GPU Heatsink And Thermal Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

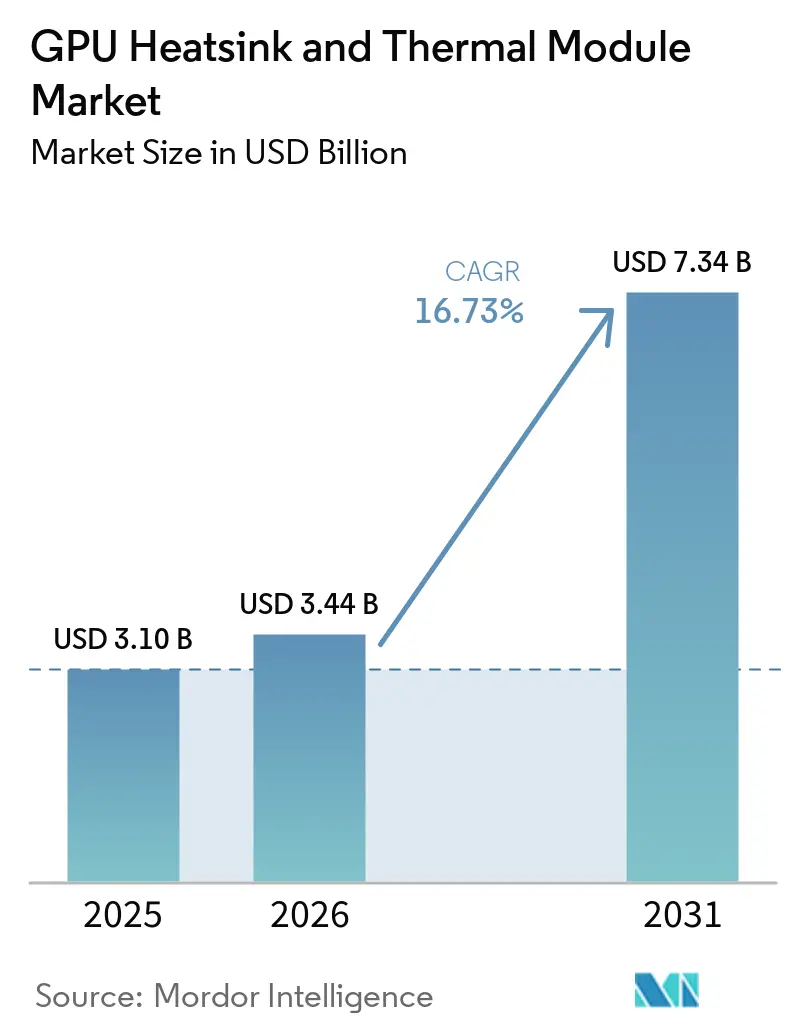

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 7.34 Billion |

| Growth Rate (2026 - 2031) | 16.73% CAGR |

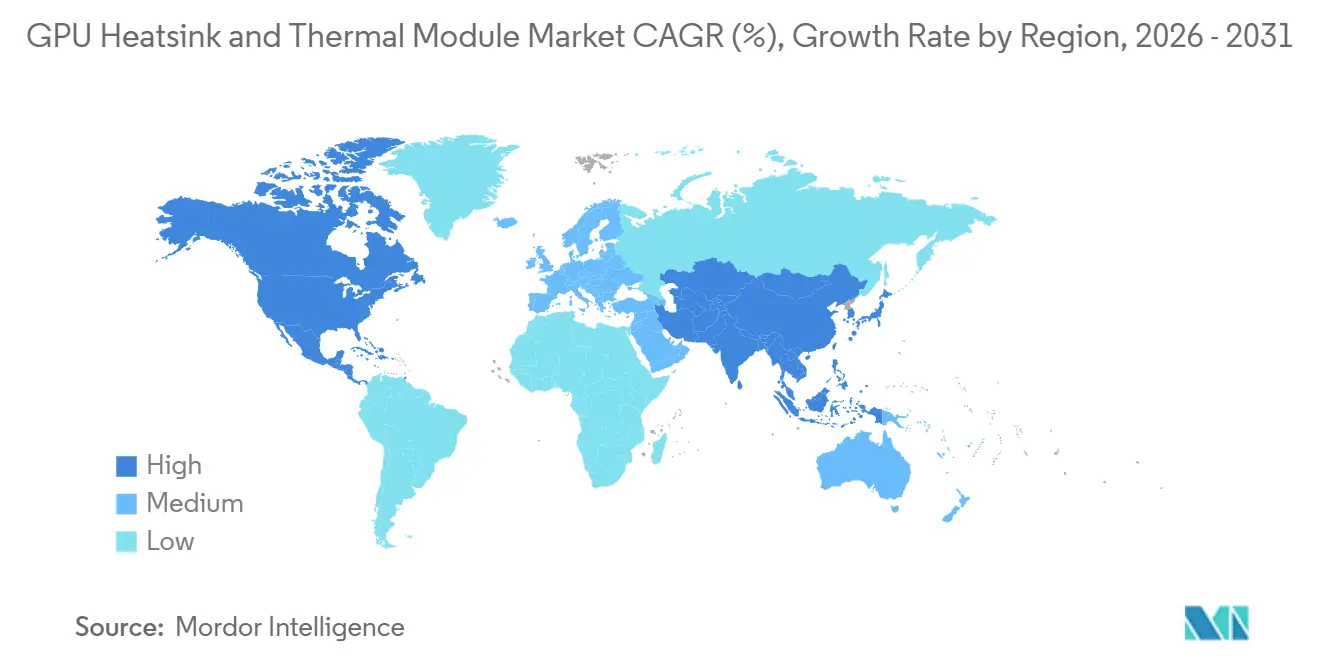

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Heatsink And Thermal Module Market Analysis by Mordor Intelligence

The GPU heatsink and thermal module market size is expected to increase from USD 3.1 billion in 2025 to USD 3.44 billion in 2026 and reach USD 7.34 billion by 2031, growing at a CAGR of 16.37% over 2026-2031. Robust demand stems from liquid-cooled generative-AI clusters that dissipate 100-150 kilowatts per cabinet, gaming GPUs that now draw up to 600 watts under ray-tracing loads, and chiplet architectures that concentrate hotspots across multiple dies. Data-center operators already allocate 40% of new GPU deployments to liquid cooling in 2026 because air-cooled heat sinks cannot cost-effectively manage the 750-watt thermal design power of AMD’s MI300X or the 1 200-watt envelope of Intel’s Gaudi 3. Commodity copper prices oscillating between USD 10,500 and USD 13,300 per tonne compress margins for hybrid aluminum-copper modules and accelerate the shift toward thinner solder-attached vapor chambers. Together, these factors signal that the GPU heatsink and thermal module market will remain on a double-digit growth trajectory as thermal headroom becomes a gating variable for both performance and uptime.

Key Report Takeaways

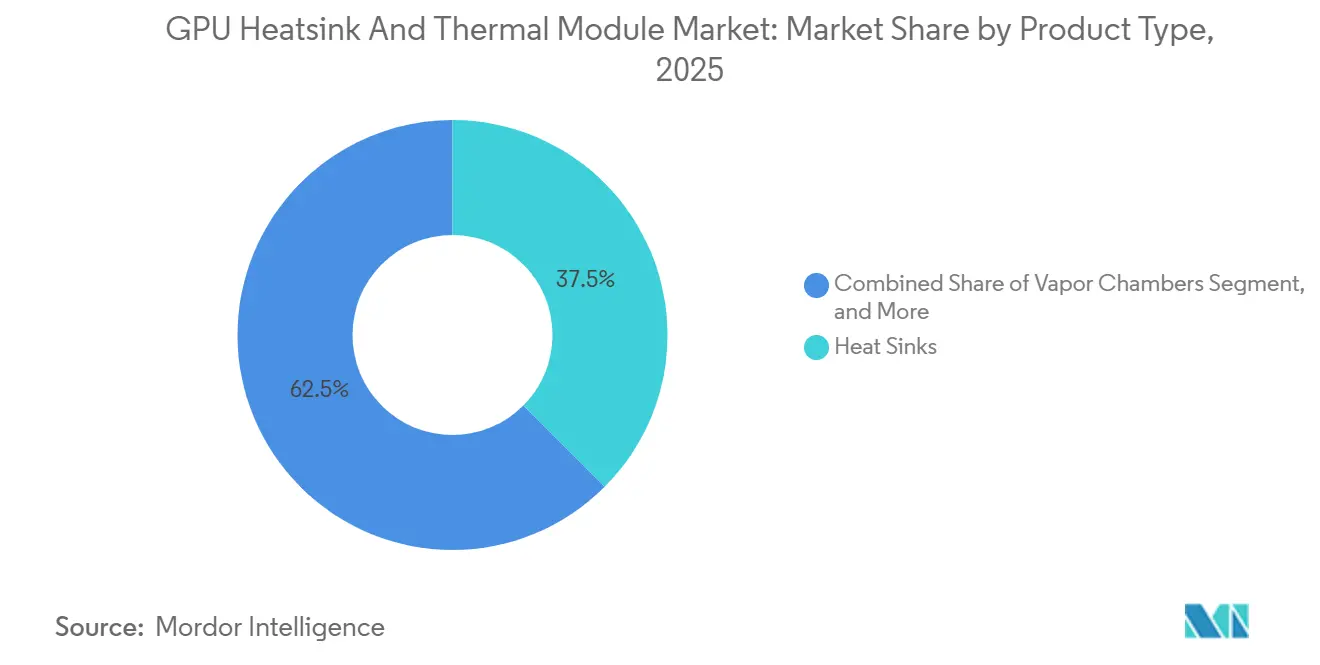

- By product type, vapor chambers are on track to capture the fastest growth, advancing at a 17.17% CAGR to 2031, while heat sinks retained a 37.48% revenue share in 2025 but are losing relevance in workloads above 400 watts.

- By material, aluminum-based solutions accounted for 52.56% of revenue in 2025, whereas hybrid aluminum-copper designs are expanding at 16.97% because they deliver nearly copper-class conductivity at 60% of the cost.

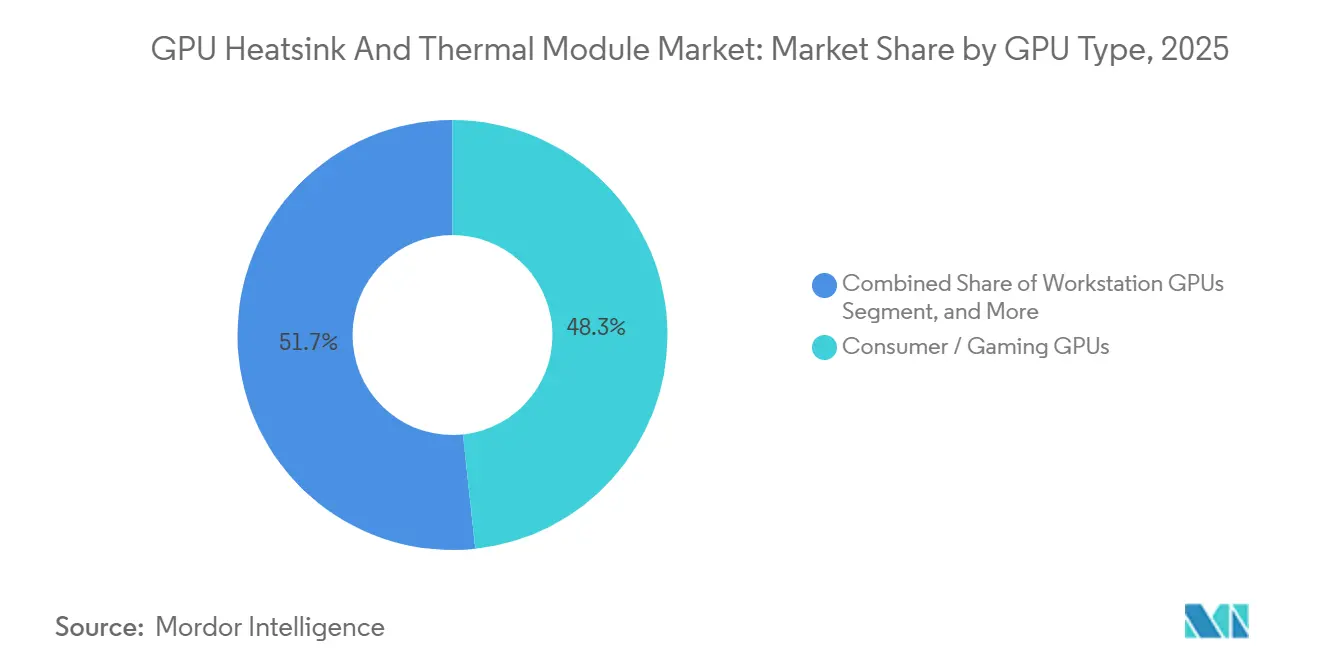

- By GPU type, consumer and gaming GPUs accounted for 48.32% of revenue in 2025, yet data-center and AI accelerators are forecast to grow at a 16.88% CAGR, reflecting hyperscalers’ willingness to pay premiums for liquid-cooled reliability.

- By geography, Asia-Pacific commanded 67.81% of the GPU heatsink and thermal module market share in 2025 and is projected to sustain a 17.29% CAGR through 2031, underpinned by Taiwan’s vapor-chamber fabrication ecosystem.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Heatsink And Thermal Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI Workloads Driving Data-Center GPU Shipments | +4.2% | Global, with concentration in North America and Asia-Pacific hyperscale clusters | Medium term (2-4 years) |

| Escalating Thermal Design Power of Advanced Nodes | +3.8% | Global, led by North America data centers and Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Emergence of Chiplet-Based GPU Architectures | +2.6% | Global, early adoption in North America and Europe workstation segments | Long term (≥ 4 years) |

| Growth of Ray-Tracing Gaming Titles | +2.3% | Global, with highest intensity in North America, Europe, and developed Asia-Pacific markets | Medium term (2-4 years) |

| Expansion of Cloud Gaming Infrastructure Globally | +1.9% | Global, spill-over from North America and Europe to Asia-Pacific and South America | Medium term (2-4 years) |

| Increasing Use of Solder-Attached Vapor Chambers in Workstations | +1.5% | North America and Europe professional workstation markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging AI Workloads Driving Data-Center GPU Shipments

Hyperscale operators spent more than USD 300 billion on AI infrastructure in 2026, a figure that includes liquid-cooling distribution units needed to prevent throttling in racks exceeding 100 kilowatts. NVIDIA’s H200 dissipates 700 watts, and AMD’s MI300X reaches 750 watts, pushing air-cooled designs beyond their economic limits. Intel’s Gaudi 3 delivers 1200 watts only under liquid cooling, a 33% power-density premium that translates into faster model-training cycles. Delta Electronics reports liquid-cooling penetration climbing from 14% in 2024 to 40% in 2026, illustrating a decisive industry pivot. The bifurcated market now sees traditional finned heat sinks limited to edge-inference boxes below 300 watts, whereas vapor chambers and cold plates dominate the 500-watt-plus tier.

Escalating Thermal Design Power of Advanced Nodes

GPU power envelopes rise with each process generation. NVIDIA’s RTX 5090 approaches 600 watts under sustained ray tracing, and memory junctions climb to 92 °C despite triple-slot coolers. RTX 4090’s 450-watt spec already forced board partners to adopt vapor chambers that spread heat across larger fin surfaces. Data-center accelerators follow the same arc, with 700 watts becoming the entry point. Thermal-interface materials now exceed 15 W m-K but demand metal backplates to maintain contact pressure. IEC 62368-1 touch-temperature limits further constrain fin density, forcing creative airflow management.[1]International Electrotechnical Commission, “IEC 62368-1,” iec.ch

Emergence of Chiplet-Based GPU Architectures

AMD’s RDNA 3 multi-chiplet design highlighted how localized hotspots challenge monolithic coolers. Early vapor-chamber defects on the Radeon RX 7900 XTX caused throttling and recalls. Chiplets concentrate heat in millimeter-scale regions, requiring precision cold-plate contact. Solder-attached vapor chambers remove spring-compression layers, reducing junction temperatures by up to 15%, but increase reliability risks if joints crack during thermal cycling. As vendors mix process nodes within a single package, heatsink designers must model transient heat maps rather than assume uniform flux.

Growth of Ray-Tracing Gaming Titles

Ray tracing sustains high utilization for hours, elevating average draw well above raster workloads. The RTX 5090 maintains 71-80 °C in path-traced Cyberpunk 2077 even on liquid loops. GeForce NOW runs GPUs on 24-hour duty cycles, which triples thermal stress compared to desktop usage. Form-factor limits in 1U and 2U blades mandate low-profile vapor chambers with high-static-pressure blowers, because tall towers block adjacent slots. Developers see ray tracing as a visual baseline, so thermal headroom will continue to shape card dimensions and rack density.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Shift Toward Integrated Liquid Cooling Loops | -2.1% | Global, with early adoption in North America and Europe data centers | Short term (≤ 2 years) |

| Volatility in Copper Commodity Prices | -1.8% | Global, acute impact in Asia-Pacific manufacturing hubs reliant on spot pricing | Medium term (2-4 years) |

| Supply Chain Concentration in East Asia | -1.3% | Global, with supply disruptions rippling from Taiwan and China production bases | Medium term (2-4 years) |

| Environmental Regulations on Mining of Thermal Interface Metals | -0.9% | Europe and North America, with compliance costs spreading to Asia-Pacific exporters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Shift Toward Integrated Liquid Cooling Loops

Server builders now ship closed-loop liquid systems pre-installed, bypassing the aftermarket for discrete modules. Lenovo’s Neptune achieves a 1.1 power-usage effectiveness and recycles waste heat for facility heating, cutting cooling energy by 40%.[2]Lenovo, “Neptune Liquid Cooling,” lenovo.com Dell’s PowerCool eRDHx enables 80-kilowatt racks that air systems cannot meet without prohibitive noise. Asetek’s USD 35 million, two-year supply contract underscores the pivot toward OEM-centric revenue streams. While liquid loops enlarge the total market, they erode unit sales of standalone heat sinks, especially in data-center GPUs where liquid is the default.

Volatility in Copper Commodity Prices

Copper prices spiked to USD 13,300 per tonne in January 2026 due to supply disruptions at the Grasberg and El Teniente mines. Spot-purchasing ODMs in Taiwan and China saw 3-5 percentage-point swings in margins. Hybrids that use copper only in the base plate mitigate exposure, yet data-center cold plates remain copper-intensive. Manufacturers weigh hedging contracts against potential downside if prices retreat. Graphene pads and diamond-like-carbon coatings offer longer-term relief but lack commercial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vapor Chambers Lead Thermal Innovation

Vapor chambers accounted for the fastest expansion, posting a 17.17% CAGR outlook as GPU envelopes breach 600 watts. Heat sinks still secured 37.48% of 2025 revenue, covering sub-300-watt consumer GPUs, yet their share will contract as board partners migrate high-end designs to vapor chambers. Heat-pipe modules serve RTX 4080-class cards around 320 watts, but they face capillary-limit ceilings. Solder-attached vapor chambers lower GPU junction temperatures by 10-15%, making them indispensable in professional rendering stations. Active thermal modules integrate pumps and radiators, unlocking rack densities above 100 kilowatts. TaiSol’s 3D vapor chamber layers evaporators to match chiplet footprints, while Cooler Master’s FreeForm 2.0 allows dual-GPU loops on one radiator.[3]TaiSol Electronics, “Company Overview,” taisol.com

The GPU heatsink and thermal module market share of vapor chambers is rising because they deliver sub-0.1 °C-W thermal resistance in a thin profile, critical for multi-slot cards. Meanwhile, the GPU heatsink and thermal module market share of traditional heatsinks will shrink as air-cooling meets diminishing returns beyond 400 watts. Active modules remain niche in volume but command high average selling prices in AI servers. Together, these product-type dynamics keep innovation centered on vapor-chamber geometry and cold-plate microchannels rather than on fin-stack height.

By Material: Hybrid Formulations Balance Conductivity and Weight

Aluminum-based solutions accounted for 52.56% of 2025 revenue, as extrusion enables lightweight, complex fins ideal for low- to mid-range GPUs. Hybrid aluminum-copper designs are set to rise at 16.97%, pairing copper bases with aluminum fins to combine conductivity and mass efficiency. Pure copper modules dominate data-center accelerators due to their 385 W m-K conductivity, but weight and cost limit their desktop adoption. RoHS restrictions on lead push suppliers toward indium-based solders and graphene pastes, adding cost even as they enhance reliability.

The GPU heatsink and thermal module market size for hybrid materials is witnessing significant growth as Original Equipment Manufacturers (OEMs) strive to achieve 90% of copper’s thermal performance while reducing costs. The fluctuating prices of copper are driving manufacturers to either secure long-term contracts or shift their designs toward aluminum-based solutions wherever feasible. This trend is fostering innovation in hybrid materials, which combine the benefits of both copper and aluminum. By 2031, hybrid architectures are projected to surpass pure aluminum in terms of value, highlighting the industry's ongoing focus on optimizing thermal performance relative to weight, often referred to as grams-per-watt optimization.

By GPU Type: Data Center and AI Accelerators Reshape Demand

Consumer and gaming GPUs accounted for the largest share of revenue in 2025, contributing 48.32% to the market. However, data-center and AI accelerators are experiencing the fastest growth, with a compound annual growth rate (CAGR) of 16.88%. Rack-mount GPUs, commonly used in data centers, are equipped with liquid-cooled cold plates, which are priced significantly higher at USD 150-USD 200 each, compared to the USD 40-USD 60 range for consumer air coolers. The extended replacement cycles for workstations support a stable, high-margin niche market. However, the thermal architectures of these workstations often replicate those of gaming flagships, which limits opportunities for unique design innovations.

The market share of GPU heatsinks and thermal modules is gradually shifting toward accelerators, driven by hyperscalers' focus on enhancing the mean time between failures. Sunonwealth’s development of 1,000-watt cold plates indicates that the next generation of AI silicon will further amplify this trend. While gaming GPUs continue to dominate unit sales, demand for aftermarket air-cooler upgrades is expected to decline as OEMs improve the quality and performance of bundled cooling solutions.

Geography Analysis

Asia-Pacific generated 67.81% of 2025 revenue and is forecast to grow at a compound annual growth rate (CAGR) of 17.29% through 2031, driven by Taiwan’s expertise in vapor-chamber manufacturing and China’s large-scale assembly capabilities. Delta Electronics has committed NTD 12.1 billion (USD 380 million) to expand its Taoyuan production capacity, further solidifying the region’s dominance in the market. Japan’s Furukawa Electric plays a key role by supplying sintered pipes specifically designed for 1U chassis, while Vietnam and Thailand are emerging as alternative hubs for assembly, offering cost advantages and reducing reliance on traditional manufacturing centers.

North America ranks as the second-largest market, supported by hyperscale data center campuses located in states such as Virginia, Oregon, and Iowa. These facilities are increasingly adopting liquid-cooled racks with power capacities exceeding 100 kilowatts. Favorable tax incentives and access to renewable energy sources continue to drive the construction of new data centers in the region. In Europe, demand is concentrated in Germany’s automotive simulation clusters and the United Kingdom’s fintech data centers. Both regions operate under stringent carbon-pricing regulations, which are pushing buyers to adopt energy-efficient solutions such as advanced cold plates to meet sustainability goals.

South America, the Middle East, and Africa are still in the early stages of market development. In South America, Brazil’s data center facilities are transitioning to 30-kilowatt racks that require advanced vapor-chamber designs to effectively manage heat dissipation. Meanwhile, Gulf nations in the Middle East are deploying liquid-cooled workstations to support AI-driven oil exploration activities, reflecting the region’s growing interest in high-performance computing. Geographic diversification remains a key trend, as suppliers are increasingly establishing production lines in countries such as Vietnam, Thailand, and Mexico to mitigate risks associated with Taiwan-centric manufacturing and to meet the growing global demand for thermal management solutions.

Competitive Landscape

Competition in the GPU heatsink and thermal module market remains moderately fragmented, with no single firm holding more than a 15% market share. Taiwanese ODMs, such as Asia Vital Components and TaiSol, dominate the supply of vapor chambers to most add-in-board partners, thereby maintaining a strong presence in the market. Meanwhile, European brands like Noctua and Arctic focus on catering to the premium DIY tower segment, offering high-performance cooling solutions. Liquid-cooling specialists, including Asetek and EKWB, continue to secure OEM design wins for their closed-loop systems, further solidifying their market position. Asetek’s recent USD 35 million, two-year contract highlights the growing trend of long-term supply agreements, reflecting the increasing demand for reliable and efficient cooling solutions.[4]Asetek A/S, “Investor Relations Home,” investor.asetek.com

Major OEMs like Lenovo and Dell have started integrating proprietary liquid loops that combine GPU and CPU plates, gradually reducing the demand for discrete aftermarket solutions. In a strategic move to maintain relevance, Noctua partnered with ASUS to launch the RTX 5080 Noctua Edition, showcasing how cooler brands are co-labeling GPUs to strengthen their market presence. Innovations such as TaiSol’s 3D vapor chambers and Cooler Master’s modular FreeForm 2.0 technology underscore the ongoing race to achieve sub-0.1 °C-W thermal resistance, a critical benchmark for high-performance cooling systems.

Opportunities for growth remain in the hybrid air-liquid cooler segment, particularly for mid-tower gaming PCs. Arctic’s Liquid Freezer WS360, designed to handle 800-watt workstation loads, offers a consumer-friendly solution that bridges the gap between air and liquid cooling. Meanwhile, phase-change startups are exploring refrigerant loop technologies for sub-ambient cooling, although challenges such as condensation risks and stringent F-gas regulations continue to hinder widespread adoption. Additionally, environmental certifications like ISO 14001 are becoming increasingly influential in procurement decisions, compelling vendors to provide detailed assessments of their extrusion and refining processes to meet sustainability standards.

GPU Heatsink And Thermal Module Industry Leaders

Boyd Corporation

Hon Hai Precision Industry Co., Ltd.

Delta Electronics, Inc.

Asia Vital Components Co., Ltd.

Cooler Master Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Delta Electronics announced a NTD 12.1 billion (USD 380 million) expansion in Taoyuan to manufacture 50 000 liquid-cooling distribution units per quarter for hyperscale data centers.

- March 2026: Arctic released the Liquid Freezer WS360 all-in-one cooler rated for 800 watts, targeting multi-GPU workstations.

- October 2025: Asetek secured a minimum USD 35 million, two-year agreement for its Ingrid liquid-cooling platform with a returning OEM customer.

- September 2025: Sunonwealth disclosed development of closed-loop cold plates rated above 1 000 watts during its Q2 2025 results call.

Global GPU Heatsink And Thermal Module Market Report Scope

The GPU Heatsink and Thermal Module Market refers to the global industry that designs, manufactures, and deploys thermal management solutions specifically developed for graphics processing units (GPUs). These solutions are critical for dissipating heat generated by high-performance GPUs, ensuring optimal operating temperatures, sustained performance, and long-term reliability across a wide range of computing applications.

The GPU Heatsink and Thermal Module Market Report is Segmented by Product Type (Heat Sinks, Vapor Chambers, Heat Pipe-Based Modules, and Active Thermal Modules), Material (Aluminum-Based, Copper-Based, and Hybrid), GPU Type (Data Center/AI GPUs, Workstation GPUs, and Consumer/Gaming GPUs), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Heat Sinks |

| Vapor Chambers |

| Heat Pipe-Based Modules |

| Active Thermal Modules |

| Aluminum-Based |

| Copper-Based |

| Hybrid (Aluminum + Copper) |

| Data Center / AI GPUs |

| Workstation GPUs |

| Consumer / Gaming GPUs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Rest of South America | |

| Middle East and Africa |

| By Product Type | Heat Sinks | |

| Vapor Chambers | ||

| Heat Pipe-Based Modules | ||

| Active Thermal Modules | ||

| By Material | Aluminum-Based | |

| Copper-Based | ||

| Hybrid (Aluminum + Copper) | ||

| By GPU Type | Data Center / AI GPUs | |

| Workstation GPUs | ||

| Consumer / Gaming GPUs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the GPU heatsink and thermal module market?

The GPU heatsink and thermal module market size reached USD 3.1 billion in 2025 and is projected to grow to USD 3.44 billion in 2026 and USD 7.34 billion by 2031.

Which product type is expanding the quickest?

Vapor chambers lead growth with a forecast 17.17% CAGR because they handle 600-watt-plus GPUs more effectively than traditional heat pipes.

Why are data-center GPUs driving demand for liquid cooling?

AI accelerators such as NVIDIA's H200 and AMD's MI300X dissipate 700-750 watts, and hyperscale racks surpass 100 kilowatts, making liquid loops the only practical way to avoid thermal throttling.

How do commodity copper prices affect suppliers?

Price swings between USD 10,500 and USD 13,300 per tonne can trim 3-5 percentage points from manufacturer margins, prompting a shift toward hybrid aluminum-copper designs and long-term hedging contracts.

Which region dominates manufacturing and consumption?

Asia-Pacific holds 67.81% of revenue, supported by Taiwan's vapor-chamber ecosystem and China's large-scale assembly capacity, and is forecast to sustain the fastest regional CAGR through 2031.

What strategic moves are companies making to stay competitive?

Leading firms are pursuing vertical integration, OEM partnerships, and material innovation, exemplified by Aseteks long-term supply agreements and TaiSols 3D vapor-chamber technology.

Page last updated on: