Asia-Pacific Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

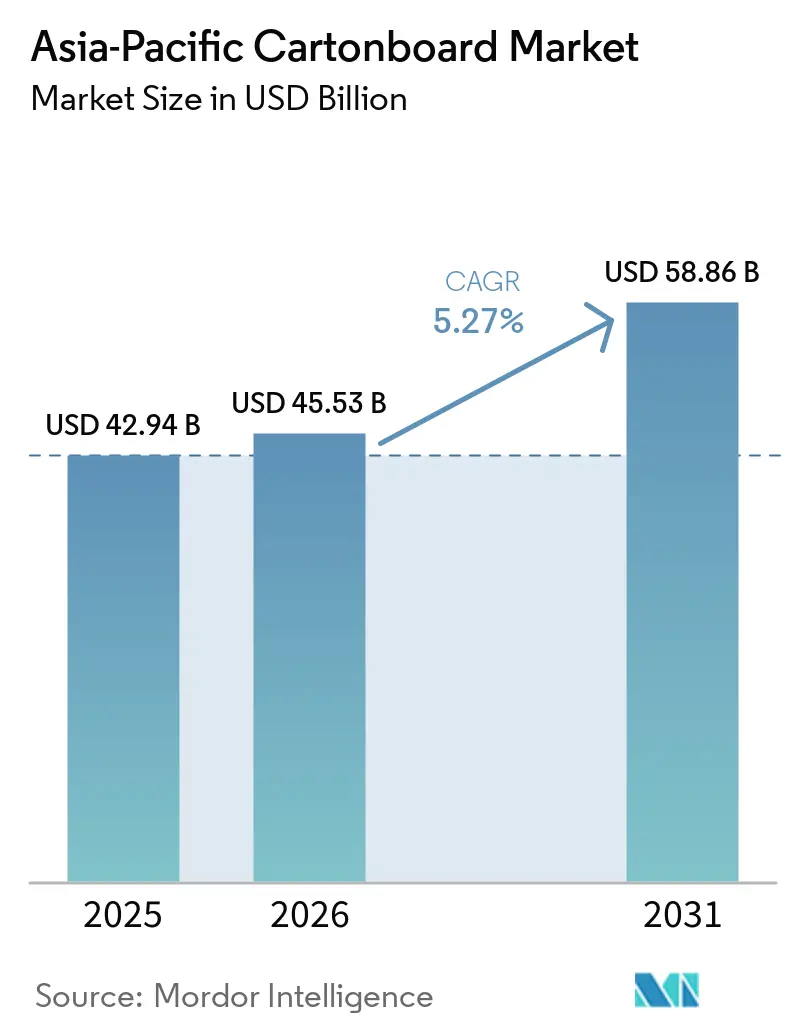

| Base Year Market Size (2025) | USD 42.94 Billion |

| Market Size (2026) | USD 45.53 Billion |

| Market Size (2031) | USD 58.86 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

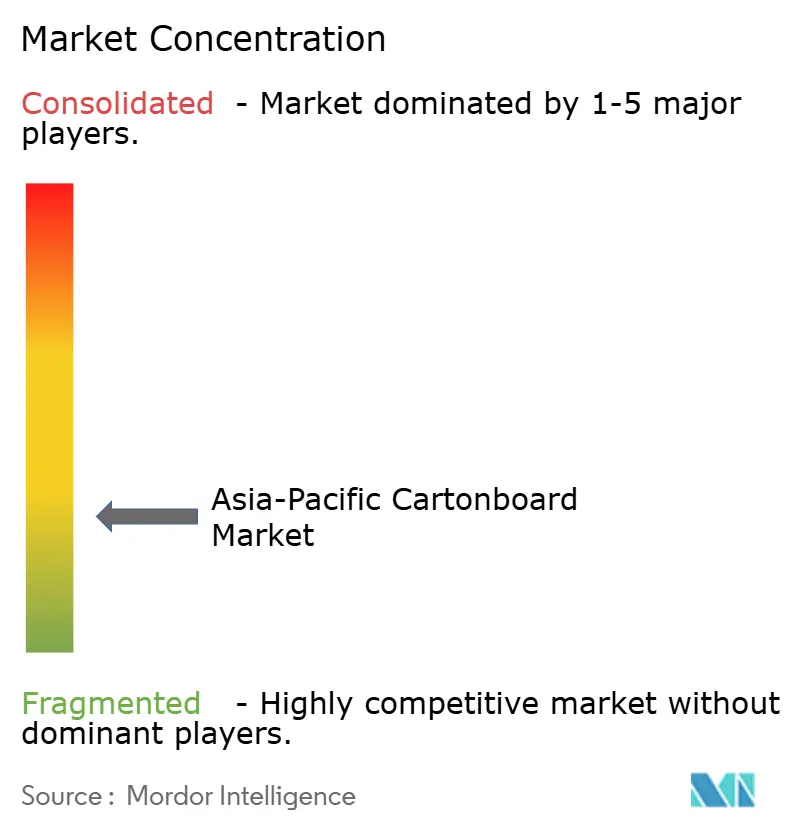

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Cartonboard Market Analysis by Mordor Intelligence

The Asia-Pacific Cartonboard Market size is expected to increase from USD 42.94 billion in 2025 to USD 45.53 billion in 2026 and reach USD 58.86 billion by 2031, growing at a CAGR of 5.27% over 2026-2031.

The Asia-Pacific cartonboard market is being lifted by tighter rules on single-use plastics in China and India, which are pushing brand owners toward recyclable paper-based formats before formal deadlines arrive. Demand is also being supported by a larger processed food base, wider modern retail penetration, and rising use of aseptic packaging for dairy, juice, and functional beverages across South and Southeast Asia. At the same time, the Asia-Pacific cartonboard market is becoming more polarized, with large integrated mills competing hard on scale and cost in standard grades while global specialists protect margins through barrier technologies, certified substrates, and application-specific designs. This mix is keeping pricing firm in premium formats even when average selling prices remain under pressure in more commoditized categories. The main limits on faster expansion remain fiber cost volatility and the continued use of flexible plastics in sub-markets where EPR enforcement still lacks consistency.

Key Report Takeaways

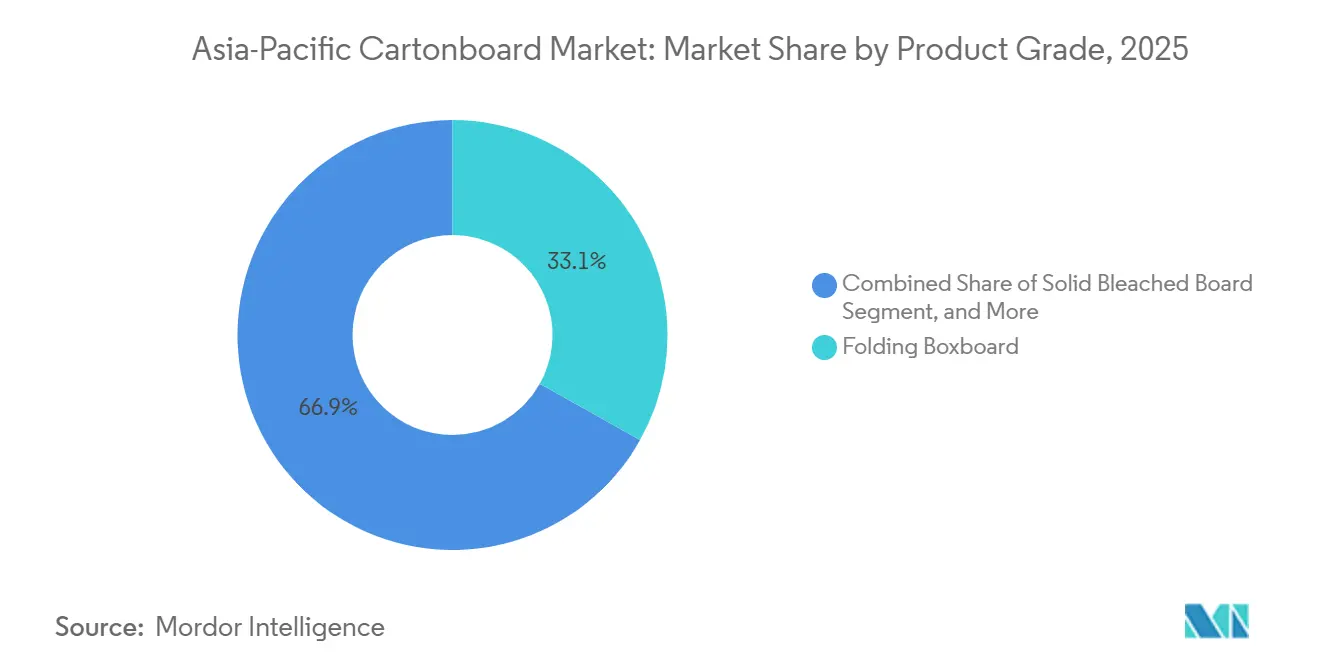

- By product grade, folding boxboard held 33.12% of the Asia-Pacific cartonboard market size in 2025, while liquid packaging board is projected to expand at 5.51% CAGR through 2031.

- By packaging format, folding cartons held 56.78% of the Asia-Pacific cartonboard market share in 2025, while liquid packaging is forecast to grow at 5.55% CAGR through 2031.

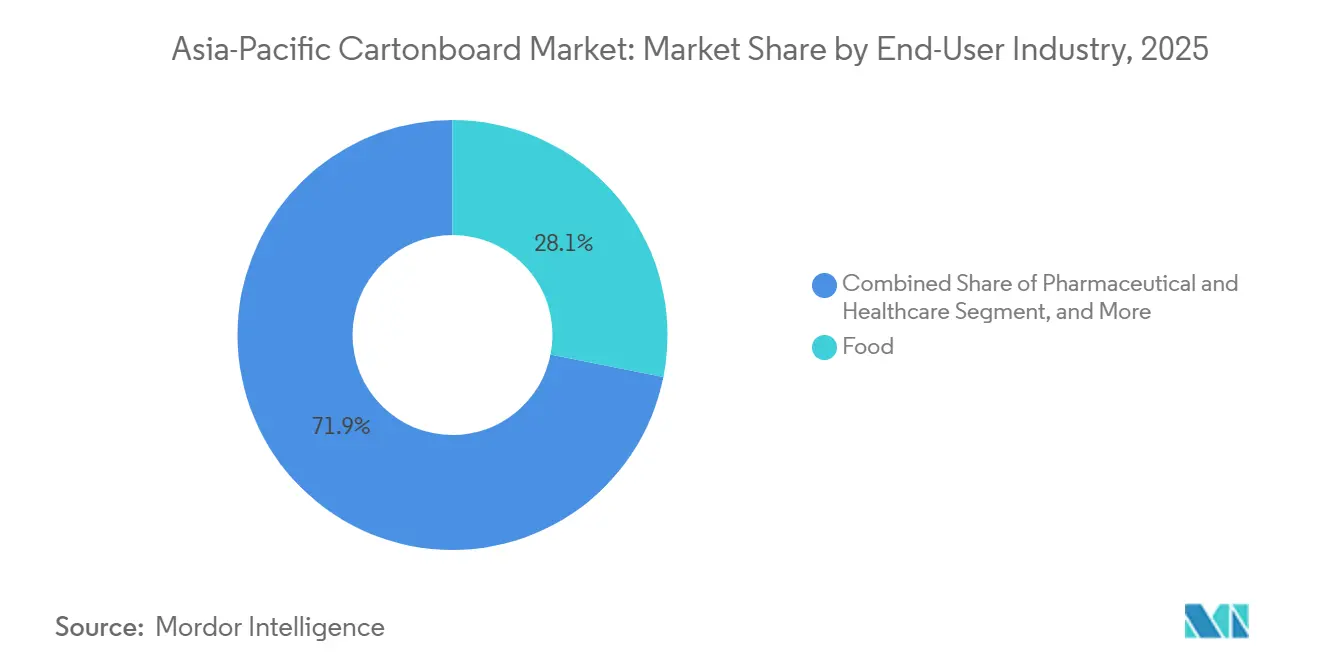

- By end-user industry, food accounted for 28.12% of the Asia-Pacific cartonboard market size in 2025, while pharmaceutical and healthcare is projected to expand at 5.43% CAGR through 2031.

- By geography, China held 43.21% of the Asia-Pacific cartonboard market share in 2025, while India is forecast to advance at 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic Substitution Mandates And Brand Sustainability Targets | +1.8% | Global, strongest in China, India, and ASEAN, Thailand, Vietnam, Indonesia | Short term (≤ 2 years) |

| Packaged Food Demand And Retail Modernization | +1.5% | China, India, and Southeast Asia, Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Beverage And Dairy Carton Demand In Aseptic And Chilled Formats | +1.2% | China, India, Southeast Asia, with spill-over to South Korea and Japan | Medium term (2-4 years) |

| Pharmaceutical And Healthcare Packaging Demand With Traceability And Hygiene Needs | +0.8% | China, India, Japan, South Korea, and export-oriented ASEAN markets | Medium term (2-4 years) |

| PFAS-Free And High-Barrier Board Innovation Unlocking Foodservice Conversion | +0.5% | APAC core markets, with regulatory spill-over from EU compliance requirements | Long term (≥ 4 years) |

| Premiumization And Anti-Counterfeit Print Demand In Beauty, Healthcare, And Tobacco Cartons | +0.3% | China, South Korea, Japan, and premium ASEAN retail clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic Substitution Mandates And Brand Sustainability Targets

India's Plastic Waste Management Amendment Rules took effect from April 2026 and attached EPR fees to non-recyclable packaging, which improves cartonboard's cost position against flexible film in more product categories. China's Green Packaging Law requires 75% of express packaging to be recyclable or reusable by end-2027, which gives converters and brand owners a clear compliance timeline. Enforcement has already become more tangible in parts of China, with Zhejiang using penalties of CNY 50,000, USD 7,000, per violation, which pushes procurement changes forward rather than leaving them to the deadline year. Brand commitments are reinforcing the same shift, and Unilever China stated a goal of moving 90% of personal-care secondary packaging to paper by 2027, removing an estimated 12,000 metric tonnes of flexible plastic each year. South Korea also tightened its EPR framework from January 2026 with stronger label-free and recycled-content requirements, which supports investment in printable and recyclable folding boxboard across the Asia-Pacific cartonboard market.

Packaged Food Demand And Retail Modernization

India's food processing sector expanded 8.7% in 2025, which widened the base for branded retail packaging that depends on folding cartons and coated boxboard rather than plain transit formats. As general trade shifts toward organized retail in India, Indonesia, and Vietnam, brand owners need better shelf appearance, clearer print quality, and more consistent food-contact compliance, which raises demand for higher-value board grades. This change also affects pack design, because more products are moving from simple secondary wrapping toward structured, shelf-ready cartons that hold graphics, traceability elements, and retailer-specific labeling. Indonesia's beverage sector expanded 6.3% in 2025, and that added to demand for branded retail packaging in channels that increasingly value presentation and transport efficiency. In China, Meituan targeted 80% of packaging to be eco-certified, which shows that large digital retail and food delivery platforms are already shaping procurement standards in the Asia-Pacific cartonboard market.

Beverage And Dairy Carton Demand In Aseptic And Chilled Formats

The shift toward local aseptic carton production is shortening lead times and reducing import dependence in parts of South and Southeast Asia. Tetra Pak completed a EUR 97 million, USD 104.8 million, second production line at Binh Duong in Vietnam in July 2025, more than doubling the site's output capacity to 30 billion packs a year and adding 15 packaging formats for markets across Southeast Asia.[1]Tetra Pak International S.A., “Tetra Pak Binh Duong Expansion Accelerates Beverage Carton Packaging Innovation to the Philippines and Wider Asia Pacific Region,” Tetra Pak, tetrapak.com SIG's first aseptic carton plant in Ahmedabad became fully operational with phase 1 capacity of 4 billion sleeves annually, which gives India a local supply base for underpenetrated dairy and juice carton demand. SIG also reported APAC revenue of EUR 892 million, USD 963 million, in 2025, with volume growth tied to aseptic cartons, protein drinks, functional beverages, and co-packing activity across several regional markets. Once filling lines are installed, packaging demand becomes more locked into approved substrates and technical specifications, which gives the Asia-Pacific cartonboard market a longer and more stable volume tail than many flexible formats can match.

Pharmaceutical And Healthcare Packaging Demand With Traceability And Hygiene Needs

China's National Medical Products Administration is enforcing drug traceability requirements, while India's CDSCO framework requires barcoding and authentication features for regulated pharmaceutical supply, which is raising the need for printable and tamper-evident folding cartons.[2]National Medical Products Administration, China, “Drug Traceability System Overview,” National Medical Products Administration, China, nmpa.gov.cn Thailand's pharmaceutical exports grew 9.1% in 2025, and that supported demand for cartons that can meet traceability, labeling, and compliance requirements across export markets. This trend favors mills and converters that can supply certified fiber traceability, low-fluorescence surfaces, and stable print performance for codes, tamper evidence, and digital verification tools. It also reduces the room for commodity-grade suppliers in export-linked drug packaging, because multinational buyers are aligning specifications across countries rather than treating each market separately. As a result, the Asia-Pacific cartonboard market is seeing more value move toward board that supports hygiene, data integrity, and regulatory auditability in healthcare packaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virgin Pulp And Recovered Fiber Cost Volatility | -1.0% | Global, particularly affecting import-dependent markets in Japan, South Korea, and India | Short term (≤ 2 years) |

| Competition From Flexible Plastic And Lightweight Alternative Formats | -0.8% | APAC-wide, most acute in Southeast Asia and tier-2 cities in China | Medium term (2-4 years) |

| Incomplete Collection And Recycling Economics For Multilayer Liquid Cartons | -0.5% | India, Southeast Asia, and tier-2 and tier-3 cities across China | Long term (≥ 4 years) |

| Food-Contact Compliance And Barrier-Performance Trade-Offs In Sensitive Uses | -0.3% | Japan, South Korea, Australia, and export-oriented Chinese converters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Virgin Pulp And Recovered Fiber Cost Volatility

Fiber remains the clearest near-term margin pressure point for cartonboard producers across the region. Hardwood pulp prices recorded 30% inflation during 2024, and that raised production costs for mills that depend on purchased pulp rather than captive fiber systems. Asian mills responded with price hikes of USD 31.50 per tonne for early 2025, which shows how quickly raw material swings pass through to converter procurement and customer contracts. Mills that lack plantation control or deep recovered fiber networks remain more exposed to spot cycles and currency weakness on imported pulp. China is reducing part of that exposure through greater pulp-paper integration, but Japan and South Korea still face a more structural dependence on imported board-grade fiber, which keeps costs less predictable in the Asia-Pacific cartonboard market.

Competition From Flexible Plastic And Lightweight Alternative Formats

Flexible plastic still holds a cost advantage in several snack, condiment, and small beverage applications where regulation is not enforced with equal intensity across all channels. That advantage is strongest in tier-2 and tier-3 cities and in less formal retail systems, where board conversion does not always receive the same compliance push seen in large urban markets. Flexible formats are also reducing resin use per pack and improving barrier performance, which narrows the technical gap that once made cartonboard the easier choice in many shelf-stable uses. Mono-material films are now being positioned as recyclable options ahead of tougher EPR rules, and that weakens part of the policy-led demand tailwind for board. This means some substitution cycles in the Asia-Pacific cartonboard market are likely to stay slower than expected, especially in price-sensitive sub-markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Aseptic Investment Supports Liquid Board Growth

Folding boxboard commanded a 33.12% revenue share in 2025 and remained the largest product grade in the Asia-Pacific cartonboard market. Its lead came from its wide use in food, cosmetics, and pharmaceutical secondary packaging, where print quality, stiffness, and good converting behavior matter more than the lowest possible material cost. The grade also benefits from broad regional availability, because integrated mill and converter networks in China, Japan, and India keep supply relatively steady for mainstream applications. Solid bleached board still serves premium niches in tobacco and healthcare packaging, while white-lined chipboard stays relevant in cost-sensitive secondary packs in markets with mature recovered fiber systems such as Japan and South Korea.

Liquid packaging board is projected to grow at 5.51% CAGR through 2031, making it the fastest-growing grade and one of the clearest expansion pockets within the Asia-Pacific cartonboard industry. That rise is tied to new aseptic and chilled dairy infrastructure in India and Southeast Asia, where more local carton production is reducing import dependence and improving supply flexibility. Tetra Pak's February 2026 rollout of paper-based barrier technology on high-speed A3/Speed lines in Asia, with Maeil Dairies in South Korea as the first producer globally to implement it, shows how substrate innovation is widening the addressable board base without giving up throughput. Food service board is also adding incremental demand as quick-service and takeaway formats move toward PFAS-free cups and trays. Solid unbleached board remains a smaller but steady part of the mix, especially where strength and cost balance matter more than premium surface appearance.

By Packaging Format: Folding Cartons Remain The Region's Core Format

Folding cartons accounted for 56.78% of the Asia-Pacific cartonboard market share in 2025, which kept them well ahead of every other packaging format. Their position reflects the scale of fast-moving consumer goods retail in China, Japan, and South Korea, where brand visibility, structured pack design, and dependable line efficiency still favor cartons. The format is also benefiting from higher-resolution print, shorter production runs, and more frequent design changes, all of which help converters capture better value even when some mature categories grow more slowly. This makes folding cartons both the largest volume base and one of the most commercially resilient parts of the Asia-Pacific cartonboard market.

Liquid packaging is expected to expand at 5.55% CAGR through 2031 and is the fastest-growing format in the Asia-Pacific cartonboard market. Its momentum is supported by dairy and beverage launches, school milk programs, institutional demand, and added filling capacity across India and Southeast Asia. Sleeve and tray formats are also gaining ground in e-commerce secondary packaging and cold chain distribution because they stack well and can lower dimensional weight pressure. Other foodservice formats are moving forward as PFAS-free barrier coatings improve the commercial case for fiber-based packs. APP Group's Foopak Bio Natura platform, which is certified for food contact and reported less than 20 milligrams per kilogram of total fluorine, shows how foodservice conversion is already happening at scale in the Asia-Pacific cartonboard industry.

By End-User Industry: Food Leads While Healthcare Gains Pace

Food retained the largest end-user share at 28.12% in 2025 and continued to provide the broadest demand base for the Asia-Pacific cartonboard market. The segment is supported by packaged food growth, organized retail expansion, and the need for print-ready, food-contact compliant packaging in India and Southeast Asia. Beverage ranked next, helped by dairy, juice, protein drink, and health-focused launches across South Korea and Japan that continue to favor both folding cartons and liquid board. Tobacco still uses premium solid bleached board with anti-counterfeit printing in China and Indonesia, even though long-term smoking trends remain mixed across the region. Cosmetics and toiletries are also sustaining demand as brands in Japan and South Korea shift more pack value into secondary cartons with stronger print quality and shelf presentation.

Pharmaceutical and healthcare is projected to rise at 5.43% CAGR through 2031, giving it the fastest growth profile within the Asia-Pacific cartonboard market size by end-user industry. China's drug traceability framework and India's authentication requirements are steadily lifting the minimum technical standard for pharmaceutical cartons across domestic and export channels. This is shifting procurement away from commodity grades and toward certified, traceable folding boxboard that can support tamper evidence, serialization, and reliable code printing. Other end-user groups, including toys, apparel, household goods, and electrical products, still provide a broad long tail of demand that is increasingly shaped by sustainability targets and e-commerce packaging rules.

Geography Analysis

China held 43.21% of the Asia-Pacific cartonboard market share in 2025, which made it the clear regional leader. Its lead comes from a large mill base, extensive converting capacity, and a broad consumer goods and food delivery ecosystem that still absorbs major carton volumes. Meituan's push toward eco-certified packaging shows how platform-led procurement is already supporting recyclable carton formats in large urban delivery networks. New bleached folding boxboard capacity has strengthened domestic supply, while tighter environmental standards are making it harder for smaller producers to remain competitive. China's Green Packaging Law and related recyclability targets are also pushing procurement toward producers with stronger recovery and compliance systems.

India is forecast to grow at 6.32% CAGR through 2031, making it the fastest-growing geography in the Asia-Pacific cartonboard market. Plastic waste rules and EPR-linked compliance from 2026 are nudging brand owners toward paper-based packaging that is easier to report, recover, and defend under regulatory review. Local carton and board production is widening, and the build-out of aseptic carton infrastructure is adding another source of demand for liquid packaging board and related converting activity. TERI reported a 48% national recycling rate for used beverage cartons in 2025, up from 29% in 2011, although the 63.66% rate in surveyed cities still shows that collection quality remains uneven outside major urban centers.

Japan and South Korea remain mature but innovation-active markets, where demand is tied more to premium food, cosmetics, and pharmaceutical packaging than to rapid volume growth. South Korea's extended EPR system took effect in January 2026 with stronger label-free design and recycled-content requirements, which is steering brand owners toward compliant board formats.[3]Korea Environment Corporation, “Extended Producer Responsibility (EPR) System Overview 2026,” Korea Environment Corporation, keco.or.kr Japan's sustainable packaging certification framework, launched in January 2026, favors low-carbon mono-material corrugated and folding carton formats and supports mills with stronger environmental credentials. Indonesia, Vietnam, Thailand, the Philippines, and Malaysia are the next growth layer, and SCG Packaging's THB 10,000 million, USD 280 million, investment budget for 2026 in Vietnam and Indonesia shows continued confidence in the region's demand trajectory within the Asia-Pacific cartonboard market.

Competitive Landscape

The Asia-Pacific cartonboard market is moderately concentrated at the mill level, but it remains much more fragmented at the converting and filling levels. Large integrated Asian producers, including Nine Dragons Paper, Oji Holdings, Nippon Paper Industries, and ITC Limited, compete mainly on fiber access, scale, and regional supply reach. Global specialists, including Tetra Pak, SIG Group, and Stora Enso, compete more on barrier performance, food-contact compliance, and technical support for demanding end uses. This split keeps standard-grade pricing under pressure, but it also leaves room for better margins in high-barrier, premium-print, and regulated healthcare applications. Oji Holdings' Medium-Term Management Plan 2027, released in May 2025, signaled a stronger push into sustainable and liquid packaging after the April 2024 acquisition of Walki Holding Oy added barrier paper and plastic-reducing technologies to its portfolio.[4]Oji Holdings Corporation, “Integrated Report 2025,” Oji Holdings Corporation, ojiholdings.co.jp

Tetra Pak and SIG are widening the technology gap through paper-based and aluminum-free barrier systems that are designed for live commercial aseptic lines rather than limited pilot use. These moves matter because once fillers approve a board system for speed, shelf life, and migration performance, supplier switching becomes slower and more costly. The clearest white space remains in high-barrier foodservice board, pharmaceutical cartons that need traceability features, and premium folding cartons for beauty and personal care in India and Southeast Asia. Smaller converters in Vietnam, Indonesia, and the Philippines are also winning selected mid-tier accounts by offering shorter runs and faster design changes than larger scale suppliers usually provide.

Compliance remains a strong filter across the Asia-Pacific cartonboard market, because ISO 22000, FSSC 22000, fiber traceability, and food-contact checks raise the entry barrier in premium segments. Producers that meet these requirements can protect pricing better, while commodity suppliers stay more exposed to substitution and spot-price competition. SCG Packaging's 2026 expansion budget, Tetra Pak's February 2026 rollout of paper-based barrier packaging on high-speed lines, and SIG's fully operational India aseptic carton plant show that leading companies are still investing ahead of demand growth. Within the wider packaging peer group, companies focused mainly on metal cans, PET bottles, or glass remain less central than board-focused suppliers when evaluating the competitive shape of the Asia-Pacific cartonboard market.

Asia-Pacific Cartonboard Industry Leaders

Nine Dragons Paper (Holdings) Limited

Oji Holdings Corporation

Nippon Paper Industries Co., Ltd.

SCG Packaging Public Company Limited

Rengo Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Tetra Pak extended its paper-based barrier packaging technology to high-speed Tetra Pak A3/Speed filling lines in Asia, with South Korea's Maeil Dairies becoming the first producer globally to implement the solution for soya beverage. The milestone accelerates the transition toward low-carbon, renewable packaging substrates on high-throughput commercial lines and expands the addressable cartonboard volume in the premium dairy segment.

- January 2026: SCG Packaging allocated a THB 10,000 million (approximately USD 280 million) investment budget for 2026, covering M&A, business expansion, and machinery upgrades. The company identified Vietnam, Indonesia, and India as priority expansion markets, targeting an EBITDA of THB 18,300 million for 2026 and increasing average packaging paper capacity utilization to approximately 90%.

- December 2025: SIG Group's first aseptic carton manufacturing plant in India, located in Ahmedabad, Gujarat, became fully operational. Phase 1 capacity reached approximately 4 billion sleeves annually, with plans to scale to 10 billion sleeves in subsequent phases, directly serving India's fast-growing dairy and juice carton market and supporting regional export.

Asia-Pacific Cartonboard Market Report Scope

The Asia-Pacific Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Asia-Pacific Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries), and Geography (China, India, Japan, South Korea, Indonesia, and Rest of Asia-Pacific). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Rest of Asia-Pacific |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the size of the Asia-Pacific cartonboard market in 2026 and where is it headed by 2031?

The Asia-Pacific cartonboard market is valued at USD 45.53 billion in 2026 and is projected to reach USD 58.86 billion by 2031, growing at a 5.27% CAGR.

Which product grade is leading cartonboard demand across Asia-Pacific?

Folding boxboard leads by product grade with a 33.12% revenue share in 2025, supported by broad use in food, cosmetics, and pharmaceutical secondary packaging.

Which packaging format is growing fastest in the region?

Liquid packaging is the fastest-growing format, with a projected 5.55% CAGR through 2031, driven by dairy, juice, and aseptic packaging investments across India and Southeast Asia.

Why is pharmaceutical packaging becoming more important for cartonboard suppliers?

Pharmaceutical and healthcare packaging is forecast to grow at 5.43% CAGR through 2031 because serialization, barcoding, tamper evidence, and traceability rules are raising board specifications.

Which country leads regional demand and which one is expanding fastest?

China holds the largest regional share at 43.21% in 2025, while India is the fastest-growing geography with a 6.32% CAGR through 2031.

What are the main risks for producers and converters in this space?

The biggest risks are fiber cost volatility and continued competition from lightweight flexible plastics in sub-markets where EPR enforcement is still uneven.

Page last updated on: