Europe Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.17 Billion |

| Market Size (2026) | USD 13.63 Billion |

| Market Size (2031) | USD 16.42 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cartonboard Market Analysis by Mordor Intelligence

The Europe cartonboard market size is projected to be USD 13.17 billion in 2025, USD 13.63 billion in 2026, and reach USD 16.42 billion by 2031, growing at a CAGR of 3.79% from 2026 to 2031. Growth remains measured because plastic substitution is adding demand while lightweighting and reuse rules are limiting tonnage growth per pack. The European cartonboard market is also becoming more valuable per tonne as premium print finishes, barrier coatings, and serialization features raise average selling prices faster than raw volumes. Consumer preference is reinforcing this shift, with cartons increasingly favored over plastic in everyday purchase decisions and retailer sourcing requirements. Integrated producers continue to use fiber access, energy integration, and mill scale to defend margins, while converters compete on print quality, lead times, and sustainability credentials. The result is a European cartonboard market that is expanding steadily through compliance-led material shifts, premiumization, and tighter commercial discipline after a period of heavy capacity buildout.

Key Report Takeaways

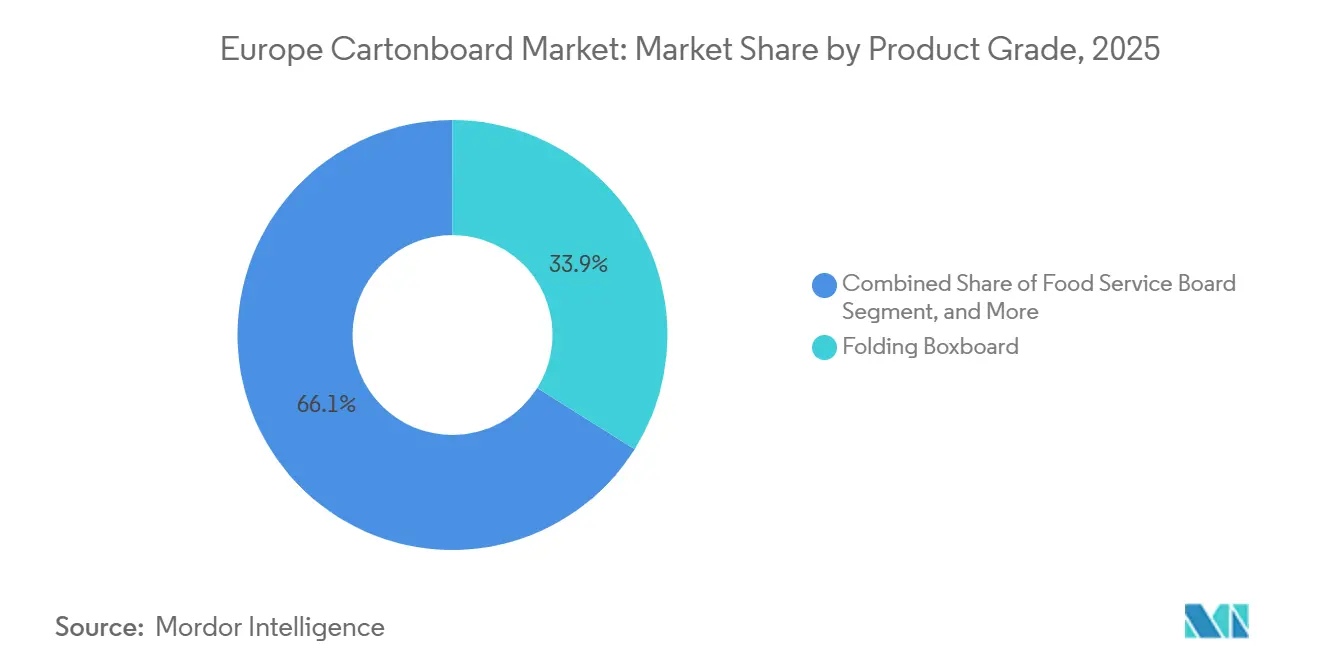

- By product grade, folding boxboard captured 33.91% of the Europe cartonboard market share in 2025.

- By packaging format, the Europe cartonboard market size for the liquid packaging formats segment is forecast to advance at a 5.43% CAGR through 2031.

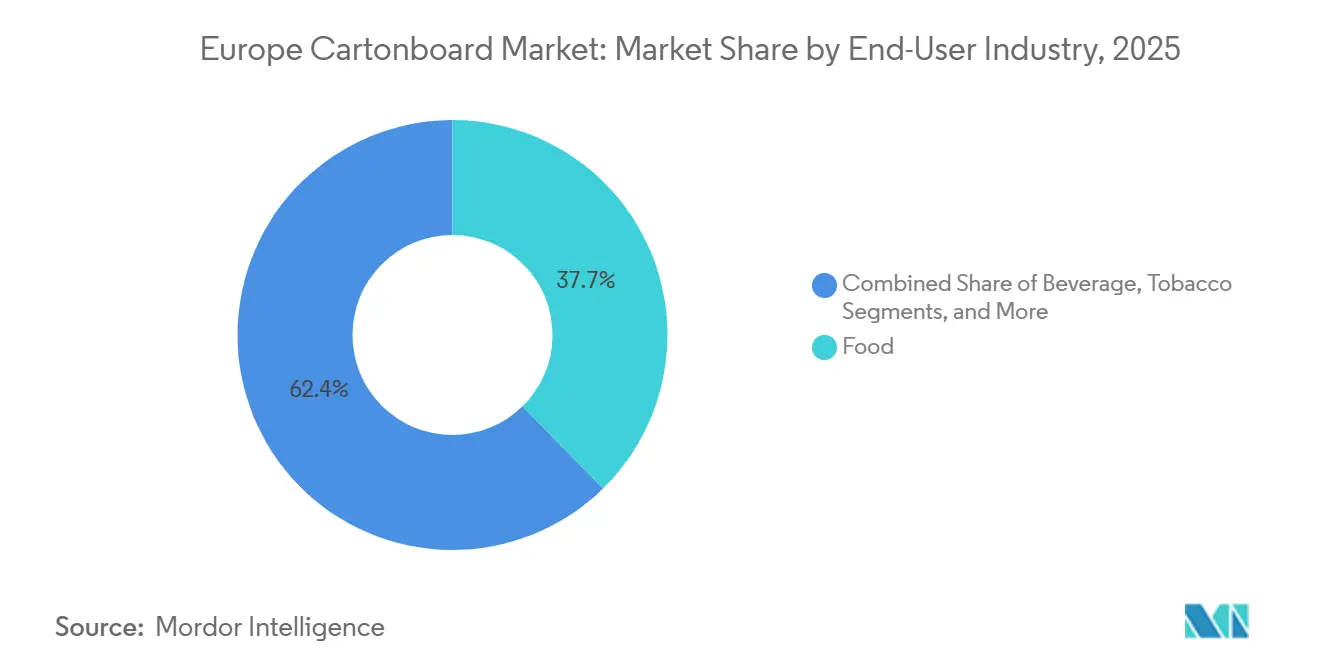

- By end-user industry, food captured 37.65% of the Europe cartonboard market share in 2025.

- By geography, the Europe cartonboard market size for the Spain segment is forecast to advance at a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-To-Fiber Substitution Under PPWR And SUPD | +1.1% | EU-27 wide, concentrated in Germany, France, and Italy | Short term (≤ 2 years) |

| Recyclable Shelf-Ready Packs In Food Retail | +0.9% | Northern and Western Europe, Germany, France, United Kingdom | Short term (≤ 2 years) |

| Pharmaceutical Serialization And Tamper-Evident Cartons | +0.6% | Germany, France, Italy | Medium term (2-4 years) |

| Premium Beauty And Personal Care Carton Upgrading | +0.4% | Western Europe, France, United Kingdom, Italy | Medium term (2-4 years) |

| QR-Enabled Compliance And Digital Labeling On Pack | +0.2% | EU-wide, stronger early uptake in Germany and France | Long term (≥ 4 years) |

| PFAS-Free Barrier Migration In Food Service Board | +0.1% | EU-27 wide, effective August 2026 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Fiber Substitution Under PPWR And SUPD

Regulation (EU) 2025/40 entered into force on February 11, 2025, and will apply across all 27 EU member states from August 12, 2026, giving the Europe cartonboard market one common packaging rulebook across the region.[1]European Commission, “Regulation (EU) 2025/40 of the European Parliament and of the Council on Packaging and Packaging Waste,” Official Journal of the European Union, ec.europa.eu The regulation goes beyond the earlier directive model by tying design-for-recycling criteria, recycled-content obligations, and EPR fee modulation directly to packaging choices that brand owners cannot easily delay. In practical terms, this places greater pressure to redesign complex plastic formats, while many carton formats already meet recyclability expectations under the new framework.[2]European Commission, “Packaging and Packaging Waste Regulation, Guidelines on Implementation for Economic Actors and Member States,” European Commission, ec.europa.eu Mayr-Melnhof Karton AG has already positioned fiber-based materials as transition tools for customers working through packaging change programs, showing how regulation is becoming part of the sales process in the Europe cartonboard market. Pro Carton found in its 2026 consumer survey that 53% of European respondents cited non-recyclable packaging as a reason for brand switching, which is pushing retailer specifications and brand-owner timelines in the same direction.[3]Pro Carton, “The Power of Packaging, What Makes European Consumers Trust, Stay or Switch? Consumer Survey 2026,” Pro Carton, procarton.com

Recyclable Shelf-Ready Packs In Food Retail

Food retail packaging programs in Germany, France, and the United Kingdom are moving shelf-ready formats toward recyclable mono-material carton solutions, turning sustainability from a brand preference into a commercial listing condition in more categories. This matters because EPR fee modulation increasingly rewards recyclable packaging, so the financial case for carton conversion now sits alongside the merchandising case, making decisions easier to justify internally. The effect supports folding boxboard demand because shelf-ready packs favor formats that print well, convert efficiently, and remain easy to recycle even when basis weights are reduced. Smurfit Westrock’s 2026 Innovation Event in the Netherlands brought together more than 450 customers and introduced 3 AI-based packaging design tools that demonstrate how digital development is shortening customization cycles for shelf-ready packaging. The same logic now extends to e-commerce secondary packaging, where brands want one cartonboard format that can move from shelf display to last-mile shipment with minimal redesign and a clearer sustainability claim.

Pharmaceutical Serialization And Tamper-Evident Cartons

Ongoing enforcement of the EU Falsified Medicines Directive continues to support demand for specialized folding cartons with 2D data matrix codes, Braille text, and tamper-evident features in the Europe cartonboard market. Those requirements push converters toward tighter tolerances and higher-specification board grades than standard food cartons usually need, which raises the technical threshold for participation. The compliance burden also narrows the pool of qualified suppliers because validation, print accuracy, and line integration matter as much as basic board supply. This keeps pharmaceutical packaging demand steadier than many consumer-facing applications because medicine packaging standards do not soften when retail demand becomes uneven. The result is a part of the Europe cartonboard market where revenue tends to rise faster than tonnage, since each added compliance feature lifts board and converting value per square meter.

Premium Beauty And Personal Care Carton Upgrading

Beauty and personal care brands across Western Europe continue to replace plastic inner structures, windows, and inserts with cartonboard formats that are easier to align with recyclability claims and retailer sustainability expectations. Stora Enso’s September 2025 launch of Ensovelvet, a premium uncoated SBS board developed for luxury cosmetics and perfume packaging, showed that producers are creating purpose-built grades rather than adapting commodity output for premium work.[4]Stora Enso Oyj, “Stora Enso Introduces Ensovelvet, a New, Premium Uncoated Paperboard for Luxury Packaging,” Cision News, news.cision.com The European Carton Excellence Award 2025 winners included Van Genechten Packaging’s Rituals Cosmetics gift set, which used Stora Enso board and demonstrated that premium carton solutions are already viable in gift and travel formats that once relied more heavily on plastic components. Premium finishes still matter in this category because tactile quality, print performance, and shelf appearance influence brand positioning as much as recyclability does. Pro Carton’s 2026 survey found that 77% of Italian consumers felt more positive toward brands using eco-friendly packaging materials, which helps explain why beauty-focused supply chains are directing more upgrade activity toward Italy-facing demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Pulp Cost Volatility, Especially In Recycled Grades | -0.7% | Pan-European, most acute in France, Italy, and the Netherlands | Short term (≤ 2 years) |

| Reuse And Packaging-Minimization Rules Capping Unit Growth | -0.4% | EU-27 wide, effective August 2026 | Short term (≤ 2 years) |

| Compliance Data Burden For Small And Mid-Sized Converters | -0.3% | EU-wide, most acute in Southern Europe | Medium term (2-4 years) |

| Lightweighting Reducing Tonnes Faster Than Unit Demand | -0.3% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy And Pulp Cost Volatility, Especially In Recycled Grades

Energy and fiber costs remained the most immediate operating challenge for producers in 2026, and the European cartonboard market felt that pressure most sharply in grades with less protection from integrated fiber and energy systems. Billerud stated in its Q4 2025 results that overcapacity in cartonboard and white top kraftliner in Region Europe kept demand subdued and price pressure visible into Q1 2026, limiting mills’ ability to recover higher input costs through pricing. That combination of loose supply and volatile utilities is especially difficult for recycled-board producers because they have less margin room when market conditions turn unstable. It also changes converter purchasing behavior, with buyers placing more value on contract stability and supply consistency when spot pricing becomes harder to read. Until capacity utilization improves more clearly, margin recovery in the European cartonboard market is likely to remain uneven across grades and producer types.

Reuse And Packaging-Minimization Rules Capping Unit Growth

PPWR will start applying from August 12, 2026, and its reuse provisions and empty-space minimization rules will limit unit growth in some packaging formats even while fiber substitution supports demand. That means the Europe cartonboard market can gain material share in packaging choices without seeing the same rate of growth in carton counts per shipment. The rule set reduces room for unnecessary grouped and secondary packaging, which is positive for compliance outcomes but less supportive for pure unit-volume expansion. Small and mid-sized converters face the heaviest adjustment because digital product passports, EPR reporting, and packaging-data management require system spending that larger groups can spread across broader revenue bases. The likely result is faster consolidation among converters that cannot absorb the full compliance burden on their own.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Anchors Volume While Liquid Packaging Board Leads Growth

Folding boxboard held 33.91% of the European cartonboard market share in 2025, making it the largest product grade because it can serve food, pharmaceutical, and cosmetics applications through a single broad converting base. Its leading position also reflects its compatibility with offset, digital, and flexographic printing, enabling the grade to move from everyday grocery packaging into higher-value retail presentation formats with minimal friction. That scale is supported by established converter infrastructure and by shelf-ready retail specifications that already favor folding boxboard across much of the region. Stora Enso’s EUR 1 billion (USD 1.08 billion) Oulu line in Finland added 750,000 tonnes of annual capacity, and Metsä Board’s EUR 210 million (USD 227 million) Husum expansion added 200,000 tonnes annually, which has weighed on near-term price recovery while new supply is still being absorbed. Solid bleached board continues to occupy the premium tier in food service, pharmaceutical packaging, and luxury beauty work, while solid unbleached board remains more niche in industrial and heavy-duty uses, and food service board is moving through PFAS-free reformulation ahead of the August 2026 compliance date.

Liquid packaging board is projected to expand at a 5.17% CAGR from 2026 to 2031, making it the fastest-growing product grade in the European cartonboard market. Tetra Pak and Sterilgarda Alimenti launched a 1-liter aseptic carton with a paper-based barrier in April 2026, providing the first commercial industrial-scale proof point for aluminum-free carton technology. Tetra Pak also committed EUR 60 million (USD 65 million) to a paper-based barrier pilot plant in Lund, Sweden, as part of its plan to invest EUR 100 million (USD 109 million) annually through 2030 in sustainable packaging development, underscoring how quickly the liquid carton technology frontier is advancing. Producers are also upgrading core liquid board assets to improve efficiency, quality control, and product flexibility as demand shifts toward more paper-intensive beverage formats. White-lined chipboard still serves price-sensitive secondary packaging, but its relative position is weaker when energy costs and cost visibility become less stable across the European cartonboard market.

By Packaging Format: Folding Cartons Lead While Liquid Packaging Formats Gain Momentum

Folding cartons accounted for 55.41% share of the Europe cartonboard market size in 2025, and this format remained the structural center of demand across food retail, pharmaceutical distribution, and personal care. Their dominance comes from both breadth and value density, because the same folding carton can range from a simple grocery pack to a premium presentation format with embossing, hot stamping, soft-touch coatings, or digital short-run graphics. This keeps revenue share ahead of physical tonnage share in many premium applications, especially when shelf impact and compliance printing need to coexist in a single pack. Van Genechten Packaging’s award-winning work for Rituals Cosmetics at the European Carton Excellence Awards 2025 used Stora Enso board to remove virgin plastic while preserving recyclability and premium finish quality. Cups and food-service containers are also moving toward SBS-based solutions with water-based barriers as converters prepare for the August 2026 regulatory environment.

Liquid packaging formats are projected to expand at a 5.43% CAGR through 2031, the strongest pace among packaging formats in the European cartonboard market. SIG Group stated that its aluminum-layer-free aseptic cartons recorded 24% sales growth in 2025, which shows that paper-intensive liquid formats are gaining commercial traction rather than remaining only a development project. Elopak’s Q1 2026 results showed continued organic revenue growth across Europe and the Americas, and the company is targeting 4-6% annual organic revenue growth as it extends carton simplification work across its portfolio. Sleeve and tray formats remain smaller in share, but retailers are adopting them more widely when a single paper-based format can function as both shelf-ready presentation and secondary packaging. That dual function matters because it improves handling efficiency while also supporting the broader shift toward recyclable fiber-based pack formats in the European cartonboard market.

By End-User Industry: Food Holds The Structural Lead While Pharmaceutical And Healthcare Gains Pace

Food accounted for 37.65% of revenue in 2025, making it the largest end-user segment in the European cartonboard market and anchoring demand across ambient, chilled, frozen, and food-service packaging. Its importance lies in the breadth of formats it uses, as food applications draw on folding boxboard, solid bleached board, food service board, and recycled grades across both primary and secondary packs. Beverage demand sits close to this segment because liquid packaging board growth is tied to dairy, juice, plant-based drinks, and other fresh-fill categories that are replacing more plastic-heavy formats. This broad food footprint gives the European cartonboard industry a stable demand base, even as higher-value consumer categories move unevenly through the business cycle. Tobacco remains a smaller but still premium application for outer cases and inner frames, and its gradual unit decline is partly offset by the continued need for higher-specification board in travel retail and limited-edition packs.

Pharmaceutical and healthcare packaging is projected to grow at a 5.34% CAGR through 2031, making it the fastest-expanding end-user segment in the European cartonboard market. Commission Delegated Regulation (EU) 2016/161 keeps demand centered on compliance features such as Braille embossing, 2D data matrix codes, and tamper-evident closures, all of which raise board and converting requirements. Because those features add production steps and validation needs, pharmaceutical carton revenue tends to rise faster than pharmaceutical carton tonnage. Cosmetics and toiletries remain the highest-margin outlet for premium board grades, and producers are responding with launches such as Ensovelvet and with award-winning beauty packs that bring tactile finish and recyclability together in one format. That mix of regulated healthcare demand and premium beauty work keeps the European cartonboard market more value-driven than volume-driven across much of its end-use structure.

Geography Analysis

Germany accounted for 24.18% of Europe's cartonboard market share in 2025, which made it the largest national market in the region. That position rests on a combination of a dense FMCG production base, strong pharmaceutical demand, and a mature retail-ready packaging infrastructure that supports both high-volume and specification-heavy work. The United Kingdom and France form the next tier of demand for different reasons. The United Kingdom favors premium food and personal care cartons, while France remains closely tied to beauty and fragrance packaging. Italy also carries strategic weight in the European cartonboard market because its food, beauty, and pharmaceutical packaging base aligns with strong consumer support for eco-friendly packs, and Pro Carton’s 2026 survey found that 77% of Italian consumers felt more positive toward brands using sustainable packaging materials.

Spain is projected to expand at a 5.12% CAGR from 2026 to 2031, making it the fastest-growing national market in the Europe cartonboard market. Its growth profile reflects stronger e-commerce activity, export-oriented food packaging demand, and an improving pharmaceutical manufacturing base that is lifting demand for functional and compliant carton formats. The rest of Europe, including Poland, the Netherlands, Belgium, the Nordic countries, and Central and Eastern Europe, is taking a larger role as food and pharmaceutical production spreads toward lower-cost manufacturing locations. Poland is emerging as an attractive converter location because Western European brand owners want shorter lead times and simpler regional compliance management. Nordic countries remain dominated by integrated producers, but specialty coated grades and premium folding boxboard continue to shape cross-border trade flows within the region.

A major regional divide is emerging between Nordic integrated mills and Continental mills because energy exposure differs across the two supply bases. Mills in Scandinavia benefit more from biomass cogeneration and lower dependence on external grid electricity, which protects virgin-fiber grades when energy markets become unstable. That shifts relative economics in favor of Scandinavian folding boxboard, while energy-exposed Continental production faces more pressure in recycled grades. The result is that more converters are leaning toward longer-term supply agreements with Nordic producers, trading some logistical flexibility for better cost visibility in the European cartonboard market.

Competitive Landscape

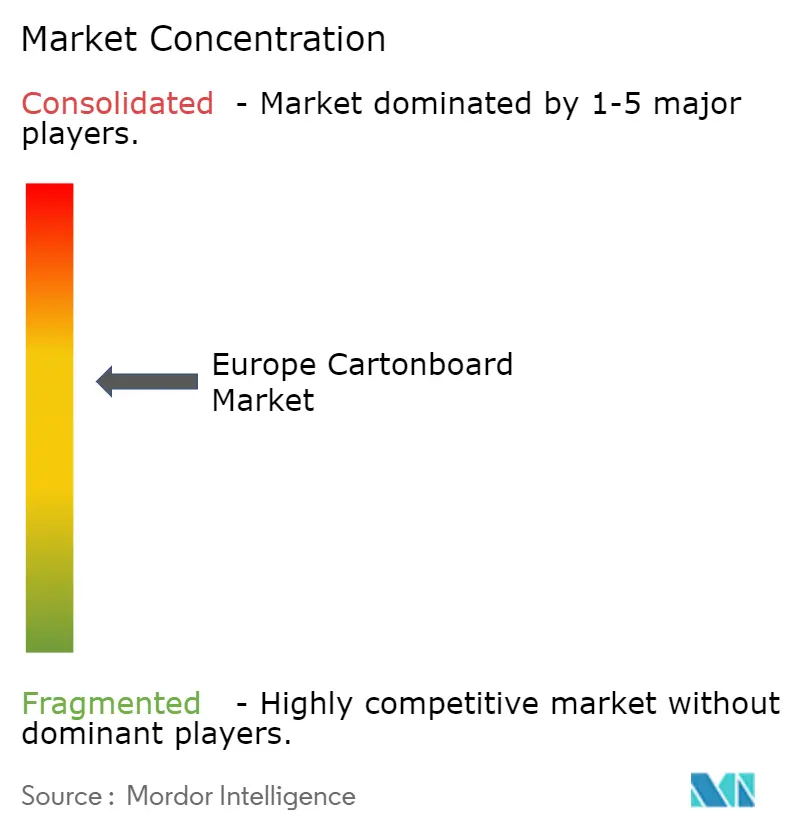

The Europe cartonboard market has a moderately concentrated structure at the board-producer level, with Metsä Board, Stora Enso, and Mayr-Melnhof Karton AG holding leading positions across integrated mill networks in Scandinavia, Finland, and Central Europe. Their advantage is rooted in integration depth, because control over fiber sourcing, energy generation, board production, and, in some cases, converting gives them more protection when input costs swing, and supply conditions tighten. Mayr-Melnhof expanded MCM SMART GD2-grade recycled cartonboard production to a third European mill in Austria, alongside sites in Germany and Slovenia, thereby strengthening supply redundancy and shortening delivery distances for customers across Central Europe. Metsä Board’s March 2026 Lead the Pack strategy for 2026-2030 shifted the company’s emphasis from heavy investment to profitability improvement, following roughly EUR 1 billion (USD 1.08 billion) in capacity and competitiveness spending over 5 years. Billerud stated in its Q4 2025 results that overcapacity in cartonboard and white top kraftliner in Region Europe kept demand and pricing under pressure into Q1 2026, which shows why pricing discipline is still reforming across the Europe cartonboard market.

Competition is also moving beyond raw board volume, as large suppliers use design software, service tools, and packaging-system support to deepen customer relationships and increase switching costs. Smurfit Westrock’s 2026 Innovation Event in the Netherlands introduced 3 AI-based packaging design tools and ActiBlu, a glueline-free paper-based packaging prototype, which underlined how digital development and structural redesign are becoming commercial differentiators. Premium specialty positions remain important, where pharmaceutical accuracy and luxury presentation leave little room for board defects or caliper variation, thereby protecting the role of high-specification suppliers in select niches. RDM Group strengthened its position in recycled board through the Fiskeby Board acquisition, giving it a broader platform in a part of the European cartonboard market where independent scale still matters.

Converters still compete intensely on print quality, lead time, embellishment capability, and sustainability credentials, which keeps the downstream market more fragmented than the upstream mill base. Van Genechten Packaging’s 2025 award-winning Rituals Cosmetics pack showed how converters can win business by combining recyclability with premium execution rather than competing only on price. The same dynamic supports short-run pharmaceutical and beauty work, where digital and UV offset printing capability can matter more than mill scale alone for customer retention. This leaves the European cartonboard market in a position where large integrated producers set the tone on capacity and cost, while specialized converters protect margins through execution, speed, and customer-specific design work.

Europe Cartonboard Industry Leaders

Metsa Board Corporation

Stora Enso Oyj

Mayr-Melnhof Karton AG

Billerud Aktiebolag

Sappi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Tetra Pak and Italian dairy company Sterilgarda Alimenti unveiled the industry's first 1-litre aseptic carton with a paper-based barrier, commercially validating aluminum-free carton technology at full industrial scale. The launch was accompanied by Tetra Pak's EUR 60 million (USD 65 million) investment in a paper-based barrier pilot plant in Lund, Sweden, part of the company's commitment to invest approximately EUR 100 million (USD 109 million) annually through 2030 in sustainable packaging development.

- March 2026: Metsä Board reported comparable EBITDA of EUR 17 million (USD 19 million) for Q1 2026, citing early results from the transformation program launched in mid-2025 as its "Lead the Pack" strategy for 2026-2030 entered its first implementation phase.

- November 2025: Mondi launched an extended food packaging portfolio incorporating solid board solutions and digital printing capabilities following the integration of Schumacher Packaging, strengthening its European solid-board footprint and adding regional supply reliability for food-industry customers across Central and Western Europe.

- October 2025: Elopak announced the addition of a third production line at its Arkansas plant in the United States, bringing total plant investment to USD 128 million. Concurrently, Elopak invested in Blue Ocean Closures AB, a Swedish company developing fiber-based closures, to extend material simplification from the carton body to the cap.

Europe Cartonboard Market Report Scope

The Europe Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Europe Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe cartonboard market size in 2026 and where is it expected to reach by 2031?

The Europe cartonboard market entered 2026 at USD 13.63 billion and is forecast to reach USD 16.42 billion by 2031, growing at a 3.79% CAGR.

What is driving cartonboard demand across Europe?

The main drivers are plastic-to-fiber substitution under PPWR, recyclable shelf-ready packaging in food retail, pharmaceutical serialization needs, and premium beauty packaging upgrades.

Which product grade is growing the fastest in Europe cartonboard?

Liquid packaging board is the fastest-growing product grade, with a projected 5.17% CAGR through 2031, supported by paper-based barrier innovation in aseptic cartons.

Which packaging format still leads demand in Europe?

Folding cartons remained the leading format with 55.41% of market value in 2025 because they serve food, pharmaceutical, and personal care applications at scale.

Which country leads regional demand and which one is expanding the fastest?

Germany led with a 24.18% share in 2025, while Spain is forecast to record the fastest growth at a 5.12% CAGR through 2031.

Why is pharmaceutical packaging becoming more important for cartonboard suppliers?

Pharmaceutical and healthcare packaging is projected to grow at 5.34% CAGR through 2031 because serialization, Braille, and tamper-evident features raise both board specifications and converting value.

Page last updated on: