Healthy Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

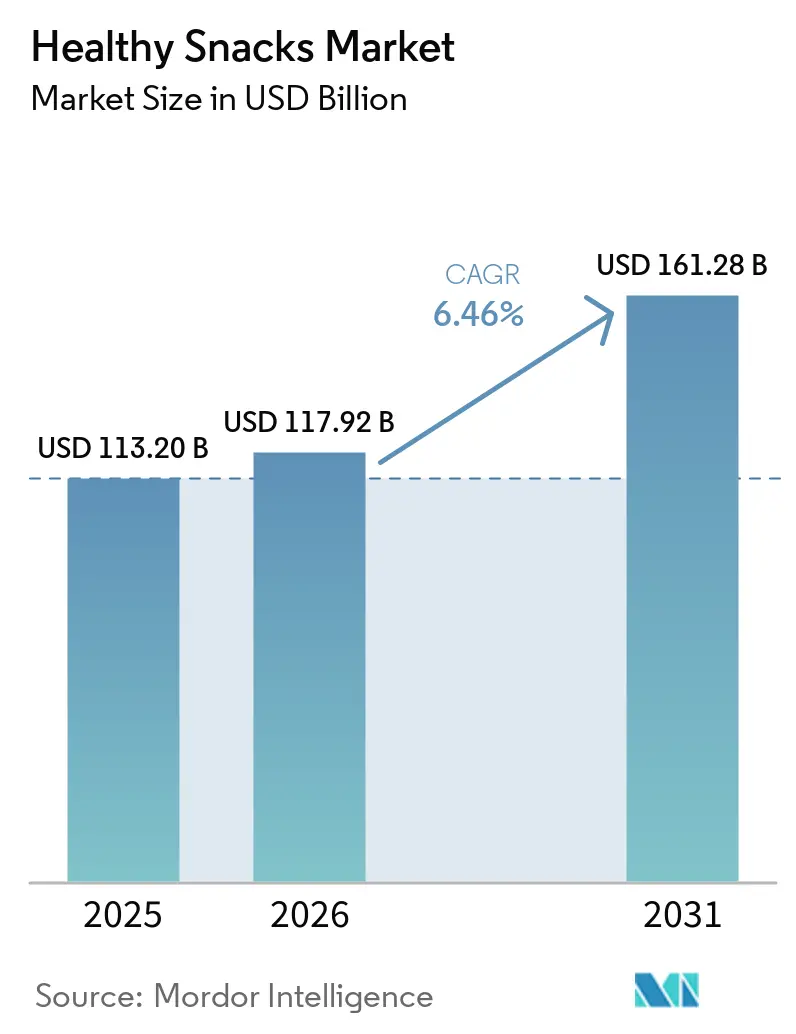

| Market Size (2026) | USD 117.92 Billion |

| Market Size (2031) | USD 161.28 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthy Snacks Market Analysis by Mordor Intelligence

The healthy snacks market size is expected to increase from USD 113.2 billion in 2025 to USD 117.9 billion in 2026 and reach USD 161.3 billion by 2031, growing at a CAGR of 6.5% over 2026-2031. The healthy snacks market is benefiting from a durable shift in consumer buying behavior, as routine snacking is moving closer to everyday nutrition rather than occasional indulgence. Product development is also becoming more targeted, with brands focusing on protein, fiber, portion control, and cleaner ingredient lists to improve repeat purchase and shelf differentiation. The healthy snacks market is also being reshaped by wider channel access, since large retailers are expanding health-oriented shelf space while digital channels help smaller brands reach niche demand without heavy physical distribution costs. At the same time, premium pricing and rising scrutiny of health claims remain important limits on faster adoption, especially when households compare better-for-you products with lower-priced conventional snacks. This keeps the healthy snacks market attractive, but it also means that companies with clearer labeling, stronger formulation credibility, and better pricing architecture are in a stronger position through 2031.

Key Report Takeaways

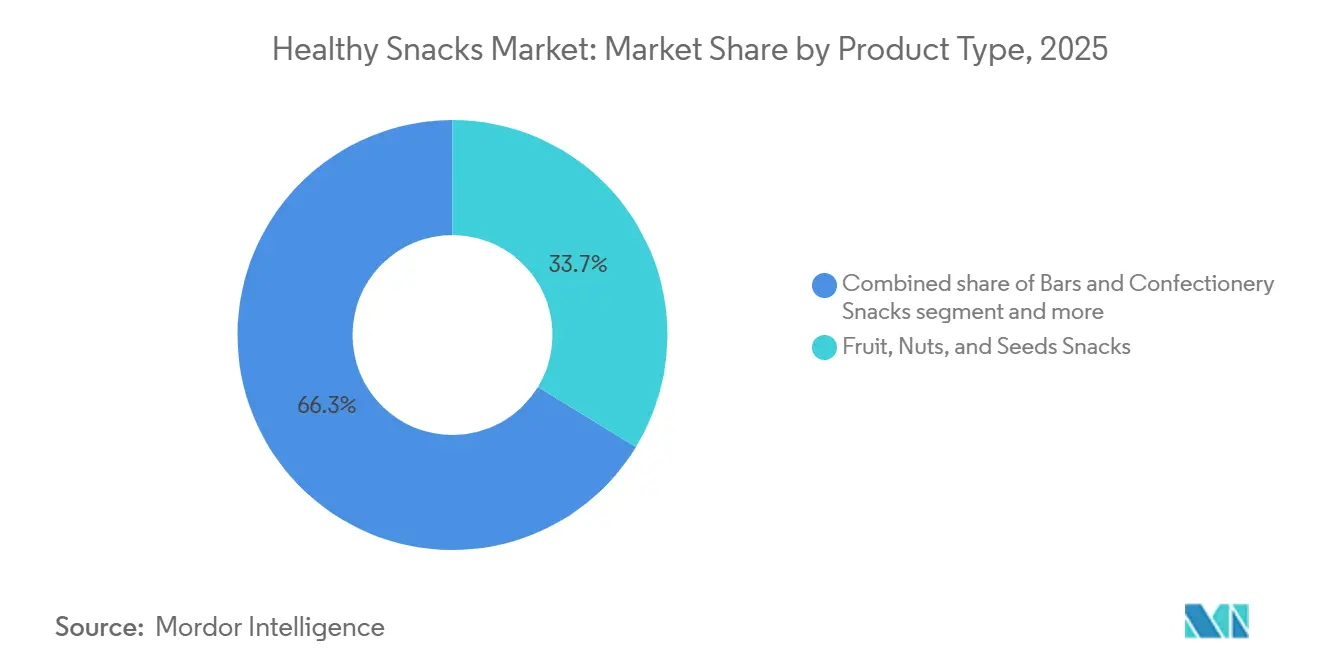

- By product type, fruit, nuts, and seeds snacks accounted for the largest share of the healthy snacks market, at 33.71% in 2025, while bars and confectionery snacks are projected to grow at the fastest CAGR of 7.46% during 2026-2031.

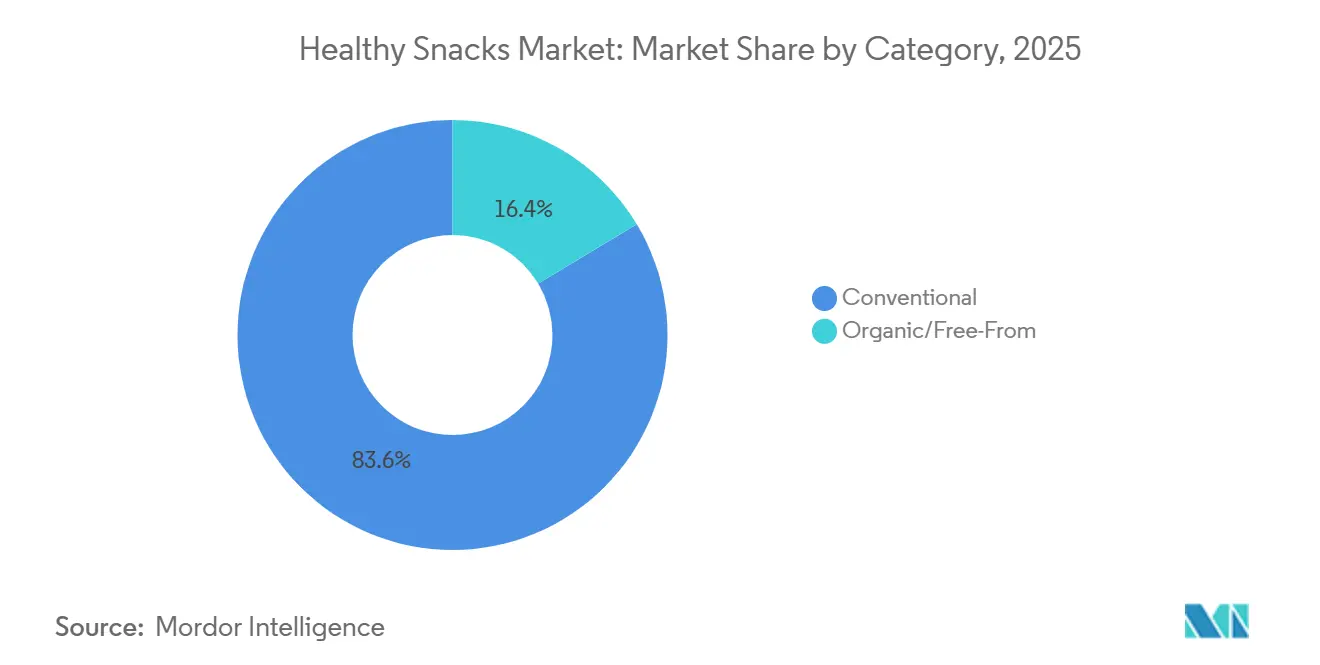

- By category, the conventional segment retained 83.62% share of the healthy snacks market in 2025, whereas organic and free-from products are forecast to expand at an 8.11% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for the largest share of the healthy snacks market, at 52.13% in 2025, while online retail stores are projected to grow at the fastest CAGR of 7.51% during 2026-2031.

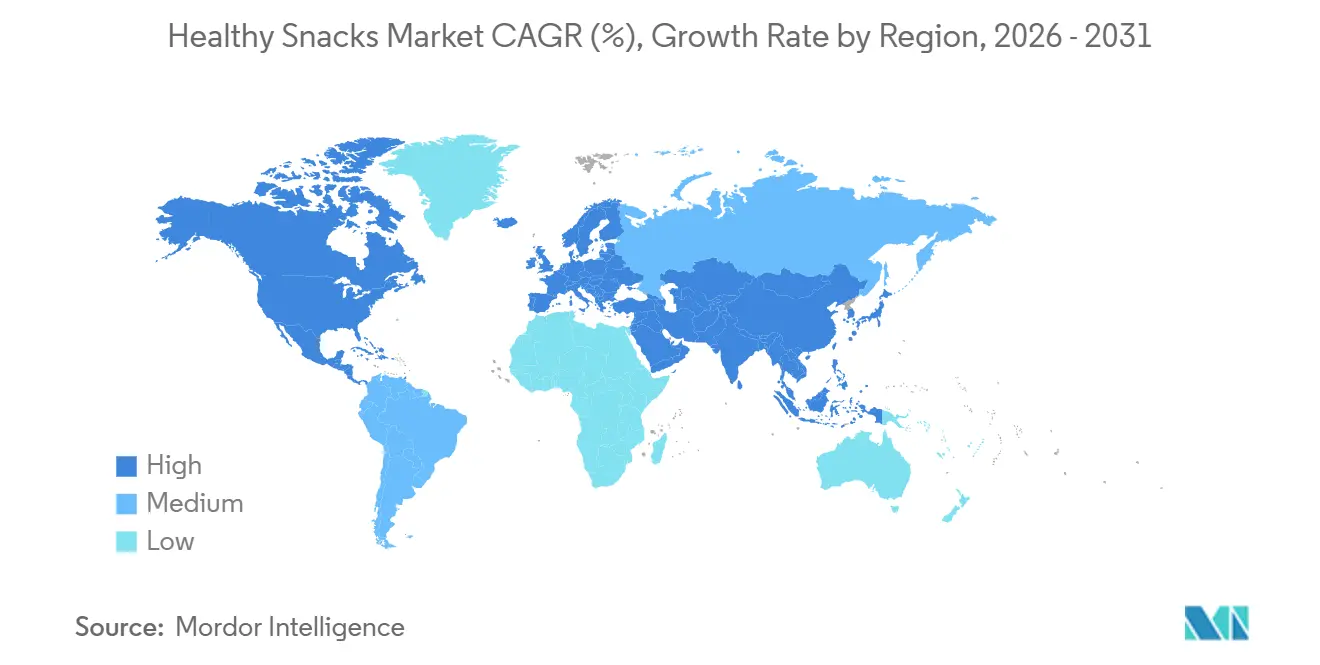

- By geography, North America accounted for the largest share of the healthy snacks market, at 36.40% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 7.98% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthy Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Consciousness and Preventive Nutrition | +1.4% | Global | Long term (≥ 4 years) |

| Clean Label and Ingredient Transparency Demand | +0.7% | North America and Europe | Medium term (2-4 years) |

| Growing Snacking Frequency and Meal Replacement Trends | +0.7% | Global | Short term (≤ 2 years) |

| Portion-Controlled Snacking for Busy Lifestyles | +0.4% | North America and the Asia-Pacific urban centers | Short term (≤ 2 years) |

| Functional Snacking for Protein, Fiber, and Satiety | +1.8% | Global; strongest in North America and the Asia-Pacific | Medium term (2-4 years) |

| E-Commerce and Direct-To-Consumer Expansion | +0.8% | Global; strongest in the Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and preventive nutrition

As consumers increasingly view food as a tool for long-term wellness, weight management, and disease prevention, the global healthy snacks market is witnessing significant growth, driven by rising health consciousness and a focus on preventive nutrition. Health authorities, including the World Health Organization (WHO) and the U.S. Department of Agriculture (USDA), advocate for diets abundant in whole grains, fruits, nuts, seeds, fiber, and protein, while simultaneously urging reductions in sugar, sodium, and unhealthy fats[1]Source: U.S. Department of Agriculture, “National Organic Program,” USDA, usda.gov. This dietary shift is fueling a heightened demand for nutrient-dense snacks that offer health benefits beyond mere nutrition. Market studies reveal a consistent consumer shift from traditional snacks to alternatives that are low in sugar, high in protein, and boast clean labels, bolstering category growth. Reflecting this trend, Wellbe Foods debuted 14 healthier snack products in 2025, ranging from vacuum-cooked options to traditional snacks with enhanced nutritional profiles. Concurrently, many brands broadened their high-protein snack selections. By 2026, manufacturers ramped up innovation, introducing protein-rich bars, bites, and other health-centric snack formats tailored for preventive health and active lifestyles, further propelling market growth.

Functional snacking for protein, fiber, and satiety

While protein has long been the leading functional claim in the realm of healthier snacking, fiber's rapid rise to prominence signals a pivotal shift in product strategy. By 2025, a significant number of consumers were actively seeking to boost their fiber intake. Yet, a mere 5% of Americans were hitting their daily fiber targets. This discrepancy presents a lucrative opportunity: brands are now capitalizing on the integration of natural fiber sources into everyday snacks. For the year ending March 22, 2026, granola bars emphasizing fiber saw a notable uptick in repeat purchases, suggesting that initial trials are swiftly turning into brand loyalty. This trend is further bolstered by the rising adoption of GLP-1 medications. Users of these medications undergo changes in digestion, amplifying their need for dietary fiber. This creates a favorable market environment for brands that have established a strong fiber presence in their nutritious snack offerings. Food Business News, May 2026.

Growing snacking frequency and meal replacement trends

As consumers increasingly prioritize convenience and nutrition, the global healthy snacks market is witnessing a surge. Busy lifestyles are prompting many to favor smaller, more frequent eating occasions, heightening the demand for snacks that offer sustained energy and balanced nutrition. Research from the International Food Information Council (IFIC) underscores a robust consumer interest in protein-rich and functional foods, with high-protein diets emerging as a dominant eating trend. Industry surveys further reveal that over half of consumers have begun substituting traditional meals with snacks, propelling the "snackification" trend. This shift has spurred manufacturers to craft products that seamlessly blend the characteristics of snacks and meal substitutes. In 2025, in response to this evolving landscape, there was a notable uptick in the launch of protein-enriched bars, savory protein snacks, and healthier baked goods. The following year, 2026, witnessed a surge in innovation, with a focus on nutrient-dense snack bars, bites, nuts, seeds, and protein-centric snacks, all tailored to offer meal-like nutrition in a convenient format. A testament to this trend, in May 2026, Ready, a rapidly ascending name in the functional snacking realm, unveiled its premium Ready Protein Bars at Target outlets nationwide and on Target.com.

E-Commerce and direct-to-consumer expansion

The expansion of e-commerce and direct-to-consumer (D2C) channels is significantly driving the global healthy snacks market by improving product accessibility, enabling personalized consumer engagement, and accelerating the reach of emerging health-focused brands. Online platforms allow consumers to conveniently discover, compare, and purchase specialized snacks such as high-protein bars, low-sugar products, plant-based snacks, and functional foods that may have limited shelf space in traditional retail outlets. Industry analyses highlight that expanding online grocery adoption, subscription-based snack services, and D2C distribution models are helping healthy snack brands reach health-conscious consumers more effectively while gathering real-time consumer insights for product innovation. Government-backed nutrition-labeling initiatives and retailer wellness programs in regions such as Europe, the UK, and Australia are also increasing the visibility of healthier snack options in digital retail environments. Reflecting this trend, Tom Brady launched GOAT Gummies through instant-delivery platform Gopuff in 2025, while 2026 has seen continued growth in online-first healthy snack offerings, subscription models, and personalized snack recommendations supported by digital commerce platforms and AI-enabled grocery services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing Versus Conventional Snacks | -0.8% | Global; acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Shelf-Life and Texture Stability Constraints | -0.4% | Global; greater for clean-label minimal-processing formats | Medium term (2-4 years) |

| Reformulation Risk from Taste-Health Trade-Offs | -0.3% | Global | Short term (≤ 2 years) |

| Consumer Skepticism Toward Health Claims and Ultra-Processed Foods | -0.7% | North America and Europe; highest consumer awareness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium pricing versus conventional snacks

Better-for-you snacks face persistent growth challenges, primarily due to their price gap with conventional alternatives. Inflation has intensified this challenge. Research from SPINS, showcased at the 2026 Sweets and Snacks Expo in Las Vegas, highlights a duality in consumer behavior: while health motivations drive choices, there's a pronounced sensitivity to price. This dynamic compels brands to showcase clear functional value to justify any premium pricing. Another dimension, often overlooked, is the influence of private labels. Retailers' own healthy snack lines, accounting for an estimated 20-25% of market value in major retail channels, are putting pressure on the margins of branded better-for-you products in mainstream markets. Brands positioned in the mid-market, lacking a distinct functional or sensory claim, find themselves at risk. They're squeezed from above by premium innovators and from below by well-funded retailers. However, strategies like price-pack architecture, which offer the same functional claims across varied serving sizes and price points, have seen notably stronger household penetration, especially among demographics sensitive to inflation.

Consumer skepticism toward health claims and ultra-processed foods

Health claims are no longer just a marketing hurdle; they're becoming a significant barrier for brands promoting healthier snacks. The urgency is heightened by the US FDA's regulatory influence. Research from Oregon State University, set to be published in 2025, underscores this: FDA-approved "Healthy" labels can boost a product's price by an average of USD 0.59[2]Source: Oregon State University, “FDA-Endorsed Healthy Labels Increased Consumer Willingness To Pay,” Oregon State University Newsroom, oregonstate.edu. This premium is largely due to the trust a government endorsement brings, bridging a gap that brand claims often struggle to fill. Across the Atlantic, brands in Europe must tread carefully. Compliance with EU Regulation (EC) No 1924/2006 is non-negotiable[3]Source: European Commission, “Nutrition and Health Claims,” European Union, europa.eu. This regulation dictates what health claims can be made on packaging. Brands that stray from these guidelines risk not only product withdrawal but also damage to their reputation. The stakes are high: when brands exaggerate benefits without solid evidence, they don't just erode their own credibility. They sow distrust across the entire category, creating a compliance challenge that hits smaller, less-resourced brands the hardest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bars and Confectionery Outpace Fruit and Nut Segment Leadership

In 2025, Fruit, Nuts, and Seeds Snacks captured a dominant 33.71% revenue share, leading all product types. This dominance stems from consumers increasingly recognizing these snacks as clean-label and minimally processed. The preference for these whole-food options underscores a demand for health-oriented products that don't rely heavily on marketing. Bakery Snacks and Savory Snacks hold significant mid-tier positions. Their growth is bolstered by reformulations that swap out artificial stabilizers for natural ones. However, the added cost of these clean-label ingredients does temper their expansion. Meanwhile, as cold-chain logistics advance in emerging markets, Frozen and Refrigerated Snacks are becoming more prominent. This progress allows for a broader distribution of fresh, protein- and vegetable-based snacks. Dairy Snacks are riding the wave of high-protein dairy trends. Formats like Greek yogurt pouches, cheese crisps, and drinkable kefirs resonate with today's health-focused consumers prioritizing macronutrients. Other Product Types highlight a range of emerging snacks, from mushroom-based treats to seaweed crisps, appealing to ingredient-savvy early adopters.

Bars and Confectionery Snacks are set to outpace all others, boasting a projected 7.46% CAGR through 2031. This surge underscores the bar format's evolution into a key arena for healthier snacking, blending indulgence with functional benefits. Highlighting this trend, Mondelēz International's Q1 2026 report unveiled its Perfect Snacks Protein + Prebiotics bars. Each serving packs 20 grams of protein and 6 grams of prebiotic fiber, showcasing how major players are now leveraging health claims once exclusive to niche protein bar brands.

By Category: Conventional Reformulation Subsidizes Organic/Free-From Growth

In 2025, the Conventional segment commanded a dominant 83.62% share of category revenues, yet this figure belies a noteworthy shift in formulations. Leading manufacturers are increasingly purging artificial colors, flavors, and synthetic preservatives from their conventional lines. This move aligns with clean-label trends, effectively bridging the perceived quality divide between Conventional and Organic/Free-From categories, all without pushing consumers to a higher price tier. In January 2026, PepsiCo unveiled its strategy to phase out artificial colors and flavors from its primary snack lines. Concurrently, the company introduced Simply NKD Cheetos and Doritos, touting them as variants with cleaner ingredients. This subtle reformulation within the conventional tier underscores a two-pronged approach: maintaining volume while positioning for premium line introductions.

While the Conventional segment remains dominant, the Organic/Free-From category is set to outpace all others, projected to grow at an 8.11% CAGR through 2031. Certified organic brands, operating in their two primary markets, lean on benchmarks like the USDA National Organic Program (NOP) and the EU's Organic Regulation (EU) 2018/848. These certifications not only validate their claims but also serve as trust signals amidst prevalent skepticism. In 2024, Germany, the EU's organic frontrunner, saw a 5.7% uptick in organic food sales, driven more by volume increases than mere price inflation, as reported by the German Federation of Organic Food Producers (BÖLW). Meanwhile, France, the continent's second-largest organic market, rebounded from a post-inflation slump, achieving total organic sales of EUR 12.2 billion in 2024. These positive trends in Europe's organic markets bolster the global growth outlook for the Organic/Free-From segment.

By Distribution Channel: Online Retail Closes In on Brick-and-Mortar Supremacy

In 2025, supermarkets and hypermarkets command a leading 52.13% share of channel revenues in the healthy snack distribution arena. Their dominance is bolstered by dedicated health food aisles, prime promotional shelf space, and the capacity to simultaneously stock both branded and private-label nutritious snacks. With a physical density underscored by 7-Eleven's operation of over 80,000 outlets across 16 countries, brick-and-mortar retail is poised to anchor category volume for the foreseeable future. Convenience stores are adapting, seizing on-the-go functional eating moments with smaller, portion-controlled items that cater to the meal-replacement trends among urban youth. Meanwhile, other distribution avenues, like specialty health retailers, gym kiosks, and vending operators, are tapping into niche segments, leveraging a premium pricing strategy due to a higher willingness to pay, a feat not easily achievable in mainstream channels.

Online retail stores are leading the charge, boasting a robust 7.51% CAGR through 2031, the highest among all distribution channels, and reshaping the brand-building landscape for healthy snacks. Direct-to-consumer (DTC) challengers are now engaging health-conscious shoppers via e-commerce and direct subscription services, sidestepping the traditional slotting fees that once restricted physical shelf access. Subscription models, like Calbee's innovative Body Granola service, are proving particularly adept at fostering brand loyalty. Launched in Japan in April 2023 and making its way to Singapore by April 2026, Calbee's service not only offers granola but also pairs it with a gut microbiome testing subscription, already embraced by over 50,000 customers in Japan. This approach elevates a mere product purchase into a recurring health service, boasting impressive retention rates. Brands that adeptly navigate both the logistical and data facets of DTC are carving out competitive advantages that traditional channel strengths struggle to match.

Geography Analysis

In 2025, North America commanded a dominant 36.40% share of the global revenue, solidifying its top position in the healthy snacks market. The region's success is attributed to its well-established retail infrastructure, heightened consumer awareness regarding health and wellness, and a diverse clientele eager to experiment with reformulated snack offerings. The U.S. stands as the cornerstone of this market, boasting significant scale, a high density of product innovations, and a robust mix of both branded and private-label suppliers. Meanwhile, Canada is carving out a reputation as a burgeoning hub, particularly in plant-based, reduced-sugar, and high-fiber snack formats.

Europe, while holding the second spot in the healthy snacks arena, is distinguished by its rigorous scrutiny of labeling and health claims. As per the German Federation of Organic Food Producers (BÖLW), Germany led Europe in organic food sales in 2024, raking in EUR 17.09 billion, followed closely by France with EUR 12.2 billion. Spain is poised for the swiftest growth in Europe, driven by younger urban consumers gravitating towards health-focused snacks. South America, still in its nascent stages, sees Brazil and Argentina fueling demand, thanks to urbanization, a burgeoning middle class, and the adoption of modern retail formats.

Asia-Pacific is set to outpace all others, with a projected CAGR of 7.98% through 2031 in the healthy snacks market. This surge is bolstered by rising incomes, urban lifestyle shifts, and a pronounced tilt towards preventive nutrition. While China dominates as the largest value reservoir, India is rapidly gaining ground, especially as distribution hurdles diminish and healthier packaged choices become more accessible. India's momentum is further amplified by the visibility of initiatives like 'Eat Right' and the heightened promotion of millet-based foods. Japan stands as a seasoned hub for innovations in functional dairy and gut-health snacks, whereas Southeast Asia and Australia are championing the demand for natural and clean-label products. Though the Middle East and Africa represent the smallest segments in absolute terms, urban expansions in the UAE, Saudi Arabia, Nigeria, and Egypt are bolstering the retail landscape for healthy snack distributions.

Competitive Landscape

The healthy snacks market remains moderately fragmented, with no single company commanding a dominant share. Competition is intensifying as major food groups increasingly invest in protein, fiber, and cleaner labels, as well as snack formats that can double as meal substitutes. This shift is redefining competition, emphasizing portfolio quality, functional credibility, and rapid innovation over mere shelf presence. Consequently, the market witnesses heightened rivalry among global players, natural food specialists, and digitally-native challengers.

In 2025 and 2026, a notable trend emerged: portfolio repositioning via acquisitions. PepsiCo made headlines with its USD 1.2 billion acquisition of Siete Foods in January 2025 and followed up with a USD 1.95 billion deal for poppi in May 2025. Simultaneously, PepsiCo streamlined its focus by cutting nearly 20% of its U.S. snack SKUs, zeroing in on priority formats. Nestlé, in June 2026, fully acquired Yfood, a smart food brand boasting 2025 sales of EUR 150 million (USD 162 million), integrating it into its Nutrition division. Mars, in a significant move, announced a USD 35.9 billion acquisition of Kellanova in August 2024, bolstering its snacking portfolio with brands like RXBAR and NutriGrain. These strategic acquisitions underscore the market's allure, with major players keen to tap into the burgeoning demand for functional and meal-adjacent snacks.

Opportunities abound in areas like personalization, gut health, and targeted nutrition formats. Here, nimble smaller players often outpace their larger, diversified counterparts. Simply Good Foods, with its early brand ownership of high-protein snacking giants Quest and Atkins, underscores this trend, even as it braces for a gross margin dip of 300 to 350 basis points in fiscal 2026. Similarly, Lotus Bakeries showcases the power of focus: its brands BEAR, TREK, and nākd. under Lotus Natural Foods raked in EUR 300 million (USD 324 million) in branded revenue, constituting 25% of the group's total. The next competitive edge will likely stem from product personalization, enhanced ingredient intelligence, and adept utilization of digital shelf data. In this landscape, firms attuned to consumer behavior can fortify their market position, even without an expansive legacy distribution network.

Healthy Snacks Industry Leaders

Nestlé S.A.

PepsiCo, Inc.

Mondelēz International, Inc.

Kellanova

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Nestlé completed the full acquisition of Yfood, a Munich-based "smart food" brand generating approximately EUR 150 million (USD 162 million) in 2025 revenues at double-digit year-on-year growth. The deal brings Yfood into Nestlé's newly formed Nutrition division alongside Boost Nutritional Drinks, with international expansion beyond Europe and GLP-1-aligned positioning as the strategic rationale.

- March 2026: PepsiCo launched Doritos Protein (10 grams of protein per serving) and Smartfood FiberPop as headline products in a major strategy reset that includes cutting nearly 20% of US SKUs and closing 3 manufacturing plants, pivoting capital toward protein, fiber, and cleaner-label functional formats. The restructuring follows pressure from activist investor Elliott Investment Management, which had built approximately a USD 4 billion stake.

- February 2026: ondelēz International launched Perfect Snacks Protein + Prebiotics bars delivering 20 grams of protein and 6 grams of prebiotic fiber, including 3 grams of prebiotic fiber per serving, combining two of the most sought-after functional snacking claims in a single mainstream format. The launch builds on Mondelēz's strategy of strengthening its protein bar offerings across Perfect Bar, Builders, and Z Bar brands.

Global Healthy Snacks Market Report Scope

Healthy snacks are nutrient-dense, minimally processed foods consumed between meals to sustain energy, curb hunger, and provide essential vitamins and minerals. The global healthy snacks market is segmented by product type, category, distribution channel, and geography. By product type, the market is segmented into fruit, nuts, and seeds snacks, frozen and refrigerated snacks, bakery snacks, savory snacks, bars and confectionery snacks, dairy snacks, and other product types. By category, the market is segmented into conventional and organic/free-from. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Fruit, Nuts, and Seeds Snacks |

| Frozen and Refrigerated Snacks |

| Bakery Snacks |

| Savory Snacks |

| Bars and Confectionery Snacks |

| Dairy Snacks |

| Other Product Types |

| Conventional |

| Organic/Free-From |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Fruit, Nuts, and Seeds Snacks | |

| Frozen and Refrigerated Snacks | ||

| Bakery Snacks | ||

| Savory Snacks | ||

| Bars and Confectionery Snacks | ||

| Dairy Snacks | ||

| Other Product Types | ||

| Category | Conventional | |

| Organic/Free-From | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of healthy snacks by 2031?

The healthy snacks market is projected to reach USD 161.3 billion by 2031, up from USD 117.9 billion in 2026.

How fast are healthy snacks expected to grow through 2031?

The category is forecast to grow at a 6.5% CAGR during 2026-2031, supported by stronger demand for functional and nutrition-forward snacking.

Which product type leads revenue today?

Fruit, nuts, and seeds snacks led with a 33.71% revenue share in 2025, reflecting strong demand for simple and familiar better-for-you formats.

Which category is growing the fastest?

Organic and free-from products are expected to expand at an 8.11% CAGR through 2031, outpacing the broader category despite the larger size of conventional products.

Page last updated on: