Industrial PC (IPC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

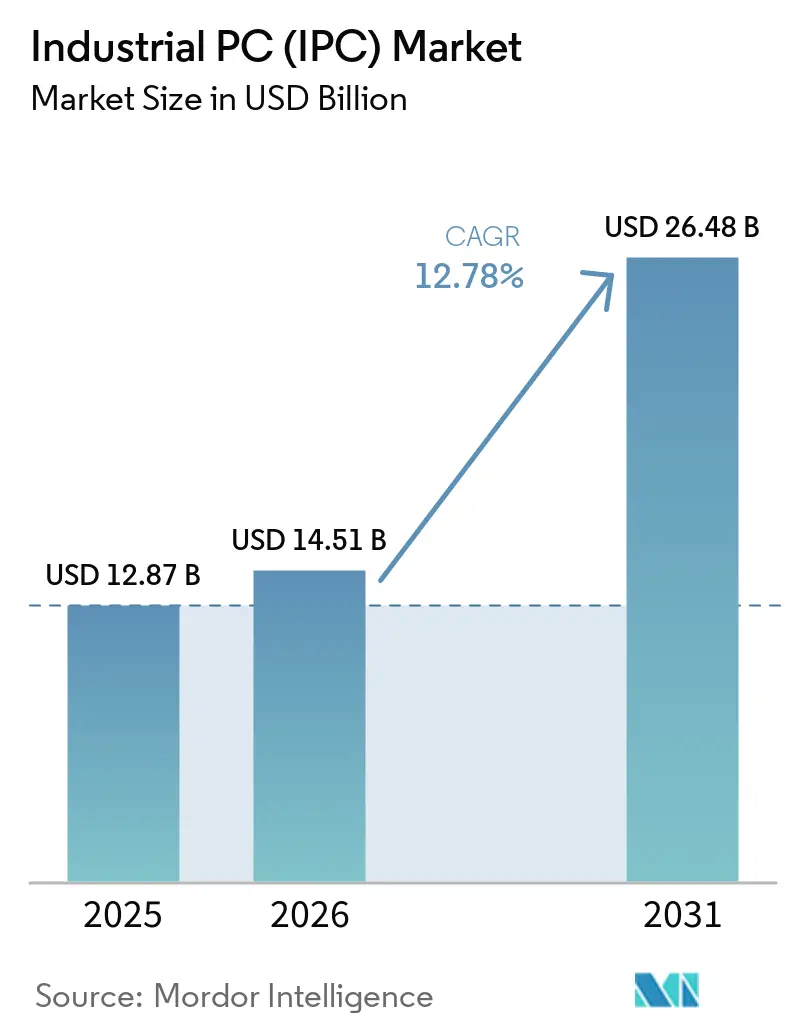

| Market Size (2026) | USD 14.51 Billion |

| Market Size (2031) | USD 26.48 Billion |

| Growth Rate (2026 - 2031) | 12.78% CAGR |

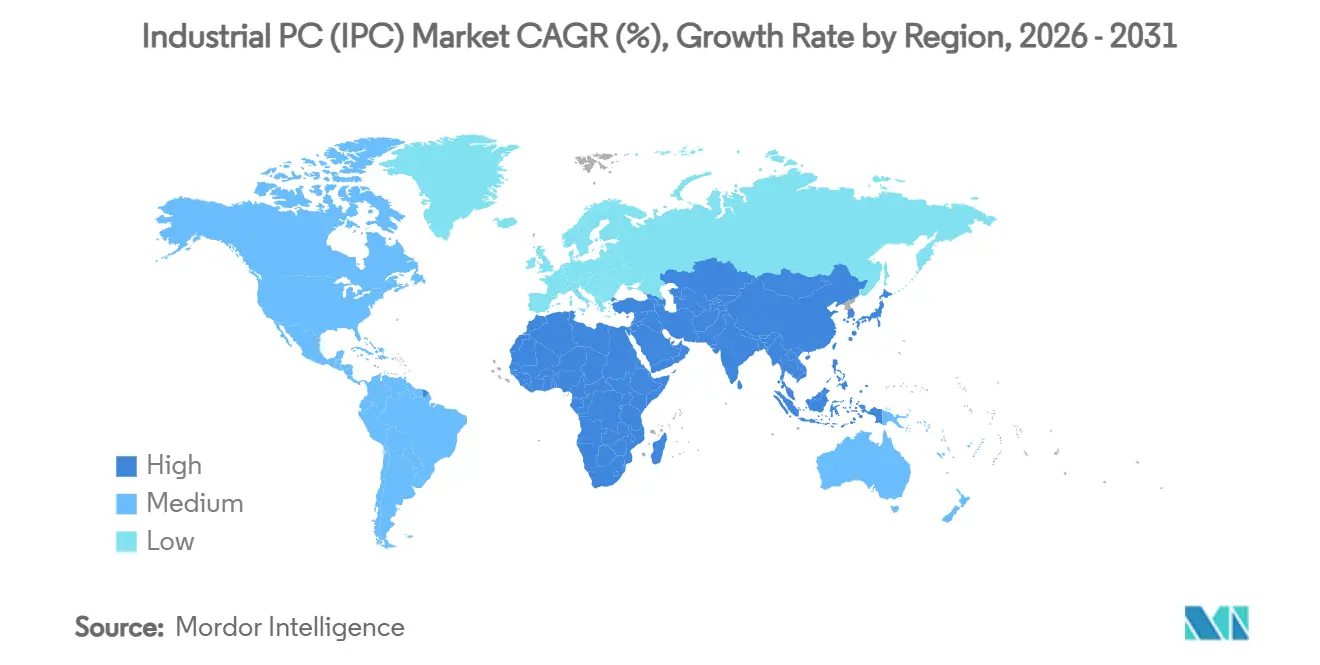

| Fastest Growing Market | Asia Pacific |

| Largest Market | Africa |

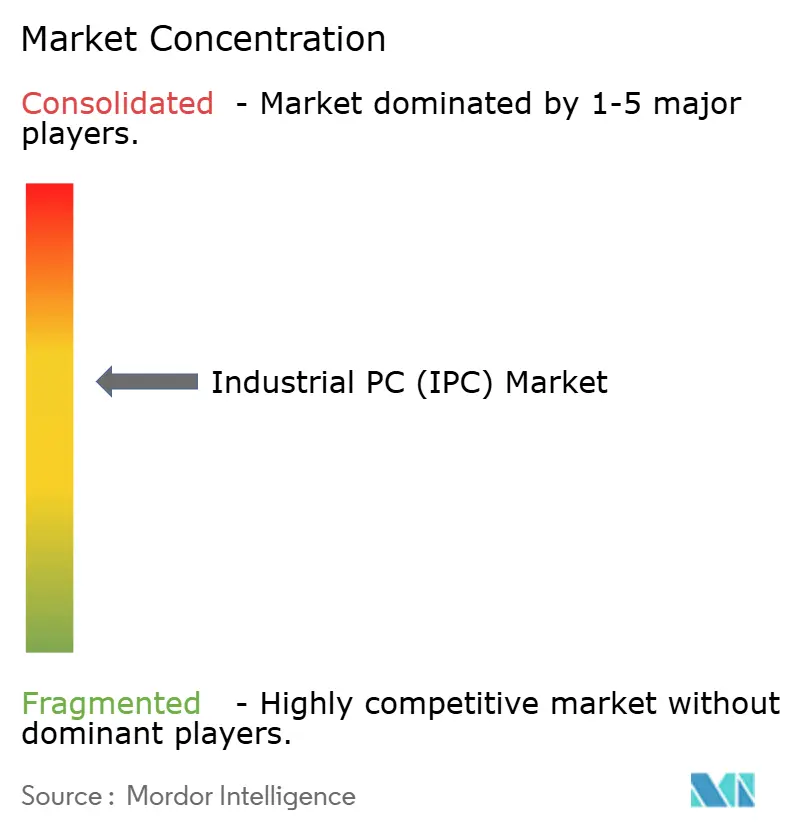

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial PC (IPC) Market Analysis by Mordor Intelligence

The industrial pc market size is expected to increase from USD 5.49 billion in 2025 to USD 5.87 billion in 2026 and reach USD 8.44 billion by 2031, growing at a CAGR of 7.53% over 2026-2031. Real-time data orchestration across discrete manufacturing is accelerating procurement as plant engineers seek sub-millisecond synchronization for robotics and digital twins. Modular architectures, remote device management, and bundled middleware are shortening commissioning cycles, while edge-AI workloads are migrating from cloud servers to GPUs embedded in fanless controllers. Semiconductor fabs, renewable-energy microgrids, and vehicle electrification lines remain the highest-value use cases because they demand deterministic control in harsh environments. Competitive intensity is rising because Tier-1 vendors preload software subscriptions that offset thinning hardware margins, compelling niche suppliers to differentiate through rapid customization, cybersecurity hardening, and IEC 62443 certifications.

Key Report Takeaways

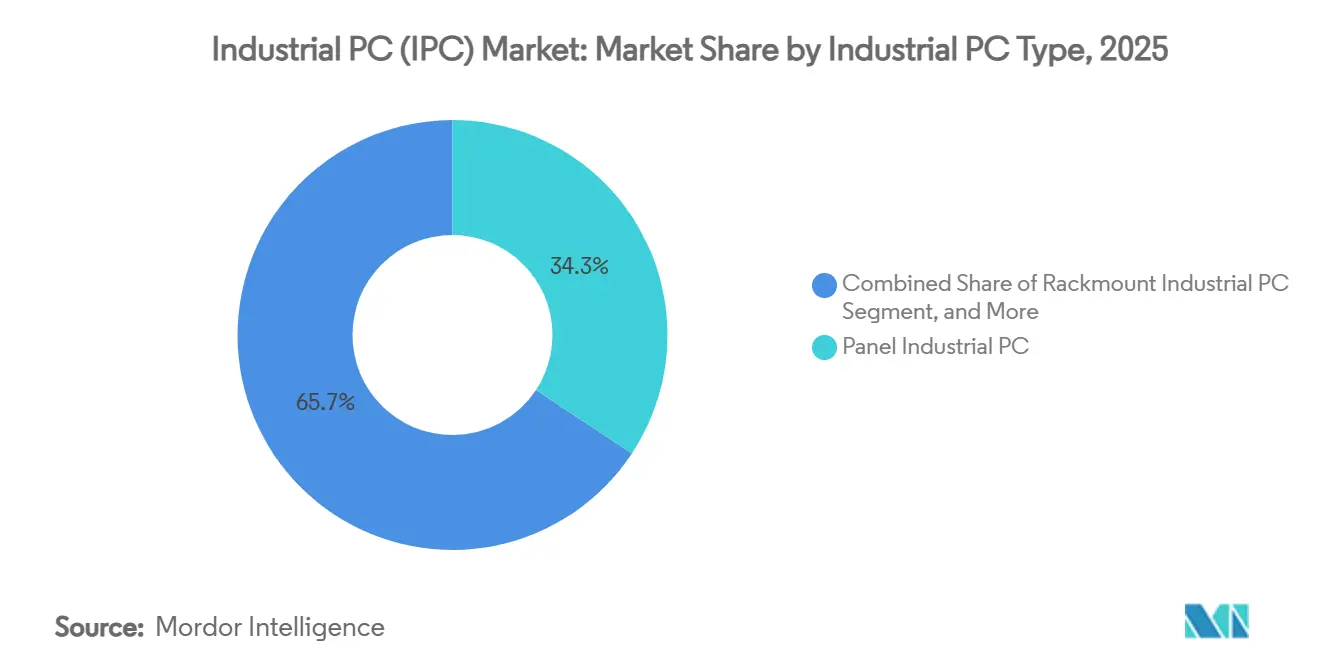

- By industrial PC type, panel industrial PCs held 34.29% of the industrial pc market share in 2025, while embedded box IPCs are projected to expand at an 8.53% CAGR through 2031.

- By end-user industry, electronics and semiconductor fabrication absorbed 24.18% of shipments in 2025, whereas renewable energy and utilities is forecast to advance at an 8.13% CAGR to 2031.

- By component, CPUs accounted for 28.67% of the industrial PC market in 2025, and GPUs are projected to grow at a 7.93% CAGR through 2031.

- Direct sales accounted for 42.91% of 2025 revenue, yet e-commerce platforms are scaling at an 8.23% CAGR as procurement teams favor rapid-prototyping orders.

- By geography, Asia-Pacific commanded 46.39% of 2025 revenue, and Africa is on track for a 7.53% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial PC (IPC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Industry 4.0 in Discrete Manufacturing | +2.1% | Global with clusters in Germany, United States, China, Japan | Medium term (2-4 years) |

| Rising Demand for Rugged Computing at the Edge in Harsh Environments | +1.8% | Asia-Pacific core, Middle East oil and gas, Africa mining belt | Medium term (2-4 years) |

| Expanding Deployment of AI-Enabled Vision Inspection Systems | +1.5% | Taiwan, South Korea, United States electronics hubs | Short term (≤ 2 years) |

| Proliferation of 5G and Time-Sensitive Networking for Real-Time Control | +1.3% | North America and Europe automotive corridors, China smart factories | Long term (≥ 4 years) |

| Growth of Renewable Energy Microgrids Requiring Robust Control | +0.9% | Africa, India, Latin America off-grid installations | Long term (≥ 4 years) |

| Emergence of Modular, Upgradeable IPC Platforms for Lifecycle Extension | +0.7% | Global early adoption in automotive and aerospace | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Industry 4.0 in Discrete Manufacturing

Manufacturers are embedding IPCs into machine-tool controllers, automated guided vehicles, and digital-twin gateways to achieve deterministic cycle times. Dual-redundant power supplies, conformal-coated PCBs, and OPC UA servers are now pre-installed, cutting commissioning time from weeks to days. Survey data show that operators at Level 3 digital maturity deploy nearly 4 times as many IPCs per production cell as those at Level 1, confirming a direct link between automation depth and controller density. Emerson launched its PACSystems RXi2 industrial PC in early 2025 with dual Intel Core processors and TSN-ready Ethernet ports, targeting automotive body-shop lines where weld-gun sequencing must coordinate across 40 robots within a 10-millisecond window.[1]Emerson Automation Solutions, “PACSystems RXi2 Industrial PC Launch,” emerson.com Vendors that offer turnkey time-sensitive networking and MQTT brokers gain preference because they align with enterprise cloud strategies. As discrete manufacturers converge their operational and information technology stacks, demand for scalable compute modules that match the 15-year lifecycle of CNC machines is steadily rising.

Rising Demand for Rugged Computing at the Edge in Harsh Environments

Oil refineries, mining pits, and outdoor substations require controllers that withstand temperature swings from -40 °C to 70 °C, 50G shock loads, and IP66 ingress protection. Fanless magnesium-alloy chassis dissipate up to 65 W without throttling GPUs that run vision analytics next to blast furnaces or drilling heads. ARBOR Technology introduced its ARTS-7670 fanless box PC in mid-2025, certified to MIL-STD-810H for vibration and featuring a magnesium-alloy chassis that dissipates 65 watts passively, enabling deployment on offshore drilling platforms where dust and salt spray corrode conventional enclosures within months.[2]ARBOR Technology Corp., “ARTS-7670 Fanless Box PC Product Announcement,” arbor-technology.com Projected-capacitive touchscreens usable with heavy gloves remove a long-standing ergonomics barrier in chemical plants. Compliance with ATEX and IECEx certification is a baseline specification across Middle East petrochemical complexes. Edge inference accelerates the trend because on-device analysis eliminates latency that can trigger safety trips when robotics operate inside explosive atmospheres.

Expanding Deployment of AI-Enabled Vision Inspection Systems

Manufacturers replace manual quality checks with GPU-accelerated IPCs that run convolutional neural networks in under 50 milliseconds, improving first-pass yield and slashing rework. Vision-system sales to electronics assemblers advanced at double-digit rates in 2025 as solder-joint inspection moved from the human eye to the camera. Aerospace composites, smartphone modules, and automotive paint lines all report defect-escape reductions that deliver multi-million-dollar savings per plant. Low-code platforms bundled with IPCs let line engineers train models without data-science staff, widening adoption among Tier-2 suppliers. Predictive maintenance modules piggyback on the same hardware, analyzing vibration signatures to schedule bearing changes hours before catastrophic failure.

Proliferation of 5G and Time-Sensitive Networking for Real-Time Control

Hybrid wired-wireless topologies anchored by 5G-TSN gateways guarantee sub-5-millisecond latency, enabling mobile robots to share networks with fixed machinery. Deterministic packet scheduling survives even when a third of nodes communicate over radio links, a breakthrough for factories that rearrange lines weekly. TSN traffic shaping embedded in industrial Ethernet switches prioritizes safety frames over IT packets, protecting emergency-stop signals from congestion. Field pilots in automotive final-assembly plants show packet-loss reductions of more than 90% in high EMI zones near induction welders. As private 5 G licenses expand, demand for IPCs with integrated modems and synchronized clocks accelerates in brownfield retrofits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Costs for SMEs | -1.2% | Global, acute in South America, Southeast Asia, Eastern Europe | Short term (≤ 2 years) |

| Supply Chain Volatility in Semiconductor Components | -0.9% | Global with ripple effects from Taiwan and South Korea fabs | Medium term (2-4 years) |

| Cybersecurity Vulnerabilities in Legacy Industrial Networks | -0.6% | North America and Europe installed base, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Intense Price Competition Driving Margin Compression | -0.5% | Global, concentrated in commodity panel IPC segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Costs for SMEs

Small and medium enterprises require internal rates of return above 25% to justify controller purchases, yet financing often carries interest rates double those available to large manufacturers. A median IPC deployment costs USD 87,000 per line, or more than a year of gross profit for a 50-employee contract plant. Surveys across India, Mexico, and Southeast Asia consistently rank capital cost as the primary adoption barrier, surpassing skills gaps and cybersecurity fears. Pay-per-use leasing models are emerging but remain limited to borrowers with audited statements and long-term offtake contracts. Consequently, two-thirds of North American job shops processing under 50,000 units annually remain outside the immediate addressable base.

Supply Chain Volatility in Semiconductor Components

Tungsten shortages for high-bandwidth memory substrates are extending lead times for GPU-accelerated boards, forcing redesigns that delay product launches by up to 6 months. Allocation delays exceeded 16 weeks for 41% of vendors in 2024 as foundries prioritized consumer chips over industrial-temperature variants. Firms that rely on single-source fabs experienced revenue swings triple those of peers who qualified alternate foundries, underscoring the value of multi-supplier strategies. Lead times for industrial-grade NVMe SSDs with power-loss protection now stretch past 30 weeks, prompting some integrators to accept lower performance or revert to SATA. Although new 300-millimeter fabs in the United States and Europe are ramping, geopolitical export controls threaten fresh disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Industrial PC Type: Embedded Box Designs Outpace Panel Systems

Embedded box controllers contributed an 8.53% compound annual growth rate (CAGR) to the industrial PC market during the forecast period from 2026 to 2031. This growth highlights the increasing demand for modular compute-on-modules, designed to extend the operational lifecycles of industrial PCs beyond 10 years. These controllers are particularly valued in industries where long-term reliability and adaptability are critical. Additionally, panel systems maintained a significant position in the industrial PC market, holding 34.29% of the market share in 2025. This dominance is attributed to the suitability of integrated touchscreens for various industrial applications, including packaging lines, batch reactors, and wash-down food processing plants. The ability of panel systems to withstand harsh environments while providing user-friendly interfaces makes them a preferred choice in these sectors.

Rackmount configurations remain favored in centralized utility control rooms where hot-swap drive bays and IPMI remote management simplify maintenance. DIN-rail IPCs occupy minimal panel space in electrical cabinets and continue to win building automation projects, while thin-client units hold niche positions in pharmaceutical cleanrooms that restrict the use of moving parts. Modular rackmount designs that host multiple compute modules let manufacturers dedicate separate hardware to recipe control, audit trails, and analytics without cross-contamination, reinforcing demand for scalable chassis.

By End-User Industry: Electronics Leads, Renewable Energy Accelerates

Electronics and semiconductor fabrication accounted for 24.18% of 2025 shipments as fabs upgraded to advanced packaging lines that require sub-micron motion control. This growth is driven by rising demand for high-performance chips and the need for greater precision in manufacturing processes. Renewable energy and utilities, in contrast, are projected to grow at an 8.13% CAGR, supported by advancements in battery-storage orchestration, the adoption of microgrid controllers, and the integration of hydrogen-electrolyzer balance-of-plant systems to enhance energy efficiency and sustainability.

Automotive, pharmaceutical, and food-and-beverage plants each account for mid-single-digit shares of the industrial pc market size. These industries are embedding controllers in various applications, such as welding cells in automotive manufacturing, cleanrooms in pharmaceutical production, and pasteurization loops in food and beverage processing. Aerospace and defense, industrial machinery, and process industries are increasingly adopting IPCs that meet stringent certifications such as MIL-STD-461 or ATEX Zone 2. This trend is driving incremental demand for specialized components, including conformal-coated boards and wide-temperature components, to ensure reliability and performance in harsh and regulated environments.

By Component: GPUs Capture Momentum as Edge-AI Proliferates

CPUs remained the largest slice at 28.67% of 2025 revenue, maintaining their dominance in the industrial PC market due to their critical role in processing and computational tasks. Kontron's KBox B-301-RPL, launched in early 2025, pairs an Intel Raptor Lake processor with an NVIDIA RTX A2000 GPU and supports up to 64 GB of ECC memory.[3]Kontron AG, “KBox B-301-RPL Embedded Box PC,” kontron.com However, GPUs are projected to experience a robust 7.93% CAGR as vision inference increasingly shifts to edge computing. This growth is driven by the rising adoption of GPU boards in industrial applications, particularly as factories transition from cloud-hosted analytics to on-device models. These on-device models significantly reduce latency and network fees, offering a more efficient and cost-effective solution for real-time data processing.

Storage devices equipped with power-loss protection and industrial-grade flash memory continue to dominate logging applications, particularly those that require high-frequency polling of vibration sensors at kilohertz rates. These devices ensure data integrity and reliability in demanding industrial environments. I/O modules, which capture data from communication protocols such as CAN, Profibus, and EtherCAT, account for approximately one-eighth of the bill of materials. These modules are increasingly transitioning from external cards to mezzanine modules, a shift that minimizes cabling requirements and enhances system integration. Additionally, networking components, including TSN-capable switches and private 5G modems, are experiencing significant growth. This trend aligns with the expansion of autonomous mobile robot fleets, which rely on advanced networking technologies to enable seamless communication and coordination in industrial settings.

By Form Factor: Compact and Fanless Chassis Gain Ground

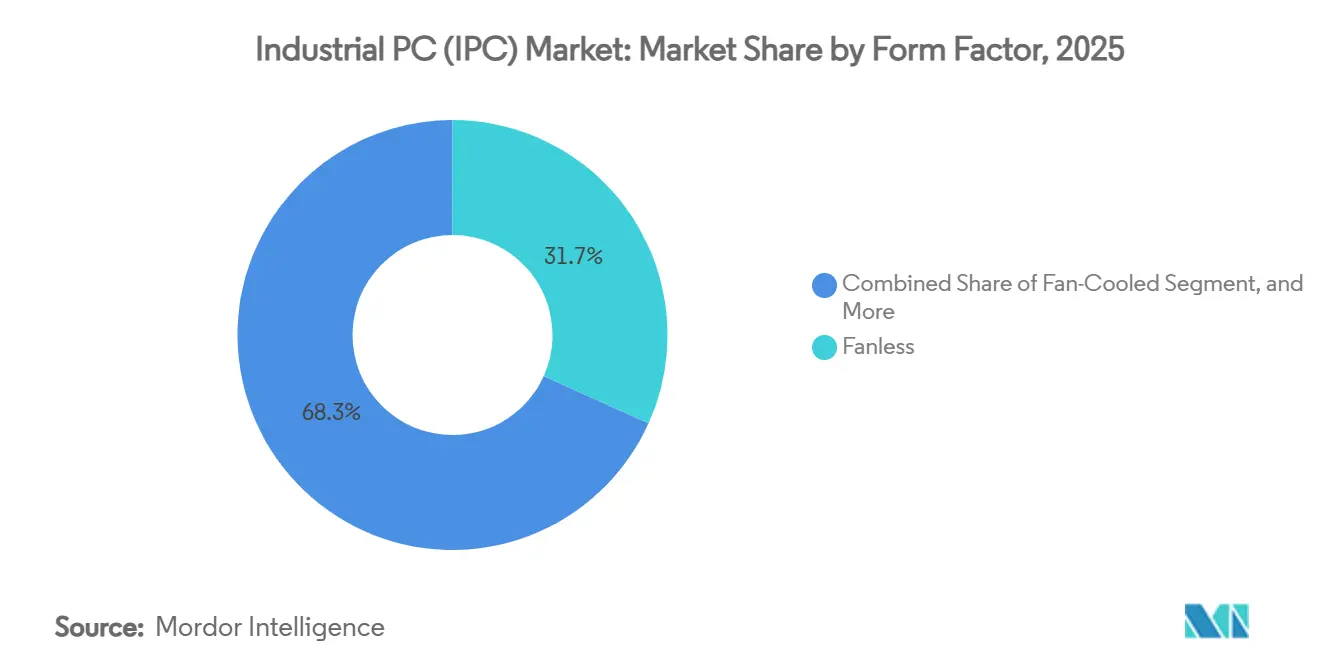

Fanless designs accounted for 31.73% of 2025 revenue, driven by their suitability for environments where dust, debris, or corrosive substances can clog or degrade traditional fans over time. These designs are particularly favored in industries such as manufacturing, mining, and chemical processing, where equipment reliability is critical. Compact footprints are also witnessing significant growth, expanding at a 9.13% CAGR, as robotics integrators increasingly require controllers that can fit into mobile platforms or confined spaces within crowded cabinets. This trend is further supported by the growing adoption of automation in industries where space optimization is a priority.

Rackmount and fan-cooled enclosures remain relevant, especially in applications where PCIe slots are needed to host motion-control or FPGA accelerator cards that require higher cooling than passive systems can provide. Panel-mount units equipped with multi-touch displays are now being designed with IP65-rated aluminum housings, making them highly durable and capable of withstanding frequent wash-downs in environments such as meat-processing plants, where hygiene standards are stringent. Additionally, extended-temperature box PCs are gaining traction in railway, drone, and traffic-monitoring projects. These systems are engineered to endure extreme temperature fluctuations, ranging from -40 °C to 70 °C, making them ideal for deployment on rolling stock, roadside poles, and other outdoor or mobile applications where environmental conditions can be harsh.

By Sales Channel: E-Commerce Platforms Democratize Procurement

Direct sales accounted for 42.91% of 2025 revenue, as high-volume OEM projects still rely on field-application engineers for thermal simulations, customized configurations, and service-level agreements to meet specific industrial requirements. These engineers play a critical role in ensuring that the systems are optimized for performance and reliability in demanding environments. However, online marketplaces are scaling at an 8.23% CAGR as integrators increasingly place single-unit orders for proof-of-concept testing and small-scale deployments. The industrial PC market benefits significantly from platforms that allow engineers to configure processor, memory, and I/O options online, offering flexibility and convenience. Additionally, next-day delivery services for North American locations further enhance the appeal of these online channels, enabling faster project execution.

Value-added resellers (VARs) are also playing a pivotal role in the market by bundling SCADA systems, networking equipment, and commissioning services into comprehensive turnkey packages. These packages are particularly valuable for industries such as water-treatment plants and mining operations, where seamless integration and operational efficiency are critical. The increasing commoditization of industrial PCs has pressured vendors to provide exhaustive datasheets, detailed technical specifications, and 3D CAD models. This shift caters to buyers who prefer to self-educate and conduct thorough evaluations independently, rather than scheduling in-person demonstrations. Price competition remains most intense in the low-power panel PC segment, where cost sensitivity is high. In contrast, mission-critical rackmount systems, which are often used in applications requiring high reliability and performance, continue to transact primarily through direct sales channels, maintaining their stronghold in the market.

Geography Analysis

Asia-Pacific contributed significantly to the industrial PC market revenue in 2025, driven by several key factors. China’s mandate to upgrade millions of AI-capable industrial terminals by 2027, Japan’s leadership in robotics density, and South Korea’s substantial investment in advanced packaging fabs collectively bolstered the region’s dominance. Regional original equipment manufacturers (OEMs) increasingly adopted RISC-V processors to reduce costs associated with x86 licensing and to mitigate risks stemming from export controls. Additionally, high-temperature-grade controllers gained traction in Japanese and Korean manufacturing lines, where precision requirements have become increasingly stringent, particularly for heterogeneous chiplet assembly processes.

Africa, while smaller in overall market size, is projected to experience notable growth over the forecast period due to rising demand for fanless industrial PCs capable of operating in extreme temperatures and harsh environments. This demand is driven by the expansion of microgrids and green-hydrogen zones, which require robust and reliable systems rated for high temperatures and ingress protection.[4]International Energy Agency, “Africa Energy Outlook 2025,” iea.org Sub-Saharan governments are actively supporting this growth by offering tax incentives and subsidized power within eco-industrial parks. These measures are accelerating the adoption of industrial controllers in sectors such as battery-cell assembly, agricultural processing, and off-grid telecommunications infrastructure. Industry events, such as the Africa Automation Fair, are also playing a pivotal role by attracting numerous OEM exhibitors targeting applications in mining and mobile power systems.

North America and Europe collectively accounted for a significant share of the industrial PC market revenue in 2025, primarily driven by retrofit projects to replace outdated programmable logic controllers (PLCs) with modern, containerized edge controllers. These regions are focusing on upgrading legacy systems to enhance operational efficiency and meet evolving industrial requirements. Meanwhile, South America presents growth opportunities, particularly in Brazil’s automotive sector and Argentina’s food processing plants. However, challenges such as currency fluctuations and import tariffs continue to hinder the pace of market expansion in the region. In the Middle East, adoption is centered around upgrading petrochemical supervisory control and data acquisition (SCADA) systems and implementing advanced control rooms for desalination plants. These facilities increasingly specify ATEX Zone 2-compliant systems equipped with Arabic-language human-machine interfaces (HMIs) to meet regional needs.

Competitive Landscape

The top five vendors, Advantech, Beckhoff, Kontron, ADLINK, and Siemens, collectively controlled about 38% of 2025 revenue, confirming moderate concentration. Siemens bundles its Industrial Edge runtime on Simatic IPCs, and Rockwell Automation combines FactoryTalk Edge Gateway with Allen-Bradley panel PCs, substituting recurring software fees for eroding hardware margins. Niche suppliers differentiate through stainless-steel housings, quick-turn customization, and IEC 62443 pre-certification, eliminating month-long security audits for pharmaceuticals and food processors.

RISC-V-based Chinese designs challenge incumbent x86 price points in value-sensitive segments, while NVIDIA’s Jetson Orin and IGX Thor modules allow vision integrators to bypass traditional IPC vendors, compressing the supply chain. Patent activity in liquid cooling suggests forthcoming rackmount systems that host 300-W GPUs on the factory floor, extending AI training to the edge. Standards work inside IEC TC65 on OPC UA over TSN will gradually commoditize fieldbus interfaces, shifting differentiation toward lifecycle management, cyber-resilience, and in-field upgradeability.

Mergers and acquisitions remain likely as automation majors seek vertical integration of hardware, middleware, and analytics, mirroring earlier deals that folded cloud platforms into controller portfolios. Smaller players pursue joint ventures with AI start-ups to embed low-code anomaly detection onto existing chassis, monetizing installed bases without invasive retrofits. Competitive positioning, therefore, hinges on ecosystem partnerships, rather than raw hardware specifications alone.

Industrial PC (IPC) Industry Leaders

Advantech Co., Ltd.

Beckhoff Automation GmbH and Co. KG

Kontron AG

ADLINK Technology Inc.

IEI Integration Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Siemens launches the Simatic IPC RX700 series built on 16-core RISC-V processors, native TSN networking, and on-device cybersecurity monitoring, targeting deterministic control inside battery-cell gigafactories.

- March 2026: NVIDIA and Advantech unveil a joint reference design that integrates the IGX Thor module into a fanless box IPC rated for 60 °C ambient operation, enabling 2,000 TOPS edge-AI inference on automotive assembly lines.

- February 2026: ADLINK announces the LCX-6000 liquid-cooled rackmount IPC supporting twin 300 W GPUs, designed for real-time defect analytics in semiconductor back-end test operations.

- January 2026: Beckhoff introduces the C7025 18.5-inch IP65 panel PC powered by Intel Meteor Lake processors and integrated Wi-Fi 6E, aimed at space-constrained injection-molding cells.

Global Industrial PC (IPC) Market Report Scope

The Industrial PC (IPC) market comprises ruggedized computing systems designed for use in industrial environments where reliability, durability, and continuous operation are critical. These systems are engineered to withstand harsh operating conditions, including extreme temperatures, dust, vibration, and moisture, and are widely used for automation, control, monitoring, and data processing across various industries.

The Industrial PC Report is Segmented by IPC Type (Panel, Rackmount, Embedded Box, DIN-rail, and Thin Client), End-User Industry (Automotive, Electronics and Semiconductor, Food and Beverage, Pharmaceutical, Energy and Utilities, Aerospace, Machinery, Oil and Gas, Chemical, and Metals and Mining), Component (CPU, GPU, Storage, I/O, Networking, Displays, OS, and Middleware), Form Factor (Fanless, Fan-cooled, Compact, Expandable, Panel Mount, and Rack Mount), Sales Channel (Direct, Indirect, and E-commerce), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Panel Industrial PC |

| Rackmount Industrial PC |

| Embedded Box Industrial PC |

| DIN-rail Industrial PC |

| Thin Client Industrial PC |

| Automotive and Transportation Manufacturing |

| Electronics and Semiconductor |

| Food and Beverage Processing |

| Pharmaceutical and Biotechnology |

| Energy and Utilities |

| Aerospace and Defense |

| Industrial Machinery |

| Oil and Gas |

| Chemical |

| Metals and Mining |

| CPU |

| GPU |

| Storage |

| I/O Modules |

| Networking Components |

| Displays and Human Machine Interfaces |

| Operating System Software |

| Middleware and Industrial Software |

| Other Components |

| Fanless |

| Fan-cooled |

| Compact |

| Expandable |

| Panel Mount |

| Rack Mount |

| Direct Sales |

| Indirect Sales |

| E-commerce |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Industrial PC Type | Panel Industrial PC | ||

| Rackmount Industrial PC | |||

| Embedded Box Industrial PC | |||

| DIN-rail Industrial PC | |||

| Thin Client Industrial PC | |||

| By End-User Industry | Automotive and Transportation Manufacturing | ||

| Electronics and Semiconductor | |||

| Food and Beverage Processing | |||

| Pharmaceutical and Biotechnology | |||

| Energy and Utilities | |||

| Aerospace and Defense | |||

| Industrial Machinery | |||

| Oil and Gas | |||

| Chemical | |||

| Metals and Mining | |||

| By Component | CPU | ||

| GPU | |||

| Storage | |||

| I/O Modules | |||

| Networking Components | |||

| Displays and Human Machine Interfaces | |||

| Operating System Software | |||

| Middleware and Industrial Software | |||

| Other Components | |||

| By Form Factor | Fanless | ||

| Fan-cooled | |||

| Compact | |||

| Expandable | |||

| Panel Mount | |||

| Rack Mount | |||

| By Sales Channel | Direct Sales | ||

| Indirect Sales | |||

| E-commerce | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is demand growing for controllers in renewable-energy microgrids?

Shipments tied to renewable-energy and utilities applications are forecast to grow at an 8.13% CAGR through 2031, reflecting rapid microgrid deployment across Africa, India, and Latin America.

Which industrial PC type is expanding quickest?

Embedded box IPCs are projected to outpace all other categories with an 8.53% CAGR between 2026 and 2031 because compute-on-module designs allow processor upgrades without full enclosure replacement.

Why are GPUs gaining share inside factory controllers?

Edge-AI vision inspection is migrating to fanless IPCs, driving GPU revenue to a 7.93% CAGR as manufacturers replace cloud inference with on-device convolutional neural networks to eliminate latency.

What geography represents the largest share of spending?

Asia-Pacific held 46.39% of 2025 revenue, buoyed by China's mandate to modernize AI-capable industrial terminals and by record semiconductor-fab investments in South Korea.

How are small manufacturers financing automation?

SMEs face higher capital-cost hurdles, yet pay-per-use leasing programs and e-commerce marketplaces offering single-unit purchases are gradually lowering barriers, especially in North America and Europe.

Which vendors currently lead the competitive field?

Advantech, Beckhoff, Kontron, ADLINK, and Siemens together accounted for roughly 38% of 2025 sales, indicating a moderately concentrated environment where software bundling is the key differentiator.

Page last updated on: