Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.96 Billion |

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia In-Vitro Diagnostics Market Analysis by Mordor Intelligence

Australia in vitro diagnostics market size in 2026 is estimated at USD 2.06 billion, growing from 2025 value of USD 1.96 billion with 2031 projections showing USD 2.63 billion, growing at 5.02% CAGR over 2026-2031. Rapid adoption of decentralized testing, expanding precision-medicine funding, and accelerating molecular innovation are jointly reshaping the diagnostic ecosystem. Intensifying chronic and infectious disease burdens are propelling glucose monitoring, infectious-disease multiplex panels, and oncology sequencing into routine care pathways. Public–private investment cycles remain strong, with rising private-equity ownership of oncology clinics complementing federal budget allocations to precision oncology and point-of-care (POC) programs. Meanwhile, stringent Therapeutic Goods Administration (TGA) rules and fragmented reimbursement for novel genetic assays temper near-term uptake, even as digital-health interoperability initiatives lower systemic bottlenecks.

Key Report Takeaways

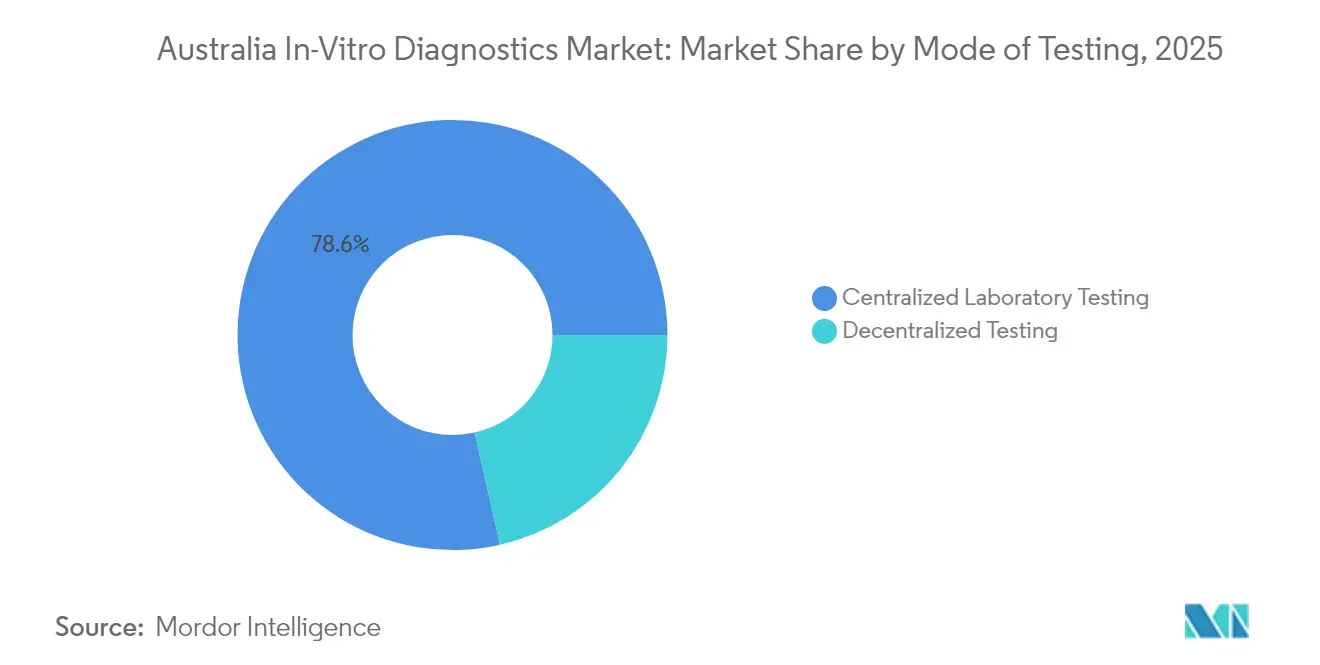

- By mode of testing, centralized laboratory testing commanded 78.55% of the Australia in vitro diagnostics market share in 2025; point-of-care testing is forecast to post the fastest 11.15% CAGR through 2031.

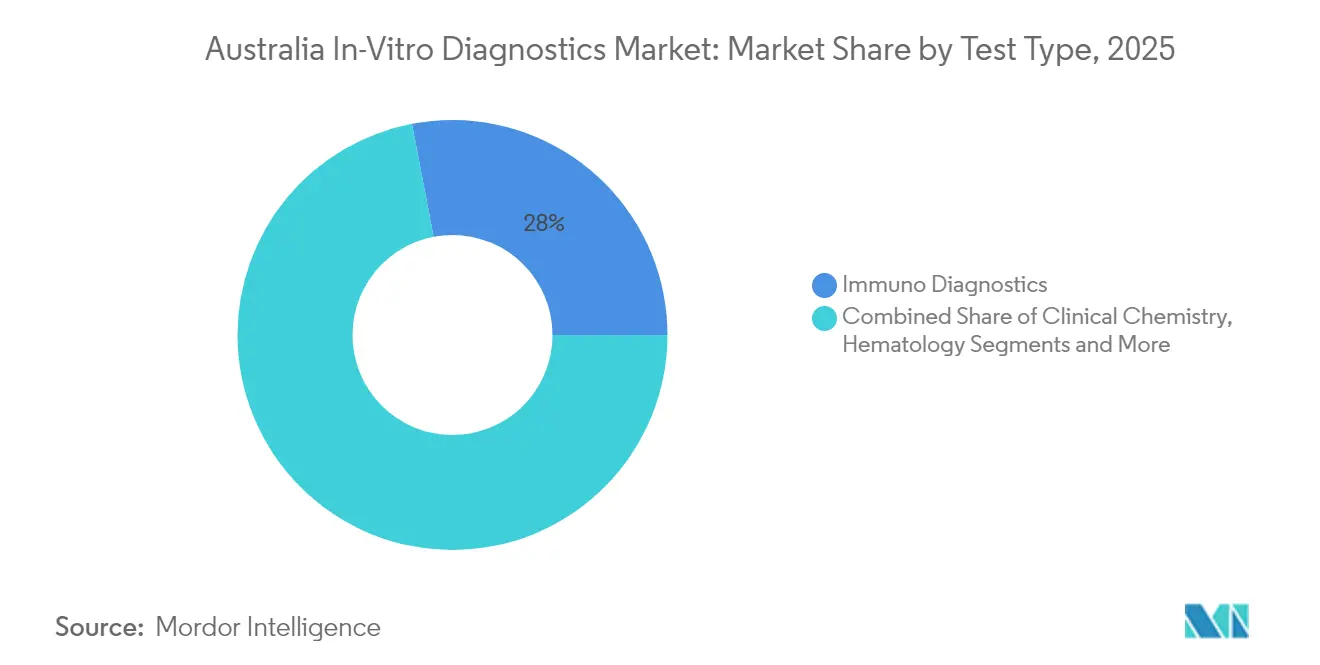

- By test type, immuno diagnostics led with 28.02% revenue share in 2025, while molecular diagnostics is projected to expand at a 9.32% CAGR to 2031.

- By product type, reagents and consumables captured 66.65% of the market share in 2025; software and services show the fastest outlook at a 10.09% CAGR to 2031.

- By technology, PCR accounted for 38.42% of the Australia in vitro diagnostics market size in 2025 and next-generation sequencing is advancing at a 12.21% CAGR through 2031.

- By application, infectious-disease testing held 32.15% of the Australia in vitro diagnostics market size in 2025; oncology applications are expected to grow at a 10.45% CAGR to 2031.

- By end user, independent diagnostic laboratories captured 53.78% of the Australia in vitro diagnostics market share in 2025, whereas home-care and self-testing users are growing at 11.86% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding federal & state investment in precision medicine and POC infrastructure | +1.8% | National (rural & remote emphasis) | Medium term (2-4 years) |

| Escalating burden of chronic & infectious diseases | +1.5% | National | Long term (≥4 years) |

| Rapid adoption of advanced molecular & digital IVD technologies | +1.2% | Urban centers first, regional later | Medium term (2-4 years) |

| Transition toward decentralized, consumer-centric testing models | +1.0% | National, early rural gains | Medium term (2-4 years) |

| Growing private healthcare expenditure & insurance penetration | +0.8% | Socio-economically advantaged urban areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expanding Federal & State Investment in Precision Medicine and POC Infrastructure

Federal precision-oncology funding of USD 130 million coupled with a USD 123.2 million Medicare allocation for new POC listings is accelerating adoption of specialized assays across public and remote settings. Indexation of labor-intensive pathology items beginning July 2025 ensures reimbursement integrity for tissue pathology and cytology, easing cost pressures for high-volume providers. Regional laboratories benefit as POC programs shorten care pathways, allowing rural clinicians to link rapid results with timely therapy. Manufacturers leveraging this supportive fiscal environment are fast-tracking menu expansions tailored to remote sample-to-answer platforms. Collectively, these public investments strengthen domestic demand while signaling long-term policy commitment to advanced diagnostics.

Escalating Burden of Chronic and Infectious Diseases Elevating Diagnostic Demand

More than 1.5 million Australians live with diabetes, boosting demand for near-patient glucose and HbA1c testing. Concurrently, permanent Medicare funding for COVID-19 and respiratory-pathogen PCR from July 2024 embeds infectious-disease testing in primary care. The National Hepatitis C Testing Policy 2025 prioritizes both laboratory and POC assays, encouraging earlier case identification and treatment initiation. Combined chronic and communicable-disease pressures are intensifying test volumes, especially in community clinics. Providers that bundle multiplex respiratory panels and continuous glucose-monitoring solutions are well-positioned to capture incremental volumes as disease prevalence rises.

Rapid Adoption of Advanced Molecular and Digital IVD Technologies

MSAC endorsement of whole-genome and whole-exome sequencing for mitochondrial disorders catalyzes broader clinical use of high-throughput genomic tools. The National Framework for Genomics in Cancer Control embeds sequencing in oncology care, producing a pull-through effect for sample-to-insight NGS workflows. Parallel investments in the Australian Digital Health Agency’s interoperability agenda drive demand for cloud-enabled data analytics, laboratory middleware, and AI-enhanced interpretation[1]Department of Health, “Precision Oncology Funding Factsheet,” health.gov.au. Vendors aligning assay chemistries with secure data pipelines gain competitive advantage through seamless clinician access and standardized electronic ordering.

Transition Toward Decentralized, Consumer-centric Testing Models

The First Nations Molecular POC Testing Program now spans more than 100 communities, demonstrating clinical impact by reducing result-to-treatment time from 14 days to as little as 90 minutes. Consumer acceptance of self-administered kits is rising as remote monitoring dovetails with telehealth consultations. Budget funding for sexually transmitted infection POC pilots reinforces policy support for decentralized diagnostics. Manufacturers that integrate Bluetooth-enabled devices with mobile applications satisfy user preferences for real-time feedback while meeting quality-assurance requirements. The growth of retail pharmacy testing counters access disparities and expands market reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval & compliance requirements | -1.2% | National | Short term (≤2 years) |

| Persistent workforce & skill shortages | -1.0% | Rural & remote areas | Medium term (2-4 years) |

| Fragmented reimbursement pathways for novel genetic & specialty tests | -0.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval and Compliance Requirements (TGA, MSAC)

TGA mandates rigorous Essential-Principles conformity and has introduced new software-device classification rules, extending compliance timelines and increasing dossier complexity[2]Therapeutic Goods Administration, “Cost Recovery Implementation Statement 2024-25,” tga.gov.au. Fee increases under the 2024-25 Cost Recovery Implementation Statement elevate market-entry costs, disproportionately affecting small innovators. Subsequent MSAC health-technology-assessment cycles add layers of evidence generation before public reimbursement. Vendors must navigate overlapping regulatory and funding milestones, often delaying commercialization. Strategic early engagement with regulators and adaptive clinical-evidence designs mitigate approval risks but raise initial capital needs.

Persistent Workforce & Skill Shortages Across Pathology Services

Pathologist trainee numbers have stagnated for six years, and anatomical pathology constitutes 44.5% of an aging workforce. Laboratory-scientist gaps are acute, with 32% of medical laboratory scientists concentrated in Victoria, leaving rural sites under-staffed. Automation is relieving some workload but cannot fully substitute expert interpretation for complex molecular assays. Recruitment challenges persist because remote laboratories face retention hurdles linked to professional isolation and limited career progression. Workforce scarcity threatens turnaround times and test-menu breadth, constraining market growth until training pipelines expand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Disrupting Routine Paradigms

Immuno diagnostics held a 28.02% share of the Australia in vitro diagnostics market in 2025, buoyed by their entrenched use in hormone, cardiac, and infectious-disease assays. Molecular diagnostics, however, is accelerating at a 9.32% CAGR, redefining the Australia in vitro diagnostics market size for high-complexity testing with next-generation sequencing and PCR panels. Laboratories increasingly bundle oncology gene panels with companion-therapy reporting, aligning with precision-oncology grants. Integrated AI in molecular platforms enhances variant-interpretation speed, allowing clinicians to move from sample to actionable report within 48 hours. Clinical chemistry remains a cost-efficient backbone for liver, renal, and metabolic profiling, maintaining volume resilience amid disruptive technologies. Hematology analyzers adopt flow-cytometry modules to support leukemia monitoring, slightly lifting their revenue contribution. Coagulation systems expand into direct oral anticoagulant monitoring, while microbiology sees renewed demand via rapid antimicrobial-susceptibility tests. Emerging segments such as blood-gas and urinalysis incorporate cartridge-based designs that suit decentralized settings, blending traditional laboratory needs with modern POC workflows.

The Australia in vitro diagnostics market is witnessing oncology laboratories adopt multiplex PCR for minimal residual disease detection, displacing single-analyte immuno assays. Meanwhile, pharmacogenomic tests guide antidepressant selection, creating new outpatient opportunities. Combined, these shifts illustrate how molecular advances compress testing timelines and expand clinical reach, drawing reimbursement attention and pushing manufacturers toward end-to-end workflow integration.

By Product Type: Software Integration Redefines Diagnostic Ecosystems

Reagents & consumables delivered 66.65% of 2025 revenue in the Australia in vitro diagnostics market, underscoring recurring demand for assay kits across high-throughput core labs. Instruments contribute lower but stable revenue as health-system consolidation centralizes capital purchases; QIAGEN’s 96-sample QIAsymphony Connect exemplifies the scaling trend toward oncology-ready platforms. The software & services category is expanding at 10.09% CAGR, demonstrating how cloud analytics, middleware, and subscription-based bioinformatics are redefining the Australia in vitro diagnostics industry’s revenue mix. Middleware solutions now provide auto-verification rules that cut manual review by nearly 30%, freeing scarce staff to focus on complex interpretations. Vendors bundle assay reagents with remote instrument monitoring, creating lifecycle-service annuities and boosting customer stickiness. Integrated ecosystems that synchronize instruments, reagents, and data analytics are supplanting stand-alone offerings, fostering strategic partnerships between platform providers and local distributors.

Instruments face longer replacement cycles, yet digital upgrades such as artificial-intelligence quality control prolong usability, delaying capital refreshment. Still, laboratories prioritize platforms that facilitate reagent rental models to align cash flow with Medicare bulk-billing realities. Emerging start-ups focus on low-cost, IoT-enabled readers targeting community pharmacies, broadening access without large capital expenditure. Software innovators leverage Australia’s My Health Record interface to enable direct clinician notification, enhancing diagnosis-to-therapy continuity.

By Technology: Next-Generation Sequencing Powers Genomic Revolution

PCR secured 38.42% of the Australia in vitro diagnostics market share in 2025, aided by entrenched respiratory-virus testing and robust supply lines. Yet, next-generation sequencing is growing at 12.21% CAGR, adding roughly USD 135 million to the Australia in vitro diagnostics market size by 2030 through oncology, rare-disease, and pathogen-surveillance applications. National cancer-genomics frameworks encourage reference labs to offer tumor mutational burden and microsatellite instability panels, solidifying NGS as a first-line diagnostic for solid tumors. Immunoassay platforms introduce chemiluminescence upgrades, boosting sensitivity for cardiac markers and vitamin-D tests. Mass spectrometry—especially LC-MS/MS—gains niche traction in therapeutic-drug monitoring due to its high specificity. Microarrays serve as bridge technologies for gene-expression profiling in research hospitals, while loop-mediated isothermal amplification supports rapid pathogen detection in low-resource areas.

Convergence is evident as hybrid workflows combine PCR for initial screening with targeted NGS reflex testing, optimizing cost per diagnosis. Cloud-based bioinformatics pipelines feature automated variant classification, reducing data-analysis bottlenecks. Vendors developing reagent-agnostic sequencers appeal to service labs juggling multi-vendor assay menus, highlighting flexibility as a purchase differentiator.

By Mode of Testing: POC Revolution Alters Service Delivery

Centralized laboratories captured 78.55% of 2025 revenue, leveraging economies of scale and the Medicare bulk-billing model that reimburses nearly 100% of out-of-hospital tests. Nonetheless, POC testing is slated to grow at 11.15% CAGR, adding mobile diagnostics and pharmacy-based services to the Australia in vitro diagnostics market. The First Nations Molecular POC Testing Program reduced respiratory-virus result wait times to under 90 minutes, demonstrating clinical effectiveness in remote settings. QAAMS diabetes POC has shown improved HbA1c control, underscoring decentralized efficacy. Hospitals integrate bedside blood-gas analyzers in critical care to enhance rapid-response decisions. POC devices now feature CLIA-waived cartridges for cardiac troponin, enabling urgent-care triage without central lab reliance.

Centralized hubs continue to dominate complex genomic panels and high-volume chemistry assays, yet hybrid models emerge where regional labs oversee quality while local clinics run selected rapid tests. Manufacturers focusing on connectivity—HL7 or FHIR-enabled devices—ensure seamless data flow into electronic medical records, meeting digital-health mandates. Ultimately, patients benefit from faster diagnosis, while laboratories recalibrate menus to balance throughput and immediacy.

By Application: Oncology Diagnostics Catalyze Precision Care

Infectious-disease assays held 32.15% of 2025 revenue within the Australia in vitro diagnostics market, reflecting sustained respiratory-panel demand and hepatitis C elimination targets. Oncology diagnostics exhibit the highest 10.45% CAGR, propelled by USD 130 million in federal precision-oncology grants and broader coverage of genomic tumor profiling. Cardiology assays expand with NT-proBNP Medicare listing, supporting primary-care heart-failure detection. Autoimmune panels integrate multiplex testing for systemic lupus and rheumatoid arthritis, improving rule-out efficiency. Blood-screening services adopt nucleic-acid amplification for transfusion safety, maintaining baseline demand. Prenatal screening moves toward cell-free DNA assays, aligning with consumer preferences for non-invasive options. Nephrology biomarkers observe incremental uptake as chronic-kidney-disease prevalence increases.

Oncology laboratories partner with pharmaceutical sponsors for companion-diagnostic co-development, expanding menu breadth. Liquid biopsy research advances ctDNA tests for minimal residual disease, promising future expansion areas. As reimbursement matures, oncology’s share of the Australia in vitro diagnostics market is expected to close the gap with infectious disease by the decade’s end.

By End User: Self-Testing Reshapes Consumption Models

Independent diagnostic laboratories controlled 53.78% of revenue in 2025, enabled by consolidated service networks and extensive courier logistics. Hospital and clinic labs retain complex test portfolios that support acute care. Point-of-care settings inside GP clinics and pharmacies are broadening diagnostics for chronic-disease management, offering real-time HbA1c and lipid panels. Home-care and self-testing is the fastest-growing user group at 11.86% CAGR, driven by digitally connected pregnancy, ovulation, and COVID-19 kits that integrate with telehealth apps. Consumer empowerment aligns with Australia’s digital-health strategy, which grants patients online access to laboratory results.

Self-testing challenges traditional labs by diverting low-complexity tests yet generates confirmatory demand for positive results. Laboratories are responding with consumer portals providing convenient phlebotomy bookings and at-home sample-collection kits for colorectal-cancer screening. Device makers collaborate with insurers to bundle self-testing subscriptions into wellness programs, deepening penetration among younger, tech-savvy populations.

Geography Analysis

New South Wales accounts for the largest provincial share of the Australia in vitro diagnostics market size due to its dense hospital network and concentration of reference mega-labs in Sydney. Victoria follows closely, supported by a high proportion of medical laboratory scientists and vibrant biotech clusters around Melbourne. Queensland’s public-health emphasis, particularly in tropical disease surveillance, underpins steady test-volume growth and targeted POC deployments in Far North communities. Western Australia exhibits moderate uptake of advanced molecular platforms, propelled by mining-sector employer demand for occupational-health screening.

Rural and remote regions collectively capture a smaller share yet experience above-average growth as POC and telepathology bridge access gaps. Federal grants channeled through the Rural Health Multidisciplinary Training Program finance mobile lab units that rotate across Indigenous communities, improving chronic-disease monitoring. Cross-state procurement alliances now negotiate volume discounts on reagents, creating procurement efficiencies that offset shipping costs to distant sites.

Interstate referral testing flows reinforce the hub-and-spoke model, with complex NGS panels often sent to east-coast super-labs, while routine chemistry is processed locally. Government incentives for regional genomics hubs aim to decentralize capacity, although workforce shortages remain a limiting factor. As digital interoperability matures, laboratories in Tasmania and the Northern Territory will gain faster access to specialist consults, narrowing diagnostic-equity gaps across the federation.

Competitive Landscape

The Australia in vitro diagnostics market is moderately concentrated. Sonic Healthcare, Healius, and Australian Clinical Labs collectively command the majority of routine pathology volumes, leveraging national collection center networks and high-throughput laboratories. Recent expansion into Southeast Asian and European markets gives these incumbents diversified revenue bases and access to emerging molecular technologies that can be repatriated to Australia. Mergers among smaller regional laboratories continue but attract ACCC scrutiny to prevent excessive market power concentration.

Strategic partnerships proliferate as niche players seek scale: Abacus dx teamed with Roche to co-market life-science reagents and specialized instruments, adding depth to oncology and immunology portfolios. Instrument manufacturers operate via exclusive distribution, intensifying competition for hospital tenders where long-term reagent contracts lock in revenue. Digital-health vendors form alliances with pathology groups to embed secure result-delivery systems into clinician workflows, enhancing stickiness.

Innovation focus is shifting toward integrated ecosystem offerings that combine extraction, amplification, detection, and informatics. Global firms introduce lease-to-own financing to mitigate capital barriers for independent labs. Meanwhile, regulatory vigilance over data privacy and cyber-security compels firms to invest in ISO 27001-certified infrastructures, raising entry costs for new entrants.

Australia In-Vitro Diagnostics Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche AG

Siemens Healthineers AG

Thermo Fisher Scientific Inc.

bioMerieux SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Department of Health introduced annual indexation for selected pathology services beginning July 2025, targeting labor-intensive items such as tissue pathology and cytology to sustain high bulk-billing levels.

- April 2025: The Department of Health, Disability and Ageing announced AUD 1.8 million (USD 1.2 million) Quality Use of Pathology Project Grants for 2025-2027 to advance economic efficiency and service quality in Australia’s pathology sector.

Australia In-Vitro Diagnostics Market Report Scope

As per the scope of this report, in-vitro diagnostics involves medical devices and consumables that are utilized to perform in-vitro tests on various biological samples. They are used for the diagnosis of various medical conditions and chronic diseases. The in-vitro diagnostics market in Australia is classified by test type (clinical chemistry, molecular diagnostics, immunodiagnostics, hematology, and other test types), product type (instruments, reagents, and other types of products), application (infectious disease, diabetes, cancer/oncology, cardiology, autoimmunity, and other applications), and end user (diagnostic laboratories, hospitals, and clinics, and other end users). The report offers the value (in USD million) for the above segments.

By Test Type

| Clinical Chemistry |

| Immuno Diagnostics |

| Molecular Diagnostics |

| Hematology |

| Coagulation |

| Microbiology |

| Others (Urinalysis, Blood Gas, etc.) |

By Product Type

| Instruments |

| Reagents & Consumables |

| Software & Services |

By Technology

| PCR |

| Next-Generation Sequencing (NGS) |

| Immunoassay |

| Mass Spectrometry |

| Microarrays |

| Others (Flow Cytometry, LAMP, etc.) |

By Mode of Testing

| Centralized Laboratory Testing |

| Point-of-Care/Decentralized Testing |

By Application

| Infectious Disease |

| Diabetes |

| Oncology |

| Cardiology |

| Autoimmune Disorders |

| Blood Screening |

| Others (Prenatal, Nephrology, etc.) |

By End User

| Independent Diagnostic Laboratories |

| Hospital & Clinic-based Labs |

| Point-of-care Settings (GP Offices, Pharmacies) |

| Home-care & Self-testing Users |

| By Test Type | Clinical Chemistry |

| Immuno Diagnostics | |

| Molecular Diagnostics | |

| Hematology | |

| Coagulation | |

| Microbiology | |

| Others (Urinalysis, Blood Gas, etc.) | |

| By Product Type | Instruments |

| Reagents & Consumables | |

| Software & Services | |

| By Technology | PCR |

| Next-Generation Sequencing (NGS) | |

| Immunoassay | |

| Mass Spectrometry | |

| Microarrays | |

| Others (Flow Cytometry, LAMP, etc.) | |

| By Mode of Testing | Centralized Laboratory Testing |

| Point-of-Care/Decentralized Testing | |

| By Application | Infectious Disease |

| Diabetes | |

| Oncology | |

| Cardiology | |

| Autoimmune Disorders | |

| Blood Screening | |

| Others (Prenatal, Nephrology, etc.) | |

| By End User | Independent Diagnostic Laboratories |

| Hospital & Clinic-based Labs | |

| Point-of-care Settings (GP Offices, Pharmacies) | |

| Home-care & Self-testing Users |

Key Questions Answered in the Report

How big is the Australia in vitro diagnostics market in 2026?

The market is valued at USD 2.06 billion in 2026 and is projected to grow steadily at a 5.02% CAGR through 2031.

Which testing mode is growing fastest within Australian diagnostics?

Point-of-care testing shows the highest momentum, forecast to expand at 11.15% CAGR between 2026 and 2031 on the back of rural-health and consumer demand.

What segment holds the largest Australia in vitro diagnostics market share today?

Immuno diagnostics leads with 28.02% revenue share thanks to widespread use in routine hormone, cardiac, and infectious-disease panels.

Why is next-generation sequencing attracting investment?

NGS is growing at 12.21% CAGR because national cancer genomics frameworks and MSAC reimbursement endorsements are embedding high-throughput sequencing into standard care.

How are workforce shortages affecting Australian pathology services?

Slow trainee growth and regional staffing gaps threaten turnaround times, prompting laboratories to accelerate automation and digital-result verification to maintain service levels.

Page last updated on: