Protein Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

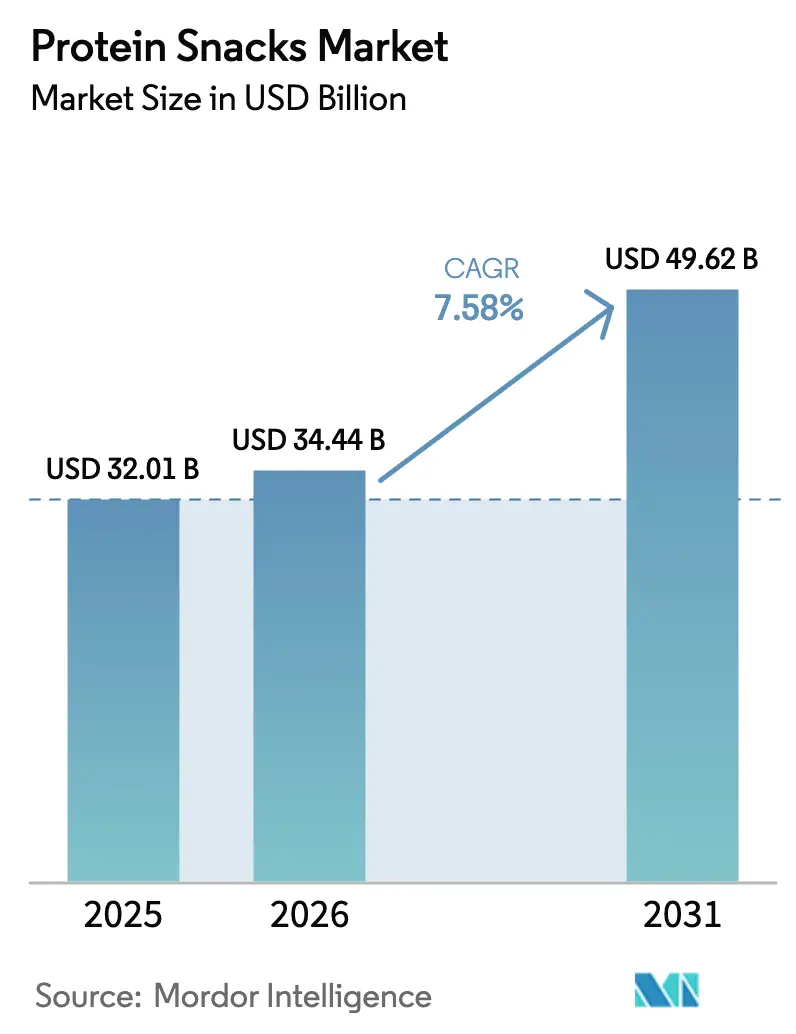

| Market Size (2026) | USD 34.44 Billion |

| Market Size (2031) | USD 49.62 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

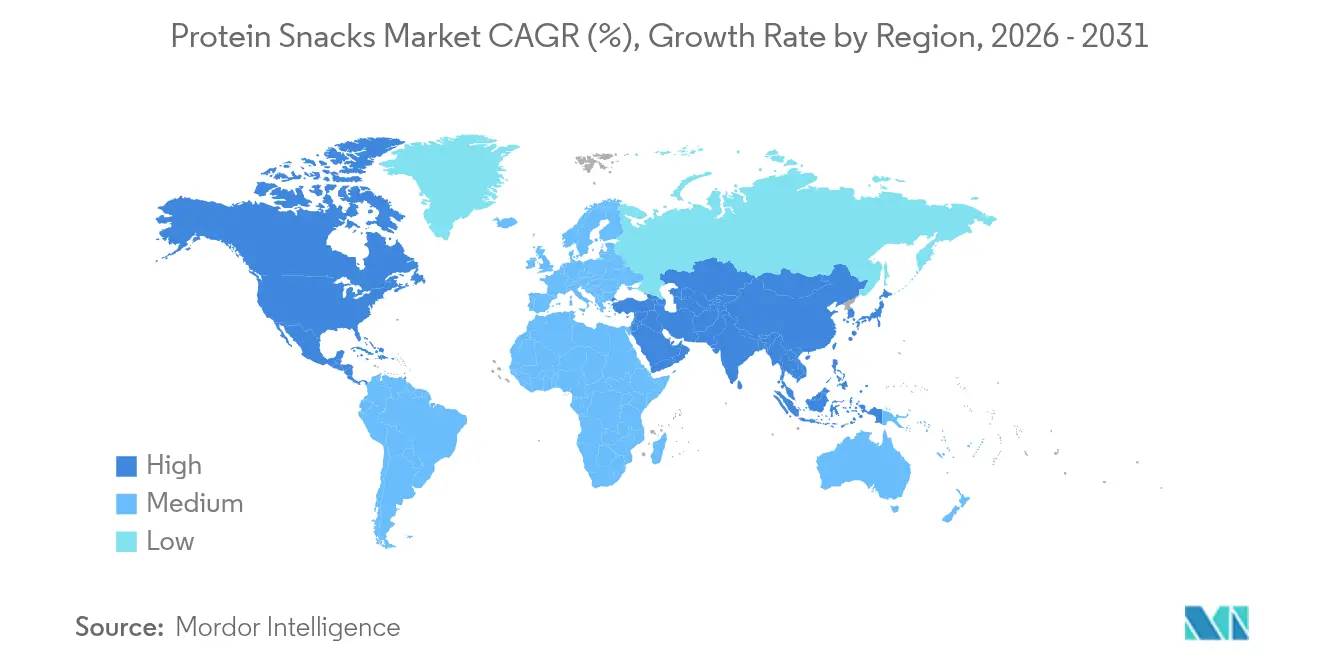

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

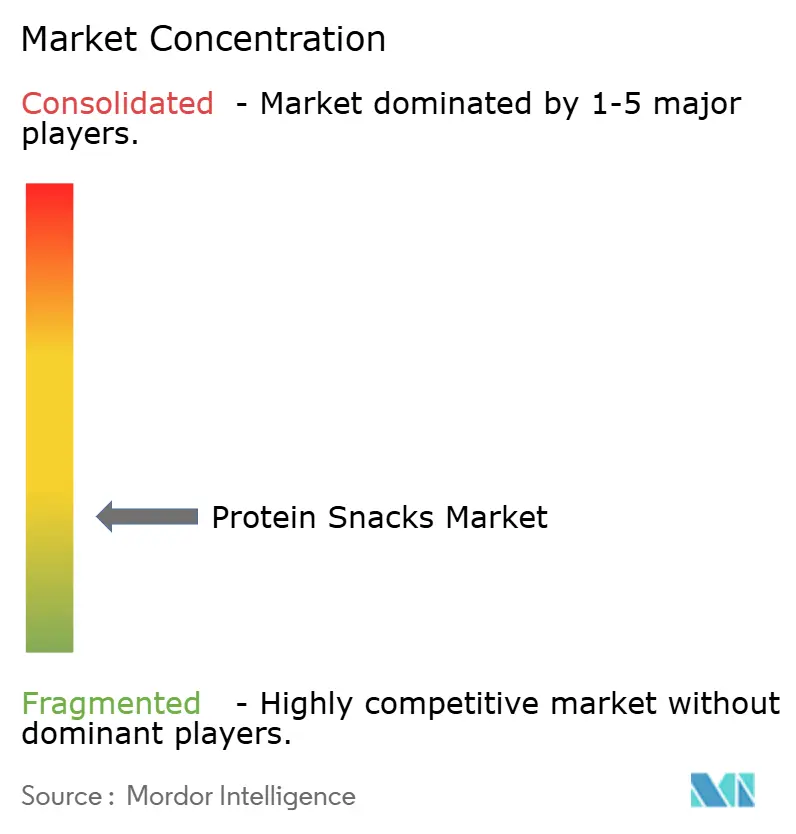

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Protein Snacks Market Analysis by Mordor Intelligence

Protein snacks market size in 2026 is estimated at USD 34.44 billion, growing from 2025 value of USD 32.01 billion with 2031 projections showing USD 49.62 billion, growing at 7.58% CAGR over 2026-2031. Starting in 2025, the FDA's revamped definition of "healthy" is poised to bolster regulatory clarity and boost confidence in labeling. This shift will likely empower a greater number of protein snack products to assert health claims. Such regulatory backing is fueling market innovation, spotlighting emerging technologies like fermentation, cultivated protein production, and insect-based protein, all lauded for their sustainability and cost-effectiveness. While traditional animal-derived proteins maintain their dominance, there's a notable surge in plant-based and alternative protein formats. North America remains at the forefront of market adoption, buoyed by a strong distribution network and a discerning consumer base. In contrast, the Asia-Pacific region is rapidly emerging as a growth hotspot, driven by increasing income levels and heightened urban health consciousness. The rise of e-commerce and direct-to-consumer channels is revolutionizing access to protein snacks, particularly among the younger, tech-savvy crowd. Products like RXBARs, Jack Link’s beef jerky, and KIND protein bars underscore the market's pivot towards shelf-stable, nutrient-rich offerings that seamlessly blend convenience with health benefits.

Key Report Takeaways

- By product type, meat snacks captured 55.02% of the protein snacks market share in 2025; Chips & Crisps are forecast to expand at a 9.02% CAGR through 2031.

- By protein source, animal-derived formats accounted for 68.10% of the protein snacks market size in 2025, while fermented, cultivated, and insect proteins are projected to grow at a 10.05% CAGR between 2026-2031.

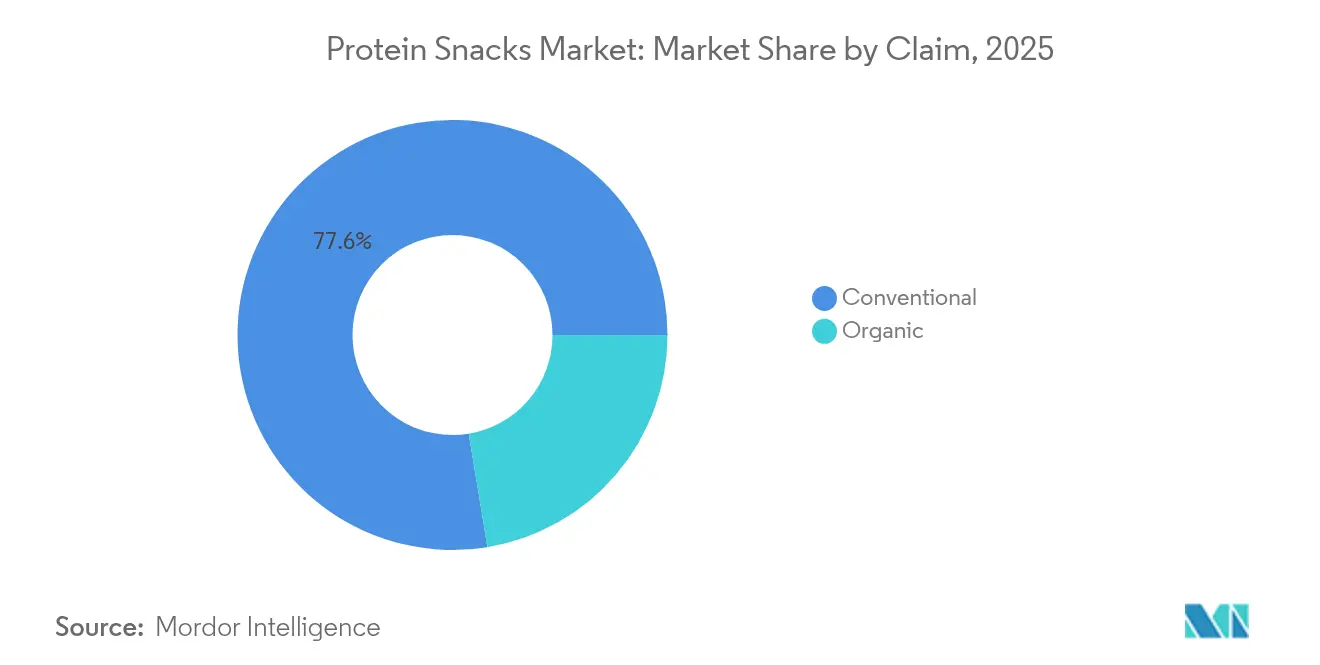

- By claim, conventional products held 77.60% revenue share in 2025; organic variants are anticipated to advance at a 9.08% CAGR to 2031.

- By distribution channel, supermarkets & hypermarkets maintained 41.70% share of the protein snacks market size in 2025, whereas online retail is expected to rise at a 9.35% CAGR through 2031.

- By geography, North America led with 37.55% of the protein snacks market share in 2025, and Asia-Pacific is poised for the quickest expansion at 9.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for higher daily protein intake | +1.8% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Rising sports participation and fitness culture among youth | +1.2% | Global, strong in Asia-Pacific and North America | Medium term (2-4 years) |

| Demand for convenient, on-the-go snacking options | +1.4% | Global, urban centers | Short term (≤ 2 years) |

| Product innovation spanning new flavors, formats and ingredients | +1.0% | North America and Europe leading | Medium term (2-4 years) |

| Clean-label and natural ingredient focus boosting trust | +0.9% | North America and Europe | Medium term (2-4 years) |

| Celebrity and influencer collaborations driving trial | +0.5% | Global, social-media-driven markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Awareness and Preference for Higher Protein Intake as a Lifestyle Change

Consumer preference for high-protein diets is driving demand in the hot dogs and sausages market, which caters to modern dietary priorities with its convenient, protein-dense offerings. As protein consumption gains traction, especially among women and Gen Z, categories like sausages, once predominantly male, are now enjoying wider appeal. In 2024, brands such as Applegate and Hebrew National rolled out clean-label, protein-centric products, including organic turkey sausages and low-sodium beef franks, specifically targeting health-conscious consumers. Platforms like TikTok, where high-protein meal prep content frequently goes viral, have transformed items like chicken sausages from occasional treats to daily staples. Cargill’s 2025 Protein Profile highlighted that 61% of consumers upped their protein intake in 2024 [1]Source: Cargill, “2025 Protein Profile,” cargill.com. Concurrently, the International Food Information Council (IFIC) noted a rise in the percentage of U.S. consumers aiming for higher protein intake, jumping from 59% in 2022 to 71% in 2024 [2]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org. This protein-centric trend has also spurred growth in complementary snack segments, with retail favorites like Jack Link’s Beef Jerky, KIND Protein Bars, and Premier Protein Shakes taking center stage, underscoring the expanding footprint of protein-focused consumption.

Increased Sports Participation and Fitness-Oriented Culture Among Younger Demographics

As younger generations increasingly embrace strength training and fitness, the demand for packaged protein snacks is surging. These consumers are on the lookout for convenient, high-protein options that aid in muscle growth and recovery. According to the CDC’s 2023 Youth Risk Behavior Survey, U.S. adolescents are once again engaging in muscle-strengthening exercises at least three times a week, reversing a prior downward trend [3]Source: Centers for Disease Control and Prevention, “Youth Risk Behavior Survey 2023,”cdc.gov. This shift in behavior is spurring a demand for functional snacks that fit seamlessly into active lifestyles. In 2024, products such as Quest Protein Bars, Jack Link’s Beef Jerky, and Premier Protein Shakes saw heightened visibility at retail chains like Target and CVS, specifically targeting gym enthusiasts, athletes, and the fitness-savvy. These products resonate with younger consumers who view protein as pivotal for their performance and body composition aspirations. This trend isn't confined to the U.S.; in the Asia-Pacific region, a surge in youth gym enrollments and a fitness-centric social media culture are driving demand for portable, high-protein snacks like chips, bites, and ready-to-drink shakes. As strength training transitions from a niche pursuit to a mainstream lifestyle, the consumption of protein snacks is becoming commonplace, propelling the expansion of the broader category.

Convenience and On-the-Go Snacking Options

As busy lifestyles take center stage, the packaged protein snacks market is witnessing a surge, especially in formats like cookies, crisps, yogurt cups, and ready-to-drink shakes. Consumers are increasingly favoring these portable, functional nutrition options over traditional meals. According to Mondelez’s 2024 State of Snacking report, 60% of global consumers now opt for multiple small snacks throughout the day, with a striking 91% snacking daily. This underscores convenience as a key driver of consumption. In response, brands have rolled out innovations catering to this on-the-go demand. Notable offerings include Good Culture’s Protein-Packed Cottage Cheese Cups, Enlightened Protein Puffs, and Oikos Pro Yogurt Drinks. These products, boasting high protein content and resealable, single-serve formats, have found a home in outlets like Walgreens and Kroger, prominently displayed in grab-and-go or wellness sections. E-commerce models, particularly subscription-based ones from Core Power and Catalina Crunch, further bolster accessibility, enabling consumers to stock up on protein snacks for work, travel, or gym sessions. This shift towards convenience is not just altering the snacking landscape but is also amplifying the significance of protein-rich packaged snacks in daily eating habits.

Celebrity and Influencer Collaborations Fueling Demand Surge

Celebrity and influencer collaborations are reshaping the packaged protein snacks market, especially among Gen Z and urban millennials, turning everyday consumption into a lifestyle statement. Brands are tapping into the cultural sway of celebrities, with 52% of consumers trying new protein products after online exposure, to enhance visibility and trust. A notable instance in November 2024, SuperYou, was co-founded by Bollywood actor Ranveer Singh. SuperYou introduced high-protein chips, wafers, and bars, catering to the Indian youth's desire for functional yet trendy snacks. Owing to its bold, social-media-centric marketing and celebrity endorsement. Fitness influencers on platforms like TikTok and Instagram amplify this trend, showcasing protein bars and chips in recipe hacks and “what I eat in a day” segments, thereby reshaping consumer perceptions of taste and performance. Global players, including Barebells and Lenny & Larry’s, are riding this wave, leveraging influencer-generated content and exclusive limited-edition releases to boost engagement and trial. This evolving consumer mindset, viewing protein snacks as both aspirational and accessible, is broadening the category's appeal and speeding up the adoption of premium products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs for premium protein sources | -1.2% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Allergen concerns with whey, soy and nut proteins | -0.8% | North America and Europe | Medium term (2-4 years) |

| Taste and texture challenges vs. traditional snacks | -0.6% | Global, especially plant-based formats | Medium term (2-4 years) |

| Consumer price sensitivity in lower-income markets | -0.9% | Emerging markets and value segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs, Especially for High-Quality Protein Sources

In 2024, disruptions in the dairy supply chain and fluctuations in energy costs led to a 20–50% surge in whey protein prices. This spike has had a direct effect on the pricing of products such as ready-to-drink shakes, protein bars, and yogurts, all of which heavily rely on whey. Further compounding these challenges, the USDA forecasts a 41.1% rise in egg prices for 2025. Such inflationary pressures are pushing brands to either reformulate their products, reduce sizes, or hike retail prices, consequently making them less affordable for budget-conscious consumers. Adding to the woes, regulatory trade actions have intensified the situation. In 2023, the U.S. slapped a hefty 122.19% dumping margin on Chinese pea protein, a rapidly growing plant protein source. This move not only disrupted the supply chain but also nudged brands towards pricier alternatives. Smaller brands, on the other hand, grapple with manufacturing bottlenecks. The capital-intensive nature of protein-fortification processes demands precision equipment and energy, straining their resources. This financial strain not only tightens profit margins but also stifles innovation and curtails market penetration in emerging economies, hindering global expansion efforts.

Price sensitivity among consumers

Despite a growing awareness of health and fitness, many consumers still view protein snacks as luxury items rather than daily essentials. High-quality ingredients, such as whey isolate, nut butters, and grass-fed meats, push prices up, creating a psychological hurdle for potential buyers, especially when immediate benefits aren't evident. Younger consumers, particularly college students and early-career professionals, often see protein snacks as "aspirational" treats, indulging post-workout or during specific routines, but not as daily snacks due to budget constraints. Price-sensitive families, especially in lower and middle-income brackets, prioritize volume and fullness over nutritional benefits. They often choose multi-pack conventional snacks, which provide more quantity for the same price as a single protein bar. Even those motivated by health hesitate if protein snacks don't seem to offer value, be it in taste, portion size, or energy boost relative to their price. In retail settings, consumers often pit protein snacks against traditional options like chips, cookies, or granola bars. Faced with a 40–80% price difference, many set aside their initial interest in protein snacks. While promotions can spark first-time purchases, they seldom lead to habitual buying once regular prices resume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat Snacks Lead While Innovation Diversifies

In 2025, meat snacks dominate the market, seizing 55.02% of the total share. This dominance underscores a robust consumer inclination towards complete protein sources, convenience, and savory flavors. The segment's maturity is bolstered by established retail placements and a high rate of repeat purchases. Brands like Country Archer exemplify this momentum, with sales hitting USD 200 million in 2024 and projected to soar to USD 300 million by 2025. This growth is fueled by innovations such as the Ancestral Beef Blend Meat Sticks, catering to the surging demand for nutrient-dense, functional meat products.

Chips and crisps are the market's fastest-growing category, boasting a CAGR of 9.02% through 2031. Their swift ascent underscores the successful protein fortification of traditional snacks, maintaining taste and texture. Biena’s Crispy Edamame, with its 13 grams of protein per serving, epitomizes this trend, matching the protein standards of staples like eggs. Protein Bars serve as a primary entry point for many consumers, with high-protein variants raking in nearly USD 1.5 billion, thanks to their functional convenience and portability. Newer segments like cookies and bites and puddings, and yogurts are diversifying the landscape, merging indulgence with protein benefits. In contrast, ready-to-drink shakes are grappling with stiff competition from solid snacks, which resonate more with evolving consumer desires for satiety and texture.

By Protein Source: Animal Proteins Dominate While Alternatives Accelerate

In 2025, animal-derived proteins command a dominant 68.10% market share, owing to their superior amino acid profiles, high bioavailability, and longstanding consumer trust. Whey and casein play pivotal roles in crafting protein bars and ready-to-drink shakes, enjoying the benefits of a well-established processing infrastructure and widespread acceptance. Meat-based proteins, particularly those featured in jerky, sticks, and fortified chips, continue to entice consumers with their familiar flavors and satiating qualities. Meanwhile, hybrid protein products melding dairy with meat or plant-based elements are garnering attention for their nutritional and taste balance.

Fermented, cultivated, and insect proteins are the fastest-growing segment, boasting a CAGR of 10.05% projected through 2031. A consumer shift towards sustainability, innovative food technologies, and a broader protein source diversification drives this surge. Innovations in packaged products underscore this trend, with offerings like Brave’s Roasted Crickets, packing 14g of protein per serving, and Quorn’s mycoprotein snacks, now prominently featured in high-protein snack sections across the United Kingdom and select international markets. Such advancements herald a wave of opportunities for clean-label, ethically sourced snacks, resonating with the evolving values of today's consumers.

By Claim: Conventional Products Lead While Organic Gains Premium

In 2025, conventional protein snacks dominated the market with a 77.60% share, thanks to their cost-effectiveness and widespread appeal. Established supply chains, reduced production expenses, and extensive retail presence position conventional products as the go-to for budget-conscious consumers. Retail giants, recognizing this trend, are amplifying their private label offerings. Notable examples include Aldi’s Millville protein bars and Walmart’s Pure Protein line, both targeting mainstream shoppers who prioritize functional benefits without straining their wallets. This edge in affordability not only boosts purchase volumes but also cements brand loyalty across mainstream retail channels.

On the other hand, organic protein snacks are on an upward trajectory, boasting a 9.08% CAGR through 2031. This surge underscores a growing consumer preference for clean-label, minimally processed products that resonate with health and environmental consciousness. Brands such as Orgain and RXBAR Organic have carved a niche by spotlighting their certified organic ingredients and steering clear of artificial additives. Furthermore, the FDA’s revamped "healthy" claim regulations, set to roll out in February 2025, are poised to bolster the allure of organic-centric products.

By Distribution Channel: Supermarkets/Hypermarkets Dominates While E-commerce Surges

In 2025, supermarkets/hypermarkets capture a 41.70% market share, thanks to their widespread physical presence and deep integration into consumers' weekly shopping habits. These retailers capitalize on impulse buying, in-store promotions, and collaborations with leading protein snack brands, ensuring these products enjoy prime shelf space. Brands such as Pure Protein and Quest Nutrition leverage this channel's visibility, utilizing multi-pack formats and endcap displays to promote trial and bulk purchases. With its vast assortment and easy accessibility, this format stands out as the primary channel for mass-market protein snack distribution.

Online retail stores are emerging as the fastest-growing channel, boasting a projected CAGR of 9.35% through 2031, driven by a digital transformation in shopping habits. Brands like Chomps and ALOHA, operating on a direct-to-consumer model, harness subscription services and social media marketing to cultivate loyalty and ensure repeat sales. Meanwhile, Amazon broadens consumer choices with its private label and third-party marketplace offerings, though these come with a reliance on platform algorithms and logistics. Specialty sports and health stores maintain their niche allure with curated selections and expert staff. In contrast, Convenience and grocery stores, situated in bustling urban locales, cater to on-the-spot consumption needs. As omnichannel shopping becomes the norm, brands are increasingly merging their online and offline strategies to provide a cohesive and tailored shopping journey.

Geography Analysis

In 2025, North America commands the global protein snacks market with a 37.55% share, bolstered by consumers' deep-rooted affinity for snackable proteins and a well-established retail framework. Across U.S. supermarkets, health-food aisles, and convenience stores, protein bars like Pure Protein and meat snacks such as Jack Link’s Beef Jerky have cemented their presence, extending their appeal beyond just post-workout consumption. These offerings not only thrive on effective private-label alternatives, exemplified by Walmart’s Pure Protein line, but also benefit from a mature logistics system and adept shelf management, ensuring they're consistently available nationwide.

Asia-Pacific emerges as the frontrunner in the packaged protein snacks arena, boasting a projected CAGR of 9.42% through 2031. In India and China, urban middle-class consumers are gravitating towards high-protein snacks like Diretto Protein Bars, SuperU Chips, and Yörk Protein Cookies. Their choices are fueled by a desire for convenient, protein-rich options that resonate with their fast-paced lifestyles and health goals. The surge in e-commerce and the rise of modern retail formats, particularly in urban India, are further propelling this trend, with delivery platforms and wellness branding gaining significant traction.

While other regions witness moderate growth in the packaged protein snacks market, Europe sees its consumers leaning towards clean-label options. Snacks like Orgain Protein Bars and Nākd Protein Bites are favored for their health claims, taste, and trusted certifications. In South America and the Middle East & Africa, the penetration of protein snacks is gradual. While products like Well Yeah Protein Yogurts and Barebells Bars find their way into select modern retail outlets, challenges such as infrastructural gaps, cost sensitivity, and logistical hurdles hinder a more expansive reach.

Competitive Landscape

The protein snacks market is fragmented, and brands are increasingly turning to marketing strategies as a means of differentiation. Both established names and new entrants are aligning with consumer preferences, emphasizing clean-label positioning, transparency, and compelling storytelling. Brands like Chomps and ALOHA are highlighting their commitment to non-GMO, gluten-free, and sustainably sourced ingredients, fostering trust and emotional ties with health-conscious consumers. Through social media campaigns, influencer collaborations, and user-generated content, these brands are crafting relatable narratives that resonate with their audience. Moreover, direct-to-consumer models empower newer entrants to sidestep traditional retail hurdles, allowing them to tailor offerings and cultivate loyalty via subscription services and focused email marketing.

Technological advancements are becoming pivotal, especially in ingredient sourcing, texture enhancement, and ensuring shelf stability. Companies are turning to techniques like high-moisture extrusion and precision fermentation to elevate the sensory experience of plant-based protein snacks. For example, extrusion technology is enabling brands to craft puffed, chip-like textures from pea or chickpea protein, catering to mainstream snack enthusiasts. Innovators like Clextral are employing unique processing methods to achieve scalable, meat-like textures from vegetable proteins, presenting credible alternatives to conventional jerky or bars.

To solidify their market stance, companies are pursuing strategies like vertical integration, acquisitions, and expanding manufacturing capabilities. Established food giants are snapping up niche protein snack brands for swift market entry and operational benefits, as seen with Ferrero’s takeover of Power Crunch and Flowers Foods’ acquisition of Simple Mills. On the other hand, emerging players like Chomps are forging partnerships, such as with Western Smokehouse Partners, to establish dedicated production facilities, enhancing their supply chain oversight and scalability.

Protein Snacks Industry Leaders

Mondelez International

PepsiCo Inc.

General Mills Inc.

Nestle S.A

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ferrero Group completed acquisition of protein-snack maker Power Crunch, broadening Ferrero North America’s better-for-you offerings.

- January 2025: Flowers Foods announced a USD 795 million takeover of Simple Mills to accelerate its foothold in healthy snacks.

- December 2024: TruFood Manufacturing and Bar Bakers merged to form Tandem Foods, creating an eight-plant contract manufacturer focused on protein bars and cookies.

- November 2024: Actor Ranveer Singh launched Super You, debuting vegan protein wafer bars delivering 10 g protein per serving via bio-fermented yeast protein technology.

Global Protein Snacks Market Report Scope

| Protein Bars | |

| Meat Snacks | Jerky |

| Sticks | |

| Sausages | |

| Other Product Types | |

| Chips & Crisps | |

| Cookies and Bites | |

| Ready-to-Drink Protein Shakes | |

| Puddings and Yogurts | |

| Others |

| Animal-Derived | Whey and Casein |

| Meat-Based | |

| Egg Protein | |

| Others | |

| Plant-Based | Soy |

| Pea | |

| Others | |

| Others (Feremented, Cultivated and Insect Proteins) |

| Organic |

| Conventional |

| Supermarkets and Hypermarkets |

| Convenience/Gorcery Stores |

| Specialty Sports and Health Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Protein Bars | |

| Meat Snacks | Jerky | |

| Sticks | ||

| Sausages | ||

| Other Product Types | ||

| Chips & Crisps | ||

| Cookies and Bites | ||

| Ready-to-Drink Protein Shakes | ||

| Puddings and Yogurts | ||

| Others | ||

| By Protein Source | Animal-Derived | Whey and Casein |

| Meat-Based | ||

| Egg Protein | ||

| Others | ||

| Plant-Based | Soy | |

| Pea | ||

| Others | ||

| Others (Feremented, Cultivated and Insect Proteins) | ||

| By Claim | Organic | |

| Conventional | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience/Gorcery Stores | ||

| Specialty Sports and Health Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the protein snacks market?

The global protein snacks market size is USD 34.44 billion in 2026.

How fast is the protein snacks market expected to grow?

It is forecast to post a 7.58% CAGR, reaching USD 49.62 billion by 2031.

Which product segment leads the protein snacks market?

Meat snacks dominate with 55.02% revenue share, though chips and crisps register the quickest growth at 9.02% CAGR.

Which region shows the highest growth potential?

Asia-Pacific is projected to expand at a 9.42% CAGR between 2026-2031 due to rising incomes and health awareness.

Page last updated on: