South America Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

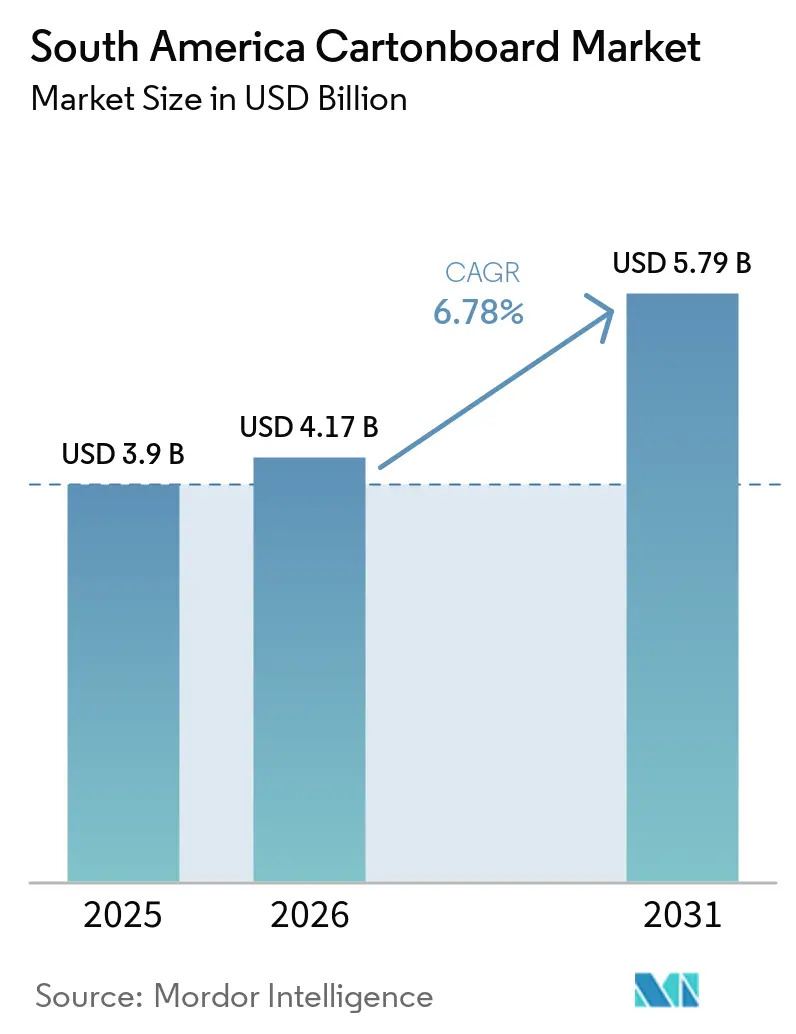

| Base Year Market Size (2025) | USD 3.9 Billion |

| Market Size (2026) | USD 4.17 Billion |

| Market Size (2031) | USD 5.79 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

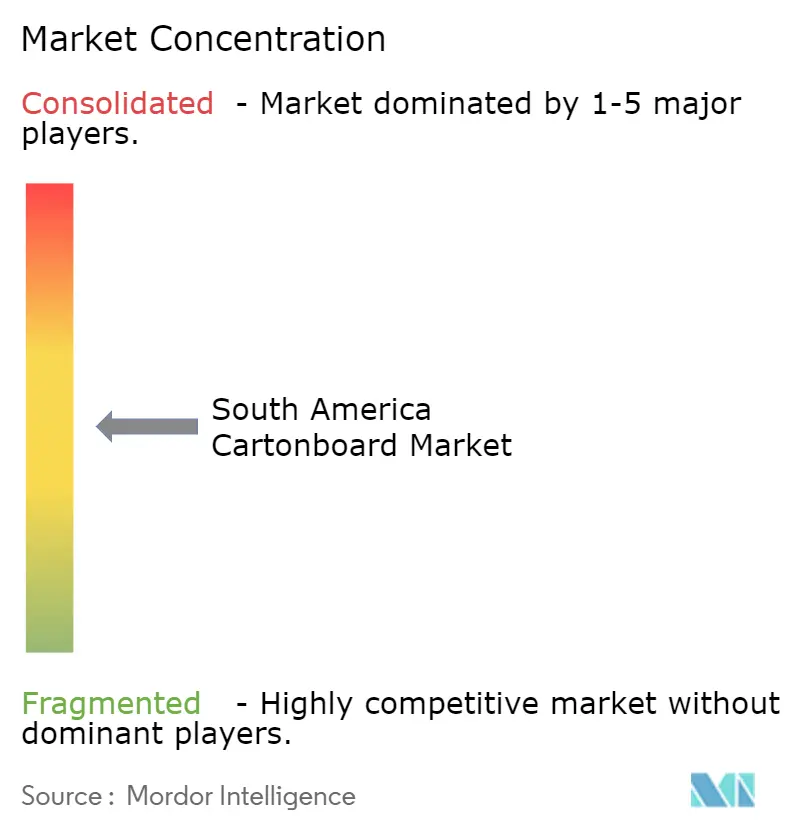

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Cartonboard Market Analysis by Mordor Intelligence

The South America Cartonboard Market size is expected to grow from USD 3.9 billion in 2025 to USD 4.17 billion in 2026 and is forecast to reach USD 5.79 billion by 2031 at 6.78% CAGR over 2026-2031.

This expansion reflects the combined effect of tighter rules on single-use plastics, wider consumption of processed food and beverages, and a regional fiber cost advantage supported by large eucalyptus plantation resources. Brazil's reverse logistics framework for plastic packaging and related recycled-content obligations are raising the compliance burden on plastic formats, while paper and cardboard packaging remains outside those duties. Digital printing and PFAS-free aqueous barrier coatings are also moving cartonboard into food, foodservice, and personal care uses that previously depended on coated plastic structures. The South America cartonboard market is increasingly split between a premium tier led by bleached grades for pharmaceutical and beauty packs and a commodity tier where standard grades face sharper price competition. This keeps the strongest opportunity in higher-specification cartons, premium import substitution, and converter models built around design speed, print quality, and regulatory fit.

Key Report Takeaways

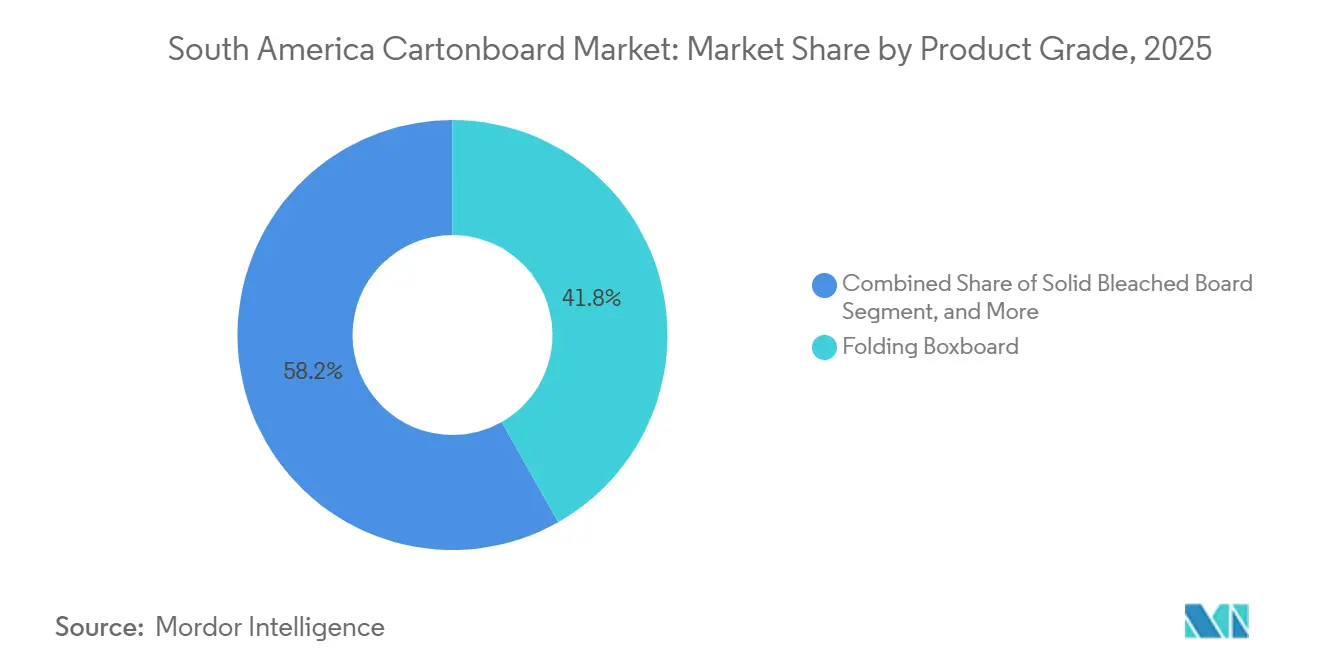

- By product grade, folding boxboard held 41.81% share in 2025, while solid bleached board is forecast to expand at 8.09% CAGR through 2031.

- By packaging format, folding cartons held 51.23% share in 2025, while liquid packaging is projected to grow at 5.90% CAGR through 2031.

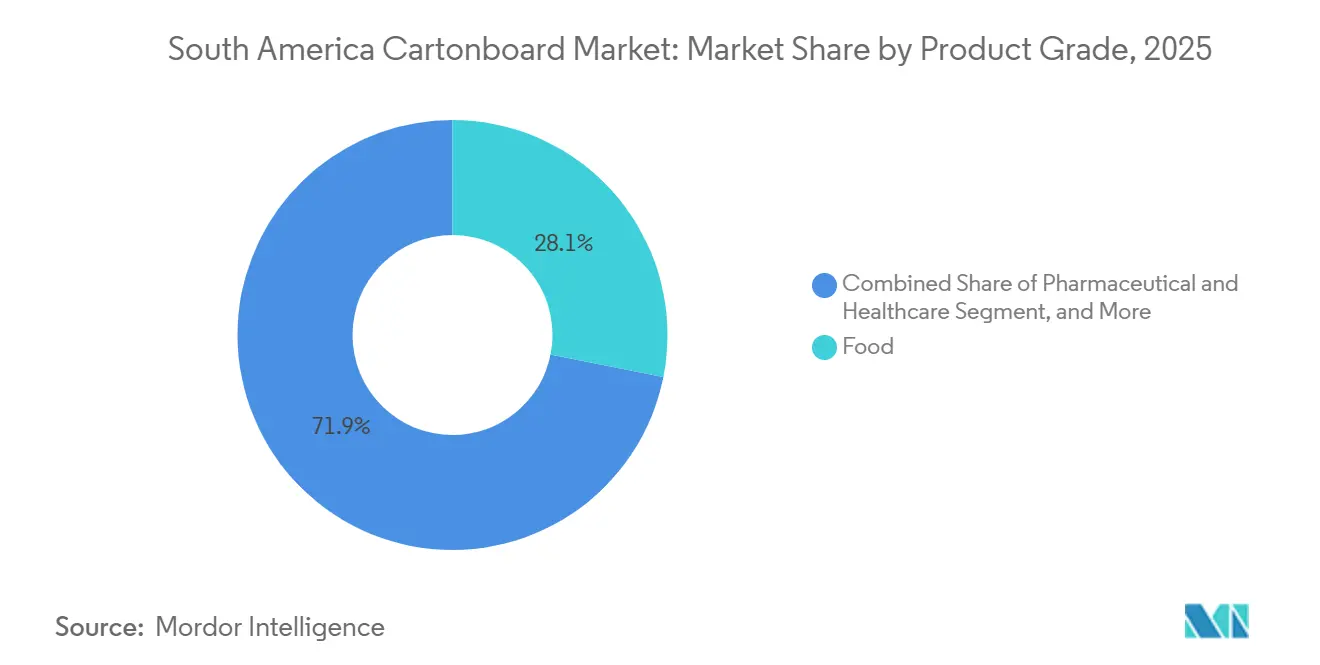

- By end-user industry, food accounted for 30.32% share in 2025, while cosmetics and toiletries is forecast to advance at 7.12% CAGR through 2031.

- By geography, Brazil held 47.43% of the South America cartonboard market in 2025, while Peru is projected to expand at 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic Substitution Mandates And Brand Sustainability Targets | +2.1% | Brazil, Colombia, Chile, with spill-over into Peru and Argentina | Long term (≥ 4 years) |

| Packaged Food Demand And Retail Modernization | +1.7% | Brazil, Argentina, Colombia, especially major urban centers and secondary cities | Medium term (2-4 years) |

| Beverage And Dairy Carton Demand In Aseptic And Chilled Formats | +1.3% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Pharmaceutical And Healthcare Packaging Demand With Traceability And Hygiene Needs | +0.8% | Brazil, Colombia, Chile, Peru | Long term (≥ 4 years) |

| PFAS-Free And High-Barrier Board Innovation Unlocking Foodservice Conversion | +0.4% | Global supply push, with adoption centered in Brazil and Chile | Long term (≥ 4 years) |

| Premiumization And Anti-Counterfeit Print Demand In Beauty, Healthcare, And Tobacco Cartons | +0.3% | Brazil, Colombia, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic Substitution Mandates And Brand Sustainability Targets

Regulation has moved plastic substitution from a voluntary brand agenda into a compliance issue across the South America cartonboard market. Brazil's Decree 12,688 created a national reverse logistics system for plastic packaging, required a 32% plastic recycling rate in 2026, set a path to 50% by 2040, and imposed a minimum 22% recycled-content obligation in new plastic packaging from 2026 for larger companies, while paper and cardboard packaging remained explicitly exempt. Colombia's Law 2232, Resolution 1407, Chile's Ley 21.368, and Peru's draft recyclable and biodegradable tableware regulation widened the policy gap between fiber-based formats and harder-to-comply plastic items. That shift is pushing brand owners to redesign broader SKU portfolios rather than only the units directly covered by regulation, because regional packaging systems and procurement standards are increasingly managed at portfolio level. It also supports stronger carton adoption in foodservice, healthcare-adjacent secondary packaging, and selected beauty lines where recyclability claims now matter alongside brand presentation. For the South America cartonboard market, this creates a policy-backed demand floor that is less exposed to short consumer slowdowns than many other packaging materials.

Packaged Food Demand And Retail Modernization

Processed food demand and the steady spread of modern retail formats continue to give the South America cartonboard market a reliable volume base. Empapel reported 756,000 tonnes of paperboard production in 2025, and food packaging remained the single largest end-use area within that output mix. The same source showed that January 2026 carton shipments reached a record 347,000 tonnes, which signaled firm order flow at the start of the forecast period. ABRE also reported that Brazil's overall packaging production volume slipped 0.3% in 2025, yet food and hygiene packaging volumes remained broadly stable, which confirmed cartonboard's defensive role in essential-goods packaging. Outside Brazil, retail formalization in Peru, Colombia, and Chile is encouraging branded suppliers to move from simpler flexible formats toward printed cartons that improve shelf presence and support clearer brand differentiation. This mix keeps the South America cartonboard market tied to staple consumption while still leaving room for higher-value graphics, convenience formats, and stronger converter margins in better specified applications.

Beverage And Dairy Carton Demand In Aseptic And Chilled Formats

Beverage and dairy packaging remains the most capital-intensive growth path in the South America cartonboard market because it depends on filling systems, customer qualification, and specialized liquid board. SIG reported that its Americas revenue grew 3.0% at constant currency in 2025, with new filling line installations in Brazil serving both existing and new customers across dairy and ambient beverage categories. The same company stated that customer ramp-up in Colombia and higher dairy and beverage volumes in Chile supported broader carton growth across its packaging activities. In April 2026, Tetra Pak and Sterilgarda Alimenti launched the first 1-liter aseptic carton with a paper-based barrier, a structure that lifts traceable renewable content to 80% and up to 92% when paired with plant-based polymers. Tetra Pak backed that shift with a EUR 60 million investment in a dedicated paper-based barrier pilot plant, which points to a longer change in technical specifications rather than a one-off launch. As those systems spread, the South America cartonboard market is likely to demand more recyclable liquid board structures with lower reliance on conventional multilayer inputs.

Pharmaceutical And Healthcare Packaging Demand With Traceability And Hygiene Needs

Healthcare packaging gives the South America cartonboard market a steadier premium outlet than many consumer-led applications. Folding boxboard remains central to pharmaceutical outer cartons and blister-card packaging, where tamper evidence, traceability, and barrier performance shape board selection and print requirements. The February 2025 MERCOSUR packaging documentation update introduced revised traceability and post-consumer recycled-content documentation requirements for pharmaceutical-grade food-contact and packaging materials. Those tighter documentation needs raise specification complexity and favor suppliers that can deliver consistent board quality, clean converting performance, and reliable print surfaces across serialized or regulated packs. Premium beauty and healthcare packs also share a need for higher surface whiteness and stronger anti-counterfeit presentation, which pulls demand toward better bleached grades rather than lower-cost standard substrates. In the South America cartonboard market, that leaves solid bleached board and premium folding boxboard better insulated than commodity grades when regulation and traceability carry more weight in buying decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virgin Pulp And Recovered Fiber Cost Volatility | -1.8% | South America-wide, with Brazil most exposed through domestic production economics and import pricing | Short term (≤ 2 years) |

| Competition From Flexible Plastic And Lightweight Alternative Formats | -0.9% | Brazil, Argentina, Colombia, especially commodity food packaging | Medium term (2-4 years) |

| Incomplete Collection And Recycling Economics For Multilayer Liquid Cartons | -0.5% | Brazil, with spill-over into Argentina and Colombia | Medium term (2-4 years) |

| Food-Contact Compliance And Barrier-Performance Trade-Offs In Sensitive Uses | -0.3% | Brazil and the wider MERCOSUR standards framework | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Virgin Pulp And Recovered Fiber Cost Volatility

Input cost volatility remains the most immediate margin threat for producers and converters in the South America cartonboard market. The pressure does not come only from virgin pulp pricing, because exchange-rate swings also change the local-currency cost of imported board, chemicals, and specialty inputs that many converters still need. Recovered fiber adds a second layer of uncertainty because collection quality and availability move with consumption patterns and with the speed at which informal recovery systems become more organized. Billerud described prices as challenged in its first-quarter 2026 interim report even while it continued to fund board upgrades, which shows how supply-side confidence can coexist with tight near-term pricing conditions. Mayr-Melnhof likewise kept its 2026 focus on fixed-cost reduction, process harmonization, and structural adjustments, which reflected the need for discipline in a market where costs can move faster than selling prices. When those cost swings meet aggressive imported offers, local mills lose pricing power and converters face narrower pass-through windows.

Competition From Flexible Plastic And Lightweight Alternative Formats

Flexible plastic remains the clearest substitute threat to the South America cartonboard market, especially in lower-value food packs where buyers focus first on unit economics. The risk is highest in dry food, single-serve, condiment, and selected personal care applications where thin-film or pouch formats can reduce pack weight and transport cost. This pressure is not uniform, because regulatory tightening in Brazil, Colombia, and Chile keeps fiber formats more attractive for many branded SKUs that need better recyclability or cleaner sustainability messaging. Even so, lightweight mono-material pouch systems are narrowing the sustainability gap that once favored cartonboard more clearly in several categories. That is forcing converters to compete with barrier performance, print quality, and short-run customization rather than with fiber content alone. For the South America cartonboard market, the result is continued growth in higher-value niches and more pressure on commodity folding carton applications where substitution is easier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Anchors Volume While Bleached Grades Gain Value

Folding boxboard held 41.81% of the South America cartonboard market share in 2025, while the South America cartonboard market size for solid bleached board is projected to expand at 8.09% CAGR from 2026 to 2031. Folding boxboard remained the core volume grade because it balanced printability, stiffness, and cost across food, pharmaceutical outer-carton, and personal care packaging. Its position was also reinforced by the availability of locally produced grades from integrated Brazilian mills, which helped buyers manage lead time and working-capital needs more effectively than fully import-dependent sourcing models. Solid bleached board is rising faster because pharmaceutical and cosmetics packs increasingly require higher whiteness, cleaner print reproduction, and better compatibility with holographic, embossed, and anti-counterfeit finishing. Billerud's Evolution Program is allocating SEK 1.4 billion (USD 128.8 million) across 2024-2027 to upgrade its Quinnesec and Escanaba mills for solid bleached board production, which shows that global suppliers expect durable SBS demand in South America.

White-lined chipboard continues to serve cost-sensitive secondary packaging in food and beverage, especially where recycled fiber economics support a lower-cost grade mix. Solid unbleached board remains relevant in industrial and bulk uses that need structural strength more than premium graphics or bright white surfaces. Liquid packaging board and food service board sit at the most specialized end of the South America cartonboard industry because they depend on barrier chemistry, hygiene compliance, and converter process control rather than only board availability. Compliance needs in pharmaceutical and premium food packs are also raising the bar for traceability and print performance, which supports gradual value migration toward better specified bleached and premium folding grades. Mayr-Melnhof's Fit-For-Future program, which remained ahead of schedule in early 2026, suggests that European suppliers will keep targeting export competitiveness in recycled cartonboard grades that feed the region's mid-tier applications.

By Packaging Format: Folding Cartons Lead While Liquid Packaging Builds Scale

Folding cartons held 51.23% share of the South America cartonboard market in 2025, while the South America cartonboard market size for liquid packaging is projected to advance at 5.90% CAGR through 2031. Their lead reflects entrenched use across dry food, pharmaceuticals, personal care, and tobacco, where carton converting lines and retail presentation are already well established. Folding cartons also benefit from the ability to support product versioning, sharper print work, and faster regional replenishment than formats that depend more heavily on imported finished packs. That combination keeps them central to the South America cartonboard market even as competition intensifies in lower-specification boxes. Liquid packaging is scaling faster because aseptic and gable-top systems continue to expand in Brazil, Colombia, and Chile, widening demand for technically advanced board structures.

SIG's 2025 performance showed new line installations in Brazil and customer ramp-up in Colombia, which indicates that liquid carton adoption is moving beyond Brazil's traditional base. Sleeves and trays are also gaining ground as organized retail and cold-chain distribution deepen in Peru, Colombia, and Chile. Cups and foodservice containers are becoming more attractive as PFAS-free barrier systems reduce dependence on PE lamination in several end uses. Michelman's Nuvita Life coatings and the BASF-UPM Joncryl HPB collaboration both lowered the technical barrier for recyclable fiber packs in demanding foodservice uses during 2026. This broadens the downstream opportunity set for the South America cartonboard industry because more converters can enter premium foodservice and fresh-food applications without relying on older lamination routes.

By End-User Industry: Food Holds The Base While Cosmetics And Toiletries Expands Faster

Food accounted for 30.32% of the South America cartonboard market size in 2025, while cosmetics and toiletries is projected to advance at 7.12% CAGR from 2026 to 2031. Food stayed largest because dry food, frozen, confectionery, and meal-kit uses give cartonboard a steady base linked to everyday consumption rather than purely discretionary spending. ABRE reported that food and hygiene packaging volumes stayed broadly stable in 2025 even as Brazil's overall packaging output edged down, which reinforces the defensive role of essential-goods packaging. Cosmetics and toiletries is rising faster because urban premiumization rewards soft-touch cartons, molded-pulp inserts, and higher-end print finishes that help brands protect both image and sustainability claims. Those attributes make beauty packaging one of the clearest value pools within the South America cartonboard market.

Beverage remains the second-largest end-user because aseptic and chilled dairy packs continue to absorb new filling-line capacity across the region. Pharmaceutical and healthcare packaging provides a stable premium outlet for folding boxboard and solid bleached board because tamper evidence, traceability, and hygiene standards keep specification discipline high. Tobacco cartons still face long-term volume pressure, yet the category preserves value through anti-counterfeit printing and premium structural formats that limit down-trading. Other end-user industries, including toy, apparel, automotive, household, electrical, and foodservice, create a broad demand tail that matters most in large manufacturing clusters. Together these patterns keep the South America cartonboard market exposed to staples for volume and to beauty, beverage, and healthcare for value growth.

Geography Analysis

Brazil accounted for 47.43% of the South America cartonboard market share in 2025. Its lead comes from a large FMCG base, integrated pulp-to-converting capacity, and national policy that increasingly favors fiber packaging over harder-to-comply plastic formats. Empapel reported 756,000 tonnes of paperboard production in 2025, with food packaging remaining the largest end use within the country's paper packaging mix. January 2026 carton shipments reached 347,000 tonnes, which showed that demand entered the forecast period with firmer momentum than the prior year. Brazil also retains a structural fiber advantage through its eucalyptus plantation base, which helps the South America cartonboard market keep a strong regional production center even when import pressure rises.

Argentina, Colombia, and Chile form the next demand tier, but each follows a different path. Argentina keeps a baseline need for dairy and pharmaceutical cartons even when currency conditions weigh on broader purchasing. Colombia benefits from packaging demand concentrated in its main urban centers and from pharmaceutical supply links into nearby Andean markets. Chile pairs dairy and beverage growth with stronger recycling habits that support fiber-based packaging, and SIG reported carton growth from customer ramp-up in Colombia and expanding beverage and dairy volumes in Chile and Argentina during 2025.

Peru is the fastest-growing geography in the South America cartonboard market, with a projected 6.32% CAGR from 2026 to 2031. Modern retail expansion is widening shelf space for branded products, which raises the need for printed folding cartons and shelf-ready packaging. Peru's agroexport cycle, centered on blueberries, avocados, grapes, and asparagus, also supports demand for cold-chain compatible fiber formats. ACCCSA reported that Peru's containerboard demand grew 11.6% in 2025, which signals a broader packaging investment cycle that supports future cartonboard consumption. The rest of South America remains smaller in scale, but it adds incremental growth as retail formalization, cross-border packaged food trade, and fiber-based packaging adoption continue to spread.

Competitive Landscape

The South America cartonboard market has a mixed structure in which a limited set of integrated global suppliers sits above a wider field of local and regional converters. Smurfit Westrock is the clearest pan-regional integrated operator, and its position is strengthened by mill access, converting reach, and customer coverage across multiple packaging formats. The company's South America-related regional operations reported an adjusted EBITDA margin of 20% in Q1 2026, which showed how vertical integration can protect profitability better than standalone converting models in a volatile price environment. Graphic Packaging adds a technology-centered competitive layer through barrier-coated paperboard formats, machinery capability, and a portfolio of more than 1,100 patents cited in its first-quarter 2026 results. European board mills, including Stora Enso, Mayr-Melnhof, Billerud, and Metsä Board, remain important suppliers of premium folding boxboard and solid bleached board into the region.

One strategic gap remains domestically produced solid bleached board, because the region still relies heavily on imported SBS for pharmaceutical and beauty applications. That gap matters because local production would pair shorter freight routes with South America's eucalyptus fiber advantage and with a policy backdrop that favors fiber-based packaging in several countries. Billerud's SEK 1.4 billion (USD 128.8 million) Evolution Program and Stora Enso's EUR 1.1 billion (USD 1.19 billion) Oulu consumer board line show that global suppliers are still adding or upgrading premium grade capacity relevant to South American demand. Mayr-Melnhof's Fit-For-Future program, which remained ahead of schedule in early 2026, also points to continued cost and export discipline from European producers selling recycled cartonboard grades.

Competition is also changing at the converter level because barrier-coating innovation is lowering the entry threshold for higher-value foodservice and fresh-food packs. Michelman introduced 100% bio-based dry-film PFAS-free coatings in April 2026, and BASF with UPM followed in May 2026 with recyclable high-performance barrier systems for food-contact uses. Tetra Pak and SIG continue to shape the aseptic end of the South America cartonboard market because filling-line ecosystems, board specifications, and customer qualification remain tightly linked in liquid packaging. This leaves the market with a premium layer led by technology, surface quality, and regulatory fit, and a broader volume layer where service, speed, and cost discipline matter more.

South America Cartonboard Industry Leaders

Klabin S.A.

Smurfit Westrock plc

Tetra Pak International S.A.

Suzano S.A.

Empresas CMPC S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UPM Specialty Materials and BASF announced a strategic collaboration combining UPM's barrier and barrier-base papers with BASF's Joncryl HPB high-performance barrier technology resins, enabling high-performance, recyclable fiber-based packaging that meets demanding food-contact regulatory requirements; the development directly supports PFAS-free conversion of cartonboard in foodservice and fresh-food applications relevant to South America's export-oriented food sector.

- April 2026: Tetra Pak and Italian dairy company Sterilgarda Alimenti launched the first 1-litre aseptic carton with a paper-based barrier, achieving up to 92% traceable renewable content when combined with plant-based polymers and reducing the carbon footprint by up to 43%; the innovation is backed by Tetra Pak's EUR 60 million (USD 64.8 million) pilot-plant investment in Lund, Sweden, and is expected to progressively reset liquid packaging board specifications across South America's dairy and beverage sectors.

- April 2026: Michelman introduced the Nuvita Life 4002 and Nuvita Life 4605 bio-based, PFAS-free barrier coatings for fiber-based food packaging; both coatings are 100% bio-based in dry film, SUPD-compliant, and aligned with the EU Packaging and Packaging Waste Regulation, enabling recyclable cartonboard formats for brands serving South America's export-facing food and personal care markets.

- January 2026: Billerud commenced SEK 400 million (USD 36.8 million) investments in 2026 to upgrade its Quinnesec and Escanaba mills for solid bleached board production as part of the company's SEK 1.4 billion (USD 128.8 million) Evolution Program spanning 2024-2027.

South America Cartonboard Market Report Scope

The South America Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The South America Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America cartonboard market in 2026, and what is the 2031 outlook?

The South America cartonboard market stands at USD 4.17 billion in 2026 and is expected to reach USD 5.79 billion by 2031, growing at a 6.78% CAGR.

Which product grade leads current demand in South America cartonboard?

Folding boxboard leads demand with a 41.81% share in 2025 because it balances printability, rigidity, and cost across food, pharma, and personal care packaging.

What is driving faster growth in premium board grades across the region?

Solid bleached board is growing fastest at 8.09% CAGR as pharmaceutical and cosmetics packs need better surface whiteness, cleaner print results, and stronger anti-counterfeit finishing.

Why is Brazil so important for cartonboard demand and supply?

Brazil held 47.43% of regional demand in 2025 and benefits from integrated pulp-to-converting capacity, a large FMCG base, and regulation that improves cartonboard's position against plastic packaging.

Which packaging format is expanding fastest in beverage and dairy uses?

Liquid packaging is the fastest-growing format at 5.90% CAGR through 2031, supported by aseptic and gable-top line expansion in Brazil, Colombia, and Chile.

Which end-user group offers the best growth potential through 2031?

Cosmetics and toiletries offers the strongest growth at 7.12% CAGR as urban premiumization increases demand for higher-value folding cartons, molded-pulp inserts, and premium print finishes.

Page last updated on: