Decentralized Identity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

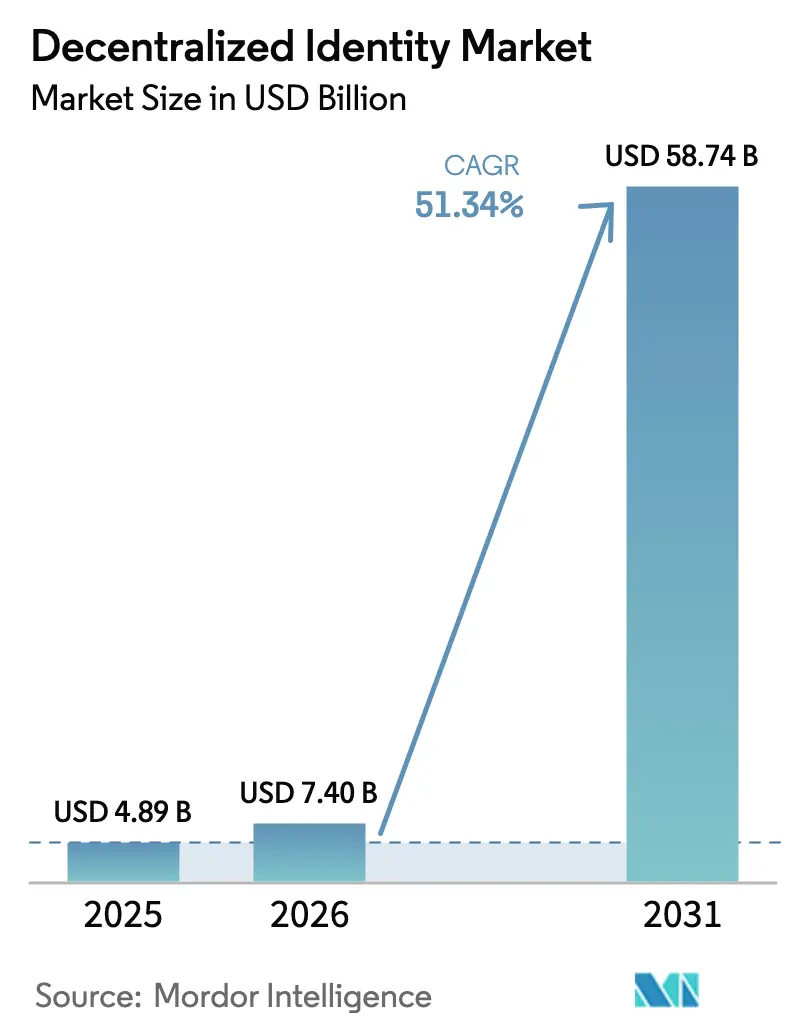

| Market Size (2026) | USD 7.4 Billion |

| Market Size (2031) | USD 58.74 Billion |

| Growth Rate (2026 - 2031) | 51.34% CAGR |

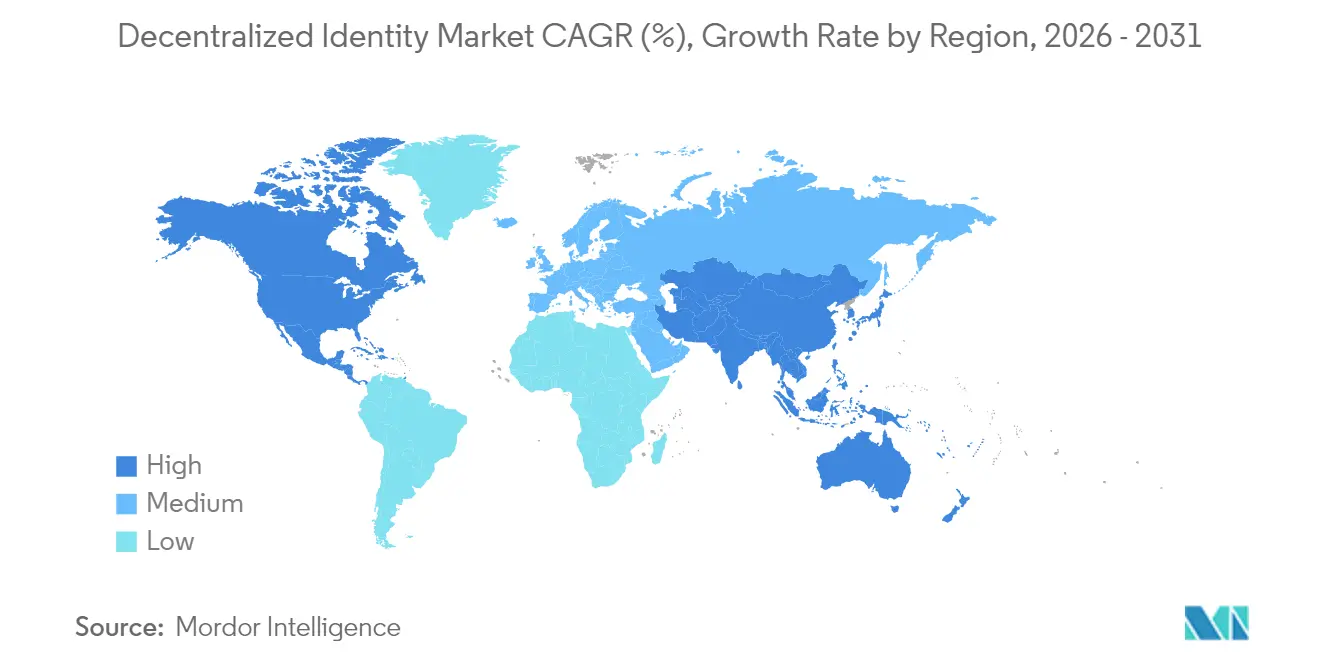

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decentralized Identity Market Analysis by Mordor Intelligence

The decentralized identity market size in 2026 is estimated at USD 7.4 billion, growing from 2025 value of USD 4.89 billion with 2031 projections showing USD 58.74 billion, growing at 51.34% CAGR over 2026-2031. Propelled by sweeping regulatory mandates, accelerated enterprise digitization, and ongoing breakthroughs in blockchain tooling, the market is redefining how organizations and individuals verify credentials online. Rapid wallet roll-outs under the European Union’s eIDAS 2.0 framework, rising reliance on biometric authentication, and mounting venture funding for privacy-preserving protocols are setting new adoption benchmarks. Enterprises are pivoting toward cloud-native deployments to gain elastic scalability, while sector-specific use cases—from cross-border payments to patient record sovereignty—continue to multiply. Taken together, these forces are compressing implementation timelines and expanding the total addressable user base for decentralized identity platforms worldwide.

Key Report Takeaways

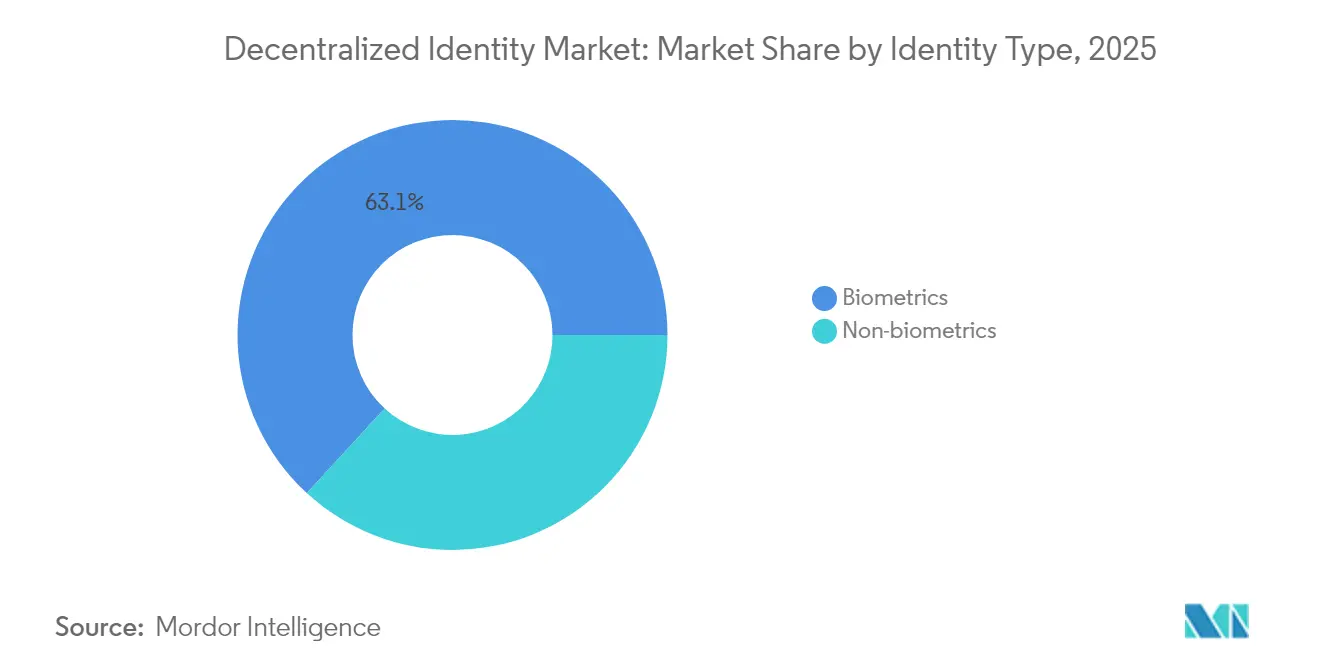

- By identity type, biometrics led with 63.15% decentralized identity market share in 2025, while non-biometric credentialing is forecast to grow at 20.85% CAGR through 2031.

- By deployment model, cloud architectures captured 59.05% of implementations in 2025; hybrid cloud is poised for the fastest CAGR at 17.75% to 2031.

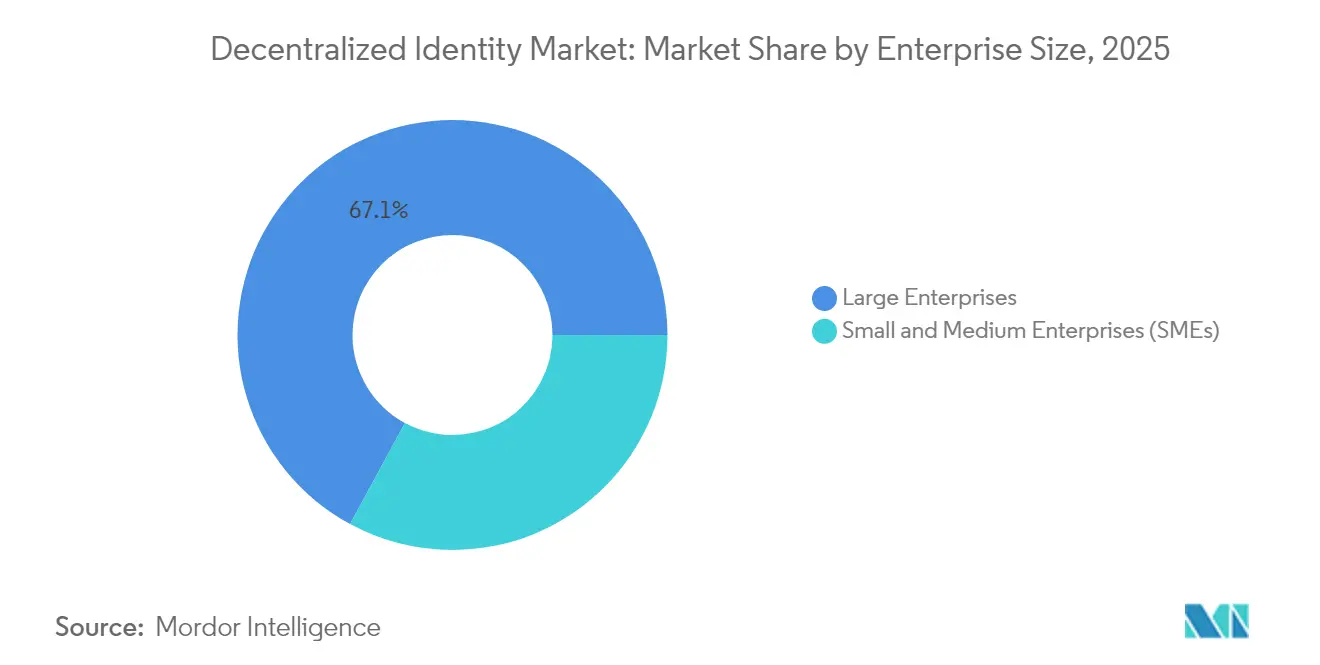

- By enterprise size, large enterprises controlled 67.10% of the decentralized identity market size in 2025, whereas SMEs are expected to post an 17.9% CAGR and outpace all other cohorts.

- By end-user industry, BFSI commanded 32.15% revenue share in 2025, while healthcare is projected to exhibit the highest 23.4% CAGR through 2031.

- By geography, North America held 37.95% share of the decentralized identity market size in 2025; Asia-Pacific is projected to log the quickest 19.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Decentralized Identity Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy regulations (GDPR, eIDAS 2.0) | +12.5% | Europe; spillover to North America and Asia-Pacific | Medium term (2-4 years) |

| Accelerating blockchain adoption in BFSI and government | +11.2% | Global | Medium term (2-4 years) |

| Surge in digital onboarding and remote KYC | +9.8% | Global | Short term (≤ 2 years) |

| Mobile-first identity apps in emerging markets | +8.4% | Asia-Pacific core; MEA and South America | Medium term (2-4 years) |

| Explosion of non-human identities (APIs, bots) | +7.6% | North America and Europe | Long term (≥ 4 years) |

| Metaverse and gaming wallets demand reusable IDs | +4.2% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Regulations Drive Sovereign Identity Adoption

Mandatory European Digital Identity Wallets under eIDAS 2.0 establish common cryptographic rules, enabling citizens to reuse credentials across borders and sectors[1]European Commission, “European Digital Identity Wallet,” ec.europa.eu. Enterprises now embed selective disclosure and zero-knowledge proofs to lower liability and pass privacy audits, cutting onboarding friction by up to 40% in FCA-supervised SSI pilots. Open-source wallet reference stacks are dampening vendor lock-in and fostering a vibrant ecosystem of specialized middleware providers. Banks, telcos, and public agencies alike perceive tangible cost savings from harmonized KYC processes. As adjacent jurisdictions pursue reciprocal arrangements, European standards influence global working groups shaping the next generation of verifiable-credential profiles.

Accelerating Blockchain Adoption in Financial Services

Global banks increasingly treat decentralized identifiers as frontline defenses against credential stuffing and account-takeover attacks that hit 86% of financial institutions in 2024. High-profile pilots, such as PASS—a blockchain credit bureau backed by Eric Schmidt—prove that pseudonymous lending can comply with AML rules via on-chain attestations. Governments augment the push: India’s Digital Public Infrastructure-as-a-Service model offers smaller nations turnkey stacks anchored on verifiable credentials. Interoperability efforts coalesce around W3C DID and Verifiable Credential specifications, giving the decentralized identity market an open-standards bedrock on which mainstream financial rails can confidently build.

Surge in Digital Onboarding and Remote KYC

Enterprises now issue reusable KYC credentials that cut recurring verification costs up to 60% while safeguarding personal data via zero-knowledge proof schemes. Coupling liveness detection with cryptographic attestations thwarts synthetic identities without exposing biometrics in centralized silos. For highly regulated verticals—capital markets, online gaming, telemedicine—verifiable credentials streamline audits because every regulatory checkpoint sits immutably on ledger. By plugging the same verified identity into multiple services, users experience single-tap enrollment, and organizations curb friction that previously stalled customer acquisition. The decentralized identity market benefits from this dual mandate of compliance and convenience.

Mobile-First Identity Applications Transform Emerging Market Access

More than one billion people still lack formal ID, yet smartphone penetration tops 80% in many emerging economies. Mobile wallets such as FlexID, funded by the Algorand Foundation, bundle payments, credentials, and consent dashboards into a single UI. Malaysia’s MyDigital ID Superapp extends the pattern nationally, using blockchain for tamper-proof issuance while letting citizens sign legally valid documents online. As Asia-Pacific fintechs race to onboard under-banked populations, demand for lightweight decentralized identity SDKs grows. Because wallet apps can operate offline and sync when connectivity returns, they solve real-world access gaps across archipelagos and rural regions.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of global interoperability standards | -8.9% | Global | Medium term (2-4 years) |

| Regulatory uncertainty across jurisdictions | -7.3% | Global | Short term (≤ 2 years) |

| Poor UX and key-custody hurdles for mass users | -6.4% | Global | Medium term (2-4 years) |

| Layer-1 scalability limits for high-TPS DID networks | -5.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability Standards Fragmentation Limits Cross-Platform Adoption

Although W3C DIDs define the core data model, divergence in DID methods, credential schemas, and revocation lists hampers seamless cross-chain validation. Enterprises must integrate multiple resolver libraries to service partners anchored on different ledgers, inflating deployment timelines. The absence of uniform trust frameworks complicates liability allocation when credentials traverse borders. Healthcare and financial regulators often postpone green-lighting pilots until there is clarity on who bears breach responsibility. Fragmentation thus tempers the breakneck expansion otherwise expected for the decentralized identity market.

User Experience Barriers Impede Mainstream Adoption

Surveys show 68% of prospective users exit wallet setup once confronted with seed-phrase management. Custody anxiety persists even when hardware keys or social-recovery contacts are proposed. Emerging fixes—passkeys, account abstraction, encrypted cloud backups—improve onboarding completion yet remain unevenly deployed across wallet vendors. Until household-name platforms bake in intuitive UX metaphors, decentralized identity stands to remain an early-adopter phenomenon rather than a ubiquitous consumer utility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Identity Type: Biometrics Underpin Momentum in Privacy-Centric Verification

Biometric modalities accounted for 63.15% decentralized identity market share in 2025, underscoring the appetite for friction-less yet non-transferable authentication at scale. Market leaders integrate liveness and anti-spoofing algorithms that resist deepfake attempts and synthetic fraud. Humanity Protocol’s palm-scanning solution, now valued at USD 1.1 billion after successive funding rounds, typifies investor conviction in privacy-preserving biometrics. Complementary innovations employ iris codes and voiceprints bound to decentralized identifiers, thereby enabling revocable proofs without central repositories. The result is a layered risk posture that satisfies regulators while improving user convenience.

Non-biometric schemes ride cryptographic assurances instead of physical traits, furnishing vital alternatives where biometric capture triggers cultural or legal objections. Verifiable credentials, behavioral analytics, and devicefingerprinting offer operators flexibility, particularly in high-compliance enterprise corridors where data controllers must demonstrate minimal data collection. Hybrid deployments blending both approaches are gaining favor because they let end users select the verification path that best balances privacy and certainty. Such configurability keeps the decentralized identity market responsive to jurisdictional nuances while sustaining robust growth trajectories through 2030.

By Deployment Model: Cloud Infrastructure Unlocks Elastic Verification Workloads

Cloud-hosted solutions commanded 59.05% of deployments in 2025, reflecting the cost and time advantages of running identity-verification logic on hyperscale platforms that auto-provision compute for resource-intensive zero-knowledge proof calculations. Microsoft’s Entra Verified ID suite shows how identity-as-a-service plug-ins can sit inside existing SSO consoles, allowing enterprises to extend W3C-compliant verifiable credentials to workforce, partner, and consumer populations in days rather than quarters. Managed services also absorb patching, uptime, and audit obligations, freeing compliance teams to concentrate on governance policy.

On-premises and hybrid models remain essential in sovereign-data scenarios such as defense, central-bank digital currency pilots, and certain public-health registries. Here, sensitive underlying registries stay inside an organization’s firewall, while public-key resolution or schema hosting sits in the cloud to retain global reach. Hybrid patterns therefore extend best-of-both design and are expected to post an 17.75% CAGR, the fastest within this segmentation. Elastic architectures in turn encourage service providers to roll out new credential types—employee badges one quarter, product authenticity certificates the next—without infrastructure re-engineering, cementing cloud’s pivotal role in the decentralized identity market.

By Enterprise Size: SMEs Fuel Uptake Through Low-Code SaaS Offerings

SMEs clocked an 17.9% CAGR, making them the speediest adopters between 2026 and 2031. Low-code APIs and wallet SDKs let firms embed verifiable-credential flows in e-commerce or HR portals without standing up dedicated security teams. The World Bank tallies onboarding costs dropping 30-50% for SMEs that retire cumbersome document scans in favor of cryptographically signed attributes. This saving levels the playing field with larger rivals and converts compliance budgets from cost centers into catalysts for new cross-border services.

Large enterprises still captured 67.10% revenue in 2025 because their sprawling ecosystems—employees, contractors, suppliers—demand unified credential governance. These organizations are weaving decentralized identifiers into existing IAM stacks, effectively overlaying a verifiable credential rail adjacent to conventional OAuth or SAML flows. The coexistence strategy avoids forklift upgrades while positioning firms to phase out central credential stores once policymakers endorse full-scale decentralized architectures. Consequently, both cohorts reinforce the decentralized identity market’s momentum: SMEs expand breadth, corporates deepen ticket size.

By End-User Industry: Healthcare Leads on Patient Sovereignty, BFSI on Volume

Healthcare registered the fastest 23.4% CAGR by 2031 as hospitals shift from siloed EHR environments to patient-held wallets containing verifiable lab results, prescriptions, and insurance attestations. Early pilots in the United Kingdom’s National Health Service reveal reductions in manual credentialing for traveling clinicians, trimming administrative overhead, and expediting emergency staff redeployment. Combining decentralized identity with federated learning frameworks preserves confidentiality while enabling algorithm training on aggregate data, a model already showcased by the Decentralized Intelligence Health Network.

Meanwhile, BFSI held the largest 32.15% share of the decentralized identity market size in 2025 as banks, insurers, and capital markets players codify stringent KYC regimes into shareable credentials. A single digital certificate that confirms source-of-funds checks is now accepted across multiple service lines—from brokerage onboarding to mortgage origination—yielding operational savings. Adjacent verticals like IT and telecom deploy DID-anchored device identities to defend 5G core networks, whereas retail platforms rely on verifiable credentials to combat account takeover fraud. Each industry underscores a distinct but mutually reinforcing logic for adoption: compliance, cost control, and customer experience.

Geography Analysis

North America retained 37.95% of the decentralized identity market size in 2025, powered by early enterprise pilots in financial services and big-tech-backed protocol development. The region’s venture ecosystem provided a runway for innovators such as Humanity Protocol’s palm-scan wallet, which secured USD 50 million across its seed and Series A raises. Collaboration between public agencies and private consortia keeps legal frameworks adaptive, enabling sandbox trials that shorten the time from proof-of-concept to production. Standard-setting bodies such as the Decentralized Identity Foundation, with contributions from Block and Microsoft, further cement the United States as a technical thought leader.

Asia-Pacific emerges as the fastest-growing territory at a 19.9% CAGR through 2031. Government-led drives in Japan, Singapore, Malaysia, and India place mobile wallets at the center of digital public-infrastructure strategies. Japan’s decision to embed My Number credentials in Apple Wallet fuses consumer-grade UX with state-backed assurance, broadening acceptance at hospitals, banks, and municipal offices. Malaysia rolled out its MyDigital ID Superapp backed by blockchain, a template likely to be emulated across ASEAN markets where cross-border labor flows necessitate interoperable IDs. Regional alliances like the Asia Pacific Digital Identity Consortium signal industry commitment to common governance rules despite cultural and linguistic diversity.

Europe continues to steer regulatory direction thanks to eIDAS 2.0. Mandatory European Digital Identity Wallets align more than 440 million residents under standardized cryptography and certification services, enhancing cross-border business, tourism, and public-service delivery. Corporate projects—from PwC Italy’s verifiable-credential infrastructure to Dentsu’s OID4-VC wallet—demonstrate how professional-services firms are already productizing eIDAS alignment ahead of the 2026 deadline. In parallel, smaller markets across South America, the Middle East, and Africa adopt proven blueprints to tackle financial inclusion, often leapfrogging legacy ID card programs through mobile-first strategies. These spillover benefits expand the decentralized identity market beyond early adopters into truly global terrain.

Competitive Landscape

The decentralized identity market remains fragmented, with no single vendor exceeding a double-digit slice of global revenue. Traditional IAM firms—Microsoft, Okta, Ping Identity—are embedding verifiable-credential toolkits into existing policy engines, betting on integration depth as their competitive moat. In parallel, blockchain-native newcomers such as Privado ID (spun out of Polygon) specialize in zero-knowledge workflows that let issuers prove statements—age, accreditation, balance—without disclosing raw data[2]Polygon Labs, “Agglayer Breakout Program,” polygon.technology. This specialization model—protocol layer, wallet layer, orchestration layer—allows best-of-breed alliances rather than winner-takes-all consolidation.

Strategic moves illustrate a race toward high-assurance yet privacy-first frameworks. Microsoft’s ION protocol anchors decentralized identifiers to the Bitcoin network via Sidetree, providing audit-grade immutability without congesting Layer-1 throughput. At the same time, funding volumes validate market appetite: venture investors led by Animoca Brands and Delphi Capital joined Humanity Protocol’s oversubscribed rounds, while PASS gained backing from former Google leadership to build on-chain credit bureaus state regulators can trust. Interoperability alliances—DIF Labs, Trust Over IP Foundation, OpenWallet Foundation—accelerate the convergence necessary to push verifiable credentials into every consumer smartphone.

Because industry roles span standards drafting, wallet UX, key management, verifiable-data registries, and analytics, the scoreboard favors collaboration over zero-sum rivalry. However, barriers to switching remain low thanks to open data models, suggesting that service quality, certification coverage, and user support will define durable leadership positions. The next competitive wave will likely involve turnkey toolchains enabling mid-market enterprises to issue and verify credentials without in-house cryptography expertise, widening revenue pools while amplifying price competition.

Decentralized Identity Industry Leaders

Microsoft Corporation

Ping Identity Holding Corp.

International Business Machines Corporation (IBM)

Okta Inc.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Polygon Foundation introduced the Agglayer Breakout Program, selecting Privado ID and Miden for token incentives that knit identity services into the broader Polygon ecosystem.

- March 2025: PwC Italy partnered with SKChain Advisors to build blockchain-aligned EU digital identity products on Coinbase’s Base layer-2.

- January 2025: Malaysia launched the MyDigital ID Superapp via MYEG and MyDigital ID Solutions, establishing a nationwide blockchain identity ecosystem.

- January 2025: Humanity Protocol completed USD 20 million Series A funding round, bringing total financing to USD 50 million and a USD 1.1 billion valuation for palm-scan-based decentralized verification technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the decentralized identity market as all software platforms, managed services, and developer tools that let individuals or enterprises create, hold, and selectively disclose verifiable credentials using decentralized identifiers anchored on distributed-ledger or equivalent trust frameworks.

Identity wallets, credential issuance services, resolver nodes, and supporting governance layers are included, whereas generic single sign-on suites, centralized KYC utilities, and hardware-only authentication tokens are excluded.

Segmentation Overview

- By Identity Type

- Biometrics

- Non-biometrics

- By Deployment Model

- Cloud-based

- On-premises

- Hybrid

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- IT and Telecommunications

- Retail and E-commerce

- Healthcare

- Media and Entertainment

- Government and Public Sector

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed wallet providers, credential issuers, regulatory architects, and CISO-level buyers across North America, Europe, and Asia-Pacific. These discussions refined adoption curves, average selling prices, and regulatory timing, and they supplied real-world guardrails against optimistic vendor claims.

Desk Research

We began by screening open standards bodies such as W3C, DIF, and ISO for authoritative definitions and adoption metrics, then layered in government portals (NIST, EU eIDAS, UK DCMS, BIS), customs shipments for HSMs, and cybercrime statistics from ENISA and FBI IC3. Annual reports and 10-Ks of leading digital-identity vendors, patent families gathered through Questel, and news archives on Dow Jones Factiva strengthened trend mapping. Company-level revenue splits were validated on D&B Hoovers, while blockchain-node telemetry and published verifiable-credential counts from public ledgers offered usage signals. The sources cited illustrate our approach; many other public domain and subscription materials supported data collection and clarification.

Market-Sizing & Forecasting

A top-down reconstruction started with active digital-identity user pools by sector, adjusted for credential penetration and weighted ASPs. Selective bottom-up roll-ups of supplier revenues and sampled enterprise contract sizes cross-checked totals. Key variables like monthly DID wallet downloads, number of verifiable credentials per user, regional regulatory go-live schedules, enterprise blockchain project counts, and reported identity-fraud losses feed a multivariate regression model that projects revenue to 2030. Forecast error bands narrow once interview-based scenario weights are applied, and any data voids in the supplier checks are bridged through conservative imputation anchored to preceding-year growth medians.

Data Validation & Update Cycle

Triangulated outputs pass an anomaly screen and peer review before sign-off. Our team refreshes the model annually, triggering interim updates whenever material events, such as a major jurisdiction mandating eIDAS 2.0 wallets, shift baseline assumptions.

Why Mordor's Decentralized Identity Baseline Commands Reliability

Published figures differ widely because firms pick dissimilar scopes, base years, and wallet versus platform splits.

We flag these structural choices upfront, so decision-makers see how scope hygiene, refresh cadence, and transparent assumptions shape valuations.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.89 B (2025) | Mordor Intelligence | |

| USD 1.13 B (2023) | Global Consultancy A | Narrow software-only scope and earlier base year omit emerging wallet services |

| USD 1.52 B (2024) | Industry Association B | Excludes enterprise credential issuance spend; relies on vendor press releases without ledger cross-checks |

The comparison shows that smaller estimates stem from tighter scopes or unverified inputs, whereas our disciplined mix of ledger analytics, regulatory tracking, and dual-approach modeling yields a balanced, actionable baseline clients can trust.

Key Questions Answered in the Report

What is the current value of the decentralized identity market?

The decentralized identity market size is USD 7.4 billion in 2026, with projections indicating USD 58.74 billion by 2031 at a 51.34% CAGR.

Which sector is expanding the fastest for decentralized identity adoption?

Healthcare leads growth, expected to post a 23.4% CAGR as patient-controlled records and verifiable clinical credentials gain traction.

Why is Asia-Pacific considered the fastest-growing region?

Government-backed mobile wallets, national blockchain-ID programs, and high smartphone penetration drive a projected 19.9% CAGR through 2031.

How do decentralized identity solutions reduce onboarding costs?

Reusable verifiable credentials enable enterprises to perform Know-Your-Customer checks once and share results across services, slashing repeat verification costs by up to 60%.

What are the main barriers to mainstream consumer adoption?

Fragmented interoperability standards and complicated key-custody processes create friction; simplified UX and global trust frameworks are needed to overcome these hurdles.

Which deployment model dominates and why?

Cloud-based deployments hold 59.05% share because hyperscale infrastructure delivers the elasticity required for compute-heavy zero-knowledge proofs and rapid global rollout.

Page last updated on: