Mexico Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

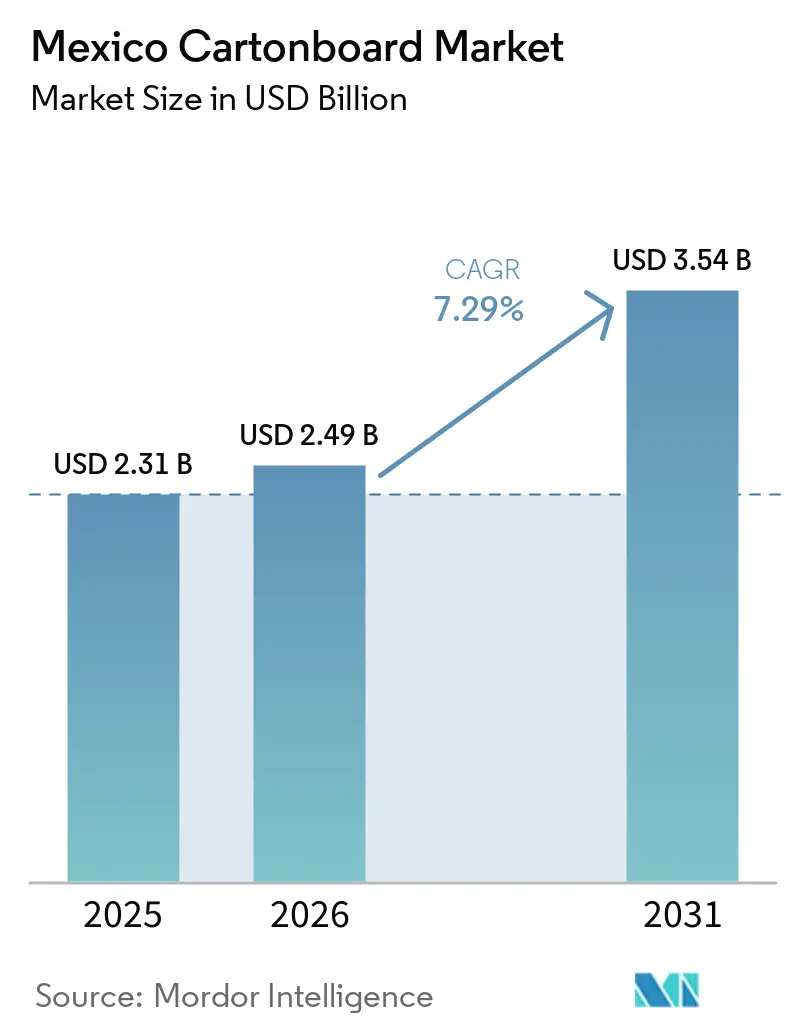

| Base Year Market Size (2025) | USD 2.31 Billion |

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

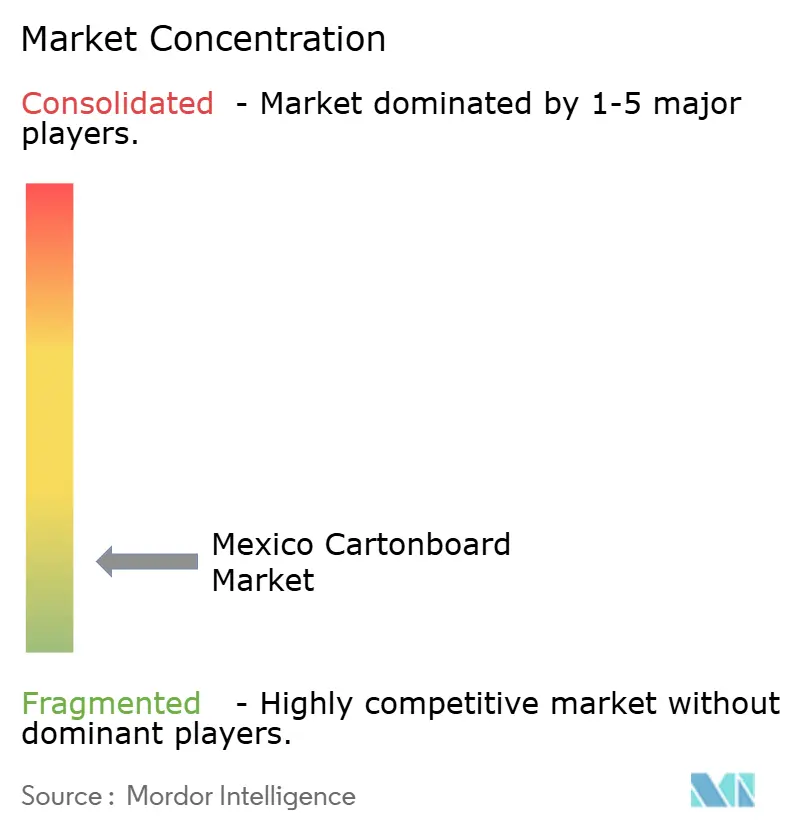

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Cartonboard Market Analysis by Mordor Intelligence

The Mexico cartonboard market size is projected to expand from USD 2.31 billion in 2025 and USD 2.49 billion in 2026 to USD 3.54 billion by 2031, registering a CAGR of 7.29% between 2026 to 2031. The Mexican cartonboard market in 2026 reflects a demand recovery after boxboard consumption in Mexico declined 2.8% in 2025, as tighter credit conditions and softer processed food export volumes weighed on buying activity. Recovery is being supported by mill operating rates moving to 78%, import substitution after Mexico's 2024 tariff measures on cartonboard from non-trade-agreement countries, and a sharper tilt toward domestic consumption channels. Capacity commitments by large international packaging groups are also raising the operating threshold in the Mexico cartonboard market, as players invest ahead of medium-term demand rather than only current volumes. The January 2026 circular economy law is changing packaging design and compliance requirements in ways that favor integrated recycling capabilities and larger converting platforms. These shifts keep the Mexico cartonboard market tied to food consumption, premium packaged goods, nearshoring-led manufacturing, and North American supply chain integration.

Key Report Takeaways

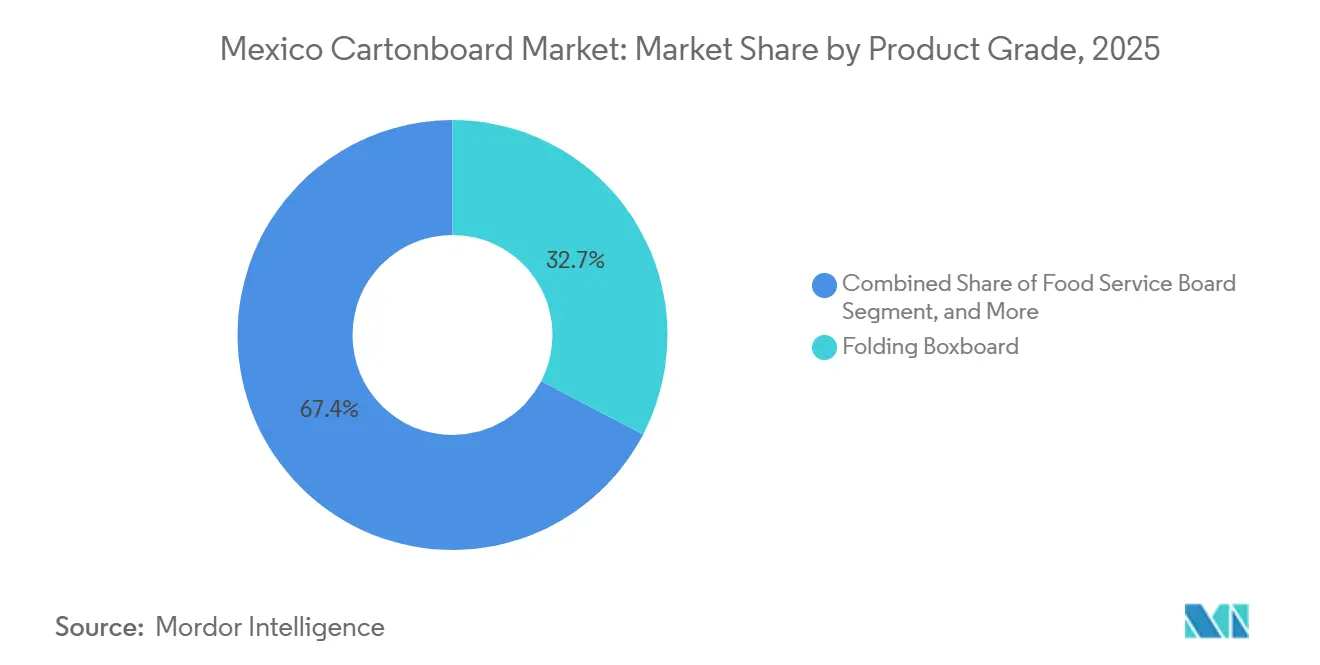

- By product grade, folding boxboard captured 32.65% of the Mexico cartonboard market share in 2025.

- By packaging format, the Mexico cartonboard market size for the liquid packaging segment is forecast to advance at a 7.91% CAGR through 2031.

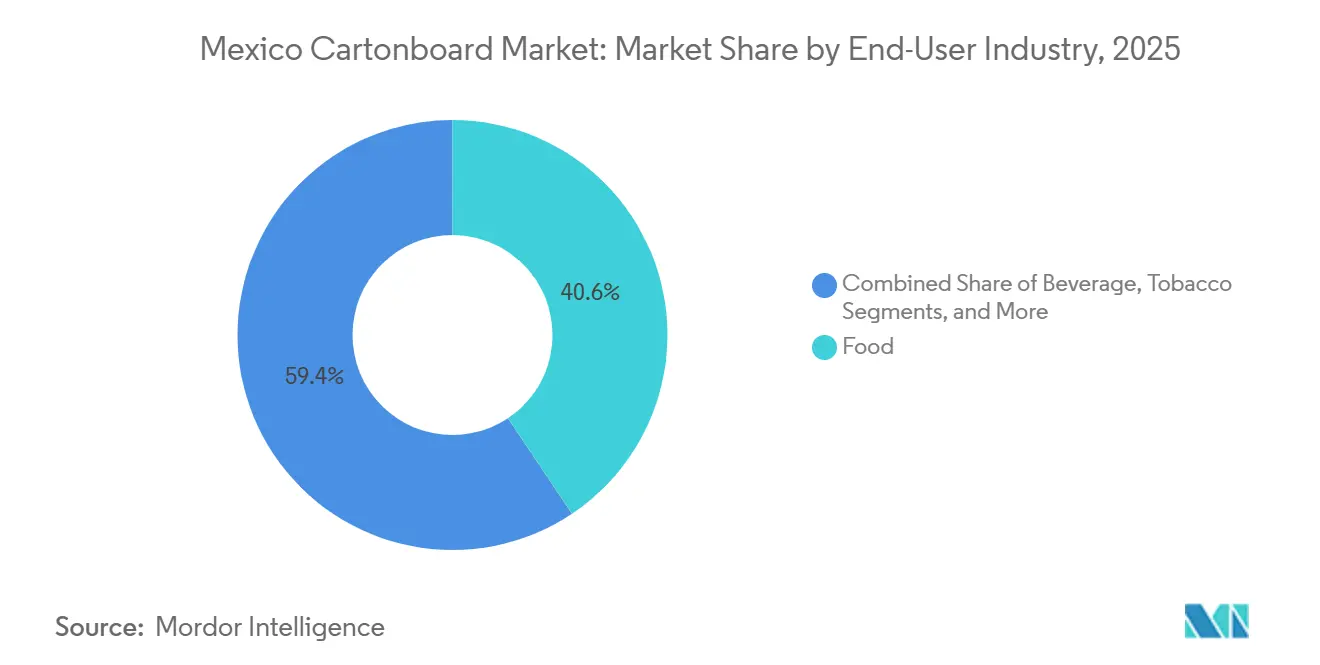

- By end-user industry, food captured 40.63% of the Mexico cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Packaged Food And Modern Retail Demand | +2.1% | National, concentrated in Mexico City, Guadalajara, Monterrey metro areas | Short term (≤ 2 years) |

| Sustainability Shift Toward Recyclable Fiber-Based Packaging | +1.5% | National, early adoption in Nuevo León, Mexico City, and Querétaro industrial zones | Medium term (2-4 years) |

| Premiumization In Beauty, Personal Care, And Shelf-Ready Food Packs | +0.9% | Urban centers nationwide, particularly Mexico City, Guadalajara, and Monterrey | Long term (≥ 4 years) |

| Rising Secondary Packaging Needs In Pharmaceutical And Healthcare Products | +0.7% | National, with primary gains in Mexico City, Jalisco, and Nuevo León pharmaceutical clusters | Medium term (2-4 years) |

| Circular Economy Law-Induced Circular Design And EPR Readiness | +0.5% | National, with early compliance gains in CDMX, Monterrey, and Guadalajara metro areas | Medium term (2-4 years) |

| Aseptic Small-Format Capacity Expansion In Mexico | +0.4% | Querétaro, Baja California, and Estado de México manufacturing corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Packaged Food And Modern Retail Demand

Modern retail penetration and wider packaged food adoption continued to support structural cartonboard demand in Mexico, even as export-facing processed food shipments faced pressure in 2025. Mexico's quick-service restaurant channel exceeded USD 73 billion in systemwide sales in 2025, which shows the scale of branded food consumption formats that rely on cartons, cups, lids, and carry-out packaging.[1]Arcos Dorados Holdings Inc., “Form 6-K: Full-Year 2025 Results,” Stock Titan, stocktitan.net Arcos Dorados reported full-year 2025 adjusted EBITDA of USD 575.2 million, indicating solid operating conditions across large franchise systems that require steady packaging procurement. In March 2026, The Wendy's Company finalized two franchise agreements to build more than 60 new restaurants across Mexico, with expansion centered on Chihuahua, Nuevo León, Baja California, and Sonora.[2]The Wendy's Company, “The Wendy's Company Announces More Than 60 New Restaurants in Mexico,” PR Newswire, prnewswire.com That rollout supports recurring demand for food service board and branded paper-based service packaging, which makes this demand stream less exposed to the broader cartonboard cycle than export-linked food processing volumes. Nearshoring-led population concentration in northern manufacturing cities adds another layer of support because it lifts modern retail throughput and reinforces domestic consumption channels in the Mexico cartonboard market

Sustainability Shift Toward Recyclable Fiber-Based Packaging

The move from plastic-heavy formats toward fiber-based packaging gained legal backing in January 2026 when Mexico's General Law on Circular Economy took effect and made extended producer responsibility a binding policy tool. Producers and importers are required to file Circular Management Plans once SEMARNAT publishes sector-specific agreements, and that shifts packaging decisions from voluntary preference to compliance planning. This structure gives recyclable cartonboard a stronger position than multi-material flexible packaging in applications where brand owners need shelf display, traceability, and recoverability. The compliance timetable is also unlikely to fall evenly across the value chain, because larger multinational brand owners are positioned to face earlier and more formal obligations than smaller domestic producers. That uneven timing could move large fast-moving consumer goods accounts toward compliant fiber solutions faster than the rest of the market. Bio Pappel's Urban Forest closed-loop model, reviewed by Environment Minister Alicia Bárcena in February 2026 under Plan México, shows how integrated recycled-fiber players are positioning themselves as infrastructure partners for this shift.

Premiumization In Beauty, Personal Care, And Shelf-Ready Food Packs

Premium cartonboard demand in cosmetics and personal care packaging is rising faster than broad cartonboard consumption as brand owners invest in tactile finishes, stronger shelf impact, and cleaner print execution across modern retail channels. Solid bleached board and higher-grade folding boxboard remain central in this application cluster because they offer the surface brightness, coating response, and print definition needed for premium packaging. Mexico's role as a manufacturing base for both domestic beauty products and exports to the United States means premium board demand is not tied only to local spending patterns. This keeps the Mexican cartonboard market exposed to higher-value packaging programs even when volume growth in lower-specification applications turns uneven. Cosmetics and toiletries formats also raise the quality bar for domestic converters, as brand owners increasingly expect GC1 or SBS-equivalent performance in high-graphics folding cartons. MM Group's collaboration with Foli ES on cartonboard sheeting and MCM recycled-board lamination optimization shows how Mexico's converting base is aligning with tighter board performance expectations.[3]MM Group, “Foli and MM Board and Paper Collaborate to Optimise Cartonboard Sheeting and Printing Performance,” MM Group, mm.group

Rising Secondary Packaging Needs In Pharmaceutical And Healthcare Products

Pharmaceutical secondary packaging is becoming a more distinct source of demand in the Mexico cartonboard market because it depends on technical compliance rather than broad consumer packaging cycles. Domestic drug manufacturing is scaling up, and export-oriented pharmaceutical shipments require more consistent secondary packaging quality for labeling, tamper evidence, and traceability. These requirements are pushing converters toward investments in Braille embossing, tighter coding systems, and more reliable carton line performance. That raises the barrier for smaller operators and directs regulated accounts toward mid-sized and larger converters with stronger process control. The healthcare packaging segment is projected to grow at a 7.98% CAGR through 2031, placing it ahead of the overall market and supporting demand for cleaner, higher-specification folding boxboard and solid bleached board. Mexico's position along the USMCA corridor adds to this trend, as converters can serve North American pharmaceutical distribution from a lower-cost manufacturing base with a growing export orientation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Fiber And Imported Cartonboard Costs | -1.1% | National, with acute exposure in northern and central mills reliant on imported board grades | Short term (≤ 2 years) |

| Competition From Flexible Packaging In Single-Serve And Convenience Uses | -0.8% | National, concentrated in Mexico City, Guadalajara, Monterrey consumer markets | Medium term (2-4 years) |

| Uneven Recovery Infrastructure For Post-Consumer Cartons | -0.4% | National, with infrastructure gaps most acute outside major metropolitan areas | Long term (≥ 4 years) |

| Tighter Traceability And Coding Complexity On Regulated Packs | -0.3% | Pharmaceutical clusters in CDMX, Jalisco, and Nuevo León | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Fiber And Imported Cartonboard Costs

Mexico remains dependent on imported virgin-fiber cartonboard grades, especially solid bleached board and higher-brightness folding boxboard that domestic mills do not produce at scale. That exposure ties converters to global pulp cycles, freight rate swings, and cross-border supply changes in a way that recycled-fiber domestic producers do not face. Brazil's cartonboard exports to Mexico fell from nearly 25,000 tonnes in January to July 2024 to less than 2,700 tonnes in the same period of 2025 after Mexico imposed tariffs of 25-35% on imports from countries without trade agreements. The tariff action was intended to support domestic producers, but it also raised near-term cost pressure for converters that still needed imported premium grades. The shift also redirected attention toward Chinese supply, and Mexico already represented more than 40% of total Chinese boxboard exports to South America in 2024. That substitution reduces one dependency but creates another, keeping input cost volatility a meaningful drag on the Mexican cartonboard market.

Competition From Flexible Packaging In Single-Serve And Convenience Uses

Flexible packaging continues to take volume from cartonboard in single-serve, sachet, and convenience applications across food and personal care categories. Its lower weight, strong barrier performance, and established economics in Mexico's informal retail channel give it a durable position in price-sensitive use cases. Sauces, condiments, and personal care sachets remain key examples where multi-layer pouches replace cartons that might otherwise serve the lower end of the consumer market. The growth of on-demand food delivery adds another substitution path, as lightweight, moisture-resistant, flexible formats often fit those logistics better than rigid paperboard structures. This pressure is most visible in convenience-led urban consumption patterns, where pack function and unit cost often matter more than shelf presence. Even so, the Mexican cartonboard market is still expanding at a 7.29% CAGR through 2031, as premiumization, regulation, and demand from formal retail and healthcare applications offset these losses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Food Service Board Accelerates As Folding Boxboard Anchors

Folding boxboard held 32.65% of the Mexican cartonboard market share in 2025, making it the leading product grade by a clear margin over adjacent board types. Its position reflects the fit between Mexico's largest packaging applications and the grade's core strengths, especially print quality, stiffness, and smooth conversion on high-speed erection lines. Packaged food, personal care, and pharmaceutical secondary packaging all rely on these attributes, so demand remains broad rather than tied to a single narrow end use. This also makes folding boxboard a central reference point for the Mexican cartonboard market when converters evaluate performance, substrate substitution, and customer quality expectations.

Solid bleached board remained the premium option for tobacco, luxury cosmetics, and pharmaceutical packs that require higher surface whiteness and cleaner print definition. Solid unbleached board served industrial and selected food-contact uses where fiber strength and a kraft visual profile matter more than visual brightness. White-lined chipboard competed in lower-specification applications, such as private-label food and general consumer goods packaging, where cost discipline outweighed premium print performance. The foodservice board is projected to grow at an 8.12% CAGR through 2031, ahead of the broader Mexico cartonboard industry, as quick-service restaurants, institutional foodservice, and delivery-led formats continue to expand across urban centers. That growth is less tied to broad cartonboard cycle swings because restaurant openings follow franchise commitments, and Wendy's March 2026 plan to add more than 60 restaurants provides visibility into that.[4]SIG Group AG, “SIG Announces Expansion Plan for Its Querétaro Plant to Double Production Capacity in North America,” PR Newswire, prnewswire.com Liquid packaging board is also attracting growing investment attention as aseptic small-format demand for dairy alternatives and single-serve ambient beverages grows, while food-contact compliance standards continue to challenge smaller domestic mills that have not upgraded their board quality systems.

By Packaging Format: Liquid Packaging Gains Ground On Folding Cartons

Folding cartons accounted for 56.17% of the Mexican cartonboard market in 2025, underscoring their widespread use across food, pharmaceuticals, cosmetics, and tobacco. Their role extends from simple tuck-end packs to high-graphics shelf-ready structures, which makes them difficult to displace across a broad application base. This breadth gives the Mexican cartonboard market a stable demand core, even as some niche formats move through faster or slower cycles. It also explains why format leadership remains tied to versatility rather than to premium positioning alone.

Sleeves and trays continued to serve secondary packaging needs in beverage multipacks and retail display-ready configurations, especially where modern trade retailers push for higher shelf efficiency. Other formats, including cups, foodservice containers, and die-cut specialty pieces, remained smaller in scale but rose with restaurant traffic and delivery-oriented consumption. Liquid packaging is projected to grow at a 7.91% CAGR through 2031, driven by major aseptic capacity investments that are repositioning Mexico as a regional production base. SIG Group announced in April 2026 that it would expand its Querétaro plant from 1.5 billion to 3 billion aseptic carton packs per year through a phased MXN 1,910 million (USD 96 million) investment with extrusion integration scheduled by the end of 2028. The plan is expected to remove approximately USD 130 million in annual coil imports to Mexico once complete, indicating that the project affects the supply chain structure as much as plant output. Tetra Pak's earlier investment of more than MXN 1,000 million (USD 53 million) to expand its Mexicali caps plant by at least 60% supports the same direction and strengthens Mexico's role in the North American liquid packaging supply

By End-User Industry: Pharmaceutical Uptick Diversifies Beyond Food Dominance

Food accounted for 40.63% of the Mexican cartonboard market in 2025, which kept it as the anchor end-user industry by a wide margin. Demand came from bakery, confectionery, frozen food, and dry packaged goods that require moisture-resistant coatings and reliable high-speed conversion. This leadership reflects both Mexico's large domestic food consumption base and its role as a packaged food exporter under the USMCA framework. The food segment, therefore, provides the Mexican cartonboard market with a recurring baseline demand tied to staple consumption and branded retail packaging requirements.

Beverages contributed through liquid packaging board and folding carton multipacks, while tobacco remained a smaller but high-specification outlet for premium solid bleached board and solid unbleached board. Cosmetics and toiletries packaging also expanded with premiumization in the Mexico City, Guadalajara, and Monterrey metropolitan areas, which supported higher-value folding cartons. Pharmaceutical and healthcare packaging is projected to grow at a 7.98% CAGR from 2026 to 2031, making it the fastest-growing end-user category in the Mexican cartonboard market. That growth is linked to expanding domestic pharmaceutical production in Jalisco, Estado de México, and Nuevo León, as well as to stricter packaging requirements for exports to the United States and Europe. Demand in this area is concentrated in folding boxboard and solid bleached board grades that require high surface cleanliness and print fidelity, which favors import-grade boards or stronger domestic producers. COFEPRIS requirements for labeling, serialization, and tamper evidence continue to set a stable technical threshold in this part of the Mexican cartonboard industry, making healthcare packaging a more specification-driven demand stream than many consumer categories.

Geography Analysis

The Mexico cartonboard market is a single-country market, but demand remains highly uneven across industrial corridors because manufacturing, modern retail, and food processing are concentrated in a limited number of regions. The Bajío-Central corridor, which includes Querétaro, Guanajuato, Jalisco, and Estado de México, is the most active demand cluster because it combines pharmaceutical manufacturing, food and beverage processing, and a broad base of fast-moving consumer goods production. Querétaro and Estado de México also anchor liquid packaging activity through SIG Group and Tetra Pak operations, while Guadalajara supports steady demand for folding boxboard and solid bleached board through its established pharmaceutical and cosmetics base. The corridor's road and rail links to United States border crossings make it attractive for nearshored consumer goods producers that need a stable packaging supply. Manufacturing FDI in Mexico reached USD 40.8 billion in 2025, up 10.8% year on year, and manufacturing accounted for 36% of committed capital, strengthening the investment case for new converting capacity around industrial parks in this region.

Northern Mexico, especially Nuevo León, Chihuahua, Sonora, and Baja California, forms the second major demand node for the Mexico cartonboard market because it is closely tied to export manufacturing under USMCA specifications. Smurfit Westrock's USD 65 million plant in Cajeme, Sonora, which broke ground in December 2025 and is expected to start operations in early 2027, shows a direct bet on stronger converting demand in northwest Mexico. Tetra Pak's Mexicali caps plant exports 60% of its output to the United States, demonstrating that Baja California functions as a trans-border manufacturing platform rather than solely as a domestic demand center. PRONAL Corrugados also opened its first plant in Nuevo León in January 2026 as part of a USD 150 million investment program spanning three facilities, which adds more integrated packaging capacity to the Monterrey industrial cluster.

Mexico City and the broader central valley, including Puebla and Hidalgo, remain the largest consumer demand zone by population and retail throughput, even though converting capacity is spread across many smaller operations. The federal plan to establish a Pole of Circular Economy for Well-Being in Puebla will bring more centralized recycled-fiber infrastructure to this region, which could support recycled-grade converters. The 2026 DBGIR report showed that Mexico generated more than 139,000 tonnes of municipal solid waste each day, while only 5% received treatment. That gap shows why post-consumer carton recovery still limits the scale of recycled fiber outside major metropolitan areas. It also shows why infrastructure investment remains a long-term support factor for the Mexican cartonboard market, especially where recycled board grades can reduce input exposure.

Competitive Landscape

The Mexico cartonboard market has a two-tier structure, comprising a small group of globally integrated players and a large, fragmented set of domestic converters serving regional and sector-specific needs. Smurfit Westrock, Graphic Packaging, Tetra Pak, SIG Group, and MM Group define the upper end of technical capability and capital intensity, while domestic firms such as Bio Pappel, Cartographic, Grupo Gráfico Romo, and Maquiladora Gráfica Mexicana compete through specialization and customer proximity. This mix keeps the Mexico cartonboard market competitive because large players raise quality and compliance expectations, while local converters remain active in narrower order sizes and niche applications. The result is a market where scale matters in premium and regulated applications, but agility still matters in regional converting.

Capital deployment is one of the clearest signals of rising competitive pressure. SIG Group announced in April 2026 that it would double Querétaro's aseptic carton capacity to 3 billion packs per year by 2028 through a phased investment program, thereby raising the competitive floor in liquid packaging and shifting more processing to Mexico. Smurfit Westrock also broke ground in December 2025 on a USD 65 million plant in Sonora for corrugated, microcorrugated, and high-graphic folding carton production, expanding its presence in a nearshoring-led corridor. Graphic Packaging's 2026 emphasis on free cash flow generation and portfolio discipline following the Waco recycled paperboard investment cycle suggests a more selective investment stance, leaving space for Bio Pappel and mid-tier converters in recycled-grade applications.

White-space opportunities remain strongest in pharmaceutical-grade folding boxboard converting, food service board for delivery-led restaurant formats, and premium cartons for export-oriented personal care packaging. Domestic mid-tier converters such as Cartographic and Maquiladora Gráfica Mexicana are building defensible positions by serving smaller, specification-intensive accounts that larger global groups may not prioritize at lower order volumes. The January 2026 circular economy law could accelerate consolidation, as converters with closed-loop sourcing, recycled-content controls, and compliance documentation will be better positioned once SEMARNAT publishes sector agreements. FSC certification is also becoming more relevant in procurement, and SIG's Querétaro plant has already used this as part of its positioning with brand owners operating in Mexico. That combination of compliance, capital spending, and technical differentiation keeps the Mexican cartonboard market fragmented overall, but more demanding for smaller converters that lack scale or specialty depth.

Mexico Cartonboard Industry Leaders

Tetra Pak International S.A.

SIG Group AG

Smurfit Westrock plc

Graphic Packaging Holding Company

Bio Pappel, S.A.B. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SIG Group AG announced an expansion plan for its Querétaro, Mexico plant to double aseptic carton production capacity from 1.5 billion to 3 billion packs per year by 2028, in a phased investment of MXN 1,910 million (USD 96 million). Phase I, starting in 2026, adds finishing lines and a new printing line in 2027. Phase II integrates extrusion processes by end of 2028 and will eliminate approximately USD 130 million in annual coil imports once complete. The expansion reinforces Mexico's role as a North American liquid packaging board production hub and relocates some European production processes to Querétaro.

- March 2026: The Wendy's Company finalized two franchise agreements to build more than 60 new Wendy's restaurants across Mexico in the coming years, concentrating expansion in Chihuahua, Nuevo León, Baja California, and Sonora. This commitment, citing 7.1% annual growth projections for Mexico's foodservice sector, will generate sustained incremental demand for food service board and branded foodservice carton packaging.

- February 2026: Mexico's Environment Minister Alicia Bárcena visited Bio Pappel's Tizayuca, Hidalgo recycling plant as part of a review of circular economy projects under Plan México, a USD 277 billion development strategy. SEMARNAT confirmed plans to complement the facility with 10 additional recycling plants nationwide by 2030, scaling the infrastructure for post-consumer carton fiber recovery essential to the LGEC's EPR compliance framework.

- January 2026: Mexico's General Law on Circular Economy, LGEC, took effect on January 19, 2026, introducing extended producer responsibility as a binding policy instrument requiring producers and importers to file Circular Management Plans with SEMARNAT once sector-specific agreements are published. This law fundamentally reshapes packaging design obligations for cartonboard producers and converters operating in Mexico across all end-user categories.

Mexico Cartonboard Market Report Scope

The Mexico Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Mexico Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast size of the Mexico cartonboard market?

The Mexico cartonboard market was valued at USD 2.31 billion in 2025, stands at USD 2.49 billion in 2026, and is projected to reach USD 3.54 billion by 2031 at a 7.29% CAGR.

Which product grade leads cartonboard demand in Mexico?

Folding boxboard led with a 32.65% share in 2025 because it fits packaged food, personal care, and pharmaceutical secondary packaging requirements.

Which packaging format is growing fastest in Mexico cartonboard applications?

Liquid packaging is the fastest-growing format, with a projected 7.91% CAGR through 2031, supported by aseptic capacity additions from SIG Group and Tetra Pak.

Why does food remain the largest end-user base for cartonboard in Mexico?

Food held 40.63% share in 2025 because bakery, confectionery, frozen food, and dry packaged goods require recurring carton formats across domestic retail and export channels.

What is driving pharmaceutical carton demand in Mexico?

Pharmaceutical and healthcare packaging is projected to grow at a 7.98% CAGR through 2031 as domestic drug manufacturing expands and export packaging standards become stricter.

What are the main risks affecting cartonboard producers and converters in Mexico?

The main risks are imported fiber and premium board cost volatility, substitution by flexible packaging in convenience uses, and uneven post-consumer recovery infrastructure outside major cities.

Page last updated on: