Memory Subsystem For GPUs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.76 Billion |

| Market Size (2031) | USD 27.89 Billion |

| Growth Rate (2026 - 2031) | 20.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Memory Subsystem For GPUs Market Analysis by Mordor Intelligence

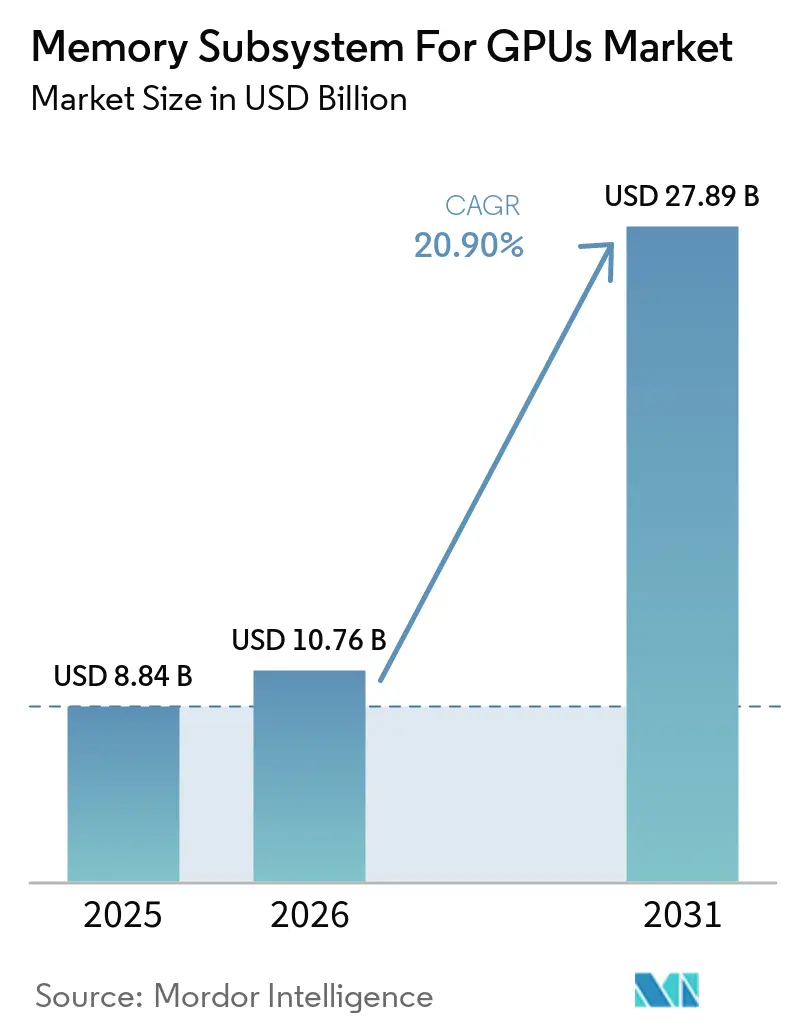

The memory subsystem for GPUs market size is projected to expand from USD 8.84 billion in 2025 and USD 10.76 billion in 2026 to USD 27.89 billion by 2031, registering a CAGR of 20.90% between 2026 to 2031. The memory subsystem for GPUs market is rising because memory content per accelerator is moving higher with every new AI platform generation, which is lifting revenue even when GPU socket growth alone does not explain the full increase. The memory subsystem for GPUs market is also being shaped by a supply chain where memory packaging and high-end DRAM availability remain the main near-term constraints, which keeps pricing firm across premium deployments. Export controls are redirecting advanced memory demand toward allied markets and are changing where high-bandwidth systems are deployed, which gives North America, Europe, Japan, South Korea, and India a clearer role in future demand formation. Competitive positioning is moving beyond unit supply and toward deeper design alignment between GPU vendors and memory suppliers, which raises switching costs and shortens qualification cycles. The strongest opportunities in the memory subsystem for GPUs market sit in AI accelerators, edge inference platforms, advanced packaging, and high-density memory designs that improve bandwidth within tighter power and space limits.

Key Report Takeaways

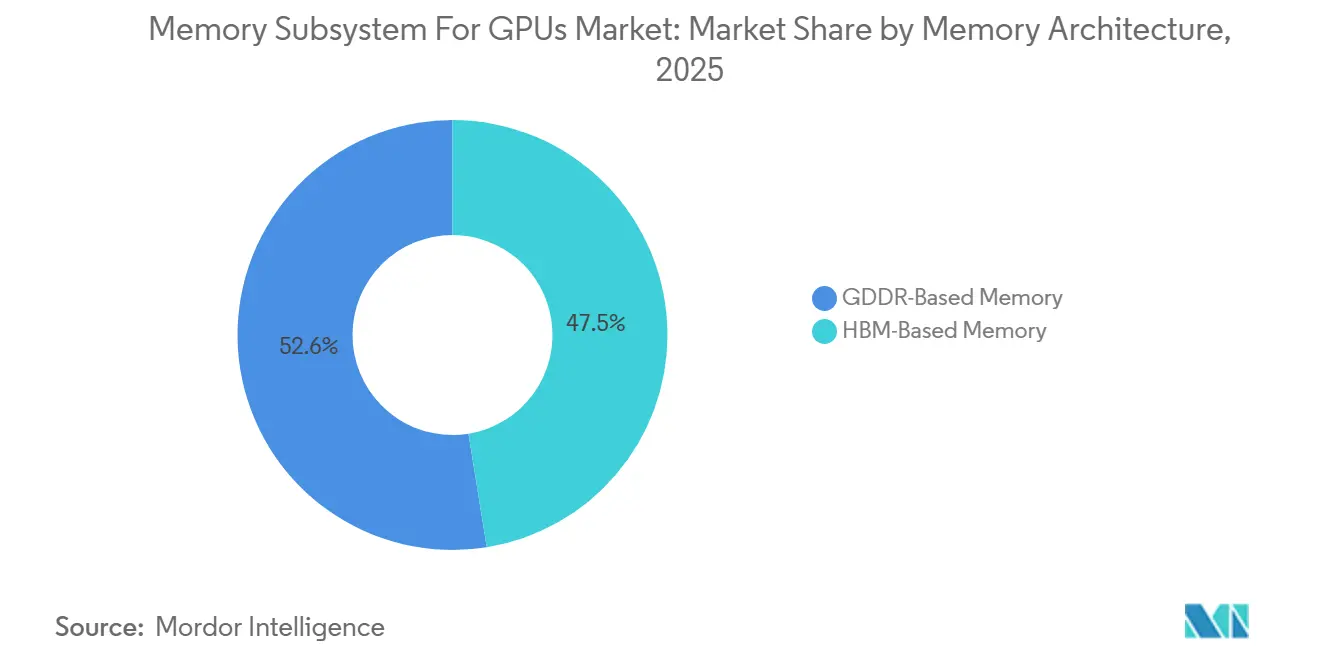

- By memory architecture, GDDR-Based Memory held 52.55% of the memory subsystem for GPUs market in 2025, while HBM-Based Memory is projected to expand at a 21.52% CAGR through 2031.

- By memory capacity, the 16 GB to 32 GB tier accounted for 28.33% of the memory subsystem for GPUs market in 2025, while Above 64 GB is expected to record the highest CAGR of 21.46% through 2031.

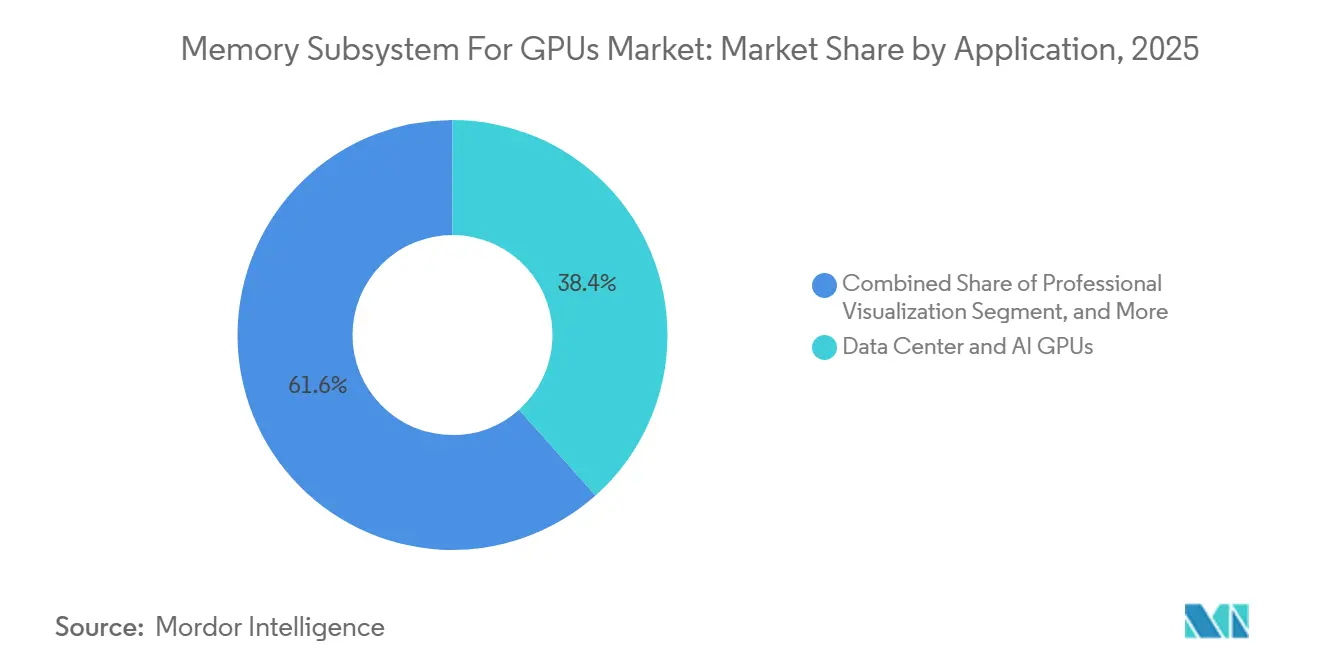

- By application, Data Center and AI GPUs represented 38.42% of the memory subsystem for GPUs market in 2025, while Edge AI and Embedded is projected to grow at a 21.35% CAGR through 2031.

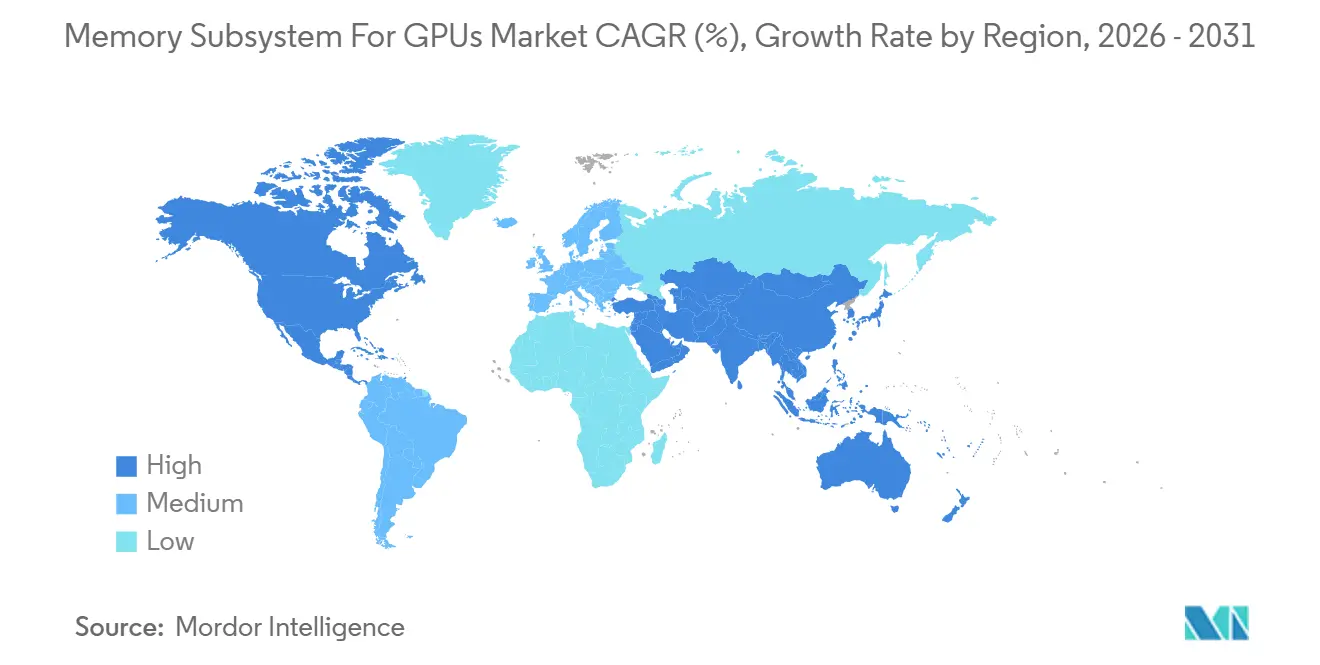

- By geography, Asia-Pacific held 42.44% of the memory subsystem for GPUs market in 2025 and is projected to advance at a 21.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Memory Subsystem For GPUs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Accelerator Memory Density Requirements | +5.5% | Global, concentrated demand in North America and Asia-Pacific, especially Taiwan and South Korea | Short term (≤ 2 years) |

| Transition From GDDR to HBM in Premium GPU Platforms | +4.6% | Global, strongest in North America and East Asia where AI data center build-out is fastest | Medium term (2-4 years) |

| Rapid Adoption of GDDR7 in Gaming and Creator GPUs | +3.4% | Global, with core demand in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Co-Design Between GPU Vendors and Memory Suppliers | +2.6% | North America and East Asia, especially South Korea, Japan, and Taiwan | Long term (≥ 4 years) |

| Export-Control-Driven Supply Reallocation to Friendly Markets | +1.9% | North America, Europe, Japan, South Korea, and India | Medium term (2-4 years) |

| On-Package and Chiplet Integration Improving Bandwidth Per Watt | +1.5% | Global, with innovation hubs in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI Accelerator Memory Density Requirements

The memory subsystem for GPUs market is moving higher because the amount of memory attached to each accelerator is rising faster than overall unit shipments. Higher memory density is now a basic requirement for AI training and large-scale inference platforms, so suppliers have to redesign stack counts, thermal behavior, and packaging flow more often than before. This shift matters because revenue per GPU deployment rises when the same system footprint carries more memory content. The market also benefits from the fact that memory bandwidth and memory capacity now influence accelerator usefulness as much as core compute performance. That makes premium memory less optional and more central to platform qualification across hyperscaler and enterprise buying programs. As a result, the memory subsystem for GPUs market is benefiting from a demand pattern that is tied to system specification depth, not only to shipment volume.

Transition From GDDR to HBM in Premium GPU Platforms

The memory subsystem for GPUs market is also being lifted by the move from GDDR toward HBM in the highest-performance GPU platforms. HBM requires a more involved integration process, which links memory supply more tightly with advanced packaging and GPU die assembly. Samsung stated that its next-generation HBM4 uses a 1c-class DRAM process and a 4 nm logic base die, with speeds up to 13 Gbps and bandwidth up to 3.3 TB/s, which shows how far premium memory requirements have moved beyond earlier graphics DRAM norms.[1]Samsung Electronics, “Samsung and AMD Expand Strategic Collaboration on Next-Generation AI Memory Solutions,” Samsung Global Newsroom This migration supports the memory subsystem for GPUs market because every transition to HBM raises the technical value of memory content within the total GPU bill of materials. It also narrows the field of suppliers that can serve premium platforms at scale. Over time, that makes the memory subsystem for GPUs market more dependent on high-end process execution and less dependent on commodity memory economics.

Rapid Adoption of GDDR7 in Gaming and Creator GPUs

The memory subsystem for GPUs market continues to draw support from GDDR7 adoption in gaming, workstation, and creator systems. GDDR7 remains the practical option for a large installed base that needs high bandwidth without the full packaging cost of HBM. ADLINK launched MXM modules powered by NVIDIA Blackwell with GDDR7, delivering up to 896 GB/s bandwidth at 24 GB capacity for edge AI use cases, which shows that GDDR7 is spreading beyond consumer graphics and into embedded deployments.[2]ADLINK Technology, “ADLINK Launches MXM Modules Powered by NVIDIA Blackwell, Empowering Edge AI with High-Performance GPU Solutions,” ADLINK Technology Newsroom That broadens the memory subsystem for GPUs market because one architecture can now serve gaming, professional visualization, and some edge AI designs at the same time. The result is a wider addressable base for advanced graphics memory even when the fastest AI training systems remain centered on HBM. This is why the memory subsystem for GPUs market still relies on GDDR-based platforms for volume, even while HBM captures more value at the top end.

Co-Design Between GPU Vendors and Memory Suppliers

The memory subsystem for GPUs market is becoming more relationship-driven as GPU vendors and memory suppliers move into deeper co-development arrangements. NVIDIA and SK hynix announced a multiyear technology partnership in June 2026 to co-develop memory for Vera Rubin AI supercomputers, RTX Spark-powered personal AI computers, and Jetson Thor robotics systems. Samsung and AMD also expanded their strategic collaboration in March 2026, with Samsung designated as the primary HBM4 supplier for the AMD Instinct MI455X GPU. These agreements matter because they cut qualification friction and align memory design choices earlier in the product cycle. They also make it harder for smaller suppliers to enter the memory subsystem for GPUs market on specification alone. In practice, the memory subsystem for GPUs market is shifting toward partnerships where design access, qualification trust, and supply continuity matter as much as raw manufacturing scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HBM Packaging Capacity Constraints | -3.2% | Global, concentrated in South Korea and Taiwan through CoWoS-class packaging | Short term (≤ 2 years) |

| High Cost Premium Versus Conventional Graphics DRAM | -2.3% | Global, with sharper pressure in price-sensitive markets across South America, Southeast Asia, and Middle East and Africa | Medium term (2-4 years) |

| Qualification Complexity Across GPU and Memory Generations | -1.4% | Global, with longer certification cycles in North America and East Asia | Medium term (2-4 years) |

| Power and Thermal Limits in Compact GPU Designs | -0.8% | Global, most limiting in mobile and edge AI form factors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HBM Packaging Capacity Constraints

The main near-term restraint on the memory subsystem for GPUs market is not end demand but the difficulty of packaging high-bandwidth memory at scale. HBM output depends on advanced assembly steps that are more complex than standard graphics DRAM integration, so production cannot expand as quickly as demand for AI accelerators. This bottleneck affects the full memory subsystem for GPUs market because GPU shipments cannot fully convert into revenue when memory packaging remains tight. It also reinforces supplier pricing power, since available premium memory must be directed toward the highest-value programs first. The constraint is especially important in AI hardware because performance-class systems cannot easily substitute lower-end memory once a platform is designed around HBM. Until advanced packaging capacity broadens in a meaningful way, the memory subsystem for GPUs market will continue to face a ceiling that is created by supply execution rather than weak procurement interest.

High Cost Premium Versus Conventional Graphics DRAM

The memory subsystem for GPUs market also faces a restraint from the large cost gap between HBM and conventional graphics DRAM. HBM serves workloads that can justify higher bandwidth density and stronger power efficiency, but that same cost profile limits adoption in more price-sensitive platforms. This creates a split market where premium AI systems absorb expensive memory while gaming and mid-range professional systems remain anchored to GDDR. The divide keeps the memory subsystem for GPUs market from moving entirely toward HBM even though top-end performance demand is strong. It also means suppliers have to balance value capture in AI systems with broader volume participation in cost-sensitive categories. For much of the forecast period, the memory subsystem for GPUs market will remain a dual-architecture space because price discipline matters as much as technical capability below the highest-value segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Architecture: HBM Redefines Performance Benchmarks in AI Platforms

GDDR-Based Memory held 52.55% of the memory subsystem for GPUs market share in 2025, which shows how strongly the installed base still supports conventional graphics DRAM. The segment remained the larger revenue contributor because gaming, creator, and professional visualization systems continue to rely on GDDR6 and GDDR7 for balanced cost and bandwidth. In the memory subsystem for GPUs market, GDDR also benefits from simpler board-level integration and wider use across mainstream and performance consumer designs. That installed base gives the segment durability even as AI hardware spending shifts toward denser memory formats. The memory subsystem for GPUs industry still depends on GDDR for scale because many applications do not need HBM-class packaging or cost intensity.

HBM-Based Memory is projected to record a 21.52% CAGR through 2031, which makes it the fastest-growing architecture in the memory subsystem for GPUs market size discussion. Growth is tied to AI accelerators where memory bandwidth and memory density directly shape usable compute throughput. Samsung said its HBM4 platform reaches up to 13 Gbps and 3.3 TB/s, which reflects the performance step that premium GPU programs now require. NVIDIA and SK hynix also moved into multiyear co-development for next-generation AI memory, which supports the view that HBM will remain central to premium accelerator roadmaps.[3]NVIDIA Corporation, “NVIDIA and SK Hynix Announce Multiyear Technology Partnership to Advance Memory for AI Factories,” NVIDIA Newsroom As more top-end platforms are designed around this memory class, the memory subsystem for GPUs market is likely to see HBM capture a larger share of value even if GDDR continues to lead in unit-driven categories.

By Memory Capacity: Density Escalation Tracks AI Model Parameter Growth

The 16 GB to 32 GB tier accounted for 28.33% of the memory subsystem for GPUs market size in 2025, which reflects its strong fit with gaming and mid-range professional GPU deployments. This range remains practical for a large installed base because it meets common performance needs without the full cost burden of high-capacity premium memory. In the memory subsystem for GPUs market, that balance supports consistent demand from users who need capable graphics and workstation performance within tighter budget limits. The range also remains relevant because GDDR7 can stretch performance further before buyers need to move into more expensive architectures. For a large part of the memory subsystem for GPUs industry, this tier remains the commercial middle ground.

Above 64 GB is projected to grow at a 21.46% CAGR through 2031, making it the fastest-rising capacity band in the memory subsystem for GPUs market. The shift is tied to AI platforms where larger models and heavier inference loads make on-package memory capacity more valuable. NVIDIA Blackwell platforms and similar accelerators have pushed expectations higher for how much memory premium systems should carry, which is moving the market toward denser configurations over time. At the same time, the 32 GB to 64 GB band remains an important transition zone where high-density GDDR7 can still compete with lower-stack HBM in some professional and workstation designs. The 8 GB to 16 GB and up to 8 GB tiers continue to serve entry-level and cost-sensitive products, but the strongest long-range value expansion in the memory subsystem for GPUs market is concentrated in the highest-capacity end.

By Application: Data Centers Lead in Value, Edge AI Commands the Growth Rate

Data Center and AI GPUs represented 38.42% of the memory subsystem for GPUs market in 2025, which made them the largest application by revenue. This lead comes from the fact that hyperscalers and enterprise AI buyers prioritize bandwidth density, memory capacity, and system throughput over the lowest possible component cost. In the memory subsystem for GPUs market, data center deployments therefore create a stronger revenue contribution per unit than gaming systems do. These platforms also favor HBM because they are built around AI training and large inference tasks where bandwidth pressure is constant. That is why the memory subsystem for GPUs market continues to derive its value center from data center and AI programs even though unit volumes are broader elsewhere.

Edge AI and Embedded is projected to expand at a 21.35% CAGR through 2031, making it the fastest-growing application area in the memory subsystem for GPUs market. Growth is coming from autonomous systems, industrial robots, smart cameras, and connected devices that need meaningful compute performance in smaller power envelopes. ADLINK's Blackwell-based MXM modules with GDDR7 and 24 GB of memory show how advanced graphics memory is being adapted to embedded form factors instead of staying limited to rack-scale infrastructure. Gaming GPUs still represent the largest end-use category by unit volume, while professional visualization remains a focused niche where GDDR7 often delivers a better balance of bandwidth and cost than HBM. This keeps the memory subsystem for GPUs market segmented by workload needs, with each application group favoring the memory architecture that best fits its power, cost, and integration requirements.

Geography Analysis

Asia-Pacific held 42.44% of the memory subsystem for GPUs market share in 2025 and is projected to grow at a 21.56% CAGR through 2031. The region leads because South Korea remains central to advanced DRAM and HBM production, while Taiwan remains critical for the packaging infrastructure that supports high-end GPU memory integration. The memory subsystem for GPUs market in Asia-Pacific also benefits from the close proximity of memory fabrication, packaging, and electronics manufacturing ecosystems. This concentration gives the region a structural edge in both supply responsiveness and technical coordination across the value chain. India and Southeast Asia remain smaller contributors today, but they are gaining relevance as local cloud and AI infrastructure activity expands.

North America is the main consumption center for premium AI memory by value, since the largest hyperscaler and accelerator programs are concentrated there. The memory subsystem for GPUs market in this region is shaped by procurement intensity from AI platform developers and cloud operators that can absorb high-end memory at scale. Export policy is reinforcing this position, since the BIS said advanced computing items tied to China-linked entities continue to require licensing regardless of the recipient's physical location outside those countries. That framework directs more advanced memory deployments toward allied geographies and supports stronger allocation visibility for North American programs. As a result, the memory subsystem for GPUs market in North America is constrained more by available supply than by weak end demand.

Europe remains concentrated in automotive AI, professional computing, and cloud infrastructure use cases where reliable supply and system quality matter. The memory subsystem for GPUs market in Europe benefits from a strong industrial and automotive base, especially where advanced driver assistance and simulation workloads need dependable GPU memory support. South America stays smaller and is led more by consumer graphics demand than by large-scale AI accelerator procurement. Middle East and Africa is still emerging, but sovereign AI programs are starting to generate a clearer path for data center GPU deployments. Together, these regions broaden the demand map for the memory subsystem for GPUs market, even though Asia-Pacific supply leadership and North American AI demand still shape the global balance most strongly.

Competitive Landscape

The memory subsystem for GPUs market is moderately concentrated at the memory manufacturer level and highly concentrated at the advanced packaging level. A small group of suppliers controls commercially viable HBM production, which gives them disproportionate influence over premium AI hardware supply. The memory subsystem for GPUs market also depends on advanced packaging partners that can integrate high-bandwidth memory with leading GPU logic, which adds another layer of concentration. This structure keeps entry barriers high because success depends on process capability, qualification history, and secure access to packaging capacity. It also means competition is not only about price, since suppliers must prove yield quality, long-term roadmap alignment, and delivery reliability.

NVIDIA and SK hynix announced a multiyear technology partnership in June 2026 to co-develop next-generation AI memory across supercomputing, personal AI computing, and robotics platforms. Samsung and AMD expanded their strategic collaboration in March 2026, with Samsung positioned as the primary HBM4 supplier for AMD Instinct MI455X and with broader cooperation around memory for future AI systems. These moves show that the memory subsystem for GPUs market is being shaped by early design alignment rather than simple spot procurement. Samsung's integrated approach across DRAM process, logic base die, and packaging gives it a strong position as platform complexity rises. SK hynix remains well placed through its close relationship with NVIDIA and its focus on high-stack HBM execution. Micron also remains an important competitor because supply tightness creates room for every scaled supplier that can qualify into premium programs.

The memory subsystem for GPUs market still leaves room for supporting players beyond the main DRAM vendors. Interface and controller specialists, along with packaging partners, gain leverage when memory qualification becomes more demanding and platform timelines become tighter. The market also favors companies that can improve die-to-die interconnects, thermal management, and advanced bonding methods, because these capabilities influence how far high-density memory can scale. Over the forecast period, competitive advantage in the memory subsystem for GPUs market will rest on co-design depth, manufacturing consistency, and the ability to move new memory generations into production without long qualification delays. This is why the market remains concentrated but not static, since each major supplier is using partnerships, process integration, and production planning to improve its position.

Memory Subsystem For GPUs Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK hynix announced a multiyear technology partnership to co-develop next-generation AI memory for the Vera Rubin AI supercomputer platform, Vera CPUs, RTX Spark-powered personal AI computers, and Jetson Thor robotic computing systems. The agreement commits both companies to applying AI to semiconductor design workflows, using NVIDIA CUDA-X libraries and NVIDIA PhysicsNeMo to accelerate TCAD simulations and SK hynix fab operations through factory digital twins built on NVIDIA Omniverse, per the NVIDIA Newsroom. This partnership formalizes SK hynix as NVIDIA's primary strategic memory co-development partner for the current and next GPU generation.

- June 2026: Samsung confirmed all three major memory suppliers, Samsung, SK hynix, and Micron, were cleared by NVIDIA for HBM4 supply to the Vera Rubin platform, ending the exclusive supplier phase of the HBM4 transition. Samsung separately confirmed HBM4 sales exceeded USD 1 billion within 4 months of mass production initiation, and Samsung's cumulative HBM4 sales target for year-end 2026 stands at USD 10 billion.

- May 2026: Big Tech hyperscalers extended direct investment proposals to SK hynix, offering to fund production lines at the Yongin semiconductor cluster and co-finance ASML EUV lithography equipment purchases, according to Seoul Economic Daily. SK hynix's total Yongin Y1 fab investment commitment stands at approximately 31 trillion Korean won (USD 22.8 billion), with mass production targeted for early 2027 at an initial capacity of 30,000 wafers per month.

- March 2026: Samsung and AMD signed an MOU expanding their strategic collaboration, designating Samsung as primary HBM4 supplier for the AMD Instinct MI455X GPU. Samsung's HBM4 is built on its 1c-class DRAM process and 4nm logic base die, achieving speeds up to 13 Gbps and a maximum bandwidth of 3.3 TB/s. The agreement also covers DDR5 memory for AMD's 6th Generation EPYC "Venice" processors and explores a foundry partnership for future AMD silicon, per the Samsung Global Newsroom.

Global Memory Subsystem For GPUs Market Report Scope

The Global Memory Subsystem for GPUs Market refers to the industry segment dedicated to the development, integration, and commercialization of advanced memory architectures and subsystems that support Graphics Processing Units (GPUs) in executing high-performance computing tasks.

The Memory Subsystem for GPUs Market Report is Segmented by Memory Architecture (GDDR-Based Memory and HBM-Based Memory), Memory Capacity (Up to 8 GB, 8 GB to 16 GB, 16 GB to 32 GB, 32 GB to 64 GB, and Above 64 GB), Application (Gaming GPUs, Data Center and AI GPUs, Professional Visualization, and Edge AI and Embedded), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| GDDR-Based Memory |

| HBM-Based Memory |

| Up to 8 GB |

| 8 GB to 16 GB |

| 16 GB to 32 GB |

| 32 GB to 64 GB |

| Above 64 GB |

| Gaming GPUs |

| Data Center and AI GPUs |

| Professional Visualization |

| Edge AI and Embedded |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Architecture | GDDR-Based Memory | |

| HBM-Based Memory | ||

| By Memory Capacity | Up to 8 GB | |

| 8 GB to 16 GB | ||

| 16 GB to 32 GB | ||

| 32 GB to 64 GB | ||

| Above 64 GB | ||

| By Application | Gaming GPUs | |

| Data Center and AI GPUs | ||

| Professional Visualization | ||

| Edge AI and Embedded | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the size outlook for the memory subsystem for GPUs space?

The memory subsystem for GPUs market size was USD 8.84 billion in 2025, stands at USD 10.76 billion in 2026, and is forecast to reach USD 27.89 billion by 2031 at a 20.90% CAGR.

Which memory architecture leads revenue today?

GDDR-Based Memory led in 2025 with 52.55% share because gaming, creator, and professional GPU platforms still rely on it for a better cost and integration balance.

Which architecture is growing the fastest through 2031?

HBM-Based Memory is projected to grow the fastest at a 21.52% CAGR as AI accelerators continue to require higher bandwidth and denser memory configurations.

Which application contributes the most value?

Data Center and AI GPUs led with 38.42% share in 2025 because hyperscalers and enterprise AI buyers prioritize memory bandwidth and capacity over lower component cost.

Which region is strongest in this field?

Asia-Pacific held the largest regional share at 42.44% in 2025 and is also forecast to grow the fastest at a 21.56% CAGR due to its concentration in memory production and advanced packaging.

What is the main factor limiting faster expansion?

HBM packaging capacity remains the main brake on growth because premium GPU memory depends on complex advanced packaging that cannot scale as quickly as AI demand.

Page last updated on: