Mobille PC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

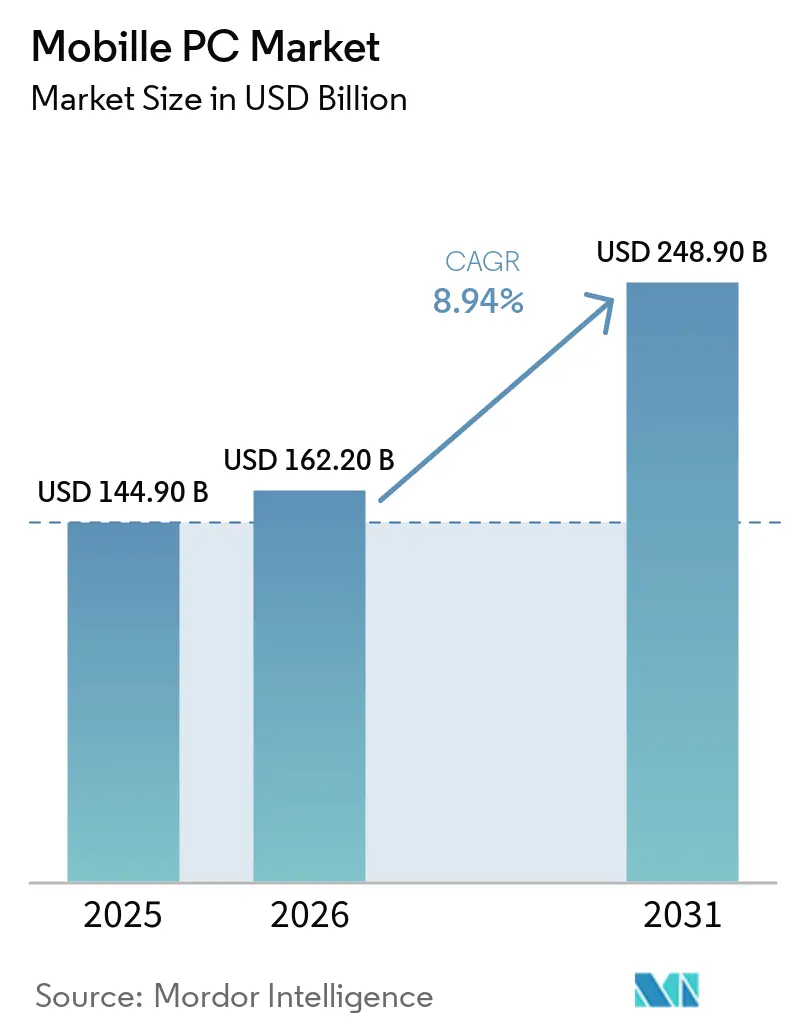

| Market Size (2026) | USD 162.20 Billion |

| Market Size (2031) | USD 248.90 Billion |

| Growth Rate (2026 - 2031) | 8.94% CAGR |

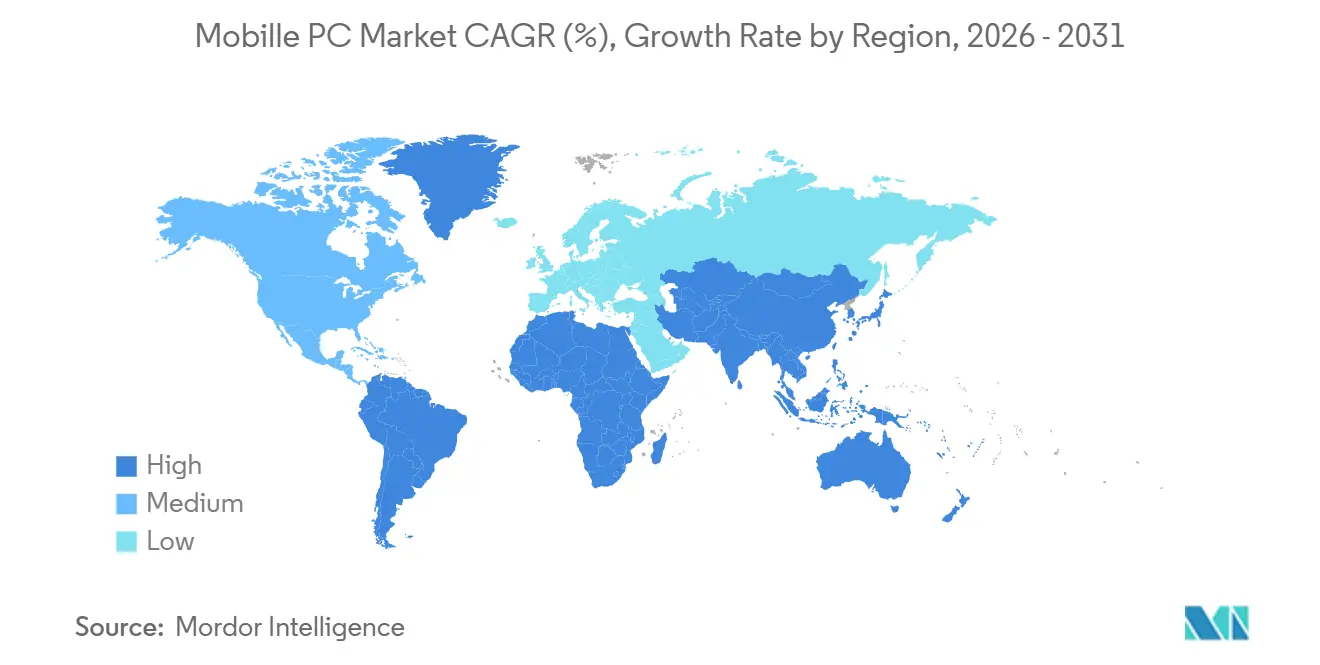

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

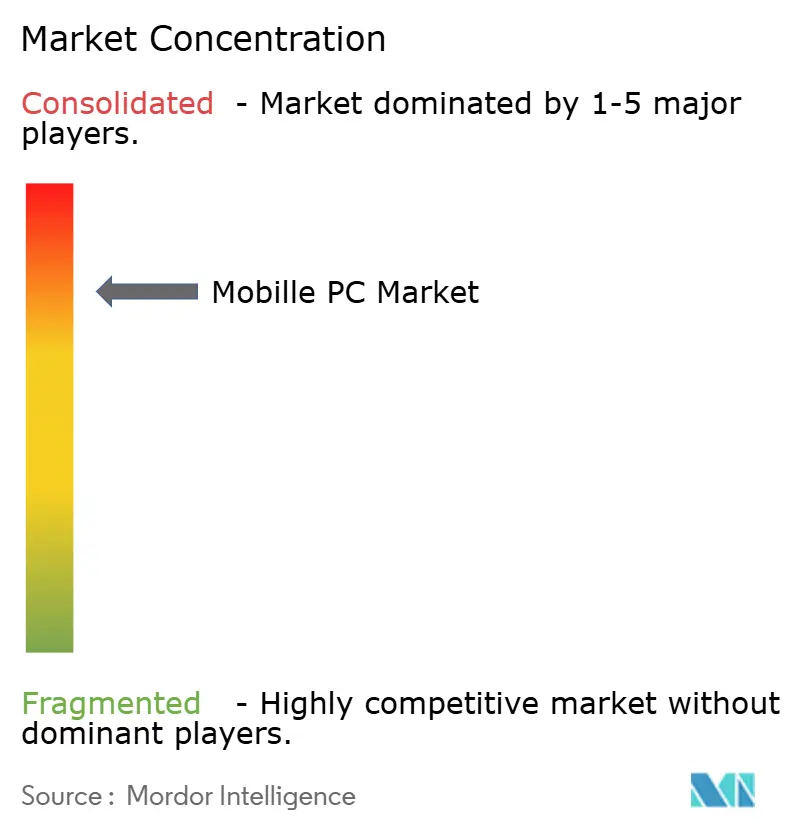

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobille PC Market Analysis by Mordor Intelligence

The Mobile PC market size is projected to expand from USD 144.9 billion in 2025 and USD 162.2 billion in 2026 to USD 248.9 billion by 2031, registering a CAGR of 8.94% between 2026 and 2031. Forced refresh cycles tied to Windows 10 end-of-support, the mainstreaming of on-device artificial intelligence, and tight memory supply are accelerating upgrade decisions across enterprises and small businesses alike. Commercial buyers are front-loading orders before DRAM prices rise further, while consumer demand is moderating as households stretch replacement cycles beyond five years. Vendors with early access to 40 TOPS neural processing units have gained a pricing premium, and sustainability requirements embedded in public-sector tenders are driving interest in modular, repairable designs that extend economic life. Clamshell notebooks still anchor revenue, yet detachables and convertibles command the fastest growth as hybrid work normalizes pen-and-touch workflows.

Key Report Takeaways

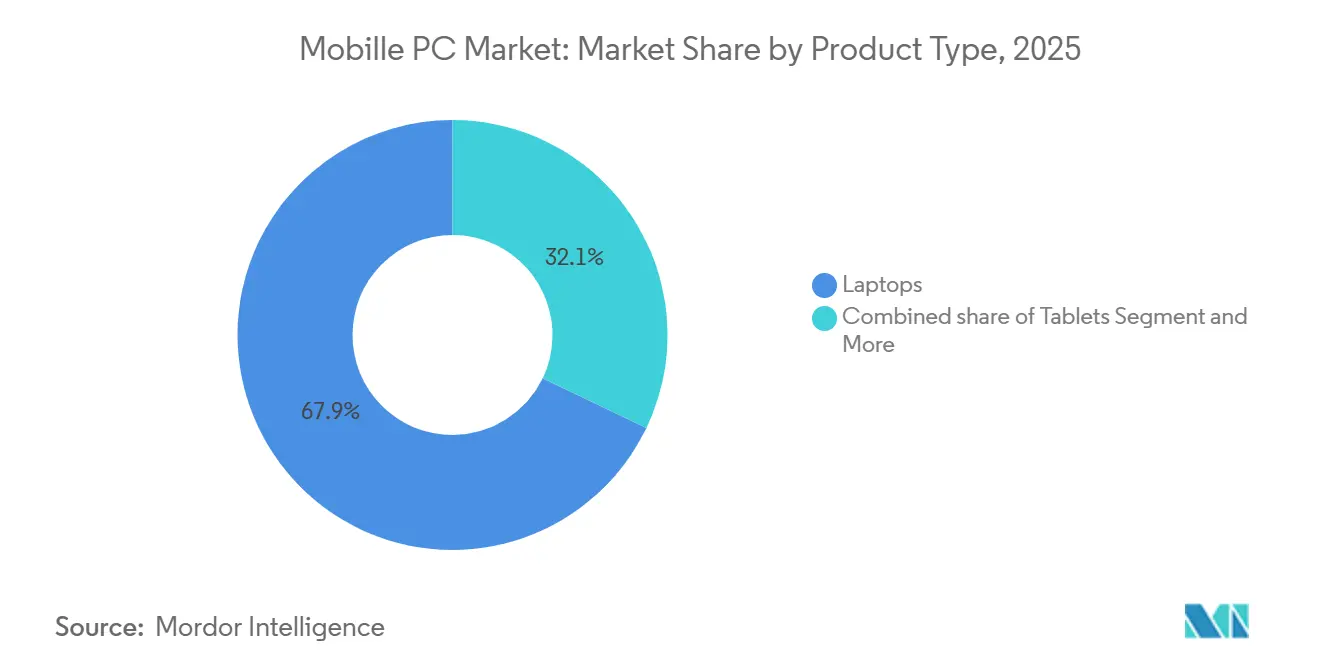

- By product type, laptops led with 67.89% of 2025 revenue, while 2-in-1 detachables are forecast to grow at a 9.8% CAGR through 2031.

- By operating system, Windows retained 73.24% of 2025 revenue and is projected to expand at a 9.3% CAGR through 2031.

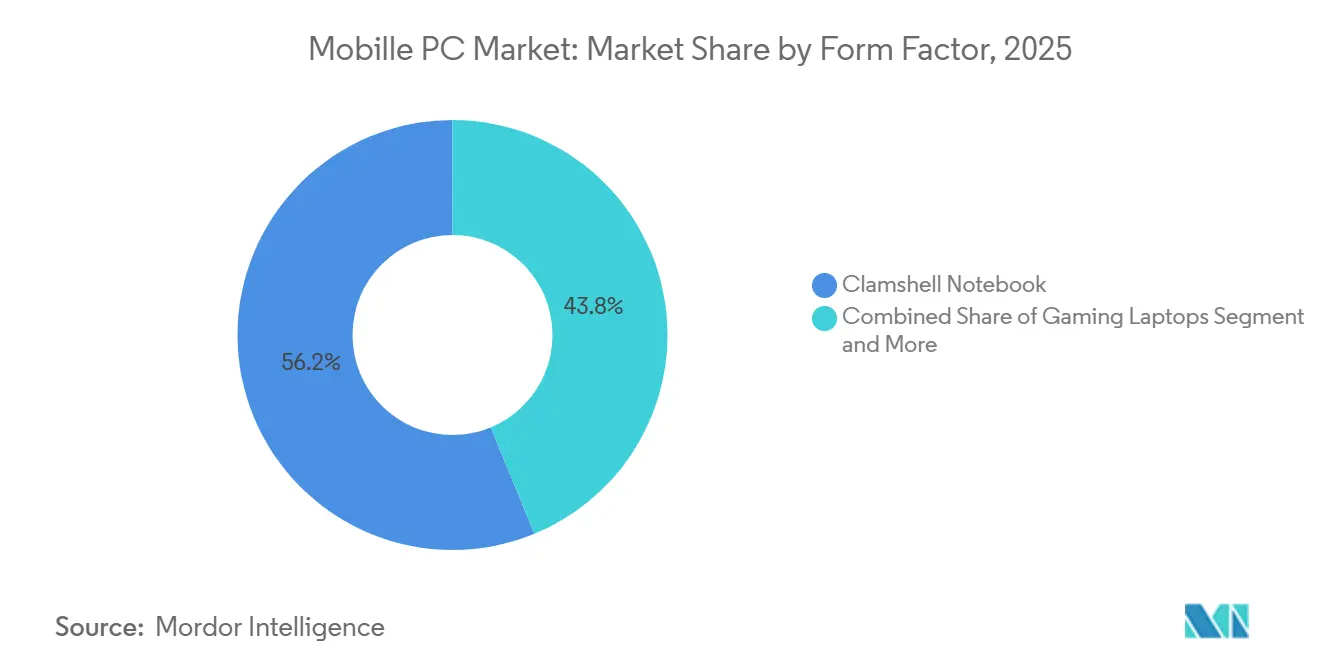

- By form factor, clamshell notebooks captured 56.23% of 2025 revenue; detachable tablets are advancing at a 9.8% CAGR through 2031.

- By end user, small and medium enterprises held 9.26% CAGR growth prospects to 2031, outpacing the consumer segment at 47.59% of 2025 demand.

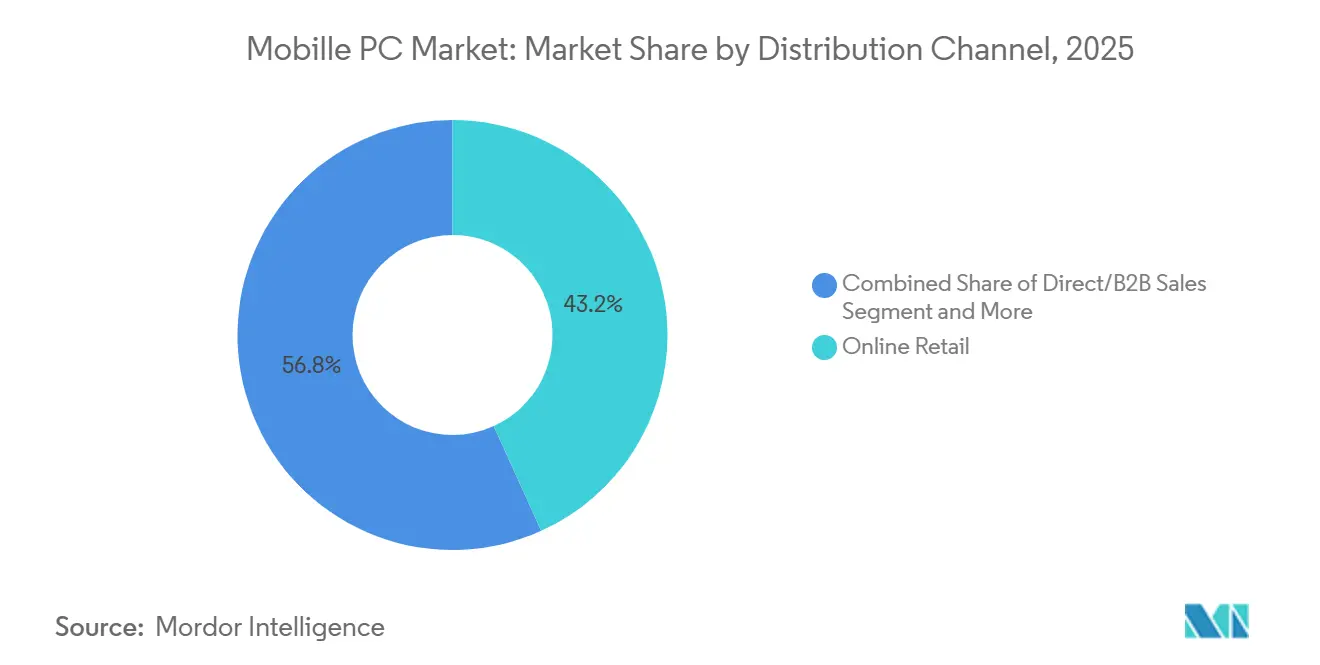

- By distribution channel, direct and business-to-business sales are projected to expand at a 9.8% CAGR through 2031, surpassing online retail’s 43.23% 2025 share.

- By geography, Asia-Pacific accounted for 36.48% of 2025 revenue; the Middle East is expected to rise at a 10.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobille PC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Windows 10 end-of-support driven refresh cycle | +2.80% | Global, concentrated in North America and Europe enterprise | Short term (= 2 years) |

| AI-enabled PCs becoming de-facto purchase criterion | +2.30% | Global, early adoption in Asia-Pacific and North America commercial | Medium term (2-4 years) |

| Chromebook penetration in cost-sensitive education tenders | +1.10% | North America K-12, emerging in South America and Middle East education | Medium term (2-4 years) |

| Memory-price pull-forward procurement | +1.40% | Global, acute in Asia-Pacific manufacturing and North America enterprise | Short term (= 2 years) |

| 5G laptop launches expanding always-connected use cases | +0.90% | North America and Europe field services, Asia-Pacific urban professionals | Long term (= 4 years) |

| Carbon-neutral device mandates in enterprise RFPs | +0.70% | Europe and North America public sector, spill-over to Asia-Pacific multinationals | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Windows 10 End-Of-Support Driven Refresh Cycle

Microsoft ended security updates for Windows 10 on 14 October 2025, leaving over 400 million enterprise endpoints exposed. Extended Security Updates start at USD 61 per device in year one and double annually, making them economically unattractive versus replacement. As a result, most organizations shifted to full hardware refresh cycles. Procurement backlogs in early 2026 extended lead times from 4 to 12 weeks, favoring vendors with established enterprise supply agreements. Additionally, legacy devices fail Windows 11 TPM 2.0 requirements, increasing replacement costs by up to 30%.[1] Michael Dell, “AI PCs in Asia Pacific Adoption Study,” Dell Technologies, delltechnologies.com

AI-Enabled PCs Becoming De-Facto Purchase Criterion

Neural processing units exceeding 40 TOPS shifted artificial intelligence from a premium feature to a baseline specification in 2025, with Qualcomm, Intel, and AMD all crossing this threshold. This enables real-time transcription, summarization, and background blur directly on-device without cloud dependency. A regional survey indicates 48% of Asia-Pacific organizations had deployed AI PCs by end-2025. Enterprises realize up to 80% cost savings on inference workloads while avoiding cross-border data residency compliance costs, as processing remains local, improving latency, security, and operational efficiency across enterprise environments.[2]TrendForce Team, “DRAM and NAND Market Outlook 2025-2027,” TrendForce, trendforce.com

Chromebook Penetration In Cost-Sensitive Education Tenders

K-12 districts accelerated Chromebook adoption in 2025 and 2026 due to low IT overhead and automatic updates, reducing the total cost of ownership. However, street prices increased from USD 299 to USD 459 following the reintroduction of 54% laptop tariffs in early 2026, adding approximately USD 4.2 billion to 5-year U.S. school budgets. This cost pressure is driving institutions in South America and the Middle East to evaluate cloud-centric education models, replicating North America’s approach to centralized device management, scalability, and lower long-term operational complexity.[3]Ana Swanson, “Tariffs Push Laptop Prices Higher,” Reuters, reuters.com

Memory-Price Pull-Forward Procurement

DRAM and NAND prices rose 40% to 70% during 2025 as data centers and AI accelerators absorbed roughly 70% of global supply. Memory now accounts for about 35% of notebook bill of materials cost, compressing gross margins by around 3 percentage points. Enterprises responded by locking in multi quarter procurement agreements to secure supply continuity. However, overbuying risk increased, creating potential inventory overhang and working capital strain if demand softens or component prices normalize in subsequent quarters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DRAM and NAND allocation to AI and data-center depressing supply | -1.80% | Global, acute in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Tariff volatility distorting quarterly shipments | -1.20% | North America imports, spill-over to South America and Europe | Short term (≤ 2 years) |

| Arm-x86 software compatibility gaps slowing adoption | -0.90% | Global enterprise, concentrated in North America and Europe IT departments | Medium term (2-4 years) |

| Extended device replacement cycles in mature markets | -1.40% | North America and Europe enterprise, emerging in Asia-Pacific commercial | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

DRAM And NAND Allocation To AI And Data-Center Depressing Supply

Memory manufacturers prioritized high-bandwidth products for servers, leaving client devices with roughly 60% of the required supply. This imbalance drove laptop average selling prices up by 15% to 30%, disproportionately impacting education and entry-level consumer segments. Enterprises unable to secure sufficient allocations are extending Windows 10 usage beyond the end of support, increasing cybersecurity exposure and compliance risk. The constraint is expected to persist until additional fabrication capacity becomes operational, with meaningful supply relief anticipated only by late 2027.

Tariff Volatility Distorting Quarterly Shipments

A 54% duty on China-assembled laptops and a 25% semiconductor levy introduced in early 2026 triggered shipment surges ahead of implementation, followed by inventory corrections that distorted year-on-year comparisons. Vendors are actively relocating final assembly to Vietnam, Mexico, and India to mitigate tariff exposure and diversify supply chains. However, ramp-up of production quality in new locations can take up to 18 months, creating execution risk. Ongoing policy uncertainty is also delaying capital investment decisions, as manufacturers remain cautious about committing to long-term capacity expansion.[4]Monica Chen, “Memory Makers Shift Output to AI Servers,” Bloomberg, bloomberg.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Detachables Erode Laptop Supremacy

Laptops accounted for 67.89% of 2025 revenue, reinforcing their central role in enterprise workflows and standardized IT environments. The mobile PC segment for 2-in-1 detachables is projected to grow at a 9.8% CAGR from 2026 to 2031, about 1 percentage point above overall market growth. Tablets remain preferred in healthcare and field operations, while Chromebooks continue to address education demand due to low management overhead. Qualcomm Snapdragon-powered detachables now deliver up to 23 hour battery life in sub-1 kg designs, eliminating prior performance and mobility trade-offs.

This shift is reflected in vendor product strategies, with Microsoft Surface Pro, Dell Latitude 7350, and HP EliteBook X increasingly centered on detachable form factors with removable keyboards and active pen support. Tablets face substitution risk from large-screen smartphones, and Chromebook pricing advantages have narrowed following tariff increases. However, detachables continue to gain enterprise traction as professionals adopt pen-enabled workflows for whiteboarding, note-taking, and collaboration in hybrid work environments, improving productivity and device utilization.

By Operating System: Windows Retains Ecosystem Lock-In

Windows captured 73.24% of the revenue share in 2025, and its mobile PC footprint is set to expand as enterprises transition to NPU-ready Windows 11 systems at a 9.3% CAGR through 2031. macOS retains strength among developers and creative professionals, while Chrome OS continues to serve cost-sensitive education segments. Linux remains below 5% share, largely confined to specialized technical environments. AI workloads, security requirements, and enterprise standardization around Windows ecosystems are driving the upgrade cycle.

Copilot+ certification, requiring 40 TOPS NPUs, reinforces Windows ecosystem lock-in by incentivizing early hardware adoption and giving Microsoft an estimated 18-month lead over competitors before they reach comparable performance. Chrome OS momentum weakened as tariff-driven cost increases reduced Chromebook affordability, while macOS benefits from Apple M-series silicon efficiency gains but remains constrained by enterprise-scale management limitations and compatibility considerations.

By Form Factor: Clamshells Anchor Revenue, Detachables Lead Growth

Clamshell notebooks delivered 56.23% of 2025 form factor revenue, supported by established ergonomics, keyboard comfort, and thermal headroom required for sustained enterprise workloads such as development, analytics, and multitasking. Their standardized design aligns well with corporate IT procurement and lifecycle management practices. However, detachable tablets are projected to grow at a 9.8% CAGR through 2031, the fastest among form factors, driven by increasing demand for portability, touch interfaces, and pen enabled collaboration. Hybrid work environments are accelerating adoption as users prioritize flexibility without compromising baseline productivity performance.

Gaming laptops and rugged devices remain specialized segments with clearly defined value propositions. Gaming systems prioritize high performance computing with discrete GPUs, advanced cooling, and high refresh displays, typically sacrificing portability and battery efficiency. Rugged devices comply with MIL STD 810H standards, addressing durability needs in sectors such as defense, utilities, and field services. Meanwhile, clamshell margins are under pressure due to rising memory costs and component inflation. Vendors are responding by shifting portfolios toward premium ultraportables and detachable formats, where differentiation, pricing power, and feature driven value propositions remain more defensible.

By End User: SMEs Accelerate, Consumers Plateau

Consumer buyers represented 47.59% of 2025 demand, reflecting strong baseline volume driven by personal productivity, entertainment, and remote work needs. However, small and medium enterprises are projected to grow at a 9.26% CAGR through 2031 as they increasingly adopt device-as-a-service models that convert capital expenditure into predictable operating costs. Large enterprises continue to rely on multi-year procurement contracts, while education favors Chromebook fleets for cost efficiency. Government buyers prioritize sustainability, embedding carbon-neutral and energy-efficiency criteria into large-scale procurement frameworks and vendor selection processes.

AI-enabled notebooks are gaining traction among SMEs, as on-device inference reduces reliance on cloud infrastructure, avoiding compliance costs and delivering savings of up to USD 13,000 over 3 years. Consumer segment growth remains constrained by longer replacement cycles and substitution by high-end smartphones. Education demand shows variability due to funding cycles and tariff-driven price fluctuations, creating procurement uncertainty. Vendors must balance pricing strategies, financing models, and feature differentiation to capture growth across segments with distinct purchasing behaviors and budget sensitivities.

By Distribution Channel: Direct Sales Capture Margin

Online retail accounted for 43.23% of 2025 revenue, driven by price transparency, wide assortment, and convenience. However, direct and B2B channels are projected to grow at a 9.8% CAGR through 2031 as vendors bypass intermediaries to protect margins and bundle device-as-a-service offerings. Offline retail remains relevant for customers who require hands-on evaluation, particularly for higher-value purchases. Value-added resellers continue to play a role in enterprise deployments, offering integration, configuration, and lifecycle management services for complex, large-scale rollouts.

The share of direct channels is increasing as enterprise procurement portals enable IT teams to customize configurations, pricing, and service bundles without intermediary markups. While online channels face margin pressure from free shipping, returns, and price competition, direct leasing and subscription models provide predictable, recurring revenue streams. These multi-year contracts also improve customer retention and lifecycle visibility. Vendors are strategically shifting toward direct engagement models to enhance control over pricing, customer relationships, and long-term revenue stability.

Geography Analysis

Asia Pacific generated 36.48% of 2025 revenue, supported by strong volume contributions from China at 42.1 million units and India at 15.9 million units, with India growing 10.2% year over year despite ongoing memory supply constraints. The region shipped 106.6 million units in 2025 but is projected to decline to 92.0 million in 2026 due to timing effects from tariffs that distorted prior demand cycles. Procurement normalization, pricing volatility, and delayed enterprise refresh cycles are expected to weigh on near-term shipment performance across key regional markets.

The Middle East has the fastest growth trajectory, with a projected 10.46% CAGR through 2031, driven by sovereign AI initiatives and large-scale digital infrastructure investments. Government-backed mega projects prioritize locally assembled devices capable of supporting on-device inference to meet data sovereignty requirements. Lenovo’s expansion in Riyadh strengthens its position for public-sector contracts. Procurement criteria in Gulf markets increasingly emphasize Arabic-language natural language processing capabilities and carbon-neutral certifications, reflecting both localization needs and sustainability mandates shaping vendor selection strategies.

North America and Europe are experiencing slower growth as enterprises extend device lifecycles beyond traditional 3-year replacement cycles using telemetry-driven asset management tools. Tariff uncertainty continues to inflate procurement costs, while regulatory frameworks such as the UK Procurement Policy Note 006 favor modular device designs with transparent lifecycle emissions reporting. South America and Africa remain smaller in absolute volume but show growth potential through education digitization programs that prioritize cost-effective Chromebooks and entry-level Windows devices to expand digital access and support workforce development initiatives.

Competitive Landscape

The top five suppliers, Lenovo, HP, Dell, Apple, and ASUS, account for roughly 65% to 70% of global revenue, indicating moderate market concentration with scale advantages in procurement, distribution, and enterprise relationships. Ongoing memory shortages are forcing OEMs to prepay for DRAM and NAND at premiums of 40% to 70% compared to 2024 levels, compressing margins and raising entry barriers for smaller competitors. Larger vendors are better positioned to absorb cost volatility, while smaller players face working capital strain, reduced pricing flexibility, and increased exposure to supply chain disruptions.

Strategic responses center on expanding device-as-a-service portfolios, shifting final assembly to tariff-neutral locations, and securing 40 TOPS-class silicon to meet Copilot+ readiness requirements. Framework Computer targets a modular niche aligned with sustainability mandates, while Arm-based Windows devices offer 20-plus-hour battery life but continue to face compatibility challenges with legacy enterprise software and drivers. These constraints limit near-term enterprise-scale adoption despite clear efficiency gains, creating a transitional phase in architecture standardization across the mobile PC ecosystem.

HP and Dell are embedding carbon accounting into their service offerings to align with enterprise ESG requirements, while Lenovo is expanding localized assembly in Gulf markets to capture public-sector demand. Apple maintains a performance-per-watt advantage with its M-series silicon, particularly in creative and professional workloads. Regional challengers such as Xiaomi and Huawei leverage vertically integrated supply chains to offer cost-competitive alternatives. Gaming-focused vendors like MSI and Razer are adapting by integrating AI frame generation via NPUs, reducing reliance on power-intensive discrete GPUs.

Mobille PC Industry Leaders

Lenovo Group Limited

HP Inc.

Dell Technologies Inc.

Apple Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microsoft released Windows 11 24H2, enabling Copilot+ APIs that require 40 TOPS NPUs.

- January 2026: Dell launched the Latitude 7350 2-in-1 featuring Intel Core Ultra chips and 45 TOPS NPUs for hybrid workers.

- February 2026: HP expanded Carbon Neutral Computing Services to bundle lifecycle offsets with device-as-a-service subscriptions.

- March 2026: Qualcomm began shipping the Snapdragon X2 Elite with 80 TOPS NPU and 25-hour battery life in fanless designs.

Global Mobille PC Market Report Scope

The Mobile PC Market comprises portable personal computing devices designed for untethered, on-the-go use, powered by integrated rechargeable batteries, and capable of running full desktop-class operating systems, including Windows, macOS, ChromeOS, and Linux. The market is measured by revenue (USD), covering devices sold through all distribution channels, including offline retail, e-commerce, direct enterprise procurement, and government tenders.

The Mobile PC Market Report is Segmented by Product Type (Laptops, Tablets, 2-in-1 Detachables, and Chromebooks), Operating System (Windows, macOS, Chrome OS, Linux and Others), Form Factor (Clamshell Notebook, Convertible 2-in-1, Detachable Tablet, Rugged/Industrial Laptop, and Gaming Laptop), End User (Consumer, Small and Medium Enterprises, Large Enterprises, Education and Government and Public Sector), Distribution Channel (Online Retail, Offline Retail, Direct/B2B Sales, and Value-Added Resellers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, anddAfrica). The Market Forecasts are Provided in Terms of Value (USD).

| Laptops |

| Tablets |

| 2-in-1 Detachables |

| Chromebooks |

| Windows |

| macOS |

| Chrome OS |

| Linux and Others |

| Clamshell Notebook |

| Convertible 2-in-1 |

| Detachable Tablet |

| Rugged/Industrial Laptop |

| Gaming Laptop |

| Consumer |

| Small and Medium Enterprises |

| Large Enterprises |

| Education |

| Government and Public Sector |

| Online Retail |

| Offline Retail |

| Direct/B2B Sales |

| Value-Added Resellers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Type | Laptops | |

| Tablets | ||

| 2-in-1 Detachables | ||

| Chromebooks | ||

| By Operating System | Windows | |

| macOS | ||

| Chrome OS | ||

| Linux and Others | ||

| By Form Factor | Clamshell Notebook | |

| Convertible 2-in-1 | ||

| Detachable Tablet | ||

| Rugged/Industrial Laptop | ||

| Gaming Laptop | ||

| By End User | Consumer | |

| Small and Medium Enterprises | ||

| Large Enterprises | ||

| Education | ||

| Government and Public Sector | ||

| By Distribution Channel | Online Retail | |

| Offline Retail | ||

| Direct/B2B Sales | ||

| Value-Added Resellers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Mobile PC market be by 2031?

The Mobile PC market size is forecast to reach USD 248.9 billion by 2031, growing at an 8.94% CAGR from 2026 to 2031 according to Mordor Intelligence.

Which operating system holds the highest revenue share?

Windows captured 73.24% of global revenue in 2025 and is projected to extend its lead through 2031 as enterprises migrate to Windows 11 devices with 40 TOPS NPUs.

What segment is growing the fastest within form factors?

Detachable tablets are projected to rise at a 9.8% CAGR through 2031, the fastest among form factors, as hybrid work popularizes pen-enabled collaboration.

Why are SMEs upgrading PCs faster than consumers?

Small and medium enterprises adopt device-as-a-service and AI-ready notebooks to convert capital expense into predictable leases and lower cloud inference costs, driving a 9.26% CAGR to 2031.

Which region is expected to see the quickest growth?

The Middle East leads with a forecast 10.46% CAGR through 2031, spurred by sovereign-AI mandates that demand locally assembled, on-premise inference solutions.

How are memory shortages affecting Mobile PC prices?

DRAM and NAND allocation to data-center hardware lifted client-device memory costs by 40% to 70% in 2025, inflating laptop average selling prices by up to 30% and forcing enterprises to secure long-term supply contracts.

Page last updated on: