Mexico Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.68 Billion |

| Market Size (2026) | USD 3.85 Billion |

| Market Size (2031) | USD 4.93 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

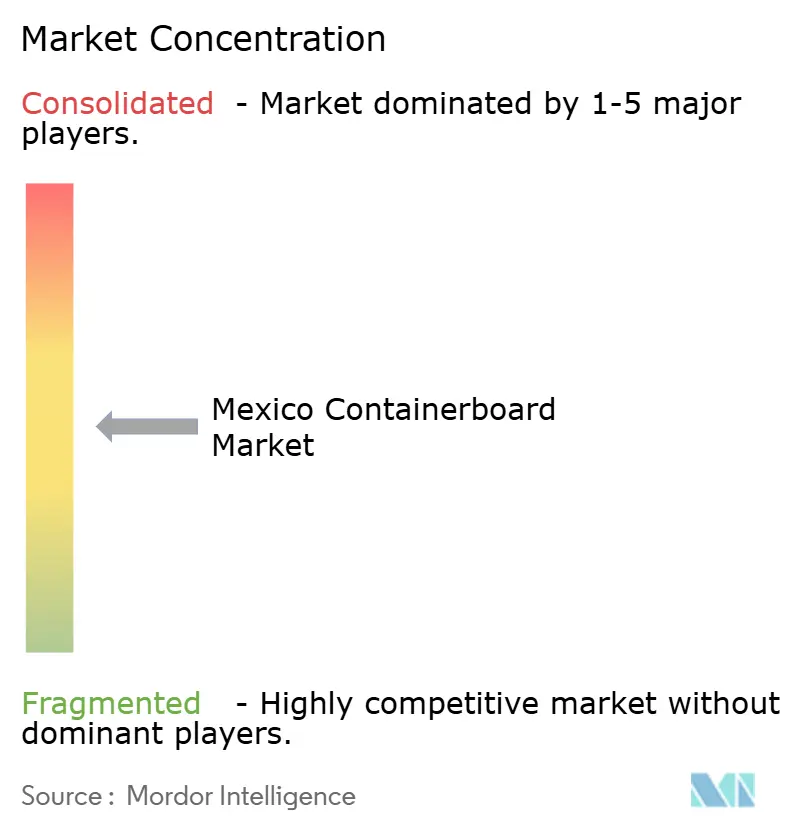

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Containerboard Market Analysis by Mordor Intelligence

The Mexico containerboard market size is projected to expand from USD 3.68 billion in 2025 and USD 3.85 billion in 2026 to USD 4.93 billion by 2031, registering a CAGR of 5.07% between 2026 to 2031. The current profile of the Mexican containerboard market reflects a change in demand quality, not just a recovery in tonnage, as nearshoring activity, the new circular economy law, and stronger product exports are raising both volume needs and specification requirements. Demand is being supported by a broad base of industrial and consumer packaging use, while the product mix is moving toward premium and high-performance grades that can meet stricter export, moisture, and print requirements. The Mexico containerboard market is also being shaped by a clear regional divide, with northern manufacturing corridors anchoring most converting activity, and the Bajío emerging as a second growth belt tied to aerospace and consumer goods production. Competition remains split between vertically integrated producers that control mill assets, fiber, and conversion, and a large base of independent box makers that serve regional demand without upstream integration.

Key Report Takeaways

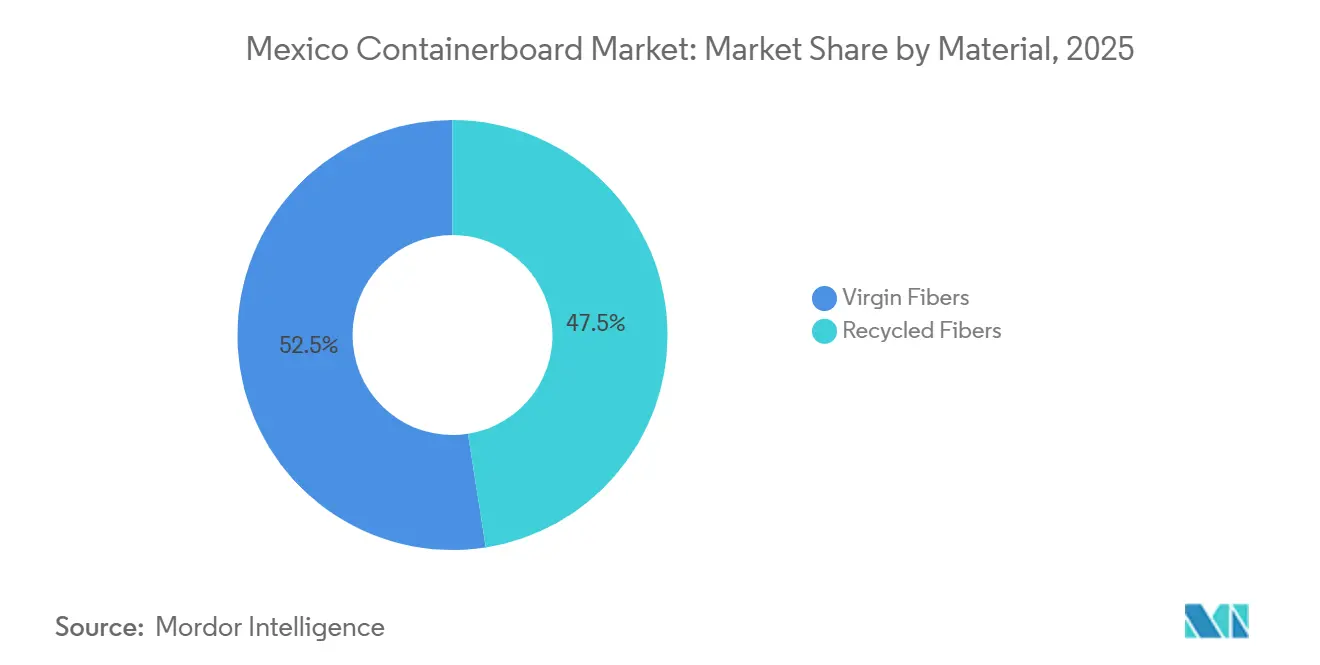

- By material, virgin fibers captured 52.47% of the Mexico containerboard market share in 2025.

- By product type, the Mexico containerboard market size for kraftliners is projected to grow at a 5.49% CAGR to 2031.

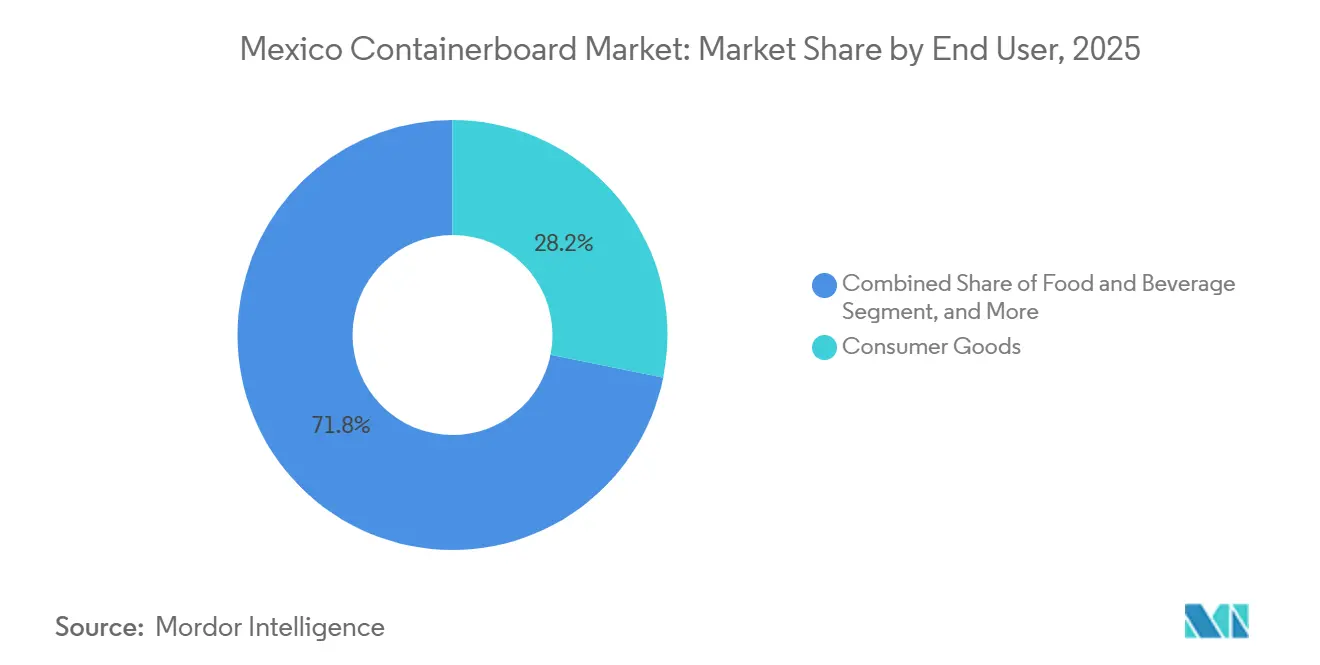

- By end user, consumer goods captured with 28.16% of the Mexico containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-Led Nearshoring Demand for High-Performance Boxes | +1.5% | Northern Mexico, spill-over to Bajío | Long term (≥ 4 years) |

| Fast-Growing E-commerce and Fulfillment Throughput | +1.2% | National, with early gains in Mexico City Metro, Guadalajara, Monterrey | Medium term (2-4 years) |

| Circular Packaging Compliance Favoring Fiber-Based Formats | +0.8% | National, urban manufacturing hubs | Long term (≥ 4 years) |

| Produce Export Corridors Increasing Moisture-Resistant Box Demand | +0.7% | Sonora, Sinaloa, Michoacán, Jalisco | Long term (≥ 4 years) |

| Shelf-Ready Retail Packaging Upgrading Print-Grade Containerboard Mix | +0.5% | National, concentrated in major metro retail clusters | Medium term (2-4 years) |

| Lightweighting Requirements Accelerating High-Performance Recycled Grades | +0.4% | National, led by e-commerce and automotive secondary-packaging converters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-Led Nearshoring Demand for High-Performance Boxes

Mexico’s manufacturing FDI reached USD 40.8 billion in 2025, up 10.8% year over year, and the manufacturing sector absorbed 36% of committed capital, providing the Mexico containerboard market with a durable factory-led demand base in the main industrial corridors. Each new factory and distribution center adds ongoing corrugated demand, and many nearshoring manufacturers that ship to the United States are specifying box designs aligned with U.S. Edge Crush Test standards instead of older domestic burst benchmarks. That shift is moving the Mexico containerboard market toward premium kraftliner and stronger medium grades, as export packaging now requires greater stacking strength, print quality, and handling consistency.

Fast-Growing E-commerce and Fulfillment Throughput

By 2026, online retail is forecast to reach 17.7% of total sales in Mexico, which keeps pushing the Mexico containerboard market toward packaging formats designed for parcel handling, automated sorting, and right-sized shipping. The main change is not only more boxes, but different boxes, since e-commerce operators increasingly require light single-wall and E-flute cases that can meet dimensional and handling tolerances across large fulfillment networks. As large marketplace operators centralize procurement, the Mexican containerboard market is likely to see a gradual shift in pricing power and product specifications away from many small buyers and toward a smaller group of logistics-driven customers.

Circular Packaging Compliance Favoring Fiber-Based Formats

Mexico enacted the General Law on Circular Economy on January 19, 2026, and it became effective on January 20, 2026, creating a binding national framework for extended producer responsibility and circular product design. Article 36 requires productive sectors to adopt circular design criteria and progressively integrate secondary raw materials, which supports the Mexican containerboard market because fiber-based secondary packaging aligns more closely with these policy goals than many plastic alternatives. Bio Pappel’s Urban Forest model, which turns recovered paper and cardboard into new 100% recycled products without tree harvesting, positions its recycled offering well as the Mexican containerboard market adapts to compliance-led specification changes.[1]Bio Pappel, “We Welcomed the SEMARNAT to Our Tizayuca Plant,” Bio Pappel, biopappel.com SEMARNAT is expected to publish implementing rules by July 19, 2026, and packaging is widely seen as one of the early priority categories under the new framework.

Produce Export Corridors Increasing Moisture-Resistant Box Demand

Mexico supplies 63% of U.S. vegetable imports and 47% of U.S. fruits and nuts, and 91% of Mexico’s horticultural exports go to the U.S., which makes fresh produce a specialized but important source of demand in the Mexico containerboard market. Avocados From Mexico forecast a record GBP 2.5 billion (USD 3.1 billion) of U.S. imports for the 2025 to 2026 season, and strawberry exports from Mexico were projected to reach 300,000 tonnes by the end of the 2024 to 2025 season, up 25%. These volumes do not translate into standard corrugated demand because produce exporters need packaging that can tolerate cold-chain handling, long trailer dwell times, and indirect food-contact requirements. That is why the Mexico containerboard market is seeing a niche pull toward wax-coated or polymer-laminated double-wall structures and premium moisture-resistant linerboard grades, especially in Sonora and Michoacán.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OCC and Imported Containerboard Cost Volatility | -0.9% | National, with the highest exposure in recycled-fiber mill clusters | Short term (≤ 2 years) |

| Water and Power Constraints in Northern Manufacturing Corridors | -0.7% | Northern Mexico | Long term (≥ 4 years) |

| 40-Hour Workweek Reform Raising Conversion and Mill Labor Costs | -0.5% | National, especially labor-intensive converting plants and shift-based paper mills | Long term (≥ 4 years) |

| U.S. Import Pressure During Peso-Strength Cycles | -0.4% | National, most acute in domestic testliner and medium grades, competing with U.S. imports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OCC and Imported Containerboard Cost Volatility

Mexico remains a net importer of containerboard, with the United States supplying more than 99% of imports, while domestic recycled-fiber mills rely heavily on OCC as their main raw material, leaving the Mexican containerboard market exposed to external cost cycles. Export OCC prices in U.S. port cities ranged from USD 136 to USD 139 per ton FAS in the first half of 2025, reflecting tighter domestic generation and competing demand from Southeast Asia. When the Mexican peso strengthens, imported kraftliner becomes more competitive than domestic testliner, which puts pressure on local margins and weakens the case for new investment in domestic mill capacity. ANFEC also noted that North American capacity cuts of nearly 6% in 2025 were contributing to upward price pressure that could keep Mexican import costs elevated through 2026.

Water and Power Constraints in Northern Manufacturing Corridors

Water scarcity and grid reliability are no longer distant risks in the Mexican containerboard market because they are already affecting the country’s main industrial and converting regions. More than 45% of Mexico’s aquifers are overexploited, rainfall is structurally low in the north, and water governance remains fragmented, making potable water security a direct operational issue for mills. Closed-loop water systems are becoming a practical requirement for operating permits in the most stressed corridors, especially for paper production that relies on steady process-water availability. On the electricity side, 91% of firms in northeastern industrial parks reported difficulties securing a reliable power supply, even though that region accounts for 45% of the national export value. BBVA Research still projects 2.4% growth in Mexico’s paper sector for 2026, but that outlook assumes larger producers with private generation or stronger operating resilience can maintain output, leaving smaller converters in Mexico's containerboard market at a lasting cost disadvantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Fiber Maintains Specification Premium Amid Recycling Push

Virgin fibers held 52.47% of the Mexico containerboard market share in 2025, and this segment is projected to grow at 5.73% CAGR through 2031, which is the highest rate across the 2 material categories. This lead reflects the persistent quality gap in export applications, where electronics and automotive-component assemblers in Baja California and Chihuahua continue to specify virgin kraft linerboard for burst strength and humidity resistance. Mexico imported USD 1.18 billion worth of pulp in 2024, mainly from the United States and Brazil, which keeps virgin board economics exposed to exchange-rate swings during peso depreciation cycles. Even with that cost exposure, the Mexico containerboard market still relies on virgin grades, where box failure incurs higher logistics or product-risk costs.

Recycled fibers remain important in the Mexico containerboard market as domestic recovery systems improve and regulatory support strengthens. Bio Pappel recycled 1.93 million short tons of paper and corrugated material in 2024, and Mexico recovered 60% to 65% of used cardboard, which shows that local feedstock collection already provides a meaningful base for recycled board supply. The 2026 circular economy law reinforces that trend by requiring the progressive integration of secondary raw materials under EPR-linked product design rules.[2]Mauricio Llamas and Sofia de Llano, “Mexico Enacts Circular Economy Law, Extended Producer Responsibility and Product Design, Guiding Principles,” Hogan Lovells, hoganlovells.com Over the forecast period, that should narrow the share gap between virgin and recycled grades in FMCG and consumer goods applications where domestic distribution matters more than strict cross-border export standards.

By Product Type: Kraftliners Anchor Export Demand, Flutings Leverage Agricultural and Industrial Growth

Kraftliners accounted for 53.89% of the Mexican containerboard market in 2025 and are projected to expand at a 5.49% CAGR through 2031. Their lead is tied directly to the export manufacturing profile of the Mexico containerboard market because U.S.-bound goods often require ECT performance levels that standard domestic testliner does not consistently deliver. Kraft grades, therefore, remain the default choice for nearshoring-linked converters in Monterrey, Tijuana, and Juárez that serve electronics, automotive parts, and medical device shipments. Testliners still hold an essential place in the domestic packaging mix because food, FMCG, and regional distribution customers remain more price sensitive and often operate with moderate strength requirements.

Produce exports keep demand firm for moisture-resistant medium in Sonora and Michoacán, where avocado and berry shipments require stronger cold-chain packaging formats. Industrial packaging is also raising fluting requirements as automotive and aerospace clusters in Querétaro and Guanajuato move away from wooden crates toward high-performance semi-chemical grades. That substitution can reduce tare weight by up to 40% and shorten phytosanitary inspection delays at the U.S. border, making fluting quality more commercially important than a simple volume reading would suggest.

By End User: Industrial Gains Share as Manufacturing Nearshoring Reshapes Demand Mix

Consumer goods led the Mexico containerboard market with a 28.16% share in 2025, supported by domestic retail expansion and a large FMCG production base in the Estado de México and Jalisco. Industrial end users, however, are forecast to grow at a 6.14% CAGR through 2031, making them the fastest-growing demand group in the Mexico containerboard market. This matters because industrial packaging usually requires heavier-wall construction, tighter engineering tolerances, and export-grade performance, which supports higher average selling prices per tonne. The shift, therefore, changes value capture across the supply chain, not only the destination of box demand.

Food and beverage remain the most stable base in the Mexican containerboard market, as export growth and cold-chain investment continue to support recurring corrugated use in produce and packaged foods. Secondary packaging for fresh produce must comply with U.S. FDA indirect food-contact expectations, which set a firm quality floor for linerboard supplied into this channel. Other end users, including retail display packaging and small-parcel e-commerce, are still smaller but are gaining relevance as micro-corrugated and E-flute shelf-ready formats spread across modern trade. Over the forecast period, a diversified customer mix should remain the best hedge for producers in the Mexico containerboard industry because no single end-use stream fully shields mills or converters from swings in input costs, export volumes, or regulatory changes.

Geography Analysis

Nuevo León, Estado de México, and Jalisco together accounted for more than 45% of the country’s corrugated converting capacity, making these industrial belts the main production and demand centers in the Mexican containerboard market. Northern Mexico hosts the largest cluster of converting plants and the most specification-intensive packaging demand tied to automotive, electronics, medical devices, and consumer goods. This concentration keeps both virgin and high-performance recycled grades in active demand, as export-oriented plants require stronger, more consistent box performance. Nuevo León captured 8.8% of national FDI in the first half of 2025, which reinforces Monterrey’s role as a manufacturing and packaging hub. The main limit on further capacity growth in this corridor is utility availability, since power reliability and water access remain tight across northeastern industrial parks.

Baja California and Chihuahua were Mexico’s top exporting states for corrugated boxes in 2024, with export values of USD 70.9 million and USD 35.7 million, respectively, underscoring the role of border manufacturing in supporting the Mexico containerboard market. Central Mexico and the Bajío are emerging as the fastest-evolving growth corridor, as nearshoring activity is spreading beyond heavy industry into aerospace, electronics, and pharmaceuticals. Querétaro, Guanajuato, and Jalisco are benefiting from that diversification, while Estado de México anchors the logistics side through Mercado Libre’s 80,000 m² cross-dock facility that can process up to 1 million parcels per day. These patterns are lifting demand for printable virgin linerboard, coated recycled surfaces, and lighter corrugated formats designed for parcel and retail handling.

Southern Mexico remains the least-developed geography in the Mexico containerboard market because manufacturing activity is thinner, OCC collection is more fragmented, and logistics systems are less mature. Fresh produce packaging is the main demand base there, and Michoacán stands out because avocado pack-house activity creates concentrated need for moisture-resistant corrugated formats. The 2025 to 2026 avocado season is forecast to reach a record GBP 2.5 billion (USD 3.1 billion) of U.S. imports from Mexico, which supports recurring corrugated demand around Tancítaro and Uruapan.[3]Bill Martin, “Avocados From Mexico Forecasts Record 2.5 Billion Pounds of US Imports for 2025-2026 Season,” Haul Produce, haulproduce.com Plan México’s USD 20 billion water project portfolio may improve conditions over time, but a material shift in the geography of the Mexico containerboard market is unlikely within the 2026 to 2031 period.

Competitive Landscape

The Mexico containerboard market is moderately concentrated at the mill level and highly fragmented at the converting tier, which creates a clear divide between large integrated suppliers and many regional box makers. Integrated producers can absorb fiber cost swings more effectively because they combine mill assets, recovered fiber access, and converting operations, while independents remain more exposed to imported board prices and OCC volatility. The 2024 merger of Smurfit Kappa and WestRock created Smurfit Westrock plc and raised the competitive baseline at the top end of the Mexico containerboard market. International Paper’s June 2025 sale of its Xalapa containerboard mill and recycling operations in Xalapa and Apodaca to APSA also redistributed capacity toward regional hands and created room for mid-scale Mexican producers to pursue new supply relationships.[4]International Paper, “International Paper Announces Strategic Changes to Support Growth in North America,” Nasdaq, nasdaq.com Bio Pappel remains the largest purely domestic paper group, operating 24 industrial packaging plants and advancing expansion plans in the northeast and Pacific regions, which signals a stronger contest for converting share over the next few years

Strategic moves in the Mexico containerboard market are centering on geographic expansion, fiber efficiency, and higher-value packaging formats. Smurfit Westrock’s USD 65 million Sonora plant is aimed at corrugated, micro-corrugated, and high-graphic folding carton production for beer, food, and beverage customers, which reflects the shift toward specification-rich packaging demand. Bio Pappel is using its Urban Forest model, closed-loop water systems, and Bio-ENERGY cogeneration to lower operating pressure while matching the compliance direction of the new circular economy framework. Papeles y Conversiones de México also upgraded its PM 1 machine with Valmet in May 2025, raising speed, efficiency, and recycled linerboard capability rather than waiting for a greenfield capacity cycle.

The clearest white space in the Mexico containerboard market sits in high-graphic micro-corrugated formats for shelf-ready retail and point-of-purchase display uses, where print-ready domestic supply still appears tighter than evolving demand. Another competitive pressure point comes from converters using incentives to import semi-finished linerboard duty-free and convert it for U.S. demand, which bypasses some domestic mill economics and can erode local board volumes. Compliance is also becoming a stronger differentiator because food-safety, ISO, and circularity credentials are increasingly shaping buyer approval and public procurement access. Even so, the Mexico containerboard market is likely to remain only moderately concentrated through 2031 because top-end mill capacity is becoming more consolidated while hundreds of regional converters still fragment downstream supply.

Mexico Containerboard Industry Leaders

Smurfit Westrock plc

Bio Pappel, S.A. de C.V.

International Paper Company

Grupak Operaciones, S.A. de C.V.

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mexico's Federal Labour Law amendments (secondary legislation to the constitutional 40-hour workweek reform) were published in the Official Federal Gazette (DOF) on May 1, 2026, formalizing a gradual reduction from 48 to 40 hours per week by January 1, 2030 without salary reductions.

- March 2026: Mexico's constitutional reform reducing the statutory workweek was published in the DOF on March 3, 2026, with 2026 designated as an operational adjustment period for employers.

- February 2026: SEMARNAT Minister Alicia Bárcena visited Bio Pappel's Tizayuca plant to review its "Urban Forest" circular economy model, which recycles paper and cardboard into 100% recycled products without tree harvesting, zero additional carbon emissions, and with a zero-effluents water system.

- June 2025: International Paper announced the sale of its containerboard mill in Xalapa, Veracruz, and its recycling plants in Xalapa and Apodaca, Nuevo León, to Acabados de Papeles Santinados y Absorbentes (APSA) as part of a strategic portfolio optimization to focus on sustainable packaging growth in core geographies.

Mexico Containerboard Market Report Scope

The scope of the report includes an analysis of the Mexico containerboard market, which encompasses the production, consumption, and trade of containerboard materials. Containerboard is the paperboard used primarily for the manufacture of corrugated boxes and packaging solutions. The study examines market trends, key drivers, challenges, and opportunities within the forecast period, providing insights into the industry's dynamics and growth potential.

The Mexico Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users |

Key Questions Answered in the Report

What is the current size of the Mexico containerboard sector?

It stands at USD 3.85 billion in 2026 and is projected to reach USD 4.93 billion by 2031 at a 5.07% CAGR over 2026 to 2031.

Which product type leads demand in Mexico?

Kraftliners lead by product type with a 53.89% share in 2025, supported by export manufacturing needs and stronger box performance requirements.

Which end-use group is growing the fastest in Mexico?

Industrial end users are projected to grow at a 6.14% CAGR through 2031 as nearshoring raises demand from automotive, electronics, medical device, and aerospace production.

Why is recycled-content board becoming more important in Mexico?

The 2026 General Law on Circular Economy supports wider use of secondary raw materials, which strengthens the case for recycled-content packaging across food, beverage, and consumer goods supply chains.

Which regions are the main demand centers for corrugated packaging in Mexico?

Northern Mexico remains the core demand engine, while the Bajío and central corridors are gaining importance through aerospace, electronics, pharmaceuticals, and e-commerce logistics activity.

What are the main risks affecting producers and converters in Mexico?

The main pressures are OCC and imported board cost volatility, water and power constraints in northern corridors, and rising labor costs linked to the gradual 40-hour workweek reform.

Page last updated on: