Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 154.71 Billion |

| Market Size (2031) | USD 202.52 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

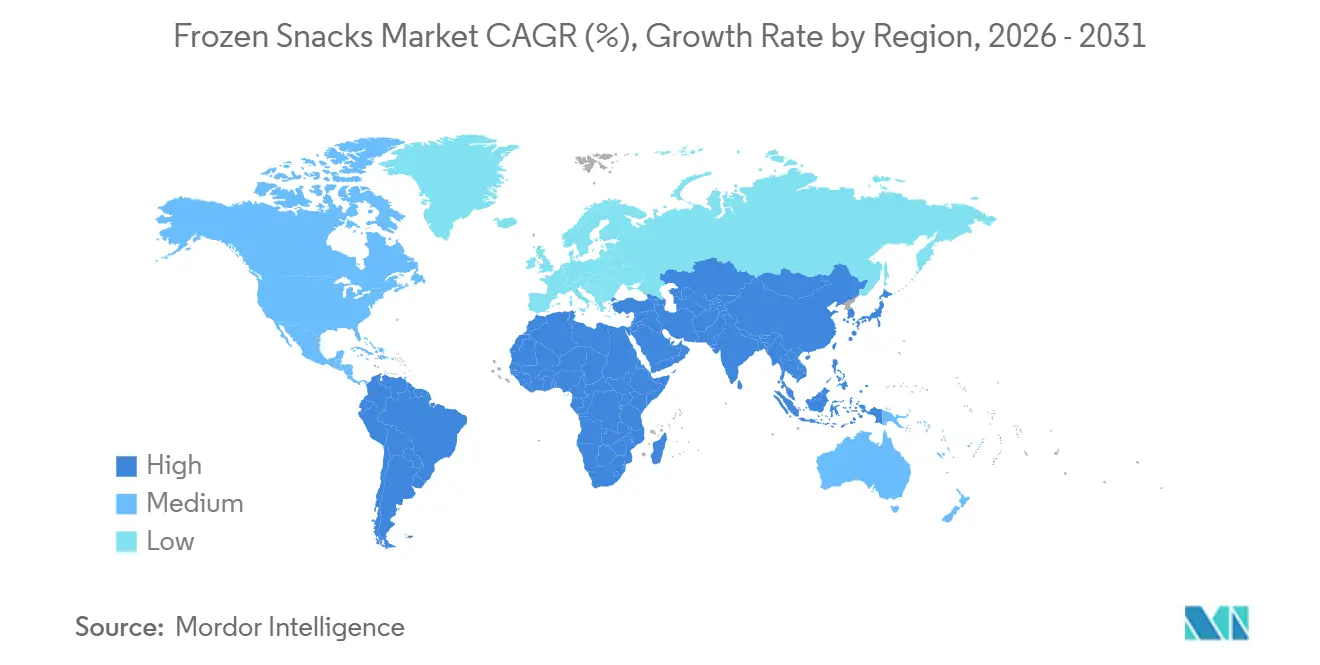

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Frozen Snacks Market Analysis by Mordor Intelligence

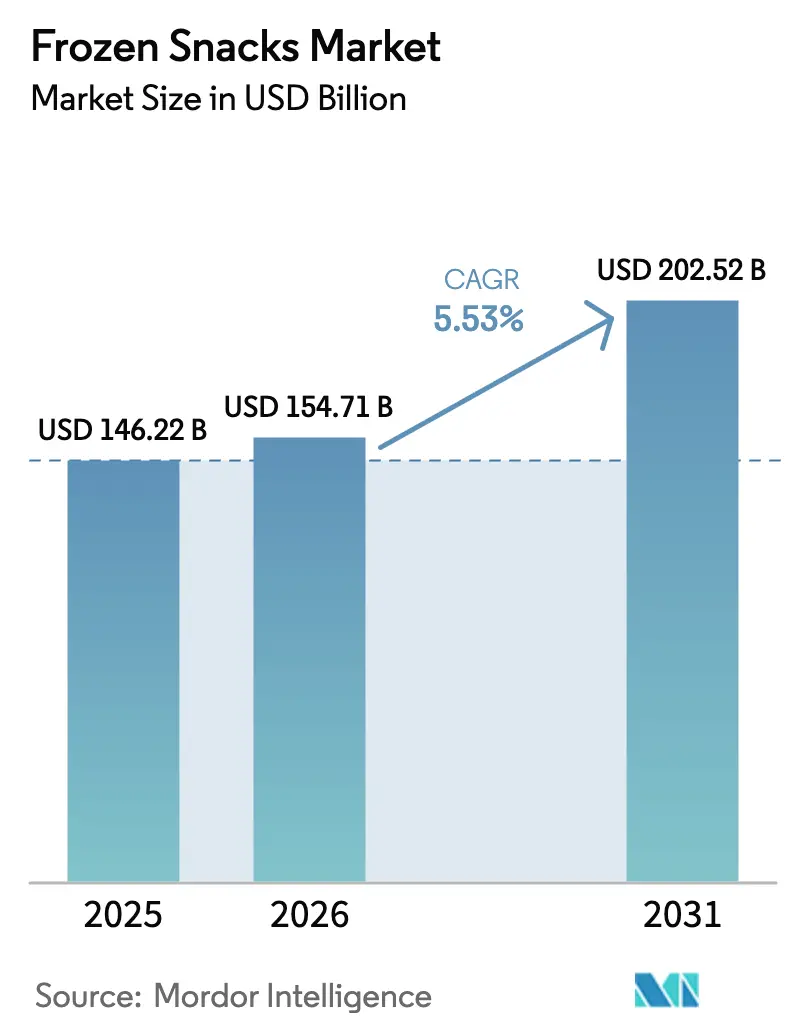

The frozen snacks market size was valued at USD 146.22 billion in 2025 and is estimated to grow from USD 154.71 billion in 2026 and is forecast to reach USD 202.52 billion by 2031, registering a compound annual growth rate (CAGR) of 5.53% during 2026-2031. The global frozen snacks market is growing due to evolving lifestyles and eating habits that prioritize quick, ready-to-cook food options with minimal preparation time. Factors such as rapid urbanization, an increasing number of working professionals, and smaller household sizes have driven the demand for convenient meal and snack solutions. Additionally, the expansion of modern retail channels, e-commerce grocery platforms, and advancements in cold-chain logistics have improved the accessibility of frozen products globally. The growth of quick-service restaurants and café chains has further popularized snack formats like fries, nuggets, and finger foods, boosting at-home consumption. In 2024, there were 199,931 quick-service restaurant franchise establishments in the United States[1]Source: International Franchise Association, "Franchising Economic Outlook 2025," franchise.org. Manufacturers are also driving consumer interest through product innovations, including healthier recipes, plant-based options, global street-food-inspired flavors, and air-fryer-compatible formats, aligning with wellness trends while maintaining taste. Rising disposable incomes in emerging economies and growing demand for consistent quality and extended shelf life further contribute to the market's sustained growth.

Key Report Takeaways

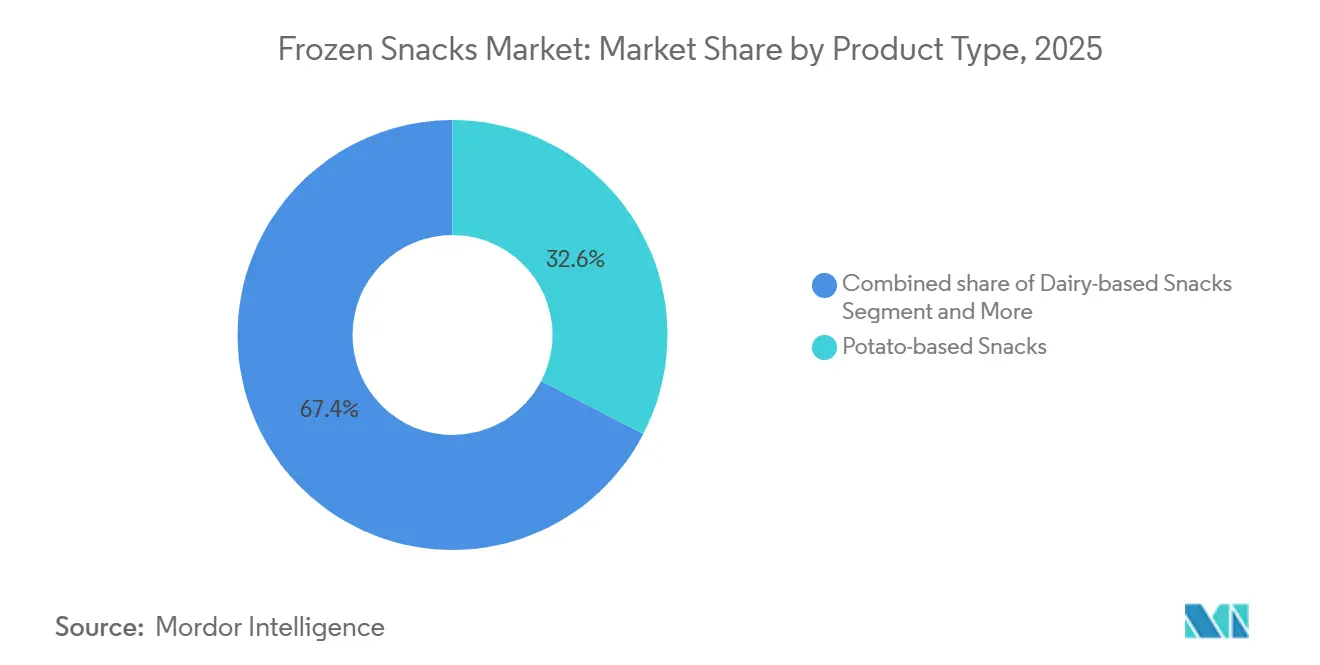

- Potato-based items led with a 32.62% Frozen snacks market share in 2025, whereas plant-based lines are projected to expand at a 6.13% CAGR through 2031.

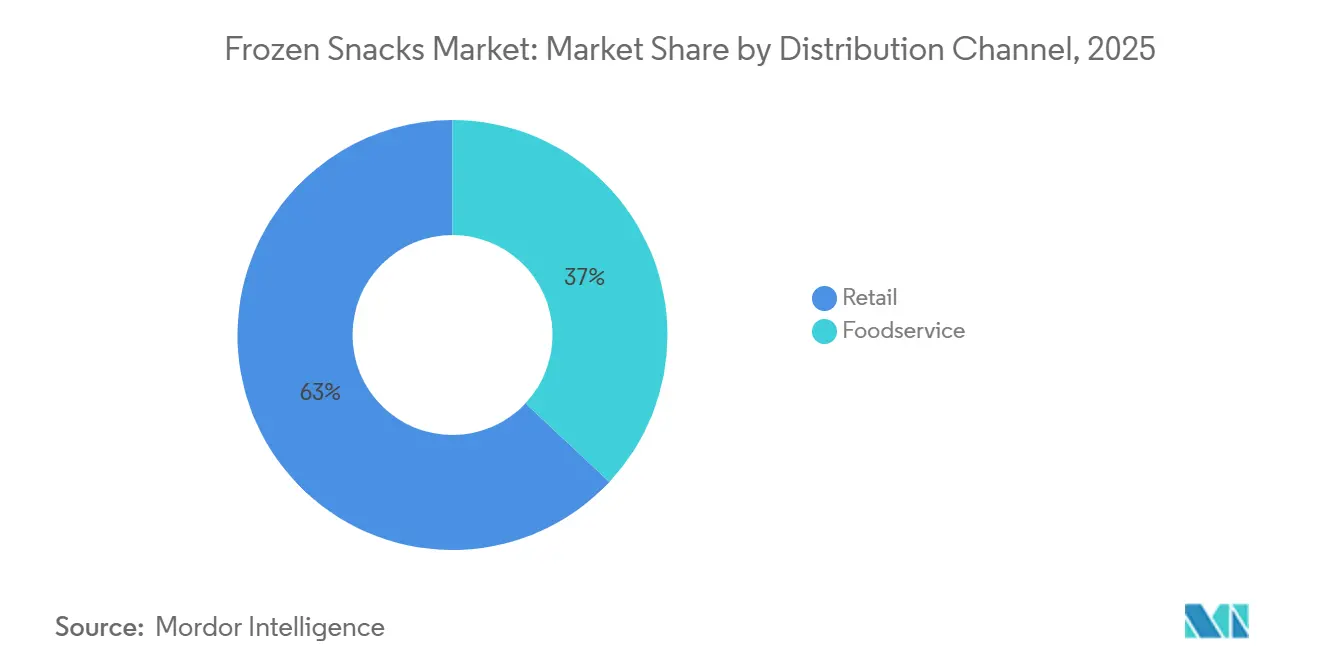

- Retail retained 63.03% of distribution revenue in 2025; however, foodservice is forecast to post the fastest rise with a 6.59% CAGR for 2026-2031.

- Europe captured 32.49% of 2025 global sales, while Asia-Pacific is on track for the highest regional CAGR at 6.37% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Frozen Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing urban preference for convenient, ready-to-eat meal options | +1.2% | Global, with highest intensity in Asia-Pacific urban centers and North America | Medium term (2-4 years) |

| Expansion of cold-chain infrastructure and online grocery platforms | +1.4% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Rapid growth of QSR and organized foodservice outlets | +0.9% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of air fryers in households | +0.7% | North America, Europe, and affluent Asia-Pacific markets | Short term (≤ 2 years) |

| Increasing popularity of international street-food styles | +0.5% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| Introduction of clean-label and plant-based product innovations | +1.1% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing urban preference for convenient, ready-to-eat meal options

The increasing urban preference for convenient, ready-to-eat meal options is a key driver of the global frozen snacks market's growth. As urbanization accelerates, daily routines become more fast-paced and structured, leaving limited time for traditional cooking. Urban consumers, particularly working professionals and students, are increasingly opting for foods that are quick to prepare without compromising on taste or variety. Frozen snacks meet this demand by offering minimal preparation time and consistent quality. Additionally, smaller living spaces and the prevalence of nuclear households encourage the purchase of portion-controlled, easy-to-store food products. The availability of appliances such as microwaves and air fryers further simplifies the preparation process. Moreover, exposure to diverse cuisines in metropolitan areas boosts the demand for frozen versions of popular street foods and international snack options. According to the World Bank Group, the global urban population represented approximately 58% of the total population in 2024, underscoring the expanding consumer base for convenient food solutions and driving the global demand for frozen snacks[2]Source: The World Bank Group, "Urban population (% of total population)," data.worldbank.org.

Expansion of cold-chain infrastructure and online grocery platforms

The expansion of cold-chain infrastructure and online grocery platforms is a significant factor driving growth in the global frozen snacks market. Frozen products rely on consistent temperature control throughout the supply chain, from manufacturing to final delivery. Advances in refrigerated transportation, warehousing, and last-mile delivery now enable companies to distribute products across broader geographic regions without compromising quality. The growth of online grocery and quick-commerce platforms has further fueled demand by allowing consumers to conveniently order frozen snacks for home delivery, often within hours, overcoming previous challenges related to spoilage risks. Retailers and logistics providers are increasingly investing in temperature-controlled storage and insulated packaging, making frozen products as accessible as fresh foods in both urban and semi-urban areas. For example, according to the India Brand Equity Foundation, India had over 8,689 cold storage facilities with a combined capacity of approximately 39.6 million metric tonnes as of August 2024. Uttar Pradesh accounted for about 38% of this capacity, followed by West Bengal at 15% and Gujarat at 10%[3]Source: India Brand Equity Foundation, "From Farms to Fridges: How Cold Chain Infrastructure is Transforming India’s Agriculture," ibef.org. Such infrastructure development enhances product availability, extends shelf life during transit, and boosts consumer confidence, thereby driving global frozen snack consumption.

Introduction of clean-label and plant-based product innovations

The introduction of clean-label and plant-based product innovations is driving growth in the global frozen snacks market, as consumers increasingly seek convenient foods that align with health and sustainability expectations. Consumers are paying closer attention to ingredient lists, favoring products made with recognizable ingredients, natural seasonings, and minimal additives. This trend has led manufacturers to reformulate recipes and emphasize transparency in packaging. Additionally, the rising popularity of vegetarian, vegan, and flexitarian diets has prompted brands to introduce plant-based frozen snacks, including vegetable-based bites, meat-free nuggets, and legume-based patties. These products aim to deliver familiar taste and texture while catering to dietary preferences. Such innovations enable consumers to enjoy indulgent snack options without compromising on nutrition or ethical values. Consequently, the combination of clean-label positioning and plant-based ingredients is broadening the appeal of frozen snacks to health-conscious and environmentally aware consumers, thereby strengthening global market demand.

Rapid growth of QSR and organized foodservice outlets

The rapid expansion of quick-service restaurants (QSRs) and organized foodservice outlets is a significant driver of the global frozen snacks market. These establishments depend on standardized, easy-to-store ingredients to ensure consistent taste, portion control, and quick preparation. Frozen appetizers such as fries, nuggets, patties, and bite-sized snacks are commonly used by QSRs, cafés, cinema counters, and cloud kitchens to maintain service speed during peak hours while minimizing kitchen preparation time and labor costs. The growth of franchise chains in urban and semi-urban areas has further increased bulk procurement of frozen snack items, promoting large-scale production and the development of extensive distribution networks. Additionally, consumers who encounter these menu items outside the home often seek similar flavors for at-home consumption, prompting retailers to stock comparable frozen options in supermarkets and online grocery platforms. This connection between foodservice adoption and retail demand enhances product visibility, familiarity, and repeat purchases, driving the global growth of the frozen snacks market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer concerns related to health and high sodium intake | -0.8% | Global, with highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Fluctuating energy and transportation expenses | -1.1% | Global, with acute pressure in Europe and energy-import-dependent Asia-Pacific markets | Short term (≤ 2 years) |

| Stricter freezer efficiency and carbon-emission regulations | -0.6% | Europe and North America, expanding to developed Asia-Pacific | Long term (≥ 4 years) |

| Tariff pressures on specialty ingredients in 2025 | -0.4% | North America and Europe, with indirect impact on global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer concerns related to health and high sodium intake

Health concerns and high sodium intake are key restraints on the global frozen snacks market, as consumers increasingly prioritize nutritional content and long-term wellness. Many frozen snack products depend on salt and preservatives to ensure flavor stability and extend shelf life, resulting in higher sodium levels compared to freshly prepared foods. Rising awareness of diet-related health issues, such as hypertension and cardiovascular diseases, has prompted consumers to reduce their intake of processed foods and scrutinize nutrition labels before purchasing. Health-conscious individuals, including parents, are opting to consume frozen snacks less frequently or are shifting to fresh, minimally processed alternatives. The perception of frozen snacks as indulgent rather than nutritious discourages repeat purchases, compelling manufacturers to reformulate products and introduce healthier options. However, until such changes are widely adopted, health and sodium concerns will continue to limit market growth.

Fluctuating energy and transportation expenses

Fluctuating energy and transportation costs pose a challenge to the global frozen snacks market due to the need for continuous temperature control throughout storage, warehousing, and distribution. The reliance on refrigeration systems, cold storage facilities, and insulated transport vehicles results in significant electricity and fuel consumption. Increases in power tariffs or fuel prices drive up operational costs across the supply chain, from production to last-mile delivery, thereby reducing profit margins or compelling companies to raise retail prices. Elevated prices can dampen consumer demand, particularly in price-sensitive markets, while smaller distributors may reduce their frozen product offerings to manage expenses. Additionally, unpredictable logistics costs make long-distance distribution less viable, limiting market expansion into remote areas. These cost-related challenges collectively impede the consistent growth of the global frozen snacks market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plant-Based Gains Outpace Legacy Formats

Potato-based snacks accounted for 32.62% of the market share in 2025, driven by their widespread taste appeal, affordability, and adaptability across various cultures. Products like fries, wedges, and hash browns are commonly used in households and quick-service restaurants due to their quick cooking time, minimal preparation requirements, and compatibility with diverse cuisines. The rising popularity of air fryers and home entertainment has further boosted at-home consumption. Additionally, large-scale potato cultivation ensures a steady supply of raw materials and competitive pricing. Their consistent texture and flavor after freezing make potato snacks a dependable comfort food option, encouraging repeat purchases worldwide.

Plant-based snacks are projected to grow at a CAGR of 6.13% through 2031. The demand for plant-based frozen snacks is increasing, driven by a growing preference for healthier and sustainable dietary options, as well as a rise in flexitarian and vegan consumers. Consumers are looking for convenient, plant-based alternatives to meat-based appetizers that offer comparable taste and texture. This has prompted brands to innovate with ingredients such as legumes, vegetables, and grain proteins. Factors such as clean-label preferences, environmental consciousness, and animal welfare concerns are further supporting the adoption of these products. Additionally, the expansion of retail distribution and diversification of foodservice menus are introducing these snacks to a broader audience. Combined, the focus on nutrition and ethical consumption is fueling the global demand for plant-based frozen snacks.

By Distribution Channel: Foodservice Momentum Challenges Retail Dominance

Retail channels accounted for 63.03% of the distribution share in 2025. The sales of frozen snacks through retail outlets have increased due to the rise in in-home consumption and the demand for quick meal solutions that accommodate busy lifestyles. Supermarkets and online grocery platforms provide a wide variety of products, promotional pricing, and bulk packaging, encouraging households to stock up for convenience and extended shelf life. The availability of freezers, microwaves, and air fryers simplifies preparation, while appealing packaging and healthier options, such as baked or plant-based products, attract families seeking both taste and practicality. Additionally, seasonal gatherings and impulse purchases during routine shopping trips further drive retail demand.

Sales through foodservice is projected to grow at a CAGR of 6.59% through 2031, driven by the operational benefits it offers to restaurants, cafés, and institutional kitchens. Pre-processed items help reduce preparation time, ensure consistent portion sizes, and lower labor requirements, enabling outlets to maintain efficient service during peak hours. Quick-service restaurants and delivery-focused kitchens utilize frozen appetizers to standardize menus across locations and manage inventory effectively, reducing the risk of spoilage. Furthermore, the growing demand for takeaway options and late-night snacking has encouraged outlets to provide easy-to-serve finger foods, supporting the consistent procurement of frozen snacks within the foodservice industry.

Geography Analysis

Europe accounted for 32.49% of the frozen snacks market in 2025, driven by well-established cold-chain systems and strong consumer familiarity with frozen foods, rooted in historical food-security practices. Major Western European economies, including Germany, the United Kingdom, and France, lead regional demand. Discount retailers significantly contribute to market growth by offering competitively priced private-label products. Environmental regulations targeting refrigerants are prompting retailers and logistics providers to upgrade refrigeration infrastructure, leading to increased capital investments while enhancing energy efficiency. In Southern Europe, countries such as Italy and Spain are emerging as growth markets due to urban lifestyles that reduce time spent on home cooking. Additionally, the Netherlands and Belgium serve as key distribution hubs, benefiting from advanced logistics networks and port access. Central and Northern European countries are witnessing steady adoption, supported by rising incomes and sustainability-focused policies promoting efficient cold-chain operations.

The Asia-Pacific region is projected to grow at a CAGR of 6.37% from 2026 to 2031, driven by factors such as rapid urbanization, a growing middle-class population, and substantial investments in cold-chain logistics, which are extending access to frozen foods beyond major urban areas. In China and India, shifting lifestyles, the prevalence of apartment living, and the rise of digital commerce are contributing to the normalization of routine frozen snack purchases. Japan's convenience-store culture supports consistent consumption, particularly among aging consumers who prefer small, easy-to-prepare portions. In Australia, there is a strong demand for imported frozen products, while Southeast Asian countries are emerging as manufacturing hubs as multinational companies increase production capacity to serve regional markets. South Korea is benefiting from the global popularity of its cuisine, which is driving international demand for traditional snack formats. Meanwhile, Singapore serves as a regional redistribution center, supported by its advanced storage and transportation infrastructure.

North America is a mature market, led by the United States, where quick-service restaurants and modern cooking appliances drive frozen snack consumption. Canada grows steadily with domestic production and retail partnerships, while Mexico expands rapidly due to retail modernization and rising purchasing power. Manufacturers face margin pressures from imported ingredient costs and health-focused regulations, favoring larger companies with strong R&D capabilities. South America holds a smaller market share, led by Brazil and Argentina with their meat-processing industries. Demand grows as retail infrastructure and refrigeration improve in countries like Chile and Colombia. The Middle East and Africa region grows gradually, driven by South Africa, Saudi Arabia, and the United Arab Emirates, where modern retail and expatriate populations boost demand. The United Arab Emirates also acts as a redistribution hub.

Regulatory Landscape

Frozen snacks suppliers operate under a tightening mix of microbiological safety, traceability, labeling, and cold-chain environmental compliance requirements. In the European Union, Commission Regulation (EU) 2024/2895 applies from July 1, 2026, strengthening the Listeria monocytogenes criterion for certain ready-to-eat foods across shelf life. This raises the burden on producers to validate shelf-life and process controls for products that can support pathogen growth.

In the United States, FDA traceability requirements under FSMA 204 continue to shape packaging and recordkeeping roadmaps across frozen and refrigerated supply chains, with the compliance deadline extended to July 20, 2028, and FDA issuing draft guidance for industry on additional traceability records in February 2026. For exporters, import-market rules add further complexity: China updated its national food safety standards catalog on January 8, 2026 (1,725 standards), reinforcing bilingual and lot-level labeling and documentation expectations for certain fresh and frozen meat imports. That can affect meat-based frozen snack lines and ingredient sourcing.

Value Chain Analysis

The value chain spans agricultural and animal-protein inputs (potatoes, vegetables, grains and legumes for plant-based lines, poultry and meat, and dairy), ingredient processing (breading, seasonings, oils, and binders), manufacturing (forming, par-frying or baking, freezing, and packaging), and then temperature-controlled storage and distribution to retail and foodservice. Scale and vertical coordination matter most in high-volume categories such as potato-based snacks (32.62% share in 2025), where stable raw-material procurement, high-throughput lines, and consistent quality specs support both supermarket freezer shelves and quick-service restaurant back-of-house demand.

Cold-chain logistics is the critical control point from factory gate through cross-docks, ports, and last-mile delivery, since time out of cold handling and warm-cold cycling can damage texture and safety margins. Trade and logistics coverage through 2024-2025 also flagged periodic constraints in reefer equipment and inland capacity, increasing cost and service variability for global movements. At the same time, the chain is becoming more data-driven as operators adopt IoT temperature monitoring and digital traceability practices to meet food safety and recordkeeping expectations, enabling faster audits and tighter inventory rotation across omnichannel distribution.

Competitive Landscape

The global frozen snacks market is highly fragmented, with large multinational food companies competing alongside regional manufacturers and retailer private-label brands within the same retail and foodservice channels. Entry barriers for basic production are relatively low due to the reliance on standardized processing equipment and widely available raw materials. However, competitive advantages are more pronounced with scale, particularly in areas such as cold-chain distribution, marketing budgets, and securing favorable shelf placement in modern retail stores. Some companies focus on high-volume efficiency, especially in potato-based categories supported by vertically integrated supply chains, while others differentiate through premium positioning, including organic certification, clean-label ingredients, or specialty dietary offerings.

Innovation is reshaping competition as brands develop products tailored for modern cooking appliances and evolving dietary preferences, such as hybrid protein formats that combine plant and animal ingredients. The adoption of technology is enhancing demand forecasting and inventory planning, enabling larger firms to maintain better product availability and freshness. At the same time, smaller emerging brands are leveraging direct-to-consumer sales and subscription models to reduce reliance on traditional retail channels and target younger households seeking curated product selections. Companies are also increasingly integrating upstream to secure key ingredients and mitigate exposure to commodity price volatility, thereby strengthening supply chain stability.

Regulatory requirements related to refrigeration efficiency and environmental standards are emerging as competitive barriers, favoring financially stronger companies capable of upgrading infrastructure and absorbing compliance costs. Additionally, long-term contracts with quick-service restaurants and institutional caterers are becoming more significant as they provide predictable revenue streams. However, these contracts require dedicated sales teams, customized packaging, and reliable logistics networks. Consequently, larger players with operational scale and robust distribution capabilities tend to dominate the foodservice segment, while smaller manufacturers focus on niche retail markets and differentiated product offerings.

Frozen Snacks Industry Leaders

-

McCain Foods Limited

-

Conagra Brands Inc.

-

Nestlé S.A.

-

Tyson Foods Inc.

-

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and channel whitespace is opening around formats engineered for modern preparation and away-from-home consumption occasions, particularly air-fryer-compatible snacks, delivery-hold crispness, and higher-protein or portion-controlled lines. Category-first positioning has been used to build demand in-market, as shown by McCain Foods India partnering with Philips to launch an air-fryer-specific frozen snacks range in April 2025, which supports premiumization and repeat purchase through improved at-home outcomes. Foodservice pull-through continues to shape retail assortment as quick-service and organized outlets standardize fries, nuggets, and finger foods that translate into household purchases.

Capacity, automation, and sustainability programs are also defining near-term investment themes in the frozen ecosystem. In March 2026, Conagra Brands initiated a USD 220 million expansion of its Fayetteville, Arkansas manufacturing plant to increase chicken production capacity for frozen meals, underscoring strategic focus on protein-based frozen platforms that share processing and cold-chain needs with snack adjacencies. On the cold-chain side, industry bodies such as AFFI and GCCA are advancing the Move to -15C initiative through baseline monitoring protocols (Version 1.1 released July 2025). This is creating a concrete pathway for energy and emissions reduction in storage and transport, with the potential to lower operating costs while maintaining product integrity.

Recent Industry Developments

- June 2026: Tyson Foods expanded its Tyson Chicken Cups line with three new flavors: Garlic and Herb, BBQ, and Harissa. The rollout strengthens the companys frozen snack proposition in convenient, protein-forward formats and broadens flavor-led differentiation for both retail and foodservice-adjacent occasions.

- November 2025: HyFun Foods launched a new retail range of ready-to-cook frozen snacks in India, expanding beyond its core potato-based portfolio. The broader assortment, including momos, cheese sticks, and Manchurian balls with gravy mix, supports basket-building in modern retail and increases competitive intensity in urban convenience-led frozen aisles.

- April 2024: McCain Foods India partnered with Philips to introduce Indias first frozen snacks range designed specifically for air fryers, using Sure Crisp technology for crisp results with low or no oil. The collaboration formalized appliance-led product engineering as a commercial strategy, raising the bar for texture performance and premium positioning in at-home frozen snack preparation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the frozen snacks market covers packaged snack and light-meal items sold in frozen form and stored through a cold chain until consumption, across retail and foodservice. Value is tracked in USD based on sales of frozen snack products at the market level.

Scope exclusions: Shelf-stable snacks, chilled only items, and fresh prepared snacks sold without frozen storage are not counted.

Segmentation Overview

-

By Product Type

- Potato-based Snacks

- Pizza Snacks

- Meat-based Snacks

- Baked Snacks

- Dairy-based Snacks

- Plant-based Snacks

- Others

-

By Distribution Channel

-

Retail

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail Stores

- Discounters & Club Stores

- Others

-

Foodservice

- Quick-Service Restaurants (QSR)

- Full-Service Restaurants

- Institutional Catering

-

Retail

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base around frozen foods, snacking frequency, and cold-chain distribution, and then it is narrowed to frozen snack formats. We rely on public datasets such as USDA and Economic Research Service releases, USITC/UN Comtrade trade statistics, Eurostat food industry tables, FAO food balance style indicators, and select national statistics office releases for retail food and manufacturing context.

On the company side, we review annual reports, investor presentations, and press releases to map category mix, capacity additions, and pricing moves that can explain year-to-year shifts. A paid subscription for company financials and news helps cross-check revenue direction and major event timing, and an import and export shipment-level database is used selectively where trade flows are a meaningful signal. These desk sources are not exhaustive, and we used additional public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what qualifies as a frozen snack in real buying and selling situations, and to confirm channel splits between retail and foodservice. We spoke with a mix of manufacturers, ingredient and packaging participants, cold-chain and distribution stakeholders, and retail or foodservice category teams across major regions. The respondent input was then used to close gaps we found during desk research on pricing, mix, and demand drivers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 43% |

| Mid tier: 54% | Functional/Unit leaders: 38% | EMEA: 30% |

| Smaller Players: 17% | Managers: 48% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built mainly from a top-down model where frozen food and snacking consumption signals are reconstructed by region, and then filtered down using category shares and channel participation for frozen snacks. To keep the totals realistic, we corroborate outputs with selective bottom-up approximations, such as sampled price per pack multiplied by estimated volumes, along with supplier and channel checks to adjust for mix differences.

Key inputs include retail freezer penetration and cold-chain reach, foodservice and quick-service restaurant demand for frozen snack formats, import and export direction for relevant frozen prepared foods, average selling price movement by major product group, and household snacking frequency changes that affect at-home consumption. Forecasting relies on scenario analysis supported by light multivariate regression where variables like disposable income, urbanization, and cold-chain expansion explain the demand curve. When bottom-up signals are missing for a smaller country, we bridge using proxy indicators from similar markets, before rolling the figures back into the regional total.

Data Validation & Update Cycle

Validation is done by checking whether the modeled value path matches independent signals like frozen food trade patterns, cold storage build-out, and retail and foodservice category momentum reported in public updates. If an outlier appears, the assumptions are re-opened, and targeted follow-ups are triggered to confirm whether the change came from pricing, mix, or a short-term supply constraint.

Before sign-off, the model goes through a multi-step analyst review where inputs, formulas, and year-to-year transitions are rechecked for consistency. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity additions, regulation shifts affecting frozen foods, or notable inflation changes. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Frozen Snacks Market Size Compared With Other Published Estimates

Published market sizes for frozen snacks can look far apart because the category label is used differently across sources, and the same year is not always treated as the same point in time. Differences also come from how foodservice is handled versus retail, and whether the estimate is built on value only or is anchored with volume checks.

The biggest gap drivers we see are scope choices, like counting frozen pizzas and adjacent frozen prepared items inside snacks, and then applying a single pricing uplift across regions without validating channel mix. Some publications also extend the forecast horizon and back-cast a base year using an aggressive growth path, which can inflate the starting value. By keeping retail and foodservice logic separate and using value plus tonnage sense checks for the 2025 to 2026 step, the spread is reduced in a way that is easier to trace. This is a modeling choice described by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 146.22 B (2025) | |

| Global Consultancy A | USD 119.66 B (2025) | Uses a narrower definition that tends to exclude some frozen snack formats sold through foodservice, which pulls down the addressable value for the same year. |

| Industry Publisher B | USD 181.50 B (2025) | Reports a higher starting value that likely blends a wider set of frozen prepared foods into the snack label and applies broad growth assumptions without clearly separating retail versus foodservice pricing and mix. |

Overall, the table shows that most of the variation is explainable once scope and channel treatment are made explicit. When definitions are aligned and pricing and mix are checked against real-world distribution patterns, the resulting market size becomes more stable and easier for decision-makers to use year after year.

Key Questions Answered in the Report

How large will global frozen snack sales be by 2031?

The frozen snacks market size is forecast to reach USD 202.52 billion by 2031.

Which region is expected to grow fastest?

Asia-Pacific is projected to advance at a 6.37% CAGR between 2026 and 2031.

Which product segment leads revenue today?

Potato-based snacks held a 32.62% Frozen snacks market share in 2025.

What channel is expanding quicker than retail?

Foodservice distribution is on track for a 6.59% CAGR, outpacing retail growth.

Page last updated on: