Japan Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

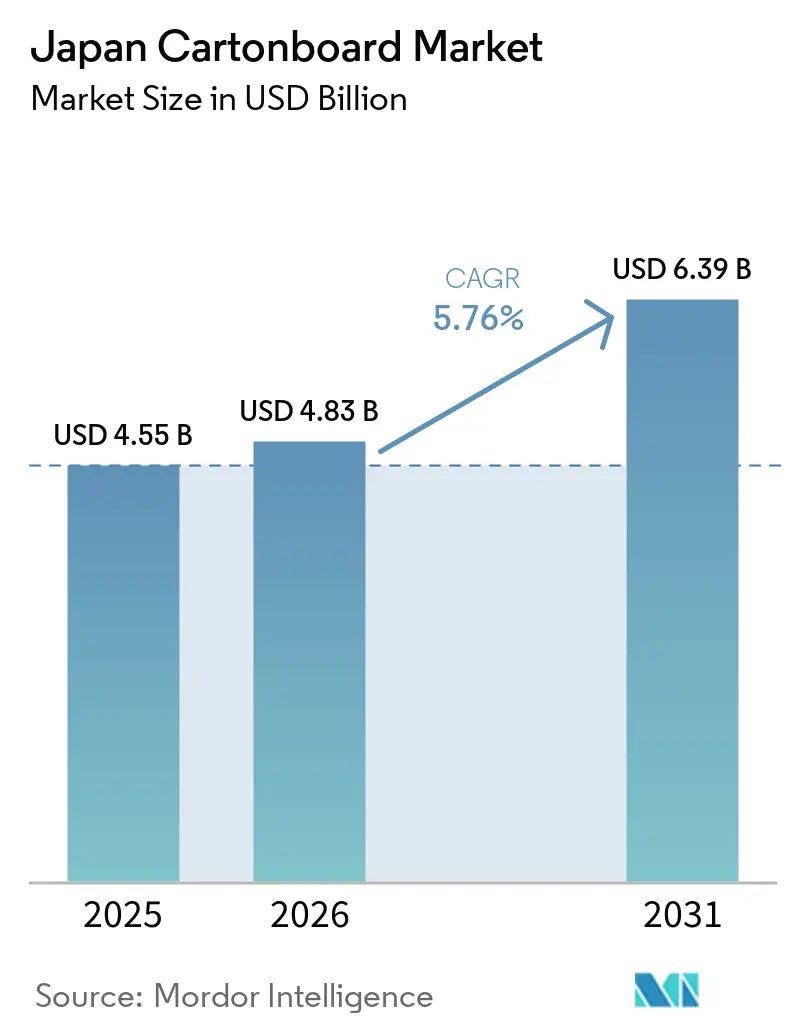

| Base Year Market Size (2025) | USD 4.55 Billion |

| Market Size (2026) | USD 4.83 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

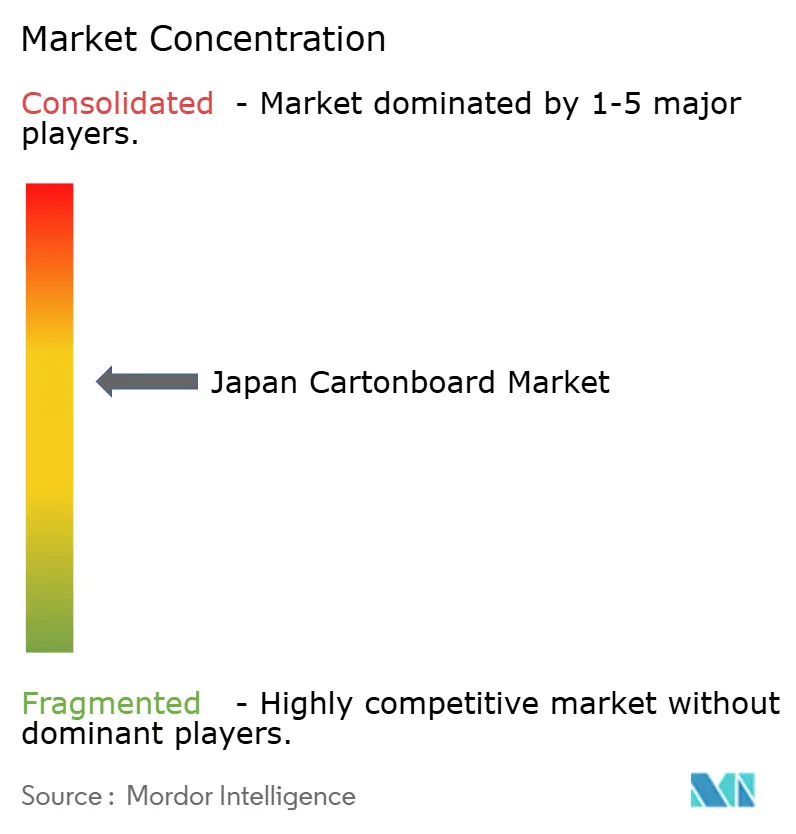

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Cartonboard Market Analysis by Mordor Intelligence

The Japan Cartonboard Market size is projected to expand from USD 4.55 billion in 2025 and USD 4.83 billion in 2026 to USD 6.39 billion by 2031, registering a CAGR of 5.76% between 2026 to 2031.

Growth is taking shape even as Japan's wider paper and paperboard base keeps shrinking, which pushed the total market below 20 million tons and extended the decline in packaging paper shipments into a fourth straight year. That contrast shows how the Japan cartonboard market is drawing spend away from lower-value graphic grades and toward rigid fiber formats with stronger print quality, barrier performance, and recycling alignment. Regulation is reinforcing that shift, as packaging users face tighter recycling and plastic-reduction obligations, and the 2026 naphtha supply disruption also made paper substitution more urgent for retailers and converters. Demand is also rising from e-commerce, premium FMCG packs, and brand investment in higher-graphics cartons that improve shelf presence and delivery performance. Population decline, cost pressure in pulp and energy, and the structural strength of flexible pouches still limit the pace of expansion, which keeps competition active even in a market led by integrated paper companies.

Key Report Takeaways

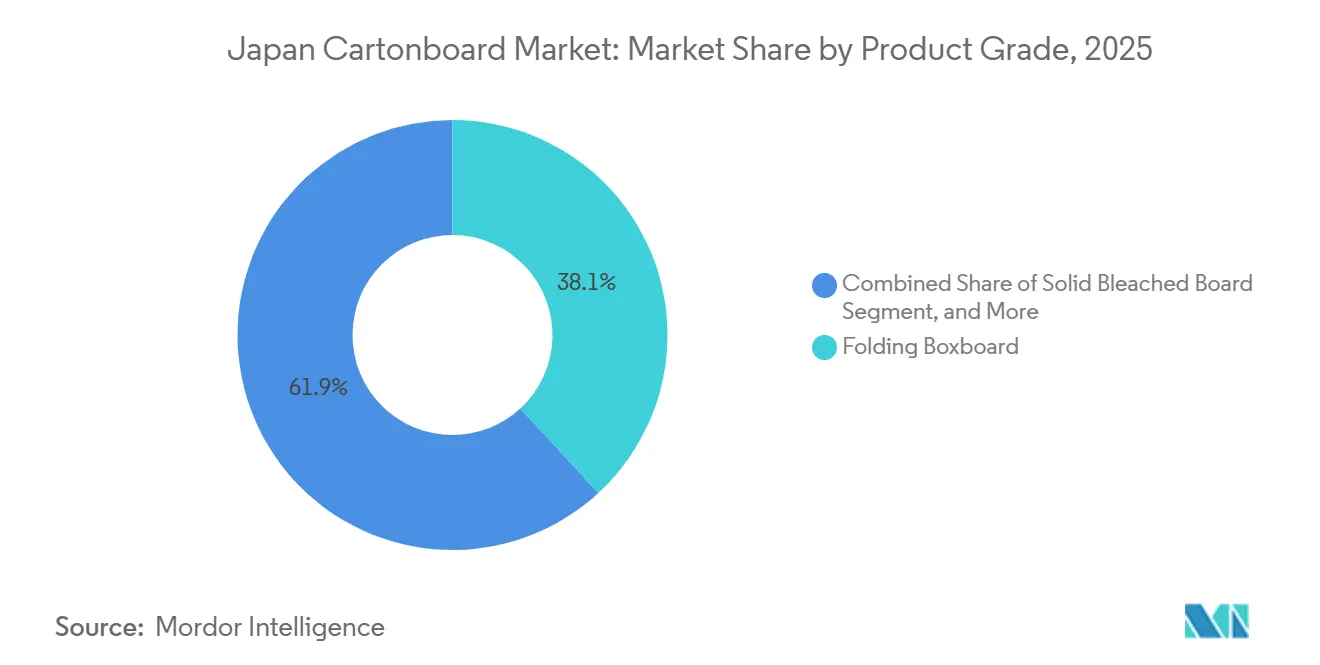

- By product grade, folding boxboard led with 38.13% revenue share in 2025, while white-lined chipboard is forecast to expand at a 7.26% CAGR through 2031.

- By packaging format, folding cartons accounted for 50.50% of the Japan cartonboard market size in 2025, while liquid packaging is projected to grow at a 6.34% CAGR through 2031.

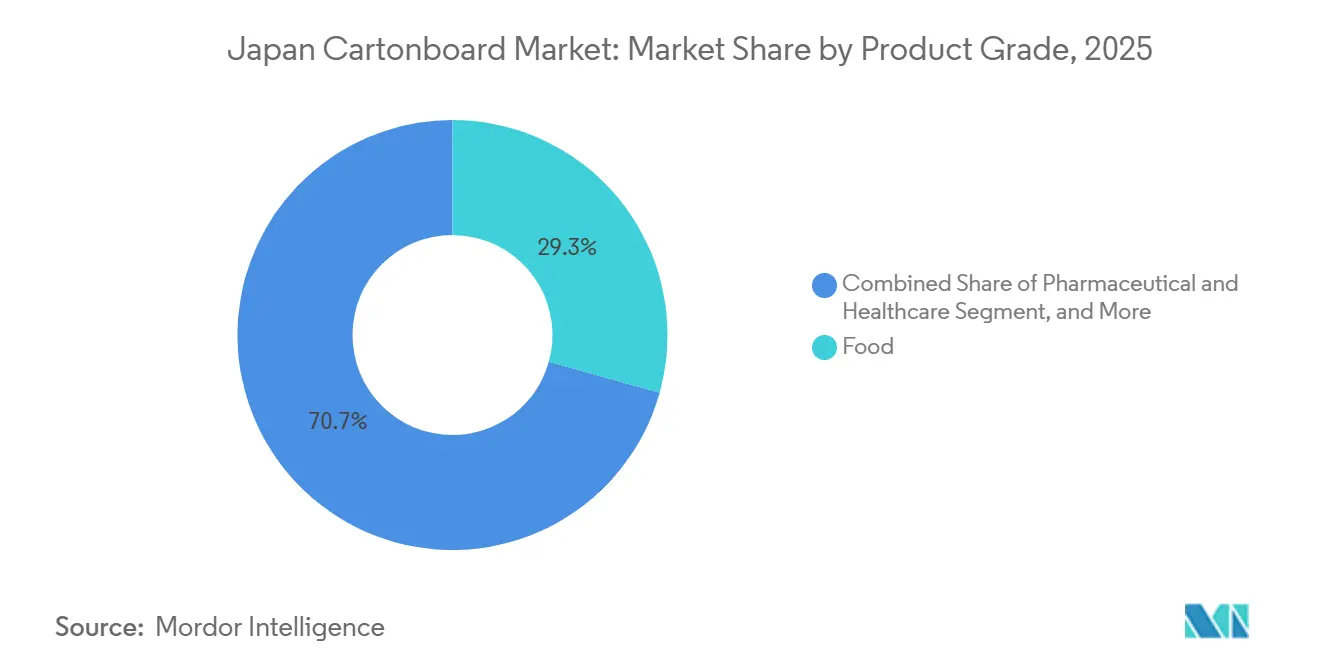

- By end-user industry, food represented 29.32% of the Japan cartonboard market size in 2025 and is also set to record the fastest segment growth at a 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-Reduction Regulation Shifting FMCG Packs To Board | +1.5% | National, accelerating in major FMCG retail corridors across Kanto and Kansai | Short term (≤ 2 years) |

| Food And Beverage Folding Carton Demand Resilience | +1.1% | National, anchored by convenience store density in Tokyo, Osaka, and Nagoya metro areas | Medium term (2-4 years) |

| E-Commerce And Private-Label Short-Run Print Demand | +0.8% | National, highest intensity in Tokyo and major logistics hub corridors | Medium term (2-4 years) |

| Premium Cosmetics And Health Products Need High-Graphics Cartons | +0.5% | National, concentrated in premium urban retail and department store channels | Long term (≥ 4 years) |

| Administrative Recycling Of Liquid And Oil Paper Packs | +0.4% | National, regulatory framework enforced by Japan's Ministry of the Environment | Medium term (2-4 years) |

| Domestic Liquid Carton Localization And Barrier Paper Innovation | +0.3% | National, production centered on major integrated mills in Honshu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Reduction Regulation Shifting FMCG Packs To Board

Japan's packaging framework combines recycling obligations for paper packs with the Plastic Resource Circulation Act, and that policy mix is giving the Japan cartonboard market a stronger compliance-led demand base in 2026. The regulatory effect is stronger now because businesses using large packaging volumes face clearer reduction and reporting expectations than they did in the early phase of plastic-control policy. The demand pull also intensified when the 2026 naphtha supply disruption tightened plastic packaging availability and raised urgency around fiber substitution in Japanese retail channels. Retail actions such as the shift from plastic food-service lids and containers toward paper alternatives show that substitution is moving from policy intent into commercial execution across the Japan cartonboard market. Converters that can supply food-contact grades, verified recycling routes, and reliable fiber sourcing are therefore in the best position to capture near-term gains as compliance and supply risk start working in the same direction.[1]Ministry of the Environment, “Act on Promotion of Resource Circulation for Plastics,” Ministry of the Environment, plastic-circulation.env.go.jp

Food And Beverage Folding Carton Demand Resilience

Food and beverage remains the most dependable demand base in the Japan cartonboard market because daily replenishment cycles favor rigid packs that combine print quality, structural stability, and shelf visibility. Japan's dense convenience store network keeps carton demand active across ready meals, confectionery, and ready-to-drink products, especially in large metro areas where shelf turnover is high and retail response times are short. Premium food positioning is also helping revenue hold up better than volume, since higher-value packs carry better print requirements, stronger board specifications, and more finishing work per unit. Rengo's Paperboard and Paper Processing segment posted JPY 397,163 million in net sales, equivalent to USD 2.65 billion, in the first 3 quarters of FY2026, with 1.1% year-over-year growth, which shows that pricing and mix management remained effective in a cost-heavy environment. That pattern supports the Japan cartonboard market because food packs are not only a volume anchor, they are also a practical route for passing through higher input costs without losing relevance in essential consumer categories.[2]Rengo Co., Ltd., “Fiscal Year Ending March 2026 Q3 Financial Results,” Japan IR, japanir.jp

E-Commerce And Private-Label Short-Run Print Demand

The Japan cartonboard market is also benefiting from the overlap between e-commerce growth and private-label expansion, because both trends raise demand for flexible print runs and retail-ready fiber packs. Japan's sustainable packaging market was growing at over 7% annually as of 2025, showing that brands were already allocating more budget to fiber-based transit and presentation formats for online retail. That demand is especially relevant for cartonboard converters because branded shipping packs, own-label launches, and promotional packaging all depend on shorter runs and quicker artwork changes than legacy long-run formats. White-lined chipboard's projected 7.26% CAGR fits this shift, since recycled-fiber content, acceptable print performance, and good strength-to-weight balance make it suitable for fulfillment and secondary packaging applications described in the Japan cartonboard market. Converters with digital presses and faster make-ready capability are therefore better placed to capture value, because the winning offer is increasingly based on turnaround speed and version flexibility rather than on pure mill scale.

Premium Cosmetics And Health Products Need High-Graphics Cartons

Prestige beauty and healthcare packaging is giving the Japan cartonboard market a durable premium layer because these products rely on appearance, surface quality, and technical functionality at the same time. High-end cosmetics still depend on rigid cartons for gifting, seasonal launches, and brand storytelling, which keeps demand firm for boards that can handle embossing, specialty coatings, and clean print reproduction. TOPPAN's PAPER JAR, launched in November 2025 with more than 50% paper by weight, FSC-certified substrate, and GL BARRIER film, shows that innovation is also extending cartonboard into container applications that were once more plastic dependent. Healthcare adds another layer of support because aging-related pharmaceutical demand favors packs with braille, tamper evidence, and easy-open features that call for stable converting quality rather than low-cost format substitution. This makes the Japan cartonboard market less dependent on mass retail packaging alone, because premium cosmetics and health products support higher unit values and more specialized conversion work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virgin Pulp And Energy Cost Volatility | -0.8% | National, exposed to global BSKP and BHKP commodity markets and energy import prices | Short term (≤ 2 years) |

| Flexible Pouch Substitution In Snacks And Convenience Formats | -0.7% | National, most acute in snack and single-serve convenience food segments | Medium term (2-4 years) |

| Shrinking Population Pressuring Discretionary Pack Volumes | -0.6% | National, accelerating in non-metropolitan prefectures, 45 of 47 prefectures declined in the 2025 census | Long term (≥ 4 years) |

| Barrier And Repulpability Trade-Off In Grease And Liquid Uses | -0.5% | National, particularly affecting food service and liquid packaging converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Virgin Pulp And Energy Cost Volatility

Virgin pulp and energy remain the most immediate cost risk in the Japan cartonboard market because many producers are exposed to imported fiber and volatile utility costs at the same time. That pressure became harder to manage in 2026 when the naphtha disruption raised the cost burden not only on plastics, but also on coatings and adhesives used in barrier board structures. The result is a margin squeeze that large integrated groups can absorb more easily than smaller converters, since the former have stronger procurement, broader product portfolios, and better internal pricing leverage. This uneven pressure is already supporting a more selective investment environment, where spending goes first to energy efficiency, process stability, and high-value grades rather than to broad-based capacity expansion in the Japan cartonboard market. Mid-tier operators are therefore under the greatest strain, because they face the same sustainability and upgrading demands as larger players without matching balance-sheet strength or sourcing flexibility.

Flexible Pouch Substitution In Snacks And Convenience Formats

Flexible pouches still limit the substitution runway for the Japan cartonboard market in snacks and convenience foods because they offer lower weight and strong barrier performance in small-serve formats. This matters most in categories such as chips, instant foods, seasoning sachets, and impulse confectionery, where logistics efficiency and price sensitivity remain central purchase factors. Consumer cost-saving behavior strengthened in 2025 as food prices rose, and that created a better environment for low-ticket, single-serve packaging formats that pouches serve well. The competitive response for cartonboard is not to match pouch economics on material cost, but to defend positions where shape retention, premium presentation, and better print communication support higher value realization. That leaves the Japan cartonboard market with strong opportunities in gifting, meal kits, healthcare, and premium food packs, but it also sets a clear ceiling on displacement within convenience-led snack packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Anchors Value And Recycled Grades Accelerate

Folding boxboard retained 38.13% of the Japan cartonboard market share in 2025, which kept it as the leading product grade across food, cosmetics, and pharmaceutical cartons. Its lead comes from the combination of brightness, print consistency, and converting reliability that brand owners need in primary cartons with tight quality tolerances. That position is especially important in the Japan cartonboard market because higher-value end uses are demanding more than basic stiffness, and they increasingly reward boards that combine appearance with functional performance. Solid bleached board also holds a firm place in premium and regulated applications, where food-contact confidence and surface quality remain more important than fiber-cost efficiency. Solid unbleached board stays relevant in beverage multipacks and quick-service formats, where structural strength matters more than a bright outer appearance.

White-lined chipboard is forecast to expand at a 7.26% CAGR through 2031, making it the fastest-growing product grade in the Japan cartonboard market. Its appeal comes from recycled-fiber content, fit with retail-ready packaging, and acceptable print performance for e-commerce and private-label applications that do not require the highest optical finish. Food service board is also gaining from the shift away from single-use plastics, and Oji's recycling work with quick-service restaurant partners shows how circular infrastructure can reinforce future board demand beyond the initial sale of the pack. Liquid packaging board is moving into a broader role as domestic players develop short-run paper beverage formats, and TOPPAN's Cartocan launch in May 2026 is an example of that push into customized fiber-based liquid packs. The Japan cartonboard industry is therefore seeing product-grade boundaries soften, because barrier coatings and customized structures are allowing grades once tied to narrow end uses to serve a wider set of retail and food-service needs.

By Packaging Format: Folding Cartons Dominate And Liquid Formats Gain Speed

Folding cartons represented 50.50% of the Japan cartonboard market size in 2025, confirming that they remain the default rigid format across food, healthcare, and personal care. Their lead rests on format flexibility, machine compatibility, and the ability to shift from simple shelf packs to premium decorated packs without changing the base material family. This keeps the Japan cartonboard market heavily tied to folding cartons even as other fiber-based formats gain attention, because no alternative format matches the same balance of display value and operational familiarity. Sleeve and tray formats continue to hold a stable role in retail-ready display and premium confectionery presentation, especially where visibility and structural neatness matter at the point of sale. Other cartonboard formats, including paper cups and food-service containers, are also gaining ground as commercial operators reduce plastic use and look for disposables that fit recycling narratives.

Liquid packaging is projected to grow at a 6.34% CAGR through 2031, making it the fastest-growing packaging format in the Japan cartonboard market. A key part of that growth comes from efforts to localize liquid carton capabilities, since imported high-specification board has become less attractive under a weak yen and supply risk. At the same time, format lines are becoming less rigid, because digitally printed paper beverage containers now sit between conventional folding cartons and classic liquid cartons in both use case and customer appeal. TOPPAN's Cartocan service reflects that shift by offering small-lot custom runs for corporate and institutional buyers who want branded fiber beverage packs without the scale demands of traditional aseptic formats. The Japan cartonboard industry is therefore widening its addressable packaging space, not by replacing every flexible or plastic format, but by opening targeted liquid and food-service applications where board now meets both functional and branding requirements.

By End-User Industry: Food Anchors Share And Health And Lifestyle Uses Add Depth

Food accounted for 29.32% of the Japan cartonboard market size in 2025 and is forecast to grow at a 7.18% CAGR through 2031, which makes it both the largest and fastest-growing end-user segment. That combination matters because it gives the Japan cartonboard market one clear demand center where scale, replenishment frequency, and product innovation all operate together. Dense convenience retail, ready-meal formats, snack premiumization, and refrigerated pack upgrades continue to support food-related board consumption even while broader demographic trends reduce volume growth in some categories. Beverage remains the second-largest end-user block, supported by demand from ready-to-drink coffee, juice, dairy multipacks, and emerging fiber-based liquid packaging formats. Together, food and beverage keep the Japan cartonboard market closely tied to recurring consumer-pack purchases rather than to irregular industrial cycles.

Pharmaceutical and healthcare cartons form one of the steadiest demand pillars because aging-related product use supports repeat demand for high-specification packs with safety and accessibility features. Cosmetics and toiletries also contribute strongly to value growth, since premium brands continue to invest in decorative packs and material upgrades that present sustainability without giving up shelf appeal. TOPPAN's PAPER JAR is a useful example of how the Japan cartonboard market is extending beyond outer cartons and into more visible primary-pack roles in beauty and personal care. Tobacco is moving in the opposite direction, as lower smoking prevalence and weaker category momentum reduce its contribution to premium cartonboard demand. Other end users, including toys, apparel, household goods, electrical products, and food service, give the Japan cartonboard market a wider demand base that helps steady utilization when food or personal care growth becomes uneven.

Geography Analysis

The Japan cartonboard market size is expected to increase from USD 4.83 billion in 2026 to USD 6.39 billion by 2031, which shows that value growth continues even in a country with a shrinking broader paper base. Japan's total paper and paperboard demand fell below 20 million tons for the first time since tracking began in 1988, and packaging paper shipments were expected to decline 1.0% year over year to 11.96 million tons in the 2026 domestic outlook. That backdrop matters because the Japan cartonboard market is expanding inside a national paper system that is losing volume, which raises the importance of higher-value grades and better revenue per ton. Production is centered in major industrial prefectures across Honshu, especially Shizuoka, Ehime, Yamaguchi, and Okayama, where integrated mill infrastructure supports most domestic converting supply. This industrial geography keeps the Japan cartonboard market closely linked to regions that combine mill assets, logistics access, and dense downstream manufacturing demand.

Demand concentration follows Japan's population and consumption patterns with growing precision. The Tokyo metropolitan area accounted for 30.1% of Japan's 123.05 million population in the 2025 national census, which gives Kanto a clear lead in packaged goods throughput and retail density. Kansai and Chubu remain the next key corridors, because Osaka-Kobe-Kyoto and Nagoya anchor large consumer markets, regional distribution, and major brand-owner activity. This concentration supports the Japan cartonboard market by improving delivery economics for converters that serve convenience retail, foodservice chains, and fast-moving consumer goods manufacturers. It also makes rural demand softness more visible, since only Tokyo and Okinawa recorded population growth while 45 of 47 prefectures posted declines in the 2025 census.

Import and export flows add another layer to the geography of the Japan cartonboard market. Premium bleached grades and specialized liquid packaging boards have long depended partly on imports, which leaves buyers exposed to currency shifts and supply disruptions when local alternatives are limited. That pressure is now creating stronger incentives for domestic investment in barrier performance, higher-end coatings, and liquid board capability so that more value can stay inside Japan. At the same time, leading domestic groups are pursuing overseas packaging growth to offset soft local volume conditions, and Rengo's Vision120 plan named overseas expansion as a strategic pillar through FY2029. The result is a Japan cartonboard market that is nationally concentrated, metro-driven on demand, and increasingly international in how its top companies think about capacity, sourcing, and long-run growth.

Competitive Landscape

The Japan cartonboard market is moderately consolidated at the mill level, where a small group of integrated paper companies controls much of domestic board capacity, but competition remains more dispersed at the converter level. That structure gives large producers advantages in procurement, fiber sourcing, and plant utilization, while still leaving room for active competition in service speed, print quality, and customer responsiveness. Oji has been using its Renewa recycling platform to connect paper cup collection with broader circular packaging programs, which shows that infrastructure building is becoming part of competitive positioning rather than a narrow compliance task.[3]Japan Times ESG Consortium, “To Realize A Circular Economy, Oji Advances Recycling, Partnerships,” Japan Times, japantimes.co.jp Rengo also showed relative resilience in FY2026, as its Paperboard and Paper Processing segment recorded JPY 397,163 million, or USD 2.65 billion, in net sales and grew 1.1% year over year despite a tight cost environment. Those results suggest that scale alone is not the only advantage in the Japan cartonboard market, because price discipline and portfolio mix still matter when demand growth and input inflation move in opposite directions.

Below the top tier, the field is much broader and more regional. Converters such as TOMOKU, THE PACK CORPORATION, Tokan Kogyo, and Kanae compete through location, lead times, design support, and niche format capability rather than through large domestic board output. This creates a two-layer competitive pattern in the Japan cartonboard market, where mills compete on capacity, specialization, and cost pass-through, while converters compete on execution and account service. Pricing power stays limited because flexible-pouch suppliers still hold a cost advantage in some convenience categories, and imported grades remain available in parts of the premium board range. That mix keeps the Japan cartonboard market active and disciplined, because even leading domestic players cannot rely on concentration alone to defend margins or win new business.

Strategic differentiation is increasingly centered on recyclability, barrier performance, and short-run customization. TOPPAN's PAPER JAR showed one route, by combining more than 50% paper content with oxygen and moisture protection for premium personal care applications. TOPPAN's Cartocan launch showed another route, by using digital printing and small-lot production to create a more flexible entry point into fiber-based liquid packaging. In practice, the strongest players in the Japan cartonboard market are likely to be those that pair integrated supply and converting scale with solutions that remove plastic layers, shorten print runs, and fit Japan's stricter circular packaging expectations.[4]TOPPAN Holdings Inc., “TOPPAN Begins Providing Cartocan With Custom Corporate Designs,” TOPPAN Holdings, holdings.toppan.com

Japan Cartonboard Industry Leaders

Rengo Co., Ltd.

Oji Holdings Corporation

Nippon Paper Industries Co., Ltd.

TOPPAN Inc.

Dai Nippon Printing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: TOPPAN commenced Japan's first mass production of electron beam, EB, offset-printed flexible packaging, combining low-energy-curing technology with solvent-free ink chemistry. The company is targeting JPY 3 billion in related orders by FY2028 and plans to expand the format into toiletry liquid packaging applications.

- May 2026: TOPPAN launched a custom-design Cartocan paper beverage carton service for corporate and institutional buyers, leveraging digital printing to support small-lot production runs. The company is targeting over 20 million units sold annually by 2030, positioning fiber-based beverage cartons as promotional and sustainability-aligned alternatives to single-use plastic bottles.

- May 2026: Dai Nippon Printing received ISCC PLUS certification for sterile flexible packaging manufacturing at its Izumizaki Plant, using mass balance-attributed renewable feedstocks supplied via DuPont's Tyvek platform. The certification positions DNP as a supplier of bio-attributed sterile packaging for pharmaceutical and healthcare customers seeking supply chain decarbonization.

Japan Cartonboard Market Report Scope

The Japan Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Japan Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast size of the Japan cartonboard market?

The Japan cartonboard market was valued at USD 4.55 billion in 2025, is expected to reach USD 4.83 billion in 2026, and is projected to reach USD 6.39 billion by 2031 at a 5.76% CAGR.

Which product grade leads demand in Japan?

Folding boxboard led the product-grade mix with a 38.13% revenue share in 2025 because it serves food, cosmetics, and pharmaceutical cartons that require strong print quality and consistent converting performance.

Which packaging format is growing fastest through 2031?

Liquid packaging is the fastest-growing format, with a 6.34% CAGR through 2031, supported by domestic localization efforts and stronger interest in customized fiber beverage packs.

Which end-user segment is strongest for cartonboard consumption?

Food is both the largest and fastest-growing end-user segment, with a 29.32% revenue share in 2025 and a 7.18% CAGR through 2031.

What is driving material substitution from plastic to cartonboard in Japan?

Stronger recycling and plastic-reduction rules, along with the 2026 naphtha supply disruption, are pushing retailers and converters to move more FMCG packaging toward fiber-based formats.

What are the biggest risks facing suppliers and converters?

The main risks are pulp and energy cost volatility, population decline in many prefectures, and continued pouch competition in snack and convenience formats where cost and weight remain critical.

Page last updated on: