Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

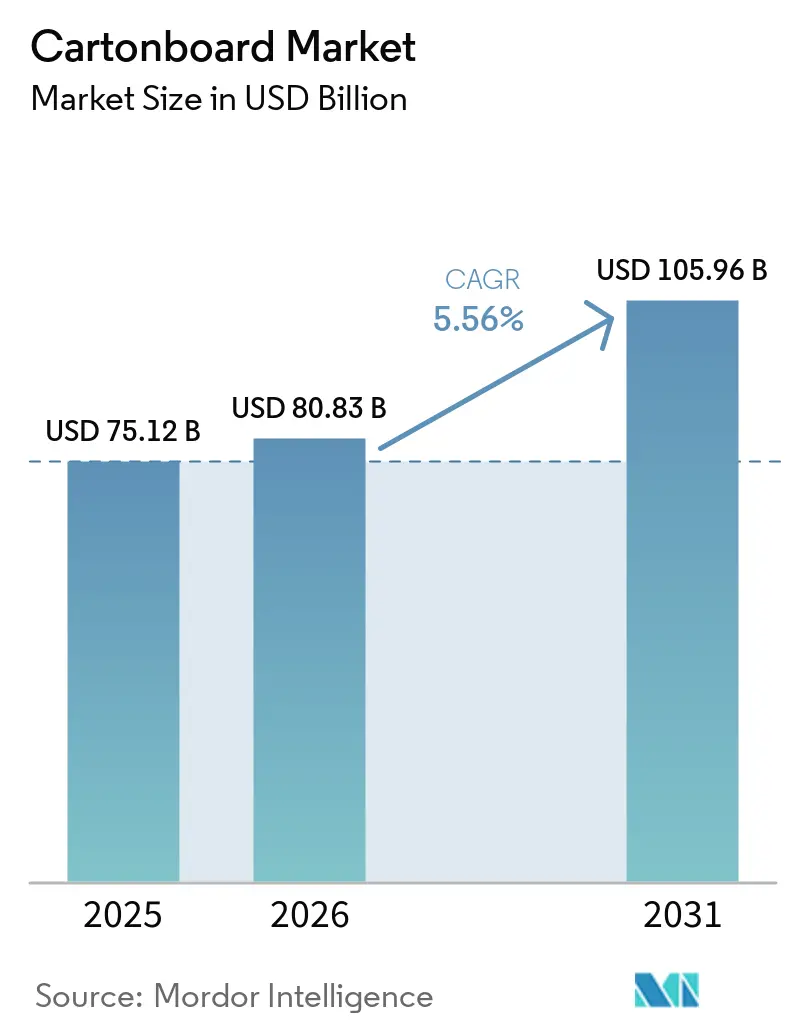

| Market Size (2026) | USD 80.83 Billion |

| Market Size (2031) | USD 105.96 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cartonboard Market Analysis by Mordor Intelligence

The cartonboard market size is projected to be USD 76.12 billion in 2025, USD 80.83 billion in 2026, and reach USD 105.96 billion by 2031, growing at a CAGR of 5.56% from 2026 to 2031. Strong policy pressure for full recyclability, mounting consumer preference for plastic-free packs, and widespread e-commerce lightweighting are steering brand owners toward fiber-based solutions. Folding cartons, sleeves, and liquid packs made from barrier-coated board are displacing rigid polyethylene terephthalate and polypropylene formats, especially in food, beverage, and cosmetics channels. Digital printing presses are unlocking profitable micro-runs for direct-to-consumer brands, while high-yield microfibrillated cellulose enables 10%-15% basis-weight cuts that translate into lower dimensional-weight freight charges. On the supply side, virgin-fiber mills continue to win premium orders in pharmaceuticals and luxury goods, whereas integrated recyclers bank on optical sorting to offset declining bale quality.

Key Report Takeaways

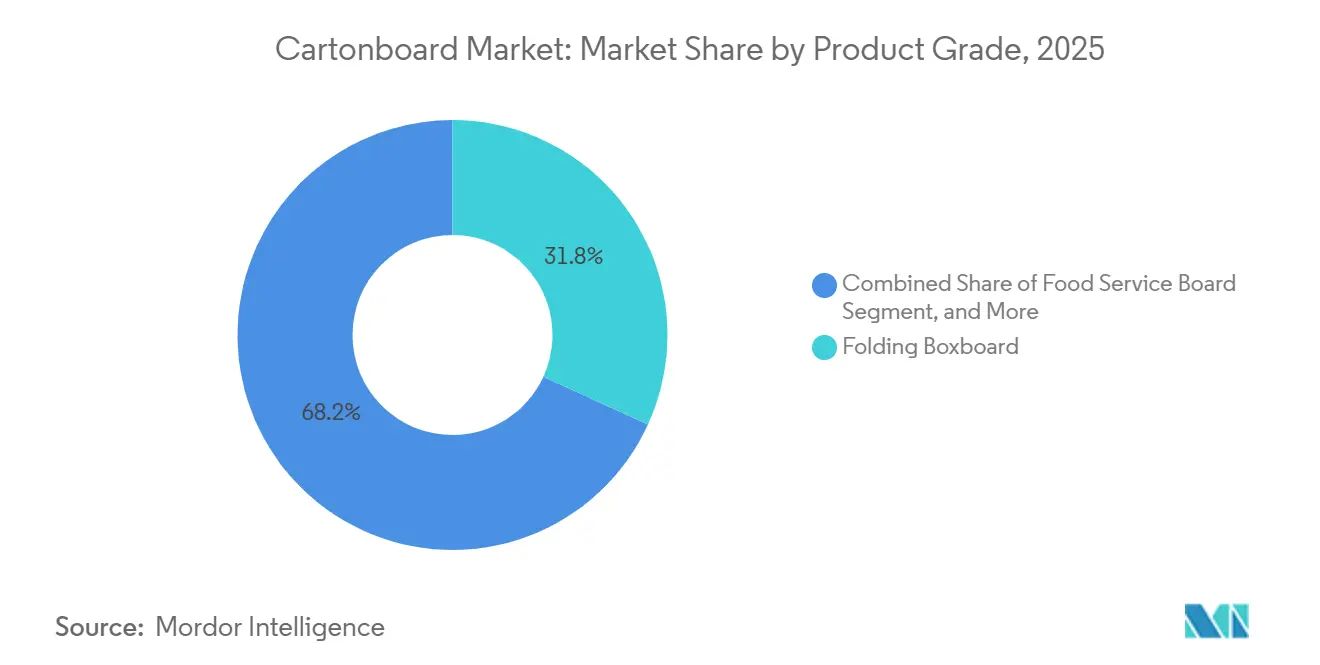

- By product grade, folding boxboard captured 31.84% of the cartonboard market share in 2025.

- By packaging format, the cartonboard market size for the liquid packaging segment is forecast to advance at a 6.33% CAGR through 2031.

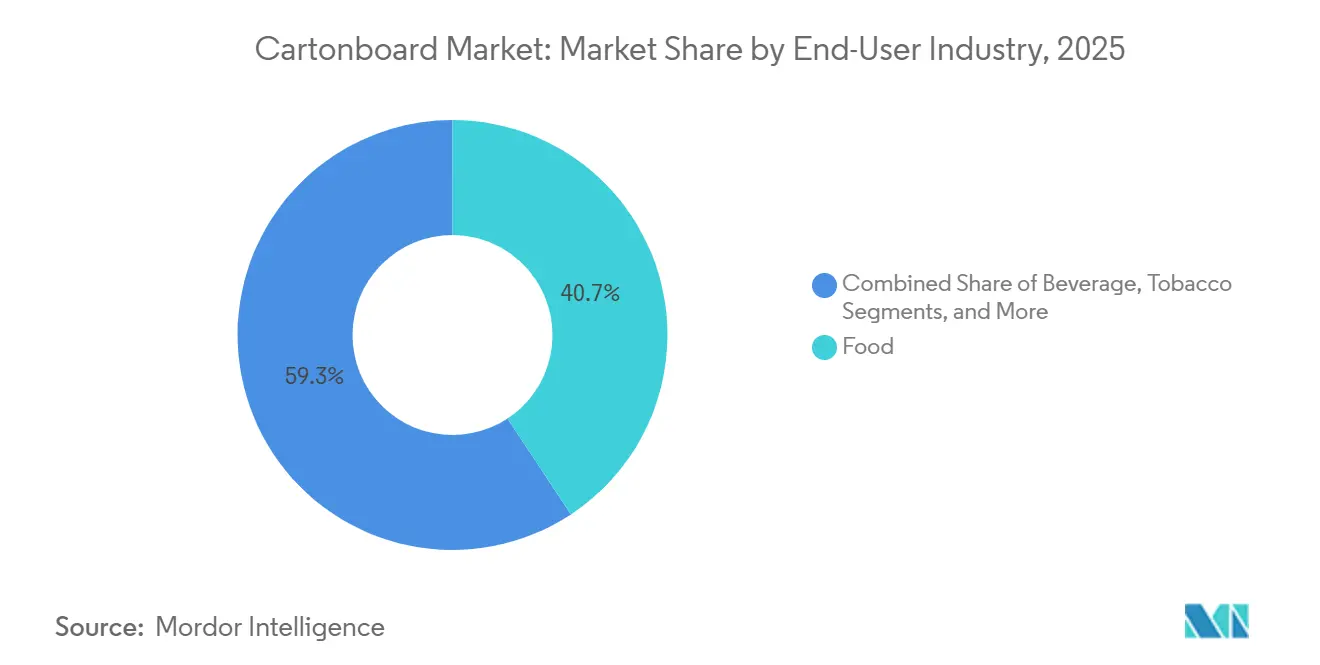

- By end-user industry, food captured 40.72% of the cartonboard market share in 2025.

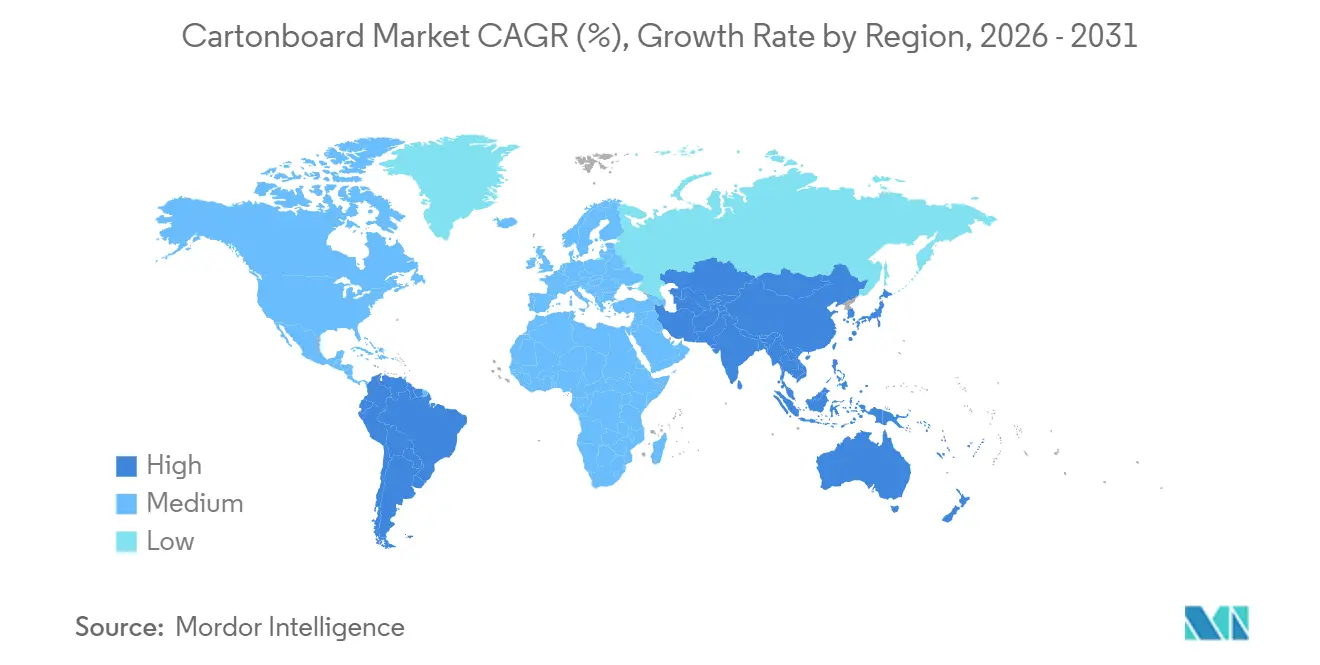

- By geography, the cartonboard market size for the South America segment is forecast to advance at a 6.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Cartonboard Substitution Surge | +1.2% | Global, concentrated in North America, Europe, and APAC e-commerce corridors | Short term (≤ 2 years) |

| FMCG Pivot to Plastic-Free Primary Packaging | +1.0% | Global, accelerated in EU, UK, and APAC markets under EPR mandates | Medium term (2-4 years) |

| Single-Use Plastic Bans in Food and Personal Care Packaging | +0.8% | EU, China, India, South America, spill-over to Middle East and Africa under national ban frameworks | Medium term (2-4 years) |

| Lightweighting Lowers Freight and Warehousing Costs | +0.6% | North America and EU, early adoption in APAC premium consumer goods | Short term (≤ 2 years) and Medium term (2-4 years) |

| High-Speed Digital Printing Supports SKU Proliferation | +0.4% | North America, Europe, Japan, South Korea, emerging in China | Medium term (2-4 years) |

| Premiumization in Luxury and Beauty Cartons | +0.3% | Europe and North America core, fast-growing in China and Gulf Cooperation Council markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Cartonboard Substitution Surge

E-commerce logistics networks are moving from heavier transport packs toward lighter cartonboard formats where product protection and parcel efficiency can still be maintained. This shift matters in the cartonboard market because lower parcel mass and lower dimensional-weight charges directly change packaging material choices at the platform and converter level. Demand is also rising for folding boxboard grades in the 200 g/m²-250 g/m² range that can run consistently on automated fulfillment lines. The quality bar is becoming stricter, as fulfillment centers need uniform caliper and strong machine-direction stiffness to avoid disruptions to high-speed packing equipment. Producers that can meet these specifications near dense delivery corridors are better positioned to win premium business as same-day and next-day delivery models expand.

FMCG Pivot To Plastic-Free Primary Packaging

Large FMCG companies are replacing plastic formats with fiber-based packs as consumer scrutiny and extended producer responsibility costs make plastic usage harder to justify. Nestlé launched a curbside-recyclable paper refill pack for Nescafé in the UK in May 2024, and it also piloted paper packs for Quality Street later in 2024, showing that paper formats are moving into branded consumer packaging rather than remaining a niche option.[1]Nestlé S.A., “Nestlé Sustainability Report 2024, Packaging Progress and Paper-Based Innovations,” Nestlé, nestle.com Mars stated that it removed 1,071 metric tons of multilayer plastic materials by using paper alternatives, with 75% of that reduction coming from converting M&M's pouches in North America.[2]Mars, Incorporated, “Mars 2024 ESG and Sustainability Disclosure, Packaging Plastic Reduction,” Mars, mars.com These packaging shifts support the cartonboard market by expanding demand across mainstream food and confectionery categories with high unit volumes. The value proposition is broader than sustainability alone, since denser pallet configurations can also improve logistics efficiency and soften the higher input cost of paperboard formats.

Single-Use Plastic Bans In Food And Personal Care Packaging

Plastic bans are creating a mandatory demand for cartonboard in food service and personal care applications where short-life packaging is heavily regulated. The EU Packaging and Packaging Waste Regulation entered into force on February 11, 2025, and tightened the policy framework for recyclability and packaging design, supporting the wider use of fiber-based recyclable substrates. In the United States, the FDA confirmed in 2024 the final action to end the use of PFAS in food packaging, which is pushing suppliers toward reformulated food-contact paper and board solutions. India’s Plastic Waste Management Rules, 2025, added stronger recycling and traceability requirements, increasing compliance pressure on plastic packaging and supporting paperboard substitution in consumer packaging chains. These policy moves closely align with demand growth for cups, clamshells, takeaway containers, and related applications, which explains why the food service board is gaining momentum in the cartonboard market.

Lightweighting Lowers Freight And Warehousing Costs

Lightweighting is becoming a practical growth lever in the cartonboard market because it cuts freight costs, reduces warehouse burden, and helps brand owners lower packaging-related emissions. Holmen introduced its Elevate ultra-lightweight cartonboard range in 2025, with grades starting at 72 g/m², aimed at reducing material use while maintaining converting performance and food-contact suitability.[3]Holmen AB, “Annual Report 2025,” Holmen, holmen.com Metsä Board completed a EUR 60 million (USD 67.7 million) modernization at its Simpele mill in October 2025, and the rebuilt coating section improved surface performance at lower coat weights for folding boxboard used in food and healthcare packaging. The sustainability case is also strengthening, since European folding carton mills reported lower cradle-to-gate carbon intensity and a lower share of fossil energy in operations. That combination of cost savings and verified environmental improvements is making lightweighting a durable growth driver for the cartonboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy Price Volatility Compresses Mill Margins | -1.3% | Europe, with high exposure, APAC and North America with moderate exposure | Short term (≤ 2 years) |

| Recycled Fiber Availability and Quality Imbalance | -0.9% | North America and Europe core, spill-over to APAC recycled-board producers | Medium term (2-4 years) |

| Barrier Coating Compliance Raises Capex and Operating Costs | -0.6% | Global, most acute in EU and North America regulatory jurisdictions | Medium term (2-4 years) |

| Molded Fiber and Flexible Paper Substitution in Some Applications | -0.4% | Global, particularly in foodservice and e-commerce cushioning segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy Price Volatility Compresses Mill Margins

Energy cost volatility remains the largest near-term constraint on the cartonboard market because it directly affects mill competitiveness and margin stability. Assocarta reported that Italy’s wholesale electricity price averaged EUR 111 (USD 125) per MWh in October 2025, compared with EUR 84 (USD 95) per MWh in Germany and EUR 57 (USD 64) per MWh in France, showing how sharply cost conditions can diverge inside Europe.[4]Assocarta and Confindustria, “Italian Pulp and Paper Sector Energy Cost Report,” Assocarta, assocarta.it These gaps matter most for non-integrated mills, which have less insulation from market swings and less room to absorb higher utility bills. Smurfit WestRock also pointed to higher input costs and expected effects from rising energy prices in its Q1 2026 outlook, which confirms that the pressure remained active rather than temporary. Larger producers with renewable energy and biomass assets are better protected, widening the structural gap between major integrated groups and smaller regional operators.

Recycled Fiber Availability And Quality Imbalance

Recovered fiber quality is becoming less reliable, which is making life harder for recycled-board producers in the cartonboard market. The Bvse recovered paper report noted that quality and supply conditions remained volatile in 2025 as more complex fiber-based packaging moved through collection streams and increased the sorting burden. Germany’s packaging system maintained a 90% collection quota for paper, board, and carton packaging, yet high collection volumes alone did not solve the purity problem created by mixed household disposal and composite formats. The issue is becoming more complex as PFAS-free and other barrier-coated food-contact boards spread more widely, since those coatings can improve product performance in use while making repulping and fiber recovery more difficult. This quality imbalance limits yield, raises processing costs, and weakens the competitive position of producers that rely heavily on recycled feedstock.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Anchors Volume, Food Service Board Drives Growth

Folding boxboard held 31.84% of the cartonboard market share in 2025 and remained the largest product grade because it serves food, pharmaceutical, and cosmetic applications that demand print quality, stiffness, and barrier performance. The grade has become central to the cartonboard market in consumer packaging because it balances appearance and functionality across regulated and highly branded categories. Solid bleached board and solid unbleached board continued to serve more specialized needs in food service, luxury goods, and beverage secondary packaging, where brightness, strength, or wet resistance mattered more. White-lined chipboard retained its role as a cost-effective option for non-food retail packaging where appearance still matters, but input costs are closely watched. Liquid packaging board also remained important, especially in dairy, juice, and plant-based beverages, where aseptic filling extends shelf life without refrigeration.

The food service board segment is projected to grow at a 6.18% CAGR during 2026-2031, making it the fastest-growing product grade in the cartonboard market. The main support comes from single-use plastic bans that are redirecting demand from plastic-lined and polystyrene formats toward PFAS-free coated cartonboard used in cups, containers, and takeaway packs. Sappi completed the conversion and expansion of Somerset Mill PM2 in May 2025, doubling solid bleached sulfate board capacity from 240,000 tpy to 480,000 tpy with total capital expenditure of USD 525 million. That investment showed how producers are shifting assets away from declining graphic paper and toward higher-growth packaging grades. Compliance with food-contact standards in the United States and Europe also gives premium foodservice board suppliers a quality moat that supports margin resilience within the cartonboard industry.

By Packaging Format: Folding Cartons Lead, Liquid Packaging Accelerates

Folding cartons captured 56.16% of the cartonboard market in 2025, reflecting their broad use across dry foods, frozen meals, pharmaceuticals, and personal care products. They remain the leading format because they offer labeling space, shelf presence, child-resistant design options, and compatibility with QR codes and other traceability features. Graphic Packaging completed the ramp-up of its Waco, Texas, recycled paperboard facility in late 2025 after a total investment of USD 1.67 billion, reinforcing its commitment to folding carton demand in North America. Sleeve and tray formats also continued to gain use in retail-ready packaging, where supermarkets value shelf-facing efficiency for chilled meals and fresh produce. Cups and other food service formats moved in the same direction as new food service board capacity entered the market.

Liquid packaging is projected to expand at a 6.33% CAGR during 2026-2031, making it the fastest-growing packaging format in the cartonboard market. Growth is being driven by aseptic packaging in dairy, juice, soups, broths, ready-to-drink nutrition, and plant-based beverages, where cartonboard combines stiffness and printability with multilayer barrier performance. SIG stated that it is targeting aseptic carton structures with at least 85% paper content by 2025 and 90% by 2030, including work on paper-based closures. This direction increases the fiber share in each pack and expands the long-term addressable space for liquid packaging board. As a result, liquid packaging is becoming an increasingly important growth segment for the cartonboard market, even though folding cartons still dominate total volume.

By End-User Industry: Food Dominates Demand, Pharmaceutical And Healthcare Grows Fastest

The food segment accounted for 40.72% of the cartonboard market in 2025 and remained the largest end-user segment, as cartonboard is deeply embedded in frozen food, cereal, confectionery, takeaway packaging, and broader grocery retail. The cartonboard market depends heavily on food packaging because the material can combine shelf appeal with the moisture, grease, and oxygen barriers required in daily-use applications. The shift toward PFAS-free aqueous barriers is now creating a new product development cycle across food-contact board grades. Food and FMCG demand also supported packaging activity in Brazil during 2025, according to ABRE and FGV IBRE reporting on the country’s packaging production trend. Cosmetics, toiletries, beverages, and tobacco also contributed to meaningful demand, with premium-coated and specialty grades gaining attention in prestige packaging.

The pharmaceutical and healthcare sector is projected to record a 6.54% CAGR during 2026-2031, making it the fastest-growing end-user segment in the cartonboard market. Demand is being supported by aging populations, rising prescription and over-the-counter unit volumes, and tighter procurement standards around traceability and verified fiber sourcing. Pharmaceutical buyers are increasingly specifying child-resistant structures, tamper-evident formats, Braille surfaces, and space for 2D serialization codes, which raises the technical threshold for converters. That dynamic favors larger integrated suppliers and capable folding carton specialists that can meet compliance and consistency requirements across large product portfolios. In this part of the cartonboard industry, quality assurance and documentation have become as important as basic board supply.

Geography Analysis

Asia-Pacific accounted for 43.62% of the cartonboard market share in 2025 and remained the largest value center within the broader global demand base, driven by China, India, Japan, South Korea, and Australia. China’s scale in e-commerce, food and beverage, and electronics packaging continued to anchor regional demand, while India added support through FMCG growth and plastic substitution in consumer packaging. Nine Dragons Paper reported record sales volume of 12.4 million tonnes in 1H FY2026, with net profit up 225.1% year on year, reflecting the strength of integrated paperboard production in China. Japan’s convenience retail model also sustained steady demand for precision-formatted folding cartons used in frequent replenishment cycles. South Korea and Australia remained premium packaging markets where sustainability-driven substitution continued to support the cartonboard market.

South America is projected to expand at a 6.57% CAGR during 2026-2031, making it the fastest-growing region in the cartonboard market. Brazil remained the region’s largest packaging paper base, and ABRE reported packaging production growth of 1.6% in the first quarter of 2025 and 1.8% in the second quarter of 2025. Klabin inaugurated its Piracicaba II facility in March 2025, investing BRL 1.56 billion (USD 274 million) and achieving an annual corrugated packaging capacity of 240,000 tonnes, strengthening regional conversion and logistics infrastructure. North America also remained a major demand hub for the cartonboard market, supported by food, beverage, and pharmaceutical packaging demand and by domestic sourcing shifts after early 2026 trade uncertainty. The Middle East and Africa remained an emerging growth zone, with urbanization, modern retail expansion, and rising adoption of liquid packaging supporting steady demand growth.

Europe continued to benefit from rules that encourage the use of recyclable fiber-based packaging. The PPWR entered into force in February 2025 and sharpened the policy push toward recyclable packaging formats across the European Union. Western Europe remained a major center for food, beverage, and pharmaceutical demand, and procurement standards in these sectors supported the use of premium board grades. Germany also stood out for its strong paper, board, and carton collection framework, including a 90% quota that reinforces demand for recyclable materials and verified recovery systems. At the same time, new virgin-fiber capacity in Scandinavia and Italy increased supply pressure on some European recycled-board mills.

Competitive Landscape

The cartonboard market is moderately consolidated at the top, with a group of large integrated producers influencing capacity, pricing, and customer access across major regions. Smurfit WestRock, created by the 2024 combination of Smurfit Kappa and WestRock, reported net sales of USD 31.2 billion in its first full fiscal year and positioned itself as the largest listed packaging company by revenue. International Paper’s acquisition of DS Smith in 2025 further tightened the competitive structure in several packaging segments, even though the cartonboard market still includes many regional converters and specialist producers. That leaves a market where top-tier suppliers shape strategic direction, but service, specialization, and geographic proximity still matter for a large share of day-to-day business. The balance between consolidation and fragmentation is a defining feature of the cartonboard market in 2026.

A clear pattern in the cartonboard market is the conversion of graphic paper assets into packaging capacity. Sappi’s Somerset Mill PM2 conversion and expansion in the United States is one example, with USD 525 million invested to double SBS capacity and reposition the asset for packaging demand. Another pattern is cost-focused restructuring, and Mayr-Melnhof said its Fit-for-Future program is targeting structural sustainable profit improvements of more than EUR 150 million (USD 165 million) by 2027. The company also closed its Turkey cartonboard mill in November 2025 while reinforcing investment at its Romanian site, showing a deliberate mix of rationalization and reinvestment. These moves show that scale alone is not enough, since producers are also reshaping portfolios to protect margins and improve grade mix.

Technology and product development are also separating leaders from the rest of the cartonboard market. Metsä Board’s Simpele modernization focused on curtain-coating technology that improves surface quality and supports lighter board structures in demanding end uses. SIG’s move toward higher paper-content aseptic cartons shows how system suppliers are increasing cartonboard intensity in liquid packaging applications. Smurfit WestRock also highlighted AI-enabled design tools that reduced packaging development time from months to weeks, thereby strengthening customer retention and enabling faster conversion wins across large SKU portfolios. Chinese integrated producers such as Nine Dragons are adding pressure in export-oriented markets by combining scale, fiber integration, and quality control improvements.

Cartonboard Industry Leaders

Asia Pulp & Paper Company Ltd.

Mayr-Melnhof Karton AG

Nine Dragons Paper (Holdings) Limited

Smurfit WestRock plc

Graphic Packaging Holding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Smurfit WestRock announced the closure of 1 paper machine at its La Tuque, Quebec, mill and an extrusion facility in Pointe-aux-Trembles, Quebec, with 90 affected employees, as part of its North American portfolio optimization strategy. The closures were consistent with the company’s value-based selling repositioning following the 2024 combination with WestRock.

- February 2026: Nine Dragons Paper (Holdings) Limited reported interim results for 1H FY2026, the 6 months ended December 31, 2025, with net profit surging 225.1% year on year to CNY 2.21 billion (USD 307 million) and sales volume reaching a record 12.4 million tonnes, up 8.3%, driven by its pulp-paper integration strategy entering its harvest phase.

- February 2026: Smurfit WestRock published its Medium-Term Investor Update, targeting USD 7 billion in adjusted EBITDA and USD 14 billion in cumulative discretionary free cash flow through 2030, along with annual capital expenditures of USD 2.4 billion-USD 2.8 billion. The plan targeted market growth of 1.6% in North America, 1.7% in Europe, and 2.0% in South America.

- November 2025: Mayr-Melnhof Karton AG closed its cartonboard mill in Turkey, effective November 7, 2025, citing structural overcapacity and weak demand. MM also announced reinforced investments in its Romanian site as a key production and export hub for southeastern Europe, in line with its group-wide Fit-for-Future transformation program.

Global Cartonboard Market Report Scope

The Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Product Grade | Solid Bleached Board | ||

| Solid Unbleached Board | |||

| Folding Boxboard | |||

| White-Lined Chipboard | |||

| Liquid Packaging Board | |||

| Food Service Board | |||

| By Packaging Format | Folding Cartons | ||

| Liquid Packaging | |||

| Sleeve and Tray | |||

| Other Packaging Formats (Cups, Foodservice Containers) | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Pharmaceutical and Healthcare | |||

| Tobacco | |||

| Cosmetics and Toiletries | |||

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the cartonboard market?

The cartonboard market stood at USD 76.12 billion in 2025, is estimated at USD 80.83 billion in 2026, and is forecast to reach USD 105.96 billion by 2031 at a 5.56% CAGR.

Which product grade leads demand for cartonboard?

Folding boxboard leads demand with a 31.84% share in 2025 because it is widely used in food, pharmaceutical, and cosmetics folding cartons.

Which packaging format is growing the fastest in cartonboard applications?

Liquid packaging is the fastest-growing format, with a projected 6.33% CAGR through 2031, supported by aseptic packaging in dairy, juice, and other beverage categories.

Why is food service board gaining traction so quickly?

Food service board is projected to grow at a 6.18% CAGR through 2031 because plastic bans and food-contact rule changes are pushing cups, containers, and takeaway packs toward coated cartonboard formats.

Which end-user segment is expanding the fastest?

Pharmaceutical and healthcare is the fastest-growing end-user segment, with a 6.54% CAGR through 2031, driven by compliance-heavy packaging needs such as tamper evidence, Braille, and serialization space.

Which region offers the strongest growth outlook?

South America has the strongest growth outlook with a projected 6.57% CAGR through 2031, while Asia-Pacific remained the largest value region in 2025 with a 43.62% share.

Page last updated on: