Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The PC Accessories Market Report is Segmented by Product Type (Mouse, Keyboards, Headsets, Monitor Arms, Gaming Chairs, Webcams), Connectivity (Wired, Wireless RF/Bluetooth, USB-C/Thunderbolt Docks, Hybrid Multi-Device), End User (Gaming Enthusiasts, Enterprise and Office, and More), Distribution Channel (Online Retail, Offline Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

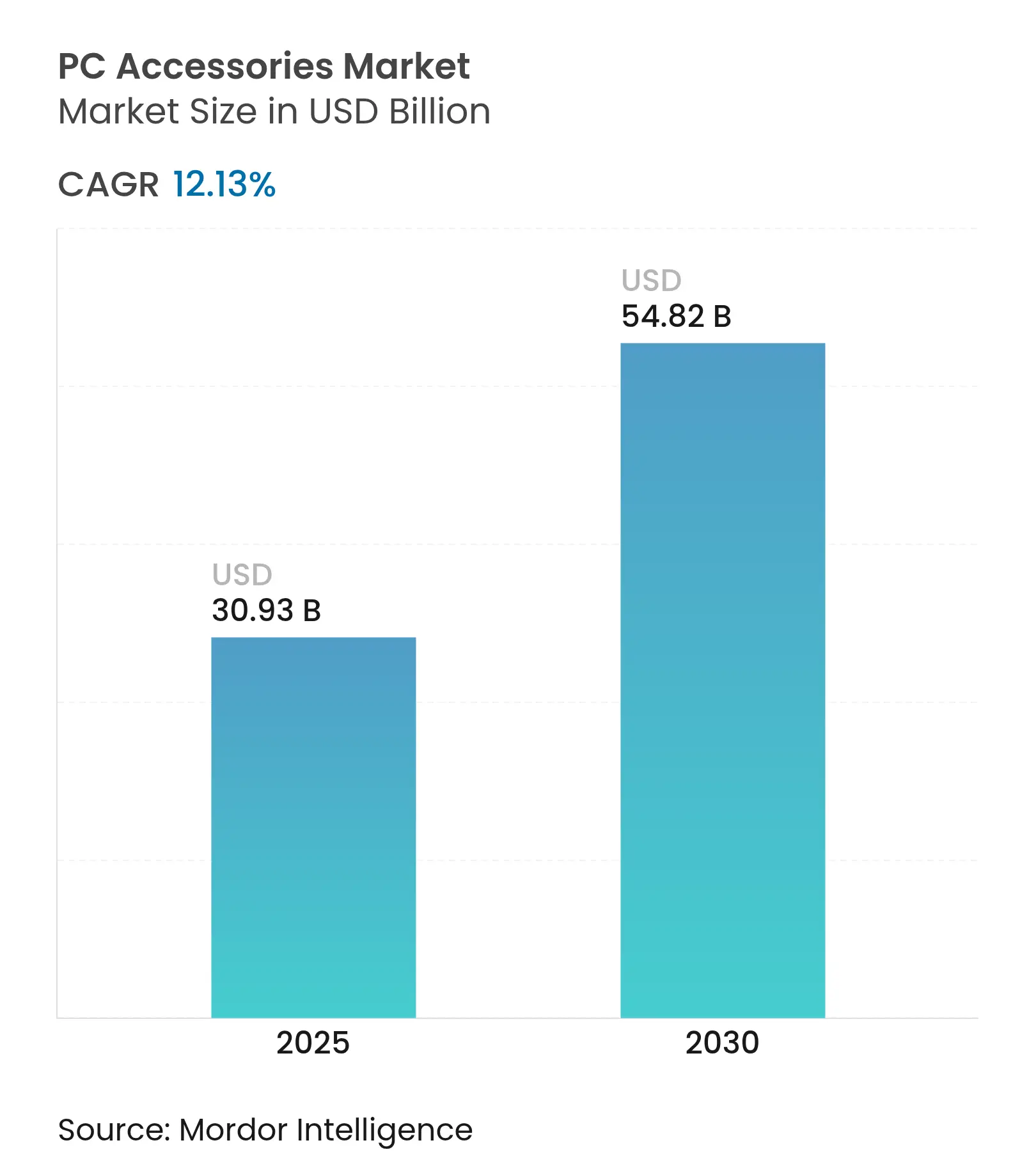

| Market Size (2025) | USD 30.93 Billion |

| Market Size (2030) | USD 54.82 Billion |

| Growth Rate (2025 - 2030) | 12.13 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The PC accessories market size stood at USD 30.93 billion in 2025 and is projected to reach USD 54.82 billion by 2030, reflecting a 12.13% CAGR over the forecast horizon. The upward trajectory is anchored in the maturation of global gaming ecosystems, sustained enterprise digital transformation investments, and rapid advances in wireless connectivity standards. Bluetooth Low Energy innovations shorten upgrade cycles, while hybrid-work ergonomics and sustainability mandates diversify growth avenues across mature and emerging economies. Competitive intensity is rising as incumbents defend margins against direct-to-consumer brands, and strategic acquisitions accelerate technology convergence that differentiates premium offerings. At the same time, supply-chain volatility, component cost inflation, and tighter cybersecurity regulations add operating complexity, prompting vendors to pursue vertical integration, multi-sourcing, and AI-enabled product road maps to protect profitability.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR (%) | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid growth in e-sports and competitive gaming ecosystems Rapid growth in e-sports and competitive gaming ecosystems | +2.8 | Global – strongest in Asia-Pacific and North America | Medium term (2–4 years) | (~) % Impact on CAGR (%):+2.8 | Geographic Relevance:Global – strongest in Asia-Pacific and North America | Impact Timeline:Medium term (2–4 years) |

Rising adoption of wireless and Bluetooth connectivity Rising adoption of wireless and Bluetooth connectivity | +3.2 | Global – led by North America and Europe enterprises | Short term (≤ 2 years) | |||

Proliferation of remote and hybrid work demanding ergonomic peripherals Proliferation of remote and hybrid work demanding ergonomic peripherals | +2.1 | North America and Europe core, expanding to Asia-Pacific | Medium term (2–4 years) | |||

Continuous declines in component costs enabling affordability Continuous declines in component costs enabling affordability | +1.4 | Global – greatest in price-sensitive emerging markets | Long term (≥ 4 years) | |||

AI-powered personalization enhancing user experience AI-powered personalization enhancing user experience | +1.8 | Early uptake in North America and Europe | Medium term (2–4 years) | |||

Corporate sustainability mandates favoring recycled-material peripherals Corporate sustainability mandates favoring recycled-material peripherals | +0.9 | Europe and North America regulatory-driven | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Growth in E-Sports and Competitive Gaming Ecosystems

Tournament standardization and professional endorsements transform peripheral demand by making “tournament-grade” gear aspirational for mainstream consumers. Saudi Arabia’s gaming revenue climbed to USD 1.13 billion in 2023 and is tracking toward USD 1.36 billion by 2026, demonstrating the spending power that large-scale e-sports investments unlock. [1]Albatul Alharthi, “Saudi Arabia Gaming Industry Report 2025,” tascoutsourcing.sa The Esports World Cup drew 500 million viewers, elevating brand visibility for headsets, mice, and gaming chairs. China exported 5 million gaming chairs in 2023, up 20% year over year, with 40% shipped to North America—a proxy for peripheral spillover beyond core hardware. Professional teams are piloting AI-enabled devices that auto-tune sensitivity and macros, speeding diffusion of premium innovations to retail channels. Collectively, these forces reinforce a self-reinforcing loop where content, competition, and peripherals co-evolve and enlarge the PC accessories market.

Rising Adoption of Wireless and Bluetooth Connectivity

Shipments of Bluetooth-enabled devices are projected to reach 7.5 billion units annually by 2028, with PC peripherals carving out a sizable share. Enterprise IT teams, once wary of latency and security vulnerabilities, now specify Security Mode 1, Level 4 compliance, prompting upgrades from wired to encrypted wireless mice, keyboards, and headsets. [2]Logitech, “Workspace Setups for Hybrid Work,” logitech.com Premium gaming boards supporting 4,000 Hz wireless polling have closed the performance gap to wired options, stimulating enthusiast acceptance. Because peripherals refresh faster than PCs, each security or technology leap expands the installed base independent of desktop or notebook replacement cycles. The same trend widens the PC accessories market addressable pool beyond traditional OEM channels, positioning wireless upgrades as an annuity-like revenue stream.

Proliferation of Remote and Hybrid Work Demanding Ergonomic Peripherals

Permanent hybrid policies force organizations to reassess workstation ergonomics at home and satellite offices. Logitech surveys show firms allocating peripheral budgets using individualized metrics such as hand size and application mix to maximize employee well-being, and Microsoft’s decision to relaunch its accessory line through Incase underscores corporate appetite for branded ecosystems that simplify device manageability. Insurance premiums linked to repetitive-strain injuries incentivize procurement teams to choose certified ergonomic designs, pushing demand for split-layout keyboards, vertical mice, and lumbar-support chairs. Multi-device connectivity further increases attach rates as staff shuttle between laptops, tablets, and shared hot-desks. These forces anchor predictable enterprise demand within the PC accessories market, even when macro hardware cycles soften.

AI-Powered Personalization Enhancing User Experience

Peripherals are evolving from static input tools into adaptive assistants. Logitech’s USD 49.99 Signature AI M750 mouse embeds a ChatGPT shortcut that lets users summarize emails or rewrite paragraphs without toggling applications. Akko’s DeepSeek-enabled keyboards translate single-key activation into code generation, report drafting and data analysis. Early field tests show voice-to-text throughput reaching 400 words per minute at 98% accuracy, expanding addressable workflows far beyond gaming. AI also learns motion patterns to predict cursor trajectories, cutting micro-delays that matter in professional e-sports. By shifting value from commodity hardware to software intelligence, vendors secure higher margins and recurring revenues, boosting the long-term growth profile of the PC accessories market.,

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR (%) | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Price sensitivity and intense low-cost competition Price sensitivity and intense low-cost competition | -1.8 | Global – most pronounced in emerging economies and SMB segments | Short term (≤ 2 years) | (~) % Impact on CAGR (%):-1.8 | Geographic Relevance:Global – most pronounced in emerging economies and SMB segments | Impact Timeline:Short term (≤ 2 years) |

Semiconductor and sensor supply-chain volatility Semiconductor and sensor supply-chain volatility | -2.3 | Worldwide – production risks centered in Asia-Pacific | Medium term (2–4 years) | |||

Rising cybersecurity and sustainability compliance costs Rising cybersecurity and sustainability compliance costs | -1.2 | Europe and North America leadership, spreading to all major regions | Medium term (2–4 years) | |||

Counterfeit and grey-market peripheral proliferation Counterfeit and grey-market peripheral proliferation | -0.9 | Global – acute in online marketplaces across developing economies | ||||

| Source: Mordor Intelligence | ||||||

Price Sensitivity and Intense Low-Cost Competition

Component price spikes collide with consumers’ preference for bargain peripherals, particularly in mass-market mice and keyboards. Chinese ODMs leverage scale to offer full-RGB mechanical boards at USD 25 retail, undercutting branded models by 30% to 40%. Currency depreciation in India amplifies landed costs, squeezing small-business buyers who fueled a 3.8% rise in 2024 PC shipments. Retailers introduce house-brand alternatives, diluting brand equity that incumbents monetize via premium positioning. To maintain share, leading firms roll out tiered lineups and loyalty software that pairs devices with cloud profiles, though the margin gap against white-label imports persists. This tug-of-war limits near-term ASP expansion within the PC accessories market.

Semiconductor and Sensor Supply-Chain Volatility

Gallium and germanium export restrictions imposed by China in 2024 tightened the supply of high-frequency chips vital for wireless peripherals. MLCC lead times stretched to as long as 50 weeks, compelling vendors to place non-cancelable orders that lock in capital. Taiwan’s April 2024 earthquake pushed DDR5 spot prices up 17%, revealing heavy geographic dependency. The U.S. Semiconductor Industry Association predicts a 67,000-person talent gap by 2030, possibly slowing Western fab ramps. Together, these shocks raise buffer-stock requirements and prompt board redesigns, injecting cost and scheduling risk that can delay new-product introductions. For the PC accessories market, extended shortages may cap upside in premium segments reliant on cutting-edge sensors.

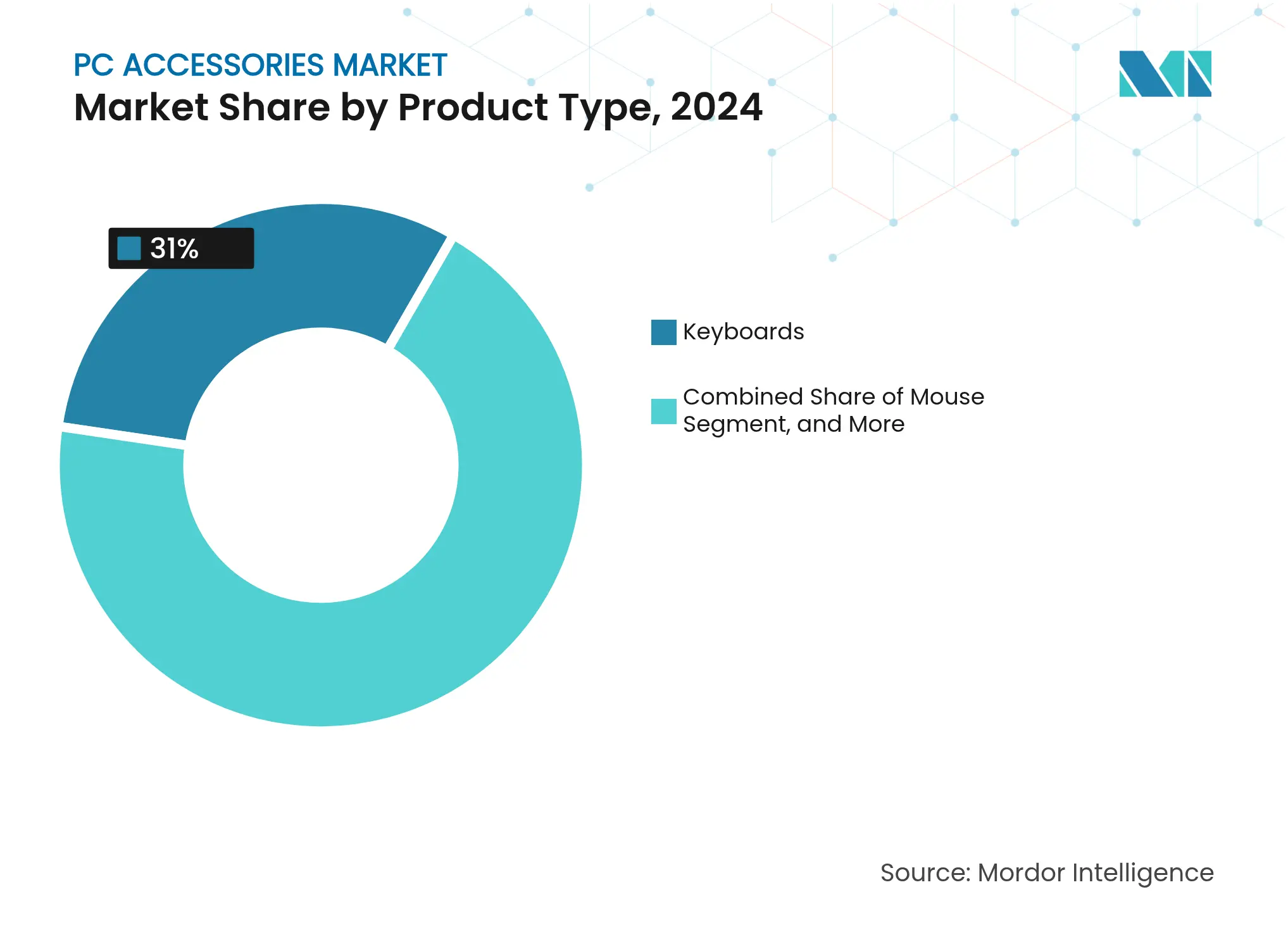

By Product Type: Gaming Chairs Drive Premium Category Expansion

Gaming chairs contributed USD 1 billion to China’s 2023 export earnings and are growing at a 12.54% CAGR, outpacing traditional input devices. Keyboard sales still represent 31% of the 2024 value, anchoring the PC accessories market size for mass-volume categories. ThunderX3’s FLEX Pro chair marries office-grade ergonomics with gamer styling, signaling convergence that broadens appeal. Mouse, headsets, and monitor arms benefit from hybrid-work multitasking, while webcams cool from pandemic highs yet remain structural necessities for video meetings. Smart-chair integrations—Bluetooth speakers, vibration motors, and heart-rate sensors—unlock fresh monetization vectors and reinforce premium ASP opportunities. The PC accessories market stands to gain both depth and diversity as furniture peripherals climb the value stack.

The rise of modular add-ons, such as HP’s 3D-printable Pulsefire Saga mouse side-plates, shows how customization invigorates mature categories. [3]Dominic Bayley, “HyperX 3D-Printable Mice,” pcworld.com Brands deploy limited-edition keycap sets and magnetic-attachment palm rests to refresh product life cycles without full redesigns. This accessories-for-accessories loop keeps enthusiasts engaged and pushes attach rates higher. Consequently, gaming chairs and bespoke peripherals serve as growth multipliers that help cushion cyclical swings in commodity keyboards and mouse.

Note: Segment shares of all individual segments available upon report purchase

By Connectivity: Wireless Dominance Accelerates Enterprise Adoption

Wireless devices held 52% revenue in 2024 while matching the highest growth pace at 12.87% CAGR, underscoring a decisive pivot toward untethered workspaces. Hybrid connectivity models—tri-mode receivers plus Bluetooth multipoint—let users flip between a laptop, tablet, and smartphone without re-pairing. On the security front, the imminent EN 18031 standard in Europe compels vendors to harden encryption and self-healing firmware, turning compliance into a selling point. Although elite gamers still prefer wired for sub-1 ms latency, new 4,000 Hz wireless polling has narrowed the gap enough that endorsements are shifting.

Rising notebook dominance also spurs demand for USB-C docks and Thunderbolt hubs, adding adjacent revenue pools within the PC accessories market. Enterprises bundling docks with mouse and keyboards create package deals that simplify procurement and increase average order values. Meanwhile, declining proprietary-dongle shipments reflect the gravitational pull of native Bluetooth across operating systems, streamlining inventory for retailers and IT departments alike.

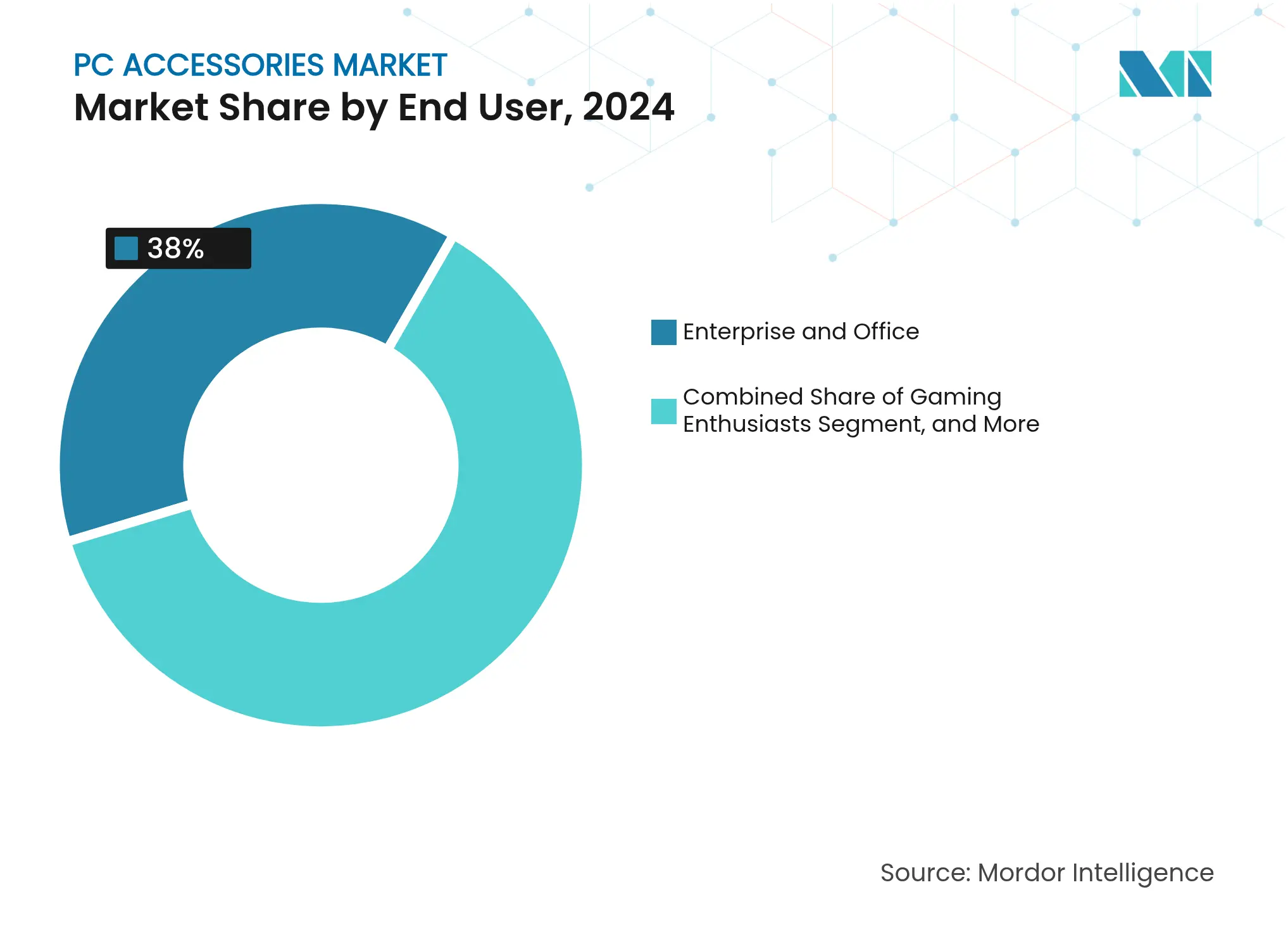

By End User: Gaming Enthusiasts Outpace Enterprise Growth

Enterprise buyers supplied 38% of 2024 revenue thanks to predictable hardware refresh cycles and ergonomic mandates. Yet gaming enthusiasts are projected to advance 13.12% annually, widening their share as disposable incomes climb in emerging markets. Corsair’s gaming and creator group logged USD 472.7 million sales in 2024, with a 37.7% margin, double its components unitmirroring the profitability of enthusiast targeting. Apple’s move to retail Corsair peripherals validates premium gamer aesthetics for mainstream consumers. In professional creator circles, AI-assisted editing shortcuts and low-latency audio headsets bridge the gap between entertainment and productivity.

Education sectors remain a smaller slice but see momentum from hybrid classrooms requiring headsets and webcams. Institutional procurement favors durable, simple-to-manage models, often through value-added resellers that preload classroom-management software. Collectively, the diversity of segments stabilizes the PC accessories market against single-channel shocks.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Retail Maintains Dominance

E-commerce captured 61% of 2024 sales and is forecast to climb 13.01% annually as consumers seek broader assortments and faster promotions. Flash sales, influencer reviews, and algorithmic recommendations expose shoppers to niche brands that would struggle in brick-and-mortar. Manufacturers launching directly on Amazon or Shopee bypass intermediaries, gaining data and higher margins. Offline stores remain relevant for high-ticket ergonomic chairs and color-matched setups where tactile evaluation matters. Distributors such as Redington and Ingram Micro leverage India’s USD 21.6 billion (INR 1.80 lakh crore) tech goods network to penetrate Tier 2 and Tier 3 cities.

OEM webshops are a fast-growing sub-channel, pairing peripherals with system purchase configurators to raise attach ratios. Value-added resellers cater to enterprises needing asset-tagging, security certification, and multiyear service contracts. Online share is expected to stabilize above 65% by 2030, cementing digital as the primary battlefield for PC accessories market differentiation.

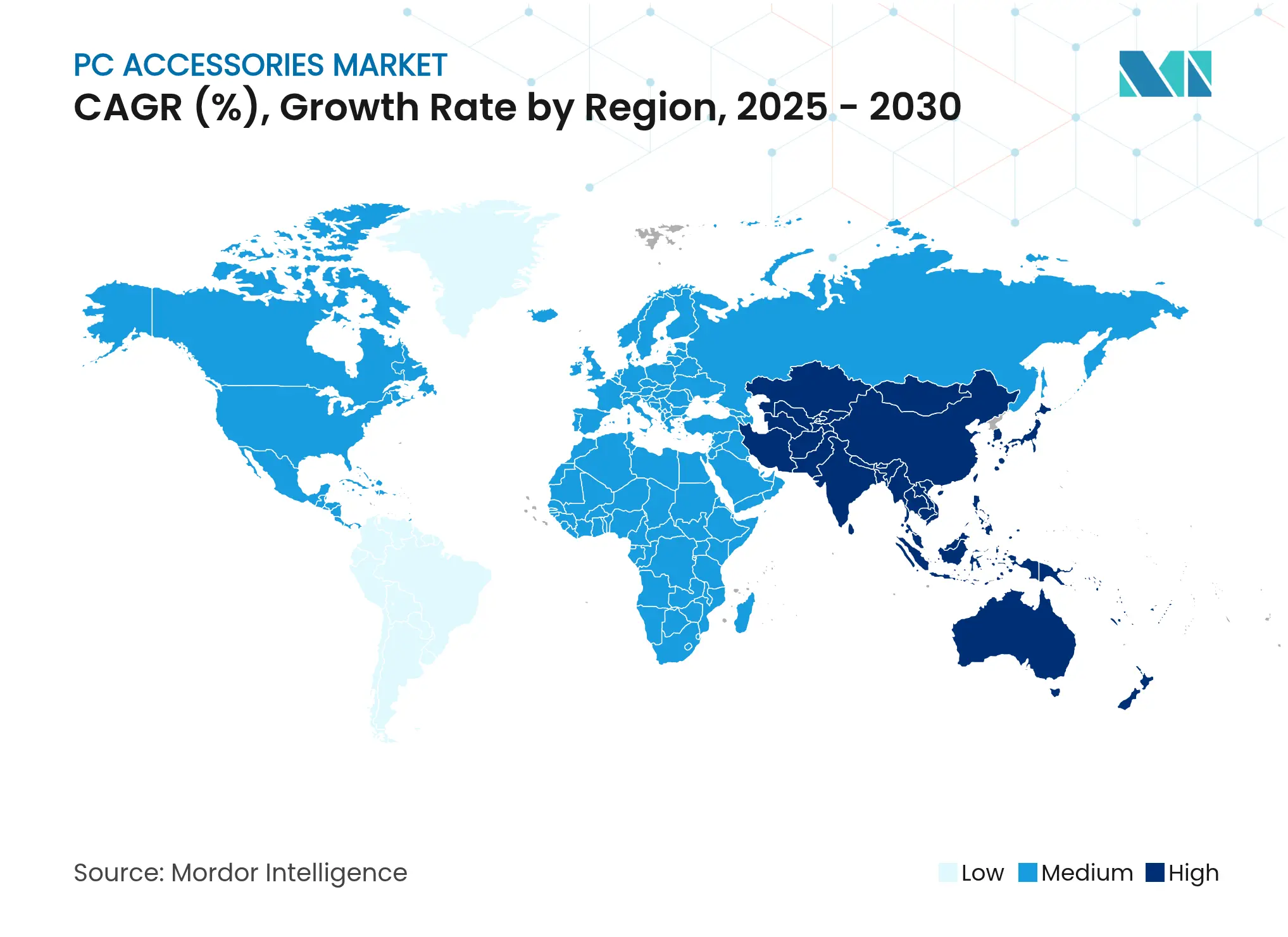

Asia-Pacific’s 48% slice of 2024 revenue underscores its primacy in both supply and demand. The region’s 12.09% CAGR stems from the proliferation of gaming cafés, government e-sports grants, and OEM production synergies. Cross-border e-commerce platforms let Vietnamese consumers buy Philippine-assembled webcams, illustrating intra-regional flows that deepen the PC accessories market. Export rebates in China cushion shipping costs, keeping FOB prices competitive even amid freight volatility. Policymakers in India and Indonesia waive import duties on components used in locally assembled peripherals, supporting indigenous value-addition and job creation.

North America benefits from the permanence of hybrid work. Employers subsidize home-office bundles featuring height-adjustable monitor arms and ANC headsets, locking in recurring revenue. The region also leads in AI-centric peripheral launches; early adoption of ChatGPT-enabled mice validates the premium consumers will pay for productivity gains. Regional logistics networks and same-day delivery promises from large retailers amplify online conversion rates, sustaining the channel’s dominance in the PC accessories market.

Europe’s regulatory stance provides a blueprint for sustainability and security. Vendors achieving EN 18031 compliance before the August 2025 deadline gain first-mover advantage in tenders. Circular-economy incentives spur refurbishment programs that funnel refurbished headsets into education markets, extending product lifecycles. However, stricter packaging taxes raise landed costs, nudging brands to experiment with minimalist, plastic-free boxes that double as store displays. These moves align operational expenditure with environmental stewardship, reinforcing the region’s influence on global design philosophies.

Market Concentration

The PC accessories market remains moderately fragmented. Logitech, Corsair and Turtle Beach together hold roughly one-third of global revenue, yet dozens of challenger brands erode pricing power. Corsair’s USD 110 million Fanatec purchase grants entry into the USD 1 billion sim-racing niche growing 20% annually. Turtle Beach’s USD 118 million PDP acquisition consolidates console controllers and multiplatform headsets, seeking scale to weather pricing pressure. Logitech leverages a 137-patent portfolio to drop modular mice and AI-enabled keyboards that command premium tags.

Private-label competition intensifies as e-commerce giants push house brands with near-zero marketing spend. To counter, incumbents bundle cloud software that tracks battery life, remaps keys, and integrates productivity analytics—services white-label peers struggle to replicate. EU cybersecurity rules potentially widen this moat by making compliance audits expensive for smaller firms. Sustainability also morphs into a competitive lever; brands boasting 85% recycled plastics secure Amazon “Climate Pledge Friendly” flags, boosting visibility.

Partnership ecosystems flourish: HP/HyperX releases 3D-printable mouse shells that invite community designs, while MSI enables hot-swappable switches using open-spec sockets. Such openness entices enthusiasts and extends product longevity. In the future, market share battles will pivot on AI-driven differentiation, security certifications, and circular-economy credentials rather than raw sensor DPI or RGB effects.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

PC accessories are any device placed on the computer that is capable of providing additional capabilities or features without requiring it. The computer printer provides the computers with printing capability and is a good example of such an accessory.

The PC accessories market is segmented by products (mice (gaming and non-gaming (enterprise and consumer)), keyboards (gaming and non-gaming (enterprise and consumer)), headsets (gaming and personal, and non-gaming (commercial)), monitor arms, gaming chairs, and webcams) and geography (North America (United States and Canada), Europe (Germany, United Kingdom, France, Italy, Russia, Switzerland, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa)).

The market sizes and forecasts are provided in value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.