Diabetic Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

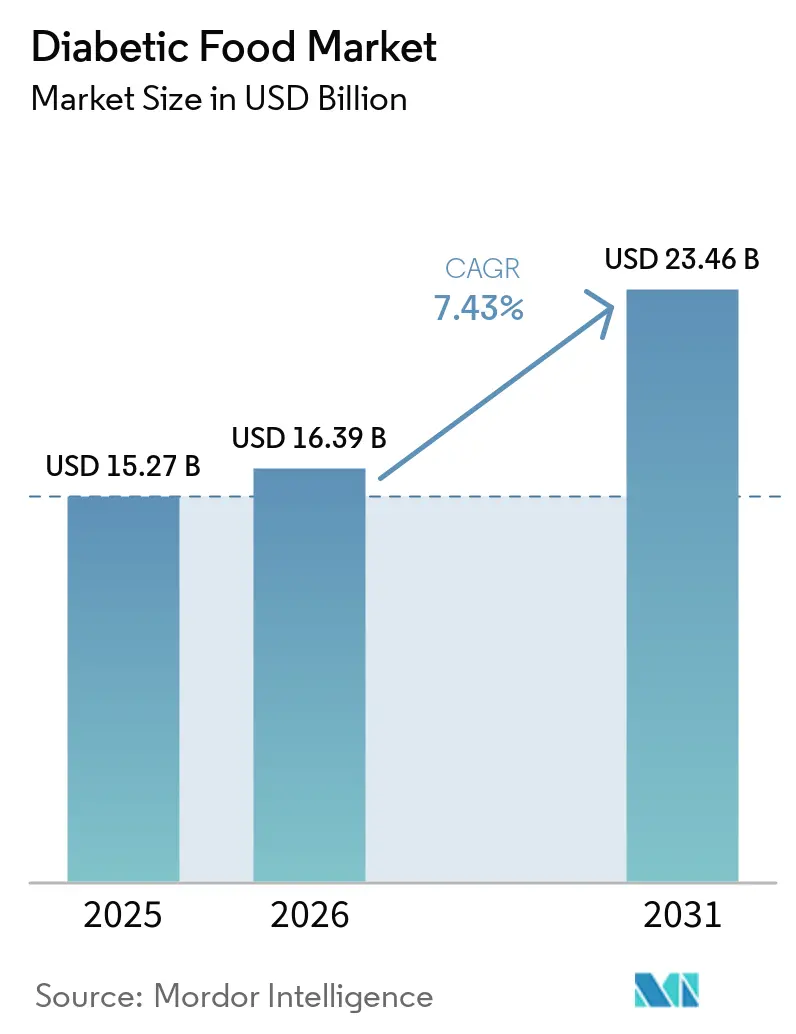

| Market Size (2026) | USD 16.39 Billion |

| Market Size (2031) | USD 23.46 Billion |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diabetic Food Market Analysis by Mordor Intelligence

The Diabetic food market size was valued at USD 15.27 billion in 2025 and estimated to grow from USD 16.39 billion in 2026 to reach USD 23.46 billion by 2031, at a CAGR of 7.43% during the forecast period (2026-2031). The pace of expansion reflects a large and still rising clinical need, as 589 million adults worldwide were living with diabetes in 2024, equal to 1 in 9 adults, and that number is projected to reach 853 million by 2050. Diabetes-related health expenditure exceeded USD 1 trillion in 2024, accounting for 12% of total global health expenditure, underscoring the importance of dietary management for health systems, clinicians, and households. The addressable base is also wider than diagnosed case counts suggest because 42.8% of adults with diabetes remained undiagnosed in 2024, and better screening will continue to convert hidden need into product demand across many countries. The diabetic food market is further supported by strong spending power in North America and faster diagnosis-led consumption growth across Asia-Pacific, where large diabetes populations and expanding retail access are reinforcing demand. Competition remains moderately fragmented, so companies that combine credible nutrition claims, lower-sugar reformulation, and convenient purchase routes are better placed to strengthen their position in the diabetic food market.

Key Report Takeaways

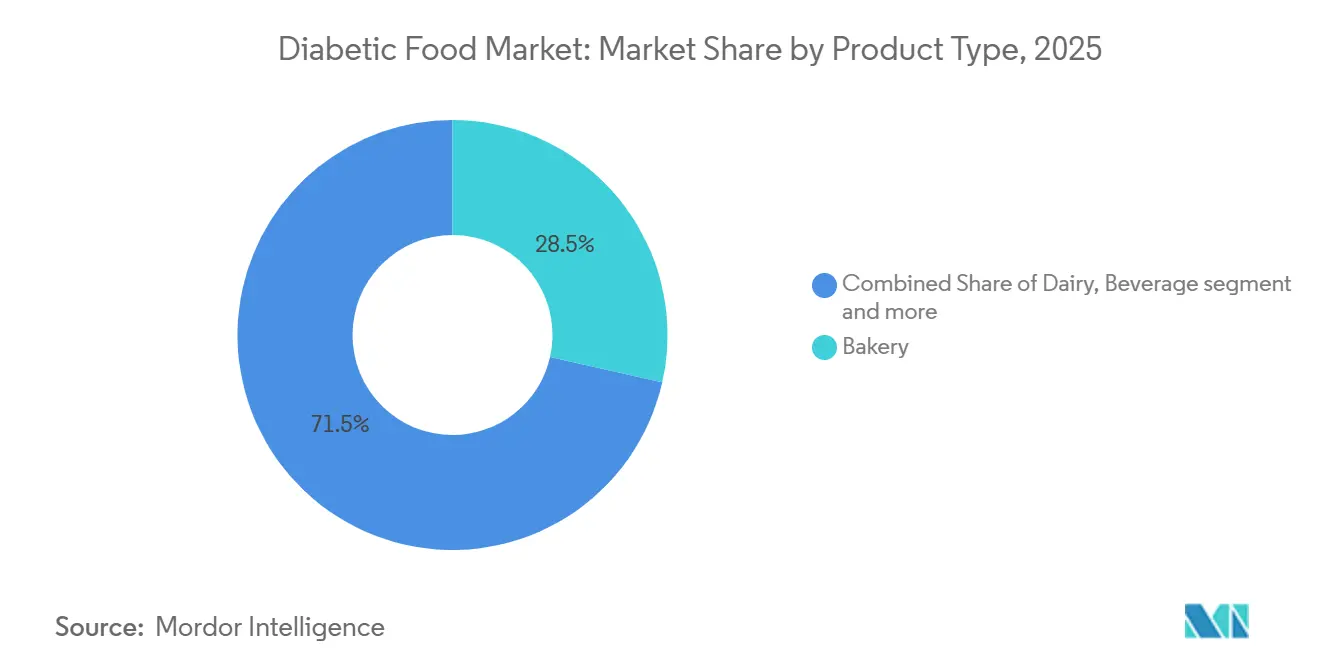

- By product type, bakery held 28.55% of the diabetic food market share in 2025, while snacks is forecast to expand at 8.37% CAGR through 2031.

- By end user, adults accounted for 83.28% of the diabetic food market size in 2025, while children are projected to grow at 8.29% CAGR through 2031.

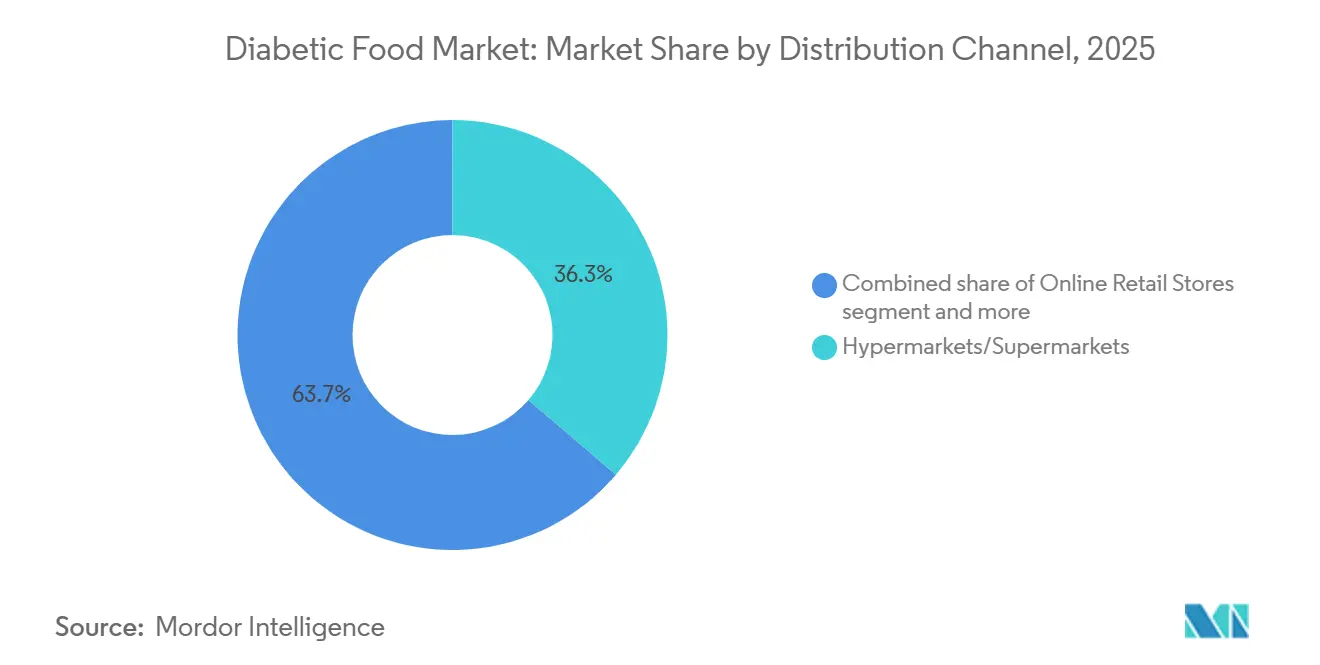

- By distribution channel, hypermarkets and supermarkets held 36.26% share in 2025, while online retail stores recorded the highest projected CAGR at 9.15% through 2031.

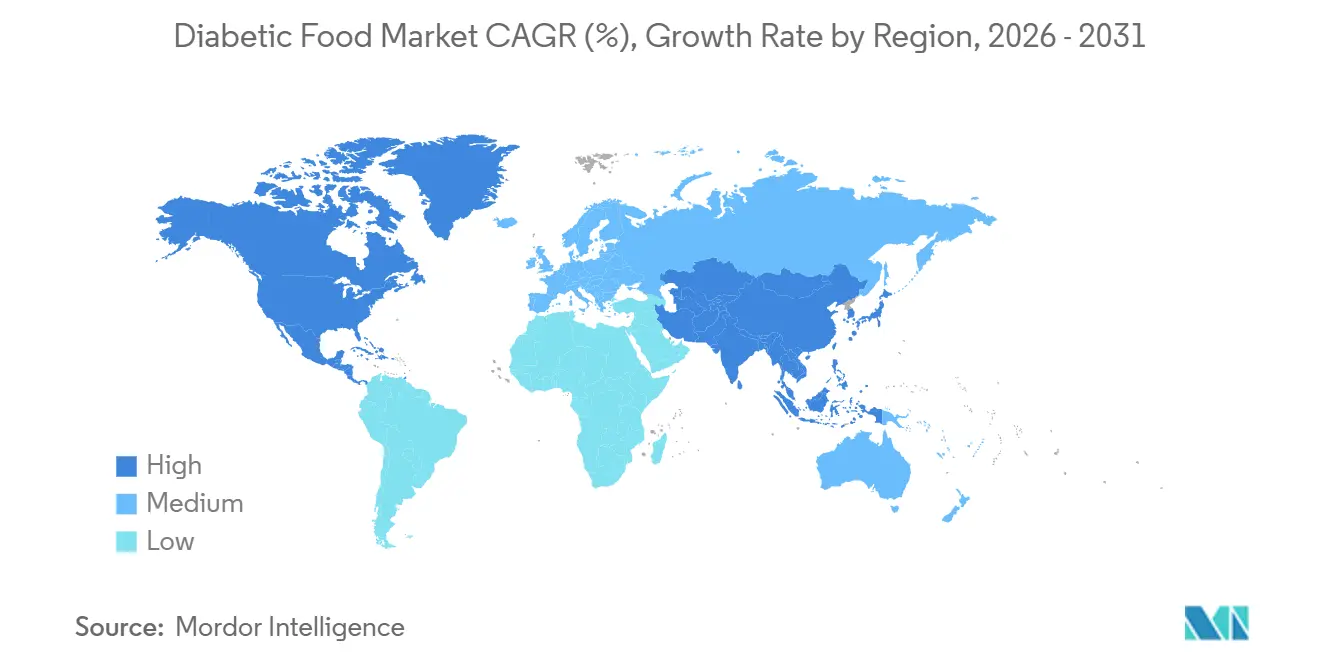

- By geography, North America commanded a 41.42% share in 2025, while Asia-Pacific is expected to grow at an 8.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diabetic Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Prevalence of Type 1 and Type 2 Diabetes | +2.1% | Global, high impact in APAC, MENA, and North America | Long term (≥ 4 years) |

| Increasing Health Consciousness and Preventive Dietary Management | +1.6% | North America, Europe, and urban APAC | Medium term (2-4 years) |

| Innovation in Sugar Substitutes, Low-GI Ingredients, and Functional Foods | +1.3% | Global, strongest in North America and the EU | Medium term (2-4 years) |

| Growing Endorsements From Healthcare Professionals and Dietitians | +0.8% | North America, Europe, and high-income APAC markets | Short term (≤ 2 years) |

| Product Innovation in Diabetic-Friendly Foods | +0.7% | Global, highest commercialization in North America and China | Medium term (2-4 years) |

| Growing Availability Across Retail Channels | +0.6% | Global, with stronger e-commerce momentum in APAC and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of type 1 and type 2 diabetes: the core demand signal

The foundational demand driver for diabetic food products is the relentless growth of the global diabetes population, which the IDF Diabetes Atlas 11th Edition estimated at 589 million adults in 2024, growing at a rate that outpaces global population expansion, with obesity trends and demographic shifts contributing 49.6% and 50.4% of the projected increase to 853 million by 2050, respectively. A less-discussed structural dimension is that 42.8% of cases remain undiagnosed in 2024, with the Western Pacific region recording a 50.0% undiagnosed proportion as per IDF Atlas, 2025, meaning that as diagnosis rates improve across Asia and Africa, the commercially addressable base of dietary management consumers will expand significantly ahead of what raw case counts imply[1]Source: International Diabetes Federation, “IDF Diabetes Atlas 11th Edition 2025,” International Diabetes Federation, idf.org. Type 1 diabetes now affects 9.5 million people globally in 2025, a 13% increase from 2021, with 513,000 new cases diagnosed annually, according to the IDF T1D Index, 2025. This growth in type 1 prevalence, particularly among children and young adults, creates demand for a distinct product architecture that neither prioritizes glycemic avoidance nor targets the age-related metabolic decline typical of type 2.

Health consciousness and preventive dietary management: a market multiplier

Preventive consumption by pre-diabetic individuals and health-aware non-diabetics is expanding the total addressable market for diabetic food well beyond the diagnosed base. The IDF Diabetes Atlas 11th Edition estimated that 634.8 million adults globally have impaired glucose tolerance (IGT) and 487.7 million have impaired fasting glucose (IFG) in 2024, populations at high risk of type 2 diabetes that are increasingly adopting low-GI, low-sugar diets as precautionary measures. The International Food Information Council's 2024 Food & Health Survey found that two-thirds of consumers actively want to limit sugar consumption, a trend that materially broadens the commercially addressable audience beyond clinically diagnosed populations[2]Source: Steve Koppes, “Finding the Sweet Spot,” Institute of Food Technologists, ift.org. China's 2025 consumer analysis found that motivation is shifting from "disease control" to "proactive health management," with healthy individuals treating diabetic food products as preventive consumption and demanding not just blood sugar management but also good taste, convenience, and emotional value. This consumer repositioning of diabetic food products as a mainstream health category, rather than a medical niche, has significant implications for shelf placement, marketing, and distribution strategy.

Innovation in sugar substitutes and low-GI ingredients: rewriting formulation economics

Sweetener science advanced further in 2024-2026 than in any comparable prior period, giving food manufacturers a materially wider toolkit for producing diabetic food products with superior taste profiles. Avansya's EverSweet stevia sweetener (fermentation-derived Reb M and Reb D) received EU and UK authorization in May 2025, bringing an ingredient with an 81% lower carbon footprint and 96% lower land use than conventional sugar into mainstream European supply chains. Allulose, a rare sugar with near-zero calories and a negligible glycemic index that mimics sucrose in browning and mouthfeel, saw a 40% increase in global product launches between 2022 and 2024, with North America recording a 135% surge in launches in 2025 alone. EFSA's August 2025 opinion on beta-glucans from oats and barley confirmed that a minimum dose of 4g/30g available carbohydrates remains the substantiated threshold for a blood glucose reduction claim under EU Regulation (EC) No 1924/2006, a compliance factor that shapes reformulation investment decisions across European bakery and cereal manufacturers. The FDA's March 2024 qualified health claim for yogurt, the first such claim for a whole food rather than an ingredient, further broadens the legitimate food-as-diabetes-management claim landscape.

Growing endorsements from healthcare professionals and dietitians

Clinical guidelines from international diabetes bodies are increasingly formalizing dietary management as a first-line intervention, directing patients toward specific food categories and formulation attributes. The ISPAD 2024 Clinical Practice Consensus Guidelines for type 2 diabetes in children and adolescents explicitly integrate healthy eating interventions, including reduced intake of high-calorie beverages, culturally appropriate meal composition, and increased fiber intake, as a cornerstone of clinical management alongside pharmacotherapy. India's RSSDI-ICMR 2025 Consensus Guidelines for type 1 diabetes advocate medical nutrition therapy aligned with ISPAD and ADA principles, emphasizing carbohydrate counting, glycemic index awareness, and telemedicine-supported dietary education, tools that inherently channel patient behavior toward labeled, categorized diabetic food products. The less-visible dimension of this driver is that dietitian endorsement in pharmacy channels, where clinical nutrition products like Abbott's Ensure Diabetes Care are stocked alongside pharmaceutical therapies, creates a prescriptive pull that bypasses conventional marketing and acts as a high-trust distribution mechanism.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of specialized diabetic food products | -0.9% | Global; most pronounced in APAC developing markets and sub-Saharan Africa | Long term (≥ 4 years) |

| Consumer skepticism toward artificial sweeteners and additives | -0.5% | North America and Europe primarily; growing in urban APAC | Medium term (2–4 years) |

| Taste and sensory preference challenges | -0.4% | Global, critical in mass-market channel expansion | Short to medium term |

| Regulatory complexities for health claims | -0.3% | EU and North America; moderate in APAC | Medium to long term |

| Source: Mordor Intelligence | |||

Premium pricing as a persistent adoption barrier

Premium pricing is the most significant structural constraint to the mass-market adoption of diabetic food products. Specialized ingredients, allulose, almond flour, stevia, high-fiber grains, and erythritol add 20-40% to formulation costs compared with conventional food manufacturing. In Japan, the clinical nutrition segment for diabetes care noted that products such as ENORAS cost approximately JPY 294 per 187.5ml pouch (USD 1.94), with per-serving costs above JPY 350 (USD 2.31) resulting in 40-50% lower conversion among elderly consumers aged 65+ who represent the largest diabetes demographic. In China, local FSMP manufacturers captured significant market share by 2025, by targeting county-level markets through 2,800 "nutrition consultant + pharmacy" networks rather than competing on premium positioning, demonstrating that pricing and distribution co-innovation is as critical to market expansion as formulation R&D. Across developing markets, the practical implication is that market leaders cannot simply export premium-positioned Western product architectures; they require tiered pricing models anchored in local ingredient economics.

Consumer Skepticism Toward Artificial Sweeteners and Additives

Consumer skepticism toward synthetic sweeteners presents a nuanced restraint that operates differently across regions and demographic cohorts. A 2024 study in the European Heart Journal linked xylitol to potential adverse cardiovascular effects in at-risk individuals, building on a 2023 Nature Medicine study raising similar concerns about erythritol, placing two widely used sugar alcohols common in diabetic food products under media scrutiny. Simultaneously, 60% of global consumers express general concern about artificial sweeteners, according to the IFT (2025). Cleaner natural alternatives face their own barriers: allulose remains unapproved in Canada and the EU as of April 2025, creating geographic fragmentation that complicates global product launch strategies. China's 2025 consumer analysis found growing sophistication around the understanding that "sugar-free ≠ healthy," pushing manufacturers beyond label claims toward substantive nutritional innovation and clinical verification. The practical risk for manufacturers is that attempts to address concerns about artificial sweeteners by switching to unregulated natural alternatives introduce new compliance exposure in key export markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery’s Scale Meets Snacks’ Growth Momentum

Bakery accounted for 28.55% of the diabetic food market in 2025, maintaining its lead over all other product categories. The diabetic food market treats bakery as a staple-led segment because consumers usually modify bread, cereal, and grain-based products rather than remove them from their daily routines. Kellanova said it removed more than 57,000 tonnes of sugar from its European cereals and snacks since 2011, increased fiber by 122% across children’s cereal ranges, and launched Kellogg’s Oaties and High Protein Bites in 2025. That pattern shows how the diabetic food market is pushing reformulated mainstream foods toward a more diabetes-conscious position without forcing consumers to shift entirely to niche products.

Snacks are projected to grow at 8.37% CAGR through 2031, which gives it the strongest momentum among product groups. The diabetic food industry is seeing faster demand for portable, portion-aware foods that fit work, travel, and between-meal eating habits without creating a high sugar load. Dairy also benefits from the FDA’s qualified health claim for yogurt and reduced type 2 diabetes risk, which adds support for products that combine convenience with clinically relevant nutrition messaging. EFSA’s 2025 position on beta-glucans further supports cereals and grain-based products that can meet the required dosage threshold for a compliant claim, while higher-protein nutrition formats are becoming more relevant in the diabetic food market for consumers seeking broader metabolic support.

By End User: Adult Dominance With a Faster Pediatric Buildout

Adults held 83.28% of the diabetic food market size in 2025, which reflects the fact that type 2 diabetes accounts for more than 95% of all diabetes cases worldwide and remains concentrated in adult populations. The diabetic food market also draws adult demand from people who are not yet diagnosed with diabetes but already have impaired fasting glucose or impaired glucose tolerance and are changing their diet to lower future risk. That makes the adult segment broader than the treated patient population, helping explain why everyday food formats remain important. Abbott’s 2025 reformulation of Ensure Diabetes Care in India, with more myo-inositol, a low-GI carbohydrate blend, dual-blend oat fiber, prebiotic FOS, and stronger micronutrient content, shows how condition-specific adult nutrition is moving toward more clinically detailed product design.

Children are the fastest-growing end-user segment, with an 8.29% CAGR expected through 2031. The diabetic food market is seeing that shift because type 1 diabetes affected 9.5 million people globally in 2025, including 1.8 million individuals under age 20[3]Source: Graham D. Ogle et al., “Global Type 1 Diabetes Prevalence, Incidence, and Mortality Estimates 2025,” Diabetes Research and Clinical Practice via DOI, doi.org. ISPAD’s 2024 guidance for type 2 diabetes in children and adolescents also gave dietary management a much more explicit frontline role, which supports demand for products that are appropriate in taste, format, and school-day use. The diabetic food industry still has a product gap here because many current offerings were designed for adults first, while children need smaller portions, better flavor acceptance, and lower reliance on synthetic sweeteners. Kellanova’s child-oriented high-fiber cereal launches in Europe suggest early recognition of this need, but the pediatric side of the diabetic food market still looks underdeveloped relative to the clinical requirement.

By Distribution Channel: Physical Scale and Digital Acceleration

Hypermarkets and supermarkets accounted for 36.26% of the diabetic food market in 2025, maintaining their position as the largest distribution channel. The diabetic food market still depends on large physical retail because visibility, trial, and repeat household purchase are easier to build where consumers shop for their routine grocery basket. Pharmacies and drug stores remain especially important for clinically positioned products because shoppers often meet them in a health-led setting rather than a pure convenience setting. That is particularly relevant in countries such as Germany, where adult diabetes prevalence reached 10.3% in 2024 and rose sharply among older age groups that are more likely to use pharmacy-linked care pathways.

Online retail stores are the fastest-growing channel, with a projected 9.15% CAGR through 2031. The diabetic food market benefits from digital platforms because products often need more room for ingredient explanation, nutrition comparisons, subscription refill options, and targeted communication than a store shelf can provide. This channel also helps smaller, specialized brands reach consumers who may not find condition-specific products at nearby stores. PepsiCo’s May 2026 launch of Propel Clear Protein across Walmart.com, Amazon, and Gatorade.com shows that direct digital access is now a core go-to-market channel for products tied to metabolic health and lower-sugar positioning. As a result, the diabetic food market is becoming more omnichannel, with physical retail driving scale and online retail driving speed, education, and assortment depth.

Geography Analysis

North America held 41.42% of the diabetic food market share in 2025, which made it the largest regional contributor. The United States alone had 38.5 million adults with diabetes in 2024, and its diabetes-related health expenditure reached USD 404.5 billion in the same year, according to the International Diabetes Federation (IDF). The broader North America and Caribbean region accounted for USD 438.6 billion in diabetes-related health spending, equal to 43.2% of the global total, which gives the region an unusually deep commercial base for specialized nutrition products, as per the IDF Diabetes Atlas 11th Edition 2025. Regulatory direction also matters here because the FDA updated the definition of the “healthy” nutrient content claim in late 2024 and added clearer limits around added sugar, which is already shaping reformulation across food categories. The diabetic food market in North America, therefore, benefits from high awareness, strong spending, rapid product commercialization, and a regulatory system that influences product standards across the value chain.

Asia-Pacific is projected to grow at a 8.86% CAGR through 2031, making it the fastest-expanding regional block in the diabetic food market. The Western Pacific region had 215.4 million adults with diabetes in 2024, while South-East Asia had 106.9 million, giving Asia-Pacific the broadest demand base tied to diabetes prevalence, as per the IDF Diabetes Atlas 11th Edition 2025. India had around 101 million adults with diabetes by 2025, which supports strong demand for condition-specific nutritional products and daily-use lower sugar foods, according to Abbott. The diabetic food market in this region is being lifted by urban diet change, higher diagnosis rates, and wider acceptance of low-sugar and functional food formats in large population centers. These conditions will keep both multinational and regional producers focused on affordable formats, local flavor fit, and broader digital and modern trade access across the diabetic food market.

Europe remained the second-largest regional market, anchored by Germany, the UK, France, Italy, and Spain. Germany’s adult diabetes prevalence reached 10.3% in 2024, rising to 20.9% among people aged 65 to 79 and 22.5% among those aged 80 and above, which supports strong pharmacy and clinical nutrition demand, according to the Robert Koch Institute. South and Central America recorded a 10.1% age-standardized diabetes prevalence in 2024, while the Middle East and North Africa posted the highest regional rate at 19.9%, which signals important long-term demand even where affordability remains a limit, according to the International Diabetes Federation (IDF). The diabetic food market therefore requires different regional playbooks, with mature geographies favoring clinically backed reformulation and emerging ones needing lower-cost access, staple-led innovation, and channel expansion.

Competitive Landscape

The diabetic food market remains moderately fragmented, and no company holds a decisive leadership position across all product categories or regions. Nestlé, Abbott Laboratories, Danone, PepsiCo, and Kellanova remain the most visible large platforms because they combine scale, product development capacity, and established nutrition brands. Even so, the diabetic food market still rewards brand differentiation more than pure scale because credibility, formulation quality, and channel fit matter at least as much as manufacturing size. Regulatory rules also keep competition in check, as health and blood glucose claims must align with stricter evidence standards in major markets. That leaves room for both multinational food companies and regional specialists to compete on trust, taste, and access inside the diabetic food market.

Abbott strengthened its position in 2025 by reformulating Ensure Diabetes Care in India with more myo-inositol, a low-GI carbohydrate system, dual-blend oat fiber, prebiotic FOS, and stronger micronutrient support, which shows a clear move toward more clinically differentiated diabetic nutrition. PepsiCo widened its metabolic health positioning in May 2026 through Propel Clear Protein, a zero-sugar powder with 20 g of whey protein, 3 g of fiber, and electrolytes, and it explicitly targeted GLP-1 users and consumers managing metabolic health. Kellanova is taking a different route by using broad reformulation and portfolio renovation, and in 2026 it tied that effort to a roadmap for high-fiber and high-protein foods with lower sugar and salt. These moves suggest that growth in the diabetic food market is coming from portfolio adaptation, nutrition science, and adjacent health positioning rather than from a single dominant product formula. They also show that leading companies are approaching the category through both condition-specific products and broader better-for-you offerings.

Upstream innovation is also shaping competition because ingredient suppliers influence how quickly brands can improve taste, reduce sugar, and defend compliant claims. Avansya’s 2025 approval for EverSweet in the EU and UK gave manufacturers another commercially usable sweetening option, which strengthens the development pipeline for lower sugar foods and beverages. The diabetic food market still leaves substantial room for regional players and focused specialists because local price points, pharmacy relationships, and consumer trust are not easy for every multinational to match. This keeps the diabetic food market competitive, varied, and more open than categories where the top few companies dominate most of the available share.

Diabetic Food Industry Leaders

Nestlé

Abbott Laboratories

Danone

PepsiCo

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Dr. Reddy's–Nestlé Health Science joint venture launched Celevida GLP+, a nutritional supplement providing 48g of protein per 100g and 27 essential nutrients, developed with endocrinologists for patients on GLP-1/GIP therapy for type 2 diabetes and obesity. The launch targets India's 1.6 million GLP-1 therapy users and addresses the 25-40% lean body mass loss associated with pharmacological weight reduction.

- May 2026: PepsiCo launched Propel Clear Protein, a zero-sugar, 90-calorie ready-to-mix powder providing 20g whey protein, 3g fiber, and electrolytes per serving, developed with registered dietitians and explicitly targeting GLP-1 users and consumers managing metabolic health. Available across Walmart.com, Amazon, and Gatorade.com.

- February 2026: Reliance Consumer Products Limited acquired 100% equity stake in Southern Health Foods Private Limited (Manna brand) for INR 156.42 crore (approximately USD 18.7 million), adding India's leading millet, oat, and multi-grain foods brand to its portfolio, categories with direct functional overlap with diabetic dietary management.

- November 2025: Abbott launched a reformulated Ensure Diabetes Care in India, incorporating a "triple care system" with 4x higher myo-inositol than the prior formulation, a low-GI carbohydrate blend, dual-blend oat fiber, prebiotic FOS, and increased chromium, vitamin D, calcium, and zinc, with no added sucrose.

Global Diabetic Food Market Report Scope

Diabetic food refers to food products specially formulated to help manage blood glucose levels and meet the nutritional needs of individuals with diabetes. The diabetic food market is segmented by product type, end user, distribution channel, and geography. By product type, the market includes bakery products, dairy products, beverages, snacks, confectionery, and other products. Based on end user, the market is segmented into adults and children. By distribution channel, the market covers hypermarkets/supermarkets, pharmacies and drug stores, specialty stores, online retail stores, and other distribution channels. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Bakery |

| Dairy |

| Beverages |

| Snacks |

| Confectionery |

| Others |

| Adult |

| Children |

| Hypermarkets/Supermarkets |

| Pharmacies and Drug Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Product Types | Bakery | |

| Dairy | ||

| Beverages | ||

| Snacks | ||

| Confectionery | ||

| Others | ||

| By End User | Adult | |

| Children | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Pharmacies and Drug Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in diabetic food demand worldwide?

Growth is being driven by rising diabetes prevalence, wider preventive nutrition use, stronger sugar-reduction innovation, and expanding clinical support for diet-based management. The category is projected to grow from USD 16.39 billion in 2026 to USD 23.46 billion by 2031 at a 7.43% CAGR.

Which product category leads diabetic food sales today?

Bakery is the leading category, with a 28.55% share in 2025. Its lead comes from the fact that consumers usually adapt staple foods such as bread and cereals rather than remove them from daily eating patterns.

Which end-user group is growing the fastest?

Children is the fastest-growing end-user group, with an expected 8.29% CAGR through 2031. This is linked to rising type 1 diabetes prevalence and stronger pediatric guidance around diet management.

Why is North America still the largest revenue contributor?

North America led with 41.42% share in 2025 because of high diabetes prevalence, very strong health expenditure, faster product commercialization, and a regulatory environment that actively shapes lower sugar reformulation.

Page last updated on: