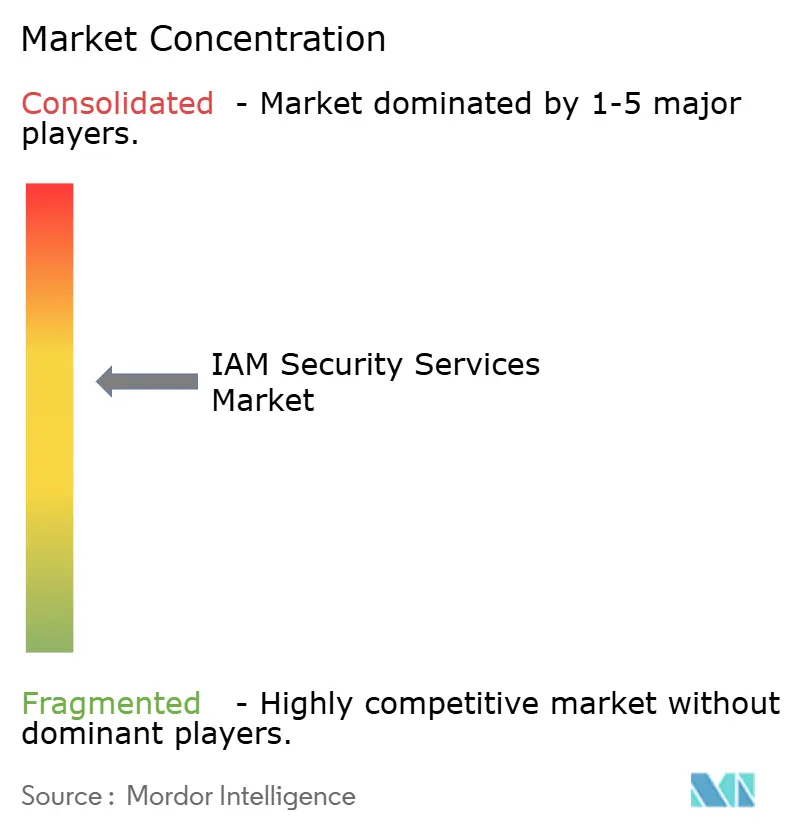

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IAM Security Services Market Analysis by Mordor Intelligence

The IAM Security Services Market size was valued at USD 19.04 billion in 2025 and is estimated to grow from USD 21.42 billion in 2026 to reach USD 36.29 billion by 2031, at a CAGR of 11.12% during the forecast period (2026-2031).

This momentum reflects an upsurge in credential-stealing campaigns, tighter statutes that now cover machine identities, and the mainstreaming of Zero Trust frameworks that interrogate every request. Machine identities already outnumber human identities by ratios as high as 45:1 in containerized clouds, adding layers of authentication complexity. Heightened ransomware losses, with the global average breach cost climbing to USD 4.88 million in 2024, further pressure boards to prioritize identity-centric defenses. Vendors are responding with unified SaaS suites that merge single sign-on, phishing-resistant multi-factor authentication, and adaptive analytics, while regulators codify real-time reporting mandates that impose four-hour notification windows on critical sectors.

Key Report Takeaways

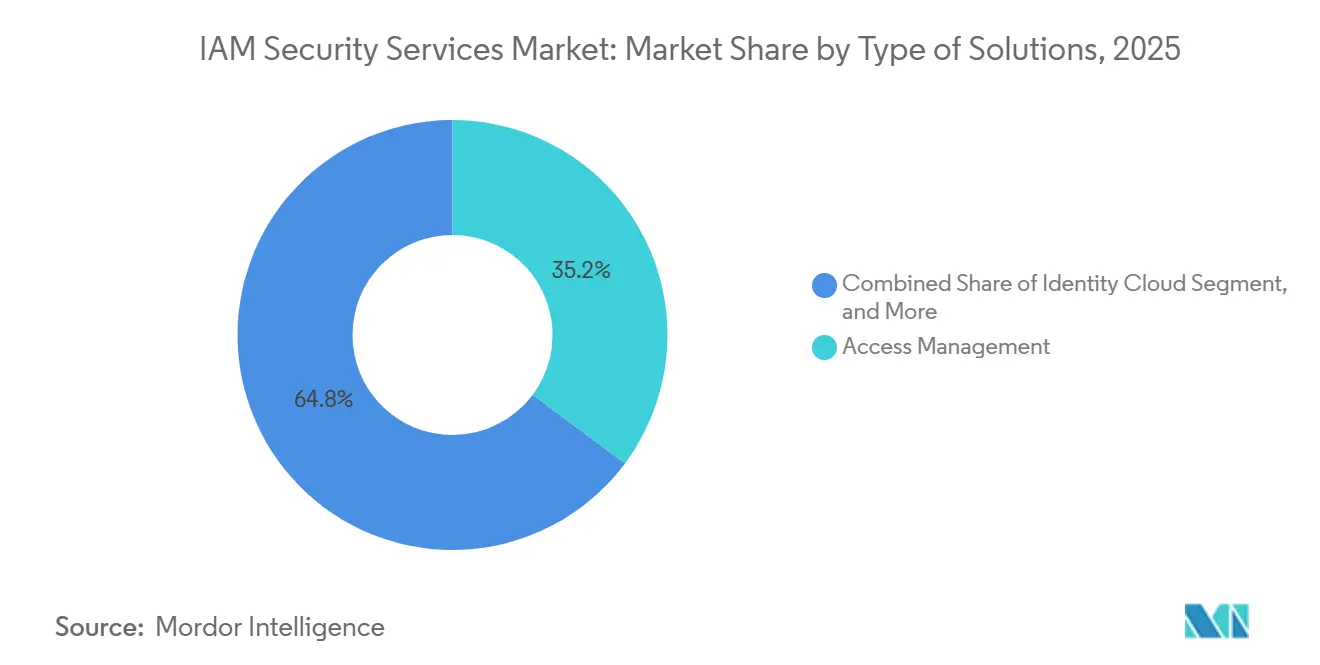

- By solution type, Access Management held 35.19% revenue share in 2025, whereas Identity Cloud is projected to grow at an 11.86% CAGR through 2031.

- By service type, Professional Services captured a 54.28% share in 2025, while Managed Services is expected to record a 12.01% CAGR to 2031.

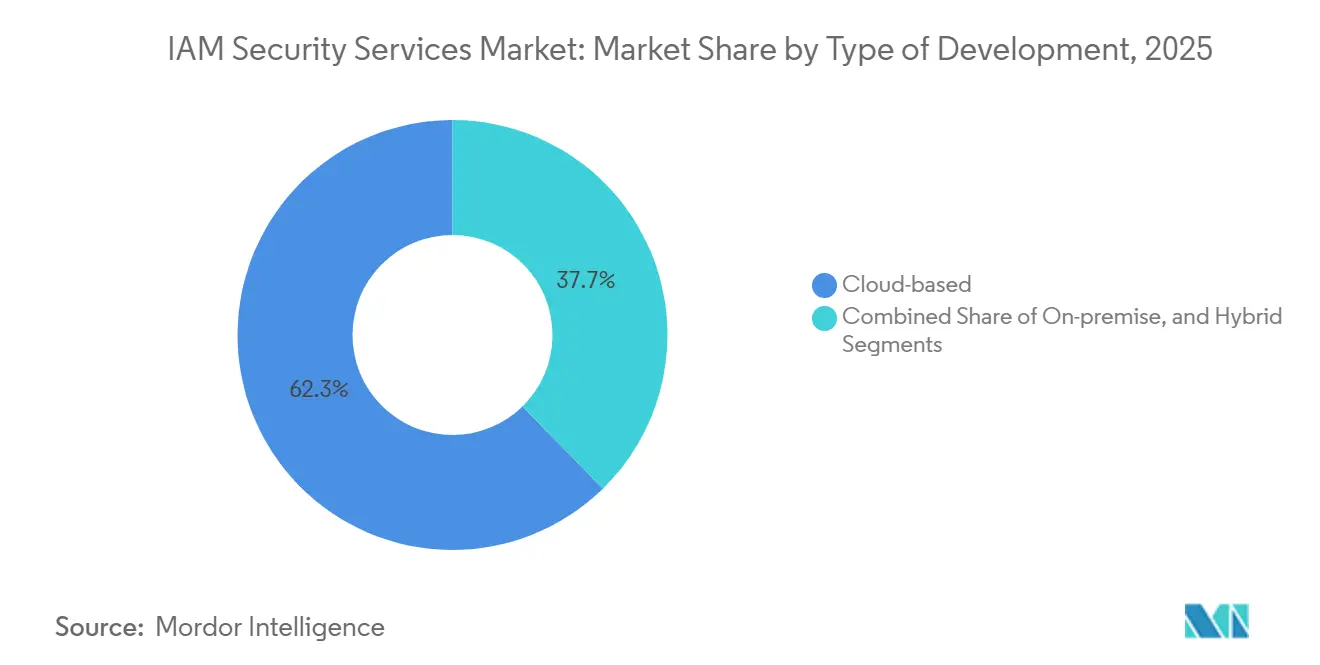

- By deployment, cloud-based models accounted for 62.33% of the IAM Security Services market share in 2025 and are forecast to expand at an 11.94% CAGR.

- By organization size, Large Enterprises generated 72.58% of 2025 spending, yet Small and Medium Enterprises should advance at a 12.15% CAGR.

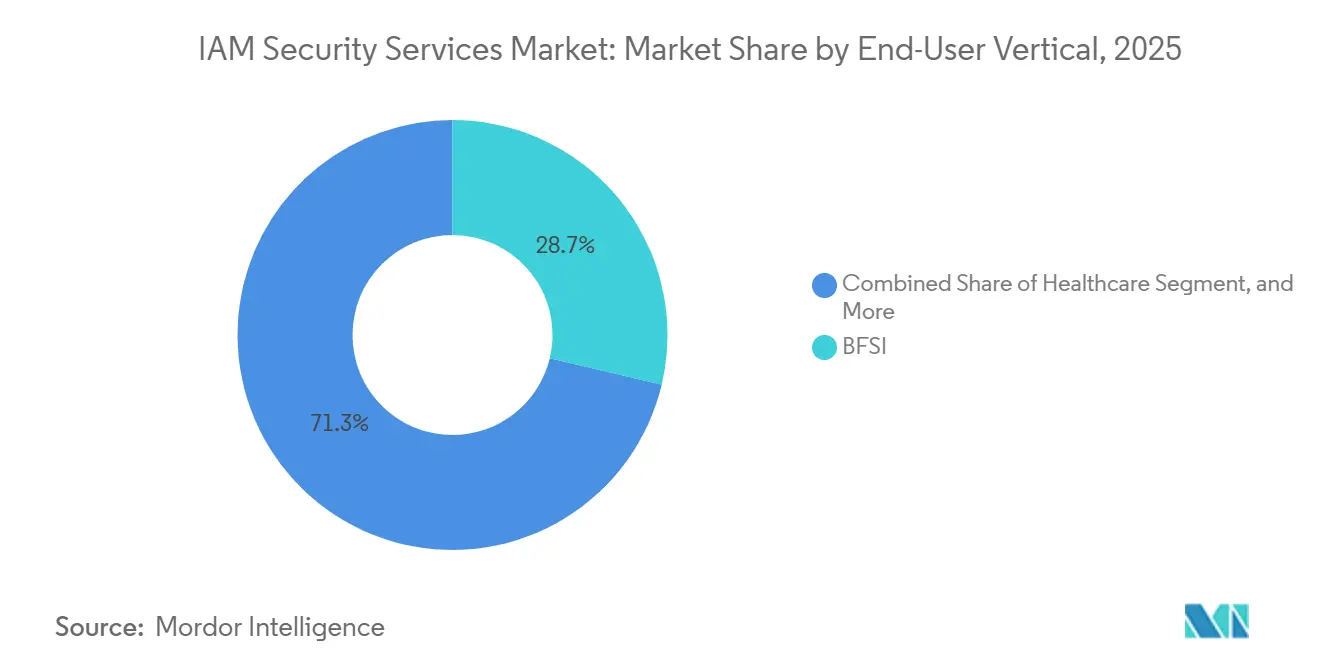

- By end-user vertical, BFSI led with 28.72% revenue share in 2025, whereas Healthcare is anticipated to grow at a 12.22% CAGR.

- By geography, North America dominated with 43.77% share in 2025, but Asia Pacific is set to climb at a 12.67% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IAM Security Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cybersecurity Threats and Data Breaches | +2.30% | Global, with acute exposure in North America and Europe | Short term (≤ 2 years) |

| Stringent Regulatory Compliance Mandates | +2.10% | Europe and North America lead; APAC accelerating under DPDP Act and MLPS 2.0 | Medium term (2-4 years) |

| Rapid Shift to Cloud and Hybrid Work Models | +1.90% | Global, with highest cloud adoption in North America and Western Europe | Medium term (2-4 years) |

| Transition Toward Zero Trust Architectures | +1.70% | North America and Europe early adopters; APAC and MEA following | Long term (≥ 4 years) |

| Explosion of Machine Identities and AI Agents | +1.50% | Global, concentrated in cloud-native enterprises and DevOps-heavy sectors | Long term (≥ 4 years) |

| Emergence of Passwordless Authentication via FIDO2 Passkeys | +1.20% | North America and Europe lead; Asia Pacific adoption rising | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cybersecurity Threats and Data Breaches

Phishing kits that automate adversary-in-the-middle attacks now bypass SMS one-time codes in real time, eroding trust in legacy factors. The United States Cybersecurity and Infrastructure Security Agency requires all federal bodies to move to phishing-resistant factors by fiscal year 2024, endorsing FIDO2 tokens and biometrics.[1]“Implementing Phishing-Resistant MFA,” CISA, cisa.gov Firms are deploying adaptive engines that interrogate device posture, geolocation, and behavioural cues, shrinking lateral movement when intrusions occur. With breach costs nearing USD 4.9 million, boards allocate larger security budgets toward identity perimeters that reduce dwell time. These investments push the IAM Security Services market toward platform bundles that fuse authentication with real-time analytics.

Stringent Regulatory Compliance Mandates

The European Union’s Digital Operational Resilience Act enforces four-hour incident alerts, forcing banks to build live identity analytics that knit privileged user activity to system anomalies.[2]“Digital Operational Resilience Act,” European Commission, europa.eu Parallel directives under HIPAA logged 725 healthcare breaches in 2024, prompting new U.S. guidance on automated de-provisioning. India’s Digital Personal Data Protection Act and China’s Multi-Level Protection Scheme 2.0 add stringent consent, audit, and localization rules, standardizing a baseline of least-privilege and immutable logging across multinationals. Compliance complexity raises operational costs but simultaneously cements IAM as a non-negotiable spend, enlarging the IAM Security Services market footprint.

Rapid Shift to Cloud and Hybrid Work Models

Cloud deployments already hold 62.33% share and scale with hybrid workers, 38% of whom connect remotely more than half the time. Identity-as-a-service platforms offload directory upkeep, with per-user pricing like Microsoft Entra at USD 12 monthly easing capital outlays.[3]“Microsoft Entra Pricing,” Microsoft, microsoft.com Yet token replay threats, made infamous in the SolarWinds supply-chain attack, expose weaknesses in long-lived SAML assertions. Continuous access evaluation, now embedded in leading suites, recalculates risk on every API call and keeps the IAM Security Services market in iterative innovation cycles.

Transition Toward Zero Trust Architectures

OMB Memorandum M-22-09 obliges all United States agencies to achieve Zero Trust milestones, including enterprise single sign-on and encrypted DNS, by 2024.[4]“Memorandum M-22-09,” Office of Management and Budget, whitehouse.gov Private-sector suppliers mirror these blueprints to ease audits, propelling adoption beyond government. Google’s BeyondCorp blueprint demonstrates how context-aware proxies replace VPN edges, shifting trust to user and device claims. Legacy workloads lacking APIs require identity-aware gateways, generating a services tailwind for integrators within the IAM Security Services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Maintenance Costs | -1.40% | Global, with acute pressure on SMEs in price-sensitive markets | Short term (≤ 2 years) |

| Legacy System Integration Complexity | -1.10% | North America and Europe, where aging infrastructure predominates | Medium term (2-4 years) |

| Shortage of Skilled IAM Professionals | -0.90% | Global, with severe shortages in APAC and emerging markets | Long term (≥ 4 years) |

| Unclear Pricing Models for Machine Identities | -0.60% | Global, concentrated in cloud-native and DevOps-heavy sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Solutions: Cloud Platforms Overtake On-Premises Directories

Identity Cloud offerings, projected to post an 11.86% CAGR through 2031, outstrip the broader IAM Security Services market as enterprises retire on-premises forests. Access Management previously commanded the largest slice at 35.19% in 2025, underscoring its role as the gateway for single sign-on and phishing-resistant factors. Continuous alignment with CISA standards keeps hardware-backed MFA at the center of modernization programs. The segment’s dominance anchors USD 7.5 billion of the 2026 IAM Security Services market size, illustrating its foundational pull within procurement blueprints.

Directory Services is trending downward as SaaS vendors expose RESTful endpoints that bypass LDAP queries. Conversely, machine identity sprawl drives demand for privileged access and certificate lifecycle tools housed in the “Other” solutions category. CyberArk’s purchase of Venafi extended coverage across human and non-human credentials, positioning platform bundles to manage 45:1 identity ratio. Identity Cloud further leverages pre-built connectors from Okta and Auth0, Inc. that shave integration cycles, making it the default for greenfield workloads and accelerating churn from legacy stacks across the IAM Security Services market.

By Service Type: Outsourcing Gains Ground Among Resource-Constrained Buyers

Professional Services absorbed 54.28% of 2025 revenue, mirroring the up-front consulting muscle needed to map entitlements and tune policies for complex estates. Yet a 12.01% CAGR propels Managed Services as mid-market firms offload 24/7 monitoring to external SOCs. For enterprises under 5,000 employees, managed fees undercut fully loaded internal analyst costs, shifting expenditure patterns toward consumption models. This pivot reshapes USD 11.3 billion of the 2031 IAM Security Services market size, adding predictable annuity streams for vendors.

Managed Detection and Response merges identity analytics with endpoint telemetry, creating a tighter loop that revokes anomalous sessions before exfiltration occurs. Professional consultancies remain indispensable for merger-driven identity consolidation among global conglomerates. Skills scarcity, with a 3.5-million-person cybersecurity gap in 2024, boosts both categories as organizations scramble for expertise. The tug-of-war between bespoke projects and turnkey outsourcing will shape competitive positioning within the IAM Security Services market.

By Type of Deployment: Elastic Economics Cement Cloud Preference

Cloud installations accounted for 62.33% of 2025 revenue and are forecast to compound at an 11.94% CAGR. The model decouples growth from data-center footprints, letting buyers scale seats moment-to-moment under usage-based tariffs. Hybrid deployments bridge mainframes and SaaS estates, synchronizing identities while teams refactor authentication code. On-premises clusters persist only where air-gapping is statutorily required, such as defense networks and critical infrastructure.

Federation risks remain the Achilles heel, as hijacked SAML certificates can impersonate administrators across linked apps. Continuous token inspection now runs server-side to slash replay windows from hours to seconds. These safeguards, bundled directly into SaaS plans, reinforce the IAM Security Services market share tilt toward cloud by marrying agility with risk-based controls.

By Organization Size: Tiered Pricing Democratizes Enterprise-Grade Controls

Large Enterprises represented 72.58% of 2025 outlays, yet Small and Medium Enterprises are set to expand at a 12.15% CAGR as vendors pare feature sets and ratchet down entry prices. Mid-market buyers embrace per-user SaaS tiers that eliminate six-figure setup fees, fuelling an incremental rise in IAM Security Services market adoption curves. Managed services overlay fills staffing gaps, enabling SMEs to access 24/7 identity-centric SOC coverage without maintaining in-house teams.

Fortune-level firms will still dominate dollar totals as they grapple with multi-forest consolidation after mergers, requiring deep professional engagements. However, democratization pressures spur vendors to design drag-and-drop policy editors and AI-driven entitlement recommendations that slash administrative overhead. Those usability gains propagate throughout the IAM Security Services market, lifting overall penetration rates.

By End-User Vertical: Healthcare Leads Growth While BFSI Retains Scale

Healthcare is projected to climb at a 12.22% CAGR, buoyed by 389 ransomware incidents that encrypted 41.8 million U.S. patient records in 2024. Heightened HIPAA oversight forces hospitals to harden privileged-access pathways, channelling incremental spend toward identity governance workflows. BFSI still holds the revenue crown at 28.72%, galvanized by Europe’s Digital Operational Resilience Act and parallel stress tests that insist on four-hour incident alerts.

IT and Telecom firms rely on IAM to wrangle exploding machine identities born from microservices and 5G edge nodes. Education leverages federated identity to streamline student access across learning platforms. Retailers converge customer identities across e-commerce, loyalty, and mobile channels to meet privacy regulations. Energy and Manufacturing adapt identity-aware proxies for operational technology gear that cannot speak modern protocols. Together, these dynamics diversify usage patterns, cementing vertical resilience in the IAM Security Services market.

Geography Analysis

North America generated 43.77% of 2025 revenue, propelled by federal edicts that demand phishing-resistant tokens and enterprise single sign-on, which spill over to contractors and regulated healthcare entities. A mature reseller ecosystem simplifies deployment, yet 80% of public-sector IT outlays still feed aging COBOL crates, dragging on modernization velocity. Cloud-first mandates and steady breach disclosures keep the IAM Security Services market entrenched in board-level agendas across the United States and Canada.

Asia Pacific is forecast to clock the fastest 12.67% CAGR through 2031. India’s Digital Personal Data Protection Act, China’s MLPS 2.0, and South Korea’s stringent breach rules converge to set unified access-logging baselines. Rapid cloud uptake across Southeast Asia presents greenfield terrain for SaaS identity suites that integrate with regional payment gateways. Local compliance nuances spur demand for on-premises variants featuring sovereign hosting, enlarging solution matrices within the IAM Security Services market.

Europe combines GDPR benchmarks with sectoral overlays like the Network and Information Security Directive 2, driving consistent investment in consent management and data-subject workflows. Germany’s focus on Zero Trust and France’s mandates for multi-factor authentication among operators of vital importance escalate platform adoption. The Middle East and Africa segment remains nascent but benefits from national digital-identity schemes that front-load authentication for citizen services. Latin America edges forward under Brazil’s Lei Geral de Proteção de Dados, unlocking gradual gains in IAM Security Services market penetration.

Regulatory Landscape

Identity and access management requirements are tightening through standards refreshes and sector regulations that affect authentication, federation, and audit logging used in IAM security services. In the United States, NIST finalized SP 800-63-4 on July 31, 2025, reframing digital identity around Digital Identity Risk Management (DIRM) and risk-based selection of IAL/AAL/FAL, which pushes enterprises and service providers toward continuous assurance rather than static controls. In payments, PCI DSS v4.0.1 became effective March 31, 2025 and raises expectations for phishing-resistant MFA for access into cardholder data environments, expanding demand for managed identity monitoring and privileged-access hardening.

In Europe, DORA has introduced four-hour incident alert requirements for financial entities (effective in 2025), accelerating demand for identity telemetry, privileged session tracing, and immutable logging aligned to operational resilience. The EU AI Act (Regulation (EU) 2024/1689, in force August 1, 2024) adds governance pressure on record-keeping and risk management for high-risk AI systems, reinforcing the need for durable authorization logs and lifecycle controls for agentic and non-human identities. Separately, eIDAS 2.0 requires member states to issue EUDI Wallets by December 2026, creating a concrete interoperability milestone for EU-facing customer identity journeys that accept wallet-based assertions and verifiable credentials.

Value Chain Analysis

The IAM security services value chain starts with standards and identity primitives (for example, NIST digital identity guidelines and FIDO-aligned authenticators), then moves into core software layers such as identity providers, privileged access management, identity governance, directory and federation services, and authorization engines. Services attach across the lifecycle, including discovery and identity inventory, architecture and integration (SSO/MFA rollout, federation hardening, and policy design), migration from legacy directories, and managed operations such as continuous access evaluation, identity threat detection and response, and privileged session monitoring. Hyperscaler ecosystems and SaaS application marketplaces serve as the main distribution rails for cloud-based deployments, while regulated or sovereign requirements support on-premises and hybrid delivery.

Downstream, channel partners and consultancies implement and operate IAM controls across complex estates that include third parties, contractors, and machine identities created by DevOps pipelines. Third-party access governance and continuous monitoring are becoming central handoffs as organizations extend controls to suppliers and network-layer administration, areas that have historically relied on ad hoc credentials and weak accountability. In media and telecom, identity controls are increasingly linked to fraud and bot defenses to reduce account takeover and automated abuse, which shifts demand toward integrated platforms and managed services that can correlate identity, device, and behavior signals at scale.

Competitive Landscape

The top five suppliers capture roughly 40% of revenue, positioning the IAM Security Services market at moderate concentration. Consolidation surged in 2025 when Palo Alto Networks agreed to acquire CyberArk for USD 25 billion, merging privileged-access oversight with network defenses for unified threat correlation. IBM’s USD 6.4 billion deal for HashiCorp in 2024 stitched secrets management and infrastructure-as-code tooling into its hybrid cloud roster.

Phantomization themes now dominate the roadmaps of vendors, shaping the future strategies in the IAM Security Services market. These vendors are integrating identity governance, access control, and endpoint telemetry into their offerings. This integration not only raises switching costs for clients but also increases the wallet share per client, making it a critical focus area for market players. Machine identity management, however, remains an untapped white space, with vendors experimenting with workload-metered pricing models. These models obscure the total cost, creating challenges for clients in assessing long-term expenses.

Challenger brands, such as Jump Cloud and Auth0, Inc., are aggressively targeting SMEs by offering swift connectors and usage-based pricing. This approach is putting significant price pressure on established incumbents, forcing them to rethink their pricing strategies and value propositions. Meanwhile, artificial intelligence layers are becoming increasingly sophisticated, enabling the suggestion of entitlement revocations and the detection of anomalous patterns. Despite these advancements, AI solutions still require expert tuning to function effectively. This reliance on expertise underscores the persistent talent scarcity in the market, which continues to drive demand for advisory services. Overall, the IAM Security Services market is witnessing a dynamic shift, with vendors focusing on innovation and differentiation to capture market share. The interplay of advanced technologies, pricing strategies, and talent challenges is shaping the competitive landscape, making it a critical area of interest for stakeholders.

IAM Security Services Industry Leaders

IBM Corporation

Oracle Corporation

Microsoft Corporation

Amazon Web Services

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity area is modernization toward risk-managed digital identity programs, where buyers align identity proofing, authentication, and federation decisions to formal risk models rather than one-size policies. NIST SP 800-63-4 (released July 2025) and the U.S. federal Enterprise ICAM policy (GSA Order CIO 2183.1A, issued December 2025) provide frameworks that translate into multi-year roadmaps for phishing-resistant authentication, identity lifecycle automation, and auditing across agencies and their vendor ecosystems. The March 2026 update to the Identity Lifecycle Management Playbook (v1.4) further operationalizes these requirements into repeatable steps for provisioning, deprovisioning, and privacy impact assessment, which expands demand for advisory, integration, and managed IAM operations.

A second whitespace is governance and control for non-human identities and AI agents, where enterprises need discovery, ownership mapping, least-privilege policy, and continuous authorization at machine speed. Vendor actions in 2026 reflect active productization of this theme, including Microsoft making passkeys the default authentication method in Microsoft Entra ID (July 2026), and platform releases that focus on identity controls for agentic workflows (for example, Palo Alto Networks Idira in May 2026 and Ping Identity agentic enterprise extensions in May to June 2026). FedRAMP Consolidated Rules for 2026 also adds pull by mandating automated lifecycle management for accounts and privileged access monitoring, widening the addressable scope for identity governance, ITDR-aligned services, and just-in-time access in regulated and public-sector-adjacent environments.

Recent Industry Developments

- July 2026: Microsoft announced that passkeys became the default authentication method in Microsoft Entra ID. The change accelerates passwordless adoption in large identity estates and shifts implementation work toward phishing-resistant enrollment, device trust, and recovery workflows managed at scale.

- June 2026: SailPoint completed its acquisition of Entro Security to add non-human identity and credential security capabilities into its identity platform. The deal strengthens end-to-end governance for service accounts and machine identities, expanding the scope of identity security services tied to discovery, remediation, and continuous monitoring.

- March 2026: Delinea completed the acquisition of StrongDM to integrate just-in-time, runtime authorization into its privileged access management stack. This strengthens continuous authorization and access broker patterns for engineering access paths across hybrid infrastructure, creating additional services demand around privileged session control, policy design, and integration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers third party services that help organizations design, implement, run, and improve identity and access management controls, so the right users and machines get the right access at the right time.

Scope exclusions: We exclude in house internal IAM labor that is not billed as an external service, and we exclude pure software license revenue when it is not packaged as a service.

Segmentation Overview

- By Type of Solutions

- Identity Cloud

- Identity Governance

- Access Management

- Directory Services

- Other Type of Solutions

- By Service Type

- Professional Services

- Managed Services

- By Type of Deployment

- On-premise

- Hybrid

- Cloud-based

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-user Vertical

- BFSI

- IT and Telecom

- Education

- Healthcare

- Retail

- Energy

- Manufacturing

- Other End-User Vertical

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the fact base for the model, and to keep assumptions tied to measurable signals. We referred to public sources such as NIST guidance, the U.S. Cybersecurity and Infrastructure Security Agency publications, and the European Union Agency for Cybersecurity material to understand how IAM controls are being interpreted in real environments. We also reviewed identity related security discussions in peer reviewed journals and conference proceedings, which helped validate where the service mix is shifting.

On the market mapping side, we used company annual reports, earnings call transcripts, and investor presentations to identify service lines and revenue descriptions that fit the scope. Supporting context came from association websites and reputable press coverage that tracks compliance deadlines and breach patterns. Where needed, we complemented this with a paid subscription for company financials and intelligence, plus a patent database to spot sustained investment themes. The sources named above are illustrative, and many other public documents were also used for collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually being bought and delivered, and how pricing is changing as buyers move from project work to ongoing managed services. We spoke with service providers, IAM practice leaders, system integrators, and end user security and IT teams across APAC, EMEA, and the Americas, and then used those inputs to confirm adoption rates, average contract values, and delivery intensity by vertical and organization size.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 43% |

| Mid tier: 44% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 17% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build using IT and security services spend signals, and then it is filtered to IAM specific service intensity by vertical and organization size. The totals are then corroborated with selective bottom-up checks using sampled provider revenue splits, channel feedback on typical contract values, and volume proxies like active workforce and customer account counts, which helps adjust for overstatement in any one input.

Key model inputs include enterprise identity modernization cycles, cloud adoption and hybrid environment share, the mix between professional services and managed services, average blended rates and project duration, and the expansion of zero trust programs that pull IAM into broader access policy work. For forecasting, we mainly use scenario analysis with a light multivariate overlay, where spend growth, cloud migration pace, and regulatory push are stress tested and then aligned to what interviewees see in pipeline and renewal behavior. If a bottom-up proxy is missing in a region or vertical, we bridge it with peer region ratios and then re-check the implied spend per employee to keep the number realistic.

Data Validation & Update Cycle

Results are validated through triangulation across independent signals, and any large variances are investigated before the figures are finalized. We run reasonableness checks like services spend per employee, managed services penetration, and regional share movement against what buyers and providers describe, and then anomalies are reviewed in a multi step analyst sign-off.

The study is refreshed annually, and interim updates are made when material events change demand or pricing, such as major compliance deadlines or sudden shifts in cloud security priorities. Before delivery, we do a final pass to re-check currency conversions, remove stale assumptions, and confirm that the latest public filings and expert inputs still support the market direction.

Mordor Intelligence's Iam Security Services Market Size Versus Other Published Estimates

Published market values for IAM security services can vary even when the topic sounds the same, because the service boundary and the timing of updates are often set differently. The year used for currency conversion, the way blended service rates are carried forward, and whether managed services renewals are counted consistently can all move the final number.

In this study, the refresh cadence is tied to the most recent filing cycle and interview re-checks, and pricing is updated through current rate cards and contract mix inputs before the total is converted in USD, which is why the 2025 figure lands at USD 19.04 B (2025) for Mordor Intelligence instead of aligning with estimates that use older FX timing or a faster ASP escalation curve.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.04 B (2025) | |

| Global Consultancy A | USD 23.08 B (2025) | Uses a different base year setup and a longer forecast arc, and the 2025 value appears to reflect more aggressive service price progression and renewal uplift assumptions carried forward from 2024. |

| Industry Publisher B | USD 14.21 B (2024) | Anchors the series on a lower 2024 starting point, and differences can come from narrower inclusion of managed service bundles or a more conservative treatment of multi-year program rollouts. |

The table shows that most of the spread is explained by timing choices and how fast pricing and recurring services are assumed to expand. By keeping the model tied to observable demand drivers and then re-validating the key rate and mix assumptions, our output remains traceable and repeatable even when inputs are imperfect.

Key Questions Answered in the Report

How large is the IAM Security Services market in 2026?

The market reached USD 21.42 billion in 2026 and is projected to grow at an 11.12% CAGR through 2031.

Which solution segment currently commands the largest share?

Access Management led with 35.19% of 2025 revenue, driven by unified single sign-on and multi-factor authentication deployments.

Which geography is expected to grow fastest through 2031?

Asia Pacific is forecast to register a 12.67% CAGR, supported by new privacy laws in India and China.

Why are managed services gaining traction?

Managed Services are expanding at a 12.01% CAGR as mid-market firms outsource 24/7 identity monitoring to overcome skills shortages.

What is the primary driver behind healthcare adoption?

A surge in ransomware incidents that encrypted 41.8 million U.S. patient records in 2024 is pushing hospitals to tighten privileged-access controls.

How does Zero Trust influence IAM purchasing decisions?

Zero Trust mandates from regulators require continuous verification of user and device context, steering enterprises toward integrated identity platforms.

Page last updated on: