Infectious Disease In Vitro Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.63 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

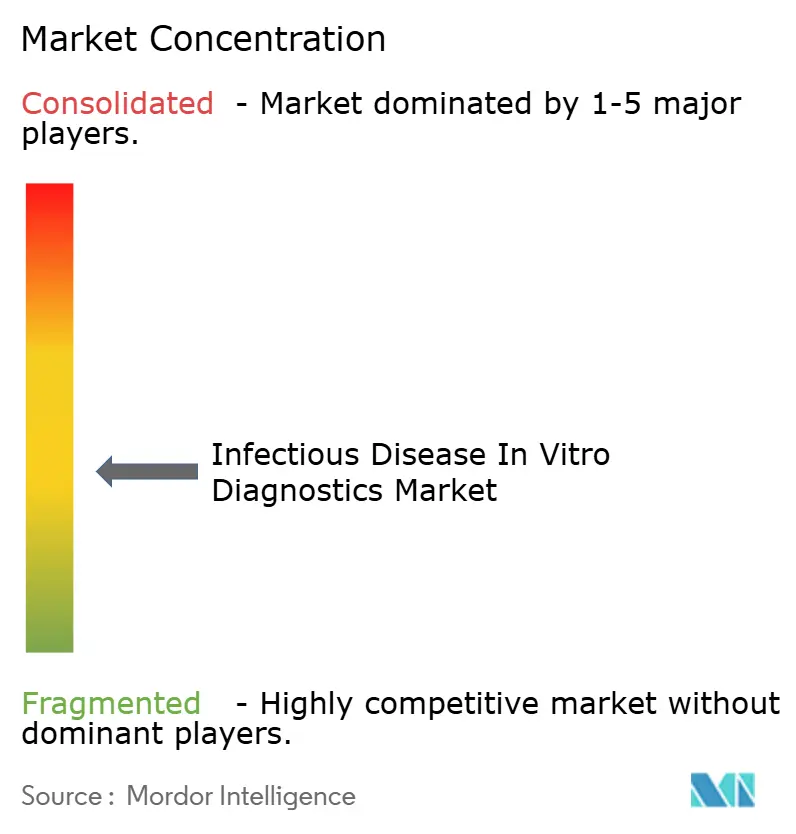

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infectious Disease In Vitro Diagnostics Market Analysis by Mordor Intelligence

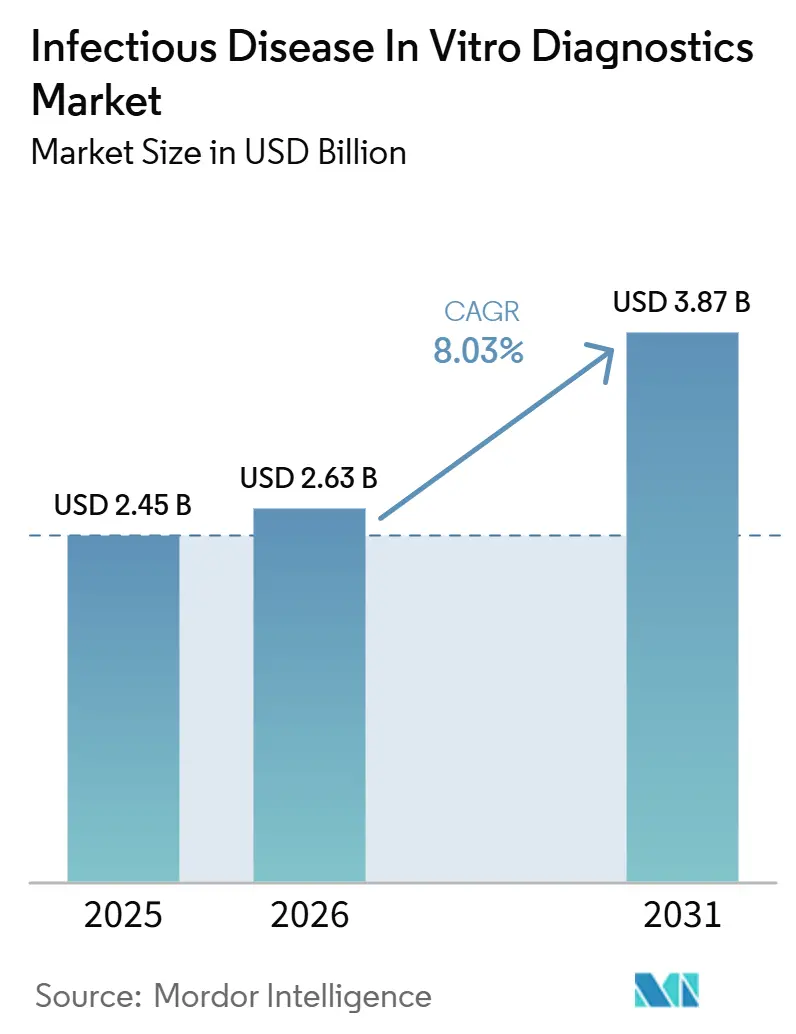

The Infectious Disease In Vitro Diagnostics Market size is projected to expand from USD 2.45 billion in 2025 and USD 2.63 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 8.03% between 2026 to 2031.

The infectious disease in vitro diagnostics market is moving on a more durable base of hospital demand and public health testing needs rather than the temporary surge pattern seen during pandemic-led screening cycles. Growth in the infectious disease in vitro diagnostics market is supported by the continued burden of respiratory and bloodstream infections, the wider use of multiplex molecular platforms, and the spread of decentralized testing networks across South Asia, Southeast Asia, and sub-Saharan Africa. The infectious disease in vitro diagnostics market is also benefiting from the closer link between routine testing and antimicrobial resistance surveillance, which is making infectious disease testing a repeat need in hospital workflows instead of a periodic purchase. Competitive positioning in the infectious disease in vitro diagnostics market continues to favor companies with large installed instrument bases, broad assay menus, and strong regulatory execution across major regions. The infectious disease in vitro diagnostics market still faces reimbursement and regulatory pressure, yet the shift toward automated workflows and near-patient access keeps the growth path credible through 2031.

Key Report Takeaways

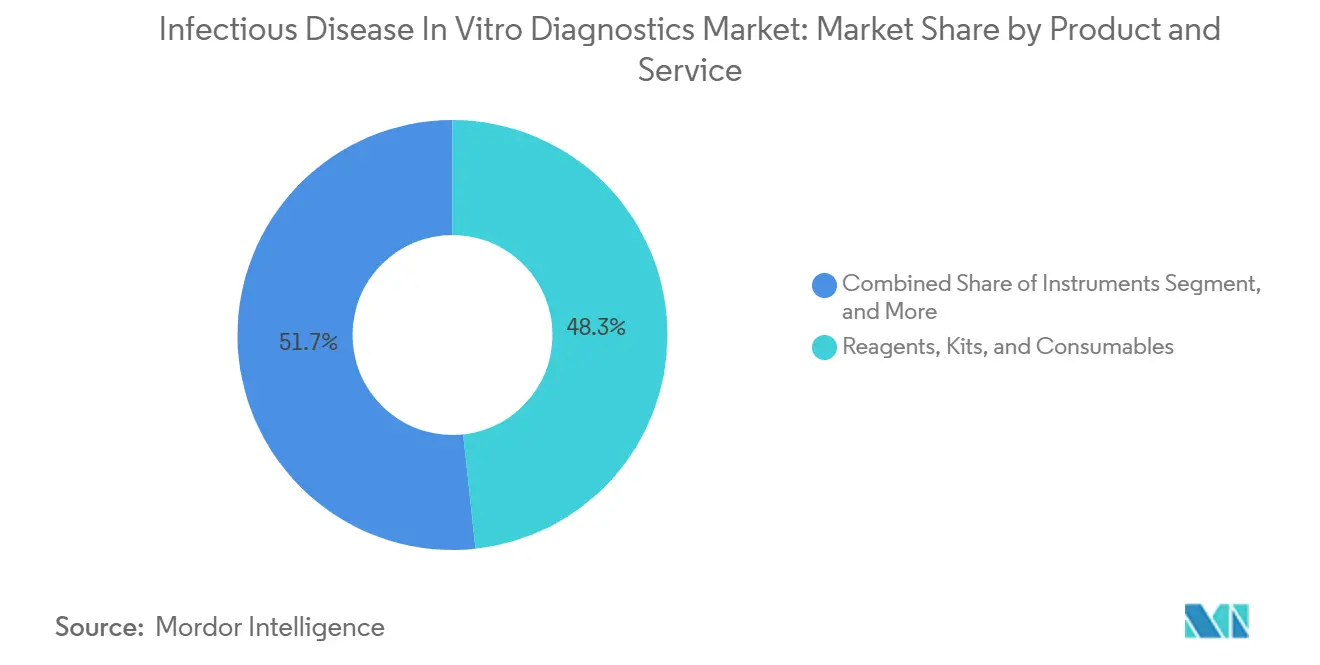

- By product and service, reagents, kits, and consumables held 48.31% of revenue in 2025, while software and services, the fastest-evolving category, are projected to grow at an 8.35% CAGR through 2031 within the infectious disease in vitro diagnostics market.

- By type of testing, laboratory testing held 61.68% of the infectious disease in vitro diagnostics market share in 2025, while point-of-care testing is projected to grow at a 9.73% CAGR through 2031.

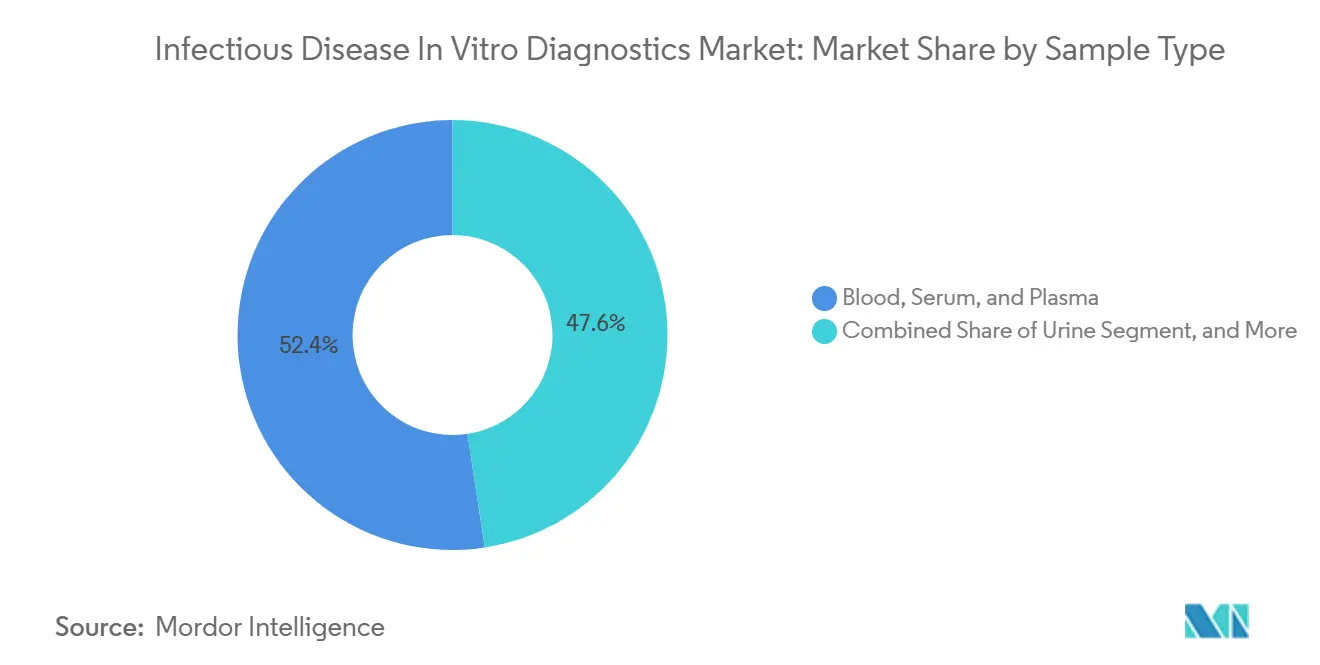

- By sample type, blood, serum, and plasma accounted for 52.42% share of the infectious disease in vitro diagnostics market size in 2025, while other sample types are forecast to expand at an 8.98% CAGR through 2031.

- By disease type, HIV represented 33.82% of revenue in 2025, while HPV is projected to grow at a 10.56% CAGR through 2031.

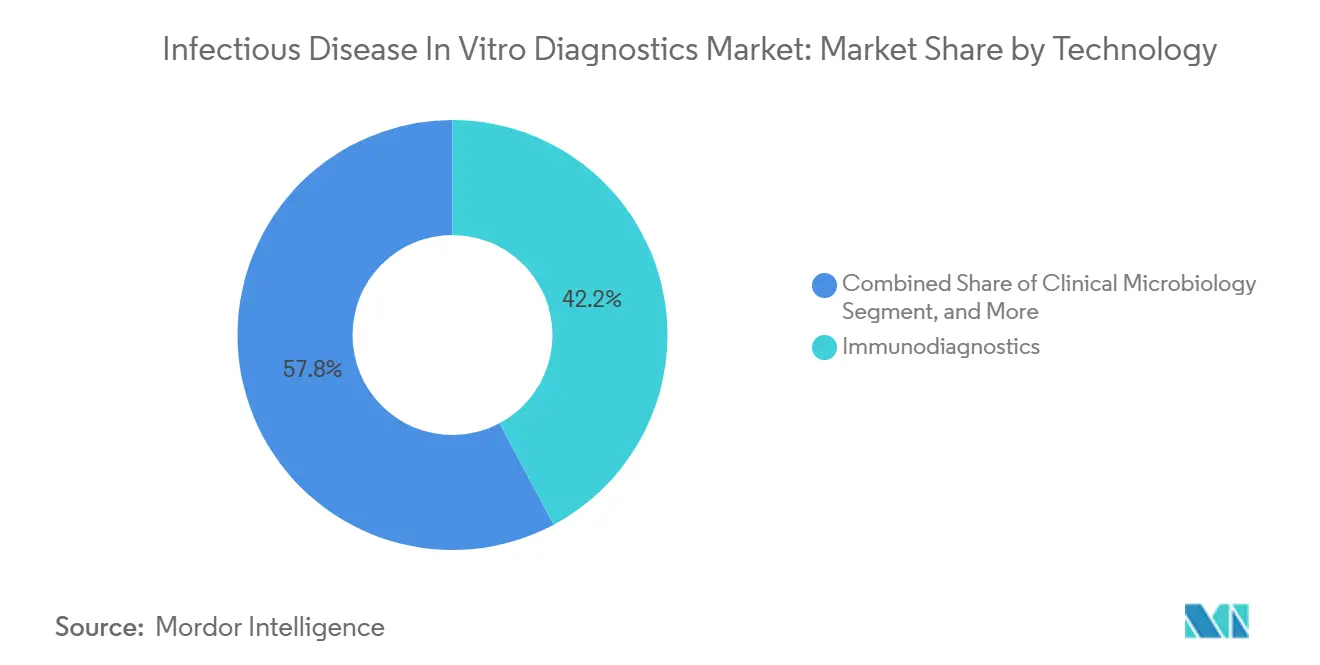

- By technology, immunodiagnostics captured 42.19% of revenue in 2025, while DNA sequencing and next-generation sequencing are expected to advance at an 8.24% CAGR through 2031.

- By clinical application, diagnostics held 86.83% of revenue in 2025, while screening is forecast to grow at a 9.29% CAGR through 2031.

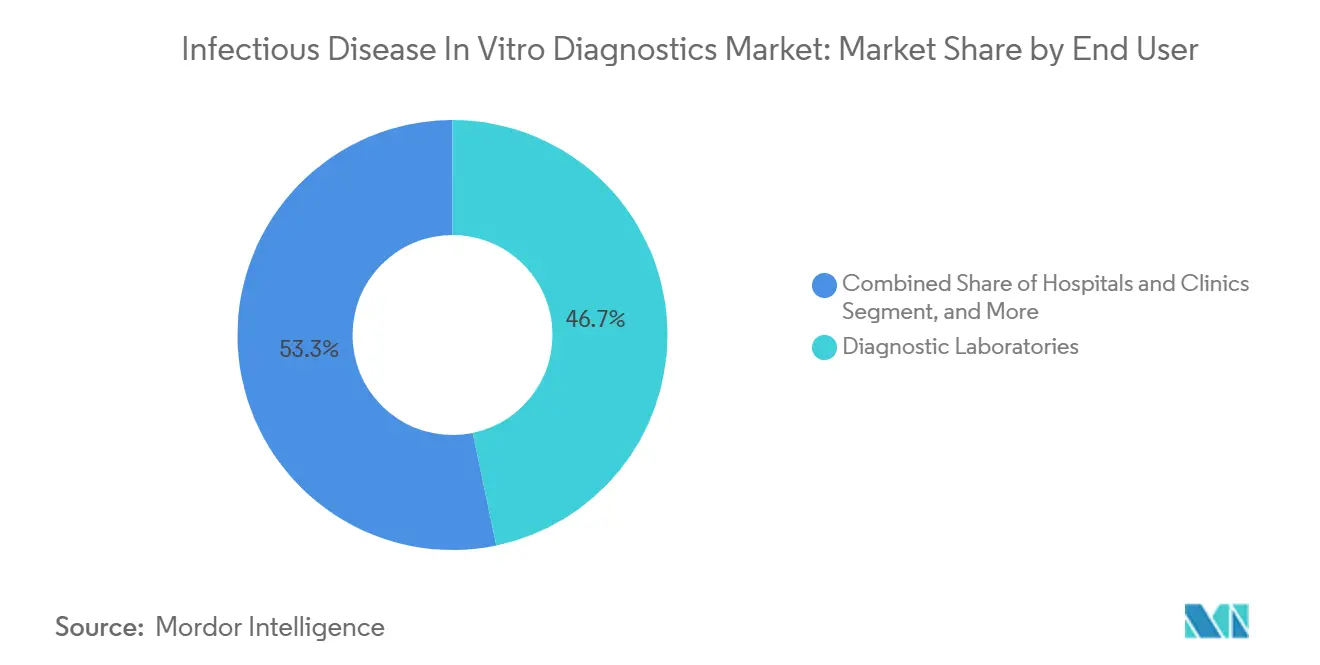

- By end user, diagnostic laboratories accounted for 46.74% of revenue in 2025, while academic and research institutions are projected to expand at an 8.04% CAGR through 2031.

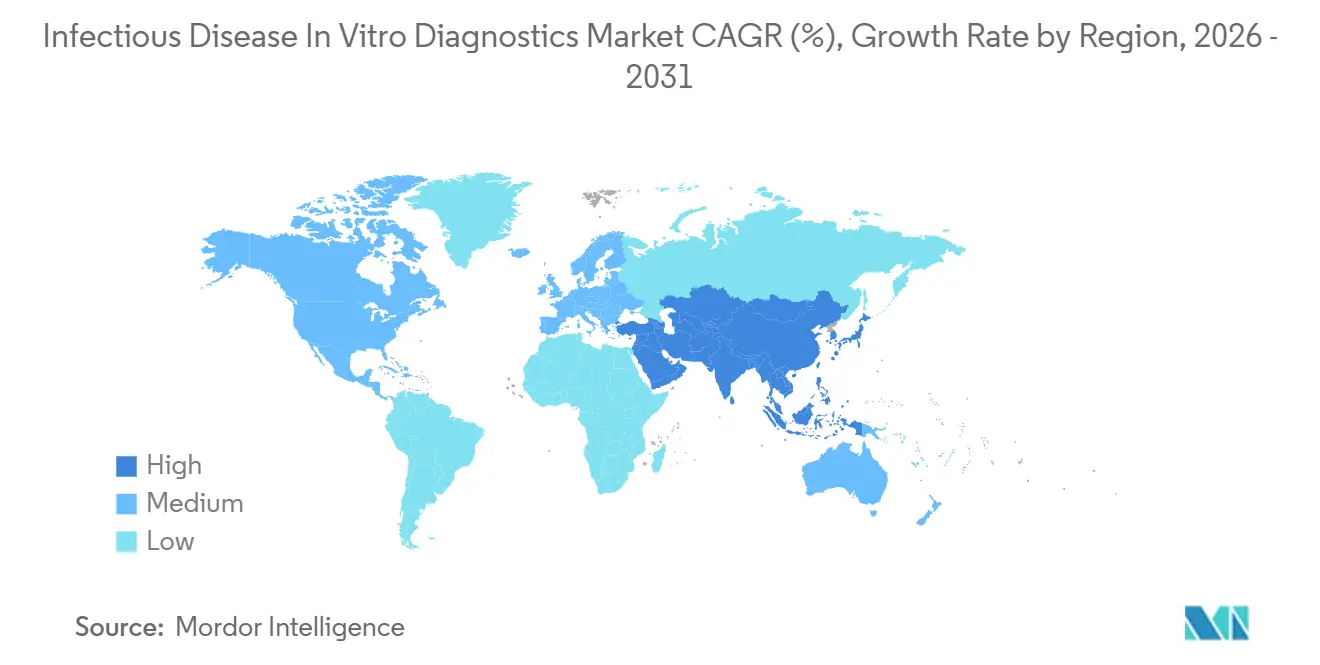

- By geography, North America held 40.86% of the infectious disease in vitro diagnostics market share in 2025, while Asia-Pacific is projected to record the highest regional CAGR at 9.58% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Infectious Disease In Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Respiratory and Bloodstream Infections | +2.0% | Global, concentrated in South and Southeast Asia, sub-Saharan Africa | Long term (≥ 4 years) |

| Shift Toward Syndromic Multiplex Testing Platforms | +1.5% | North America and Europe, with spillover to East Asia and GCC | Medium term (2-4 years) |

| Expansion of Decentralized and Point-of-Care Testing Networks | +1.2% | Asia-Pacific core, with spillover to Middle East and Africa and South America | Medium term (2-4 years) |

| Rising Adoption of Automated Molecular and Immunoassay Workflows | +0.8% | North America, Germany, Japan, China | Short term (≤ 2 years) |

| Integration of AI-Enabled Interpretation and Workflow Software | +0.4% | North America and EU, with early pilots in GCC and Singapore | Long term (≥ 4 years) |

| Increased Hospital Preparedness for Outbreak Surveillance and AMR Monitoring | +0.5% | Global, with early gains in EU, United States, and upper-middle-income Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Respiratory and Bloodstream Infections

The infectious disease in vitro diagnostics market continues to draw its strongest base demand from the persistence of respiratory, bloodstream, urinary, and gastrointestinal infections across both hospital and community settings. The WHO GLASS 2025 report analyzed more than 23 million bacteriologically confirmed cases reported by 110 countries from 2016 through 2023, and it showed that drug-resistant pathogen proportions were stable or rising across several major infection categories. This pattern matters for the infectious disease in vitro diagnostics market because high-confirmation settings are concentrated in countries with better laboratory infrastructure, while regions with heavier disease burden still remain underdiagnosed. That gap keeps demand tied not only to immediate test volumes but also to future laboratory build-out across South Asia, sub-Saharan Africa, and parts of Latin America. Hospital-acquired infections add a second layer of demand because bloodstream infections require rapid organism identification and earlier antimicrobial selection to guide the first 48 hours of treatment. The infectious disease in vitro diagnostics market, therefore, benefits from both higher infection incidence and a widening clinical need for faster and more reliable laboratory decision support.

Shift Toward Syndromic Multiplex Testing Platforms

The infectious disease in vitro diagnostics market is seeing a clear shift toward syndromic multiplex testing as hospitals try to combine faster diagnosis with tighter use of staff and instrument time. QIAGEN received FDA clearance in March 2026 for gastrointestinal panels on the QIAstat-Dx Rise system, and the broader QIAstat-Dx platform had more than 5,200 instruments installed across over 100 countries. That installed base matters because a platform that supports respiratory, gastrointestinal, and emerging pathogen panels allows hospitals to consolidate menu purchases and commit to repeat reagent spending over multi-year periods. bioMérieux received IVDR CE marking in March 2026 for its BIOFIRE SPOTFIRE R/STplus Panel, which can detect 15 pathogens in 15 minutes at the point of care.[1]bioMérieux, “bioMérieux Receives IVDR CE-Marking for Two BIOFIRE SPOTFIRE Panels to Strengthen Near-Patient Respiratory and Sore Throat Diagnostics Across Europe,” bioMérieux Press Release, biomerieux.com Faster multiplex testing also supports antibiotic stewardship because clinicians can reduce broad empirical prescribing when pathogen identification arrives earlier in the care cycle. The infectious disease in vitro diagnostics market is therefore gaining from a buying logic that now links these platforms to cost control, throughput, and treatment quality rather than to test menu expansion alone.

Expansion of Decentralized and Point-of-Care Testing Networks

The infectious disease in vitro diagnostics market is expanding beyond hospital core laboratories as more testing moves closer to patients in clinics, outreach settings, and lower-complexity care environments. Co-Diagnostics signed distribution agreements in March 2026 covering Bangladesh, Pakistan, Nepal, and Sri Lanka for its PCR Pro point-of-care instrument and SARAGENE assay line.[2]Co-Diagnostics, “Co-Diagnostics Signs Agreement to Significantly Expand Commercial and Distribution Territory Across South Asia,” Co-Diagnostics IR, ir.co-dx.com That move reflects a broader effort to close the gap between centralized molecular capacity and settings that previously depended on simple strip-based screening tools. WHO guidance issued in March 2026 supported near-point-of-care molecular diagnostics and tongue swabs for tuberculosis detection in patients unable to produce sputum, which directly improves access in settings where traditional specimen collection has limited testing reach. The decentralized shift also changes the competitive logic of the infectious disease in vitro diagnostics market because suppliers now need compact systems, simpler workflows, and distribution models that fit regional health systems. As that transition continues, testing demand is likely to become less concentrated in major urban hospitals and more evenly distributed across district and outpatient care channels.

Rising Adoption of Automated Molecular and Immunoassay Workflows

The infectious disease in vitro diagnostics market is also being supported by stronger adoption of automated workflows that reduce operator burden and improve consistency across laboratories. Roche received FDA 510(k) clearance in August 2025 for the cobas Respiratory 4-flex assay, the first diagnostic assay to use its TAGS multiplex PCR technology.[3]Roche Diagnostics, “Roche's First Respiratory Test Powered by TAGS Technology Receives FDA Clearance for SARS-CoV-2, Influenza A, Influenza B and RSV,” Roche Diagnostics, diagnostics.roche.com DiaSorin then received both FDA 510(k) clearance and a CLIA waiver in December 2025 for the LIAISON NES 4-plex respiratory panel, which widened its use into lower-complexity care settings. Hologic added to this pattern in October 2025 when Panther Fusion gastrointestinal bacterial assays received both FDA clearance and IVDR CE marking for use in the United States and Europe. Automation matters because it shortens turnaround times, reduces manual variation, and allows infectious disease in vitro diagnostics market participants to sell into sites that cannot support highly specialized laboratory staffing. The result is a broader addressable base for molecular and immunoassay platforms without requiring each care site to build a full high-complexity laboratory structure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Molecular Platforms and Assay Consumables | -1.2% | Global, pronounced in South Asia, Middle East and Africa, and Latin America | Long term (≥ 4 years) |

| Stringent Regulatory Review and Local Validation Requirements | -0.6% | EU under IVDR, United States under FDA 510(k), Brazil under ANVISA, India under CDSCO | Medium term (2-4 years) |

| Reimbursement Pressure on Non-Urgent and Low-Volume Testing | -0.5% | North America, with secondary effects in Western Europe | Short term (≤ 2 years) |

| Skilled Labor Shortages for Complex Diagnostics and Data Interpretation | -0.4% | Global, most acute in rural Asia-Pacific and sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Molecular Platforms and Assay Consumables

The infectious disease in vitro diagnostics market still faces a major access barrier from the cost of molecular systems and the consumables needed to run them. Multiplex syndromic panels often cost 5 to 10 times more per test than single-target lateral flow formats, which keeps many primary care and community settings in lower-income regions outside the practical buyer pool. A 2026 study indexed on ScienceDirect described a portable microfluidic nucleic acid amplification system with sample-to-answer results in under 30 minutes at a per-test cost of USD 1.5. That contrast shows how far much of the infectious disease in vitro diagnostics market still is from price points that can scale across high-burden low-resource settings. When hospitals cannot afford broad panel testing, they often substitute cheaper single-target methods that can miss co-infections and weaken treatment choice. Reagent rental and volume-linked pricing help at the margin, but they have not yet solved the affordability gap that limits wider market penetration.

Stringent Regulatory Review and Local Validation Requirements

The infectious disease in vitro diagnostics market also faces slower commercialization, where regulatory pathways are becoming more demanding across multiple regions. The EU IVDR framework expanded clinical evidence and post-market follow-up expectations for assays that had previously entered the market under less burdensome rules. In the United States, CMS updated MolDX billing and coding guidance effective April 2026, tightening ICD-10 documentation requirements for infectious disease syndromic panel reimbursement claims. India and Brazil add their own local validation steps, which lengthen launch timelines and place smaller innovators at a disadvantage against manufacturers with larger regulatory teams. This favors companies that can manage parallel submissions, quality documentation, and clinical evidence generation without slowing product rollout in major markets. The infectious disease in vitro diagnostics market, therefore, grows under a structure where compliance capability itself has become a competitive asset.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product and Service: Consumables support recurring revenue and platform retention

Reagents, kits, and consumables held 48.31% of revenue in 2025, which made them the largest product category in the infectious disease in vitro diagnostics market. Their position reflects a business model in which instruments are frequently placed under subsidized terms while long-term consumable purchasing drives the revenue stream. Once a laboratory validates a cartridge or reagent format, the switching burden becomes high because revalidation, retraining, and contract changes all raise replacement costs. That dynamic gives the infectious disease in vitro diagnostics market a stable, recurring layer that is less volatile than one-time capital equipment purchases. Instruments remained the second major category and covered high-throughput immunoanalyzers, PCR systems, MALDI-TOF platforms, and automated sample processors. These systems still shape laboratory buying decisions because installed hardware determines which menus and workflow formats a site can support over time.

Software and services are projected to grow at a 8.35% CAGR through 2031, but they moved into a more strategic role within the infectious disease in vitro diagnostics market as a result of connectivity and surveillance integration becoming more important. Laboratories are increasingly valuing LIS connectivity modules, antimicrobial resistance data links, and interpretation support services as part of broader contracts instead of stand-alone purchases. This shift gives large suppliers another way to deepen account retention after the initial instrument sale. It also strengthens the position of companies that can offer a multi-layer package of hardware, assays, and workflow software instead of a single test format. Within the infectious disease in vitro diagnostics industry, suppliers that pair menu breadth with service integration are better placed to defend margins when instrument pricing becomes more competitive. Quality system demands under ISO 13485 and FDA manufacturing rules also reinforce the advantage of established suppliers that can absorb compliance costs without disrupting supply continuity.

By Type of Testing: Point-of-care formats narrow the gap with centralized labs

Laboratory testing accounted for 61.68% of revenue in 2025, which kept centralized laboratories at the core of the infectious disease in vitro diagnostics market. High-complexity workups such as HIV viral load monitoring, hepatitis C genotyping, tuberculosis resistance profiling, and STI confirmation still rely heavily on hospital core labs and independent reference facilities. These settings retain an advantage because they operate with validated quality controls, specialist staff, and deep information system integration. At the same time, point-of-care testing is projected to grow at a 9.73% CAGR through 2031, making it the fastest-growing testing type in the infectious disease in vitro diagnostics market. The demand shift is less about replacing central labs and more about moving selected use cases into faster and more accessible care settings.

A 2025 article in Diagnostics described AI-enhanced point-of-care systems that reduced time-to-result from 15 minutes to as little as 2 minutes in prototype settings. WHO support for near-point-of-care tuberculosis molecular diagnostics in 2026 further widened the case for decentralized testing in endemic regions. DiaSorin's CLIA-waived LIAISON NES platform also showed how regulatory progress can move molecular testing into urgent care clinics and physician offices that do not operate under high-complexity laboratory structures. These changes improve speed and convenience, but they do not remove the role of central laboratories for confirmatory and high-volume testing. Within the infectious disease in vitro diagnostics market, the strongest suppliers are those that can serve both near-patient and centralized settings with connected menu strategies. This also reduces the risk that point-of-care growth simply cannibalizes laboratory revenue rather than expanding the total testing base.

By Sample Type: Blood stays central while alternative specimens expand access

Blood, serum, and plasma represented 52.42% of revenue in 2025, which kept this sample group at the center of the infectious disease in vitro diagnostics market size. The category remains strong because bloodstream infection diagnosis, HIV monitoring, hepatitis serology, and syphilis screening are deeply embedded in blood-based clinical pathways. Many of these tests also sit inside mandatory antenatal, transfusion, and pre-procedure screening frameworks, which makes demand less sensitive to short-term budget changes. Urine remained the second meaningful sample type because it supports urinary tract infection diagnosis, STI confirmation, and newer tuberculosis detection approaches. This sample mix shows that the infectious disease in vitro diagnostics market still depends on specimen types that fit established clinical practice and standardized processing routes.

Other sample types are projected to grow at a 8.98% CAGR through 2031, making them the fastest-expanding category in the infectious disease in vitro diagnostics market. WHO guidance on HPV DNA genotyping endorsed self-collected cervical samples and home collection in appropriate screening pathways, which expands testing outside the clinic visit model. bioMérieux also validated its BIOFIRE SPOTFIRE R/STplus panels for nasopharyngeal, throat, and anterior nasal swabs, which improves access in near-patient respiratory testing. Flexible sampling helps widen utilization because it aligns better with self-collection, outpatient use, and low-infrastructure testing workflows. It also allows suppliers in the infectious disease in vitro diagnostics market to target screening programs and community channels that are less dependent on phlebotomy and hospital-based specimen handling. Over time, broader specimen acceptance should support both access and repeat testing frequency in selected disease areas.

By Disease Type: HIV anchors scale while HPV drives the next growth phase

HIV held 33.82% of revenue in 2025, which made it the largest disease segment in the infectious disease in vitro diagnostics market. That scale reflects long-established screening programs, large public procurement volumes, and recurring needs across viral load monitoring, infant diagnosis, and resistance testing. The HIV segment is structurally resilient because testing is embedded in blood safety, antenatal care, and national public health systems across many regions. It also benefits from a procurement base that is broader and more institutionalized than many other infectious disease categories. This volume foundation gives the infectious disease in vitro diagnostics market a dependable revenue base even when other categories move with seasonal or outbreak cycles.

HPV is projected to grow at a 10.56% CAGR through 2031, making it the fastest-growing disease category in the infectious disease in vitro diagnostics market. WHO cervical cancer elimination goals have created sustained demand for high-performance screening tests across more than 100 countries. BD received WHO prequalification in late 2025 for the Onclarity HPV Assay, which supports the detection of 14 high-risk HPV types and genotype-specific risk stratification. Tuberculosis, hospital-acquired infections, mosquito-borne diseases, and STI categories also continue to add volume through surveillance programs, sexual health service expansion, and regional outbreak pressure. Influenza has retained a durable testing layer in near-patient settings even though seasonal spikes still shape short-term volumes. The infectious disease in vitro diagnostics market, therefore, combines a mature HIV base with a newer screening-led HPV growth path that is expanding demand beyond acute diagnosis alone.

By Technology: Immunodiagnostics anchors throughput while sequencing expands the frontier

Immunodiagnostics commanded 42.19% of revenue in 2025, which gave it the leading technology position in the infectious disease in vitro diagnostics market. Its strength rests on throughput, cost efficiency, and long clinical use across hepatitis serology, HIV combination testing, and syphilis assays. CLIA and ELISA formats still fit the needs of high-volume laboratories because they pair predictable workflows with established accreditation and quality control procedures. PCR remained the next major technology because it is central to STI confirmation, respiratory pathogen identification, and tuberculosis resistance profiling. Clinical microbiology also kept a meaningful role because culture and MALDI-TOF workflows continue to support bacteriology and antimicrobial stewardship programs.

DNA sequencing and next-generation sequencing are projected to grow at an 8.24% CAGR through 2031, making them the fastest-growing technology category in the infectious disease in vitro diagnostics market. A 2025 hospital-based study available through PMC found that pathogen-targeted NGS achieved a 90.9% detection rate in lower respiratory tract infections compared with 52.5% for conventional testing, while also reducing median hospital stay from 38 days to 23 days. bioMérieux strengthened this area with its 2025 acquisition of Day Zero Diagnostics, which added genome sequencing and machine learning capabilities for antimicrobial resistance detection. WHO also identified sequencing-based antimicrobial susceptibility testing as a priority area in its AMR diagnostic initiative. That institutional backing matters because sequencing still carries cost and workflow complexity that limit broad routine use. In the infectious disease in vitro diagnostics market, adoption is likely to widen first in high-acuity hospitals and public health laboratories where better sensitivity and resistance insight justify the added burden.

By Clinical Application: Diagnostics dominate today while screening expands faster

Diagnostics accounted for 86.83% of revenue in 2025, which kept symptomatic testing as the main application in the infectious disease in vitro diagnostics market. This reflects the fact that most current volume still begins when patients present with fever, respiratory symptoms, urinary complaints, or suspected bacteremia. Clinical indication remains a strong driver because reimbursement systems and hospital protocols still prioritize testing tied to active care decisions. That gives acute diagnostic use a durable volume base across both centralized and automated laboratory settings. The large share also means the infectious disease in vitro diagnostics market continues to depend heavily on healthcare utilization and disease presentation patterns rather than on broad population outreach alone.

Screening is projected to grow at a 9.29% CAGR through 2031, making it the fastest-growing application in the infectious disease in vitro diagnostics market. WHO-aligned programs in HPV, STI, hepatitis, HIV, and tuberculosis are supporting this shift by making regular testing part of population health management rather than episodic diagnosis. A 2026 article in the Journal of Translational Medicine also highlighted how software and immunoprofiling pathways may strengthen multi-infection diagnosis and treatment personalization in clinical use. Screening demand is structurally attractive because it is often linked to public programs, antenatal pathways, blood safety requirements, and preventive care initiatives. Those channels are usually less exposed to the reimbursement swings that affect low-volume or non-urgent acute diagnostics. As screening grows, the infectious disease in vitro diagnostics market should see a broader mix of volumes across community, self-collection, and organized public health channels.

By End User: Diagnostic laboratories lead current volumes while research settings accelerate adoption

Diagnostic laboratories held 46.74% of revenue in 2025, which kept them as the leading end-user group in the infectious disease in vitro diagnostics market. Their role is anchored in high-complexity molecular testing, public health surveillance support, and specialist interpretation that many care sites cannot handle internally. Independent laboratory chains in several emerging markets are also consolidating capacity and using automation to lower per-test economics. Hospitals and clinics remained the second major end-user group because they need in-house support for microbiology, immunology, blood cultures, and respiratory molecular panels. This mix shows that the infectious disease in vitro diagnostics market still depends on centralized expertise even as testing access expands outward.

Academic and research institutions are projected to grow at an 8.04% CAGR through 2031, making them the fastest-growing end-user group in the infectious disease in vitro diagnostics market. The CDC Next-Generation Sequencing Quality Initiative launched in 2025 to address quality and regulatory challenges that have limited broader sequencing adoption in clinical and public health laboratories. Research settings matter because they serve as the early testing ground for newer workflows in pathogen genomics, outbreak surveillance, and antimicrobial resistance mapping. Their uptake then shapes translational movement into routine hospital and public health use. Other end users, including blood banks and home-testing channels, are also expanding as self-testing and decentralized screening gain wider regulatory acceptance. In the infectious disease in vitro diagnostics industry, the growth of research-driven end users supports future menu development and expands the evidence base needed for wider commercial adoption.

Geography Analysis

North America held 40.86% of revenue in 2025, which made it the largest regional segment in the infectious disease in vitro diagnostics market. The region benefits from deep reimbursement coverage, a large installed base of automated molecular systems, and hospital structures that can absorb complex testing workflows. CMS updated the Clinical Laboratory Fee Schedule under the Consolidated Appropriations Act of 2026, delaying payment reductions through the end of 2026 and capping annual cuts at 15% starting in 2027. That policy gives laboratories near-term visibility even though future reimbursement pressure remains part of the operating outlook. CMS MolDX guidance effective April 2026 also tightened ICD-10 documentation requirements for syndromic respiratory and gastrointestinal panel claims. This favors suppliers that can support strong clinical evidence and coding discipline across customer accounts. Canada and Mexico remain smaller in value terms, but both continue to build demand through HIV, tuberculosis, and HPV testing pathways that align with broader regional public health priorities.

Europe remained the second-largest region in the infectious disease in vitro diagnostics market and continued to rely heavily on centralized hospital laboratory networks. Germany, the United Kingdom, France, Italy, and Spain anchor most of the region's structured testing volume through established hospital procurement systems and broad clinical adoption of molecular and immunoassay menus. IVDR remains the single strongest policy force shaping commercialization in the region because it raises the burden of evidence and re-registration across assay portfolios. bioMérieux's March 2026 CE marking for BIOFIRE SPOTFIRE respiratory and sore throat panels showed how companies with scale are moving to preserve and extend their menu positions under the new framework.

Asia-Pacific is projected to grow at a 9.58% CAGR through 2031, making it the fastest-growing regional segment in the infectious disease in vitro diagnostics market. The region combines a high infectious disease burden with expanding laboratory infrastructure and maturing regulatory pathways for localized diagnostics. India recorded 26.2 lakh tuberculosis cases in 2024, which keeps demand strong for molecular TB testing, drug resistance profiling, and near-patient workflows aligned with 2026 WHO guidance. China also remains important because infectious disease testing accounted for 41.8% of the country's IVD revenue in 2025, supported by mandatory screening for HIV, hepatitis B and C, syphilis, and tuberculosis in several care pathways. Government-supported tender programs and hospital digitization are helping the shift from manual methods to automated platforms in Tier-2 and Tier-3 city hospitals. The Middle East and Africa remain split between high-throughput investment in GCC states and donor-backed testing networks across sub-Saharan Africa. South America continues to gain from STI, dengue, and hepatitis screening expansion, although procurement fragmentation and currency volatility still moderate capital investment speed.

Competitive Landscape

The infectious disease in vitro diagnostics market remains moderately concentrated, with Roche, Abbott, Danaher, through Cepheid and Beckman Colter, bioMérieux, Siemens Healthineers, and QIAGEN holding strong positions through installed instrument bases and proprietary consumable ecosystems. Scale matters in the infectious disease in vitro diagnostics market because hospitals often prefer suppliers that can support multiple testing modalities, maintain regulatory continuity, and secure long-term service coverage. This has created a competitive pattern in which menu breadth and account retention are as important as single assay innovation. It has also raised the value of platforms that can bridge centralized laboratories, urgent care sites, and public health settings through connected workflows. Mid-tier players such as Seegene, SD Biosensor, and Molbio Diagnostics still matter because they remain active in price-sensitive and decentralized channels where flexibility and lower entry costs are important.

bioMérieux showed a two-track strategy in 2025 by acquiring SpinChip Diagnostics in January for near-patient immunoassay capability and Day Zero Diagnostics in June for sequencing and machine learning support in antimicrobial resistance detection. QIAGEN reinforced a different path through regulatory execution, with 9 FDA clearances in 24 months for the QIAstat-Dx family and more than 5,200 installed instruments across over 100 countries. These moves show that the infectious disease in vitro diagnostics market rewards both acquisition-led capability building and disciplined rollout of platform families across multiple regions. They also reinforce the recurring revenue logic that comes from broad installed bases and menu expansion on existing systems.

Structural portfolio changes have also affected competitive positioning in the infectious disease in vitro diagnostics market. BD completed the separation and combination of its Biosciences and Diagnostic Solutions business with Waters Corporation in February 2026, which reduced its direct presence in core clinical diagnostics. Abbott completed its Exact Sciences acquisition in March 2026, which is likely to direct more diagnostic attention toward cancer screening and may soften its infectious disease innovation intensity at the margin. White-space areas remain visible in low-cost multiplex point-of-care systems, AI-assisted interpretation support, and sequencing-based AMR products that can reach reimbursement acceptance. WHO prequalification and ISO 13485 compliance continue to raise the entry bar in public procurement channels, which supports incumbent advantage and reduces disruption from lightly resourced entrants. The infectious disease in vitro diagnostics market, therefore, remains open to innovation, but commercial success still depends heavily on regulatory depth, manufacturing reliability, and the ability to convert technical capability into repeat institutional buying.

Infectious Disease In Vitro Diagnostics Industry Leaders

Abbott Laboratories

bioMérieux SA

Danaher Corporation

F. Hoffmann-La Roche Ltd.

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: QIAGEN received FDA clearance for QIAstat-Dx Gastrointestinal Panels on the QIAstat-Dx Rise system, its 9th U.S. clearance in 24 months; the QIAstat-Dx Rise processes up to 160 tests per day and consolidates respiratory and GI syndromic testing on a single automated platform now deployed across 100+ countries with over 5,200 instruments placed globally.

- March 2026: Co-Diagnostics signed distribution agreements to expand its PCR Pro POC instrument and SARAGENE assay line across South Asia, Bangladesh, Pakistan, Nepal, and Sri Lanka, targeting a total addressable market estimated at USD 13 billion and advancing the commercialization of its CDSCO-licensed PCR Pro instrument in India.

- March 2026: Abbott completed its acquisition of Exact Sciences for approximately USD 21 billion in equity value, establishing Abbott as a leader in cancer screening diagnostics; while focused on oncology, the transaction is expected to reallocate a material share of Abbott Diagnostics' R&D pipeline toward molecular oncology in the near term.

- March 2026: bioMérieux received IVDR CE marking for its BIOFIRE SPOTFIRE R/STplus Panel and R/STplus Panel Mini, enabling simultaneous multiplex PCR detection of 15 and 6 respiratory and sore throat pathogens, respectively, at the point of care in CE-recognizing European countries from Q2 2026.

Global Infectious Disease In Vitro Diagnostics Market Report Scope

The Infectious Disease In Vitro Diagnostics (IVD) Market is defined as the global industry for laboratory-based tests performed on patient samples (such as blood, urine, or swabs) to detect, identify, and monitor infectious pathogens including bacteria, viruses, fungi, and parasites. These diagnostics enable accurate and timely diagnosis, guide treatment decisions, and support disease surveillance and infection control.

The Infectious Disease In Vitro Diagnostics (IVD) Market is segmented by product and service, type of testing, sample type, disease type, technology, clinical application, end user, and geography. By product and service, it includes Reagents, Kits, and Consumables, Instruments, and Software and Services. By type of testing, the market is divided into Laboratory Testing and Point-of-Care Testing. By sample type, it covers Blood, Serum, and Plasma, Urine, and Other Sample Types. By disease type, the market includes Hepatitis, HIV, Hospital-Acquired Infections, Mosquito-Borne Diseases, HPV, Chlamydia trachomatis, Neisseria gonorrhea, Tuberculosis, Influenza, Syphilis, and Other Infectious Diseases. By technology, it spans Immunodiagnostics, Clinical Microbiology, Polymerase Chain Reaction, Isothermal Nucleic Acid Amplification Technology, DNA Sequencing and Next-Generation Sequencing, DNA Microarray, and Other Technologies. By clinical application, the market is segmented into Diagnostics and Screening. By end user, it includes Diagnostic Laboratories, Hospitals and Clinics, Academic and Research Institutions, and Other End Users.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America).

| Reagents, Kits, and Consumables |

| Instruments |

| Software and Services |

| Laboratory Testing |

| Point-of-Care Testing |

| Blood, Serum, and Plasma |

| Urine |

| Other Sample Types |

| Hepatitis |

| HIV |

| Hospital-Acquired Infections |

| Mosquito-Borne Diseases |

| HPV |

| Chlamydia trachomatis |

| Neisseria gonorrhea |

| Tuberculosis |

| Influenza |

| Syphilis |

| Other Infectious Diseases |

| Immunodiagnostics |

| Clinical Microbiology |

| Polymerase Chain Reaction |

| Isothermal Nucleic Acid Amplification Technology |

| DNA Sequencing and Next-Generation Sequencing |

| DNA Microarray |

| Other Technologies |

| Diagnostics |

| Screening |

| Diagnostic Laboratories |

| Hospitals and Clinics |

| Academic and Research Institutions |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product and Service | Reagents, Kits, and Consumables | |

| Instruments | ||

| Software and Services | ||

| By Type of Testing | Laboratory Testing | |

| Point-of-Care Testing | ||

| By Sample Type | Blood, Serum, and Plasma | |

| Urine | ||

| Other Sample Types | ||

| By Disease Type | Hepatitis | |

| HIV | ||

| Hospital-Acquired Infections | ||

| Mosquito-Borne Diseases | ||

| HPV | ||

| Chlamydia trachomatis | ||

| Neisseria gonorrhea | ||

| Tuberculosis | ||

| Influenza | ||

| Syphilis | ||

| Other Infectious Diseases | ||

| By Technology | Immunodiagnostics | |

| Clinical Microbiology | ||

| Polymerase Chain Reaction | ||

| Isothermal Nucleic Acid Amplification Technology | ||

| DNA Sequencing and Next-Generation Sequencing | ||

| DNA Microarray | ||

| Other Technologies | ||

| By Clinical Application | Diagnostics | |

| Screening | ||

| By End User | Diagnostic Laboratories | |

| Hospitals and Clinics | ||

| Academic and Research Institutions | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for infectious disease in vitro diagnostics?

The market is expected to reach USD 3.87 billion by 2031 from USD 2.63 billion in 2026, with a 8.03% CAGR over 2026-2031.

Which region leads current revenue generation?

North America led with 40.86% share in 2025 because of broad reimbursement coverage, dense automated instrument placement, and strong clinical laboratory infrastructure.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at a 9.58% CAGR through 2031, supported by high disease burden, expanding laboratory investment, and localized diagnostics pathways.

Which testing model is gaining momentum the fastest?

Point-of-care testing is the fastest-growing testing type with a 9.73% CAGR, helped by near-patient molecular platforms and simpler deployment in lower-complexity settings.

Which disease area is expanding the most quickly?

HPV is the fastest-growing disease segment at a 10.56% CAGR through 2031, driven by WHO-aligned cervical cancer screening programs and wider use of molecular primary screening.

Which technology area offers the clearest long-term growth opportunity?

DNA sequencing and next-generation sequencing are growing at an 8.24% CAGR because they improve pathogen detection and support antimicrobial resistance monitoring in advanced clinical settings.

Page last updated on: