Compute-Memory Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

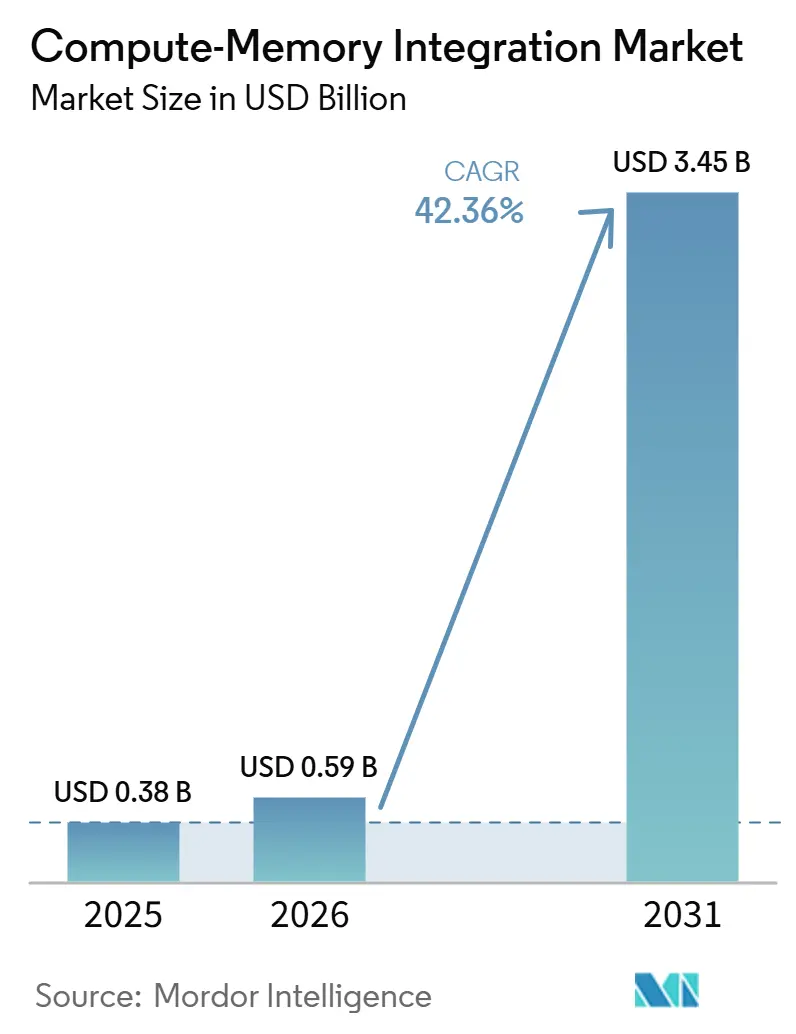

| Market Size (2026) | USD 0.59 Billion |

| Market Size (2031) | USD 3.45 Billion |

| Growth Rate (2026 - 2031) | 42.36% CAGR |

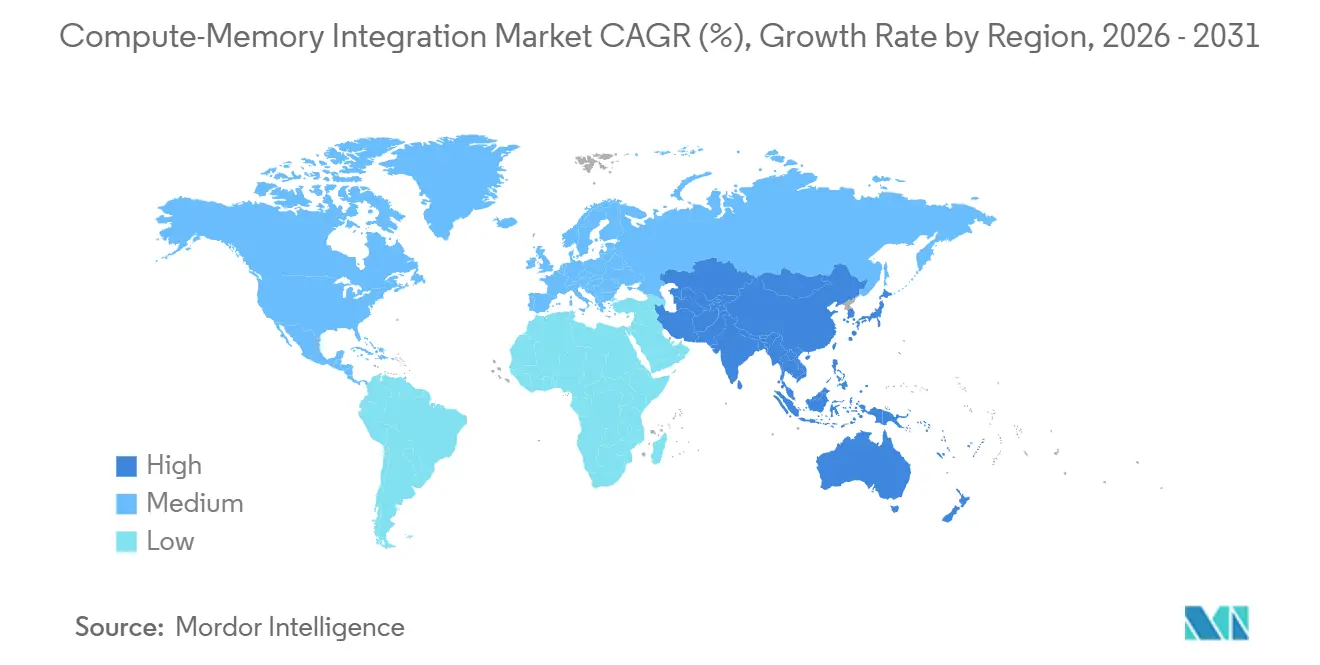

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

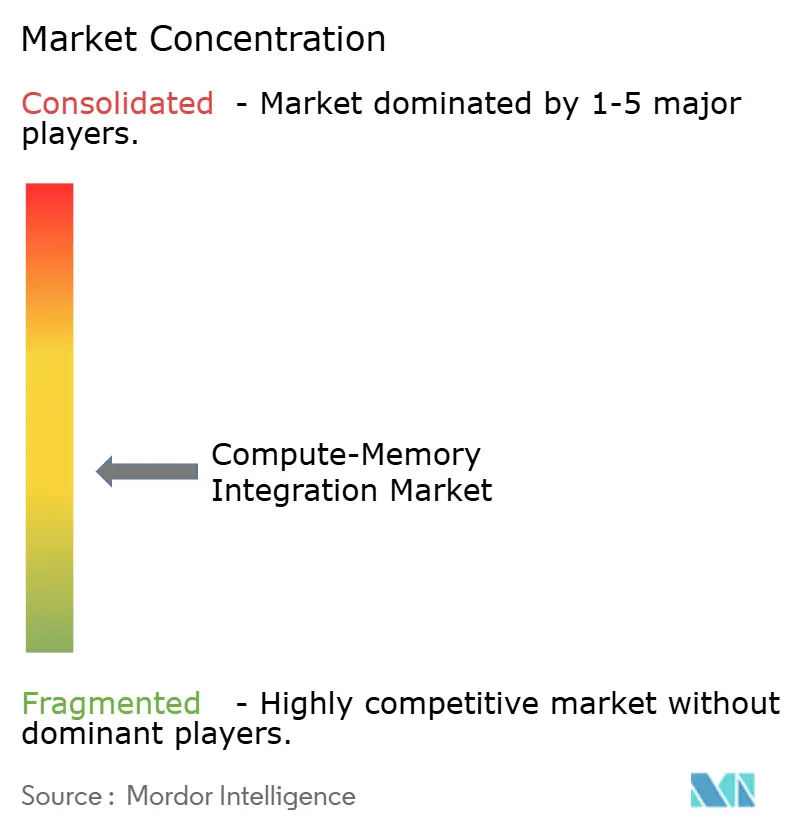

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compute-Memory Integration Market Analysis by Mordor Intelligence

The compute-memory integration market size is projected to be USD 0.38 billion in 2025, USD 0.59 billion in 2026, and reach USD 3.45 billion by 2031, growing at a CAGR of 42.36% from 2026 to 2031. The compute-memory integration market is expanding because conventional processor and memory separation is proving less effective for AI workloads that spend a large share of time and energy moving weights rather than computing on them. The strongest demand is forming where continuous inference must run within strict power limits, which keeps the compute-memory integration market closely tied to edge devices, industrial nodes, and emerging on-device AI use cases. At the same time, the compute-memory integration market is gaining a second demand stream from cloud inference, where memory bandwidth per token is becoming a direct cost issue for hyperscale operators and is pushing attention toward near-memory and in-memory approaches. Competition is split between large memory suppliers that can scale HBM and DRAM-based processing-in-memory at fabrication volume and startups that are pursuing analog and hybrid designs with stronger power efficiency claims. Growth in the compute-memory integration market will depend not only on hardware gains, but also on whether vendors can reduce precision risk, improve yield, and build software flows that are easier for enterprise and automotive buyers to qualify.

Key Report Takeaways

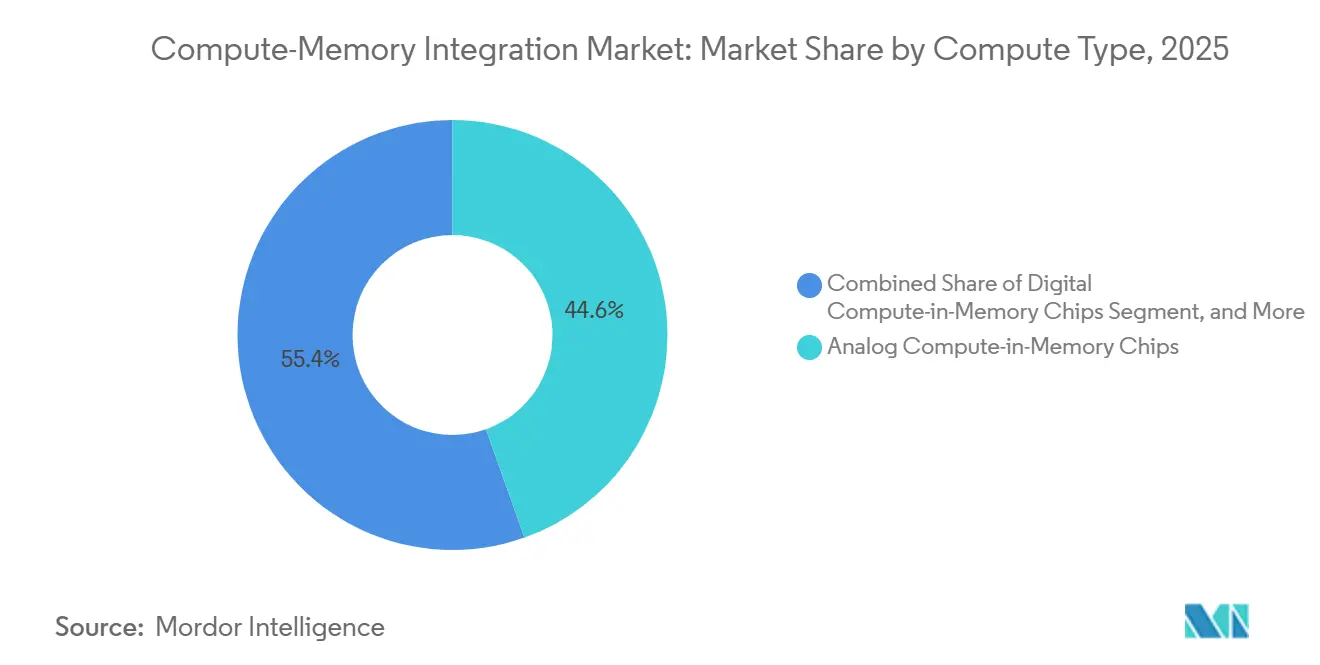

- By compute type, analog compute-in-memory chips held 44.56% share of the compute-memory integration market in 2025, while hybrid compute-in-memory chips are projected to expand at a 42.69% CAGR through 2031.

- By memory technology, flash and charge-based and other compute-in-memory technologies held 42.38% share of the compute-memory integration market in 2025, while DRAM and HBM-based processing-in-memory is projected to expand at a 42.99% CAGR through 2031.

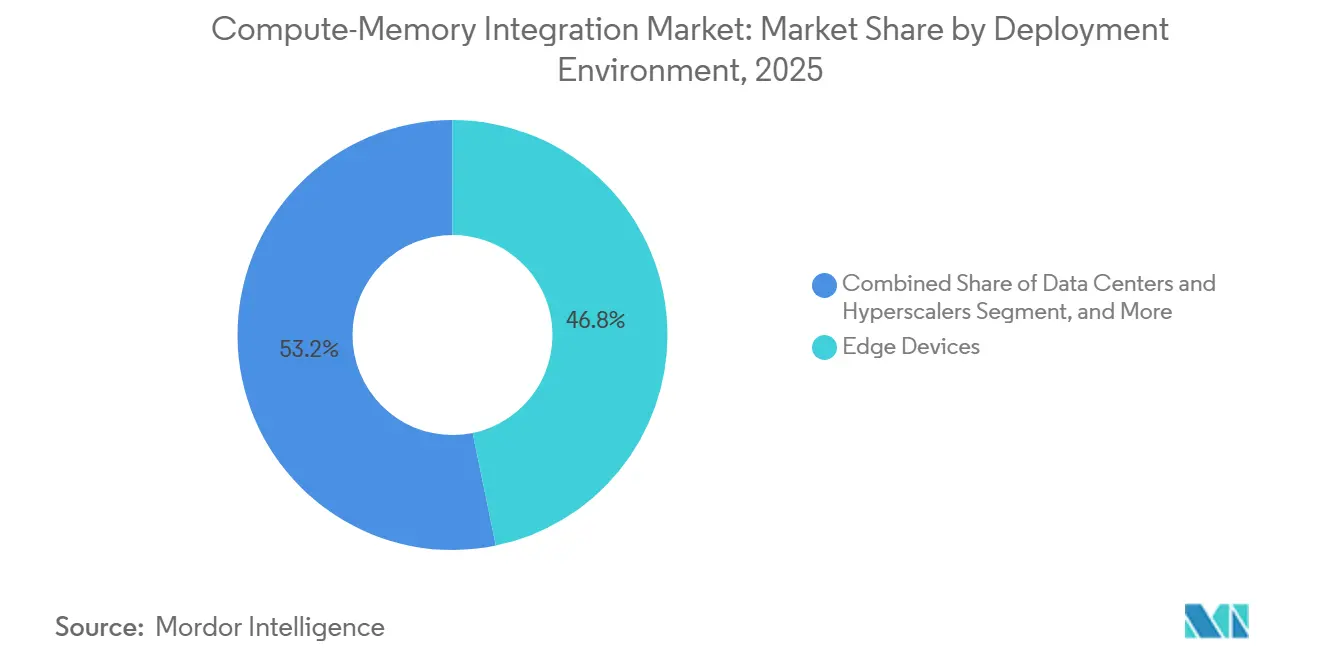

- By deployment environment, edge devices held 46.77% share in 2025, while data centers and hyperscalers are projected to advance at a 50.14% CAGR through 2031.

- By end user, semiconductor companies and chip designers held 27.68% share in 2025, while cloud and hyperscale providers are projected to grow at a 50.36% CAGR through 2031.

- By geography, North America held 66.58% share in 2025, while Asia-Pacific is projected to expand at a 50.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Compute-Memory Integration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy Efficiency Gains in Edge AI and On-Device Inferencing | +8.5% | Global, with early gains in North America and Asia-Pacific core | Short term (≤ 2 years) |

| Memory Wall Pressure From Large Language Model Workloads | +7.2% | Global, hyperscale-intensive in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rise of High Bandwidth Memory and Near-Memory Architectures in AI Servers | +6.1% | North America and Asia-Pacific, with spillover to Europe | Medium term (2-4 years) |

| Custom Silicon Demand for Power-Constrained Autonomous and Industrial Systems | +4.8% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Software Co-Optimization for Quantized AI Inference at the Edge | +3.5% | Global, with early activity in North America and East Asia | Medium term (2-4 years) |

| Compute Density Requirements in Data Centers Facing Power and Cooling Limits | +3.2% | North America and Asia-Pacific data center hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy Efficiency Gains in Edge AI and On-Device Inferencing

The compute-memory integration market is being pulled forward by always-on AI use cases that need continuous operation at the sensor, laptop, and embedded device levels without the thermal budget of conventional accelerators. In these workloads, moving model weights between memory and compute remains the largest energy burden, and compute-in-memory reduces that burden by placing arithmetic closer to where weights are stored. A mixed-precision memristor-SRAM processor published in March 2025 reached 40.91 TFLOPS/W on ResNet-20 with less than 0.45% accuracy degradation, which showed that energy gains do not require a full tradeoff in usable model quality.[1]Win-San Khwa et al., “A Mixed-Precision Memristor and SRAM Compute-in-Memory AI Processor,” Nature, nature.com EnCharge AI stated in February 2025 that its EN100 accelerator targets more than 200 TOPS at under 9W for client and edge inference, which fits the power range that mobile and fanless systems can actually absorb. The compute-memory integration market is therefore benefiting from a practical adoption path, because edge buyers often care more about sustained inference within fixed power envelopes than about peak benchmark throughput. This same pattern is encouraging hybrid designs, since many adopters want analog-class efficiency but still need digital support to keep accuracy stable across production conditions.

Memory Wall Pressure from Large Language Model Workloads

The compute-memory integration market is also advancing because large language model inference is now constrained more by memory movement than by raw arithmetic capacity. During autoregressive decoding, large models repeatedly fetch weights that are used once per token step, which keeps arithmetic intensity low and makes memory bandwidth the limiting factor in latency-sensitive serving. Frontiers in Science described the memory wall in 2025 as a cross-cutting hardware constraint for modern AI systems, which strengthened the architectural case for processing-in-memory beyond a narrow optimization argument.[2]“Breaking the Memory Wall, Next-Generation Artificial Intelligence Hardware,” Frontiers in Science, frontiersin.org Samsung announced in February 2026 that it had begun commercial HBM4 shipment with 3.3TB/s bandwidth per stack and 40% better power efficiency than HBM3E, which shows how memory vendors are responding directly to this bottleneck.[3]Samsung Electronics, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com As a result, the compute-memory integration market is moving from a niche architecture discussion into a broader infrastructure decision around token cost, latency, and system energy. This shift also raises switching costs, because logic-enabled memory products are less interchangeable than earlier commodity memory generations.

Rise of High Bandwidth Memory and Near-Memory Architectures in AI Servers

The compute-memory integration market is gaining server-side momentum as HBM evolves from passive storage into a more active part of AI system design. Large memory suppliers are embedding more logic at or near the memory stack, which lets part of the workload execute closer to the data and reduces traffic across the memory interface. SK hynix announced in June 2026 a multi-year technology partnership with NVIDIA covering next-generation memory for AI factories, which tied future HBM development directly to high-volume AI infrastructure roadmaps. Micron also introduced a 256GB LPDRAM SOCAMM2 module in March 2026 and said it improved time-to-first-token by more than 2.3x for long-context LLM inference while using one-third of the power of equivalent RDIMMs. These moves matter for the compute-memory integration market because they show that near-memory compute is not limited to one memory form factor or one buyer group. They also make leading-edge packaging, logic-based dies, and memory co-design more important to competitive position than they were in earlier AI server cycles.

Custom Silicon Demand For Power-Constrained Autonomous And Industrial Systems

The compute-memory integration market is being shaped by autonomous vehicles, industrial robotics, and always-aware machines that cannot carry the power draw of data center-class inference cards. These systems usually allocate a fixed power budget across sensing, control, connectivity, and safety functions, which leaves limited room for high-watt AI acceleration. Honda stated in February 2026 that it is co-developing an automotive SoC with Mythic and licensed Mythic technology to improve AI computing performance and energy efficiency in vehicles. STMicroelectronics also introduced the Stellar P3E as the first automotive microcontroller with built-in AI acceleration for edge intelligence and said production start was planned for Q4 2026. The compute-memory integration market is gaining credibility from these moves because automotive and industrial buyers do not adopt new architectures quickly unless the power benefit is large enough to justify qualification effort. This is also changing procurement behavior, as some OEMs are starting to work directly with architecture providers rather than waiting for standard digital accelerator roadmaps from established suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Analog Precision Variability and Yield Risk in Compute-In-Memory Designs | -5.8% | Global, most acute in high-volume production environments in Asia-Pacific | Medium term (2-4 years) |

| Immature EDA, Compiler, and Benchmark Ecosystem | -4.2% | Global, most restrictive in enterprise procurement markets in North America and Europe | Medium term (2-4 years) |

| High Integration Cost and Long Qualification Cycles | -3.5% | North America and Europe, especially in automotive and defense adoption timelines | Long term (≥ 4 years) |

| Limited Standardization Across Memory Types, Interfaces, and Programming Models | -2.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Analog Precision Variability And Yield Risk In Compute-In-Memory Designs

The compute-memory integration market still faces a major technical limit in analog precision stability, especially when neural weights are stored as physical conductance states inside non-volatile cells. Process variation, temperature drift, endurance loss, and cell-to-cell spread can all introduce noise into multiply-accumulate operations, and those errors build across deeper neural networks. A 2025 review in npj Unconventional Computing described key analog in-memory error sources and noted that mitigation methods can consume a meaningful share of the energy savings that make the architecture attractive in the first place. An IEEE Transactions on Circuits and Systems I study in 2025 also found that precision limits become restrictive under operating conditions below the peak arithmetic throughput of a 28nm SRAM-based design, which shows that measured silicon behavior can differ sharply from idealized claims. The compute-memory integration market, therefore, continues to favor hybrid architectures in many commercial settings because they preserve part of the analog energy benefit while relying on digital stages to protect output quality. This issue also widens the gap between strong academic prototypes and repeatable high-volume manufacturing, which matters most when the target customer is automotive, defense, or enterprise infrastructure.

Immature EDA, Compiler, and Benchmark Ecosystem

The compute-memory integration market is also slowed by software and design-tool limitations that make deployment harder than the hardware headlines suggest. Most current workflows still require close hardware-software co-design, since analog noise behavior, operator mapping, quantization, and calibration must be handled together rather than through standard accelerator toolchains. Nature Reviews Electrical Engineering noted in 2025 that analog in-memory computing stacks need custom treatment across the software flow, from training-aware quantization to runtime calibration, and that this remains outside mainstream GPU-style ecosystems. SPEC released its CPU 2026 benchmark suite in May 2026, but there is still no broadly adopted independent benchmark family that treats compute-in-memory workloads as a first-class category for buyer evaluation. The compute-memory integration market is affected directly because enterprise procurement teams usually discount vendor claims when they lack neutral benchmarks and mature software support. This burden falls hardest on smaller vendors, since they must explain architecture, calibration, and deployment complexity at the same time they are trying to close their first commercial programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compute Type: Analog Leads Early Revenue While Hybrid Gains The Most Strategic Momentum

Analog compute-in-memory chips held 44.56% of the compute-memory integration market share in 2025, which reflected their earlier commercialization in edge inference and the depth of research around resistive memory-based matrix operations. The market reached this position because analog arrays can execute core operations inside memory cells and avoid much of the data movement that burdens conventional digital accelerators. That advantage is strongest in weight-stationary workloads where power savings matter more than absolute numerical determinism. The analog segment also benefited from the fact that many early adoption cases, such as embedded vision and anomaly detection, can tolerate carefully managed precision tradeoffs if the energy gain is large enough. In that sense, the compute-memory integration market first opened where battery life, thermal design, and sustained local inference mattered more than universal software portability.

Digital compute-in-memory chips continue to hold a complementary role because they offer deterministic behavior and better alignment with established software expectations, even if their energy gain is lower than analog alternatives. This makes digital approaches more suitable where traceability, validation, and numerical repeatability are required by safety or operational rules. Hybrid compute-in-memory chips are projected to grow at a 42.69% CAGR through 2031, and that trajectory shows how the compute-memory integration market is trying to balance analog efficiency with digital control. A mixed-precision processor published in Nature in 2025 demonstrated that partitioning neural layers across memristor, SRAM, and digital units can preserve accuracy while still delivering strong efficiency, which is the same design logic that many hybrid vendors are now following. IBM announced in June 2026 that its NanoStack sub-1nm architecture improved SRAM density by 40% versus 2nm nodes, which supports the longer-term case for denser hybrid macro integration at advanced nodes.

By Memory Technology: Flash And Charge-Based Designs Hold Share While DRAM And HBM-Based PIM Accelerates

Flash, charge-based, and other technologies represented 42.38% of the compute-memory integration market size in 2025, which showed the value of process familiarity and broad manufacturing availability. This group benefits from the reuse of cell structures and fabrication knowledge that were originally built for high-density non-volatile storage and are now being adapted for in-array compute. The compute-memory industry has leaned on these options because they provide a practical bridge between new architecture goals and existing manufacturing habits. SRAM-based compute-in-memory remains important because it has the most transparent public silicon characterization for edge AI and gives developers a clearer view of accuracy, energy, and operating tradeoffs. Its limit is density, since SRAM takes more area per bit and is harder to scale for workloads that require larger on-chip weight storage.

DRAM and HBM-based processing-in-memory is projected to grow at a 42.99% CAGR through 2031, which makes it the fastest-moving memory technology path inside the market. Samsung said in February 2026 that its commercial HBM4 delivered 3.3TB/s per stack with 40% better power efficiency than HBM3E, which reinforces the appeal of memory-centric acceleration in AI infrastructure. SK hynix strengthened the same direction in June 2026 through its multi-year NVIDIA partnership, which linked future HBM roadmaps to AI supercomputers, consumer AI PCs, and robotics platforms. Micron added another signal in March 2026 with its 256GB LPDRAM SOCAMM2 launch, which targeted long-context LLM inference and showed that near-memory ideas are advancing across multiple DRAM categories at once. ReRAM, phase-change memory, and MRAM remain smaller in current revenue, but they retain strategic importance in applications where non-volatility, radiation tolerance, or specialized sensing and safety conditions justify a narrower but higher-value adoption path.

By Deployment Environment: Edge Devices Anchor Current Demand While Data Centers Build The Fastest Growth Runway

Edge devices held 46.77% of deployment-environment revenue in 2025, which gave them the leading position in the compute-memory integration market, as commercial revenue formed first around low-power inference. These applications include embedded vision, keyword recognition, anomaly detection, and predictive maintenance, where local response and tight power budgets matter more than training-scale flexibility. The market found product fit here because analog and hybrid designs have their clearest performance-per-watt edge in sub-10W operating ranges. That helped edge deployments move into revenue before the architecture was mature enough for large-scale server insertion. It also explains why many early compute-memory announcements focused on laptops, embedded devices, robotics modules, and sensor-adjacent systems rather than on mainstream cloud acceleration.

Data centers and hyperscalers are projected to grow at a 50.14% CAGR through 2031, and that rate shows that the compute-memory integration market is no longer defined only by edge use cases. The main driver is the cost and latency burden of memory movement during LLM inference, which pushes operators toward architectures that shorten the distance between weights and execution. Samsung, SK hynix, and Micron have each advanced products that support this shift, including commercial HBM4 and high-capacity LPDRAM modules aimed at AI infrastructure. Automotive, industrial automation, healthcare, defense, and aerospace each remain smaller by revenue today, but they are important because they reward architectures that combine energy efficiency with lifecycle assurance, safety support, or secure local inference. Consumer electronics will likely remain a volume opportunity for the compute-memory integration market only when these capabilities are embedded into merchant silicon at acceptable cost and interface standards.

By End User: Semiconductor Companies Hold The Largest Share While Cloud Providers Change The Demand Profile

Semiconductor companies and chip designers held 27.68% of the compute-memory integration market size in 2025, which reflected their role as the first large buyer group to embed compute-in-memory blocks into future SoC plans. This segment includes fabless AI chip companies, integrated device manufacturers, and design ecosystem players that influence how new memory-compute macros reach production. The market depends heavily on this group because one design decision at the chip level can pull through demand for IP, EDA support, foundry capacity, packaging, and memory co-development. These companies are not only end users, but also channel builders that determine whether compute-in-memory becomes a product feature or remains a narrow architecture experiment. Their early share, therefore, says as much about ecosystem formation as it does about direct silicon consumption.

Cloud and hyperscale providers are projected to expand at a 50.36% CAGR through 2031, which makes them the fastest-growing end-user segment in the compute-memory integration market. Their interest is driven by inference economics, since memory-bandwidth cost per token is becoming more decisive than pure compute cost for large-scale serving. That is why memory suppliers are aligning closely with hyperscale and AI platform roadmaps, as seen in Samsung's HBM4 launch, SK hynix's NVIDIA partnership, and Micron's long-context LPDRAM positioning. Automotive OEMs and Tier-1 suppliers also deserve attention because Honda's direct licensing path with Mythic suggests that some vehicle makers may bypass standard supply chains when energy efficiency becomes a platform differentiator. Government, defense, and research institutions remain smaller in direct revenue, but they continue to influence qualification standards that later shape adoption in more regulated parts of the compute-memory integration market.

Geography Analysis

North America held 66.58% of the compute-memory integration market share in 2025, which reflected the region's concentration of LLM developers, hyperscale operators, and fabless semiconductor designers. The market remained strongest there because architecture development, software optimization, and early commercial buying power are closely linked in the same regional ecosystem. North America also benefits from the presence of vendors across the stack, from startup analog compute firms to large memory and logic companies with advanced packaging ambitions. IBM reinforced this ecosystem in June 2026 when it introduced its NanoStack sub-1nm architecture and highlighted its relevance for future SRAM density and energy efficiency improvements. The region is therefore likely to remain the reference market for early compute-memory product validation, especially where buyers need close interaction between chip design, software, and system integration.

Asia-Pacific is projected to grow at a 50.74% CAGR through 2031, which makes it the fastest-growing regional block in the compute-memory integration market. The region's strength comes from its leadership in advanced memory fabrication, HBM development, and the packaging capabilities that near-memory compute increasingly requires. Samsung's commercial HBM4 shipment and SK hynix's expanded NVIDIA collaboration both showed in 2026 that South Korea remains central to the future supply path for memory-centric AI hardware. China also demonstrated technical momentum through a 2025 Acta Physica Sinica paper on a 3D NAND compute-in-memory architecture for GPT-2-124M inference, which pointed to growing local capability in production-oriented system simulation.

Europe held a smaller share of the market in the current period, but its automotive and industrial demand profile gives it influence beyond its present revenue base. The strongest regional pull is likely to come from applications that need functional safety, long lifecycle support, and energy-efficient local inference, which keeps automotive electronics especially relevant. STMicroelectronics supported that direction with its Stellar P3E introduction for automotive edge intelligence, and Honda's collaboration with Mythic also signaled how vehicle programs can accelerate compute-memory qualification when power efficiency becomes central. South America and the Middle East and Africa remain early-stage areas for the market, and their near-term adoption is more likely to emerge through targeted sovereign AI, defense, and secure on-device inference programs than through broad commercial rollout.

Competitive Landscape

The compute-memory integration market in 2026 remained moderately fragmented at the overall level, but the competitive structure differed sharply by architecture. In HBM and DRAM-based processing-in-memory, the commercial field was much tighter because Samsung Electronics, SK hynix, and Micron were the vendors with the scale, packaging capability, and customer access needed to move logic-enabled memory into production programs. Samsung advanced that position in February 2026 with the start of commercial HBM4 shipment and a claim of 3.3TB/s bandwidth per stack with 40% better power efficiency than HBM3E. SK hynix extended its competitive reach in June 2026 through a multi-year partnership with NVIDIA that covered AI supercomputers, AI PCs, robotics, and internal manufacturing collaboration. Micron also strengthened its position through the 256GB LPDRAM SOCAMM2 launch in March 2026, which showed that near-memory strategies are spreading across a wider memory portfolio and not only through HBM.

The startup field inside the compute-memory integration market remained more open, especially in analog and hybrid designs, where no single player yet controls fabrication scale or software conventions. Mythic, EnCharge AI, TetraMem, Rain AI, and other ventures are competing on power efficiency, workload specialization, and architecture novelty rather than on manufacturing volume alone. EnCharge AI drew attention in February 2025 with a USD 100 million Series B round and a client-focused EN100 accelerator positioned above 200 TOPS and below 9W. Mythic added another strategic signal in February 2026 when Honda licensed its technology for joint development of an automotive-grade analog AI chip, which showed that startups can win direct OEM relationships when their efficiency case is strong enough.

A second layer of competition in the compute-memory integration market sits with firms that shape process, density, and design viability rather than selling the end chip alone. IBM's NanoStack announcement mattered because better SRAM density can improve how future hybrid compute-memory blocks fit into advanced nodes and packaging plans. STMicroelectronics also showed that built-in AI acceleration is moving into automotive microcontroller families, which broadens the set of incumbents that can claim memory-adjacent inference efficiency rather than leaving that theme only to startups. Across the compute-memory integration market, the most durable advantage is likely to come from combining architecture, manufacturability, and software readiness rather than from headline energy claims alone. That is why the market is consolidating faster in memory-centric infrastructure products while remaining more experimental in analog edge and specialized inference segments.

Compute-Memory Integration Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Intel Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SK hynix and NVIDIA announced a multi-year technology partnership on June 8, 2026, covering co-development of next-generation HBM memory for global AI factory infrastructure. The agreement encompasses memory for NVIDIA's Vera Rubin AI supercomputers, RTX Spark consumer AI PCs, and Jetson Thor robotics platforms, and extends to applying AI to SK hynix's chip design and fabrication operations via NVIDIA CUDA-X libraries.

- June 2026: IBM unveiled the world's first sub-1nm NanoStack chip architecture on June 25, 2026, delivering 40% SRAM scaling improvement over 2nm nodes and projecting up to 70% greater energy efficiency than current-generation chips. The NanoStack transistor architecture was presented at VLSI 2026 and positions SRAM-CIM macro density as a direct beneficiary of sub-1nm process scaling.

- March 2026: Micron released the world's first high-capacity 256GB LPDRAM SOCAMM2 on March 3, 2026, delivering more than 2.3x improvement in time-to-first-token for long-context LLM inference and consuming one-third of the power versus equivalent RDIMMs, supporting liquid-cooled server architectures.

- February 2026: Samsung commenced mass production and commercial shipment of HBM4 on February 12, 2026, the industry's first such commercial HBM4 product. The product delivers 3.3TB/s bandwidth per stack, 2.7x the bandwidth of HBM3E, with 40% power efficiency improvement. Samsung projected HBM sales will more than triple in 2026 versus 2025, with HBM4E sampling expected in H2 2026.

Global Compute-Memory Integration Market Report Scope

Compute-Memory Integration Market refers to hardware and system architectures that combine processing and memory functions more closely to reduce data movement between compute units and storage. It covers compute-in-memory and near-memory approaches that improve latency, bandwidth efficiency, and power consumption in data-intensive workloads.

The Compute-Memory Integration Market Report is Segmented by Compute Type (Analog Compute-in-Memory Chips, Digital Compute-in-Memory Chips, and Hybrid Compute-in-Memory Chips), Memory Technology (SRAM-Based, DRAM/HBM-Based PIM, ReRAM-Based, Phase-Change Memory-Based, Magnetoresistive RAM-Based), Deployment Environment (Edge Devices, Data Centers and Hyperscalers, High-Performance Computing, Automotive and Transportation, Industrial Automation and IIoT, Consumer Electronics, Healthcare, and Defense and Aerospace), End User (Semiconductor Companies and Chip Designers, Cloud and Hyperscale Providers, Server and AI Accelerator OEMs, Automotive OEMs and Tier-1 Suppliers, Industrial Automation Providers, and Consumer Electronics OEMs), and Geography (North America, Europe, Asia-Pacific, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD)

| Analog Compute-in-Memory Chips |

| Digital Compute-in-Memory Chips |

| Hybrid Compute-in-Memory Chips |

| SRAM-Based |

| DRAM/HBM-Based PIM |

| ReRAM-Based |

| Phase-Change Memory-Based |

| Magnetoresistive RAM-Based |

| Edge Devices |

| Data Centers and Hyperscalers |

| High-Performance Computing |

| Automotive and Transportation |

| Industrial Automation and IIoT |

| Consumer Electronics |

| Healthcare |

| Defense and Aerospace |

| Semiconductor Companies and Chip Designers |

| Cloud and Hyperscale Providers |

| Server and AI Accelerator OEMs |

| Automotive OEMs and Tier-1 Suppliers |

| Industrial Automation Providers |

| Consumer Electronics OEMs |

| Other End Users (Government, Defense and Research Institutions) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Compute Type | Analog Compute-in-Memory Chips | |

| Digital Compute-in-Memory Chips | ||

| Hybrid Compute-in-Memory Chips | ||

| By Memory Technology | SRAM-Based | |

| DRAM/HBM-Based PIM | ||

| ReRAM-Based | ||

| Phase-Change Memory-Based | ||

| Magnetoresistive RAM-Based | ||

| By Deployment Environment | Edge Devices | |

| Data Centers and Hyperscalers | ||

| High-Performance Computing | ||

| Automotive and Transportation | ||

| Industrial Automation and IIoT | ||

| Consumer Electronics | ||

| Healthcare | ||

| Defense and Aerospace | ||

| By End User | Semiconductor Companies and Chip Designers | |

| Cloud and Hyperscale Providers | ||

| Server and AI Accelerator OEMs | ||

| Automotive OEMs and Tier-1 Suppliers | ||

| Industrial Automation Providers | ||

| Consumer Electronics OEMs | ||

| Other End Users (Government, Defense and Research Institutions) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and future value of the compute-memory integration market?

The compute-memory integration market size is projected at USD 0.38 billion in 2025, USD 0.59 billion in 2026, and USD 3.45 billion by 2031, at a 42.36% CAGR over 2026-2031.

What is driving demand for compute-memory solutions right now?

Demand is rising because AI inference is increasingly limited by memory movement and power use, especially in edge devices and large language model serving.

Which compute type leads today and which one is growing the fastest?

Analog compute-in-memory chips led with 44.56% share in 2025, while hybrid compute-in-memory chips are projected to post the fastest growth at a 42.69% CAGR through 2031.

Which memory technology path is attracting the strongest momentum?

Flash and charge-based technologies held the largest 2025 share, but DRAM and HBM-based processing-in-memory is forecast to grow the fastest at a 42.99% CAGR through 2031.

Why are cloud and hyperscale operators becoming more important buyers?

Cloud and hyperscale providers are projected to grow at a 50.36% CAGR because token-serving economics now depend heavily on memory bandwidth, latency, and energy efficiency.

Which region is strongest today and which one is expanding the fastest?

North America led with 66.58% share in 2025, while Asia-Pacific is projected to record the fastest regional expansion at a 50.74% CAGR through 2031.

Page last updated on: