Mexico Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

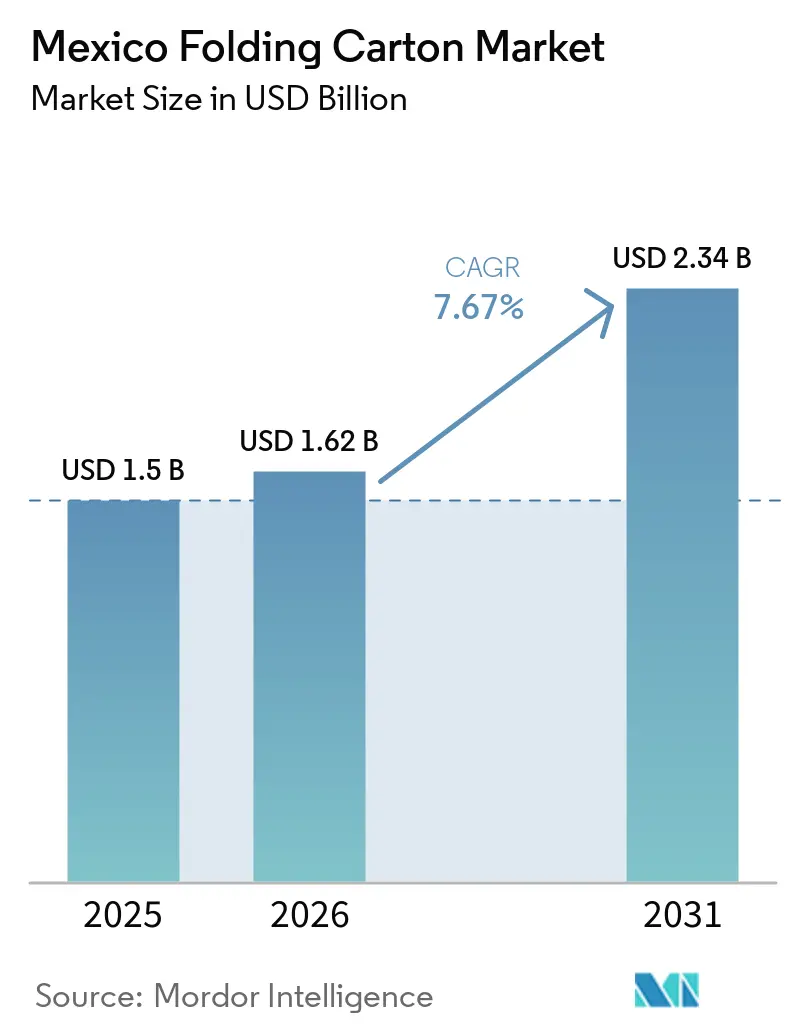

| Base Year Market Size (2025) | USD 1.5 Billion |

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 7.67% CAGR |

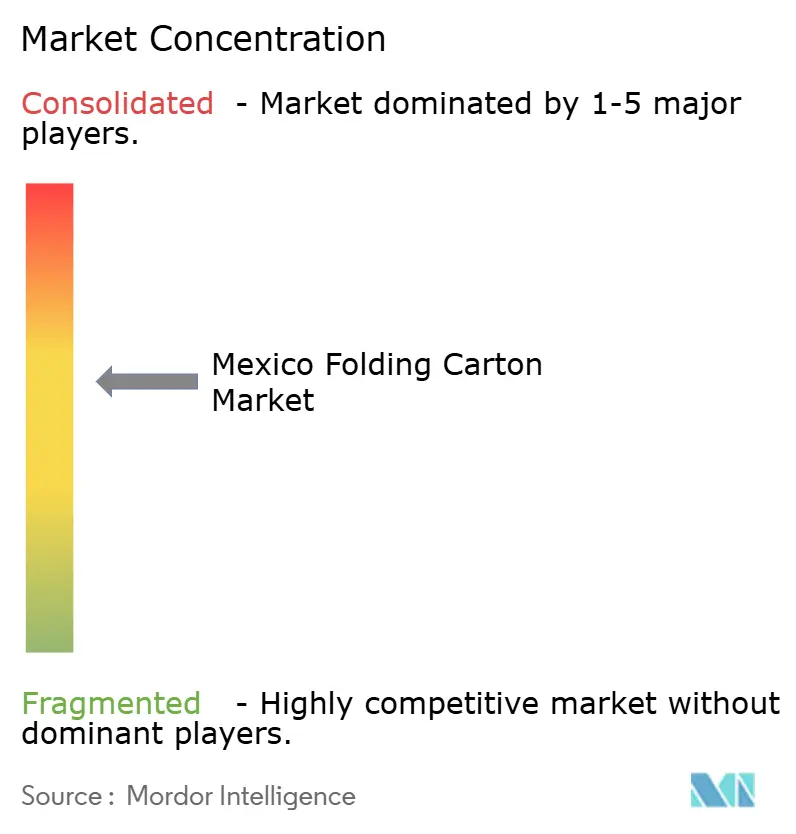

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Folding Carton Market Analysis by Mordor Intelligence

The Mexican folding carton market size is projected to expand from USD 1.50 billion in 2025 and USD 1.62 billion in 2026 to USD 2.34 billion by 2031, registering a CAGR of 7.67% between 2026 and 2031. Robust consumer-goods manufacturing migrating from Asia to northern Mexico is translating into larger print runs for food, beverage, personal-care, and electronics carton, while the United States-Mexico-Canada Agreement (USMCA) rules of origin keep production footprints inside the trade bloc. Converter revenue is also benefiting from the General Law on the Circular Economy, which entered into force in 2026, as its life-cycle-assessment requirements favor recyclable substrates over multilayer laminates. Intensifying e-commerce adoption is reshaping product design toward shelf-ready carton that reduce handling labor in fulfillment centers, and brand-owner premiumization programs are raising demand for high-graphics specialty coatings that differentiate products on crowded retail shelves. At the same time, pulp-price volatility and competition from flexible pouches are pressuring converter margins, accelerating backward integration into recycled-paperboard capacity and sparking investments in short-run digital presses capable of variable-data personalization.

Key Report Takeaways

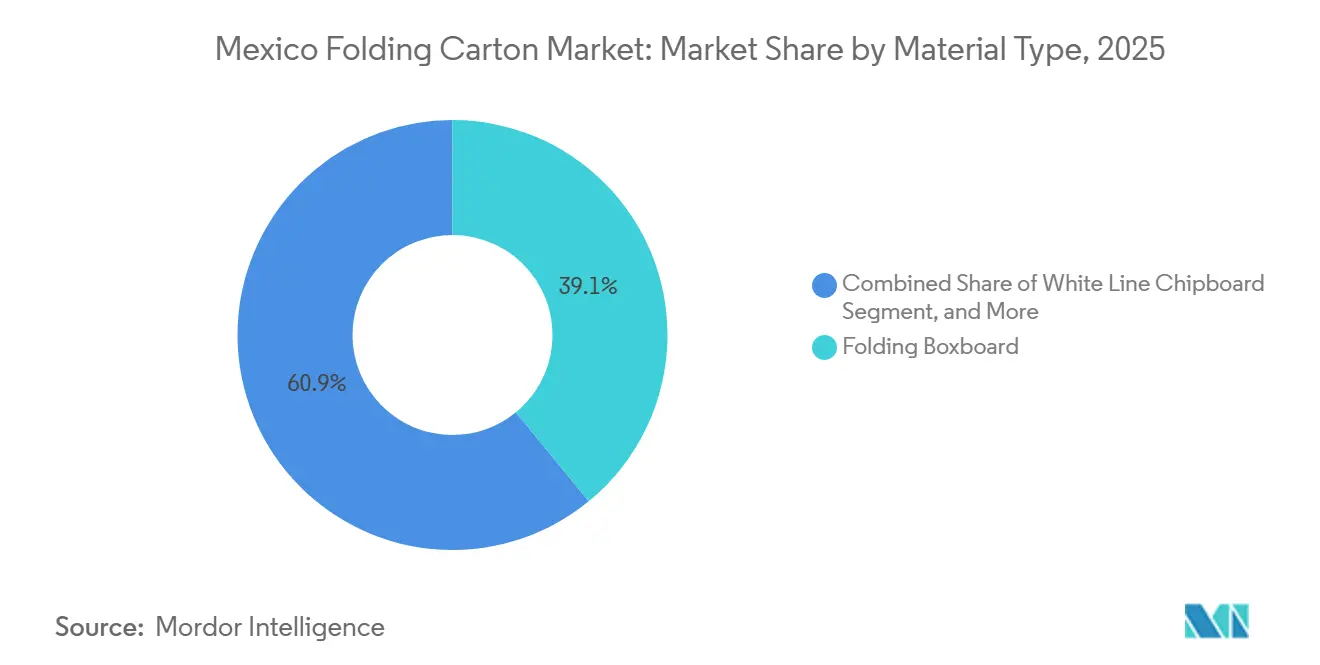

- By material type, folding boxboard captured 39.08% of the Mexico folding carton market share in 2025.

- By printing technology, the Mexico folding carton market size for the digital printing segment is forecast to advance at a 9.21% CAGR through 2031.

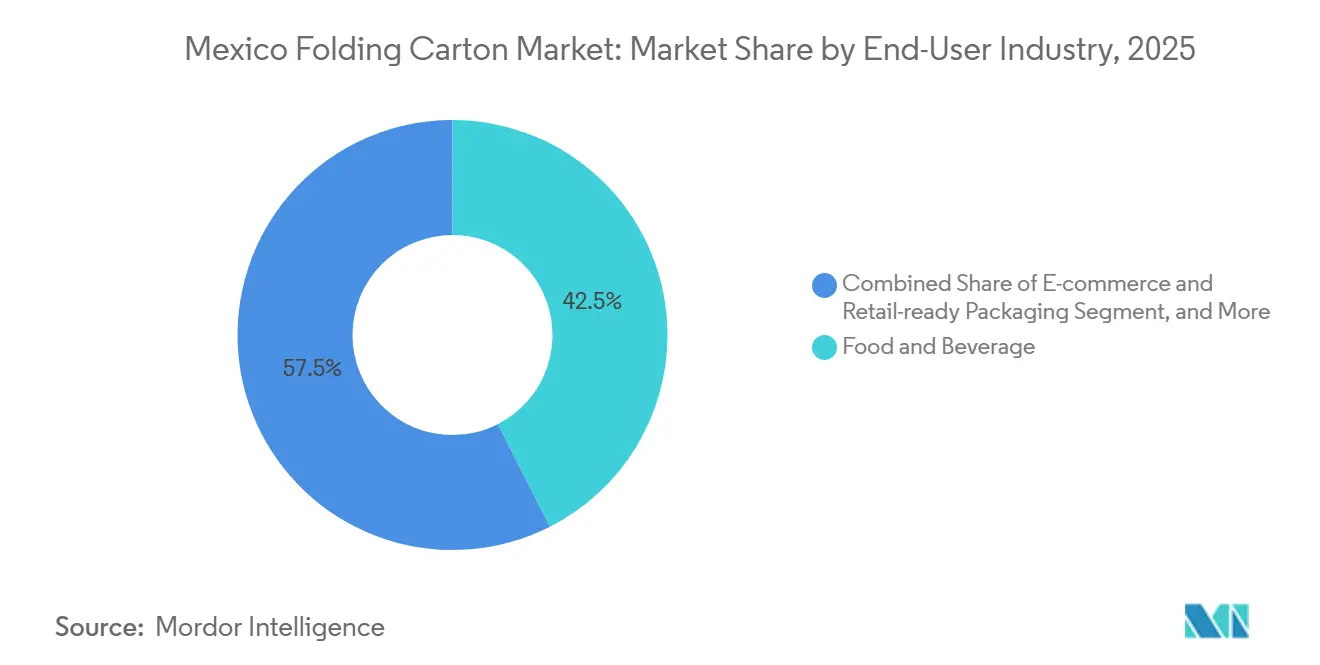

- By end-user industry, food and beverage captured 42.51% of the Mexico folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-Focused Regulations Accelerating Fiber-Based Packaging Adoption | +1.80% | Nationwide, early compliance in Mexico City, Monterrey, Guadalajara metro areas | Medium term (2-4 years) |

| Expansion of Near-Shore FMCG Manufacturing Hubs Creating Carton Demand | +2.10% | Nuevo León, Chihuahua, Sonora, Baja California, Querétaro, Guanajuato | Short term (≤ 2 years) |

| E-Commerce Boom Fueling Retail-Ready Folding Carton Volumes | +1.50% | Mexico City, Guadalajara, Monterrey fulfillment corridors | Short term (≤ 2 years) |

| Technology Shift to Short-Run Digital Printing Enabling Personalization | +1.00% | Monterrey, Querétaro, Estado de México converting clusters | Medium term (2-4 years) |

| Rising Premiumization in Food and Cosmetics Elevating High-Graphics Carton Use | +0.90% | Urban centers nationwide | Long term (≥ 4 years) |

| Government Incentives for Circular Economy Investments Boosting Recycling Capacity | +0.70% | Pilot programs in Estado de México and Nuevo León | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Focused Regulations Accelerating Fiber-Based Packaging Adoption

Mexico’s General Law on the Circular Economy established a national compliance platform that tracks packaging life-cycle assessments, and its architecture can be extended to paperboard once SEMARNAT publishes product-category agreements.[1]Duncan Randall, “Mexico Plastics Industry Prepares for Circular Economy Law,” MexicoBusiness.News, mexicobusiness.news Grupo Bimbo already achieved 94% of its packaging being recyclable or compostable in 2025, showing how major carton buyers are aligning procurement with the new framework. Converters that certify recycled-content traceability gain preferred-supplier status with multinational consumer-goods companies racing toward science-based climate targets. Because folding carton are compatible with existing curbside collection, the law tilts substrate selection toward paperboard rather than multilayer flexibles. Early movers integrating recycled-fiber monitoring software are positioned to capture long-term contracts as brand owners lock in compliant partners.

Expansion of Near-Shore FMCG Manufacturing Hubs Creating Carton Demand

USMCA local-content thresholds are driving electronics, appliance, and food-processing plants into border states and the Bajío, sharply lifting regional carton consumption. Smurfit Westrock’s USD 65 million Ciudad Obregón project will commission high-graphic folding-carton lines in 2027 to serve beer and snack makers relocating capacity from Asia.[2]Israel Molina, “Smurfit Westrock Invertirá 65 mdd en Nueva Planta de Empaque en Sonora,” Mexico Industry, mexicoindustry.com Nuevo León and Querétaro already host clusters of carton converters that deliver just-in-time supplies to automotive and consumer-goods assembly, cutting lead times versus imports. Industrial parks built around rail routes in Texas lower logistics costs, making locally converted carton cost-competitive even when Asian suppliers undercut on unit price. The nearshoring wave is therefore locking in additional square meters of print capacity in the Mexican folding carton market, supporting volume growth ahead of domestic GDP.

E-Commerce Boom Fueling Retail-Ready Folding Carton Volumes

Amazon’s and Mercado Libre’s new fulfillment centers require secondary carton that double as shelf-ready displays, which, in turn, shift design toward perforated tear strips and self-locking bottoms that eliminate repacking at the store. Retailers also pressure converters to keep dimensional weight low to manage last-mile delivery charges, incentivizing lightweighted cartonboard. Because parcel networks penalize over-box waste, converters now simulate drop tests in CAD software to optimize fiber use without compromising integrity. Variable QR codes are printed inline for item-level tracking, bridging inventory systems between warehouses and physical stores. This omnichannel packaging requirement is unique to the Mexican folding carton market because the country’s fragmented retail mix still depends on mom-and-pop tiendas that need shelf-ready packs as soon as they remove outer flaps.

Technology Shift to Short-Run Digital Printing Enabling Personalization

HP Indigo’s fifth-generation 200K press raises throughput by 45% while supporting cartonboard up to 450 microns, bringing digital economics closer to flexo for print runs under 50,000 sheets.[3]Haim Levit, “A Decade of Digital Momentum: How HP Indigo and ePac Are Scaling the Future of Flexible Packaging,” HP Newsroom, hp.com Mexican converters with legacy eight-color flexo lines face one-hour setup times and hundreds of meters of substrate waste, whereas digital changeovers take 15 minutes and generate negligible spoilage. Personal-care and craft-beer brands increasingly demand hyper-localized artwork, a requirement only feasible through variable-data workflows. Early adopters are combining digital fronts with offline embellishment, such as cold-foil and soft-touch, to deliver premium haptics without breaking recyclability. The result is a tiered production model in which commodity SKUs remain on flexo while fast-fashion SKUs migrate to digital, widening the service range each plant can offer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Virgin Pulp Prices Compressing Converter Margins | -1.20% | Nationwide, highest exposure in border states reliant on imported pulp | Short term (≤ 2 years) |

| Competition From Flexible Packaging in Single-Serve Applications | -0.80% | Snack foods, confectionery, beverage powders nationwide | Medium term (2-4 years) |

| Skilled Operator Shortage Slowing High-Speed Press Utilization | -0.50% | Monterrey, Querétaro, Guadalajara industrial clusters | Medium term (2-4 years) |

| Fragmented Paper Recovery Infrastructure Hindering Post-Consumer Collection | -0.40% | Southern states and rural municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Pulp Prices Compressing Converter Margins

Smurfit Westrock reported energy and fiber inflation in 2025, noting a North American fiber mix of 57% virgin and 43% recycled, which exposes costs to spot-market swings. Because many contracts index carton prices with a 2-month lag, spikes in Northern Bleached Softwood Kraft can wipe out entire quarters of margin for converters that lack backward integration. Smaller plants in Chihuahua and Baja California import fluff pulp through Pacific ports, adding freight surcharges that amplify volatility. Internal-cash financing dominates sector investment, as 80% of 2024 pulp and paper FDI was reinvested earnings, limiting strategic reserves.[4]Gobierno de México, “Fabricación de Pulpa, Papel y Cartón,” Data México, datamexico.gob.mx Converters are therefore negotiating multi-year supply agreements and expanding recycled-paperboard machines to immunize against volatility in virgin pulp prices.

Competition From Flexible Packaging in Single-Serve Applications

Stand-up pouches weigh up to 70% less than equivalent folding carton and integrate high-barrier films that extend shelf life for snack foods and beverage powders. HP Indigo’s new presses cater directly to flexible substrates, escalating capital inflows toward pouches and sachets. Graphic Packaging’s PaperSeal barrier-lined trays and KeelClip multipacks represent paperboard counter-offers, but the cost delta still favors film in ultra-price-sensitive segments. Retailers pushing unit-price visibility prefer clear pouches that showcase product, eroding carton share on impulse racks. Folding-carton converters must therefore accelerate lightweighting and barrier-coating R&D to keep single-serve applications inside the Mexican folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Grades Gain As Premiumization Persists

Folding Boxboard captured 39.08% of the Mexican folding carton market in 2025, retaining leadership because its stiffness and FDA-compliant coating meet mainstream food and beverage packaging requirements. White Line Chipboard is projected to record an 8.16% CAGR through 2031, reflecting brand-owner shifts toward recycled-content mandates supported by national circular-economy policy. Solid Bleached Sulfate remains the material of choice for cosmetics and pharmaceuticals that demand bright surfaces for foil stamping, while Coated Unbleached Kraft addresses frozen foods requiring wet strength. Hybrid constructions that laminate SBS facings on recycled cores are emerging to blend cost savings with premium graphics, indicating a nuanced trade-off between luxury cues and sustainability commitments. Converters expanding recycled-paperboard machines in Nuevo León are positioning to capture surging demand from e-commerce shippers that value lightweighting. Even so, premium segments preserve SBS volumes, ensuring a dual-track material landscape that rewards plants capable of switching rapidly between recycled and virgin grades without downtime.

Rising pulp-price risk and environmental compliance concerns amplify interest in recycled content, but luxury confectionery exported to the United States still specifies 92-plus brightness levels, which are only available from virgin fiber. The Mexico folding carton market size for recycled grades will therefore grow faster than total demand, yet SBS and CUK will defend niches where brand equity or functional barrier properties trump cost sensitivity. Segment profitability hinges on converters’ ability to source consistent post-consumer fiber at scale, a capability that the Circular Economy Law’s incentive pool seeks to expand. Plants that integrate de-inking and dispersion washing onsite reduce dependence on third-party recyclers and unlock material self-sufficiency, a strategic hedge against both price shocks and supply disruptions.

By Printing Technology: Digital Disrupts Flexo’s Installed Base

Flexographic units generated 37.47% of 2025 revenue thanks to decades of investment in wide-web lines across Monterrey and Guadalajara. However, digital platforms are forecast to outpace all other processes at a 9.21% CAGR, driven by SKU proliferation and retailers' calls for just-in-time replenishment. The break-even cost between flexo and digital has dropped from 10,000 sheets in 2020 to under 5,000 sheets in 2026, as click charges fall and substrate versatility widens, making digital commercially viable for regionalized promotions. Lithography maintains hold in high-fidelity cosmetic carton, and gravure serves hop-wrapper multipacks that exceed 20 million impressions annually. Converters employing hybrid workflows, preprinting digital inserts nested into flexo shells, extend service offerings from artisanal coffee micro-roasters to multinational cereal producers. Government incentives for Industry 4.0 upgrades further encourage plants to retrofit with inspection cameras and closed-loop color control, narrowing the quality gap between analog and digital systems.

Mexican converters that bundle structural design with digital personalization secure contracts to print influencer-themed limited editions, shortening product-launch cycles from 90 to 30 days. Digital job data also feeds carbon-footprint dashboards requested under the Circular Economy Law, creating a compliance edge. Conversely, plants lacking variable-data competence risk being relegated to commodity projects with thinner margins. The Mexican folding carton market is therefore on the cusp of a two-speed technology trajectory, in which early digital adopters leapfrog peers on turnaround and inventory metrics.

By End-User Industry: E-Commerce Reshapes Carton Specifications

Food and Beverage generated 42.51% of 2025 carton demand, anchored by bakery, beer, and soft-drink volumes that require grease-resistant coatings and high-speed erection. Yet e-commerce and retail-ready applications are projected to post an 8.89% CAGR, the highest among end users, fueled by fulfillment centers seeking carton that arrive shelf-ready with perforated fronts and QR-code tracking. Pharmaceuticals demand tamper-evident flaps and Braille embossing, raising technical barriers to entry for small converters, while personal-care brands push premium textures and soft-touch coatings. Electronics assemblers in Tijuana and Ciudad Juárez specify antistatic linings and rigid corner protection, adding complexity and margin compared with standard six-corner gluing. Tobacco and household-goods segments remain steady but face substitution threats from pouches and bags if carton lightweighting stalls. Consequently, converters expanding design centers that simulate drop tests and ergonomic shelf retrievals will gain share among omni-channel retailers, ensuring e-commerce remains a pivotal growth lever in the Mexican folding carton market.

Multinational CPGs such as Nestlé and PepsiCo increasingly request harmonized dielines across North America to streamline regional launches, rewarding Mexican plants certified to both ISO 22000 food safety and G7 color standards. End-user diversification helps offset cyclical softness in discretionary categories like cosmetics during economic downturns. The segment mix, therefore, cushions revenue volatility for large integrated players while still offering niche profitability for specialists in regulated pharmaceuticals or luxury confectionery.

Geography Analysis

Estado de México and Nuevo León lead the highest carton output because they host integrated mills and large consumer-goods factories, creating dense ecosystems of ink suppliers, plate engravers, and maintenance contractors. Smurfit Westrock’s Monterrey mill alone supplies more than 400,000 tonnes of containerboard and 110,000 tonnes of paperboard annually, creating scale synergies for nearby converters. Nuevo León’s proximity to the Laredo border gateway allows overnight truckloads into Texas, powering just-in-time packaging flows for auto parts and craft-brew imports. Querétaro and Guanajuato form a Bajío corridor where automotive and aerospace suppliers demand high-precision carton for component kitting, pulling graphic-capacity investments into mid-sized cities like Celaya.

Sonora, Chihuahua, and Baja California are experiencing above-average growth rates as assembly plants relocate from Asia under USMCA incentives, and the new Ciudad Obregón plant will raise local folding-carton availability once it starts in 2027. Cross-border value chains often shuttle U.S.-made paperboard south for conversion, then ship finished carton north with assembled goods, a loop that reduces tariff exposure but inflates freight costs. Southern states such as Chiapas and Oaxaca lag because limited manufacturing bases suppress carton demand and fragmented waste-paper collection hinders recycled-fiber supply, presenting future expansion targets once infrastructure upgrades unlock economies of scale.

Regional regulatory pilots further differentiate growth prospects. Mexico City has already trialed mandatory recycled-content thresholds ahead of federal guidelines, forcing capital-region converters to certify traceability systems sooner than peers in the north. Nuevo León and Estado de México host early municipal subsidies for curbside fiber collection, stabilizing post-consumer feedstock for recycled chipboard. Plants operating across multiple states can therefore hedge policy risk by allocating capacity to regions with more predictable compliance pathways, balancing their footprint in the Mexico folding carton market.

Competitive Landscape

Global integrators and domestic champions share the Mexico folding carton market. Smurfit Westrock leads with USD 2.52 billion in 2025 Mexico revenue and six integrated mills that secure virgin and recycled fiber streams, while Graphic Packaging runs three converting sites that import U.S.-made board for high-graphics applications. International Paper supplies SBS but converts limited volumes locally, relying instead on partnerships with Grupo Gondi and Papelera Ponderosa for on-the-ground finishing. Mid-tier players such as Grupo Gráfico Romo carve out niches in the cosmetics and pharmaceutical carton markets, differentiating through quick-response digital lines and ISO 13485 certification.

HP Indigo partnerships allow early adopters to offer variable-data campaigns for beer and snack brands launching regionalized promotions tied to soccer tournaments. Graphic Packaging’s CleanClose child-resistant closure, certified under U.S. standard 16 CFR §1700.20, opens regulated pharmaceutical channels where few local competitors comply. Domestic converters counter by leveraging proximity for design-for-manufacture workshops that international rivals struggle to replicate without local engineering talent. Sustainability is another wedge, with Grupo Bimbo’s supplier scorecards now weighting carbon intensity, pushing converters toward recycled content and renewable-energy sourcing.

Mergers and acquisitions remain plausible as top-line growth outpaces capacity additions, and multinationals eye tuck-in deals to gain regulatory relationships and established sales teams. Nonetheless, family-owned plants representing under 5% individual share still populate the long tail, preventing rapid consolidation. Overall, the Mexico folding carton market displays moderate concentration and high innovation intensity, rewarding players that integrate fiber security, advanced printing, and compliance expertise.

Mexico Folding Carton Industry Leaders

Smurfit Westrock plc

Graphic Packaging Holding Company

International Paper Company

Grupo Gráfico Romo, S.A. de C.V.

Cartro S.A.P.I. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: HP Inc. signed a USD 50 million agreement with ePac to install ten HP Indigo 200K digital presses worldwide, accelerating digital adoption in flexible packaging and folding carton.

- January 2026: Mexico’s General Law on the Circular Economy took effect, obligating producers to file Circular Management Plans once SEMARNAT issues product-category rules.

- December 2025: Smurfit Westrock committed USD 65 million to a new Ciudad Obregón packaging plant slated to open in 2027 with high-graphic folding-carton lines.

- September 2025: Graphic Packaging updated guidance to USD 8.4-8.6 billion in 2025 net sales and confirmed its Waco recycled-board mill would add USD 80 million to 2026 EBITDA.

Mexico Folding Carton Market Report Scope

The Mexico folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into carton for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Mexico Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Mexico folding carton market?

The Mexico folding carton market size is expected to reach USD 1.62 billion in 2026, on its way to USD 2.34 billion by 2031.

Which material type is growing fastest through 2031?

White Line Chipboard is forecast to expand at an 8.16% CAGR because its recycled content aligns with emerging circular-economy mandates.

How will nearshoring affect folding-carton demand?

USMCA-driven relocation of FMCG and electronics plants to northern Mexico is lifting local carton volumes and spurring new converting capacity near border trade corridors.

Why are converters investing in digital printing?

Variable-data digital presses shorten setup time, cut substrate waste, and enable personalized campaigns, giving converters a service edge for e-commerce and premium SKUs.

Which end-user segment offers the highest growth opportunity?

E-commerce and retail-ready packaging is projected to advance at an 8.89% CAGR as new fulfillment centers seek shelf-ready carton that reduce handling labor.

What regulatory changes will shape material selection?

The General Law on the Circular Economy mandates life-cycle assessments, favoring recyclable paperboard over multilayer laminates and accelerating recycled-content adoption.

Page last updated on: