Canada Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

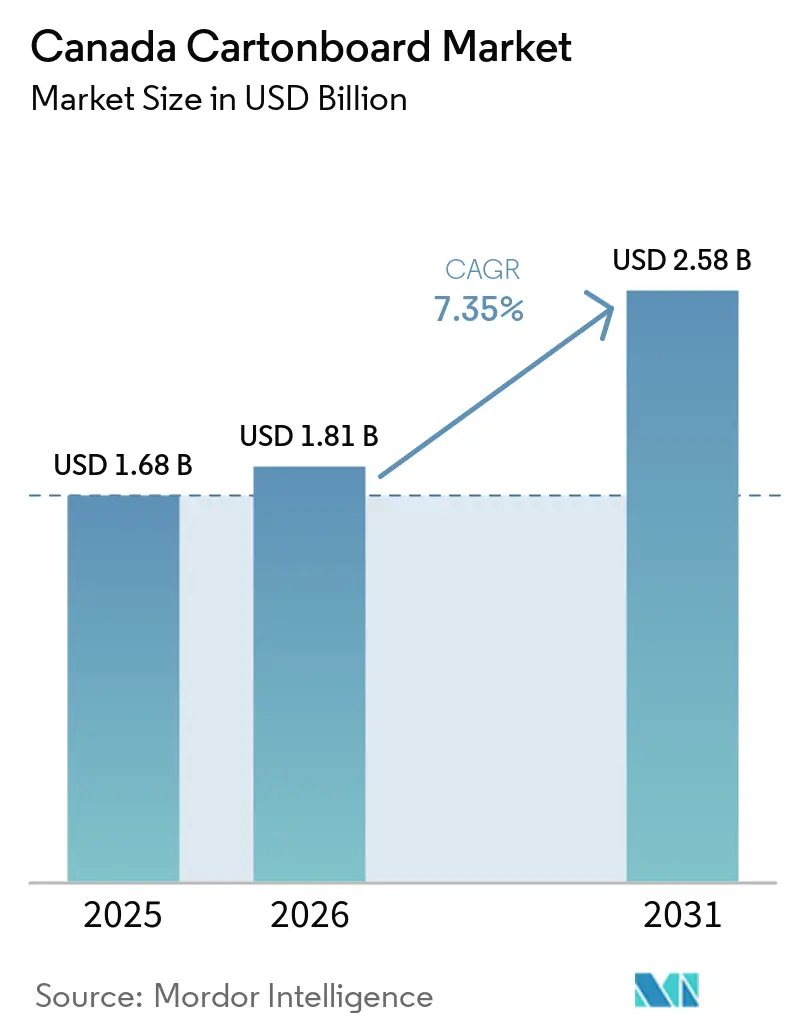

| Base Year Market Size (2025) | USD 1.68 Billion |

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 2.58 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

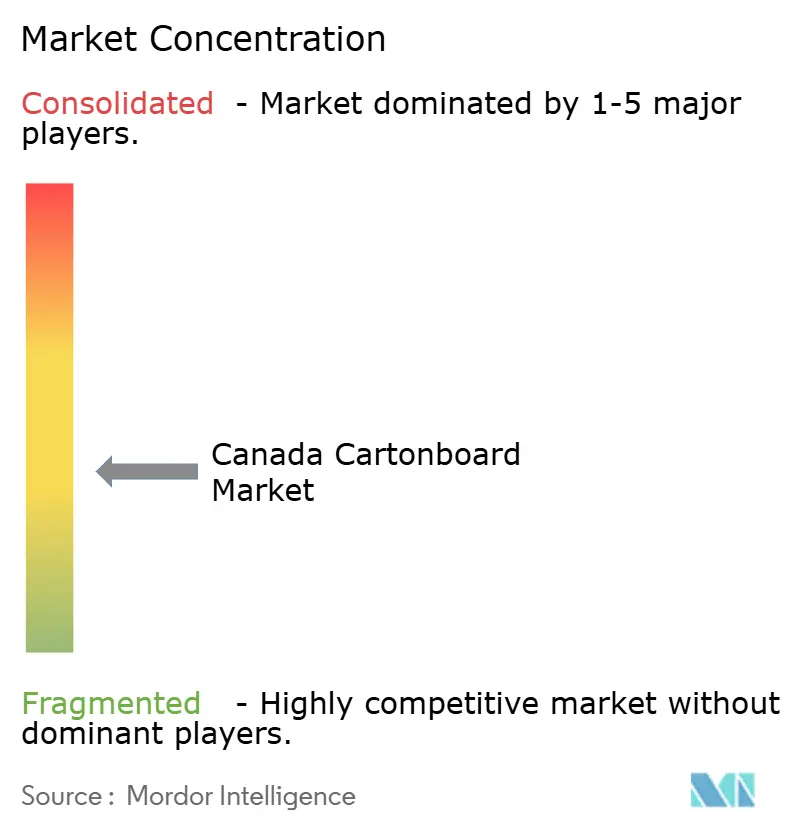

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Cartonboard Market Analysis by Mordor Intelligence

The Canada cartonboard market size is projected to be USD 1.68 billion in 2025, USD 1.81 billion in 2026, and reach USD 2.58 billion by 2031, growing at a CAGR of 7.35% from 2026 to 2031. The Canada cartonboard market is benefiting from federal and provincial restrictions on single-use plastics, which have pushed brand owners toward fiber-based packaging in foodservice, retail, and consumer goods. Producer-funded recycling programs are also changing procurement priorities because recyclable cartonboard designs now align more closely with compliance and fee structures across major provinces. The Canada cartonboard market is further supported by the country’s large food and beverage processing base, which keeps packaging demand more stable than in many discretionary consumer categories. Ontario and Quebec continue to shape demand because they combine dense consumer markets with strong food processing, pharmaceutical manufacturing, and consumer packaged goods activity. Growth is still moderated by domestic premium-grade supply tightness, input cost inflation, and import dependence for folding boxboard and other specialized grades.

Key Report Takeaways

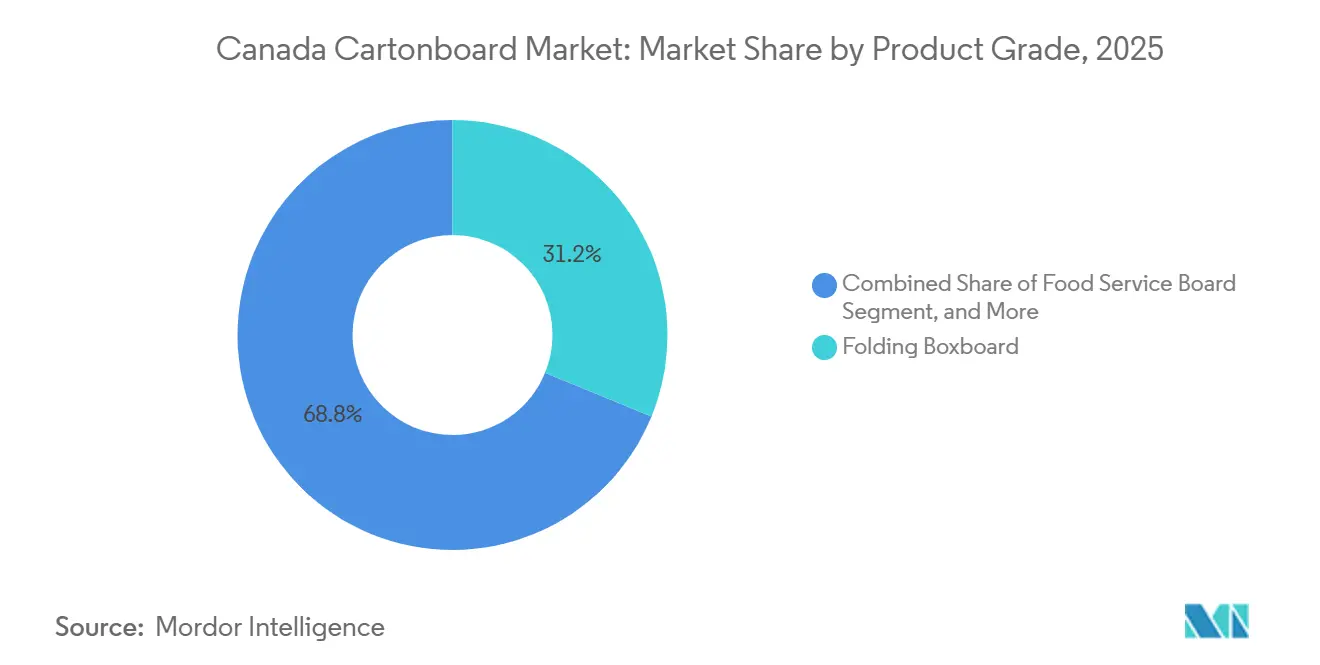

- By product grade, folding boxboard captured 31.18% of the Canada cartonboard market share in 2025.

- By packaging format, the Canada cartonboard market size for the liquid packaging segment is forecast to advance at a 7.49% CAGR through 2031.

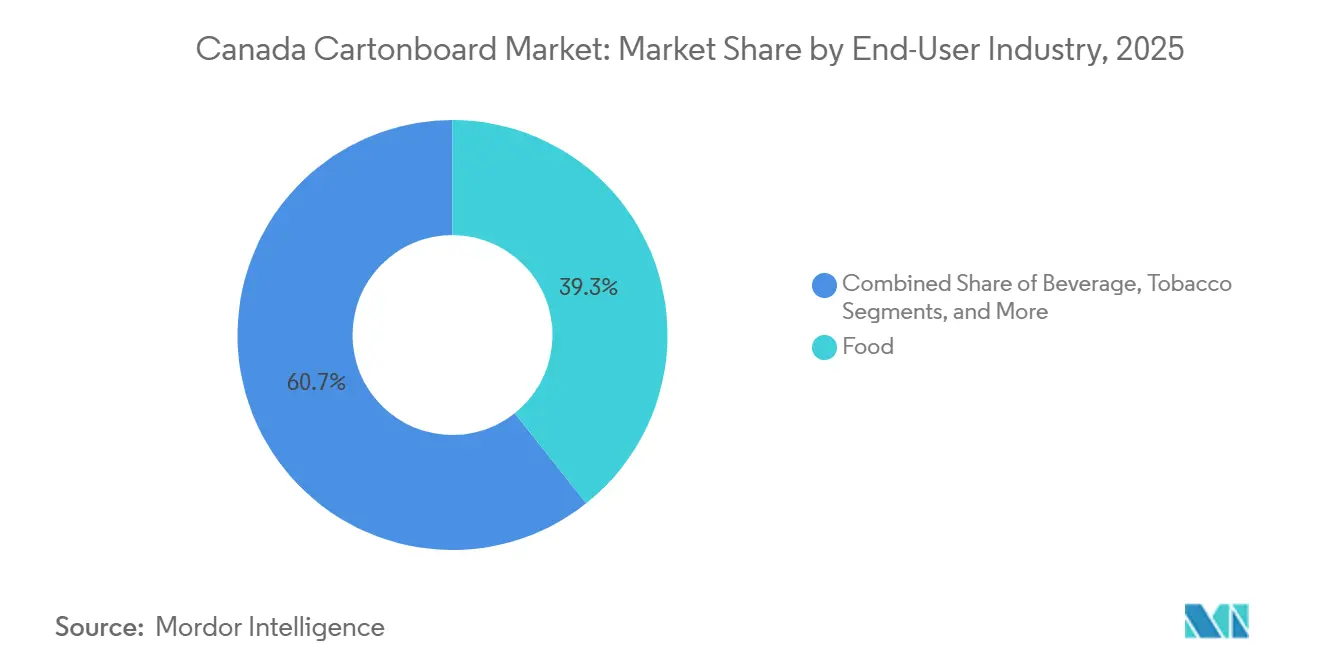

- By end-user industry, food captured 39.31% of the Canada cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiber Substitution After Single-Use Plastic Restrictions | +2.1% | National, with concentrated gains in Ontario and Quebec foodservice and retail channels | Short term (≤ 2 years) |

| Producer-Funded EPR Expanding Carton Recovery And Design Incentives | +1.6% | National, Ontario, Quebec, Alberta, and BC leading, Maritime provinces phasing in through 2027 | Medium term (2-4 years) |

| Food And Beverage Carton Demand Anchored By Canadian Manufacturing | +1.3% | National, Ontario and Quebec manufacturing hubs dominate, prairie provinces accelerating | Medium term (2-4 years) |

| Premium Printing And Compliance Needs In Pharmaceutical And Personal Care Packaging | +0.9% | National, Southern Ontario pharmaceutical corridor and Montreal cosmetics cluster most exposed | Medium term (2-4 years) |

| Ontario-Wide Cup Acceptance Improving Food Service Board End Markets | +0.6% | Ontario, with spill-over demand effects across Quebec and BC as EPR harmonization progresses | Short term (≤ 2 years) |

| Barrier-Coating Advances Expanding Cartonboard Into Frozen And Greasy Applications | +0.5% | Global supply base, national adoption concentrated in food processing provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fiber Substitution After Single-Use Plastic Restrictions

Canada’s restrictions on single-use plastic checkout bags, cutlery, foodservice ware, and stir sticks remained the clearest near-term demand driver for the Canada cartonboard market, as they moved packaging conversion from trial activity to an active portfolio rollout. The January 2024 court outcome reduced regulatory uncertainty, which had previously caused some operators to delay packaging changes and hold back commercial commitments to fiber formats.[1]Government of Canada, “Single-use Plastics Prohibition Regulations (SOR-2022-138),” Justice Laws Website, laws.justice.gc.ca Brand owners across foodservice, retail, and quick-service channels have since had stronger incentives to shift product lines toward folding cartons and food service boards. The effect is reinforced by reporting obligations tied to plastics management, which increase the compliance burden for plastic-heavy packaging systems and enhance the relative appeal of fiber solutions. This demand shift also benefits the Canada cartonboard market, as higher carton collection volumes can return more usable fiber into domestic recycling loops over time.[2]Paper Packaging and Envelope Council, “New StatsCan Data Shows Paper Fibres Most Diverted Material,” Paper Packaging and Envelope Council, ppec-paper.com

Producer-Funded EPR Expanding Carton Recovery And Design Incentives

The shift from municipality-funded recycling to producer-funded responsibility has changed how packaging is specified in the Canada cartonboard market, as design choices now affect producers' direct costs. Ontario completed its Blue Box transition by early 2026, and the system now covers more than 5 million households, 383 municipalities, and 12 First Nations communities under a unified framework administered by Circular Materials.[3]Circular Materials, “Get Ready, Ontario: Recycle More Than Ever Before Starting in 2026!,” Circular Materials, circularmaterials.ca Alberta launched Phase 1 on April 1, 2025, and broader provincial rollout across the country has continued to widen collection coverage for cartons and related fiber formats. Eco-modulated fee structures increasingly favor recyclable cartonboard designs over more complex multi-material packs, giving brand owners a financial incentive to simplify packaging substrates. That means the Canada cartonboard market is supported not only by consumer preferences and regulations, but also by cost signals built into compliance systems.

Food And Beverage Carton Demand Anchored By Canadian Manufacturing

Food and beverage processing continues to provide the Canada cartonboard market with a durable demand base because packaged food output remains essential even when household spending weakens in other categories. Dry foods, frozen foods, dairy products, confectionery, and a wide range of retail-ready goods continue to rely on folding boxboard, liquid packaging board, and food service board across both primary and secondary pack formats. Export-oriented grain, meat, and processed food chains also extend carton demand into business-to-business shipments and branded shelf-ready presentations. Retail premiumization has also mattered because private-label brands have been upgrading print quality, structural design, and surface finish, which raises the specification level of cartons used in grocery channels. The Canada cartonboard market is also seeing support from direct-to-consumer food and health supplement brands that need strong branded packs without excessive use of corrugated outers.

Premium Printing And Compliance Needs In Pharmaceutical And Personal Care Packaging

Pharmaceutical and personal care packaging requirements are raising the quality threshold in the Canadian cartonboard market because label density, traceability, and color consistency matter more in regulated categories than in general retail. Health Canada’s 2025 draft guidance on co-packaged drug products added another layer of attention to packaging and labeling, which supports ongoing redesign activity in pharmaceutical cartons. Converters with BRCGS Packaging, ISO 9001, and advanced print management capabilities are better positioned to win this business, thereby increasing the commercial value of certified operations. Jones Healthcare Group’s plan to invest USD 40 million by end-2026 in folding cartons and labels for healthcare customers shows that suppliers are building capacity to meet this demand stream.[4]Jones Healthcare Group, “Contract Pharma Exclusive With Jones on Packaging Innovation,” Jones Healthcare Group, joneshealthcaregroup.com In personal care, the Canadian cartonboard market is also supported by premium finishing needs and bilingual labeling requirements, which keep cartons attractive where flexible packaging can be less suitable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material, Energy, And Conversion Cost Volatility | -1.8% | National, BC and Quebec most exposed due to pulp price dependency, energy-intensive mill operations nationwide | Short term (≤ 2 years) |

| Competition From Flexible Plastic, Rigid Plastic, And Reusable Formats | -1.3% | National, with intensity concentrated in foodservice and health-and-beauty retail channels | Medium term (2-4 years) |

| La Tuque SBS Closure Tightening Domestic Premium-Grade Supply | -0.8% | National, Quebec and Ontario converters most affected, US import substitution increases FX exposure | Short term (≤ 2 years) |

| Heavy Dependence On Imported Folding Boxboard Raising FX And Lead-Time Risk | -0.5% | National, with disproportionate exposure in converters reliant on European specialty grades | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material, Energy, And Conversion Cost Volatility

Cost pressure remains a major brake on the Canada cartonboard market because converters are exposed to pulp, recovered fiber, fuel, electricity, and chemical inputs simultaneously. These pressures matter more for cartonboard specialists than for some larger paper producers because converters often have less room to offset sharp increases through broader product portfolios. Supply conditions in upstream pulp and paper operations have also remained uneven in western Canada, adding another layer of uncertainty around material availability and plant economics. Cascades stated in May 2026 that rising input costs and new containerboard price increases were shaping its packaging outlook, indicating that cost pressure remained active across the sector in 2026. The result is that the Canada cartonboard market continues to grow, but margin expansion is harder for converters serving price-sensitive customers or those that depend on shorter contract cycles.

Competition From Flexible Plastic, Rigid Plastic, And Reusable Formats

The Canada cartonboard market still competes with flexible plastics, rigid plastics, and reusable systems in applications where barrier performance, moisture resistance, and unit economics remain decisive. Flexible pouches continue to offer strong product protection in snacks, condiments, and pet food, while rigid plastic trays and cups keep their place in applications where cartonboard still needs coatings or additional structure to perform reliably. Reusable container systems are also entering packaging planning discussions under broader waste reduction agendas, even if they do not yet represent large direct displacement in volume terms. This keeps some end uses contested, especially in foodservice and health-and-beauty channels where performance and convenience must be balanced against sustainability claims. Barrier innovation is narrowing part of this gap, but the Canada cartonboard market still faces competition in formats where cartonboard has not yet become the default technical choice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Food Service Board Gains Ground On Folding Boxboard Leadership

Folding boxboard held 31.18% of the Canada cartonboard market share in 2025, which made it the leading grade because it works across food, pharmaceutical, and personal care packaging. Its position rests on broad converter familiarity, dependable print performance, and suitability for a wide range of carton structures used in mainstream packaged goods. The Canada cartonboard market also benefits from access to imported folding boxboard from the United States and Europe, which helps cover standard specifications as well as premium coated virgin fiber needs. White-lined chipboard continued to serve retail secondary packs and shoe boxes, but its economics remained more sensitive to swings in recovered fiber prices and margin pressure. Solid bleached board and solid unbleached board stayed important for premium food-contact and pharmaceutical uses, although premium bleached supply tightened after the La Tuque closure reduced domestic availability.

The food service board segment is projected to expand at a CAGR of 8.61% from 2026 to 2031, making it the fastest-growing grade in the Canada cartonboard market. Ontario’s province-wide acceptance of polycoated paperboard cups from January 1, 2026, gave the grade a clearer end-of-life route and removed a key objection that had limited broader brand adoption. Circular Materials also reported that a Toronto pilot increased collected polycoated paperboard by 8%, which supported confidence that food service fiber can move through residential systems at larger scale. Quick-service restaurants are also replacing foam- and plastic-based formats with fiber solutions, opening end markets that were historically harder for the Canada cartonboard industry to capture. The Canada cartonboard market is therefore seeing grade mix change not only due to regulation, but also to better recovery infrastructure and stronger converter confidence in food service applications.

By Packaging Format: Folding Cartons Anchor Demand While Liquid Packaging Accelerates

Folding cartons accounted for 54.16% of the Canada cartonboard market in 2025, keeping them well ahead of other packaging formats. Their lead reflects wide use in cereals, snacks, pharmaceuticals, cosmetics, and many other consumer categories where shelf presence, compliance printing, and efficient converting all matter. The Canada cartonboard market has a strong installed base of carton converting in Ontario and Quebec, which supports long-standing relationships between packaging suppliers and brand owners. Sleeve and tray formats also played an important role in beverage multipacks and retail-ready packaging, especially in club retail and e-commerce, where high throughput and clear merchandising performance are required. Other formats, including cups and foodservice containers, continued to post strong unit momentum because plastic substitution rules expanded the role of paperboard-based service packaging.

Liquid packaging is projected to grow at a CAGR of 7.49% from 2026 to 2031, which makes it the fastest-growing packaging format in the Canada cartonboard market. Growth is concentrated in aseptic and gable-top cartons used for dairy, plant-based drinks, soups, and sauces, where consumer adoption has remained firm across 2024 and 2025. Recovery conditions have also improved because provincial EPR systems increasingly recognize aseptic and gable-top cartons as accepted curbside materials, which strengthens the long-term position of these formats. That matters because better collection performance supports the environmental case for cartons at the same time that demand is rising in refrigerated and shelf-stable beverage segments. In the Canada cartonboard market, this creates a more favorable loop between usage, recovery, and procurement confidence than what is seen in some mature folding carton applications.

By End-User Industry: Food Sustains Volume While Pharma Commands The Growth Premium

Food held 39.31% share of the Canada cartonboard market size in 2025, which kept it as the largest end-user segment in the Canada cartonboard market. The segment draws strength from broad use across dry, frozen, chilled, bakery, and convenience food lines, where cartons continue to balance branding, structure, and retail handling. Packaging demand is especially strong in Ontario and Quebec because those provinces combine large food processing clusters with access to major population centers and distribution networks. Grocery chains are also using more display-ready and retail-ready pack formats, which adds to board consumption by improving shelf efficiency and reducing store labor. Cosmetics and toiletries also remained important because premium print surfaces and specialty finishes continue to favor folding boxboard and solid bleached board in consumer-facing packs.

The pharmaceutical and healthcare sector is projected to expand at a CAGR of 8.05% from 2026 to 2031, making it the fastest-growing end-user segment in the Canada cartonboard market. Health Canada’s ongoing packaging and labeling requirements continue to support repeat redesign cycles and keep folding cartons central to pharmaceutical secondary packaging. Jones Healthcare Group’s USD 40 million capital program through 2026 shows that suppliers expect sustained healthcare demand and are increasing capacity accordingly. Netpak’s BRCGS AA+ certification in Montreal also shows how qualification standards are shaping supplier choice in the Canada cartonboard industry, particularly for regulated healthcare customers. The beverage segment remained steady in volume terms, but healthcare is where the Canada cartonboard industry is seeing the clearest premiumization and compliance-driven growth.

Geography Analysis

Ontario and Quebec together accounted for the bulk of demand in the Canadian cartonboard market in 2025 because they combine dense consumer markets with the country’s largest food, pharmaceutical, and consumer goods production base. Ontario remained the single most influential province because it concentrated food and beverage processing in the Greater Toronto Area and the Golden Horseshoe, while also supporting a large pharmaceutical manufacturing corridor. The province’s Blue Box EPR transition was completed on January 1, 2026, and the system now covers more than 5 million households and 383 municipalities under Circular Materials, which gives Ontario the strongest carton recovery platform in the country. Ontario’s decision to accept polycoated paperboard cups province-wide from January 2026 further widened the end-market opportunity for food service board and related carton applications. Two new WM material recovery facilities in Cambridge and Greater Napanee also improved the reliability of secondary fiber sorting and strengthened the operating environment for Ontario-based recyclers and converters.

Quebec remained the second-largest regional base in the Canadian cartonboard market and carried added importance because it combines production assets with a mature recovery framework. Cascades deepened that role in March 2026 through a CAD 6.9 million (USD 5.0 million) investment in its Kingsey Falls uncoated recycled boxboard plant to improve sheet quality and food packaging surface finish. At the same time, Smurfit Westrock’s La Tuque shutdown tightened domestic premium-grade supply and increased reliance on imports for bleached cartonboard used by converters in Quebec and Ontario. Quebec’s residential collection rate and lower contamination profile also improved the case for recycled-content board grades among buyers that now place more weight on circularity and compliance.

British Columbia formed a distinct part of the Canada cartonboard market because it links coastal population centers with Asia-Pacific trade routes and a fiber-oriented industrial base. Updated EPR planning in BC kept cartons within the broader fiber stream and supported collection consistency as the province refined recycling targets. Even so, upstream pulp operations in BC continued to face fiber constraints and elevated operating costs, which limited the region’s role as a stable source of virgin-fiber supply for downstream board demand. Alberta added another layer of growth after Phase 1 of its EPR program launched on April 1, 2025, covering more than 200 communities and including aseptic and gable-top cartons on accepted lists. Atlantic provinces remained smaller contributors, but Nova Scotia and Prince Edward Island both moved further into formal EPR structures, which is likely to support a broader geographic base for the Canada cartonboard market as collection systems mature.

Competitive Landscape

The Canada cartonboard market is moderately fragmented, with global producers, imported specialty board suppliers, and domestic converters all competing across different grades and customer groups. Large multinational players such as Cascades, Smurfit WestRock, and Graphic Packaging International operate with broader North American footprints, which give them greater scale, procurement leverage, and multi-grade flexibility than many smaller converters. European suppliers also remain important in the Canada cartonboard market because premium folding boxboard and specialty virgin-fiber grades are often sourced from outside Canada for pharmaceutical, food, and cosmetics packaging. This has created a split structure where premium imported grades and domestically converted mainstream grades coexist under different margin pressures and service expectations. As a result, competition is driven not only by price, but also by supply reliability, certification depth, and the ability to meet regulated packaging specifications.

Strategic portfolio moves have become a clear differentiator in the Canada cartonboard market during 2025 and 2026. Cascades invested CAD 6.9 million (USD 5.0 million) in March 2026 to improve quality and finish at Kingsey Falls, thereby strengthening its recycled-content food packaging offering. Smurfit WestRock permanently closed the La Tuque SBS machine, reducing domestic premium bleached board capacity and shifting more demand toward imported supply channels. Graphic Packaging confirmed cost-cutting actions in May 2026 following a 90-day business review, noting that larger players were also adjusting their operating structures as they balanced demand conditions and margin goals. These moves show that scale alone is not enough, and companies are actively reshaping asset bases and spending priorities.

Competitive advantage in the Canada cartonboard market increasingly depends on certification, technical compliance, and the ability to support higher-value applications. Pharmaceutical and cosmetics customers are concentrating spend with converters that can demonstrate BRCGS Packaging, ISO 9001, and advanced color control, which narrows the addressable space for general-purpose printers. At the same time, barrier innovation is creating new opportunities in frozen and grease-sensitive food applications, where repulpable, PFAS-free coatings can help cartonboard compete more effectively with plastic-based formats. A 2025 peer-reviewed study in Cellulose showed that natural double-layer coating systems achieved a Cobb60 value of 4.5 g/m² and a Kit rating of 12/12, supporting the technical case for higher-performance paperboard barriers. This means the Canada cartonboard market is becoming more selective, with commercial success tied to compliance, functionality, and access to the right grade mix. Smaller converters can still compete well in niche work, but the broader trend favors companies that combine technical depth with stable access to supply.

Canada Cartonboard Industry Leaders

Smurfit Westrock plc

Graphic Packaging International, LLC

Metsa Board Corporation

Stora Enso Oyj

Mayr-Melnhof Karton AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Graphic Packaging International confirmed the completion of a 90-day business review and launched cost-cutting actions including a workforce reduction of more than 500 roles (approximately 3% of global workforce), with cost savings of USD 60 million targeted for 2026; the company reaffirmed full-year 2026 guidance of net sales USD 8.4 billion to USD 8.6 billion and adjusted cash flow of USD 700 million to USD 800 million.

- April 2026: Smurfit Westrock permanently shut down the SBS paper machine (machine No. 4) at its La Tuque, Quebec mill, following the February 2026 closure announcement; the shutdown removed 127,000 tons of annual SBS capacity from Canadian production and simultaneously closed the associated extrusion facility in Pointe-aux-Trembles, Quebec, affecting approximately 90 employees across both sites.

- April 2026: Prince Edward Island transitioned its deposit return system to a full EPR framework, with Encorp Atlantic as the producer responsibility organization; beverage cartons (excluding milk and plant-based) are included in the covered container scope, expanding Atlantic Canada’s carton recovery infrastructure.

- March 2026: Cascades Inc. invested CAD 6.9 million (USD 5.0 million) in its Kingsey Falls, Quebec, uncoated recycled boxboard plant (Papier Kingsey Falls), installing new equipment to improve sheet quality control and surface finish for food packaging applications, reinforcing its position in recycled-content cartonboard for food end users.

Canada Cartonboard Market Report Scope

The Canada Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Canada Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast value of the Canada cartonboard market?

The Canada cartonboard market size was USD 1.68 billion in 2025, reaches USD 1.81 billion in 2026, and is projected to reach USD 2.58 billion by 2031 at a 7.35% CAGR.

Which product grade leads cartonboard demand in Canada?

Folding boxboard led demand with 31.18% share in 2025 because it fits a wide set of food, pharmaceutical, and personal care applications.

Which packaging format is growing fastest in Canada cartonboard use?

Liquid packaging is the fastest-growing format, with a projected 7.49% CAGR from 2026 to 2031, supported by dairy and plant-based beverage demand.

Why is pharmaceutical packaging becoming more important for suppliers?

Pharmaceutical and healthcare is projected to grow at 8.05% through 2031 because compliance-driven redesign, bilingual labeling, and certification needs keep folding cartons central in the pack mix.

Which provinces matter most for cartonboard demand in Canada?

Ontario and Quebec remain the main demand centers because they combine the largest food processing, pharmaceutical manufacturing, and consumer goods packaging bases with the most developed recovery systems.

What are the biggest risks facing suppliers and converters?

The main risks are cost volatility, tighter domestic supply of premium bleached grades after the La Tuque closure, and continued competition from flexible plastic, rigid plastic, and reusable formats.

Page last updated on: