Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

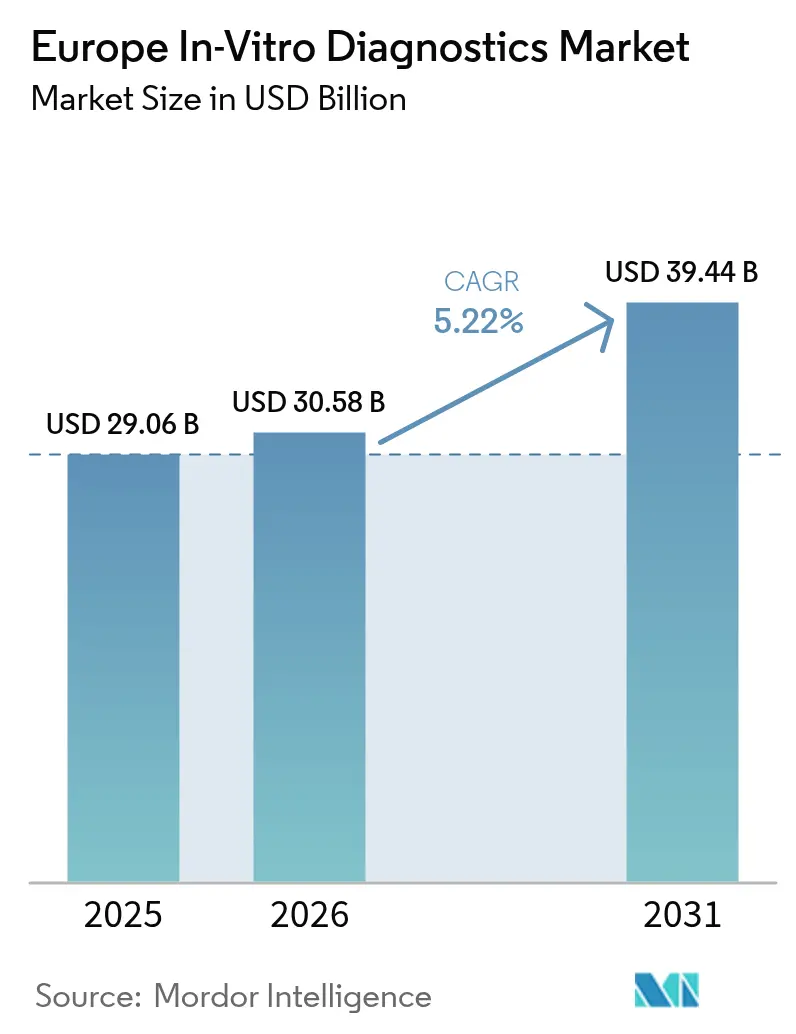

| Base Year Market Size (2025) | USD 29.06 Billion |

| Market Size (2026) | USD 30.58 Billion |

| Market Size (2031) | USD 39.44 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Europe In-Vitro Diagnostics Market size is projected to be USD 29.06 billion in 2025, USD 30.58 billion in 2026, and reach USD 39.44 billion by 2031, growing at a CAGR of 5.22% from 2026 to 2031.

Europe's in-vitro diagnostics market is experiencing significant growth as the region transitions from episodic treatments to preventive screenings and personalized care. Key drivers include increasing demand for chronic disease monitoring, the decentralization of point-of-care solutions, and the implementation of precision medicine. The aging population, with the 65-plus demographic projected to grow by 41% by 2050, continues to support consistent demand for glucose, lipid, and renal panels. Additionally, national genomic programs in France, Germany, and the UK are accelerating the adoption of sequencing reagents. Molecular diagnostics, traditionally central to infectious-disease monitoring, are expanding into oncology and rare-disease applications, supported by rising companion-diagnostic approvals and declining sequencing costs. While reagent and consumable sales dominate revenue streams, the fastest-growing segments are software-as-a-medical-device and cloud-connected analyzers, reflecting the digital transformation of laboratories under GDPR cybersecurity requirements. The competitive landscape remains intense, with multinationals defending their market share in clinical chemistry, while smaller innovators focus on rapid molecular cartridges, home testing kits, and AI-powered interpretation tools.

Key Report Takeaways

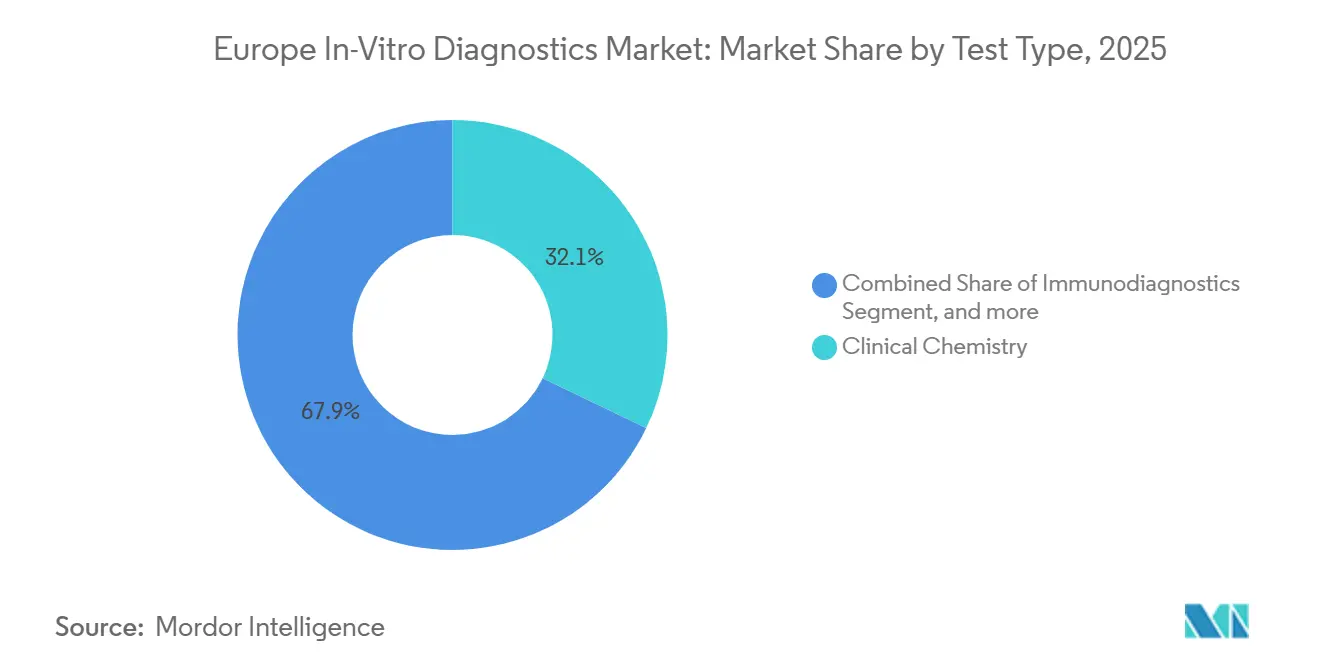

- By test type, clinical chemistry led with 32.12% Europe in-vitro diagnostics market share in 2025 while molecular diagnostics is projected to post a 7.43% CAGR through 2031.

- By product, reagents and consumables accounted for 54.65% of the Europe in-vitro diagnostics market size in 2025; software and services is forecast to expand at an 8.11% CAGR to 2031.

- By end user, diagnostic laboratories held 46.43% revenue share in 2025 whereas home-care and point-of-care centers are advancing at an 8.54% CAGR through 2031.

- By usability, disposable devices led with 67.43% Europe in-vitro diagnostics market share in 2025 while Reusable IVD Devices is projected to post a 7.65% CAGR through 2031.

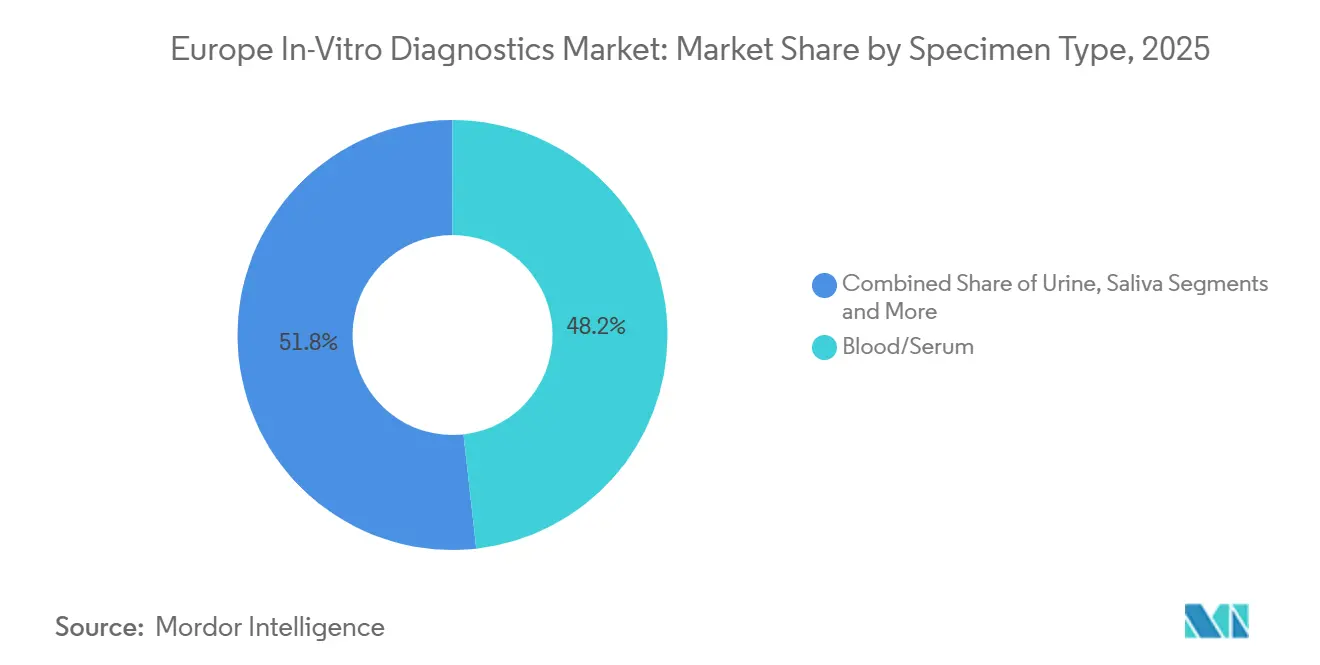

- By specimen type, blood / serum accounted for 48.23% of the Europe in-vitro diagnostics market size in 2025; urine is forecast to expand at an 7.22% CAGR to 2031.

- By application, infectious diseases held 29.94% revenue share in 2025 whereas Diabetes are advancing at an 8.43% CAGR through 2031.

- By geography, Germany captured 24.76% revenue in 2025 and the United Kingdom is poised for the fastest 6.43% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic and infectious diseases | +1.2% | Pan-European, highest in Germany, UK, France, Italy, Spain | Long term (≥ 4 years) |

| Increasing adoption of point-of-care testing | +0.9% | Germany, UK, France; rural and underserved parts of Rest of Europe | Medium term (2-4 years) |

| Rising geriatric population and preventive screening initiatives | +0.8% | Pan-European; acute in Germany, Italy, Spain | Long term (≥ 4 years) |

| Expansion of national genomic medicine programs | +0.7% | France, Germany, UK, Spain | Medium term (2-4 years) |

| Digital health integration for remote sample collection | +0.6% | UK, Germany, France, Netherlands; pilots in Nordics | Medium term (2-4 years) |

| Sustainability mandates driving eco-friendly consumables | +0.3% | EU-wide; led by Germany, Netherlands, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic and Infectious Diseases

Multimorbidity now impacts 50% of Europeans aged 65-74, rising from 44% in 2011, further widening the gap between life expectancy and healthy life years. The European Commission’s Safe Hearts Plan, targeting universal annual measurements of blood pressure, cholesterol, and blood sugar by 2035, is driving increased per-capita test volumes for HbA1c, lipid panels, cardiac biomarkers, and oncology markers[1]European Commission, “Safe Hearts Plan,” ec.europa.eu. Infectious-disease surveillance remains a critical focus, with integrated molecular panels for HIV, hepatitis, respiratory viruses, and antimicrobial resistance profiling forming the backbone of routine hospital and public health operations. The launch of bioMérieux and Oxford Nanopore’s AmPORE-TB marks a strategic shift toward rapid sequencing for the characterization of drug-resistant tuberculosis. Sustained demand across chronic and infectious disease segments is expected to contribute an estimated 1.2-percentage-point increase to the CAGR of the Europe in-vitro diagnostics market.

Increasing Adoption of Point-of-Care Testing

With the expansion of hospital-at-home programs, point-of-care formats now contribute to over 30% of the in-vitro diagnostics market in Europe. England's virtual ward initiative, supported by a GBP 450 million investment through 2024, leverages near-patient testing to reduce emergency admissions. The FDA-cleared QIAstat-Dx mini panels, which deliver gastrointestinal reports within one hour, exemplify the adoption of user-friendly cartridges in primary care and pharmacy settings[2]QIAGEN, “QIAstat-Dx FDA Clearance Press Release,” qiagen.com. Additionally, pharmacist-led testing, now authorized in 18 OECD countries, and nurse-managed remote-monitoring protocols are driving the decentralization of sample collection. Accelerating reimbursement frameworks are further fueling market growth, contributing to a 0.9-percentage-point CAGR increase in Europe's in-vitro diagnostics market.

Expansion of National Genomic Medicine Programs

France’s Plan France Médecine Génomique delivered 12,737 rare-disease and cancer reports by end-2023 with a 30.6% diagnostic yield, targeting 235,000 genomes annually by 2027. Germany’s genomDE integrates sequencing into routine oncology and rare-disease care under a unified national infrastructure. The UK NHS Genomic Medicine Service exceeded 810,000 genomic tests in 2024 and is embedding circulating-tumor-DNA assays across oncology pathways. Spain’s contribution to the Genome of Europe project underscores continental alignment. These initiatives collectively add 0.7-percentage-points to the Europe in-vitro diagnostics market growth curve as companion-diagnostic reimbursement and data-analysis capacity scale.

Digital Health Integration: Enhancing Remote Sample Collection and Result Delivery

Cloud-connected analyzers and GDPR-compliant laboratory information systems now transmit encrypted results to patient portals, supporting remote care models. The European Health Data Space sets interoperability rules for cross-border exchange, and the Safe Hearts Plan earmarks EUR 20 million for AI cardiovascular tools. CMS reimbursement for Illumina’s TruSight Oncology Comprehensive test at USD 2,989.55 signals payer acceptance of comprehensive genomic profiling in decentralized laboratories. Robust encryption, pseudonymization, and cybersecurity audits remain prerequisites for procurement, yet successful pilots contribute 0.6 percentage points to market CAGR.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and lengthy regulatory approval processes under EU IVDR | −0.8% | Pan-European; toughest for SMEs | Short term (≤ 2 years) |

| Reimbursement uncertainty for high-cost molecular diagnostics | −0.5% | Germany, France, UK, Italy; fragmented elsewhere | Medium term (2-4 years) |

| Laboratory workforce shortages and operational constraints | −0.4% | Germany, UK, France, Netherlands; rural areas | Long term (≥ 4 years) |

| Data security and privacy concerns with cloud-connected analyzers | −0.2% | Region-wide; strictest enforcement in Germany and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent and Lengthy Regulatory Approval Processes Under EU IVDR

Two-thirds of IVDs still awaited certification under the 2022 EU IVDR as of 2024, straining notified-body capacity and elongating time-to-market[3]European Commission, “IVDR Transition Status Update,” ec.europa.eu. SMEs shoulder disproportionate documentation and clinical-evidence costs, risking market exits. A December 2025 European Commission proposal outlines accelerated pathways for breakthrough devices, yet relief will not materialize before 2027. The resulting bottleneck trims 0.8 percentage points from the Europe in-vitro diagnostics market CAGR in the short term.

Laboratory Workforce Shortages and Operational Constraints

Health-workforce aging parallels patient demographics. The European Commission-OECD Health at a Glance 2024 review urges increased training slots and retention incentives amid accelerating technologist retirements. Automation offsets some gaps, yet capital budgets and service-engineer availability limit adoption in smaller labs. Persistent staffing shortages depress throughput, stretching turnaround times and subtracting 0.4 percentage points from long-run Europe in-vitro diagnostics market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Gain Momentum

Clinical chemistry retained 32.12% of 2025 revenue, yet molecular diagnostics is forecast to expand fastest at 7.43% CAGR, lifting the Europe in-vitro diagnostics market size for sequencing consumables and bioinformatics. Companion diagnostic approvals for EGFR, RET, and NTRK mutations, combined with national sequencing subsidies, drive recurring demand for reagents. Rapid multiplex platforms such as QIAstat-Dx Rise, capable of 160 molecular tests daily, exemplify throughput gains needed to meet decentralized acute-care volumes. Routine biochemistry remains indispensable for chronic-disease management, anchoring base load in hospital labs.

Beyond infectious-disease panels, molecular assays are penetrating oncology, minimal residual disease monitoring, hereditary cancer screening, and pharmacogenomics. Illumina’s CMS-reimbursed TruSight Oncology Comprehensive workflow underscores payer confidence, smoothing adoption in regional centers. Genotype-guided drug dosing in cardiology and psychiatry is on reimbursement agendas in Germany and the Netherlands, setting the stage for further Europe in-vitro diagnostics market expansion.

By Product and Service: Software and Services Accelerate

Reagents and consumables captured 54.65% of 2025 revenue thanks to recurring kits for chemistry, immunoassay, and PCR workflows. Instrument fleets are entering a replacement cycle as labs favor modular, energy-efficient analyzers with middleware connectivity. Software and services will rise at an 8.11% CAGR as laboratories integrate AI interpretation, quality dashboards, and cybersecurity hardening.

The Europe in-vitro diagnostics market benefits from subscription models: pay-per-genome analytics, cloud LIS modules, and remote calibration services, all generating predictable annuities. Gentian Diagnostics’ 2026 partnership to co-develop a novel assay on an existing high-throughput chemistry line illustrates the asset-light route for smaller innovators to ride incumbent footprints.

By Usability: Disposables Still Dominate While Reusables Gain

Single-use strips, cassettes, and molecular cartridges held 67.43% share in 2025 because they eliminate cross-contamination risk and simplify regulatory clearance. Yet reusable analyzers, electrodes, and multi-test sensors are projected to climb 7.65% CAGR as sustainability procurement criteria tighten. EU Green Deal targets and hospital carbon accounting now reward durable platforms with recyclable consumables.

Hospital-at-home models, which revisit patients daily, prefer robust portable analyzers that amortize over multiple uses, a trend tilting future Europe in-vitro diagnostics market purchases toward reusables without displacing the entrenched dominance of disposables.

By Specimen Type: Blood Leads, Urine Rises

Blood and serum generated 48.23% of 2025 revenues, maintaining primacy in chemistry, hematology, immunoassay, and NGS workflows. Annual cholesterol and glucose screening targets under the Safe Hearts Plan preserve high-volume phlebotomy throughput. Urine testing, however, is forecast to rise 7.22% CAGR as home-based microalbumin, ketone, and pregnancy kits proliferate.

Saliva is carving niches in hormone and genetic testing; tissue biopsies remain oncology gold standards while liquid biopsies emerge for serial cancer monitoring. Non-invasive matrices broaden patient compliance, yet the Europe in-vitro diagnostics market continues to rely on venous draws for the majority of clinical actionable data.

By Application: Infectious Disease Tops, Diabetes Surges

Infectious-disease assays held 29.94% share in 2025, anchored by respiratory panels, HIV, and hepatitis screening, and antimicrobial-resistance detection. Diabetes applications, however, will grow fastest at 8.43% CAGR as continuous glucose monitors integrate with insulin-delivery systems and preventive screening intensifies. Oncology and cardiology benefit from genomic medicine and Safe Hearts milestones, respectively, expanding companion-diagnostic and lipid-panel volumes.

Autoimmune, nephrology, prenatal, and transfusion safety segments round out the Europe in-vitro diagnostics industry portfolio, each supported by guideline-driven testing cadences, yet none match the growth velocity of diabetes monitoring over the forecast window.

By End User: Home-Care and POC Centers Gain Traction

Diagnostic laboratories controlled 46.43% of 2025 revenues owing to centralized high-throughput capability, but home-care and point-of-care centers are projected to register an 8.54% CAGR, narrowing the gap. Hospital-at-home programs in France, Spain, and the UK depend on portable analyzers for bedside decisions. Pharmacy and nurse-led testing further decentralize access, positioning non-traditional settings as rising contributors to the Europe in-vitro diagnostics market size.

Hospitals retain complex assay dominance, whereas academic institutes drive NGS research and biomarker discovery. Survey data suggesting up to 25% of tests could migrate to homes by 2035 underscores the momentum behind decentralized care models.

Geography Analysis

Germany, with 24.76% revenue in 2025, leverages its large insured population, intensive care infrastructure, and genomDE precision-medicine investments to maintain its largest national share. High adoption of automation and antimicrobial-resistance protocols ensures steady instrument refresh cycles and reagent pull-through.

The United Kingdom will post the fastest 6.43% CAGR to 2031 as the NHS Genomic Medicine Service integrates circulating tumor DNA assays into standard oncology, streamlines procurement for validated tests, and expands virtual wards that rely on near-patient diagnostics. A post-Brexit regulatory pathway enabling rapid approvals for innovative devices further accelerates uptake.

France, Italy, and Spain together harness EU Recovery funds for personalized medicine and sequencing under the Genome of Europe umbrella, while Nordic nations emphasize digital interoperability and eco-friendly procurement, keeping the Europe in-vitro diagnostics market vibrant across disparate health-system models.

Regulatory Landscape

Europe in-vitro diagnostics regulation is anchored by Regulation (EU) 2017/746 (IVDR), applicable since 26 May 2022, shifting most IVDs into a stronger pre-market conformity assessment regime supported by Notified Bodies and MDCG guidance. To manage certification bottlenecks and avoid product gaps, Regulation (EU) 2024/1860 (effective 9 July 2024) extended transitional timelines for eligible legacy devices to 31 December 2027 (Class D), 31 December 2028 (Class C), and 31 December 2029 (Class B and A sterile), with key application milestones tied to 26 May 2025 (Class D), 26 May 2026 (Class C), and 26 May 2027 (Class B/A sterile).

Regulatory operations increasingly depend on EU-wide infrastructure such as EUDAMED for registration and vigilance, alongside ongoing implementation coordination by the European Commission. On 16 December 2025, the European Commission published COM(2025) 1023 proposing to simplify elements of the MDR/IVDR framework, reflecting active policymaker focus on reducing administrative burden while maintaining safety and performance requirements for IVDs placed on the EU market.

Value Chain Analysis

The Europe in-vitro diagnostics value chain spans upstream specialty inputs (biological raw materials such as antibodies and recombinant proteins, plastics and microfluidic components, optics and sensors, and semiconductors), followed by assay development, instrument engineering, regulated manufacturing under quality systems, and distribution into hospitals, diagnostic laboratories, and decentralized home-care/POC settings. Reagents and consumables dominate the commercial flow because recurring test volumes pull through kits, calibrators, and controls across clinical chemistry, immunodiagnostics, and PCR/NGS workflows; instruments and middleware connectivity then anchor multi-year service, maintenance, and software revenues.

A recurring bottleneck in the chain is regulatory throughput under IVDR, where conformity assessment capacity and documentation demands can delay portfolio continuity, particularly for smaller manufacturers, and can trigger rationalization of low-volume assays. Data and interoperability requirements (GDPR-compliant systems and broader EU health data initiatives) also add steps to validation and post-market monitoring, elevating the role of digital workflow vendors and laboratory informatics partners alongside traditional manufacturers, distributors, and reference labs.

Competitive Landscape

In 2025, four multinational corporations—Roche, Abbott, Siemens Healthineers, and Danaher—dominated the market, collectively capturing over 55% of revenues through their well-established chemistry and immunoassay platforms. bioMérieux reported EUR 2.044 billion in sales during the first half of 2025 and strategically expanded into cell-therapy quality control through its 2026 acquisition of Accellix. Illumina's CMS reimbursement approval in 2026 significantly boosted demand for oncology profiling, while Revvity's partnership with Element Biosciences on neonatal sequencing exemplified co-innovation to mitigate regulatory risks.

Emerging competitors are capitalizing on niche opportunities, particularly in rapid molecular cartridges and AI-driven interpretation solutions. These players differentiate themselves through subscription-based digital workflows, eco-design initiatives, and middleware interoperability. Although proposed EU IVDR reforms could create opportunities for breakthrough entrants, the regulatory landscape continues to favor established incumbents with strong compliance infrastructures.

Europe In-Vitro Diagnostics Industry Leaders

Illumina, Inc.

Sysmex Corp.

QIAGEN N.V.

bioMerieux SA

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

IVDR transition execution creates whitespace for compliance-enabling services and product refresh cycles, especially as the extended deadlines under Regulation (EU) 2024/1860 are paired with near-term submission milestones (notably 26 May 2026 for Class C applications to Notified Bodies). Opportunities concentrate in CE-IVDR-certified menu expansions (for example, syndromic and antimicrobial resistance panels) and in software and services that help laboratories manage traceability, cybersecurity, and regulated reporting as cloud-connected analyzers and digital workflows expand in routine use.

On the supply side, localized European manufacturing investments provide tangible headroom to increase PCR and molecular testing availability and reduce supply risk. bioMérieux announced a EUR 250 million investment (May 2026) to build a new PCR manufacturing facility in La Balme-les-Grottes, France, aimed at serving the European market, and Roche confirmed continuation of its EUR 600 million diagnostics production site investment in Penzberg, Germany (June 2026), with completion scheduled for 2027. In parallel, the EU continued to tighten and harmonize conformity assessment infrastructure through implementing acts in 2026, reinforcing demand for standardized quality systems and creating a clearer pathway for scale manufacturers and notified bodies as the market moves through the IVDR transition window.

Recent Industry Developments

- July 2026: QIAGEN expanded its European bloodstream infection syndromic testing menu with the CE-IVDR-certified QIAstat-Dx BCID GN Plus AMR Panel. The launch complements the earlier gram-positive panel to broaden coverage for rapid identification and antimicrobial resistance markers, supporting faster treatment decisions in acute care workflows.

- April 2026: QIAGEN launched the CE-IVDR-certified QIAstat-Dx BCID GPF Plus AMR Panel for bloodstream infection testing in Europe. It strengthened QIAGEN's position in hospital microbiology and syndromic testing by adding an IVDR-aligned option for rapid pathogen and AMR detection.

- September 2025: QIAGEN secured European CE-IVDR certification for its full portfolio of QIAstat-Dx systems and panels. The certification milestone reduced regulatory friction for placements and menu utilization across European laboratories navigating the shift from IVDD to IVDR.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers in vitro diagnostics used across Europe, including tests run in clinical labs and near-patient or home settings to help diagnose, screen, and monitor diseases or conditions. It is measured as the revenue generated from IVD products and related offerings within the region.

Scope exclusions: This sizing does not count broader healthcare services that are not directly tied to IVD testing, such as general hospital care delivery outside the testing workflow.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immunodiagnostics

- Molecular Diagnostics

- Hematology

- Microbiology & Lateral Flow

- Coagulation

- Point-Of-Care (Rapid) Tests

- Other Tests

- By Product & Service

- Reagents & Consumables

- Instruments / Analyzers

- Software & Services

- By Usability

- Disposable IVD Devices

- Reusable IVD Devices

- By Specimen Type

- Blood / Serum

- Urine

- Saliva

- Tissue / Biopsy

- Other Specimen Types

- By Application

- Infectious Diseases

- Diabetes

- Cancer / Oncology

- Cardiology

- Autoimmune Disorders

- Nephrology & Renal Panels

- Prenatal / Genetic Screening

- Blood Screening

- Other Applications

- By End User

- Academic & Research Institutes

- Diagnostic Laboratories

- Home-Care / POC Centers

- Hospitals & Clinics

- Other End Users

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for Europe and to anchor the model on stable, repeatable data series. We referenced public sources such as Eurostat health and population tables, WHO Europe health indicators, European Commission materials related to IVD regulation, and OECD health statistics to understand testing demand signals and system capacity.

We then complemented these inputs with customs and trade statistics where relevant for equipment flows, peer-reviewed clinical publications to track adoption by test area, and company filings and investor presentations to confirm portfolio mix and Europe exposure. In some cases, paid subscription datasets compiling company financials and patent activity were used to speed verification. These examples are not exhaustive, and other sources were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming which test categories are growing, what typically drives pricing and replacement cycles, and how demand is shifting across hospital labs, independent labs, and point-of-care settings. We interviewed manufacturers, distributors, lab buyers, and clinical stakeholders across major European countries and the rest of the region. The goal was to use these inputs to tighten assumptions that desk research could not settle cleanly.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 17% | |

| Mid tier: 53% | Functional/Unit leaders: 31% | |

| Smaller Players: 17% | Managers: 52% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build where diagnosis area demand is reconstructed from Europe-level healthcare activity and testing intensity, then filtered through the IVD share that is routinely captured by lab and point-of-care workflows. Once the demand pool is framed, revenue is estimated by applying realistic price and mix assumptions for key IVD categories and then reconciling totals across the main European countries.

To keep the outputs grounded, we cross-check totals with selective bottom-up approximations, including sampled supplier revenue splits for Europe, channel feedback on volumes, and typical reagent pull-through linked to installed instruments. Inputs that shape the model include testing volumes by major disciplines (like clinical chemistry, immunoassays, molecular diagnostics, and hematology), the share of point-of-care versus central lab usage, replacement and utilization patterns for instruments, and observed pricing and reimbursement pressure in mature countries.

Forecasting uses scenario analysis supported by trend lines in chronic disease burden, aging population share, and regulatory transition impacts, then adjusts the path based on what primary respondents expect for adoption and price movement. Where direct volume signals are incomplete, gaps are handled with proxy indicators from similar countries and by applying conservative ranges that are tightened during validation.

Data Validation & Update Cycle

Model outputs are validated by checking whether implied testing volumes, per capita spend, and country splits align with independent health system indicators and trade and financial signals. When a result looks out of pattern, the assumptions are reopened, the calculations are re-run, and primary contacts are re-checked so the variance has a clear explanation before sign-off.

A multi-step analyst review is used to keep the final numbers consistent across the narrative, exhibits, and country totals. Reports are refreshed annually, and interim updates are triggered when material events occur, such as regulatory shifts, major pricing changes, or step changes in testing demand. Before delivery, a final pass is completed so the client receives an up-to-date view rather than an older snapshot.

Mordor Intelligence's Vitro Diagnostics Europe Market Size Measured Against Other Published Estimates

Published values for the Europe IVD market can vary even when the topic label looks similar, since scope boundaries and the year used for sizing are not always aligned. Differences usually come from what is counted as IVD revenue, how point-of-care and home testing are treated, and how pricing is projected as product mix changes.

The table shows a tight cluster around the 2025 value, and the spread typically depends on whether adjacent software and services are included broadly, plus how quickly prices are assumed to normalize after recent demand swings, in Mordor Intelligence's model only IVD products and directly tied offerings are counted under the Europe scope, and country totals are reconciled before rolling up to the region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.06 B (2025) | |

| Healthcare Publisher A | USD 29.13 B (2025) | Uses a broader regional definition and presents a longer horizon forecast, with limited clarity on how point-of-care and home testing revenues are separated from wider diagnostic services. |

| Industry Research House B | USD 28.99 B (2025) | Includes software and services as an explicit product bucket, which can lift totals depending on what is treated as recurring IVD revenue versus general lab informatics. |

Reading the three figures together, the main takeaway is that the market is being sized off similar end-demand, but accounting choices around add-on services and how pricing is carried forward can shift the headline number. By keeping the build traceable to country-level demand signals and clear inclusion rules, our estimate stays easier to reproduce and explain during decision-making.

Key Questions Answered in the Report

What is the projected value of the Europe in-vitro diagnostics market by 2031?

It is forecast to reach USD 39.44 billion by 2031.

Which test type is expanding fastest across Europe?

Molecular diagnostics is projected to grow at a 7.43% CAGR from 2026-2031.

How large is Germany's share of European diagnostics revenue?

Germany accounted for 24.76% of regional revenue in 2025.

Why are software and services growing quickly in European laboratories?

GDPR-compliant digital platforms, AI analysis, and subscription models are driving an 8.11% CAGR for software and services.

Which end-user setting shows the highest growth potential?

Home-care and point-of-care centers are forecast to expand at an 8.54% CAGR through 2031 as virtual-ward models scale.

What regulatory challenge currently slows device approvals?

Lengthy EU IVDR certification cycles, with 66% of devices still awaiting clearance in 2024, are creating market bottlenecks.

Page last updated on: