Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

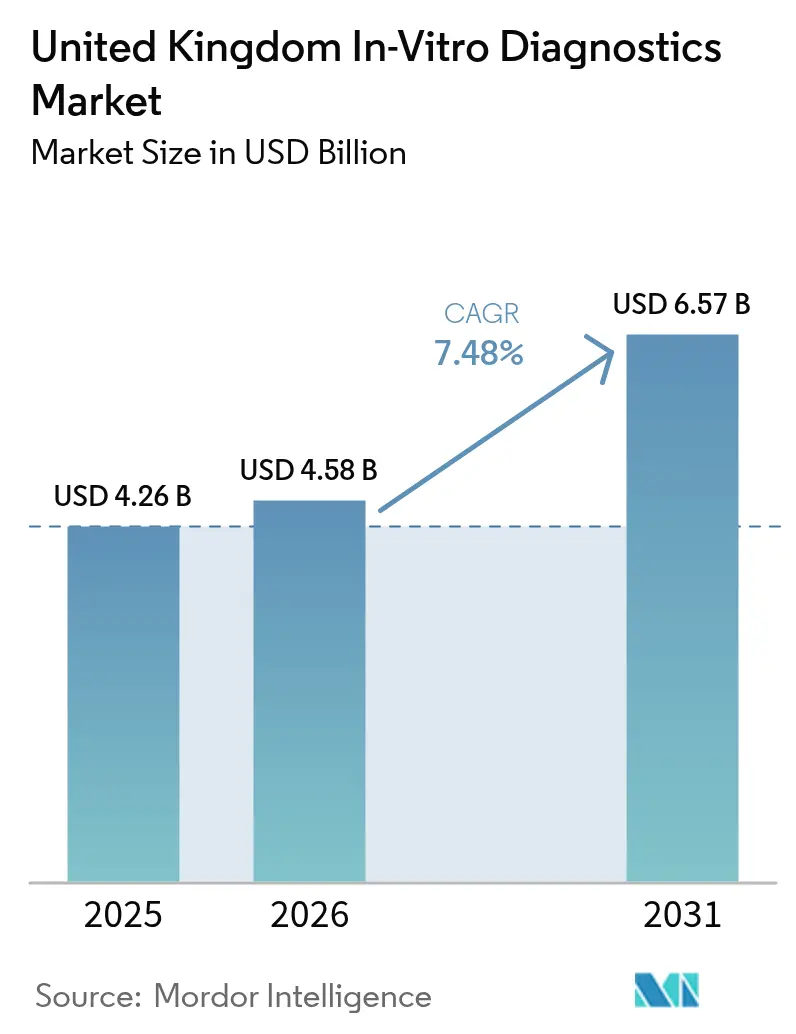

| Base Year Market Size (2025) | USD 4.26 Billion |

| Market Size (2026) | USD 4.58 Billion |

| Market Size (2031) | USD 6.57 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The United Kingdom In-Vitro Diagnostics Market size is expected to grow from USD 4.26 billion in 2025 to USD 4.58 billion in 2026 and is forecast to reach USD 6.57 billion by 2031 at 7.48% CAGR over 2026-2031.

The National Health Service (NHS) is prioritizing early detection in community settings, shifting test volumes from acute hospitals to primary-care clinics, pharmacies, and patient homes. Immuno-diagnostics maintains the largest market share, driven by high-volume cardiac and thyroid panels. However, molecular diagnostics is expanding at a faster pace, supported by the NHS Genomic Medicine Service's adoption of oncology, infectious disease, and pharmacogenomics workflows. Digital connectivity is a critical growth driver, with every new analyzer now equipped with middleware that uploads results to the Federated Data Platform, integrating laboratory data with prescribing and imaging records. Vendors delivering end-to-end solutions that combine hardware, reagents, and software services are enhancing their competitive position, as trusts increasingly value total cost of ownership and interoperability over initial capital expenditure.

Key Report Takeaways

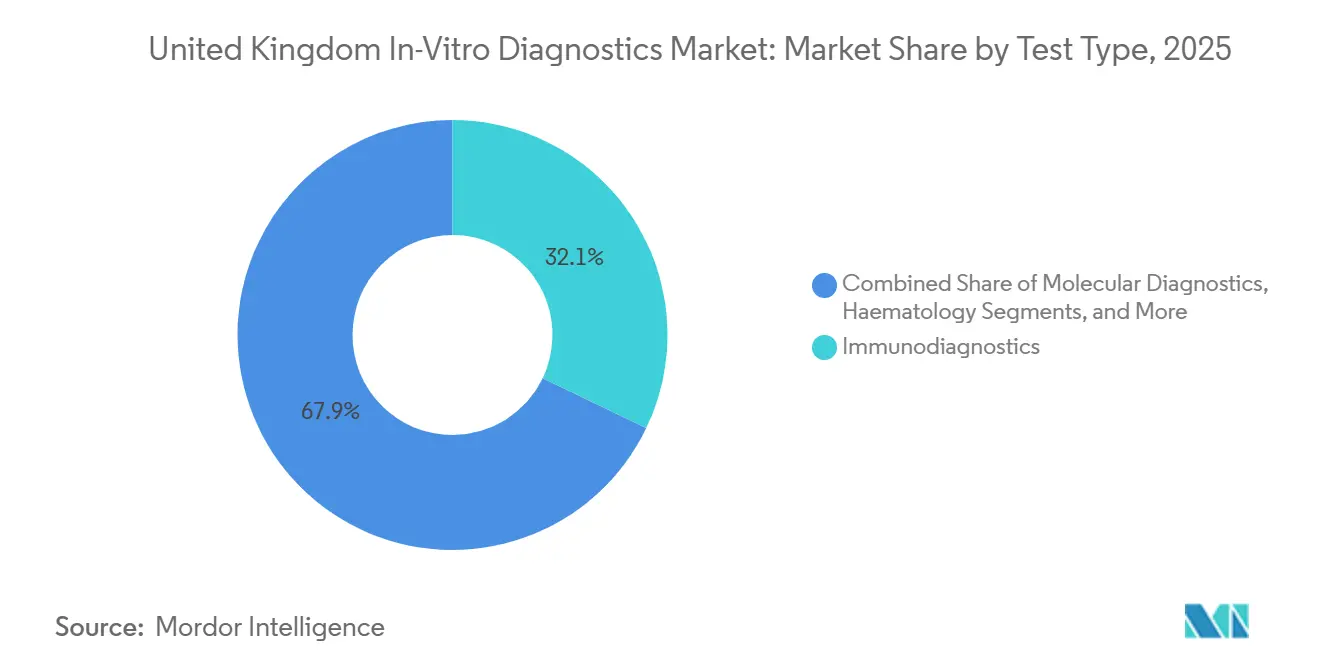

- By test type, immuno-diagnostics led with a 32.12% share of the United Kingdom in-vitro diagnostics market in 2025, while molecular diagnostics is forecast to expand at a 9.65% CAGR to 2031.

- By product, reagents and kits accounted for 65.10% of the United Kingdom in-vitro diagnostics market size in 2025; software and services are projected to grow at a 9.77% CAGR through 2031.

- By usability, disposable devices captured 80.32% of United Kingdom in-vitro diagnostics market share in 2025, whereas re-usable equipment is set to grow at a 10.21% CAGR to 2031.

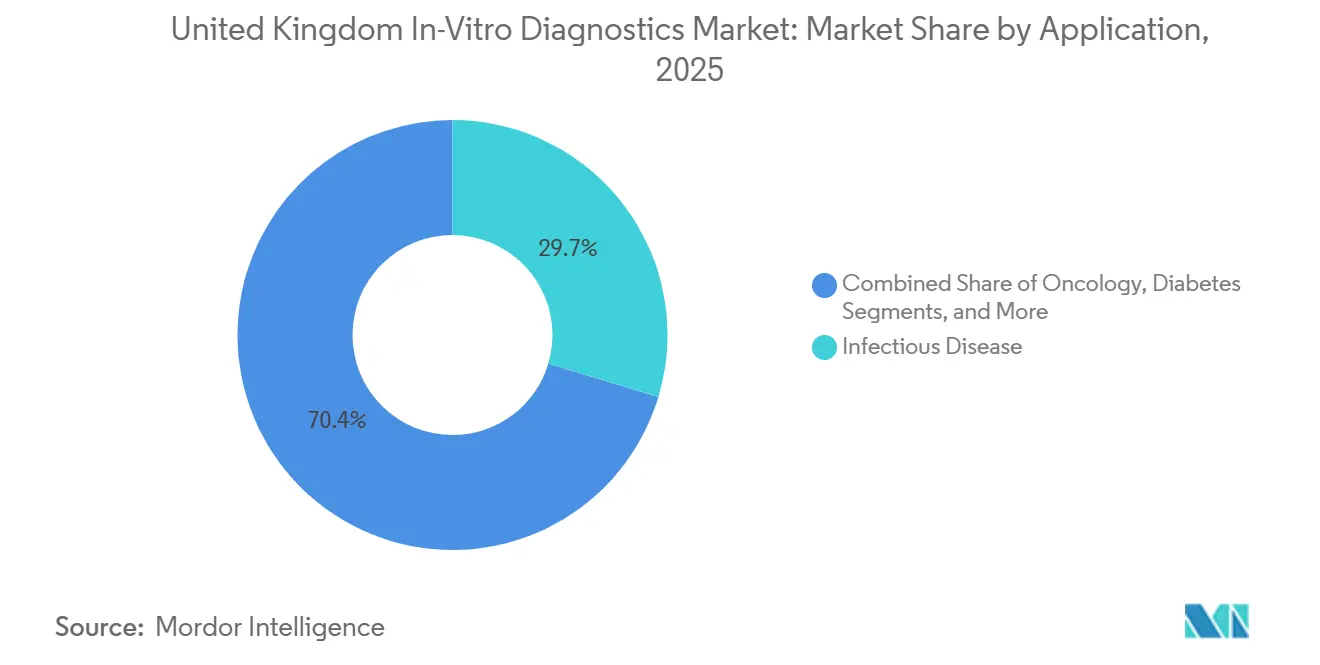

- By application, infectious-disease testing held 29.65% revenue share in 2025; oncology is the fastest growing application at a projected 10.43% CAGR to 2031.

- By end user, hospital laboratories represented 61.75% revenue share in 2025, yet home-care and self-testing are expected to rise at an 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic Diseases | +1.8% | National, with higher burden in North West England and West Midlands | Long term (≥ 4 years) |

| Ageing Population & Higher Comorbidity Burden | +1.5% | National, concentrated in coastal and rural areas | Long term (≥ 4 years) |

| Growing Adoption of Point-of-Care Testing | +1.4% | National, early gains in Community Diagnostic Centres and Pharmacy First sites | Medium term (2-4 years) |

| NHS 'Learning Healthcare System' Data Linkage Boosting Companion Dx Uptake | +1.2% | National, pilot trusts in Greater Manchester, London, and Yorkshire | Medium term (2-4 years) |

| Shift to Primary-Care Pharmacist-Led Screening Clinics Increasing Test Volumes | +1.0% | National, rapid expansion in urban and suburban areas | Short term (≤ 2 years) |

| Green NHS Procurement Mandates Driving Switch to Low-Waste Reagent Formats | +0.6% | National, compliance-driven across all NHS trusts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

One in four UK residents lived with at least one long-term condition in 2024, up from 23% five years earlier[1]Office for National Statistics, “Health State Life Expectancies,” ons.gov.uk. Diabetes is on course to reach 5.5 million cases by 2030, supporting sustained demand for HbA1c and renal-function assays. High-sensitivity troponin testing is now mandatory in every emergency department, a move that lifted immunoassay placements for Abbott, Roche, and Siemens. Integrated Care Systems reimburse vendors only when tests demonstrably lower cost per diagnosis, favoring platforms that auto-populate electronic health records with outcomes data. Autoimmune panels are also climbing because rheumatology waiting lists exceeded 500,000 in 2024, creating unmet diagnostic demand once clinical capacity improves.

Ageing Population and Higher Comorbidity Burden

The median UK age reached 40.7 years in 2024, and the over-65 cohort will grow by 1.8 million by 2031. More than half of seniors live with two or more chronic conditions, heightening the need for coagulation, metabolic, and infection testing. The Ageing Well strategy steers budgets toward rapid assays that nurses and pharmacists can perform without venipuncture. Dementia prevalence is edging toward 1 million cases, intensifying research into blood-based biomarkers that could triage patients for confirmatory imaging[2]Alzheimer’s Society UK, “Dementia UK Overview,” alzheimers.org.uk. Rural trusts coping with staffing gaps are installing consolidated laboratory hubs that courier specimens from satellite clinics, preserving turnaround times despite workforce constraints.

Growing Adoption of Point-of-Care Testing

Community Diagnostic Centres delivered 8 million tests in 2024, proof that diagnostics is leaving acute wards for retail settings. The Pharmacy First scheme alone created an estimated 500,000 extra rapid tests for common infections. Framework agreements now favor handheld devices that upload results over 4G or Wi-Fi, such as LumiraDx and Abbott i-STAT platforms. June 2025 MHRA guidance caps user-error rates at 2% for devices operated by non-laboratory staff, raising entry barriers for new brands. Middleware that funnels readings from disparate analyzers into a single dashboard is a secondary growth node because every integrated care system wants real-time population-health analytics.

NHS Learning Healthcare System Data Linkage Boosting Companion Dx Uptake

The Federated Data Platform links lab results, prescribing data, and genomic sequences, enabling automated prompts when essential companion diagnostics are missing. Whole-genome sequencing surpassed 100,000 cases by 2024 and is expanding into pharmacogenomics pilots. Eighteen oncology drugs now carry mandatory biomarker prerequisites, creating captive demand for Roche Ventana, Thermo Fisher Oncomine, and Illumina TruSight assays. Strict data-sovereignty rules require UK-hosted servers, complicating partnerships with U.S. software vendors. Retrospective linkage of test results to survival outcomes is also supplying the evidence base that NICE uses to approve novel assays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IVDR-Aligned Regulatory Stringency | -0.9% | National, affecting all device classes | Medium term (2-4 years) |

| Reimbursement Pressure on High-Cost Molecular Assays | -0.7% | National, concentrated in oncology and rare-disease pathways | Short term (≤ 2 years) |

| NHS Net-Zero Packaging Standards Disfavoring Legacy Plastic Cartridges | -0.4% | National, compliance-driven across procurement frameworks | Medium term (2-4 years) |

| Genomic Data Sovereignty Concerns Slowing Cloud-Based Bioinformatics Adoption | -0.3% | National, pilot trusts in Greater Manchester, London, Yorkshire | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IVDR-Aligned Regulatory Stringency

The December 2025 MHRA roadmap synchronizes UK rules with EU IVDR, compelling notified-body review for high-risk assays and demanding real-world data within 30 days of adverse events. Dual CE- and UKCA-mark compliance inflates launch costs by roughly GBP 200,000 per product. Post-market reporting needs three NHS trust datasets, a hurdle small firms struggle to clear. Annual revalidation for AI algorithms adds ongoing overhead. While incidents have dropped 18% since 2023, smaller innovators are delaying launches or exiting the market, trimming product variety by an estimated 12%.

Reimbursement Pressure on High-Cost Molecular Assays

NICE ruled in 2025 that liquid-biopsy monitoring exceeded the GBP 30,000 per QALY ceiling for most cancers, blocking routine coverage[3]National Institute for Health and Care Excellence, “Diagnostics Guidance: Liquid Biopsy,” nice.org.uk. Broad NGS panels cost up to GBP 2,500 each, straining the fixed GBP 500 million Genomic Medicine Service budget. Trusts now sign risk-sharing deals that pay vendors only if test results change treatment, slicing supplier margins by up to 20 points. The absence of unique reimbursement codes forces hospitals to absorb costs, restricting uptake to wealthier regions. Cheaper PCR or immunohistochemistry alternatives are filling the gap and slowing NGS growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Outpace Legacy Modalities

Molecular diagnostics, the fastest growing segment, is on track for a 9.65% CAGR that will outpace every other modality in the United Kingdom in-vitro diagnostics market. Immuno-diagnostics retains the largest 2025 share at 32.12%, but policy-driven genome sequencing programs are steering budgets toward next-generation sequencing, digital PCR, and isothermal amplification platforms. Investments in Community Diagnostic Centres also prioritize multiplex PCR panels that deliver pathogen results within 2 hours.

Growing sample throughput is reshaping instrument demand. High-sensitivity troponin rules have stabilized clinical chemistry volumes, while integrated hematology-coagulation solutions are gaining traction with consolidated lab hubs. Antimicrobial-resistance rules are pushing trusts to automate culture and susceptibility testing, swelling orders for bioMérieux and BD systems. These intertwined drivers ensure that the United Kingdom in-vitro diagnostics market size attached to molecular platforms will expand more quickly than any other modality, even though traditional assays will still dominate volume.

By Product: Software and Services Capture Recurring Revenue

Reagents and kits generated 65.10% of 2025 sales, yet software and services will grow nearly 10% each year as laboratories upgrade information systems to meet interoperability mandates. Trusts demand standardized APIs so results flow straight into electronic records, a shift that turns LIS upgrades into mandatory projects rather than discretionary purchases.

Vendors now bundle cloud analytics, AI decision support, and predictive maintenance into service contracts, creating annuity streams that cushion hardware cyclicality. Oxford Nanopore and Roche both charge per-sample bioinformatics fees, converting point sales into usage revenue. As more analyzers move to subscription or pay-per-test pricing, the United Kingdom in-vitro diagnostics market share linked to service models will climb even if reagent dominance persists.

By Usability: Re-Usable Equipment Gains on Sustainability Mandates

Single-use cartridges captured 80.32% revenue in 2025, yet carbon-footprint scoring is tilting new tenders toward durable analyzers with lower plastic waste. Green NHS criteria already award bonus points for closed-loop recycling pledges, steering hospitals to platforms that run millions of tests on the same core before disposal.

High-volume labs can now cut per-test consumable waste by 40% compared with cartridge-based systems, helping offset higher capital outlays. This dynamic should increase the United Kingdom in-vitro diagnostics market size attributable to re-usable equipment at a 10.21% CAGR, even as single-use devices stay dominant in home-care and small-clinic niches.

By Application: Oncology Diagnostics Surge on Early-Detection Pilots

Oncology is set to see the fastest 10.43% CAGR because multi-cancer early-detection pilots and liquid biopsy trials are moving from research to routine care. Interim Galleri data showed 99.5% specificity, and although early-stage sensitivity needs improvement, policymakers view the technology as complementary to established screening.

Infectious-disease testing still accounts for the largest 29.65% of revenue, driven by UKHSA surveillance and antibiotic-stewardship needs. Diabetes, cardiology, and autoimmune panels grow steadily on chronic-disease prevalence and ageing trends. Altogether, oncology’s acceleration will diversify the United Kingdom in-vitro diagnostics market share across more therapeutic areas, reducing dependence on respiratory tests that boomed during the pandemic.

By End User: Homecare and Self-Testing Users Gain Share

Hospital laboratories accounted for 61.75% of 2025 revenue but face slower growth as capacity shifts outward. Pharmacy First, Community Diagnostic Centres, and self-testing programs lift demand in retail and home settings. Continuous glucose monitors, INR meters, and self-administered flu kits illustrate new use cases where patients generate data without visiting a hospital.

Trusts still rely on centralized labs for complex molecular work, yet hub-and-spoke consolidation reduces the total number of labs while lifting throughput. The result is an 8.54% CAGR for home care and self-testing, which will increase their share of the United Kingdom in-vitro diagnostics market and ease pressure on hospital capacity.

Competitive Landscape

Market concentration is moderate; no supplier exceeds 15% share, and the top five combined hold roughly 55%. Roche leads high-throughput chemistry and immunohistochemistry through its cobas and Ventana lines, locking in consumable revenue with proprietary reagents. Abbott gains traction in decentralized care with Alinity and FreeStyle Libre, while Siemens Healthineers’ Atellica platform attracts hubs seeking chemistry, immunoassay, and hematology on a single track.

Danaher’s Beckman Coulter and Cepheid units dominate hematology and near-patient molecular testing, respectively. Local innovators add competitive tension: Oxford Nanopore supplies portable sequencers for outbreak genomics, LumiraDx sells pharmacy-focused immunoassay devices, and Genedrive offers 30-minute antibiotic-resistance panels. AI-driven cytology from Hologic and digital pathology by Philips promise efficiency gains but still await NICE reimbursement guidance.

Regulation shapes rivalry. The 2025 MHRA roadmap extends grace for CE-marked products until 2030, an advantage for incumbents that already hold both CE and UKCA files. Procurement is fragmenting as 160 Community Diagnostic Centres and thousands of pharmacies buy equipment suited to small spaces, giving agile vendors a foothold. Sustainability scoring also tilts awards toward suppliers with carbon-footprint audits and take-back schemes.

United Kingdom In-Vitro Diagnostics Industry Leaders

Thermo Fisher Scientific Inc.

Siemens Healthineers AG

Abbott Laboratories

QIAGEN N.V.

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Oxford Nanopore Technologies announced that the GridION Dx received CE and UKCA marks, making it the company's first IVD device registered in the UK and Europe. This certification confirms the device's compliance with international quality and safety standards, supporting its use in regulated clinical markets.

- March 2025: The NIHR launched the HealthTech Research Centre for In Vitro Diagnostics to accelerate innovation and adoption of diagnostic tools, focusing on cancer, infectious diseases, and primary care, supported by Imperial College London. The Centre aims to bridge the gap between research and clinical practice, fostering collaboration among industry, academia, and healthcare.

United Kingdom In-Vitro Diagnostics Market Report Scope

As per the scope of this report, in-vitro diagnostics as medical devices and consumables used to conduct tests on biological samples outside a living organism. These diagnostics play a crucial role in identifying medical conditions, including diabetes and cancer.

The United Kingdom's in-vitro diagnostics market is categorized by technique, product type, usability, application, and end user. Techniques include clinical chemistry, molecular diagnostics, immunodiagnostics, and other methods such as hematology, microbiology, and urinalysis. Product segmentation encompasses instruments, reagents, and additional items. Usability divides the market into disposable and reusable IVD devices. Applications range from infectious diseases, diabetes, and cancer/oncology to cardiology, endocrinology, and genetic testing. End users include diagnostic laboratories, hospitals, clinics, and other entities, such as clinical laboratories and academic institutions. The report provides market values (in USD) for each segment.

By Test Type

| Clinical Chemistry |

| Immuno-Diagnostics |

| Molecular Diagnostics |

| Hematology |

| Coagulation |

| Microbiology |

| Other Test Types |

By Product

| Instruments |

| Reagents & Kits |

| Software & Services |

By Usability

| Disposable IVD Devices |

| Re-Usable Equipment |

By Application

| Infectious Diseases |

| Diabetes |

| Oncology |

| Cardiology |

| Auto-Immune Disorders |

| Nephrology |

| Other Applications |

By End User

| Stand-Alone Laboratories |

| Hospital-Based Laboratories |

| Point-Of-Care Settings |

| Home-Care & Self-Testing Users |

| By Test Type | Clinical Chemistry |

| Immuno-Diagnostics | |

| Molecular Diagnostics | |

| Hematology | |

| Coagulation | |

| Microbiology | |

| Other Test Types | |

| By Product | Instruments |

| Reagents & Kits | |

| Software & Services | |

| By Usability | Disposable IVD Devices |

| Re-Usable Equipment | |

| By Application | Infectious Diseases |

| Diabetes | |

| Oncology | |

| Cardiology | |

| Auto-Immune Disorders | |

| Nephrology | |

| Other Applications | |

| By End User | Stand-Alone Laboratories |

| Hospital-Based Laboratories | |

| Point-Of-Care Settings | |

| Home-Care & Self-Testing Users |

Key Questions Answered in the Report

How fast will molecular diagnostics sales grow in the United Kingdom?

Molecular diagnostics revenue is projected to climb at a 9.65% CAGR through 2031, the quickest pace among all test types, as genome sequencing expands beyond rare diseases into oncology and infectious-disease care.

Which application area should suppliers target for the strongest expansion?

Oncology diagnostics is forecast to grow at 10.43% a year because multi-cancer early-detection pilots and companion-diagnostic mandates are increasing test volumes.

What share of revenues come from reagents and kits?

Reagents and kits produced 65.10% of 2025 sales, underlining the consumable-heavy nature of laboratory and point-of-care testing.

How are sustainability rules affecting device selection?

Green NHS procurement scores penalize high-waste cartridges, prompting trusts to favor re-usable analyzers and recyclable packaging that help suppliers win tenders.

Will pharmacies keep gaining diagnostic responsibilities?

Yes, Pharmacy First allows pharmacists to order tests for seven common conditions without GP referral, and this policy is lifting home-care and point-of-care device demand at an 8.54% CAGR.

How large is the United Kingdom in-vitro diagnostics market in 2026?

The United Kingdom in-vitro diagnostics market is expected to grow from USD 4.58 billion in 2026 and is forecast to reach USD 6.57 billion by 2031.

Page last updated on: