Low Calorie Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

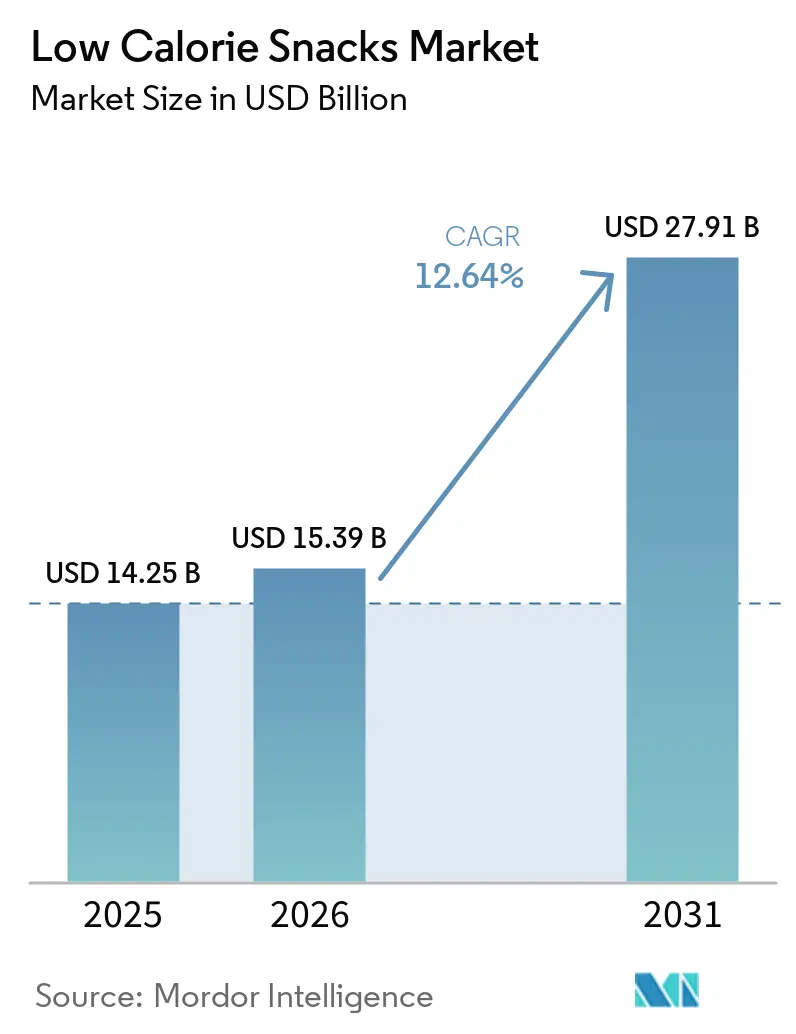

| Market Size (2026) | USD 15.39 Billion |

| Market Size (2031) | USD 27.91 Billion |

| Growth Rate (2026 - 2031) | 12.64% CAGR |

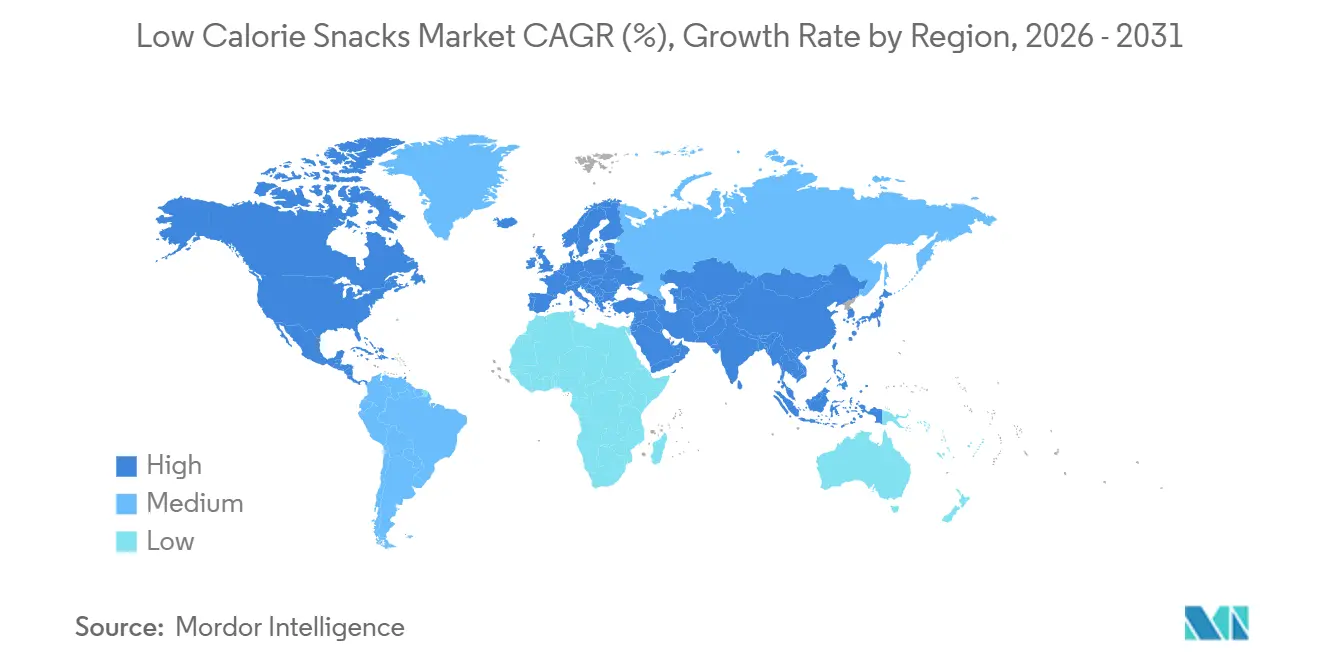

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Calorie Snacks Market Analysis by Mordor Intelligence

The Low Calorie Snacks Market size is expected to increase from USD 14.25 billion in 2025 to USD 15.39 billion in 2026 and reach USD 27.91 billion by 2031, growing at a CAGR of 12.6% over 2026-2031. As consumers increasingly seek snacks that are both satisfying and calorie-conscious, there's a notable shift in brand focus towards higher protein content, increased fiber, and cleaner ingredient lists. This evolution in the low-calorie snacks market is also evident in product designs, with established food companies emphasizing pack claims, innovative product formats, and a satiety-driven approach. Supermarkets dominate distribution, but online retail is rapidly gaining ground, offering newer brands a platform to build awareness before they expand into larger store networks. The competition is intensifying, with global snack giants leveraging acquisitions, reformulations, and brand extensions to secure shelf space. In contrast, smaller brands carve their niche through a sharper health focus. However, the challenge lies in execution: brands must bridge the gap in taste and texture, manage the costs of specialty ingredients, and avoid pricing themselves out of the market compared to conventional snacks.

Key Report Takeaways

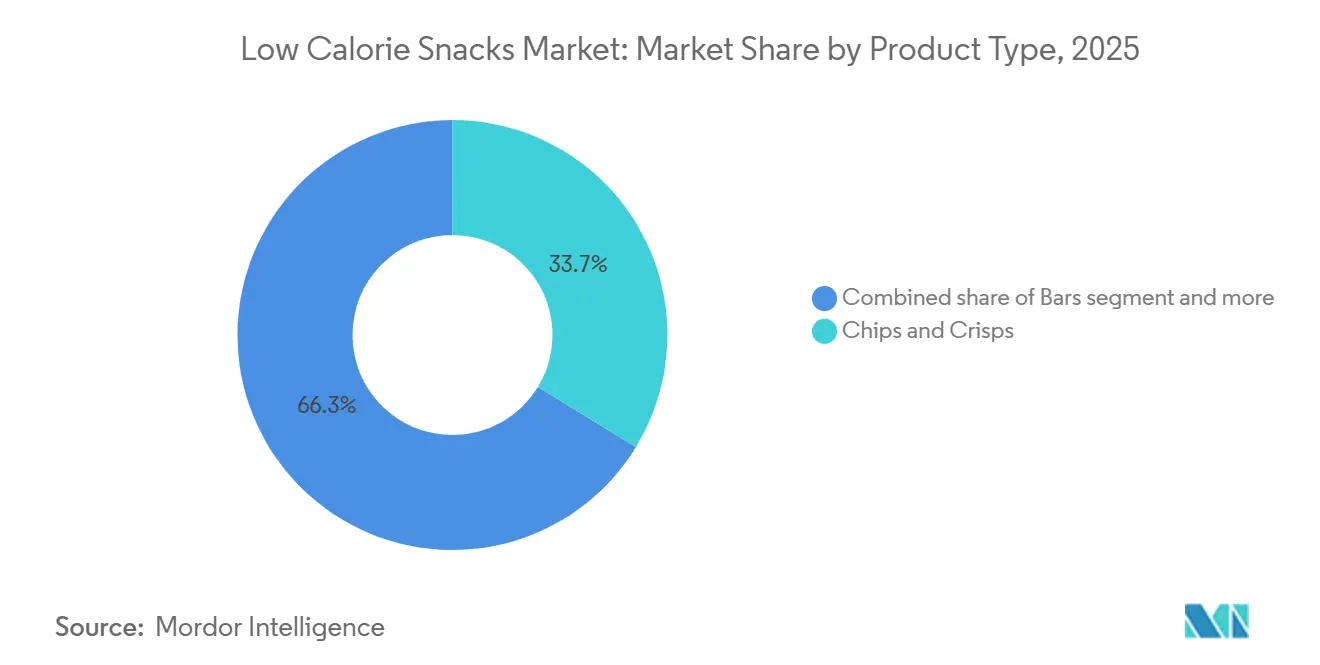

- By product type, chips and crisps accounted for the largest share of the low-calorie snacks market, at 33.7% in 2025, while bars are projected to grow at the fastest CAGR of 14.0% during 2026-2031.

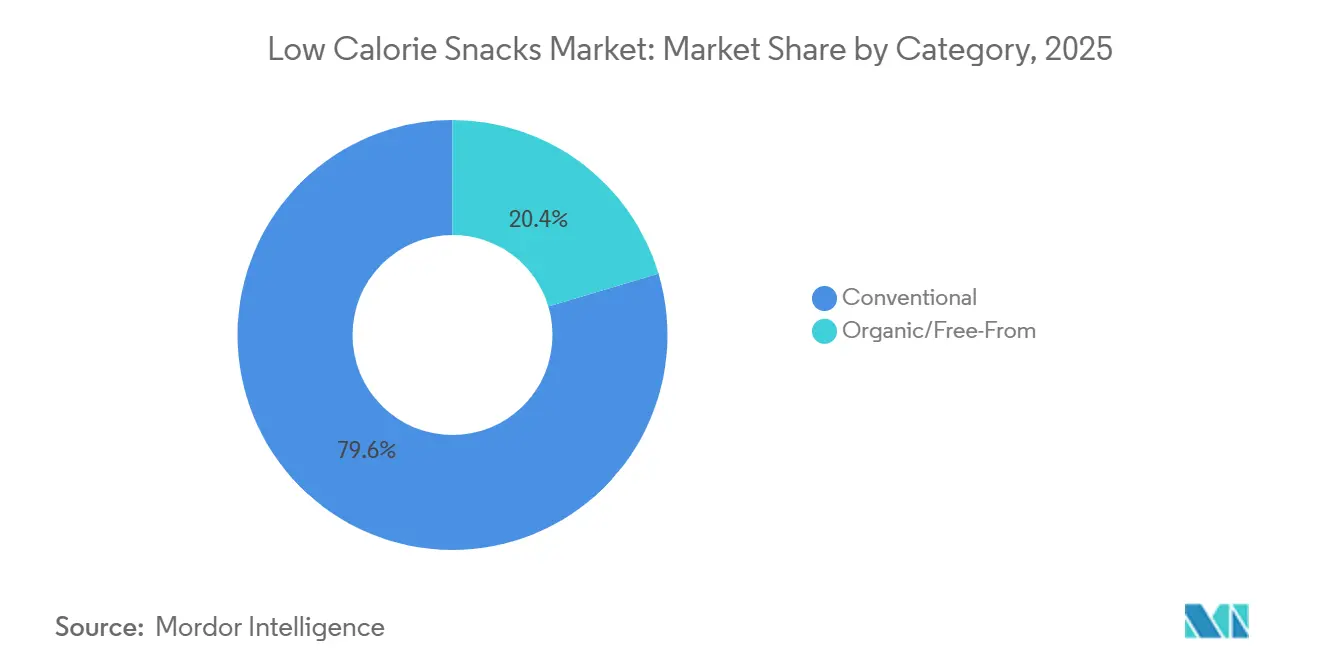

- By category, conventional products retained 79.6% share of the low-calorie snacks market in 2025, whereas organic and free-from products are forecast to expand at a 14.6% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for the largest share of the low-calorie snacks market, at 58.1% in 2025, while online retail is projected to grow at the fastest CAGR of 15.0% during 2026-2031.

- By geography, North America accounted for the largest share of the low-calorie snacks market, at 36.4% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 13.0% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Calorie Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Calorie-Controlled, High-Satiety Snacking | +2.1% | Global, led by North America and Western Europe, is expanding to the Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of Protein-Enriched and Fiber-Enriched Snack Innovation | +2.4% | Global, with the highest product launch density in North America and Europe | Short term (≤ 2 years) |

| Mainstream Retail and E-Commerce Assortment Expansion | +2.0% | Global, with early gains in North America, the Asia-Pacific, and Western Europe | Short term (≤ 2 years) |

| On-the-Go Snacking Lifestyle and Convenience Food Demand | +1.8% | Global, strongest in urban Asia-Pacific and North America | Medium term (2-4 years) |

| Clean-Label Reformulation and Sweetener Replacement Cycles | +1.5% | North America and Europe core, with spill-over to the Asia-Pacific urban centers | Medium term (2-4 years) |

| Snacking Migration into Weight-Management Routines and GLP-1 | +1.4% | North America (early leader), expanding to the United Kingdom, Europe, Japan, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for calorie-controlled, high-satiety snacking

The rising demand for calorie-controlled, high-satiety snacking is a major driver of the global low-calorie snacks market, as consumers increasingly seek products that support weight management while reducing hunger between meals. Government and health authorities such as the USDA and WHO continue to promote dietary patterns rich in protein, fiber, whole grains, fruits, vegetables, and legumes, reinforcing demand for snacks that deliver fullness without excessive calories. Research from nutrition and health organizations further highlights that protein- and fiber-rich foods enhance satiety and help control appetite, encouraging manufacturers to reformulate products around these attributes. Reflecting this trend, PepsiCo launched a line of air-popped reduced-calorie savory snacks in 2025, while Mondelez expanded its reduced-calorie, portion-controlled biscuit offerings for retail channels. Additionally, the industry is witnessing increased innovation in protein- and fiber-enriched snack bars, bites, popcorn, and crisps, addressing consumer demand for satisfying, guilt-free snacking experiences.

Expansion of protein-enriched and fiber-enriched snack innovation

New snack launches are increasingly anchored in protein, but fiber is swiftly emerging as an equally vital ingredient. Manufacturers now view both as essential components. In early 2026, PepsiCo's Frito-Lay rolled out SmartFood FiberPop, boasting 6g of fiber, and SunChips Fiber, with 3g of fiber per serving. Meanwhile, Quaker debuted Protein Rice Crisps, offering 6g of protein per serving, in April 2026 across US retailers[1]Source: PepsiCo, “Quaker Protein Rice Crisps Press Release,” PepsiCo, pepsico.com. Both products, crafted with pea protein and whole grains, proudly eschew artificial preservatives. PopCorners, traditionally known for its lightness, made a bold move into the functional snacking realm with its 2026 launch of Protein, featuring a robust 9g of protein per serving. This shift underscores a significant trend: the "protein-plus-fiber" co-fortification model is shrinking the gap between recognizing a clinical trend and seeing it on store shelves. This evolution favors manufacturers with nimble research and development capabilities, while those reliant on lengthy reformulation cycles find themselves at a disadvantage. Even challenger brands are making strides; HIPPEAS introduced Protein Crunch in May 2026, packing 8g of plant-based pea protein and boasting 55% less fat than top crunchy puffs, showcasing their ability to rival established formats[2]Source: HIPPEAS, “Protein Crunch Launch,” HIPPEAS, hippeas.com.

Snacking migration into weight-management routines and GLP-1

GLP-1 drugs are reshaping the demand for low-calorie snacks, shifting the focus from mere health awareness to a more therapeutic nutritional alignment. Currently, about 1 in 8 US adults are on GLP-1 medications like Ozempic or Zepbound. Their consumption patterns in 2026 show a more structured and sustained approach than in 2025, indicating a deepening trend rather than a fleeting change. In response, Conagra, in January 2025, marked 26 of its Healthy Choice items with an "On Track" badge, highlighting their GLP-1 compatibility. Meanwhile, General Mills ramped up its innovations in 2026, introducing GLP-1-friendly formats like Cheerios Protein, Fiber One, and Ghost Performance Nutrition bars. This trend signals to market players that GLP-1 users represent a brand-loyal segment, willing to pay a premium for products that align with their therapeutic needs. This shift is proving especially advantageous for the low-calorie snack sector, outpacing benefits seen in more indulgent categories.

Mainstream retail and e-commerce assortment expansion

Both physical and digital retail channels are reshaping the distribution landscape for low-calorie snacks. In 2025, supermarkets and hypermarkets accounted for 58.13% of revenue, underscoring their dominance for planned grocery trips. However, online channels are experiencing a more rapid growth. Social commerce is becoming a significant avenue for first-time purchases: In 2025, snack sales on TikTok Shop in the US outpaced the overall growth of online snack sales, and the UK saw similar growth on TikTok Shop. Low-calorie snack brands enjoy a unique advantage: niche, health-focused brands can cultivate direct-to-consumer audiences online, bypassing the slotting fees and volume requirements of physical stores. This online presence acts as a testing ground, paving the way for broader physical retail expansion. Mondelez's Q1 2026 earnings highlighted this trend, noting that convenience, club, and online channels effectively balanced out declining volumes in US biscuit sales, underscoring the strategic importance of cross-channel distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and Texture Gaps Versus Conventional Snacks | -0.8% | Global, most acute in emerging markets where taste parity expectations are high | Medium term (2-4 years) |

| Consumer Skepticism Toward Highly Processed Health Claims | -0.6% | Global, with North America and Europe as primary skepticism centers | Medium term (2-4 years) |

| Premium Pricing and Margin Pressure from Specialty Ingredients | -0.9% | Global, with the highest pressure in North America and Europe | Short term (≤ 2 years) |

| Reformulation Risk from Sweetener, Fiber, and Allergen Tolerability | -0.5% | Global, the strongest impact in markets with high allergen-labeling enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taste and texture gaps versus conventional snacks

Consumers often use traditional full-calorie snacks as a benchmark, posing a challenge for low-calorie alternatives. Formats like air-popped, baked, and protein-fortified often fall short in replicating the density, crunch, and mouthfeel of their fried or sugar-laden counterparts. This gap is evident in repeat-purchase rates, which highlight the difference between one-time trials and habitual consumption. While smaller companies are making strides with novel techniques like freeze-drying and high-shear extrusion, using bases like pea or rice protein, they face challenges in scaling these methods without alienating price-sensitive consumers. The crux of the issue lies in the dual nature of snacking satisfaction: it's both physiological and psychological. Consumers have ingrained associations with textures deemed "authentic," and any reformulated product must navigate these perceptions to encourage repeat purchases. Without significant advancements in processing and a shift in consumer perceptions, the journey from mere awareness to brand loyalty will remain unfulfilled for a substantial portion of the target market.

Premium pricing and margin pressure from specialty ingredients

Low-calorie snack formulations increasingly depend on specialty proteins (like whey, pea, and casein), alternative sweeteners (such as allulose, stevia, and monk fruit), and fiber-rich substrates (including chicory root inulin and oat beta-glucan). These ingredient categories come with structural costs that are significantly higher than conventional commodity inputs. In early 2026, under pressure from activist investor Elliott Management, which had amassed a stake of around USD 4 billion, PepsiCo slashed snack prices by as much as 15% and trimmed its US product lineup by 20%. This move highlights the challenges even major players face in managing margins while shifting towards functional ingredients. The Simply Good Foods Company, which owns Quest and Atkins, adjusted its fiscal 2026 net sales forecast to a decline of 10% to 7% year-over-year[3]Source: The Simply Good Foods Company, “Q2 Fiscal 2026 Earnings,” The Simply Good Foods Company, thesimplygoodfoodscompany.com. The company also anticipates a drop in gross margins by 300 to 350 basis points, attributing this partly to ingredient cost challenges and a slowdown in its Atkins line's sales. Brands that secure long-term supply agreements or move towards proprietary processing are likely to enjoy better margin profiles compared to those dependent on spot-price procurement of specialty ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reformulation Reshapes Value Share Across the Snack Aisle

In 2025, chips and crisps held a 33.71% revenue share, the largest among all product types. This dominance stems from widespread savory snack consumption and the reformulation of baked, popped, and air-puffed variants, which now sit alongside traditional fried options. The segment benefits from two key channels: supermarkets drive volume sales, while e-commerce and convenience stores promote premium, protein-fortified chip variants with higher margins. PepsiCo's February 2026 launch of Doritos Protein (10g protein per 1 oz serving) highlights the shift of chips from calorie-conscious snacks to functional nutrition. Popcorn, nuts, seeds, and crackers occupy distinct niches: popcorn for between-meal snacking, nuts and seeds for health-focused grazing, and crackers as lunchtime companions. All three are undergoing clean-label and organic transformations to meet rising demand for ingredient transparency.

Bars are the fastest-growing product category, with a 13.96% CAGR from 2026 to 2031, driven by their versatility as on-the-go meal replacements, post-workout nutrition, and GLP-1-complementary high-protein solutions. KIND's January 2026 launch of Protein Max Granola (15g protein, 9g fiber per serving) and Protein Max Bars (20g protein, 1g added sugar) reflects the shift from simple nut-and-fruit blends to clinically aligned macronutrient profiles. Cookies, though the smallest segment by growth priority, are becoming a space for "permissible indulgence." Mondelez's CLIF Builders, with its June 2026 launch of White Fudge OREO (20g protein), exemplifies the merging of indulgent and functional formats, challenging traditional segmentation models.

By Category: Conventional Dominates Volume; Organic/Free-From Drives Value Premiumization

From 2026 to 2031, the organic and free-from category is projected to grow at a blistering pace of 14.61% CAGR, outpacing all other segments. This surge is fueled by a confluence of factors: the Make America Healthy Again (MAHA) movement, a rising cohort of GLP-1 users favoring chemical-free ingredients, and Gen Z's embrace of organic certification as a badge of social identity. By 2025, the US organic snacks and candy market hit a notable USD 5.3 billion, marking a 7.3% annual uptick. Notably, nutrition bars broke the USD 2 billion sales milestone for the first time. Furthermore, a survey revealed that 38% of organic companies anticipate a boost in demand for organic snacks in 2026, driven by the growing adoption of GLP-1 drugs. Achieving USDA organic certification and Non-GMO Project verification has become a dual-edged sword: while they serve as stringent compliance benchmarks, they also act as gatekeepers, sidelining smaller entrants from premium shelf spaces. For established organic brands, this dynamic not only raises switching costs but also fortifies their market position, creating both a barrier to entry and a protective pricing umbrella.

In 2025, conventional products commanded a dominant 79.62% share of the category's revenue, underscoring the continued strength of mainstream brands. Yet, as the market evolves, it's evident that while volume flows predominantly through these conventional channels, the fresh growth dollars are gravitating towards the organic and free-from segment. The launch of Frankie's Organic Snacks in over 500 Target stores in June 2026 underscores the mainstream viability of organic products, breaking the confines of natural and specialty channels. This shift towards mainstream retail is narrowing the premium divide between organic and conventional low-calorie snacks, potentially enticing households that have traditionally shied away from organic offerings to give them a try.

By Distribution Channel: Supermarkets Lead; Online Channels Accelerate Discovery

Online retail is set to dominate the low-calorie snacks market, boasting a projected CAGR of 14.98% from 2026 to 2031. This surge underscores the dual forces of grocery digitization and the meteoric rise of social commerce as a primary discovery tool. In 2025, snack sales on TikTok Shop in the US outpaced the overall online snack sales growth. This disparity highlights social commerce's role in forging a novel purchasing route, one that sidesteps traditional shelf placements. This shift favors niche, health-oriented brands. Unlike physical retail, which often imposes slotting fees and volume minimums, the online realm acts as a breeding ground for innovations, paving the way for their eventual inclusion in supermarket assortments. Mondelez's Q1 2026 investor update revealed that channels like convenience, club, and online were instrumental in counterbalancing a dip in US biscuit category volumes.

In 2025, supermarkets and hypermarkets commanded a 58.13% revenue share, a testament not just to their historical dominance but to strategic investments by major players in category management, promotions, and product placements, especially for health-centric ranges. Convenience stores, catering to the on-the-go consumer, are now prioritizing single-serve, protein-rich, and fiber-forward snacks, adapting to the evolving snacking habits throughout the day. Meanwhile, direct-to-consumer subscription services and club stores are emerging as pivotal arenas for gauging price sensitivity and loyalty. Many budding brands are leveraging club channel launches as a litmus test for volume before casting a wider net in supermarkets.

Geography Analysis

In 2025, North America held a 36.40% share of the global low-calorie snacks market revenue, driven by the U.S.'s mature retail infrastructure, high GLP-1 drug penetration, and a focus on calorie tracking and nutritional labeling. PepsiCo's 2026 portfolio shake-up, reducing its U.S. lineup by 20% and introducing products like Doritos Protein and Quaker Protein Rice Crisps, highlights its response to evolving snacking preferences. Canada shows strong growth per Mondelez's Q1 2026 report, while Mexico is emerging as a manufacturing hub. PepsiCo's USD 467 million Sabritas plant in Celaya, part of a USD 2 billion investment through 2028, reflects confidence in Mexico as Latin America's largest consumer economy. Europe, the second-largest market, is transforming due to the EU's Nutri-Score labeling and Packaging Waste Directive. Clean-label products are expected to exceed 70% of EU food and beverage portfolios by 2025–2026, up from 52% in 2021, as clean formulations become a competitive standard.

Asia-Pacific is the fastest-growing market, with a 12.98% CAGR from 2026 to 2031. China, Japan, India, and Southeast Asia are driving growth through distinct demand dynamics. A 2026 survey by Glico and First Finance found 67.04% of Chinese consumers willing to pay a premium for health-labeled snacks, with 45.67% monitoring health attributes during purchases. This is reshaping product development for domestic and international brands in China. In Japan, wellness culture and an aging population sustain demand for portion-controlled, enriched snacks. Calbee's 2026 revamp of Harvest Snaps packaging, emphasizing fiber and protein, reflects this trend. In India, the Food Safety and Standards Authority (FSSAI) has simplified food business licensing, while smartphone penetration is driving e-commerce growth in Tier-2 cities.

South America and the Middle East & Africa are early-stage but expanding markets. Rising disposable incomes, urban retail modernization, and growing health awareness are attracting multinational and regional brands to better-for-you snacks. Brazil and the UAE are the most developed sub-markets, with new SKU launches from global manufacturers targeting growth beyond saturated developed markets. PepsiCo's Mexico manufacturing investment underscores confidence in Latin America's growth potential, while UAE-based distribution hubs are facilitating regional launches for U.S. and European health-centric snack brands into Gulf Cooperation Council markets. South America faces challenges like foreign exchange volatility and high ingredient import costs, which reduce the price competitiveness of premium imported snacks. Local manufacturing partnerships are becoming essential for brands aiming for a durable presence in markets like Argentina, Colombia, and Peru.

Competitive Landscape

The low-calorie snacks market is moderately concentrated at the top, yet remains crowded in the middle and premium tiers. Major players like PepsiCo, Nestlé, Mondelez International, General Mills, Mars, and The Hershey Company leverage extensive distribution networks, strong retailer relationships, and significant trade spending capabilities. This scale not only aids in reformulation and product launches but also secures shelf space amidst rising competition. Meanwhile, niche brands are challenging these giants with offerings centered on protein, fiber, organic ingredients, and health-conscious propositions. This interplay of scale and agility is influencing the evolution of the low-calorie snacks market, both in physical stores and online.

In a bold strategic move, PepsiCo acquired Siete Foods for USD 1.2 billion in January 2025 and Poppi for USD 1.95 billion in May 2025. In 2026, it revamped its snack lineup, introducing Doritos Protein, PopCorners Protein, SmartFood FiberPop, SunChips Fiber, and Quaker Protein Rice Crisps. Conagra Brands, in 2025, strategically added an On Track badge to 26 Healthy Choice items, aligning them with a GLP-1-friendly positioning. Meanwhile, KIND ventured deeper into performance snacking in January 2026, launching Protein Max Granola and expanding its Protein Max Bars. These moves underscore the fierce competition between global giants and specialized brands, both vying for repeat purchases in the low-calorie snacks arena.

While innovation is crucial, execution holds equal weight. Factors like price, texture, and ingredient economics can swiftly curtail the commercial potential of a well-placed product. Highlighting this vulnerability, The Simply Good Foods Company adjusted its fiscal 2026 net sales outlook downward, citing anticipated margin pressures from ingredient costs. Mondelez, in its Q1 2026 earnings call, noted that channels like convenience, club, and online helped counteract weaker U.S. biscuit volumes, underscoring the importance of channel diversification in the dynamic snack landscape. Hershey, during its 2026 Investor Day, set its sights on clinching the number 2 spot in U.S. salty snacks, indicating the ongoing fierce competition in the low-calorie snacks market as top players chase the same health-conscious consumer base.

Low Calorie Snacks Industry Leaders

PepsiCo, Inc.

Nestle S.A.

Mondelez International, Inc.

General Mills, Inc.

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Frankie's Organic Snacks launched across 500+ Target stores and Target.com, representing its largest US retail rollout to date and expanding its footprint to over 1,500 locations nationwide, signaling mainstream retailer commitment to USDA-certified organic puffed snack formats.

- June 2026: Mondelez International's CLIF BUILDERS brand introduced the White Fudge OREO-flavored protein bar, extending a 2025 collaboration into a new high-protein (20g+) format available across Albertsons, Meijer, Hy-Vee, and Amazon.

- May 2026: HIPPEAS launched Protein Crunch, 8g of plant-based pea protein per 1 oz serving, baked, not fried, with 55% less fat than leading crunchy puffs, marking the brand's entry into mainstream protein snacking beyond its chickpea puff origins.

Global Low Calorie Snacks Market Report Scope

A low-calorie snack is a small portion of food eaten between meals that provides a low amount of energy. The global low calorie snacks market is segmented by product type, category, distribution channel, and geography. By product type, the market is segmented into bars, chips and crisps, popcorn, nuts and seeds, crackers, cookies, and other types. By category, the market is segmented into conventional and organic/free-from. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Bars |

| Chips and Crisps |

| Popcorn |

| Nuts and Seeds Snacks |

| Crackers |

| Cookies |

| Other Product Types |

| Conventional |

| Organic/Free-From |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Bars | |

| Chips and Crisps | ||

| Popcorn | ||

| Nuts and Seeds Snacks | ||

| Crackers | ||

| Cookies | ||

| Other Product Types | ||

| Category | Conventional | |

| Organic/Free-From | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What will the low calorie snacks market be worth by 2031?

The low calorie snacks market will reach USD 27.91 billion by 2031, up from USD 15.39 billion in 2026, at a 12.6% CAGR over 2026-2031.

Which product type leads revenue in low calorie snacks?

Chips and crisps led revenue with a 33.7% share in 2025, supported by strong demand for savory snacks and continued reformulation into baked, popped, and air-puffed formats.

Which product segment is growing the fastest in low calorie snacks?

Bars are projected to grow at a 14.0% CAGR through 2031, helped by demand for on-the-go meal replacement, post-workout use, and high-protein formats.

Are organic and free-from snacks gaining ground faster than conventional options?

Yes. Organic and free-from products are forecast to grow at a 14.6% CAGR through 2031, while conventional products still held the larger 79.6% revenue share in 2025.

Page last updated on: