RAID Controller Card Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.99 Billion |

| Market Size (2031) | USD 12.18 Billion |

| Growth Rate (2026 - 2031) | 8.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RAID Controller Card Market Analysis by Mordor Intelligence

The RAID controller card market size is projected to expand from USD 7.34 billion in 2025 and USD 7.99 billion in 2026 to USD 12.18 billion by 2031, registering a CAGR of 8.8% between 2026 to 2031. In 2026, the RAID controller card market is gaining support from hardware refresh cycles linked to PCIe Gen5 server platforms and the continued buildout of AI infrastructure. The continued use of hardware RAID in enterprise and hyperscale environments shows that deterministic latency, cache-protected write performance, and offloaded parity computation still matter in workloads where storage reliability cannot be left to software alone. Data center expansion is keeping server and storage procurement active, which supports steady demand for high-density and high-throughput controller platforms in the RAID controller card market. Competition is being shaped by Broadcom and Microchip at the silicon layer, while newer vendors are pushing NVMe-native throughput and AI-aligned designs in the RAID controller card market. Software-defined storage and erasure coding are limiting some deployments, but strict latency targets, encrypted write caching, and power-loss protection continue to preserve a durable role for dedicated hardware in the RAID controller card market.

Key Report Takeaways

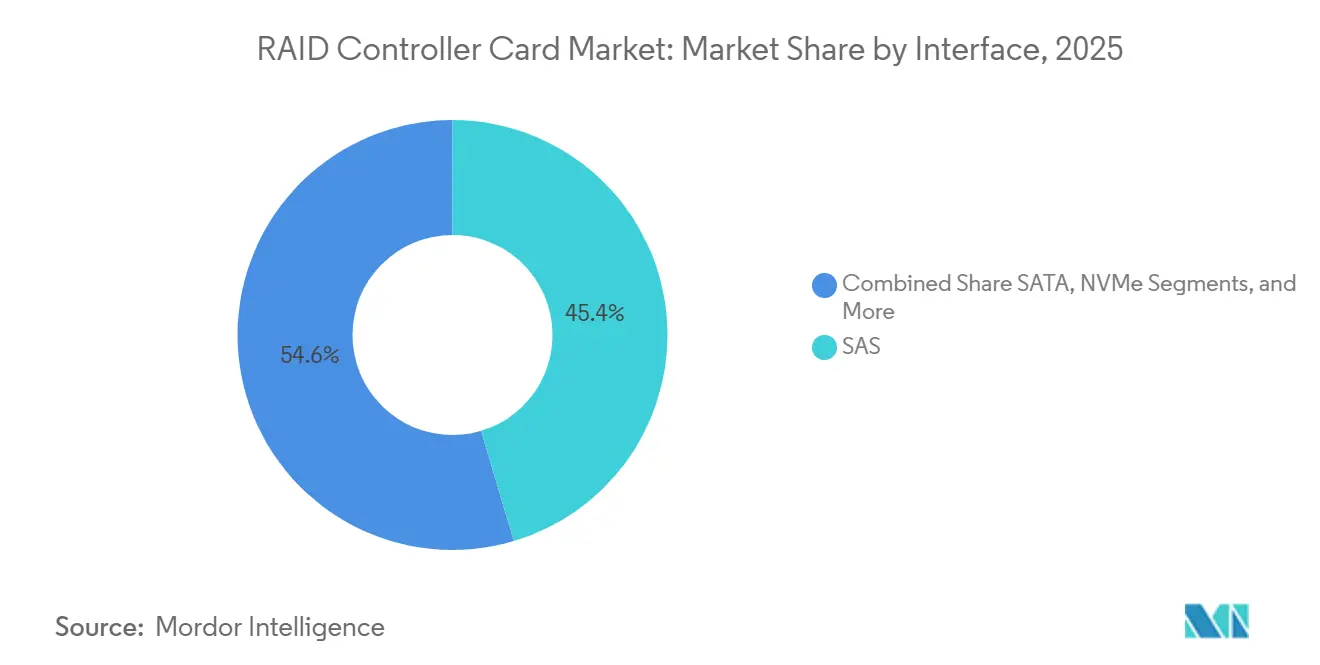

- By interface, SAS led with 45.38% share in 2025, while NVMe is forecast to expand at the fastest rate with a 9.0% CAGR through 2031.

- By form factor, PCIe RAID controller cards held 64.56% share in 2025, while OCP and embedded RAID modules are projected to grow at a 9.12% CAGR through 2031.

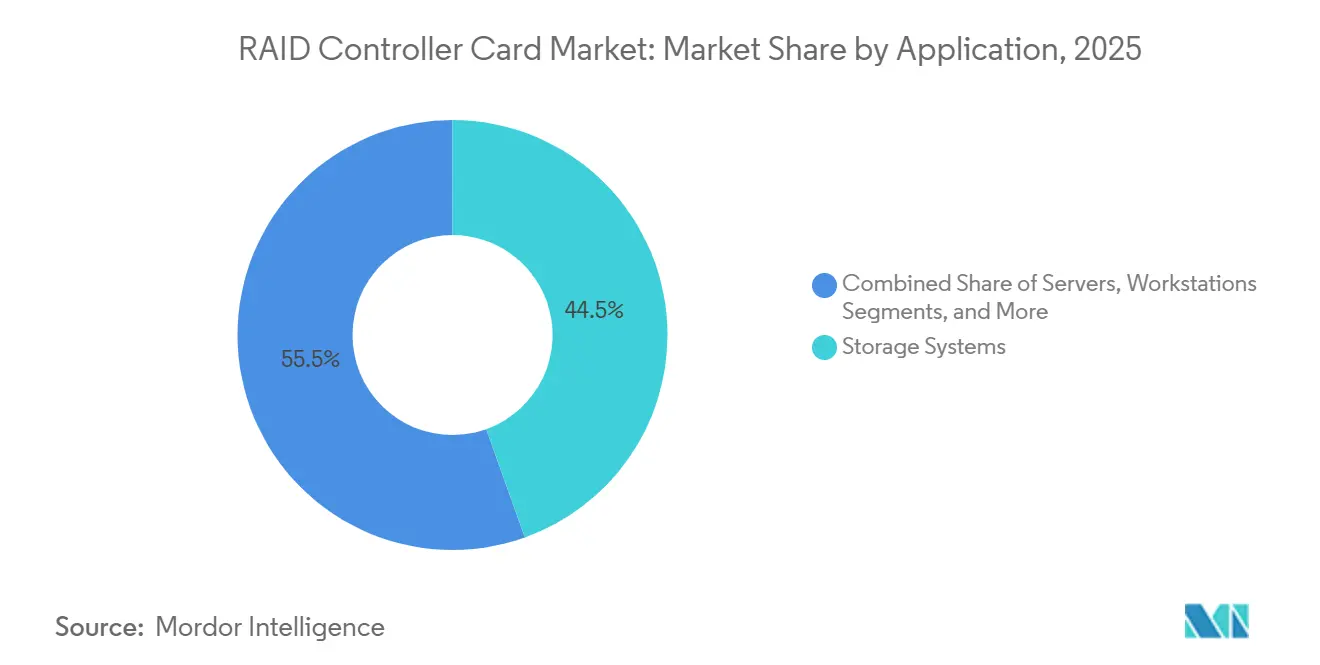

- By application, Storage Systems accounted for 44.53% share in 2025, while Servers are advancing at a 9.23% CAGR through 2031.

- By end user, Data Centers held 36.75% share in 2025 and also recorded the highest projected CAGR at 9.34% through 2031.

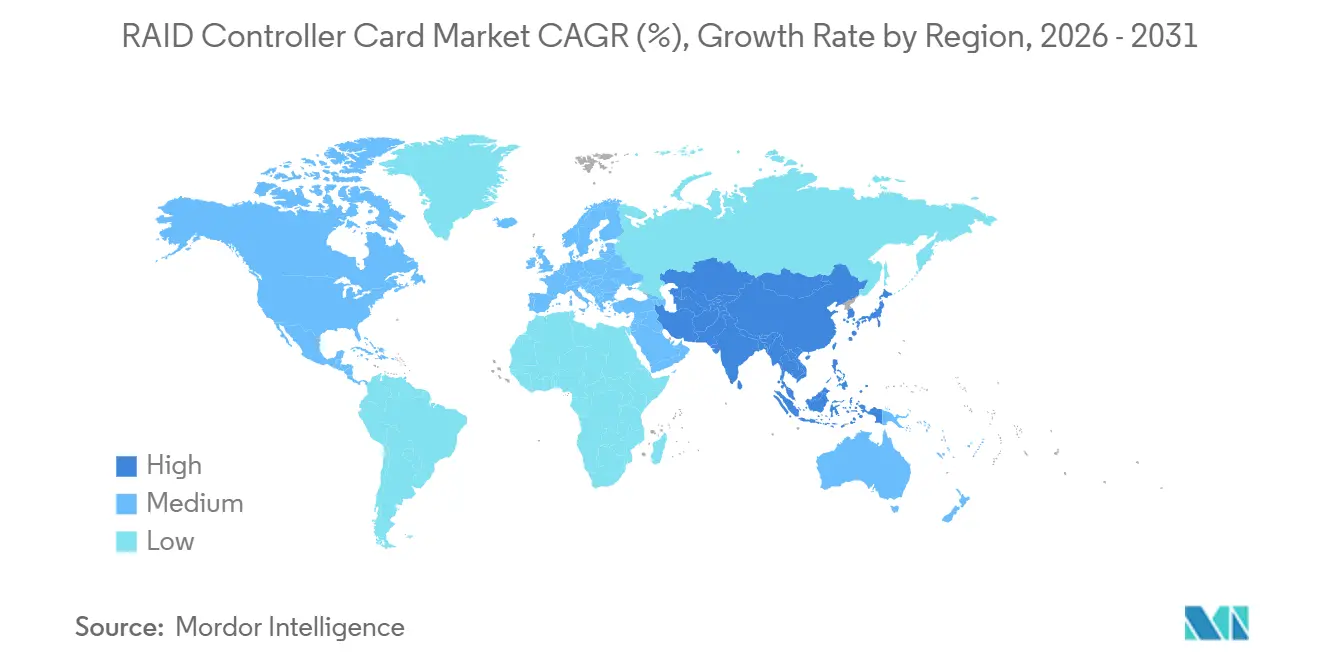

- By geography, Asia-Pacific accounted for 40.67% share in 2025 and is projected to grow at the fastest regional CAGR of 9.08% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global RAID Controller Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale And Enterprise Data Center Expansion | +3.1% | Global, core gains in North America, Asia-Pacific, and Europe | Short term (≤ 2 years) |

| NVMe And PCIe Gen5 Transition In Storage Backplanes | +2.3% | Global, with early momentum in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising Data Availability And Cyber Resilience Mandates | +1.4% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| AI And Analytics Workloads Needing Deterministic Low-Latency Storage | +1.0% | North America, Asia-Pacific, and Europe | Medium term (2-4 years) |

| Tri-Mode Controllers Simplifying Mixed SAS, SATA, And NVMe Refresh Cycles | +0.4% | Global, primarily North America and Europe enterprise installed base | Medium term (2-4 years) |

| Edge Servers Needing Compact Boot And Local Resilience RAID | +0.2% | Asia-Pacific, North America, and industrial hubs in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale and Enterprise Data Center Expansion

Hyperscale capital expenditure is lifting procurement levels in the RAID (Redundant Array of Independent Disks) controller card market beyond a normal server refresh cycle. AWS committed USD 50 billion to expand AI and high-performance computing capacity for U.S. government cloud regions, and the program moved into active development with nearly 1.3 GW of added capacity in 2026. This matters because higher rack density goals increase the number of high-speed storage devices that need controller support inside each server. Enterprise buyers are also moving through PCIe Gen5 transitions, which means new server baselines now require updated controller generations that can support faster NVMe backplanes and 24 Gbps SAS connectivity. The overlap between hyperscale expansion and enterprise platform refresh is creating a wider pull-through cycle for the RAID controller card market than the prior shift from PCIe Gen3 to Gen4.

NVMe and PCIe Gen5 Transition in Storage Backplanes

The PCIe Gen5 rollout is pushing the RAID (Redundant Array of Independent Disks) controller card market through one of its most important platform transitions in recent years. Broadcom’s 97xx MegaRAID adapters have become a current enterprise reference point because they combine PCIe 5.0 x16 host interfaces with 24 Gbps SAS tri-mode support for mixed drive environments.[1]“Broadcom 97xx PCIe 5.0, 24G SAS MegaRAID And HBA Storage Adapters, Overview,” Broadcom TechDocs, broadcom.com Dell’s PERC13 H975i showed 52.5 GB/s maximum throughput and 12.5 million IOPS in testing, and write bandwidth improved by 318% from the previous generation, which reinforced the performance gap between new hardware RAID and host-based alternatives. As Gen5 speeds rise, software RAID needs more CPU cycles for parity work, so the value of dedicated offload engines becomes clearer in the RAID controller card market. Microchip’s Adaptec SmartRAID 4300 responded to that shift by moving XOR processing to dedicated accelerator silicon while keeping direct CPU-to-NVMe data paths, and the company stated performance gains of up to 7x over earlier hardware RAID generations.

Rising Data Availability and Cyber Resilience Mandates

Regulatory changes that became active in 2024 and 2025 are adding a compliance layer to the RAID (Redundant Array of Independent Disks) controller card market. DORA became applicable on January 17, 2025, and NIS2 took effect on October 18, 2024, which extended resilience and incident obligations across financial services, digital infrastructure, healthcare, and other critical sectors. Procurement teams in these sectors are leaning toward hardware-validated protection because recovery time and recovery point targets need to be measured, tested, and documented. Controllers with SPDM device authentication and related security capabilities are moving from a technical preference to a qualification requirement in some regulated deployments, especially on current Broadcom and HPE platforms.[2]“HPE Compute MR Controllers QuickSpecs,” Hewlett Packard Enterprise, hpe.com In Europe, that is stretching procurement cycles because organizations are taking more time to validate controller firmware, attestation, and resilience behavior before full deployment. The result is a RAID controller card market that is increasingly influenced by security validation and not only by raw storage throughput.

AI and Analytics Workloads Needing Deterministic Low-Latency Storage

AI training and inference workloads are strengthening the case for dedicated acceleration in the RAID (Redundant Array of Independent Disks) controller card market because these environments mix small random reads, large checkpoint writes, and tight latency budgets. Dell reported that PERC13 reduced checkpoint save times for 1-trillion-parameter AI models by around 50% against the prior generation, which shows how storage architecture now affects compute efficiency at the cluster level. When storage-induced delays keep GPUs idle, operators have a strong reason to reduce CPU overhead from parity work and move more of that burden to the controller. Graid extended that argument by using GPU silicon for RAID processing, and the company stated that SupremeRAID can aggregate up to 32 NVMe drives into a 280 GB/s virtual pool while delivering key-value cache reads 77 times faster than standard NVMe at 1.3 milliseconds latency. That approach is widening the boundary of the RAID controller card market because it connects traditional protection functions with newer AI infrastructure design choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Software-Defined Storage And Erasure Coding | -0.8% | Global, pronounced in hyperscale North America and cloud-native Asia-Pacific deployments | Short term (≤ 2 years) |

| High Controller And Cache Protection Bill Of Materials And Integration Cost | -0.4% | Global, most acute in SME and emerging market segments | Medium term (2-4 years) |

| Secure Firmware And Encryption Validation Lengthening Design Cycles | -0.2% | North America and Europe, especially regulated verticals | Medium term (2-4 years) |

| Tariff And ASIC Supply Concentration Inflating Landed Costs | -0.2% | Asia-Pacific, Europe, and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Software-Defined Storage and Erasure Coding

The shift toward software-defined storage is one of the clearest structural limits on the RAID controller card market. Object stores, scale-out file systems, and hyper-converged environments are increasingly using distributed resiliency instead of node-level controller logic, which reduces the need for a dedicated card in some deployments. This pressure is strongest in architectures built around Ceph, Lustre, MinIO, and similar platforms where redundancy is managed across the cluster and not inside a single server. Large NVMe SSD capacities also make rebuild behavior a more visible design issue, so buyers are reevaluating where classic hardware RAID still creates the best tradeoff. Even so, the RAID controller card market remains more defensible in regulated databases, bare-metal systems, and performance-sensitive environments where deterministic latency, cache-protected writes, and power-loss protection are hard to replace with software alone.

High Controller and Cache Protection Bill of Materials and Integration Cost

The bill of materials for enterprise controllers is rising, and that is limiting adoption in the lower end of the RAID (Redundant Array of Independent Disks) controller card market. PCIe Gen5 retimers, supercapacitor-based cache protection, SPDM security support, and dense NVMe cabling all add cost before the controller reaches production volume. HPE’s current storage controller specifications show how features such as validated energy packs and secure platform support are now part of the standard enterprise design envelope. These additions are easier to justify in high-value enterprise and data center workloads than in mid-market server configurations that can fall back on simpler software RAID. The same cost stack also extends qualification timelines because controller vendors still need firmware validation across operating systems, drive models, and security policies before an OEM platform can move into broad shipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Interface: SAS Installed Base Anchors Volume as NVMe Reshapes Growth Trajectory

SAS held 45.38% of RAID controller card market share in 2025, which shows how large the installed base remains across enterprise arrays, mission-critical clusters, and tape-linked storage environments. That installed base matters because refresh cycles in these deployments are guided more by server generation changes than by fast interface obsolescence. Buyers continue to value backward compatibility, predictable firmware behavior, and long qualification histories when they replace controllers in core enterprise environments. SATA still serves cost-sensitive storage and archival use cases, but its role is narrowing as SSD density improves and NVMe becomes more attractive even for capacity-oriented designs. Fibre Channel controllers remain a specialized option in SAN-attached environments, especially in financial services and healthcare where legacy infrastructure and certification requirements still carry weight.

NVMe is projected to be the fastest-growing interface at a 9.0% CAGR through 2031, which is steadily changing design priorities across the RAID controller card market. Silicon Motion’s SM8008 showed how much engineering focus has shifted toward Gen5 NVMe infrastructure, with the company highlighting up to 14 GB/s sequential throughput and active power below 5 W on its enterprise controller platform. Tri-mode controllers are also becoming more important because many enterprises need to mix legacy SAS drives with newer NVMe additions during staggered refresh cycles. Broadcom’s current 97xx family supports that bridge with combined SAS, SATA, and NVMe capability, which turns interface migration into a platform design decision instead of a full storage replacement event. In the RAID controller card industry, vendors with strong tri-mode validation are better placed to capture mixed-refresh projects because they reduce certification work for OEMs and enterprise buyers.

By Form Factor: PCIe Cards Dominate While OCP Modules Accelerate in Hyperscale

PCIe RAID controller cards held 64.56% share in 2025, which kept them as the default form factor across most enterprise server and storage procurements. Their lead comes from broad compatibility, mature management software, and long-established qualification with major OEM server platforms. The standard half-height, half-length card still fits how many enterprises buy and service storage hardware because it gives a familiar replacement path and clear field support procedures. HPE’s current platform documents also show that controller management is increasingly tied into system-level tools such as iLO and related server management frameworks, which reinforces incumbent position in the RAID controller card market. External controllers remain relevant for direct-attached and enclosure-based use cases, but they are no longer the center of growth as more RAID logic is moving closer to the server board or enclosure controller.

OCP and embedded RAID modules are forecast to grow at a 9.12% CAGR through 2031, which makes them the fastest-moving form factor in the RAID controller card market. Hyperscale operators are driving that shift because OCP-aligned hardware can standardize deployment and preserve PCIe slots for GPUs and networking. HPE’s MR416i-o Gen11 and MR216i-o Gen11 releases show how OEMs are moving more storage protection into OCP-oriented server designs. Embedded modules also fit the boot-resilience role, where mirrored operating system volumes are required without dedicating a full add-in card to that task. In the RAID controller card industry, that means form factor choice is becoming more tied to server architecture and workload density than to controller function alone.

By Application: Storage Arrays Anchor Share While AI Server Demand Builds Fastest

Storage Systems accounted for 44.53% share of the RAID controller card market size in 2025, which kept them as the core application base for dedicated controller demand. All-flash arrays, hybrid systems, and many NAS platforms still rely on controller-assisted protection because predictable rebuild behavior and write-cache protection remain central to platform reliability. Huawei’s New-Gen OceanStor Dorado Converged All-Flash Storage underlined that point with a SmartMatrix 4.0 full-mesh design and stated tolerance for failure of 7 out of 8 controller enclosures without service interruption.[3]“Huawei Releases New-Gen OceanStor Dorado Converged All-Flash Storage To Empower The AI Era,” Huawei, huawei.com That kind of resilience profile helps explain why mission-critical storage systems still anchor the RAID controller card market even as software-defined models expand elsewhere. Workstations remain a smaller but durable use case because media production, CAD, and scientific workloads still need high local throughput with direct data protection.

Servers are forecast to grow at a 9.23% CAGR through 2031, which makes them the fastest-rising application in the RAID controller card market. AI server deployments are changing storage design because input pipelines and checkpoint behavior can now influence utilization of expensive accelerators. Microchip stated that the SmartRAID 4300 can support up to 32 CPU-attached x4 NVMe devices and reach up to 27.2 million 4K random-read IOPS in Linux on Gen5 platforms, which shows how vendors are tuning products for that environment. Edge and industrial systems are also adding demand where local resilience matters more than network dependence, especially in smart manufacturing, surveillance, and transportation. Advantech’s RAIDBOX platform reflects that pattern by targeting rugged edge settings that need local data integrity and stable uptime under industrial conditions.

By End User: Data Centers Lead in Both Scale and Growth Rate

Data Centers held 36.75% share in 2025 and are also forecast to grow at the fastest 9.34% CAGR through 2031, which gives them a clear lead within the RAID controller card market. This segment benefits from continuous capacity additions, regular server refresh cycles, and a higher mix of workloads where storage latency and uptime have direct financial impact. The strongest pull is coming from facilities that are being updated for AI training, AI inference, and high-density virtualization, where controller throughput and protection features remain material to system design. Cloud service providers share some of these infrastructure needs, but their contribution to the traditional RAID controller card market is more mixed because some of them prefer custom architectures that bypass standard add-in cards. Enterprises remain a stable volume base because multiyear server contracts and internal hardware standards create predictable procurement for Dell, HPE, Lenovo, and similar OEM ecosystems.

Data centers will continue to set the pace for the RAID controller card market through 2031, but the feature mix is also being shaped by several other end-user groups. Government and defense buyers are pulling demand toward hardware root of trust, attested firmware integrity, encrypted cache, and device authentication because those capabilities align with formal security requirements. Healthcare is also expanding its storage protection needs as medical imaging archives, electronic health records, and AI-assisted diagnostics increase both data volume and recovery sensitivity. Manufacturing demand is becoming more visible where industrial IoT aggregation and machine-vision inspection create local storage streams that cannot tolerate long interruptions. Media and other specialized users stay smaller in scale, but they still support the RAID controller card market where high local throughput and fast rebuild performance matter more than broad cloud abstraction.

Geography Analysis

Asia-Pacific held 40.67% of RAID controller card market share in 2025 and is forecast to expand at a 9.08% CAGR through 2031, which keeps it as both the largest and the fastest-growing regional market. The regional advantage comes from a mix of greenfield hyperscale builds and a large installed base of enterprise, telecom, and manufacturing systems that still rely on SAS and tri-mode controller refresh. India is one of the clearest examples, with the country’s data center market valued at USD 9 billion to USD 10 billion in 2025 and supported by more than USD 67.5 billion in hyperscaler pledges as of late 2025 according to the Data Center Association of India and the Renewable Energy Society of India. China, Japan, South Korea, and Southeast Asia are also supporting the RAID controller card market through a combination of new AI infrastructure and continuing enterprise modernization. Because many new projects in the region are starting directly on recent server generations, Asia-Pacific is well placed to adopt PCIe Gen5-aligned controller platforms earlier than slower refresh regions.

North America is the second-largest regional market for RAID controller cards, and it benefits from the deepest hyperscale footprint and one of the most advanced enterprise refresh cycles. AWS’s USD 50 billion commitment to expand U.S. government AI and high-performance computing capacity shows how public cloud and sovereign cloud programs still translate into large server and storage procurement waves. The region is also where several next-generation designs were first validated in commercial server platforms, including Dell’s PERC13, HighPoint’s Gen5 NVMe RAID adapters, and Microchip’s SmartRAID 4300. Federal supply-chain security expectations and use of the NIST Cybersecurity Framework 2.0 are also keeping attention on attested firmware and validated controller security stacks in the RAID controller card market.

Europe’s RAID controller card market is shaped by data sovereignty rules, DORA and NIS2 compliance, and a large enterprise installed base in financial services, manufacturing, and the public sector. Microsoft’s PLN 2.8 billion expansion of Polish data centers and Amazon’s EUR 33.7 billion (USD 36.40 billion) investment in Spain for AWS infrastructure show that hyperscale expansion is still adding fresh controller demand across the region. Germany, the United Kingdom, and France remain the main demand centers, while Russia’s role has weakened because of technology export restrictions. South America is smaller, but Brazil, Argentina, and Chile are creating an emerging pocket of demand, and the region remains especially sensitive to imported ASIC pricing, tariffs, and currency pressure against USD-denominated components.

Competitive Landscape

The RAID controller card market is moderately consolidated at the silicon layer and fragmented at the finished-card and system-integration layer. Broadcom and Microchip supply the dominant base of RAID-on-Chip and host bus adapter silicon used by many OEM systems, which gives those two companies strong influence over product roadmaps, firmware direction, and qualification timing across the RAID controller card market. At the same time, the visible card ecosystem remains more dispersed because vendors such as Dell Technologies, HPE, Lenovo, Fujitsu, NEC, Supermicro, HighPoint, ATTO Technology, PROMISE Technology, Infortrend, and Areca compete across different server, channel, and specialist storage positions. This split explains why the RAID controller card market can look fragmented to buyers even while core controller silicon is concentrated upstream. It also means that product competition often happens through firmware maturity, OS support, management integration, and certification depth rather than through silicon ownership alone.

Broadcom continues to anchor the mainstream enterprise side of the RAID controller card market through the 97xx family and the MegaRAID 9760W series, with current storage selection guides showing active support for tri-mode enterprise deployments. HPE has widened its Gen12 coverage with the MR932i-p x32 Lanes PCIe Gen5 SPDM Plug-in Storage Controller, which extends Broadcom-based Gen5 capability across flagship ProLiant systems. Dell also raised the performance bar with PERC13, where a large jump in throughput and AI checkpoint behavior gave it a strong position in newer PowerEdge platforms. These moves show that incumbent OEMs are defending share by tying controller value more tightly to full server management stacks, validated firmware, and secure platform support.

Challengers are taking a different path in the RAID controller card market by focusing on NVMe-native design and AI-aligned storage acceleration. Graid moved beyond its earlier niche by launching an Agentic AI Storage Portfolio in April 2026 and by taking stewardship of Intel’s Virtual RAID on CPU program through a November 2025 licensing agreement, which signals a wider attempt to connect hardware acceleration with software-defined RAID control. Microchip is targeting the same white space from another direction with SmartRAID 4300, which keeps the CPU-to-NVMe path direct while moving parity work onto dedicated accelerator silicon. Marvell adds another specialized layer with NVMe boot RAID acceleration in OCP-oriented designs, which shows that competitive gaps now exist around boot resilience, AI servers, and dense NVMe nodes as much as around classic SAS arrays.

RAID Controller Card Industry Leaders

Broadcom Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise Company

Microchip Technology Incorporated

Marvell Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Graid Technology launched its Agentic AI Storage Portfolio, a family of KV cache solutions built on SupremeRAID technology designed for "always-on" production AI applications; the portfolio includes a KV Cache Server, KV Cache Rack, and a KV Cache Platform aligned to NVIDIA's STX reference architecture, with native BlueField-4 DPU execution planned for H2 2026.

- April 2026: HighPoint Technologies launched a new line of PCIe Gen5 x16 NVMe RAID and switch adapters, Rocket 7600A Series and Rocket 1600 Series, supporting AI, machine learning, and HPC environments; the Rocket 7604A achieves up to 56 GB/s real-world transfer speed and supports RAID 0, 1, and 10.

- March 2026: Silicon Motion launched the SM8008, its first purpose-built PCIe Gen5 x4 NVMe enterprise SSD controller, targeting data center boot drives and power-sensitive enterprise storage; built on TSMC's 6nm process, the SM8008 delivers up to 14 GB/s sequential throughput, over 2.3 million random IOPS, active power under 5 W, and TCG Opal 2.0 encryption with CNSA 2.0 readiness for 2027 compliance.

- February 2026: HPE added the MR932i-p x32 Lanes PCIe Gen5 SPDM Plug-in Storage Controller, P75697-B21, to its Gen12 server portfolio, built on the Broadcom Avenger 2 ASIC; the controller supports 32 Gbps NVMe and 24 Gbps SAS, supports up to 32 drives without expander, and is validated for Windows Server 2025 deployments.

Global RAID Controller Card Market Report Scope

The global RAID Controller Card Market pertains to hardware and software solutions designed to manage Redundant Array of Independent/Inexpensive Disks (RAID) configurations. These configurations are essential in servers, storage systems, and enterprise IT infrastructures. By coordinating data distribution across multiple drives, RAID controller cards play a critical role in enhancing data storage performance, reliability, and redundancy. The market's expansion is driven by the increasing demand for high-capacity storage, robust data protection, and efficient management of enterprise workloads, particularly in sectors such as cloud computing, data centers, and IT services. Furthermore, the market is characterized by advancements in controller technology, integration with advanced storage architectures, and growing adoption across industries seeking secure and scalable data solutions.

The RAID Controller Card Market is Segmented by Interface (SATA, SAS, NVMe, Tri-Mode SAS, SATA, and NVMe, and Fibre Channel), Form Factor (PCIe RAID Controller Cards, External RAID Controller Cards, and OCP and Embedded RAID Modules), Application (Servers, Storage Systems, Workstations, and Edge and Industrial Systems), End User (Data Centers, Cloud Service Providers, Enterprises, Government and Defense, Healthcare, IT and Telecommunications, Manufacturing, Media and Entertainment, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| SATA |

| SAS |

| NVMe |

| Tri-Mode SAS, SATA, and NVMe |

| Fibre Channel |

| PCIe RAID Controller Cards |

| External RAID Controller Cards |

| OCP and Embedded RAID Modules |

| Servers |

| Storage Systems |

| Workstations |

| Edge and Industrial Systems |

| Data Centers |

| Cloud Service Providers |

| Enterprises |

| Government and Defense |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Media and Entertainment |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Interface | SATA | |

| SAS | ||

| NVMe | ||

| Tri-Mode SAS, SATA, and NVMe | ||

| Fibre Channel | ||

| By Form Factor | PCIe RAID Controller Cards | |

| External RAID Controller Cards | ||

| OCP and Embedded RAID Modules | ||

| By Application | Servers | |

| Storage Systems | ||

| Workstations | ||

| Edge and Industrial Systems | ||

| By End User | Data Centers | |

| Cloud Service Providers | ||

| Enterprises | ||

| Government and Defense | ||

| Healthcare | ||

| IT and Telecommunications | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

Which interface leads revenue and which one is growing fastest?

SAS led with 45.38% share in 2025 because of its large enterprise installed base, while NVMe is the fastest-growing interface with a projected 9.0% CAGR through 2031.

Why do hardware RAID controllers still matter when software-defined storage is expanding?

Hardware RAID still matters in workloads that need deterministic latency, cache-protected writes, offloaded parity computation, and power-loss protection, especially in regulated and performance-sensitive deployments.

Which end user segment is driving the strongest demand?

Data centers are the leading end user with 36.75% share in 2025 and the fastest projected growth at 9.34% through 2031, supported by ongoing AI and server infrastructure expansion.

Which region offers the strongest growth opportunity?

Asia-Pacific is the largest regional contributor with 40.67% share in 2025 and the fastest expected growth at 9.08% CAGR through 2031, helped by new data center buildouts and enterprise refresh demand.

What are the main risks affecting adoption of RAID controller cards?

The main limits come from software-defined storage, erasure coding, higher controller bill of materials, and longer validation cycles for secure firmware and integration.

How is competition changing in Thailand's quick commerce space?

Competition is tightening around Grab and LINE MAN Wongnai after Foodpanda's exit, and leading firms are now differentiating through merchant tools, financial services, store-based fulfillment, and better inventory control rather than price alone.

Page last updated on: