France Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 2.06% CAGR |

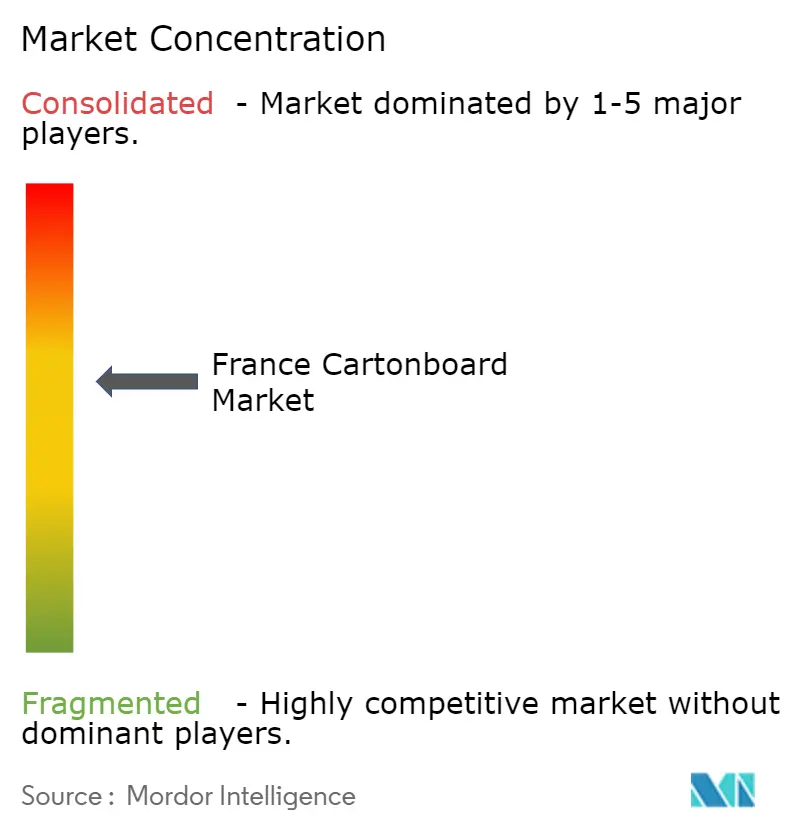

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Cartonboard Market Analysis by Mordor Intelligence

The France Cartonboard Market size is projected to be USD 1.65 billion in 2025, USD 1.68 billion in 2026, and reach USD 1.86 billion by 2031, growing at a CAGR of 2.06% from 2026 to 2031.

The growth rate remains modest, but the value mix is shifting toward higher-specification grades that command better pricing and support revenue expansion. The France cartonboard market is moving away from purely commodity supply and toward specialty boards that combine recyclability, print quality, and compliance performance. This change is strongest where premium brands need better visual appeal and tighter technical standards at the same time. Regulatory pressure is also making board substitution more durable, which gives producers and converters more room to compete through grade differentiation, certified performance, and application-specific offerings. The France cartonboard market therefore shows a steady headline profile, but the underlying demand mix is becoming more favorable for premium and technically capable suppliers.

Key Report Takeaways

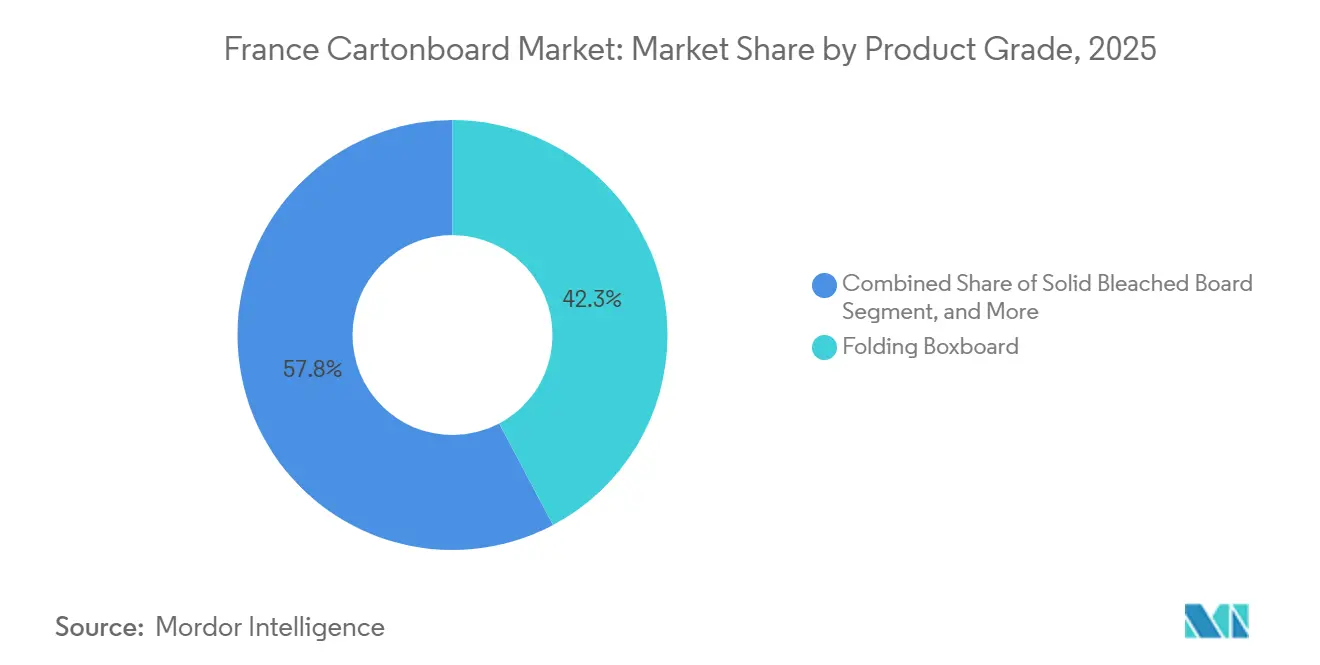

- By product grade, Folding Boxboard led with 42.25% share in 2025, while Solid Bleached Board is forecast to expand at a 5.19% CAGR through 2031 in the France cartonboard market.

- By packaging format, folding cartons held 66.12% of market value in 2025, while liquid packaging is projected to record the fastest growth at a 4.78% CAGR through 2031.

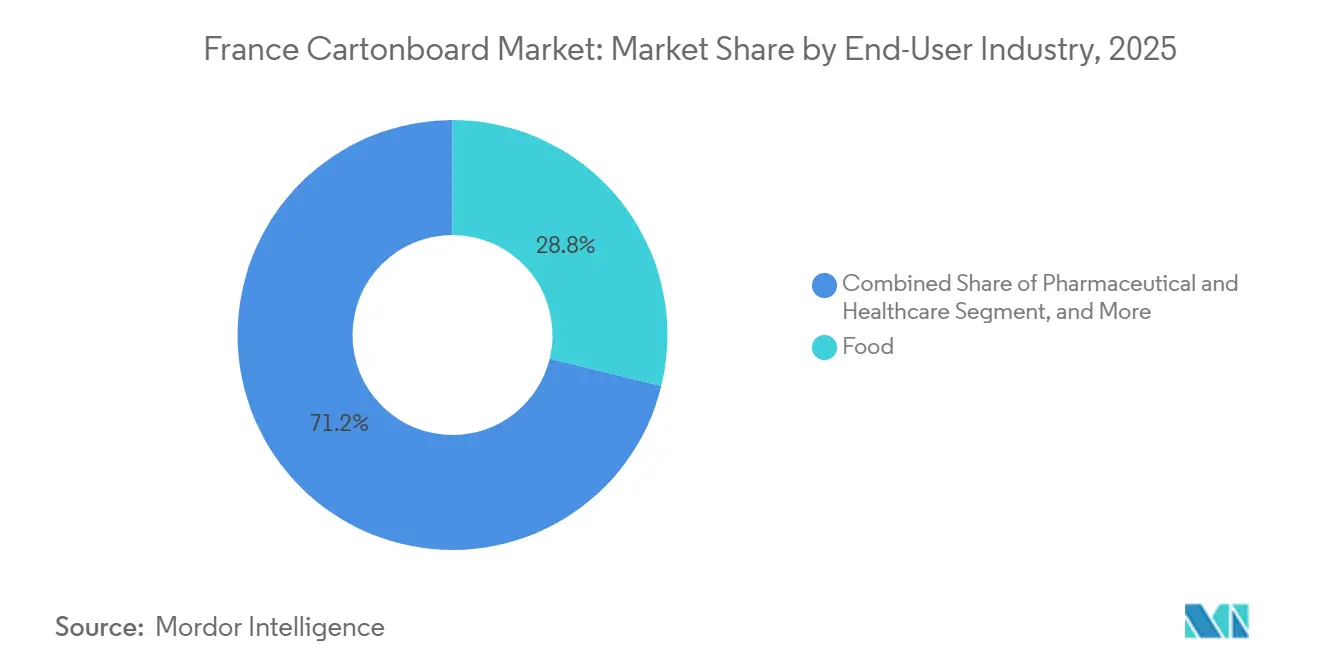

- By end-user industry, food accounted for 28.81% of 2025 revenue, while cosmetics and toiletries is expected to advance at a 5.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-to-Fiber Substitution Under AGEC and PPWR | +0.7% | National, with concentration in Paris, Lyon, and Bordeaux retail and agri-food packaging corridors | Short term (≤ 2 years) |

| Food Packaging Demand From Ready-to-Eat and Fresh Categories | +0.4% | National, with particular depth in Ile-de-France and Loire Valley agri-food processing clusters | Medium term (2-4 years) |

| Premium Beauty and Luxury Carton Demand | +0.3% | National, led by Paris, Grasse, and Provence luxury and cosmetics manufacturing clusters | Medium term (2-4 years) |

| Healthcare Serialization and Compliance Packaging Demand | +0.2% | National, concentrated in Lyon, Paris, Ile-de-France, and Alsace pharmaceutical manufacturing zones | Medium term (2-4 years) |

| EPR Eco-Modulation Rewards Design-for-Recycling Cartons | +0.2% | National, with early adoption gains concentrated among large FMCG brand owners | Short term (≤ 2 years) |

| Luxury E-Commerce Right-Sizing and Void Reduction Needs | +0.2% | National, with concentration in Paris and Rhone-Alpes logistics and fulfillment clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Fiber Substitution Under AGEC and PPWR

Plastic-to-fiber substitution is the most durable demand support for the France cartonboard market over the forecast period. The EU Packaging and Packaging Waste Regulation entered into force on February 11, 2025, and applies from August 12, 2026, which gives cartonboard a stronger compliance position in packaging formats that must demonstrate recyclability by 2030.[1]European Commission, “Packaging and Packaging Waste,” European Commission, environment.ec.europa.eu France’s AGEC law has been reinforcing the same direction through national restrictions on single-use plastic packaging, including the ban that France implemented for fresh fruit and vegetables below 1.5 kg.[2]French Ministry of Ecological Transition, “Loi Anti-Gaspillage Pour Une Économie Circulaire,” Ministère de la Transition Écologique, ecologie.gouv.fr This combination has created a long transition window in which brand owners can redesign packs around fiber rather than wait for a later compliance deadline. The France cartonboard market benefits because mono-material paperboard solutions are easier to position within the new regulatory framework than multilayer plastic structures. French converters also enter this phase with earlier redesign experience under AGEC, which supports faster customer response and better margin capture as more applications move toward recyclable board formats.

Food Packaging Demand From Ready-To-Eat and Fresh Categories

Food remains a core volume base for the France cartonboard market, and demand from ready-to-eat and fresh categories is adding to that stability. Dairy, bakery, fresh produce, frozen meals, and ambient food applications already anchor cartonboard use across the country. As food producers shift more packaging into recyclable formats, folding boxboard is being used in sleeves, trays, and direct-contact structures that support both shelf presentation and handling needs. The early phase of conversion has been strongest in applications where plastic replacement is easier to execute under AGEC, while chilled formats still offer room for further migration. That creates a more selective demand pattern, where value moves toward suppliers that can handle moisture resistance, print quality, and reliable food-packaging performance within recyclable board systems. The France cartonboard market therefore gains from food demand not only through broader pack adoption, but also through a gradual move toward more specialized grades and converting capability.

Premium Beauty And Luxury Carton Demand

Premium beauty and luxury packaging gives the France cartonboard market one of its clearest value-upgrade paths. France’s luxury cosmetics and fragrance base continues to rely on cartonboard for premium secondary packaging, where surface quality, stiffness, and print finish directly affect brand presentation. Brands increasingly specify virgin-fiber boards above 300 GSM for finishes such as foil stamping, embossing, and soft-touch lamination. Stora Enso’s September 2025 launch of Ensovelvet shows how suppliers are targeting this demand with SBS grades designed for tactile premium packaging and regulatory suitability in adjacent applications. Cosmetics and toiletries are also the fastest-growing end-user segment in the France cartonboard market at 5.18% CAGR through 2031, which keeps this premium demand stream important well beyond a short design cycle. As a result, the France cartonboard market is seeing premiumization work through both aesthetics and compliance, rather than through decorative appeal alone.

Healthcare Serialization And Compliance Packaging Demand

Healthcare packaging demand is one of the most resilient supports for the France cartonboard market. France’s medicine verification framework requires each carton of prescription medicine to carry a unique Datamatrix serial code, tamper-evident features, and batch data before release to the market. That requirement favors printable folding cartons and SBS grades with stable surfaces that can support precise coding and consistent legibility. Each new drug approval or biosimilar launch creates an additional carton SKU requirement, which makes pharmaceutical packaging demand recurring rather than optional. Mayr-Melnhof’s 2025 annual report identified healthcare packaging as a strategic growth area and referenced targeted site optimizations in France and Spain. For the France cartonboard market, this means healthcare demand provides a dependable base even when broader packaging volumes soften, because serialization and compliance packaging cannot be deferred without affecting market access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Pulp, Recovered Fiber, and Energy Costs | -0.5% | Global, with EMEA-specific exposure to natural gas pricing and Nordic pulp market swings | Short term (≤ 2 years) |

| Alternative Flexible and Lightweight Formats in Selected Uses | -0.3% | National, particularly in ambient snacking, dry condiments, and portioned ingredients | Medium term (2-4 years) |

| Migration Testing Burden for Inks, Coatings, and Adhesives | -0.2% | National, with EU-wide compliance obligations under Regulation (EC) No 1935/2004 and EuPIA GMP | Medium term (2-4 years) |

| Domestic Converting Capacity Gaps and Import Dependence | -0.2% | National, with import reliance on Germany, Austria, Finland, Italy, and Spain for board stock | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp, Recovered Fiber, And Energy Costs

Input cost volatility remains the most immediate brake on the France cartonboard market. Mayr-Melnhof’s Q1 2026 trading statement described the operating backdrop as subdued demand, structural overcapacity, and intense competition, with geopolitical pressure feeding through energy, transport, and chemical costs. Metsä Board also stated in April 2026 that rising oil and natural gas prices linked to the Iran conflict were expected to reduce its Q2 2026 operating result by EUR 10 million, which shows how quickly external shocks move into paperboard economics. In the France cartonboard market, these pressures are especially important because converters compete in an environment where customers still expect service reliability and technical compliance even when margins tighten. Cost volatility also affects product mix, since recycled-fiber grades are more exposed when both recovered fiber and energy costs move at the same time. This leaves technically stronger or more integrated suppliers better placed than smaller converters that lack pricing power or procurement leverage.

Alternative Flexible And Lightweight Formats In Selected Uses

Alternative lightweight formats still limit cartonboard conversion in selected applications across the France cartonboard market. Flexible plastics held 38.92% of France’s total packaging market by product type in 2025, which reflects the strength of installed infrastructure and supplier relationships in those uses. Ambient snacking, dry condiments, and portioned ingredients remain difficult areas for cartonboard because flexible formats can meet barrier needs with less material and lower pack weight. The regulatory picture will reduce part of that advantage over time, since recyclable design requirements place more pressure on complex multilayer plastic structures. Even so, implementation gaps still matter, and France’s own single-use plastic reduction path has shown that regulatory ambition does not always translate into immediate substitution across every format. For the France cartonboard market, that means fiber gains will keep advancing, but they will do so unevenly and with stronger traction in applications where functional trade-offs are already manageable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Premium Virgin-Fiber Boards Lift Value Mix

Folding Boxboard held 42.25% of France cartonboard market share in 2025, which kept it as the leading product grade in the France cartonboard market. Its position reflects broad use across food, pharmaceuticals, household goods, and e-commerce, where printability, stiffness, and recyclability all matter in everyday commercial decisions. Solid Bleached Board is the fastest-growing grade and is forecast to rise at 5.19% CAGR through 2031, which shows how much value is moving toward higher-specification applications in the France cartonboard industry. This shift is tied less to simple volume growth and more to substrate upgrading by luxury, pharmaceutical, and premium food customers. The France cartonboard market is therefore seeing premium grades gain share in value terms even when total tonnage does not change sharply.

Stora Enso’s Ensovelvet launch in September 2025 is a clear example of how suppliers are targeting this movement with SBS grades designed for premium fragrance and personal care packaging. The closure of the La Tuque SBS machine in February 2026 by Smurfit Westrock was a portfolio move toward higher-specification SBS supply rather than broader commodity capacity. White-Lined Chipboard remains tied more closely to price-sensitive applications, and that leaves it more exposed when energy costs and coating compliance become harder to manage. Solid Unbleached Board still holds a role in food-service and industrial uses where strength matters more than appearance, while liquid packaging board and food-service board benefit from the ongoing replacement of plastic-based formats. In practical terms, the France cartonboard market is rewarding certified virgin-fiber suppliers that can combine surface quality, regulatory readiness, and dependable delivery across end uses that now require more than low-cost board alone.

By Packaging Format: Folding Cartons Lead, Liquid Packaging Gains Speed

Folding cartons accounted for 66.12% of the France cartonboard market size in 2025, which made them the structural backbone of the France cartonboard market. Their leading position comes from wide exposure across pharmaceuticals, cosmetics, food, and household goods, which reduces dependence on any one demand pocket. Liquid packaging is the fastest-growing format and is projected to expand at 4.78% CAGR through 2031, showing where the next major format shift is taking shape. That growth reflects the move by dairy and plant-based beverage producers toward carton systems that offer a better sustainability fit than plastic bottles in selected categories. The France cartonboard industry is therefore balancing mature folding-carton demand with a more innovation-led liquid packaging segment.

Tetra Pak’s April 2026 launch of the first 1-litre aseptic carton with a paper-based barrier shows how material innovation is changing the format economics for recyclable liquid packaging. SIG Group reported 24% year-over-year growth in alu-layer-free aseptic carton sales in 2025, reaching 2 billion liters, which confirms that paper-based barrier systems have already moved beyond pilot-stage interest. Other fiber formats also benefit from France’s tighter stance on disposable plastic items in food-service settings, which keeps trays, sleeves, cups, and service-related board formats relevant in adjacent applications. Because of that, the France cartonboard market is not only defending folding cartons at scale, it is also opening a second growth lane through liquid and service-oriented board systems that fit changing compliance needs.

By End-User Industry: Food Anchors Volume While Cosmetics Lift Value

Food represented 28.81% of 2025 revenue, which made it the largest end-user base in the France cartonboard market. Dairy, bakery, frozen meals, and fresh produce keep cartonboard closely linked to daily consumer demand, and that gives the market a stable operating floor. Cosmetics and toiletries are forecast to expand at 5.18% CAGR through 2031, making them the fastest-growing end-user category in the France cartonboard market size. This performance reflects France’s strong position in beauty and luxury goods and the shift toward board grades that can carry both brand image and compliance requirements. Within the France cartonboard industry, that creates a clear split between food as the main volume anchor and cosmetics as the main value-upgrade engine.

Luxury and mass-market beauty brands both favor premium SBS and other high-quality virgin-fiber substrates when the packaging must protect brand presentation and meet tighter technical standards. Pharmaceuticals and healthcare add another resilient layer of demand because serialization rules make carton use obligatory for many prescription products released into the market. Beverage demand is also widening its use of board through liquid packaging migration, while tobacco remains in structural decline despite some continuing need for premium specialty packs. Other sectors such as toys, apparel, household electrical goods, and retail-ready e-commerce packaging keep contributing to the France cartonboard market because board delivers presentation, protection, and transport efficiency in one format. Together, these patterns show that the France cartonboard market draws its stability from food and healthcare, while much of its pricing strength comes from cosmetics, luxury, and premium branded retail uses.

Geography Analysis

France held Europe’s third-largest cartonboard consumption position, behind Germany and Italy, which gives the France cartonboard market a major regional role despite its moderate growth rate. Demand is not spread evenly across the country, because specification decisions are concentrated around corporate and brand headquarters, while converting volumes are supported by industrial and food-processing clusters. Ile-de-France stands out for cosmetics, pharmaceuticals, and FMCG decision-making, which keeps it central to premium grade selection in the France cartonboard market. Normandy, Pays de la Loire, and Rhone-Alpes support a large share of converting activity through their links to agri-food, dairy, logistics, and manufacturing demand. This geographic split means high-value demand often begins near brand and regulatory centers, while recurring board consumption is tied to production and fulfillment corridors.

France’s regulatory setting also gives the France cartonboard market a distinct regional profile within Western Europe. AGEC has been shaping packaging choices since 2020, and PPWR now adds a harmonized EU layer that applies from August 2026. FEFCO notes that the PPWR requires paper and cardboard packaging to achieve an 85% recycling rate by 2030, which supports fiber-based formats in a market already moving toward design for recycling. This makes France one of the more advanced regulatory environments for sustainable packaging in Western Europe, and that status matters because converters and brand owners have less room to delay pack redesign. The France cartonboard market therefore gains from regulation not only through substitution volume, but also through earlier adoption of higher-compliance grades and more disciplined specification review.[3]FEFCO, “EU 2025/40 Packaging and Packaging Waste Regulation and Corrugated Cardboard,” FEFCO, fefco.org

Import dependence adds another geographic feature to the France cartonboard market. France still relies on Germany, Austria, Finland, Italy, and Spain for much of its folding boxboard supply, which means foreign mill pricing and availability affect French converter economics quickly. That limits domestic leverage when substitution demand rises, especially in premium grades where Nordic and Central European suppliers remain strong. It also means larger converters with fixed supply agreements are better placed than smaller spot buyers when regional pricing tightens or overcapacity coexists with cost inflation. In that context, the France cartonboard market grows within a mature regional system where regulatory demand is local, but a meaningful part of supply discipline is still set outside France.

Competitive Landscape

The France cartonboard market is medium-concentrated at the board production level and highly fragmented at the converting level. Nordic and Central European suppliers such as Metsä Board, Stora Enso, Billerud, and Mayr-Melnhof Karton supply much of the folding boxboard and SBS used in France, while domestic activity remains more visible in premium niches and converting relationships.[4]MM Group, “Trading Statement Q1 2026,” Mayr-Melnhof Karton AG, mm.group The structure gives larger board producers an edge in grade breadth, certified sourcing, and supply reliability, but it does not eliminate local competition where customer service, technical support, and short lead times still matter. In the France cartonboard market, that balance keeps competition active even when upstream supply is concentrated in fewer hands. Independent converters therefore compete less on raw scale and more on compliance execution, print quality, finishing, and account proximity.

Several strategic moves since 2025 show how major suppliers are repositioning around premium grades and operational control. Smurfit Westrock announced the permanent closure of the La Tuque machine producing 127,000 tonnes of solid bleached sulfate annually in February 2026, which points to tighter focus on higher-specification supply rather than broad commodity output. Graphic Packaging completed the ramp-up of its USD 1.67 billion Waco recycled paperboard facility in October 2025 and then shifted its 2026 focus toward free cash flow and portfolio simplification, which suggests that large players are now prioritizing asset performance over fresh capacity expansion. Metsä Board launched its Lead the Pack strategy in March 2026, and the second phase of that plan targets growth in brand-enhancing consumer packaging solutions that fit French luxury and food applications. Billerud also continued its Evolution program investments directed at solid bleached board capacity, which shows that premium fresh-fiber grades still sit high on supplier investment agendas. These moves matter in the France cartonboard market because they shift competition further toward technical positioning, application mix, and premium customer alignment.

French converters such as Autajon Group, Verpack, TPG Pack, and Cartonnages Vaillant remain relevant because they can respond closely to customer-specific needs in pharmaceuticals, cosmetics, and branded retail packs. The most defensible positions sit where commodity board price is only one part of the buying decision, especially in pharmaceutical serialization and luxury packaging. France-MVO’s verification requirements make precise printing, tamper-evidence, and reliable carton execution necessary in medicine packaging, which raises the barrier for less specialized converters. EuPIA’s November 2025 good manufacturing practice guidance also reinforces the importance of ink, coating, and process control for suppliers serving sensitive packaging uses. At the same time, Tetra Pak and SIG Group are expanding paper-based liquid packaging systems in ways that create incremental board demand without directly competing with every folding-carton converter. That is why the France cartonboard market remains competitive, but not evenly so, because the strongest positions are now tied to regulatory fit, premium finishing, and technically validated converting capabilities rather than broad commodity exposure alone.

France Cartonboard Industry Leaders

Mayr-Melnhof Karton AG

Smurfit Westrock plc

Graphic Packaging International, LLC

La Rochette Cartonboard SAS

Tetra Pak International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Tetra Pak and Italian dairy company Sterilgarda Alimenti launched the world's first 1-litre aseptic carton with a paper-based barrier, eliminating the aluminum layer from the carton structure and reducing carbon footprint.

- April 2026: Sonoco Products raised EMEA prices by EUR 80 per tonne for uncoated recycled paperboard and 8% for tube and core goods, citing higher energy and chemical costs, a pricing action that reflects sector-wide margin pressure and signals further cost pass-through risk for French converters sourcing recycled-grade board.

- February 2026: Smurfit Westrock announced the permanent closure of the La Tuque, Quebec paper machine producing 127,000 tonnes of solid bleached sulfate annually, consolidating its SBS portfolio and redirecting European SBS supply toward higher-specification premium cartonboard grades relevant to French luxury and pharmaceutical converters.

- February 2026: Tetra Pak expanded its paper-based barrier packaging technology to high-speed Tetra Pak A3/Speed filling lines, with Maeil Dairies becoming the first global producer to implement it for soya beverage, a scalability milestone confirming industrial-speed viability for the paper-barrier liquid packaging system.

France Cartonboard Market Report Scope

The France Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The France Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

How large is the France cartonboard market in 2026 and where is it expected to reach by 2031?

The France cartonboard market stands at USD 1.68 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at a CAGR of 2.06%.

Which product grade leads cartonboard demand in France?

Folding Boxboard led product-grade demand with a 42.25% share in 2025 because it is widely used in food, pharmaceutical, household, and e-commerce packaging.

What is the fastest-growing product grade in France cartonboard?

Solid Bleached Board is the fastest-growing grade, with a projected 5.19% CAGR through 2031, supported by luxury, pharmaceutical, and premium food applications.

Which packaging format dominates cartonboard use in France?

Folding cartons held 66.12% of market value in 2025, making them the core format across pharmaceuticals, cosmetics, food, and household products.

Which end-user group is growing the fastest in France?

Cosmetics and toiletries is forecast to grow at a 5.18% CAGR through 2031, supported by premium packaging demand and tighter sustainability requirements.

What is the main factor shaping future demand for cartonboard in France?

Regulatory change is the strongest force, especially AGEC and PPWR, because both push packaging users toward recyclable fiber-based formats and away from harder-to-recycle plastic structures.

Page last updated on: