Zero Sugar Yogurt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

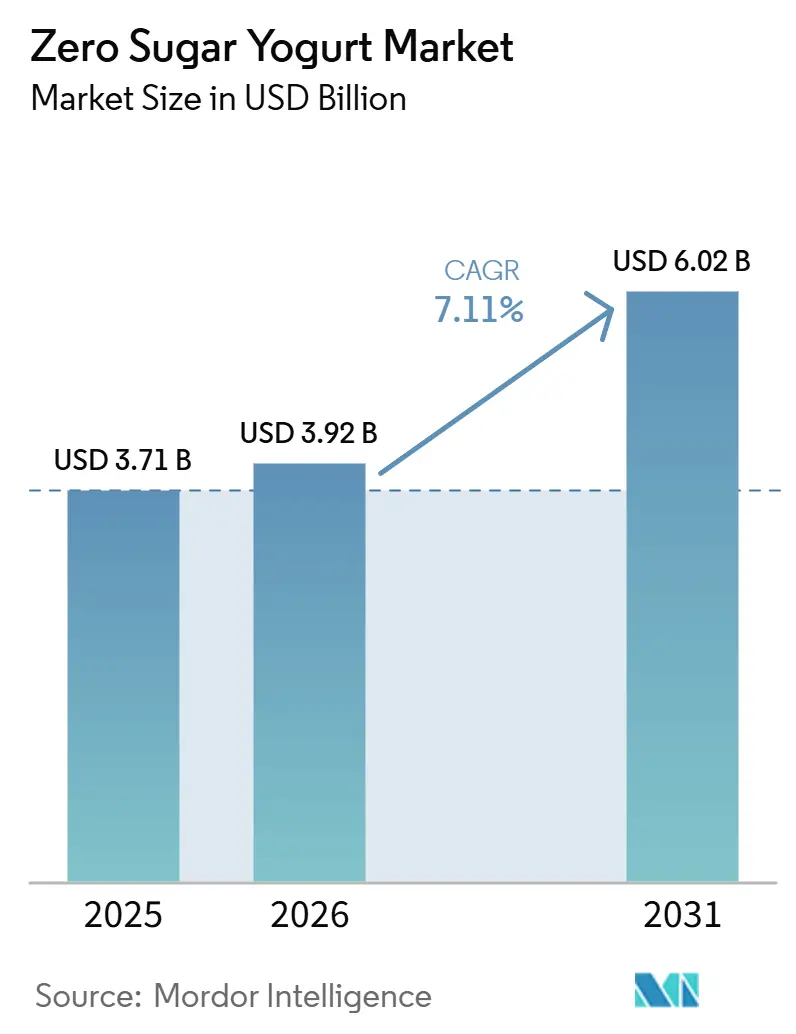

| Market Size (2026) | USD 3.92 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

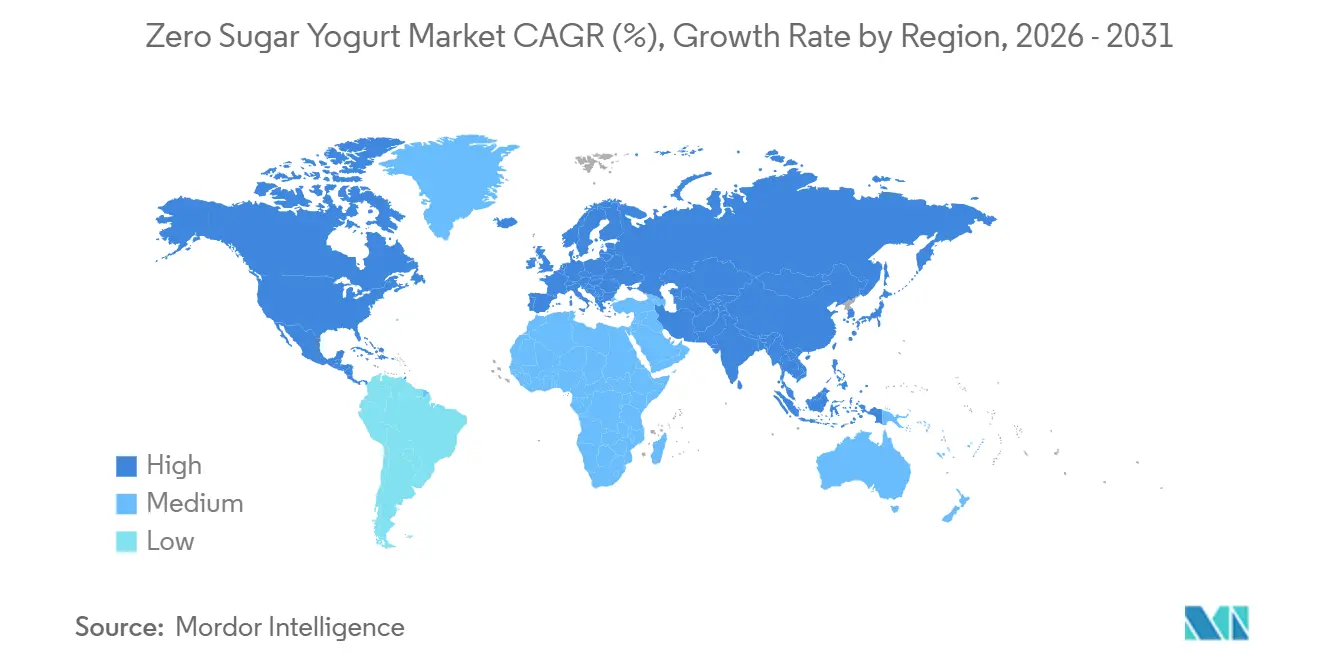

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zero Sugar Yogurt Market Analysis by Mordor Intelligence

The zero sugar yogurt market size was valued at USD 3.71 billion in 2025 and is estimated to grow from USD 3.92 billion in 2026 to reach USD 6.02 billion by 2031, at a CAGR of 7.11% during the forecast period (2026-2031). The zero sugar yogurt market is being supported by a broader shift in food choices toward sugar control, protein intake, and preventive nutrition, with the U.S. regulatory view on yogurt and type 2 diabetes risk strengthening category credibility in 2024. The zero sugar yogurt market is also drawing demand from consumers who are watching ingredient lists more closely and from GLP-1 users who prefer foods that deliver higher protein in smaller portions, which has pushed brands to sharpen both formulation and serving size strategies. The zero sugar yogurt market no longer sits only in a diet niche, because companies are now positioning it around metabolic health, digestive support, and daily use rather than occasional restriction. Competition in the zero sugar yogurt market is therefore moving toward protein density, cleaner sweetener systems, stronger sensory performance, and legally defensible front-of-pack claims. The main opportunity in the zero sugar yogurt market is still tied to better taste parity, premium everyday positioning, and broader access through modern retail and digital grocery channels.

Key Report Takeaways

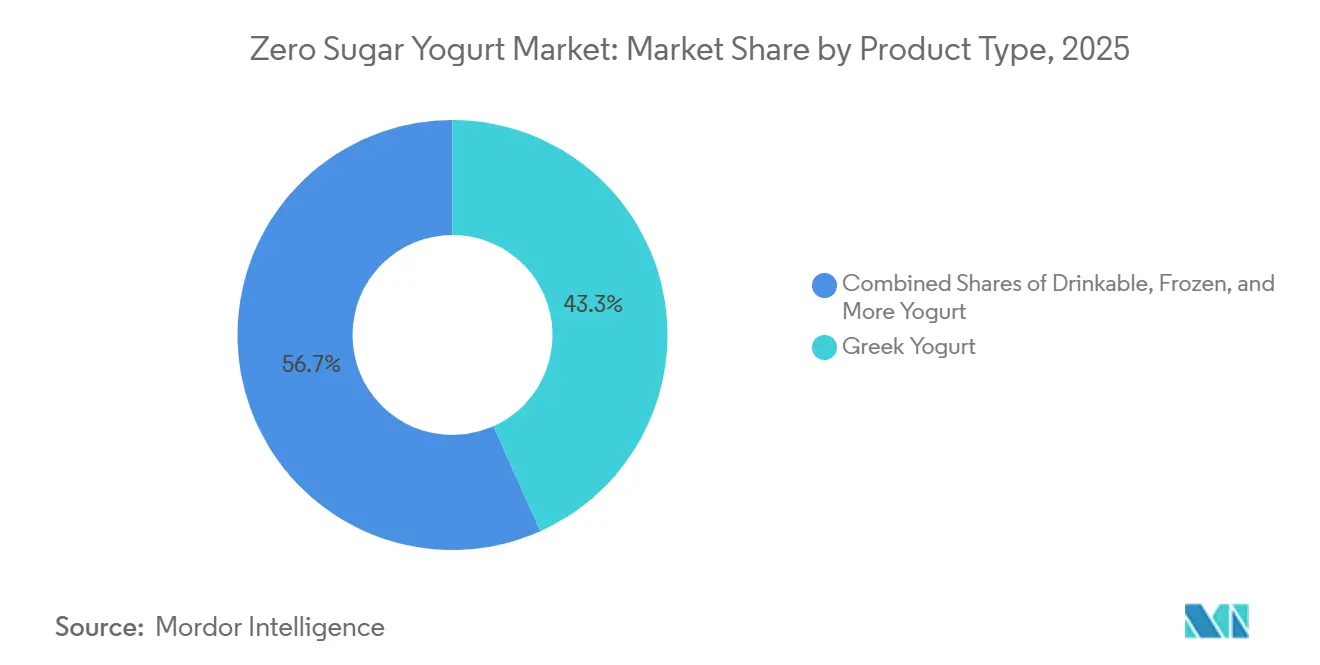

- By product type, Greek yogurt held 43.29% revenue share in 2025, while plant-based yogurt is forecast to expand at 8.72% CAGR through 2031.

- By flavor, plain variants held 75.37% revenue share in 2025, while flavored variants are projected to grow at 8.68% CAGR through 2031.

- By packaging, single-serve packs accounted for 38.26% revenue share in 2025, while drinkable bottles are forecast to grow at 8.55% CAGR through 2031.

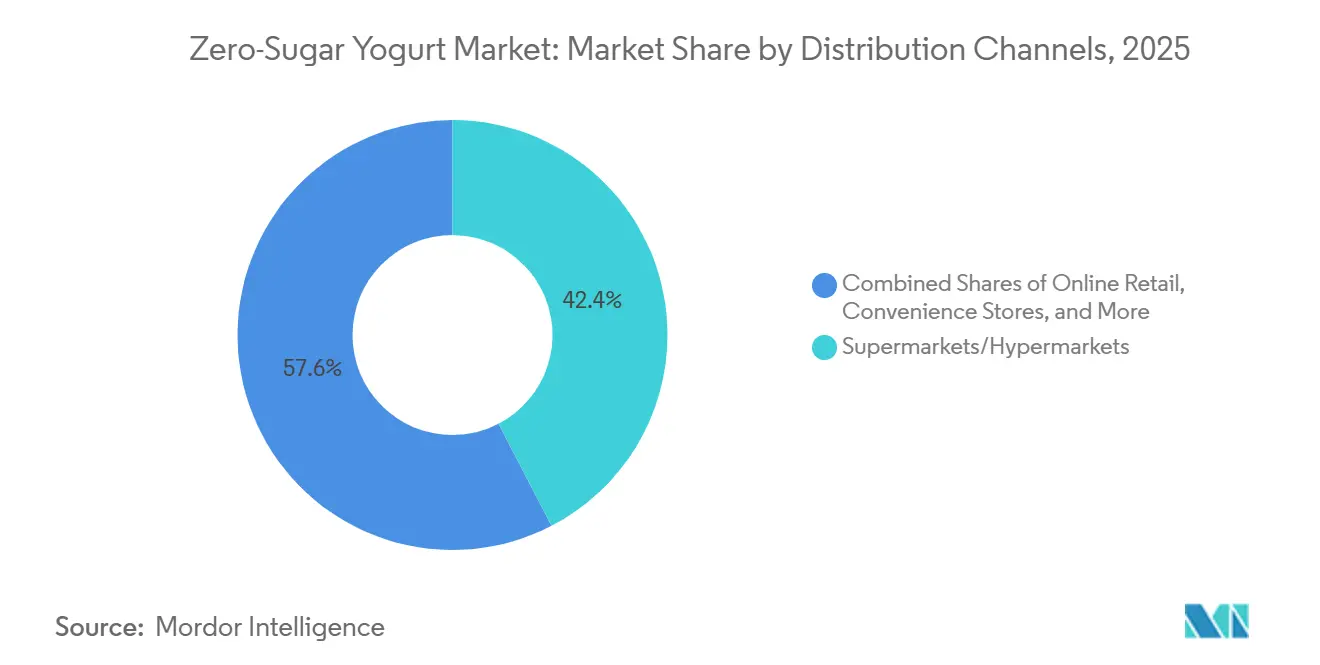

- By distribution channel, supermarkets and hypermarkets held 42.38% revenue share in 2025, while online retail is projected to expand at 8.67% CAGR through 2031.

- By geography, North America accounted for 36.48% revenue share in 2025, while Asia-Pacific is forecast to grow at 8.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Zero Sugar Yogurt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer focus on health and wellness | 2.3% | Global | Long term (≥ 4 years) |

| Rising demand for high-protein and functional yogurt products | 1.4% | North America & Europe, spill-over to APAC | Medium term (2–4 years) |

| Expansion of modern retail and online distribution channels | 1.0% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| Growing adoption of clean-label ingredients and natural sweeteners | 0.8% | North America & EU, spill-over to APAC | Medium term (2–4 years) |

| Increasing preference for convenient single-serve and on-the-go yogurt | 0.7% | North America, APAC, Europe | Medium term (2–4 years) |

| Premium product innovation with digestive and gut health benefits | 0.8% | North America & Europe, emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Focus on Health and Wellness

The zero sugar yogurt market is benefiting from the stronger link consumers now make between everyday food choices and long-term metabolic health. In March 2024, U.S. regulators recognized a qualified health claim that connected regular yogurt consumption with lower type 2 diabetes risk, and that widened category relevance beyond calorie control alone[1]Source: Food and Drug Law Institute, “FDA Announces Qualified Health Claim for Yogurt and Reduced Risk of Type 2 Diabetes,” FDLI, fdli.org. That shift mattered because it gave the zero sugar yogurt market a more credible health narrative at a time when diabetes prevalence and sugar reduction concerns were already rising. U.S. yogurt sales reached USD 11.8 billion in the 52 weeks ending April 2025, up 11.6% year on year, which shows that category demand was already broadening before the latest wave of premium product launches. The zero sugar yogurt market is now drawing more mainstream shoppers because products that fit sugar control, protein intake, and routine breakfast use are easier to justify as everyday purchases than as occasional diet items.

Rising Demand for High-Protein and Functional Yogurt Products

The zero sugar yogurt market is seeing stronger demand from shoppers who want more protein, digestive support, and practical satiety from a small serving. That shift is especially visible around GLP-1 usage, where reduced appetite makes nutrient density more important than portion volume, and Arla Foods Ingredients responded in April 2026 with no-added-sugar fermented yogurt concepts designed for that need. The product concept included a spoonable format with 20g protein per 120g serving, high calcium, and reduced lactose, which shows how the zero sugar yogurt market is moving toward tighter nutritional packaging rather than just sweeter reformulation. Scientific evidence also supports dairy yogurt as a functional delivery system, because probiotic survival rates in dairy-based matrices were reported at 50% to 80%, ahead of the 30% to 60% range seen in plant-based alternatives. When Danone’s Oikos range faced supply shortfalls in the second half of 2025, it signaled that the zero sugar yogurt market had already moved beyond trial demand and into a capacity planning challenge for major brands

Expansion of Modern Retail and Online Distribution Channels

The zero sugar yogurt market is expanding as refrigerated premium dairy products are no longer confined to shelf space in large physical stores. The rapid growth of online grocery platforms is improving product visibility, availability, and convenience for consumers seeking healthier dairy options. U.S. online grocery orders represented more than 19% of total grocery sales in the first quarter of 2026, with year-on-year growth of 20% or more for six consecutive quarters. This sustained momentum indicates that digital grocery channels are becoming an increasingly important route to market for chilled, premium, and better-for-you dairy products. Retail scale is also strengthening, as Walmart approaches a 40% share of the U.S. online grocery market and Amazon expands fresh grocery delivery windows. These developments give the zero sugar yogurt market stronger access to urban consumers, premium shoppers, and repeat-purchase households that value convenience, nutrition, and product variety.

Growing Adoption of Clean-Label Ingredients and Natural Sweeteners

The zero sugar yogurt market is at an important point on ingredient strategy because taste expectations are rising at the same time that sugar claims face closer legal and label scrutiny. In June 2026, Layn Natural Ingredients received FEMA GRAS approval for SteviUp M2, a steviol glycoside with improved solubility and reduced lingering sweetness, which directly addressed long-standing formulation complaints in yogurt applications. In the same month, Truvia introduced a tri-blend sweetener using allulose, stevia, and monk fruit in a 1:1 sugar-replacing ratio, giving the zero sugar yogurt market a more commercially ready route to improve taste while keeping no-added-sugar positioning. The May 2025 federal court ruling in Franco v. Chobani also reinforced FDA guidance that treats allulose as non-sugar for nutrition labeling purposes, which lowered legal uncertainty for zero sugar claims in the United States. Even so, the zero sugar yogurt market still faces cost pressure because monk fruit and other alternative sweeteners remain exposed to constrained supply and tariffs, making sourcing strategy almost as important as product taste

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for the taste of conventional sweetened yogurt | -0.5% | Global | Medium term (2–4 years) |

| Rising costs of natural sweeteners and product reformulation | -0.4% | Global, most acute in North America | Short term (≤ 2 years) |

| Complex regulatory requirements for labeling and health claims | -0.3% | North America & EU | Long term (≥ 4 years) |

| Consumer skepticism toward sugar-free and artificially sweetened products | -0.4% | North America & Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference for the Taste of Conventional Sweetened Yogurt

Taste remains one of the clearest limits on how fast the zero sugar yogurt market can convert mainstream buyers. A 2025 study in the Journal of Food Science found that allulose-sweetened yogurt improved purchase intent after nutritional disclosure, yet sucrose-sweetened controls still performed better on initial liking, while stevia variants faced bitterness-related declines in purchase intent[2]Source: “Rare Sugar Sweetened Yogurt, Sensory Profiles, Liking and Consumer Perception,” Journal of Food Science, doi.org. That matters because the zero sugar yogurt market is trying to win repeat buying, not just health-led trial, and repeat buying depends on taste matching routine expectations. The issue becomes more visible in flavored products, where sweetener systems must work with fruit notes, cocoa profiles, and added functional ingredients without creating off-notes. Brands that solve this balance can unlock a larger crossover audience, but until then, the zero sugar yogurt market will continue to face resistance from shoppers who still compare it directly with conventional sweetened yogurt.

Rising Costs of Natural Sweeteners and Product Reformulation

The zero sugar yogurt market is also constrained by ingredient economics, especially where natural sweeteners depend on tight supply chains and trade-sensitive sourcing. Icon Foods reported rising monk fruit prices across extract grades because of concentrated harvest cycles in southern China, logistics pressure, and tariffs on Chinese-origin alternative sweeteners including stevia, monk fruit, and erythritol. Allulose, which has become one of the most useful ingredients for achieving zero sugar labeling, also faced rising demand through 2026 as brands moved away from other sweeteners under heavier tariff pressure. Reformulation in the zero sugar yogurt market is therefore not only a technical task, because every change in sweetener ratio can affect cost, taste, label position, and product consistency. Larger manufacturers with multi-origin procurement and blended sweetener platforms are in a better position to absorb that pressure than smaller brands that rely on narrower sourcing contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Greek Yogurt Anchors Volume, Plant-Based Supports the Fastest Expansion

Greek yogurt held 43.29% of zero sugar yogurt market share in 2025, which kept it as the core volume contributor within the zero sugar yogurt market. Its position rests on naturally high casein protein, a thick texture that fits premium expectations, and better alignment with clean-label sweetener systems than more delicate bases. The zero sugar yogurt market also benefits from Greek yogurt’s strong fit with breakfast, snack, and post-workout occasions, which gives the format more daypart flexibility than narrower indulgence products. Drinkable yogurt serves a different use case centered on convenience, while frozen yogurt remains more limited because zero sugar formulations still have to protect texture through freezing and thawing.

Plant-based yogurt in the zero sugar yogurt market is projected to grow at 8.72% CAGR through 2031, making it the fastest-growing product type. A 2026 study in Future Foods showed that soy-based products represented 41% of commercial plant-based yogurt formulations, followed by coconut at 26%, oat at 13%, and almond at 8% DOI.ORG. That base mix matters because the zero sugar yogurt market can use these platforms to target consumers who want both sugar reduction and a plant-based diet in one purchase. The segment also creates room for premium positioning because it serves shoppers who may not be active in conventional dairy at all. Over the forecast period, the zero sugar yogurt market is likely to see plant-based formats reshape competition at the premium end rather than displace Greek yogurt’s scale position in the near term.

By Flavor: Plain Holds the Core, Flavored Variants Extend Usage

Plain variants accounted for 75.37% of the zero sugar yogurt market in 2025, which shows how strongly the zero sugar yogurt market still depends on simple everyday use cases. Plain products fit breakfast bowls, cooking, protein intake, and clinically oriented gut-health positioning more easily than flavored options do. They also face fewer formulation conflicts because the sweetener system does not have to carry fruit, dessert, or botanical notes at the same time. The functional advantage is reinforced by dairy yogurt’s role as a probiotic carrier, with 50% to 80% survival rates reported in dairy matrices compared with 30% to 60% in plant-based alternatives.

Flavored formats within the zero sugar yogurt market size are projected to grow at 8.68% CAGR through 2031, which makes them the main route for category broadening. The zero sugar yogurt market needs these products to reach consumers who want taste variety and a more indulgent eating experience without returning to standard sweetened yogurt. Danone Japan expanded its “Otona no Kashikoi Sweets” dessert yogurt series to full nationwide supermarket distribution in February 2026, showing that brands continue to use flavor to widen appeal while keeping calorie and sugar restraint. In Europe, yogurt launches increasingly combine digestive claims with flavor innovation, which suggests that the zero sugar yogurt market can extend beyond plain everyday formats without giving up health positioning. As sensory systems improve, flavored products should help the zero sugar yogurt market increase household penetration rather than only deepen repeat buying among existing health-focused users[3]Source: “Probiotic-Fortified Functional Foods, Integrating Nutrient Delivery and Gut Health Benefits,” Frontiers in Nutrition, frontiersin.org.

By Packaging: Single-Serve Leads Current Scale, Drinkable Bottles Build New Occasions

Single-serve packs accounted for 38.26% of revenue in 2025, keeping them as the largest packaging format in the zero sugar yogurt market. Their lead comes from portion control, portability, and suitability for fitness consumers, weight-management users, and GLP-1 users who want more nutritional control in smaller servings. Multi-serve packs remain relevant for the zero sugar yogurt market where plain yogurt is used daily at home for breakfast and cooking. The current mix also favors single-serve packs because they support premium pricing and stronger refrigerated visibility in physical retail.

Drinkable bottles in the zero sugar yogurt market are projected to grow at 8.55% CAGR through 2031, which reflects a shift toward beverage-like convenience. The zero sugar yogurt market uses this format to compete not only in dairy aisles but also against protein drinks and meal-adjacent beverages. Danone’s Oikos Protein Shakes added strawberry and mocha latte flavors in January 2026, each with 30g protein, 5g prebiotic fiber, and zero added sugar, which shows how drinkable formats stretch the category into functional beverage space. In Asia, drinkable yogurt already has strong consumer familiarity, and that supports a faster adoption path for similar zero sugar products. Over time, drinkable bottles should give the zero sugar yogurt market a broader set of consumption moments than spoonable cups can reach alone.

By Distribution Channel: Supermarkets Keep the Base, Online Retail Delivers the Fastest Gain

Supermarkets and hypermarkets accounted for 42.38% of distribution in 2025, which kept them as the leading channel in the zero-sugar yogurt market. Their role remains important because shoppers often want to check labels, sugar content, protein levels, and brand cues directly before purchase. Circana data cited by Dairy Foods showed that supermarkets captured 55% of overall U.S. yogurt sales, which supports the continued strength of physical retail for core dairy purchases. Convenience stores and specialty channels fill narrower roles in the zero sugar yogurt market, especially for impulse purchases or premium health-focused assortments.

Online retail in the zero-sugar yogurt market is projected to grow at 8.67% CAGR through 2031, making it the fastest-growing distribution format. E-commerce’s share of grocery spending is expected to rise from 18% in 2024 to 25.5% by 2028, representing around USD 452 billion, creating a larger digital addressable base for chilled dairy products. The zero sugar yogurt market gains more than volume from this channel because digital orders generate repeat-buy signals around flavor rotation, sweetener choice, and protein preference. Kroger’s e-commerce business reaching profitability earlier than expected also suggests that premium refrigerated products can support healthier online economics when fulfillment systems are in place. For challenger brands, online distribution gives the zero sugar yogurt market a route to scale without depending fully on shelf-space negotiations in traditional retail.

Geography Analysis

North America held 36.48% of zero sugar yogurt market share in 2025, which kept it as the largest regional contributor to the zero sugar yogurt market. The region benefits from clearer labeling conditions, and the May 2025 dismissal of the Franco v. Chobani class action supported the FDA's treatment of allulose as non-sugar for labeling purposes under 21 C.F.R. § 101.9. That ruling reduced legal friction around zero-sugar claims at a time when companies were already leaning harder into no-added-sugar launches. U.S. yogurt sales reached USD 11.8 billion in the 52 weeks ending April 2025, up 11.6% year on year, which points to a healthy base category for premium reformulation and premiumization. Online grocery growth also keeps improving product reach in North America, especially for premium chilled products with narrower shelf presence in smaller stores.

Asia-Pacific zero sugar yogurt market size is projected to grow at 8.25% CAGR through 2031, making it the fastest-growing regional block in the zero sugar yogurt market. The region’s yogurt retail value was already growing at 8.0% annually, ahead of the 5.4% global category average, and 68% of Asian consumers reported eating or drinking yogurt weekly. In South Korea, Pulmuone Danone launched Double Zero Activia in March 2026 with zero added sugar, zero fat, reduced lactose, and 04 billion CFUs, which shows how the zero sugar yogurt market is moving into more complete functional positioning at the regional level. Japan remains important for flavored yogurt innovation, while China’s large dairy base makes low-sugar and functional launches commercially relevant even in a more difficult category environment. India also stands out in the zero sugar yogurt market because low per-capita dairy consumption and fast modern retail expansion leave significant room for future branded adoption.

Europe remains a mature but important part of the zero sugar yogurt market, with the UK and Germany acting as key innovation points around gut health, probiotic science, and sugar reduction. The UK has led European yogurt launches, and digestive health and gut health claims have been among the fastest-growing claim platforms, which aligns well with the direction of the zero sugar yogurt market. Beyond Europe, Danone and Arcor formed a dairy joint venture in Argentina in March 2026 covering 11 production plants, which showed rising confidence in South American dairy demand and scale economics. In Africa, Arla Foods launched Cool Cow Yoghurt in Nigeria in February 2026 using 100% locally sourced milk, which signals that the zero sugar yogurt market may eventually benefit from early category-building in large population markets even where penetration remains low today

Competitive Landscape

The zero sugar yogurt market remains fragmented, but the rivalry within that fragmented structure is becoming sharper because leading brands are clustering around the same claims of high protein, no added sugar, and digestive benefit. Danone’s June 2026 lawsuit against Chobani over protein labeling in multi-serve yogurt formats showed that the zero sugar yogurt market is now competitive enough for front-of-pack communication to become a legal dispute rather than only a marketing theme. Danone also described Oikos as a EUR 1 billion franchise and said supply fell short in the second half of 2025, which indicates that brand scale alone does not remove production pressure in fast-moving functional dairy. Chobani’s USD 650 million fundraising round and stated interest in acquisitions suggest that the zero sugar yogurt market could see stronger expansion beyond legacy Greek yogurt into adjacent dairy and drinkable format. The main competitive split in the zero sugar yogurt market is between large incumbents building stacked functional claims and smaller challengers using cleaner ingredients, plant-based bases, and digital-first selling models.

White space in the zero sugar yogurt market is strongest where new health needs overlap with premium product design. Arla Foods Ingredients used that opening in April 2026 by presenting no-added-sugar, high-protein fermented yogurt concepts tailored to GLP-1 users, which offers smaller manufacturers a route to participate through ingredient partnerships rather than long internal development cycles. Danone also used acquisitions to strengthen its Asia-Pacific position through the planned purchase of MADE Group and the full buyout of its Saputo Dairy Australia joint venture, showing that the zero sugar yogurt market is important enough to shape wider regional portfolio moves. FAGE International’s planned EUR 150 million facility in the Netherlands points to another route, namely securing supply and authenticity around Greek-style yogurt rather than depending mainly on formulation novelty. These moves suggest that the zero sugar yogurt market will reward both scale expansion and format specialization, depending on the company’s starting strength.

Technology and sourcing decisions are also becoming more central in the zero sugar yogurt market. Scientific review work published in 2025 highlighted AI-based multi-omics analysis as an emerging tool for probiotic strain optimization, which may eventually give mid-tier companies more precise ways to differentiate beyond branding alone. At the same time, sweetener volatility means that procurement discipline can shape margin performance just as much as product innovation can shape shelf appeal. The zero sugar yogurt market also faces a practical pricing challenge because GLP-1-led portion control may support demand for smaller formats while making consumers more sensitive to value per serving. That keeps the zero sugar yogurt market focused on a narrow balance of nutrition, taste, legal clarity, and premium affordability.

Zero Sugar Yogurt Industry Leaders

Danone S.A.

Chobani LLC

Nestlé S.A.

Groupe Lactalis

Arla Foods amba

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Meiji expanded its functional dairy portfolio with the launch of a natural-flavoured probiotic yogurt with no added sugar, targeting consumers seeking clean-label and healthier food choices. The product combines probiotic benefits with a sugar-free formulation, reinforcing the company's focus on digestive wellness and responding to growing consumer demand for low-sugar, minimally processed yogurt products.

- September 2025: Yoplait expanded its children's dairy portfolio with the launch of Petits Filous Natural, the brand's first natural unsweetened kids' yogurt. Fortified with calcium and vitamin D and containing no added sugar, the product addresses growing consumer demand for clean-label, low-sugar dairy products while strengthening Yoplait's position in the health-focused yogurt segment.

- July 2025: Namyang Dairy Products launched Bulgaris Sugar-Free Plain, a yogurt containing no added sugar or sweeteners, with sweetness derived solely from naturally occurring lactose in milk. The launch expands the company's health-focused dairy portfolio.

Global Zero Sugar Yogurt Market Report Scope

| Greek Yogurt |

| Drinkable Yogurt |

| Plant-Based Yogurt |

| Frozen Yogurt |

| Plain |

| Flavored |

| Single-Serve Packaging |

| Multi-Serve Packaging |

| Drinkable Bottles |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Channels |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Greek Yogurt | |

| Drinkable Yogurt | ||

| Plant-Based Yogurt | ||

| Frozen Yogurt | ||

| By Flavor | Plain | |

| Flavored | ||

| By Packaging | Single-Serve Packaging | |

| Multi-Serve Packaging | ||

| Drinkable Bottles | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Channels | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the zero sugar yogurt market by 2031?

The zero sugar yogurt market is projected to reach USD 6.02 billion by 2031 from USD 3.92 billion in 2026, at a CAGR of 7.11% over 2026-2031.

Which product type currently leads zero sugar yogurt sales?

Greek yogurt led with 43.29% revenue share in 2025 because it fits high-protein positioning, premium texture expectations, and everyday consumption needs.

Which format is expanding the fastest in this category?

Plant-based yogurt is forecast to grow at 8.72% CAGR through 2031, making it the fastest-growing product type in the category.

What is driving demand for high-protein zero sugar yogurt?

GLP-1 usage, metabolic health awareness, and the need for more protein in smaller servings are pushing brands toward denser and more functional yogurt formulations.

Page last updated on: