Italy Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

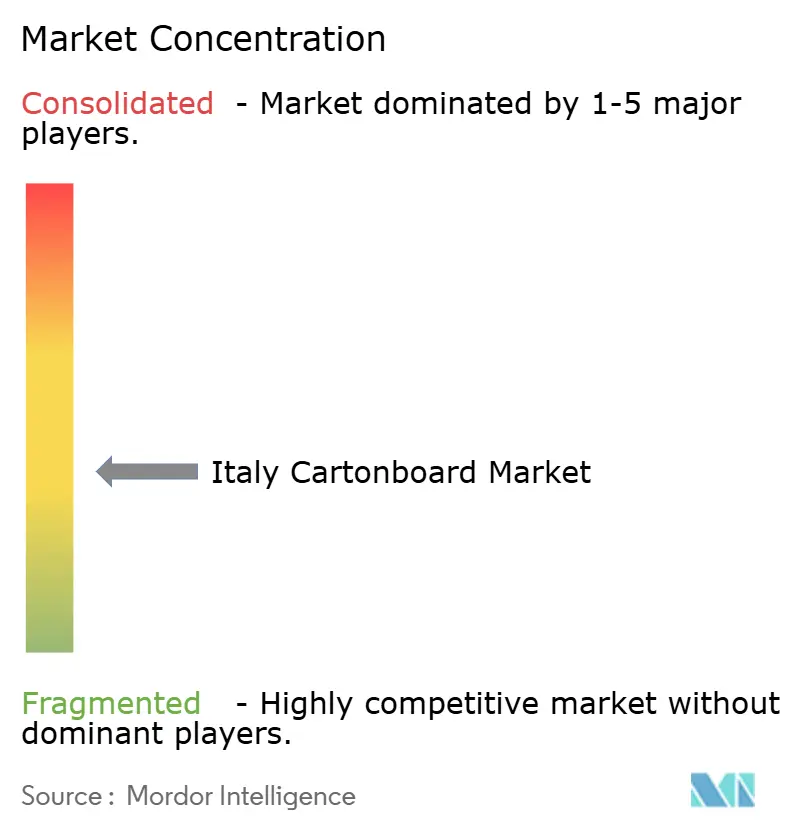

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Cartonboard Market Analysis by Mordor Intelligence

The Italy cartonboard market size is expected to increase from USD 1.65 billion in 2025 to USD 1.76 billion in 2026 and reach USD 2.43 billion by 2031, growing at a CAGR of 6.63% over 2026-2031. Growth is being supported by the early effect of the Packaging and Packaging Waste Regulation, which has pushed packaging design toward recyclable fiber-based formats and away from harder-to-recycle multi-layer plastics. Italy also benefits from its position as both a large packaging producer and an exporter of premium converted cartons, which gives local converters a wider customer base than many peers in Europe. Demand remains relatively steady because food processing, pharmaceuticals, and luxury consumer goods all require high-quality printed cartons with strong finishing and compliance standards. That mix helps the Italy cartonboard market hold value better than more commodity-exposed packaging categories. Competitive conditions remain active, with margin pressure from European board overcapacity on one side and clear opportunities in premium packaging, paper-based barriers, and regulation-led redesign work on the other side.

Key Report Takeaways

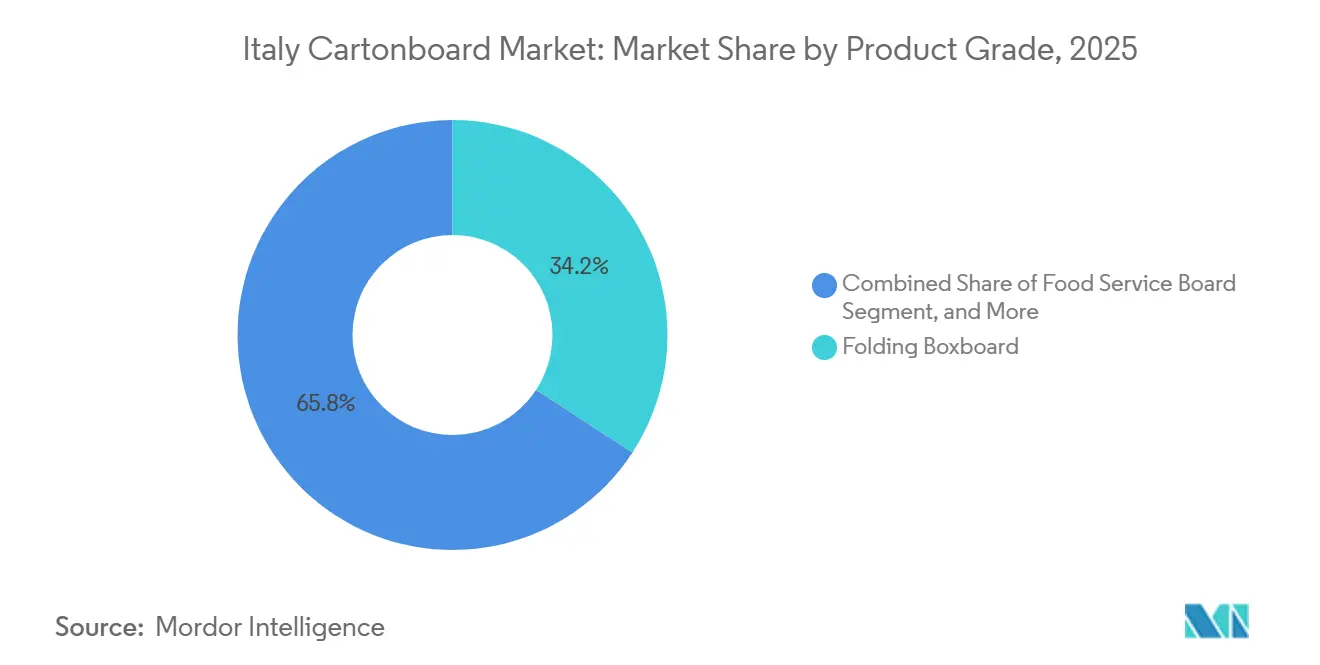

- By product grade, folding boxboard captured 34.21% of the Italy cartonboard market share in 2025.

- By packaging format, the Italy cartonboard market size for the liquid packaging segment is forecast to advance at a 6.97% CAGR through 2031.

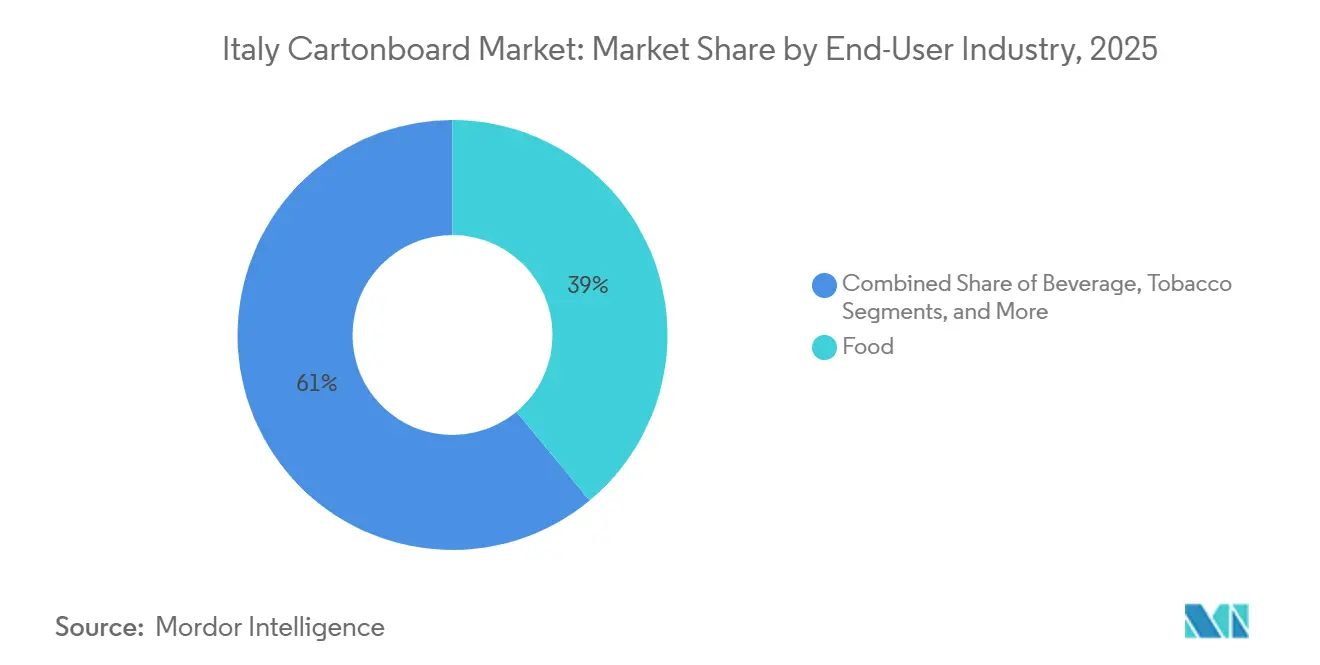

- By end-user industry, food captured 38.97% of the Italy cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-To-Paper Substitution Across Consumer Packaging | +2.1% | National, with strongest conversion activity in Lombardy, Emilia-Romagna, and Veneto industrial clusters | Short term (≤ 2 years) |

| PPWR-Driven Packaging Redesign And Void-Space Reduction | +1.4% | National, compliance burden concentrated among Northern Italy exporters with EU cross-border exposure | Medium term (2-4 years) |

| Premiumization In Food, Beauty, And OTC Packaging | +1.0% | National, with disproportionate gains in Milan-area cosmetics and OTC pharmaceutical packaging corridors | Medium term (2-4 years) |

| High Italian Paper And Board Recycling Performance | +0.6% | National, recycling leadership concentrated in Northern and Central Italy, spill-over supporting Southern Italy converter access to recycled fiber | Long term (≥ 4 years) |

| Retail-Ready And Shelf-Ready Carton Demand | +0.5% | National, with early adoption by major grocery chains in Northern Italy distribution hubs | Short term (≤ 2 years) |

| PFAS-Free And Simpler Food-Contact Barrier Structures | +0.4% | National, regulatory influence from EU PPWR Article 5 PFAS restrictions applying from August 12, 2026, affecting all food-contact packaging on the EU market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Paper Substitution Across Consumer Packaging

Plastic-to-paper substitution remains the strongest near-term demand driver for the Italy cartonboard market. The PPWR entered into force in February 2025 and will apply broadly from August 12, 2026, which makes recyclable fiber-based formats easier to position under the new EU packaging framework than many plastic alternatives.[1]European Commission, “Packaging And Packaging Waste Regulation (PPWR),” European Commission, environment.ec.europa.eu Consumer attitudes are also moving in the same direction, with Pro Carton reporting in 2025 that 89% of surveyed adults across 5 European countries preferred cartonboard to plastic packaging, while Italian and German respondents were among the most willing to pay more for sustainable packaging.[2]Pro Carton, “Pro Carton Consumer Survey Report 2025,” Pro Carton, procarton.com That change matters because demand is no longer limited to corrugated shipping packs and is moving deeper into folding cartons for frozen food, cosmetics, and other shelf-facing consumer products. As converters make lighter coated grades work in applications once dominated by plastic blisters or flexible formats, the Italy cartonboard market is gaining both volume and value opportunities. The effect is strongest where brand owners need recyclability, print quality, and premium presentation in the same pack.

PPWR-Driven Packaging Redesign And Void-Space Reduction

PPWR-led redesign is creating a second layer of demand for the Italy cartonboard market beyond simple material substitution. The regulation introduces common EU rules on packaging design and waste reduction, pushing brand owners to reduce space and reassess the structure of consumer-facing packs before the application date in August 2026. For Italy's export-oriented food and pharmaceutical converters, that pressure is especially relevant because non-compliant designs can restrict access across the full EU single market. This is increasing demand for lighter but stiffer folding boxboard grades that can preserve pack strength while trimming basis weight and pack dimensions. It also favors converters with deeper design, testing, and documentation capabilities, since customers increasingly want a packaging partner that can help them move through redesign work with less disruption. In practice, the Italian cartonboard market is benefiting not only from more board demand but also from a shift toward higher-specification grades and better-engineered packs.

Premiumization In Food, Beauty, And OTC Packaging

Premiumization continues to support value growth in the Italy cartonboard market because the country has a strong base of high-end food, beauty, and over-the-counter healthcare brands. These categories depend heavily on packaging appearance, print quality, embossing performance, and clean secondary carton structures, which lifts cartonboard value per ton. Palladio Group highlighted this shift in April 2026 when, with Bracco, it presented a science-based pharmaceutical packaging case demonstrating cartonboard alternatives to fossil-based structures for healthcare products. That example is important because it shows that premiumization in Italy is not only about luxury aesthetics but also about regulated healthcare packaging, where validation and compliance matter. As more brands combine sustainability goals with stronger shelf presentation, demand is shifting toward coated specialty boards and better converting quality. This keeps the Italy cartonboard market more resilient than packaging categories that compete mainly on price.

High Italian Paper And Board Recycling Performance

Italy's recycling system gives the Italy cartonboard market a durable operating advantage. Comieco reported 3.8 million tons of separate paper and board collection in 2024, up 3.5% year over year, and cellulosic packaging reached a 92.5% recycling rate.[3]Comieco, “30° Rapporto Annuale Su Raccolta Differenziata E Riciclo Di Carta E Cartone In Italia,” Comieco, comieco.org That performance already stood above the EU's 2030 target of 85% for paper and board packaging waste, which means Italian converters entered the PPWR transition from a stronger position than many peers. Reliable collection and recovery improve access to recycled fiber and reduce the transition cost of proving recycled-content claims to customers and regulators. This supports recycled-board users directly and also improves the credibility of cartonboard as a practical compliance route for brand owners that need fast packaging reformulation. Over time, that advantage should help the Italy cartonboard market compete more effectively for redesign projects that might otherwise go to converters in other EU countries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virgin Pulp And Electricity Cost Volatility | -1.5% | National, energy cost differential most severe for mills in Northern and Northeast Italy, where gas-indexed electricity is 30-40% above European averages | Short term (≤ 2 years) |

| Competition From Plastic And Alternative Liquid-Pack Formats | -0.8% | National, with legacy plastic-film and multi-layer carton formats most entrenched in Southern Italy dairy and beverage sectors | Medium term (2-4 years) |

| PPWR Documentation And Conformity Burden For SMEs | -0.4% | National, compliance burden disproportionately affects small and mid-size converters in Veneto and Tuscany industrial districts | Medium term (2-4 years) |

| Food-Contact Reformulation And Testing Costs After PFAS And BPA Changes | -0.2% | National, testing cost burden concentrated among specialty food-service board and food-contact folding carton producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Virgin Pulp And Electricity Cost Volatility

Cost volatility remains the clearest operating restraint for the Italy cartonboard market. Mayr-Melnhof stated in its first-quarter 2026 trading update that recent escalations in the Middle East increased pressure on energy, transportation, and chemicals from March 2026 onward.[4]Mayr-Melnhof Group, “MM Trading Statement For The First Quarter Of 2026,” EQS News, eqs-news.com In its April 2026 investor presentation, the company also said that weak market conditions and structural overcapacity persisted, which means producers have limited room to pass higher costs through the chain without risking volume loss. That combination creates a difficult environment for both virgin-fiber and recycled-board producers, as mills need to recover costs while converters remain highly price-sensitive. Financial stress at major recycled-board players adds to the caution, as RDM entered a forbearance agreement in March 2026 even though production and deliveries continued normally. Until energy, freight, and raw-material conditions stabilize, the Italy cartonboard market will continue to face margin pressure, even as underlying demand remains healthy.

Competition From Plastic And Alternative Liquid-Pack Formats

Alternative packaging formats still limit how quickly the Italy cartonboard market can gain share across applications. In liquid packaging, paper-based barriers are advancing, but flexible pouches, bag-in-box systems, and other non-board formats still hold a cost advantage in some dairy and beverage uses. SIG reported in its first-quarter 2026 financial statement that bag-in-box and spouted pouch revenue declined 5.7% at constant currency, yet these formats remain part of the competitive landscape in Europe. Elopak also noted soft consumption in Europe and declining aseptic juice demand in its first-quarter 2026 trading update, suggesting that liquid carton volumes can come under pressure even as the long-term packaging shift remains favorable. This matters in Italy because smaller food and beverage fillers often prioritize total filling cost over packaging material preference, especially in more price-sensitive regional markets. As a result, the Italy cartonboard market is growing into liquid applications, but the pace will remain uneven until paper-based solutions match alternative formats on both cost and line efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Dominates While Liquid Packaging Board Rises Fast

Folding boxboard held 34.21% of the Italy cartonboard market share in 2025, making it the largest product grade by value. Its lead came from broad use across food, OTC pharmaceuticals, cosmetics, and tobacco cartons, where stiffness, print quality, and surface finish matter as much as basic protection. White-lined chipboard remained important in mass-market packs and shelf-ready retail formats, where recycled fiber content and cost control are central to buying decisions. Solid bleached board and solid unbleached board continued to serve narrower premium niches, especially where appearance, strength, or specialty conversion requirements were more demanding.

The Italy cartonboard market size for liquid packaging board is projected to expand at a 7.31% CAGR through 2031, the fastest pace among product grades. Tetra Pak's April 2026 launch with Sterilgarda Alimenti showed that paper-based barrier technology has moved into commercial aseptic cartons and is no longer limited to development work. Tetra Pak's earlier January 2026 decision to invest EUR 60 million (USD 71.2 million) in a pilot plant for paper-based barrier development also points to sustained investment behind this grade transition. Across the Italy cartonboard industry, grade competition is shifting toward lighter structures, simpler barriers, and higher performance at lower material weight.

By Packaging Format: Folding Cartons Lead While Liquid Packaging Gains Pace

Folding cartons accounted for 57.73% of the market value in 2025, which kept them firmly at the center of the Italian cartonboard market. That dominance reflects Italy's concentration of branded food, pharmaceutical, and cosmetics manufacturing, where printed cartons remain important for both pack communication and product presentation. Sleeve-and-tray formats also benefited from retailer demand for shelf-ready solutions and from the broader move to remove unnecessary packaging layers. The PPWR reinforces that direction by favoring packaging systems that reduce waste and improve recyclability across the EU market.

Liquid packaging is projected to grow at 6.97% through 2031, making it the fastest-growing format in the Italian cartonboard market. Tetra Pak and Sterilgarda Alimenti commercially launched a 1-liter aseptic carton with a paper-based barrier in April 2026, which showed that barrier simplification can work on existing filling lines. SIG also launched an alu-layer-free full barrier solution for multi-serve aseptic cartons, adding another commercial proof point for aluminum-free structures in the Italian market. The Italian cartonboard market, therefore, has a clear opening in liquid formats, but success will depend on which suppliers can improve recyclability without disrupting converter economics or filler performance.

By End-User Industry: Food Leads Today While Pharma Expands Faster

Food accounted for 38.97% of Italy's cartonboard market revenues in 2025, making it the largest end-user segment. The category remained broad because chilled foods, confectionery, ambient products, and premium specialties all rely on printed cartons or trays for shelf presentation and transport efficiency. Retail-ready packaging also supported steady use of scored and perforated board formats in grocery distribution. Beverage demand remained strong, especially in dairy and juice cartons and premium beverage packs that require strong print execution.

The pharmaceutical and healthcare is projected to grow at a 7.06% CAGR through 2031, which makes it the fastest-growing end-user and an important part of future Italy cartonboard market size expansion. Growth in this area is tied to serialization, tamper-evidence, and higher specification requirements, which keep cartonboard central in secondary pharmaceutical packaging. Palladio Group's April 2026 presentation with Bracco showed that pharma customers in Italy are already testing validated cartonboard alternatives to fossil-based structures. The Italian cartonboard industry also benefits from premium cosmetics and spirits demand, and Pozzoli's plastic-free B-Lock system demonstrates how brand owners want stronger sustainability performance without sacrificing high-end presentation.

Geography Analysis

Northern Italy remained the main operating center within the Italy cartonboard market, supported by dense customer clusters in food, pharmaceuticals, and premium consumer goods. Tetra Pak's continued paper-based barrier work through its Modena base in Emilia-Romagna shows how product development and commercialization remain closely tied to the north of the country. Lombardy also stayed important for high-specification packaging demand, with Palladio Group using Milan's Pharma Hub 2026 to present cartonboard reformulation work developed with Bracco. That northern concentration matters because converters can work close to major brand owners, testing centers, and equipment partners when redesign cycles become more demanding. This gives the Italy cartonboard market a strong regional anchor even when broader European demand remains uneven.

Central and Southern Italy carried a smaller packaging base, but their role improved as recycling performance widened beyond the north. Comieco reported that Southern Italy passed 50 kg of paper collection per inhabitant in 2024 for the first time, while national separate paper and board collection reached 3.8 million tons, up 3.5% year over year. That change helps reduce the old fiber access gap between northern mills and southern converters, especially for recycled grades. Italy's 92.5% recycling rate for cellulosic packaging in 2024 also provides converters across the country with a stronger foundation for recycled-content claims and procurement discussions. As recovery infrastructure improves outside the main northern corridors, the Italy cartonboard market should benefit from a wider and more balanced domestic fiber network.

Italy's regulatory readiness adds another geographic advantage to the Italy cartonboard market inside the wider EU. The PPWR will apply broadly from August 12, 2026, and its common design-for-recyclability rules favor fiber-based formats that already fit Italy's packaging strengths. Because Italy already exceeded the EU's 2030 paper and board recycling target in 2024, domestic converters face less transition friction than players in countries with weaker recovery systems. This combination of location, recycling depth, and export-oriented converting capability keeps Italy strategically important in European cartonboard supply chains.

Competitive Landscape

The Italy cartonboard market combines moderate concentration at the board supply level with a much more fragmented structure in converting. Large integrated producers such as Mayr-Melnhof, Stora Enso, and Smurfit Kappa supply boards to Italy, while domestic specialists compete in pharmaceutical, luxury, and premium consumer packaging niches. Mayr-Melnhof said in its April 2026 investor presentation that weak market conditions and structural overcapacity persisted, which helps explain why pricing stayed under pressure despite stronger regulation-led demand drivers. Stora Enso's new consumer board capacity at Oulu is also expanding the premium board options available to Italian converters as the line ramps up to full output. This mix of scale upstream and specialization downstream keeps rivalry active across both price and specification.

Competitive behavior in the Italy cartonboard market is increasingly shaped by compliance support, material simplification, and premium product development. Tetra Pak's January 2026 investment of EUR 60 million (USD 71.2 million) in paper-based barrier technology shows how suppliers are trying to secure future demand by developing proprietary pack structures that still work with existing filling systems. Palladio Group's collaboration with Bracco shows a similar pattern on the converter side, where sustainability validation and regulatory readiness are becoming commercial differentiators rather than back-office tasks. Pozzoli's B-Lock paper-and-paperboard anchoring system adds another example, since it removes plastic and magnets from premium bottle packs without reducing presentation quality. These moves raise the standard for smaller converters that compete mainly on price or short-run flexibility.

The clearest pressure point remains recycled board, where RDM's March 2026 forbearance agreement showed how financial strain can surface when weak pricing meets difficult operating conditions. Even so, the Italy cartonboard market still leaves room for specialists that can meet premium print requirements, pharmaceutical compliance needs, or redesigned mono-material pack demand faster than broad-based suppliers. The field, therefore, remains open to selective consolidation upstream, while downstream conversion should remain fragmented because customer requirements vary widely by sector and pack type. On balance, the Italian cartonboard market rewards companies that pair strong board performance with customer-specific design support and compliance know-how rather than scale alone.

Italy Cartonboard Industry Leaders

Mayr-Melnhof Karton AG

Reno De Medici S.p.A.

Stora Enso Oyj

Smurfit Westrock plc

Graphic Packaging International, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pozzoli S.p.A. exhibited its B-Lock patent, a plastic-free, magnet-free paper-and-paperboard engineering system for anchoring bottles within carton trays, at Packaging Première Milan. The solution was originally developed for Jack Daniel's Bonded spirits packaging and targets the premium spirits and wine packaging segment.

- April 2026: Tetra Pak and Italian dairy company Sterilgarda Alimenti commercially launched the world's first 1-liter aseptic carton featuring a paper-based barrier, produced on existing Tetra Pak A3 filling lines. The launch reduced the carbon footprint of the pack compared with conventional aluminum-composite structures and marked a major step in liquid packaging board reformulation in the domestic dairy market.

- April 2026: Palladio Group S.p.A. presented a science-based sustainable pharmaceutical packaging case study developed in partnership with Bracco at Pharma Hub 2026 in Milan on April 15, 2026. The project demonstrated life cycle assessment-validated cartonboard alternatives to fossil-based packaging structures for healthcare products.

- March 2026: Reno De Medici S.p.A. entered into a forbearance agreement with holders of its EUR 600 million (USD 672 million) floating rate senior secured notes due 2029, after electing not to pay the March 16, 2026 coupon. The company stated that production and deliveries continued normally, although the recapitalization negotiations introduced uncertainty for its Italian mill operations.

Italy Cartonboard Market Report Scope

The Italy Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board.. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Italy Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the size of the Italy cartonboard market in 2026?

The Italy cartonboard market stands at USD 1.76 billion in 2026 and is forecast to reach USD 2.43 billion by 2031, with a 6.63% CAGR over 2026-2031.

Which product grade leads cartonboard demand in Italy?

Folding boxboard leads the product mix with a 34.21% share in 2025 because it is widely used in food, OTC pharmaceutical, cosmetics, and tobacco cartons.

Which packaging format is growing the fastest in Italy?

Liquid packaging is the fastest-growing format, with a projected 6.97% CAGR through 2031 as paper-based barrier technology gains commercial use.

Which end-user segment offers the best growth outlook through 2031?

Pharmaceutical and healthcare shows the strongest growth outlook, with a projected 7.06% CAGR supported by serialization, tamper evidence, and higher packaging standards.

Why is recycling performance important for cartonboard producers in Italy?

Italy recorded a 92.5% recycling rate for cellulosic packaging in 2024, which improves fiber availability and lowers the transition burden linked to recycled-content and recyclability requirements.

What is the main risk for cartonboard producers and converters in Italy?

The main near-term risk is cost volatility, especially in energy and raw materials, combined with competitive pressure from alternative liquid-pack formats in price-sensitive applications.

Page last updated on: