Memory-Centric Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

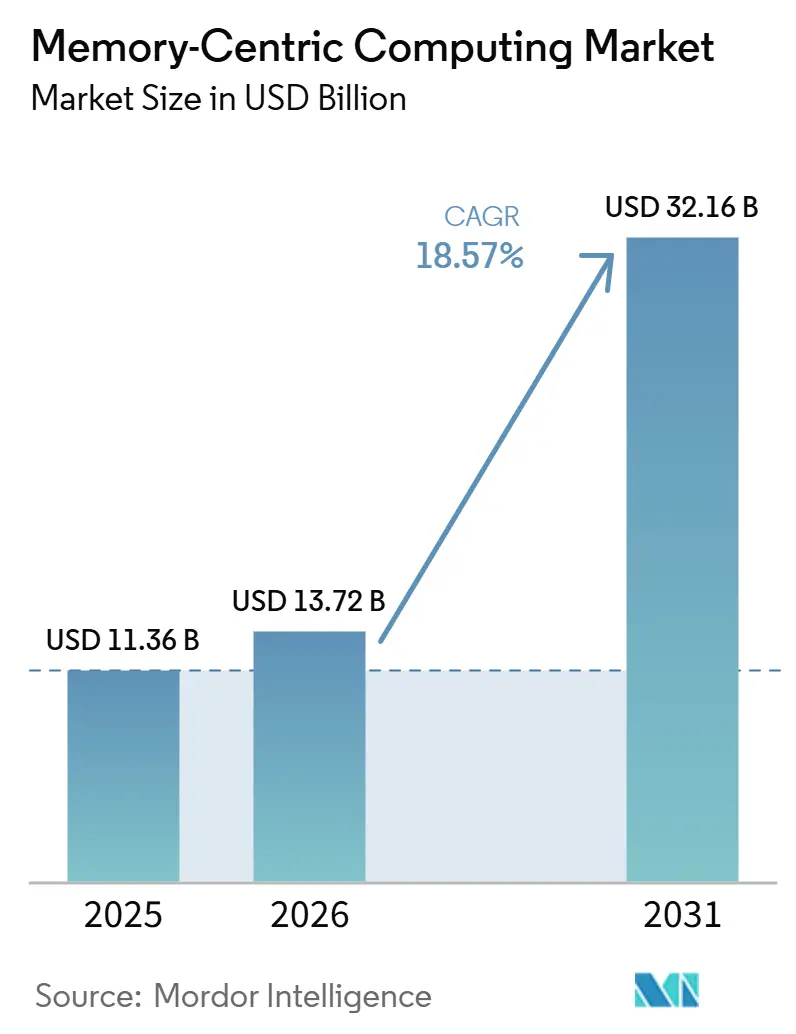

| Market Size (2026) | USD 13.72 Billion |

| Market Size (2031) | USD 32.16 Billion |

| Growth Rate (2026 - 2031) | 18.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Memory-Centric Computing Market Analysis by Mordor Intelligence

The memory-centric computing market size is projected to expand from USD 11.36 billion in 2025 and USD 13.72 billion in 2026 to USD 32.16 billion by 2031, registering a CAGR of 18.57% between 2026 to 2031. The market is moving away from disk-resident architectures because enterprises now need sub-millisecond response times for AI model serving, fraud scoring, and high-frequency analytics. This shift is being reinforced by better commercial readiness for CXL-based memory expansion and by wider enterprise access to managed in-memory services through cloud providers. Buyers are also treating memory-centric platforms less as a niche performance layer and more as a core data foundation for transaction-heavy and stateful workloads. At the same time, procurement cycles remain uneven because large-scale memory fabrics still require costly hardware refreshes and specialized engineering skills. Even with those limits, the memory-centric computing market continues to attract investment because it supports both immediate low-latency use cases and longer-term AI infrastructure modernization.

Key Report Takeaways

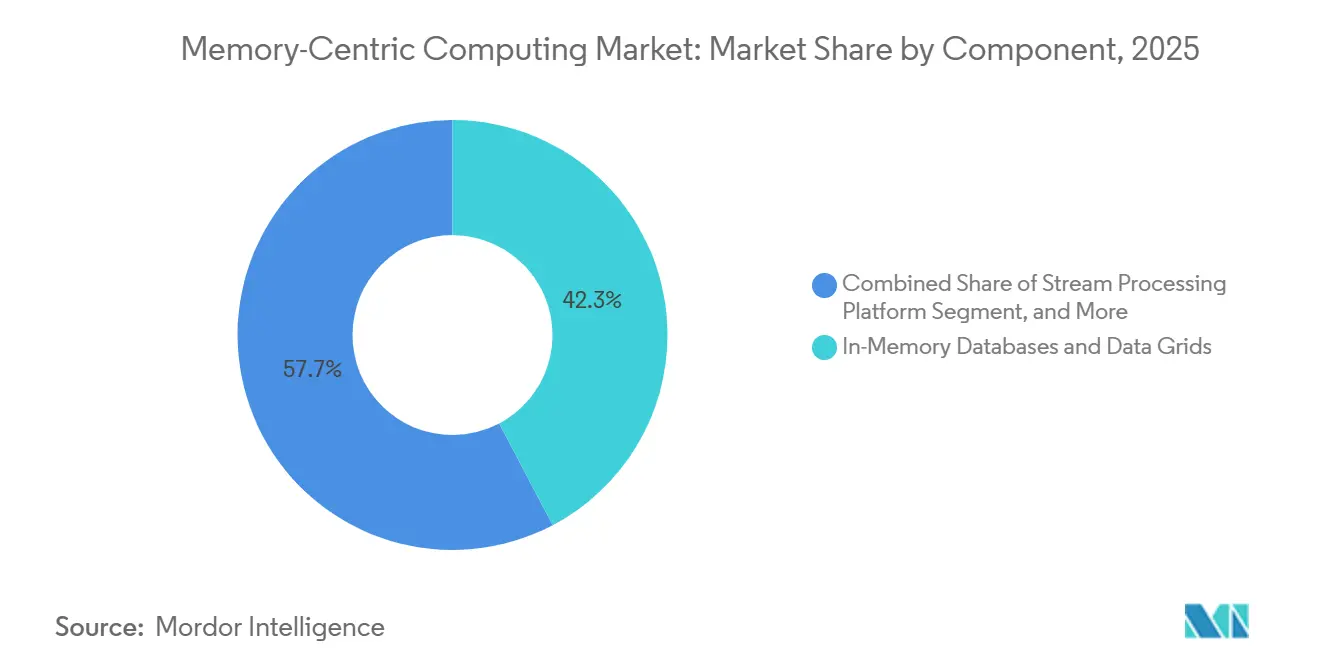

- By component, In-Memory Databases and Data Grids held 42.28% share in 2025, while In-Memory Caching and Application Acceleration Platforms recorded the highest projected CAGR at 18.99% through 2031.

- By deployment mode, Managed Cloud and SaaS held 45.66% share in 2025 and also recorded the highest projected CAGR at 19.16% through 2031.

- By application, Digital Applications, Caching, and Personalization accounted for 29.78% share in 2025, while AI/ML Applications and Decision Automation are projected to expand at a 19.11% CAGR through 2031.

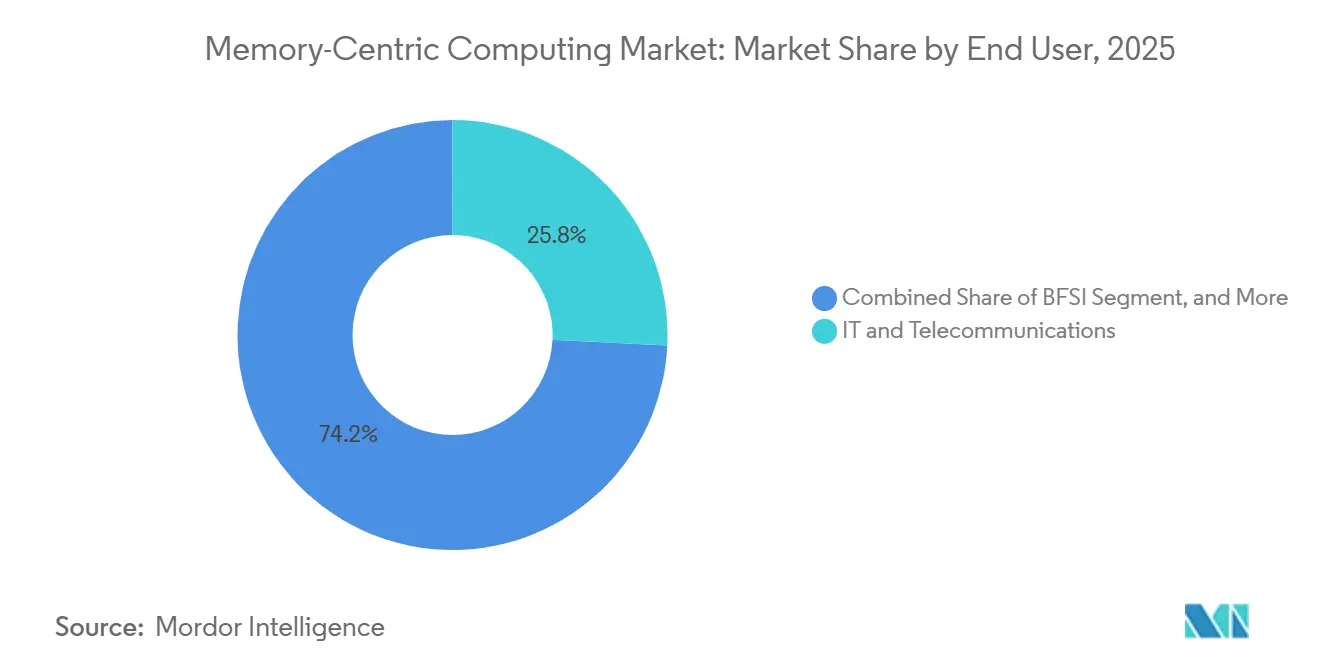

- By end user, IT and Telecommunications held 25.77% share in 2025, while Retail, E-Commerce, and Digital Platforms are projected to grow at a 19.23% CAGR through 2031.

- By data architecture, Hybrid In-Memory Architecture with Persistent Storage accounted for 66.58% share in 2025, while Pure In-Memory Architecture is projected to expand at a 19.44% CAGR through 2031.

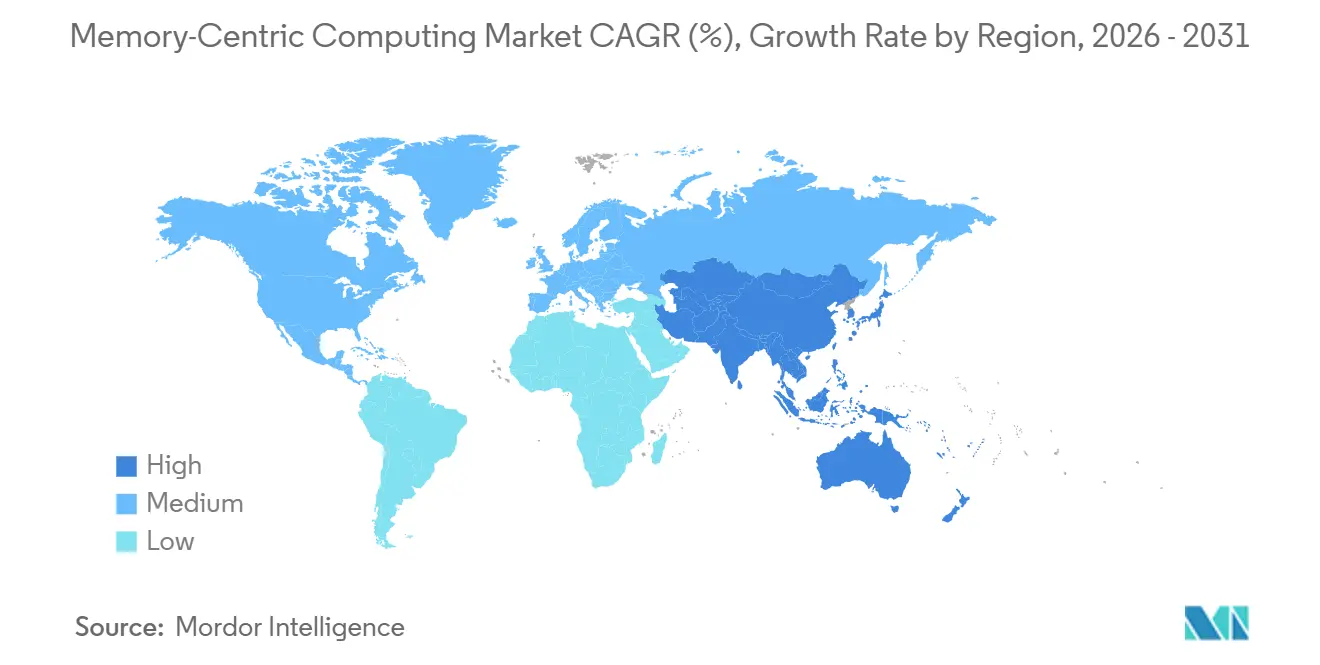

- By geography, North America held 42.34% of the memory-centric computing market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 19.46% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Memory-Centric Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of AI-Native Workloads and Vector Search | +5.5% | Global | Short term (≤ 2 years) |

| Escalating Need For Low-Latency Decision Engines in Digital Banking And Fraud Control | +3.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Growth of High-Density Data Ingestion from Cloud-Native and Streaming Applications | +3.2% | Global | Medium term (2-4 years) |

| Shift Toward Persistent Memory and Storage-Class Memory for Performance Efficiency | +2.1% | North America, Europe | Medium term (2-4 years) |

| Expansion of Edge Analytics in 5G, Industrial IoT, and Real-Time Telemetry | +1.5% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Rising Replacement Demand from Legacy Disk-Heavy Analytical Stacks | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of AI-Native Workloads and Vector Search

AI-native applications have pushed the memory-centric computing market closer to the center of enterprise infrastructure planning because inference, retrieval, and agent coordination all depend on low-latency state access. Google Research described memory-centric computing as a structural redesign of database architecture, with disaggregated memory pools offering a path to scale performance-sensitive data systems more efficiently. That shift matters because agentic systems not only read data quickly, they also need a durable multi-session state that simple cache layers cannot reliably provide. Aerospike reinforced this direction in March 2026 when it launched LangGraph integration for NoSQL Database 8 to provide durable, low-latency memory support for stateless agentic AI workflows.[1]Aerospike, “Aerospike NoSQL Database 8 Delivers Durable and Low-Latency Memory Store for LangGraph Agentic AI Workflows,” Aerospike, aerospike.com. As more enterprises move from AI experimentation to production deployment, the memory-centric computing market is benefiting from workloads that need persistence, concurrency, and fast recovery in the same stack. This is why platform selection is increasingly tied to how well vendors support agent state, retrieval pipelines, and transaction-grade responsiveness rather than raw caching speed alone.

Escalating Need for Low-Latency Decision Engines in Digital Banking and Fraud Control

The memory-centric computing market is also advancing because real-time financial decisioning no longer leaves room for deferred processing windows. A 2025 study in the International Journal of Fundamental Mathematics Research found that real-time banking fraud detection pipelines require prediction latency below 50 milliseconds per transaction, and it noted that in-memory feature stores can serve pre-computed values in single-digit milliseconds by removing disk I/O.[2]Author not disclosed, “Fast and Efficient Real-Time Banking Fraud Detection Using Stream-Based Algorithms,” International Journal of Fundamental Mathematics Research, doi.org. Volt Active Data published an architecture benchmark showing that a Tier-1 bank ran more than 2,000 production rules within a 50ms authorization budget while handling throughput above 10,000 transactions per second. This operating model changes the buying logic because compliance, customer experience, and fraud prevention now depend on the same low-latency foundation. It also helps explain why regulated institutions continue to treat in-memory platforms as core operational infrastructure rather than optional performance software. In the memory-centric computing market, financial workloads remain important because they reward stable latency, rapid rule changes, and high transaction concurrency at the same time.

Growth of High-Density Data Ingestion from Cloud-Native and Streaming Applications

High-volume streaming environments are expanding the memory-centric computing market because they generate continuous state that must be processed before it loses operational value. Apache Kafka 4.0 and Apache Flink 2.0 were both released in March 2025 by the Apache Software Foundation, and those releases lowered operational complexity while adding stronger streaming and AI-oriented capabilities.[3]The Apache Software Foundation, “Apache Kafka 4.0 Release Announcement,” Apache Software Foundation, kafka.apache.org. Flink 2.0 also added LLM inference and vector search support in streaming SQL, which pulled stateful event processing closer to the in-memory layer. This matters because enterprises that first adopt streaming for observability, payments, or customer events often end up needing distributed in-memory state to keep latency consistent under load. The result is that stream processing platforms increasingly function as an adoption path into the broader memory-centric computing market. That broadens the addressable opportunity beyond traditional database buyers and brings platform teams, application owners, and cloud architects into the same procurement cycle.

Shift Toward Persistent Memory and Storage-Class Memory for Performance Efficiency

Persistent memory and storage-class approaches are improving the economics of the memory-centric computing market by narrowing the cost gap between hybrid and full memory-resident designs. A VLDB paper on SAP HANA showed that CXL-attached memory can expand addressable datasets while preserving in-memory performance characteristics, which supports larger memory footprints without relying on the same cost structure as conventional local DRAM. A 2026 paper in IEEE Transactions on Computers added production-scale characterization evidence for deployable CXL memory systems, giving enterprises stronger engineering confidence as they evaluate rollout options. Microsoft Azure also announced CXL-based memory expansion support powered by Intel Xeon 6 processors at Ignite 2025, which moved the technology closer to public cloud consumption models. As those capabilities mature, the memory-centric computing market is likely to see more workloads move from selective hot-data acceleration toward broader memory residency. That transition supports vendors that can combine software efficiency, interoperability, and lifecycle cost control in the same offer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Hardware and Infrastructure Cost for Large-Scale Memory Fabric Deployment | -2.8% | Global | Medium term (2-4 years) |

| Data Gravity, Replication Overhead, and Inter-Cluster Latency Constraints | -1.9% | Global | Short term (≤ 2 years) |

| Vendor Lock-In Risks in Proprietary In-Memory Platforms and Appliances | -1.4% | North America, Europe | Medium term (2-4 years) |

| Shortage of Specialized Memory Systems Architects and Runtime Engineers | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Hardware and Infrastructure Cost for Large-Scale Memory Fabric Deployment

High hardware cost still limits how quickly the memory-centric computing market can move into the mid-market segment. Full memory-heavy deployments require more expensive capacity planning than flash- or disk-led architectures, and that increases approval friction for buyers with fixed infrastructure budgets. The challenge becomes larger when organizations need CXL-capable server refreshes and related integration work before they can scale production use. Microsoft Azure's support for CXL-based memory expansion shows that the technology is becoming commercially viable, but it also underlines the reality that adoption depends on compatible next-generation hardware. In practice, this keeps some enterprises in hybrid designs longer than they would prefer, especially when procurement committees weigh performance benefits against multi-year capital planning. The memory-centric computing market, therefore, continues to grow, but cost discipline still shapes the pace at which buyers move from pilot deployments to broad infrastructure replacement.

Data Gravity, Replication Overhead, and Inter-Cluster Latency Constraints

Data gravity remains a real brake on the memory-centric computing market because many enterprises cannot easily move large data estates across regions or clouds. Replicating memory-resident state across clusters introduces extra overhead, and that overhead can erode the speed advantage that justifies in-memory design in the first place. A 2025 characterization study found that cross-server CXL-expanded memory delivered much lower bandwidth and materially higher latency than local DDR5 memory in demanding configurations. That gap is especially important for multinational organizations that need strong consistency, disaster recovery, or data sovereignty controls across multiple sites. Vendors are working on better memory placement and tiering strategies, but the technical tradeoff between locality and resilience is still shaping deployment decisions. This means the memory-centric computing market will continue to favor architectures that keep the hottest state close to execution while using replication more selectively for protection and continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: In-Memory Databases Anchor Platform Consolidation

In-Memory Databases and Data Grids held 42.28% of the component segment in 2025, which made them the largest building block inside the memory-centric computing market. Their lead reflects the fact that transaction-heavy use cases in BFSI, IT, and telecommunications still need stable, low-latency reads and writes that general storage systems do not deliver consistently. These platforms also benefit from being deeply embedded in operational workflows where reliability matters as much as response time. In-Memory Caching and Application Acceleration Platforms are projected to record the fastest growth at 18.99% through 2031, as application teams place distributed cache layers between microservices and back-end databases to absorb spikes more efficiently. Stream Processing and Event Processing Platforms continue to gain share because more enterprises now treat event pipelines as a live operating layer rather than a reporting channel. Apache Flink 2.0 supported this shift by adding vector search and LLM inference capabilities directly in streaming SQL, which pulled advanced event processing closer to in-memory execution.

The structure of the component segment is becoming more competitive because functional boundaries are no longer as clear as they once were. Caching vendors are moving toward broader state management, while stream processors are increasingly handling workloads that were once reserved for purpose-built in-memory databases. That overlap widens the strategic scope of the memory-centric computing market because buyers can now enter through application acceleration, data grids, or real-time streams instead of through a core database replacement alone. Enterprises that manage several point tools are also looking for consolidation, since separate platforms for cache, streaming, and grid operations can create extra operational cost and governance complexity. In this setting, unified offerings have a stronger selling position because they reduce integration overhead while keeping latency performance within acceptable limits. The memory-centric computing industry is therefore seeing platform convergence at the component level, even though best-of-breed specialists still hold strong positions in demanding use cases.

By Deployment Mode: Cloud Delivery Models Reshape Consumption Economics

Managed Cloud and SaaS held 45.66% share in 2025 and also recorded the highest projected CAGR at 19.16%, which made it the strongest delivery model in the memory-centric computing market. That dual position shows how buyers increasingly prefer operational elasticity over fixed memory-fabric investments, especially when they want faster implementation and lower platform administration burden. Public cloud remains the next major path because hyperscalers continue to expand managed in-memory service portfolios across enterprise accounts. On-premises and private cloud still matter, particularly in regulated workloads where data sensitivity, sovereignty, or infrastructure control carry more weight than rapid migration. The DSAG Investitionsreport 2026 found that 70% of surveyed German-speaking enterprises had SAP S/4HANA migration running or completed, and that pattern supports durable demand for private and managed environments built around SAP HANA. Oracle and Microsoft also expanded Oracle Database@Azure in March 2025 with Exadata Database Service on Exascale Infrastructure, reducing minimum infrastructure costs by up to 95% versus dedicated Exadata platforms.

The deployment story is no longer a simple shift from on-premises to cloud, because hybrid models now define a large share of enterprise rollouts. In June 2026, Nokia, SAP, and Microsoft signed a multi-year agreement to run Nokia's SAP S/4HANA landscape on Microsoft Azure under RISE with SAP, which shows how large enterprises are using cloud-managed in-memory environments for major transformation programs. This kind of migration suggests that the memory-centric computing market will keep growing through coexistence models, not only through direct displacement of private infrastructure. Many enterprises still want on-premises control for sensitive data while linking those environments to managed platforms for analytics, resilience, and scaling. That keeps deployment competition broad, since vendors must serve full cloud migration, hosted private environments, and hybrid extension paths at the same time. The memory-centric computing industry is therefore being shaped as much by flexible consumption models as by raw technology differentiation.

By Application: Real-Time Intelligence Drives Broad Adoption

Digital Applications, Caching, and Personalization held the largest application share at 29.78% in 2025, while AI/ML Applications and Decision Automation are projected to grow at 19.11% through 2031 in the memory-centric computing market. The current revenue base remains anchored in digital experiences because e-commerce and platform operators still depend on low-latency state to support personalization, sessions, and recommendation flows at high interaction volumes. At the same time, the fastest growth is moving toward AI-driven automation where memory-resident state supports inference continuity, multi-step logic, and fault-tolerant execution. Aerospike's March 2026 LangGraph integration for NoSQL Database 8 directly addressed this need by providing durable low-latency memory support for stateless agentic AI workflows. Fraud Detection, Risk Management, and Financial Trading remains a structurally defensible application set because instant payment and capital markets environments reward deterministic latency over broad feature breadth. That is one reason the memory-centric computing market continues to spread across both digital consumer platforms and highly regulated operational systems.

IoT, Edge Analytics, and Telemetry Processing is adding weight because industrial environments increasingly need local inference and event handling that cloud round trips cannot support. An IEEE Letters on Networking study published in 2025 showed that AI-enhanced closed-loop telemetry control in private 5G industrial environments reduced end-to-end latency by up to 41% and jitter by up to 75%. Real-Time Analytics and Business Intelligence also remains relevant, especially as capital markets firms modernize from legacy analytical stores to faster engines. KX released KDB-X for general availability in April 2026, combining in-memory time-series processing, vector search, and GPU acceleration in a single runtime for real-time AI and trading-oriented workloads. These application shifts widen the scope of the memory-centric computing market because growth is no longer tied to one dominant use case. Instead, adoption is spreading across customer experience, industrial telemetry, AI coordination, fraud prevention, and high-speed decision support in parallel.

By End User: Financial Services Leads While Retail Accelerates

IT and Telecommunications held 25.77% of the end-user base in 2025, while Retail, E-Commerce, and Digital Platforms are projected to grow at 19.23% through 2031 across the memory-centric computing market. The telecom share is large because operators need real-time infrastructure for network orchestration, subscriber analytics, and billing workflows that run continuously at scale. Retail is growing faster because personalization engines and recommendation systems now score huge volumes of user interactions in real time, and that pushes more session and context data into memory-resident environments. BFSI remains one of the most demanding verticals because both fraud control and algorithmic decisioning impose strict latency thresholds that leave little tolerance for disk-led processing. The banking evidence is clear in the fraud domain, where sub-50ms scoring has become the operating benchmark for live authorizations. This mix of sectors keeps the memory-centric computing market balanced between infrastructure-led buyers and application-led buyers.

Healthcare and life sciences are still a smaller vertical, but their use cases are becoming harder to postpone because real-time data freshness matters more in analytics-heavy clinical and genomics workflows. Manufacturing and automotive are also building stronger demand, especially where predictive quality control, connected vehicle telemetry, and factory digital twins need fast event handling close to operations. The IEEE private 5G study supports this direction by showing meaningful latency and jitter gains in industrial edge control settings, which strengthens the case for in-memory deployment in production environments.. Government and public sector adoption is also moving forward in areas such as fraud detection, eligibility processing, and identity verification, where response speed and data control must coexist. These cross-vertical needs show that the memory-centric computing market is not defined by one customer profile, but by a common need for continuous low-latency state access across very different operational environments. The memory-centric computing industry therefore has room to deepen in established sectors while still opening new adoption tracks in public services and industrial systems.

By Data Architecture: Hybrid Architectures Establish The Enterprise Default

Hybrid In-Memory Architecture with Persistent Storage commanded 66.58% share in 2025, which made it the default design choice in the memory-centric computing market size for current enterprise deployments. Pure In-Memory Architecture is projected to expand at a 19.44% CAGR through 2031, which shows that the memory-centric computing market size for this architecture is rising faster as AI and real-time decisioning workloads demand fewer storage lookups. Hybrid systems still lead because they offer a more manageable balance of DRAM residency, durability, and cost control for mainstream enterprise workloads. This model allows buyers to keep hot data in memory while relying on persistent storage for resilience and capacity, which reduces financial risk during broader rollout. The existing 66.58% position also reflects the fact that many enterprises are still upgrading from legacy architectures rather than designing greenfield environments. For now, hybrid remains the most practical way to capture much of the performance benefit without taking on the full cost profile of pure DRAM residency.

That balance may change steadily as hardware and software support improve. The VLDB paper on SAP HANA showed that CXL-attached memory can expand memory addressability while keeping performance aligned with in-memory database requirements, which weakens one of the historic economic arguments for hybrid-first design. The 2026 IEEE Transactions on Computers study also strengthened the technical case for deployable CXL memory systems at scale. Over time, that should make it easier for some workloads to shift from hybrid persistence toward broader memory residency, especially in AI-serving and event-driven environments. Even so, the memory-centric computing market share of hybrid architecture in 2025 shows that most buyers still prefer a staged transition rather than a full redesign in one step. That makes hybrid architecture less a temporary compromise and more the current operating baseline from which future in-memory expansion will proceed.

Geography Analysis

North America held 42.34% of the memory-centric computing market share in 2025, which kept it as the largest regional contributor by revenue. The region benefits from a dense concentration of financial services technology buyers, hyperscale cloud infrastructure, and enterprise software vendors that already package in-memory capabilities into larger platform portfolios. The United States remains the center of adoption because fraud detection, algorithmic trading, and real-time personalization are already well funded and commercially scaled there. Canada adds support through financial services and government analytics demand, while Mexico is gaining relevance through nearshoring-linked manufacturing intelligence deployments. This installed base gives the memory-centric computing market a strong regional foundation where both specialist vendors and large integrated providers can commercialize new capabilities quickly.

Europe remains important because enterprise application modernization and regulatory discipline are shaping demand at the same time. Germany is the region's largest market, and DSAG reported in 2026 that 70% of surveyed German-speaking enterprises had SAP S/4HANA migration running or completed, which directly supports in-memory infrastructure demand because every S/4HANA deployment relies on SAP HANA. The United Kingdom and France also remain large markets because of sustained investment in financial services and public sector digital programs. In June 2026, Nokia, SAP, and Microsoft formalized a multi-year agreement to run Nokia's SAP S/4HANA landscape on Microsoft Azure, which highlighted the scale of enterprise in-memory migration activity taking place in Europe. Italy and the rest of Europe are growing more gradually, with demand centered on banking and automotive manufacturing rather than broad-based cloud migration.

Asia-Pacific is projected to record the fastest CAGR at 19.46% through 2031, which gives it the strongest expansion profile in the memory-centric computing market size over the forecast period. Demand in the region is being driven by digital banking growth in India and Southeast Asia, private 5G industrial deployments in Japan and South Korea, and continued scale in Chinese e-commerce and digital payments. South Korea has a dual advantage because industrial edge demand is rising while the country also remains close to semiconductor and memory hardware innovation. Japan continues to support adoption through industrial IoT, precision manufacturing, and enterprise analytics modernization. South America remains smaller but is improving as hyperscale investment reduces latency barriers in Brazil and nearby markets, while the Middle East and Africa is gaining traction from smart city programs and financial sector modernization initiatives aligned with national diversification agendas.

Competitive Landscape

The memory-centric computing market is moderately consolidated, with Microsoft, Oracle, and SAP holding anchor positions through integrated database, cloud, and enterprise application strategies. Their advantage comes from scale, installed customer relationships, and the ability to bundle in-memory capabilities into broader transformation programs instead of selling them as stand-alone products. Even so, the market is not closed because specialist vendors still compete effectively in workloads where low latency, stateful AI support, or operational simplicity matter more than full-suite breadth. Redis Ltd., Aerospike, Hazelcast, KX Systems, Exasol, and similar players remain visible because they can target narrower use cases with clearer performance or cost propositions. This structure keeps the memory-centric computing market competitive enough to support innovation, while still allowing the largest vendors to anchor large contract values and enterprise-standard deployments.

Strategic moves between 2025 and 2026 show how vendors are widening their positions. IBM completed the acquisition of DataStax in Q2 2025 to deepen watsonx capabilities in vector database and NoSQL workloads, which strengthened its position around AI data infrastructure. MariaDB completed the acquisition of GridGain Systems in March 2026 to combine its relational database base with Apache Ignite-based in-memory computing for sub-millisecond agentic enterprise applications. KX also released KDB-X in April 2026 with GPU acceleration and vector search integrated into a unified runtime, showing that specialists are using product depth to defend high-performance niches. Aerospike added an AI-native developer experience in April 2026 with Model Context Protocol server support and updated SDKs, which points to a competitive shift toward developer tooling and faster AI application creation. These moves show that competition in the memory-centric computing market is now being shaped by acquisitions, runtime innovation, and workflow support rather than by database speed claims alone.

Open-source governance has also become a strategic issue in the memory-centric computing market. Redis Ltd. changed from BSD 3-Clause to a dual-license structure starting with Redis 7.4 in 2024, and that pushed AWS, Google, and Oracle to back the Linux Foundation's Valkey fork. That licensing shift made procurement teams more aware of platform dependency and long-term cost uncertainty, especially in large managed caching estates. At the same time, cloud expansion by Oracle and Microsoft, and large SAP-linked migrations in Azure, show that integrated enterprise providers are still extending their reach into high-value accounts. The result is a market where leaders hold meaningful strategic leverage, but specialists and open-source alternatives continue to shape pricing, architecture choices, and buyer caution.

Memory-Centric Computing Industry Leaders

Microsoft Corporation

Oracle Corporation

SAP SE

IBM Corporation

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Oracle AI Database@AWS expanded availability to Spain, with the Metropolitan Transport Authority of Barcelona and Helvetia Caser among the first enterprise customers to migrate critical workloads, extending Oracle's managed in-memory database footprint into a major Southern European market.

- June 2026: Nokia, SAP, and Microsoft signed a multi-year agreement under which Nokia will run its SAP S/4HANA landscape, built on the SAP HANA in-memory database, on Microsoft Azure using the RISE with SAP framework, the agreement is designed to deliver improvements in performance, security, latency, and operational resilience.

- April 2026: KX Systems released KDB-X for general availability on April 2, 2026, a unified compute engine integrating in-memory time-series processing, vector search, and GPU acceleration, with GPU-powered operations delivering 10x to 25x performance improvements across joins, aggregations, and risk simulation workloads at near-linear multi-GPU scaling.

- March 2026: MariaDB completed the acquisition of GridGain Systems on March 24, 2026, combining MariaDB's AI-ready relational database with GridGain's open-source Apache Ignite-based in-memory computing platform to create an agentic AI data foundation targeting sub-millisecond response times.

Global Memory-Centric Computing Market Report Scope

The Memory-Centric Computing Market refers to the market for computing architectures that place memory at the center of system design to reduce data movement and improve performance. It includes technologies such as in-memory computing, compute-near-memory, memory disaggregation, and other data-centric hardware approaches.

The Memory-Centric Computing Market Report is Segmented by Component (In-Memory Databases and Data Grids, In-Memory Caching and Application Acceleration Platforms, and Stream Processing and Event Processing Platforms), Deployment (On-Premises and Private Cloud, Public Cloud, and Managed Cloud and SaaS), Application (Real-Time Analytics and Business Intelligence, Digital Applications, Caching, and Personalization, Fraud Detection, Risk Management, and Financial Trading, IoT, Edge Analytics, and Telemetry Processing, and AI/ML Applications and Decision Automation), End User (BFSI, IT and Telecommunications, Retail, E-Commerce, and Digital Platforms, Healthcare and Life Sciences, Manufacturing and Automotive, Government and Public Sector), Data Architecture (Pure In-Memory Architecture, and Hybrid In-Memory Architecture with Persistent Storage), and Geography (North America, Europe, APAC, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD).

| In-Memory Databases and Data Grids |

| In-Memory Caching and Application Acceleration Platforms |

| Stream Processing and Event Processing Platforms |

| On-Premises and Private Cloud |

| Public Cloud |

| Managed Cloud and SaaS |

| Real-Time Analytics and Business Intelligence |

| Digital Applications, Caching, and Personalization |

| Fraud Detection, Risk Management, and Financial Trading |

| IoT, Edge Analytics, and Telemetry Processing |

| AI/ML Applications and Decision Automation |

| BFSI |

| IT and Telecommunications |

| Retail, E-Commerce, and Digital Platforms |

| Healthcare and Life Sciences |

| Manufacturing and Automotive |

| Government and Public Sector |

| Other End Users |

| Pure In-Memory Architecture |

| Hybrid In-Memory Architecture with Persistent Storage |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | In-Memory Databases and Data Grids | |

| In-Memory Caching and Application Acceleration Platforms | ||

| Stream Processing and Event Processing Platforms | ||

| By Deployment Mode | On-Premises and Private Cloud | |

| Public Cloud | ||

| Managed Cloud and SaaS | ||

| By Application | Real-Time Analytics and Business Intelligence | |

| Digital Applications, Caching, and Personalization | ||

| Fraud Detection, Risk Management, and Financial Trading | ||

| IoT, Edge Analytics, and Telemetry Processing | ||

| AI/ML Applications and Decision Automation | ||

| By End User | BFSI | |

| IT and Telecommunications | ||

| Retail, E-Commerce, and Digital Platforms | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Automotive | ||

| Government and Public Sector | ||

| Other End Users | ||

| By Data Architecture | Pure In-Memory Architecture | |

| Hybrid In-Memory Architecture with Persistent Storage | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the memory-centric computing market?

The memory-centric computing market size stands at USD 13.72 billion in 2026 and is projected to reach USD 32.16 billion by 2031 at a CAGR of 18.57%.

Which deployment model leads revenue in memory-centric computing?

Managed Cloud and SaaS led with a 45.66% share in 2025 and is also the fastest-growing deployment mode at a 19.16% CAGR through 2031.

Which region is growing fastest for memory-centric computing?

Asia-Pacific is projected to expand at a 19.46% CAGR through 2031, ahead of other regions, while North America remained the largest market in 2025 with 42.34% share.

Which applications are creating the strongest demand for memory-centric platforms?

Digital applications, caching, and personalization held the largest application share at 29.78% in 2025, while AI/ML applications and decision automation is growing fastest at 19.11% CAGR.

Why are banks and payment providers investing in memory-centric platforms?

Real-time fraud detection now requires sub-50ms decisioning, which makes in-memory architectures important for transaction scoring, rule execution, and compliance-driven authorization speed.

What data architecture is most common in enterprise deployments today?

Hybrid in-memory architecture with persistent storage led with 66.58% share in 2025 because it gives enterprises a practical balance between performance, durability, and cost control.

Page last updated on: