Market Overview

| Study Period | 2020 - 2031 |

|---|---|

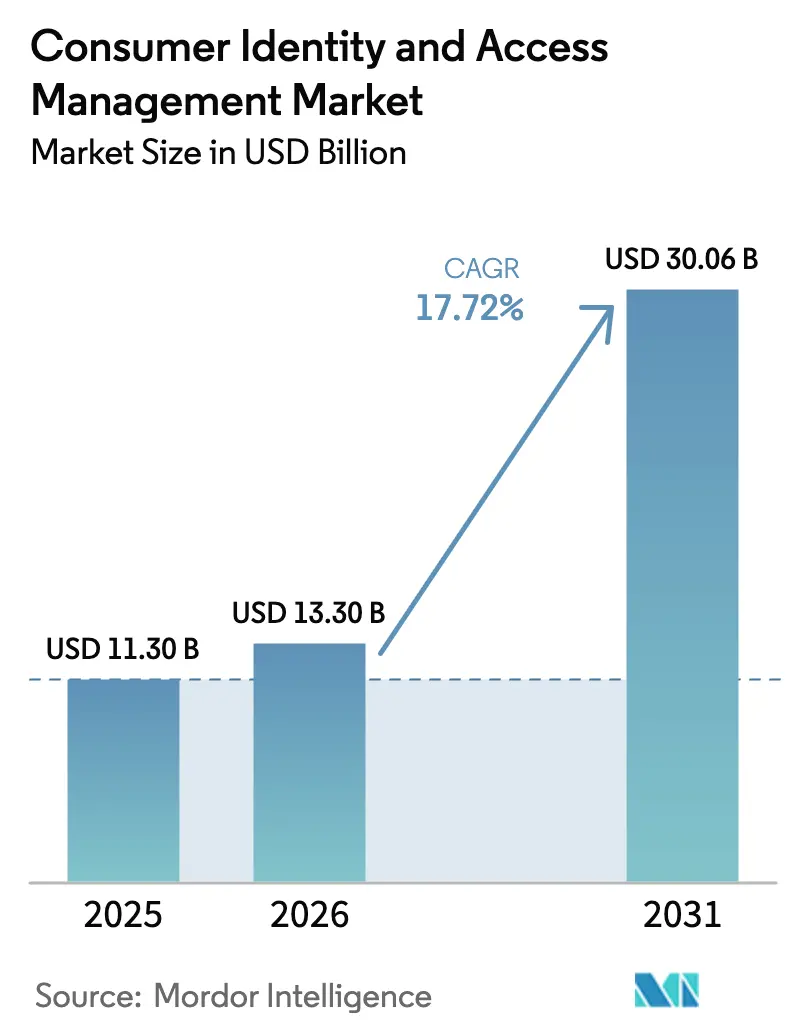

| Market Size (2026) | USD 13.3 Billion |

| Market Size (2031) | USD 30.06 Billion |

| Growth Rate (2026 - 2031) | 17.72% CAGR |

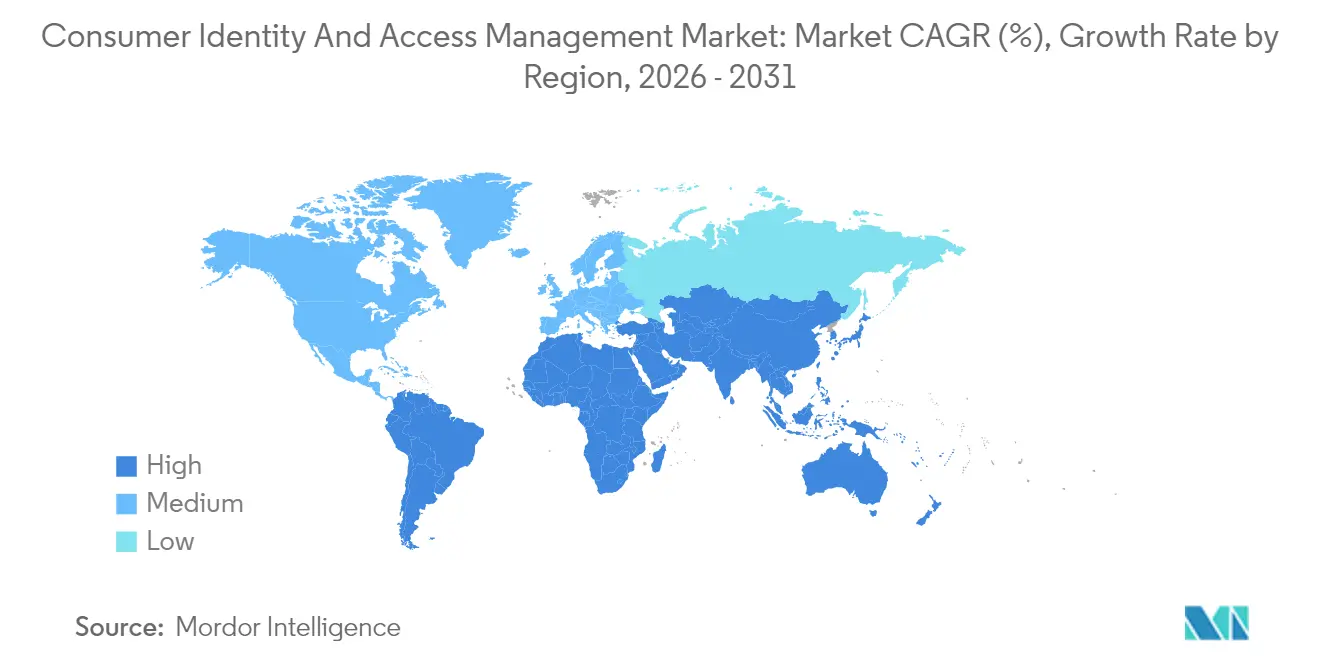

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Identity And Access Management Market Analysis by Mordor Intelligence

The customer identity and access management market size was valued at USD 11.3 billion in 2025 and estimated to grow from USD 13.3 billion in 2026 to reach USD 30.06 billion by 2031, at a CAGR of 17.72% during the forecast period (2026-2031). Sustained growth reflects enterprise moves toward customer-centric digital engagement, rising regulatory compliance duties, and a sharp uptick in sophisticated cyber threats. Generative-AI adaptive authentication, mandatory PSD3 consent orchestration, and eIDAS 2.0 digital identity wallets combine to accelerate adoption, while businesses face USD 186 billion in yearly losses from API-layer bot attacks. Solutions continue to account for the bulk of spending, but managed services gain momentum as organizations outsource complex orchestration tasks. Cloud deployment dominates new projects, driven by infrastructure modernization and regulatory acceptance of cloud controls. Healthcare, embedded finance, and super-app ecosystems offer outsized opportunities as each segment demands seamless yet privacy-preserving identity journeys.

Key Report Takeaways

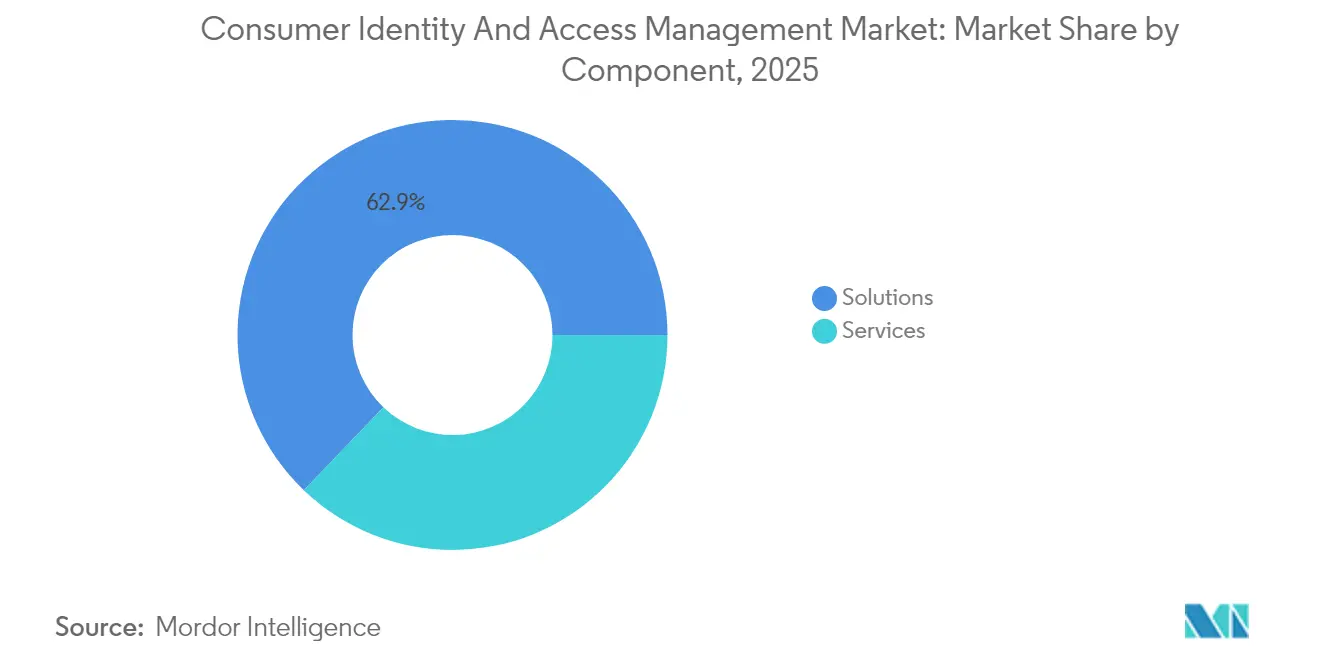

- By component, solutions held 62.85% of the customer identity and access management market share in 2025, whereas services are set to record a 18.6% CAGR to 2031.

- By deployment mode, cloud captured 77.35% of the customer identity and access management market size in 2025 and is projected to rise at a 19.35% CAGR during the forecast window.

- By end-user industry, BFSI led with 28.55% revenue share in 2025, while healthcare is advancing at a 19.08% CAGR through 2031.

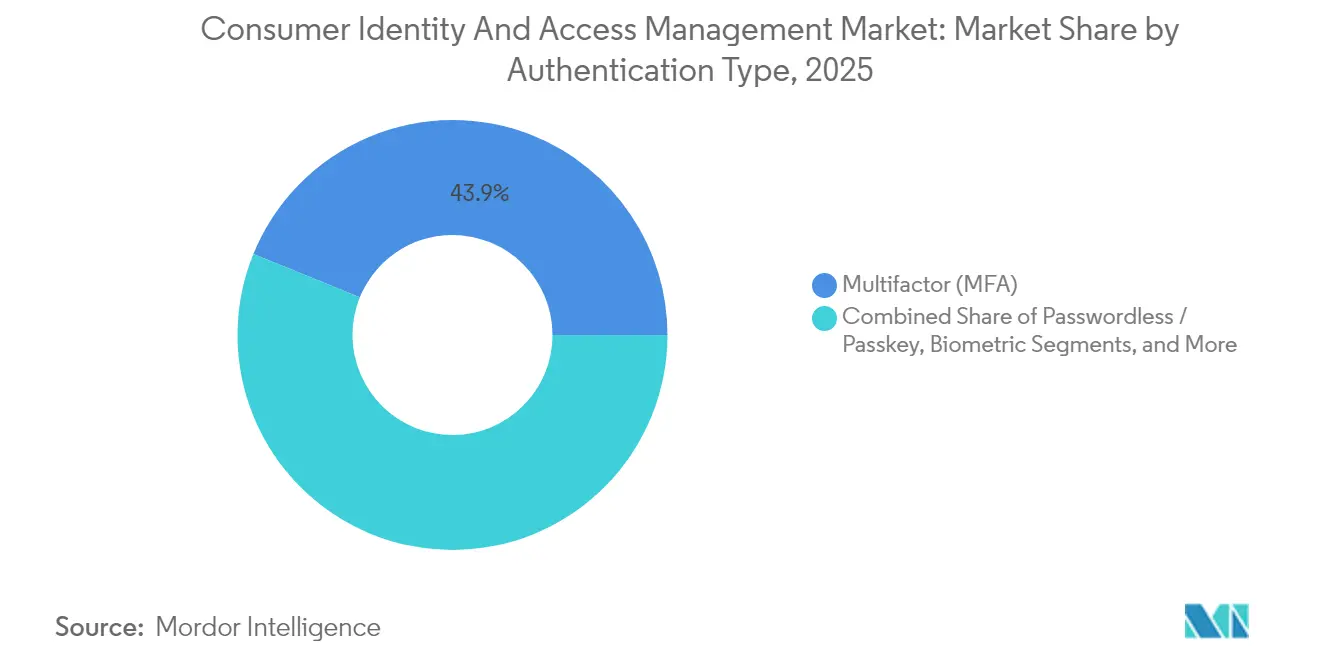

- By authentication type, multifactor authentication represented 43.85% share of the customer identity and access management market size in 2025; passwordless/passkey solutions are expanding at a 23.65% CAGR to 2031.

- By organization size, large enterprises commanded 61.15% share in 2025, whereas SMEs are growing at an 18.28% CAGR.

- By geography, North America accounted for 43.25% of the customer identity and access management market share in 2025; Asia-Pacific is forecast to post the fastest 17.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Consumer Identity And Access Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gen-AI adaptive authentication | +3.2% | Global, early uptake in North America and EU | Medium term (2-4 years) |

| Privacy–user-experience balance elevates CIAM budgets | +2.8% | Global, strongest in EU | Short term (≤ 2 years) |

| Embedded finance and super-apps need federated CIAM | +4.1% | APAC core, Latin America spill-over | Medium term (2-4 years) |

| Mandatory PSD3/CPRA consent orchestration | +2.9% | EU and expanding US scope | Long term (≥ 4 years) |

| Passwordless FIDO2 roll-out by Big Tech | +3.5% | Global, led by North America | Short term (≤ 2 years) |

| Digital identity wallets under eIDAS 2.0 and NIST | +2.7% | EU primary, US emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gen-AI Adaptive Authentication

Generative AI moves CIAM from reactive control to predictive risk assessment. Strivacity’s AI Assist shows real-time analysis of user journeys and automated compliance checks, and analysts expect 35% of organizations to embed generative AI in identity functions by 2025. [1]Strivacity, “AI Assist: Your AI Digital Identity Expert,” strivacity.com Dynamic policies based on behavior, device fingerprinting, and context trim user friction while raising security, a balance valued by healthcare providers integrating Clear with Epic for rapid patient sign-in. Adaptive mechanisms tailor step-up requirements to individual risk profiles and mitigate over-authentication fatigue that erodes conversion rates.

Growing Privacy–UX Trade-off Awareness Drives Budgets

The eIDAS 2.0 mandate effective May 2024 obliges EU states to issue national digital identity wallets by 2026, pushing enterprises to adopt privacy-protective CIAM strategies. Consumers demand frictionless journeys, so firms abandon legacy log-in screens that prioritize security at the expense of convenience. Healthcare providers illustrate this pivot; identity wallets let patients retrieve records across networks while retaining HIPAA compliance. Privacy moves from blocker to enabler of superior user experience.

Surge in Embedded Finance & Super-apps Requiring Federated CIAM

Super-apps that bundle messaging, shopping, and financial services rely on federation to authenticate users across multiple partners. The OECD Digital Economy Outlook 2024 links rapid digital services adoption in APAC to 7.6% ICT sector growth. Peru’s Yape and Plin e-wallets show 340% transaction growth, underscoring identity federation needs. CIAM platforms must manage multiple identity contexts while sustaining unified security policy enforcement.

Mandatory PSD3/CPRA Consent Orchestration Compliance

PSD3 will introduce delegated authentication and outcome-based SCA, compelling banks and fintechs to modernize consent workflows. The California Privacy Rights Act increases complexity with granular consent preferences. CIAM vendors must evolve into orchestration engines that store, update, and verify dynamic privacy directives across regions and channels.

Restraints Impact Analysis of Consumer Identity And Access Management Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| API-layer bot attacks outpace mitigation | –2.1% | Global, highest in North America and EU | Short term (≤ 2 years) |

| Fragmented data-residency laws inflate cost | –1.8% | Global, acute in APAC and emerging markets | Medium term (2-4 years) |

| CIO skill gap in CIAM orchestration | –1.4% | Global, sharpest among SMEs | Medium term (2-4 years) |

| Customer trust erosion after breaches | –1.2% | Global, varying by region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

API-layer Bot Attacks Outpace CIAM Mitigation Speed

Bots exploiting APIs compromise customer journeys and raise security costs. Enterprises now manage an average 613 API endpoints that widen attack surfaces, and related incidents climbed 28% in 2024, costing USD 186 billion annually. [2]Thales Group, “Vulnerable APIs and Bot Attacks Costing Businesses up to USD 186 Billion Annually,” cpl.thalesgroup.com Effective deterrence requires integrating CIAM with dedicated API security analytics, stretching budgets, and prolonging roll-outs.

CIO Skill Gap in CIAM Orchestration & DevSecOps Integration

Modern CIAM demands scripting policies, wiring event streams to security information and event management (SIEM) tools, and embedding automation into DevSecOps pipelines. Many SMEs lack staff with requisite IAM knowledge, echoing CISA findings that premium SSO services price out smaller firms. [3]CISA, “Barriers to Single Sign-On Adoption for Small and Medium-Sized Businesses,” cisa.gov Outsourcing partially bridges the gap but heightens vendor lock-in concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Consumer Identity And Access Management Market Segment Analysis

By Component:

Managed Services Take Center StageServices revenue is outpacing software as firms seek turnkey deployment. The component segment captured 62.85% of the customer identity and access management market size for solutions in 2025, yet services are forecast to grow 18.6% annually through 2031. Large enterprises shift orchestration to experts, and SMEs, citing JumpCloud’s survey of 42% outsourcing, follow suit.

The rising complexity of privacy, adaptive authentication, and multi-channel consent workflows makes managed services attractive. Healthcare organizations rely on Clear integrations that minimize in-house coding. As customer identity and access management market adoption broadens, competitive differentiation leans more on implementation quality than feature checklists.

By Deployment Mode:

Cloud Leads ModernizationCloud installations accounted for 77.35% share of the customer identity and access management market size in 2025 and will advance at a 19.35% CAGR as legacy on-premise estates retire. Microsoft’s Entra ID showcases continuous feature delivery, convincing risk-averse sectors that cloud meets or exceeds security benchmarks.

Hybrid deployments remain for data-sovereignty or low-latency needs, but most new roll-outs default to cloud. Enterprises prize API-first extensibility and automated scaling. Managed service providers build standardized stacks that shorten time-to-value and keep compliance artefacts current across regions, reinforcing cloud preference.

By End-user Industry:

Healthcare Rises FastHealthcare is projected to post a 19.08% CAGR, surpassing every other vertical. Digital front-door strategies, telemedicine, and interoperability programs such as SMART on FHIR compel providers to adopt modern CIAM. Meanwhile, BFSI retains a 28.55% share as of 2025, reflecting long-standing regulatory drivers.

Patient misidentification costs and cross-provider data exchange spur biometric and passkey implementations. Clear’s hospital kiosks illustrate benefits: faster check-in, fewer manual errors, and higher patient satisfaction. Growth in healthcare cements domain-specific templates as a must-have for vendors aiming to expand customer identity and access management market reach.

By Authentication Type:

Passwordless Gains GroundMultifactor methods hold a 43.85% share, yet passwordless/passkey authentication is racing ahead at a 23.65% CAGR. The customer identity and access management market is transitioning from shared secret models toward public-key cryptography backed by device biometrics. The FIDO Alliance data shows 15 billion passkey-enabled accounts as of 2024.

Enterprises grapple with account recovery and legacy compatibility, slowing full conversion. Nevertheless, Big Tech standardization lowers integration costs, and regulators increasingly recognize passkeys as strong consumer-grade authentication. Industries with high-value assets, such as healthcare and finance, lead deployments.

By Organisation Size:

SMEs Close the GapLarge enterprises retain 61.15% share, but SMEs will clock an 18.28% CAGR. The customer identity and access management market must accommodate constrained budgets and lean IT teams. Freemium tiers and simplified orchestration help vendors penetrate this segment.

CISA notes that high subscription fees deter adoption among small businesses. Vendors respond with bundled offers, managed setups, and AI-driven configuration wizards that shrink deployment times. As barrier-free digital commerce becomes table stakes, SMEs cannot ignore robust identity, fueling steady uptake.

Geography Analysis

North America Consumer Identity And Access Management Market

North America held 43.25% of 2025 revenue owing to entrenched enterprise programs and plentiful vendor ecosystems. Ongoing enhancements focus on adaptive risk analytics and regulatory alignment with CPRA, yet overall expansion rates moderate as base penetration grows. Government attention on SME affordability, reflected in CISA studies, supports broader adoption and keeps the customer identity and access management market vibrant.

APAC Consumer Identity And Access Management Market

Asia-Pacific is forecast to record the fastest 17.98% CAGR, propelled by government identity wallet schemes, super-app economics, and mobile-first consumer habits. ICT growth across OECD member economies averaged 7.6% in 2024 and was higher in leading APAC nations, underlining fertile ground for identity platforms. Vendors localize data storage and comply with national standards to capture demand.

Europe Consumer Identity And Access Management Market

Europe advances on the back of eIDAS 2.0, which mandates interoperable wallets by 2026. The initiative will enlarge the customer identity and access management market as public and private sectors converge on shared digital ID frameworks. Privacy leadership positions European vendors to export expertise abroad, although varied implementation timelines and economic headwinds inject execution risk.

Competitive Landscape

Market consolidation is underway as established providers add AI layers and cloud hyperscalers bundle CIAM into broader platforms. Ping Identity’s ForgeRock integration produced a unified orchestration suite that targets regulated verticals and extends regional data-residency coverage. Microsoft, IBM, and Okta maintain scale advantages courtesy of long-standing enterprise contracts and ecosystems.

Disruptors concentrate on vertical niches and rapid deployment. Strivacity focuses on low-code orchestration with embedded generative AI, while Frontegg emphasizes developer-centric APIs. Semiconductor supply constraints affect biometric device roll-outs as the wider component market reached USD 627.6 billion in 2024. Vendors able to secure hardware pipelines gain leverage, especially in sectors reliant on on-device biometrics.

Competition is shifting from feature counts to compliance and integration depth. Buyers value out-of-the-box orchestration for PSD3 and eIDAS 2.0, plus connectivity into API security, fraud analytics, and consent vaults. Partnerships with system integrators and managed service providers are integral to winning large multi-region deals and expanding customer identity and access management market presence.

Consumer Identity And Access Management Industry Leaders

Microsoft Corporation

IBM Corporation

Okta Inc. (incl. Auth0)

Ping Identity Holdings

Salesforce Inc.

- *Disclaimer: Major Players sorted in no particular order

Consumer Identity And Access Management Market Companies Covered in this Report

- Microsoft Corporation

- IBM Corporation

- Okta Inc. (incl. Auth0)

- Ping Identity Holdings

- ForgeRock Inc.

- Salesforce Inc.

- Amazon Web Services Inc.

- Broadcom Inc. (Symantec)

- Thales Group (Gemalto)

- HID Global (Assa Abloy)

- CyberArk Software Ltd.

- Micro Focus Intl. plc

- Duo Security (Cisco)

- OneLogin (One Identity)

- Strivacity

- Frontegg

- LoginRadius Inc.

- Authgear

- SAASPASS Inc.

- IDCUBE Systems Pvt Ltd.

- AlertEnterprise Inc.

- Convergint Technologies LLC

Read Analysis of Consumer Identity And Access Management Companies

Recent Industry Developments in Consumer Identity And Access Management Market

- May 2025: The European Commission formally launched eIDAS 2.0 roll-out, obliging member states to issue digital identity wallets by 2026.

- March 2025: Microsoft enabled full passkey workflows across Entra ID to entrench passwordless, phishing-resistant authentication.

- February 2025: Ping Identity completed ForgeRock integration, preserving customer investments while unifying orchestration capabilities for healthcare expansion.

- January 2025: Alan Turing Institute reported an upsurge in cyberattacks on digital identity systems, highlighting CIAM hardening priorities.

Consumer Identity And Access Management Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the consumer identity and access management (CIAM) market as all dedicated software and service offerings that let organizations capture, authenticate, govern, and analyze individual customer identities across digital touchpoints while maintaining privacy controls and consent logs. According to Mordor Intelligence, revenue generated from both cloud and on-premise deployments across every end-user industry and global region is counted; yet enterprise-only IAM and pure workforce access tools are excluded.

Scope Exclusions: tools built solely for internal employee identity management, physical access cards, and standalone fraud-risk scoring engines are outside this analysis.

Segments Covered in This Report

- By Component

- Solutions

- Authentication and Authorisation

- Identity Verification and Proofing

- User Profile and Consent Management

- Services

- Professional

- Managed

- Solutions

- By Deployment Mode

- Cloud-based

- On-premise

- By End-user Industry

- BFSI

- Healthcare

- IT and Telecom

- Government

- Energy and Utilities

- Transportation

- Aerospace and Defense

- Education

- By Authentication Type

- Multifactor (MFA)

- Passwordless / Passkey

- Biometric

- Social and Federated Login

- By Organisation Size

- Large Enterprises

- Small- and Medium-sized Enterprises (SMEs)

- Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of ASEAN

- Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts held structured interviews with CISOs, product leads at CIAM vendors, and implementation partners across North America, Europe, and Asia-Pacific. The conversations validated adoption triggers, average contract values, and likely migration timelines, giving us fresh checks on desk-based assumptions and region-specific growth signals.

Desk Research

We begin by gathering open data from respected bodies such as the US Federal Trade Commission, ENISA, and NIST on breach volumes and regulatory timelines, along with regional statistics from Eurostat and the Reserve Bank of India that illuminate digital transaction growth. Company 10-Ks, patent filings pulled through Questel, and news feeds from Dow Jones Factiva help our team track vendor launches, pricing shifts, and M&A moves that reshape supply. These sources, though illustrative, are supported by many additional references consulted throughout the project.

Market-Sizing & Forecasting

A top-down view that reconstructs spending from national cybersecurity budgets, e-commerce transaction counts, and average CIAM penetration rates is cross-checked with selective bottom-up rollups of supplier revenue disclosures and channel surveys. Key variables in the model include verified data-breach incidents, cloud workload share, smartphone subscriptions, GDPR-like regulation rollouts, and shift toward passwordless authentication. Multivariate regression, applied to these inputs, produces the 2025-2030 trajectory, while scenario analysis captures upside from accelerated regulatory enforcement. Gaps in vendor disclosures are bridged by interpolating regional adoption curves anchored to confirmed pilot volumes.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance checks against independent security-spend benchmarks, and a senior sign-off. We refresh the model each year and issue interim tweaks whenever material events, large breaches, landmark laws, or sizable acquisitions alter demand patterns, ensuring clients always receive our latest viewpoint.

How Mordor Intelligence's Consumer Identity And Access Management Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick distinct scope boundaries, currency conversions, and forecasting cadences.

Key gap drivers include whether consumer and workforce IAM are blended, how aggressively cloud price erosion is projected, and the frequency at which new breach statistics are folded back into models. Mordor's choice to separate enterprise IAM, apply quarterly FX averages, and re-survey experts before every refresh narrows uncertainty for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.03 B (2025) | Mordor Intelligence | - |

| USD 12.5 B (2024) | Global Consultancy A | Blends workforce IAM, annual FX spot rates |

| USD 17.86 B (2024) | Industry Research B | Uses high initial ASPs, five-year refresh cycle |

Taken together, the comparison shows that while some publishers overstate totals by mixing adjacent segments or using outdated price points, our disciplined scope setting and frequent data updates give planners a balanced, transparent baseline they can confidently defend in board discussions.

Key Questions Answered in the Report

What is the current size of the customer identity and access management market?

The market is valued at USD 13.3 billion in 2026 and is forecast to reach USD 30.06 billion by 2031.

What compound annual growth rate (CAGR) is projected for the customer identity and access management market through 2031?

Analysts expect an 17.72% CAGR during the 2026-2031 period.

Which deployment model is expanding the fastest?

Cloud-based CIAM commands 77.35% of 2025 revenue and is growing at a 19.35% CAGR as organizations modernize infrastructure and embrace API-first architectures.

Why is healthcare the quickest-growing end-user segment?

Hospitals and clinics need secure, seamless patient identity verification for telehealth, electronic health records, and interoperability, driving a 19.08% CAGR in the segment.

How are passkeys influencing CIAM strategies?

Wide passkey adoption—15 billion enabled accounts in 2024—pushes enterprises toward passwordless, phishing-resistant authentication that improves user experience and security.

Which regions will fuel the next wave of CIAM demand?

Asia-Pacific is set to post a 17.98% CAGR on the back of digital identity wallets, super-app ecosystems, and mobile-first consumers, while Europe gains momentum from eIDAS 2.0 regulations.

Page last updated on: