Hepatitis E Diagnostic Tests Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 70.71 Million |

| Market Size (2031) | USD 92.67 Million |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

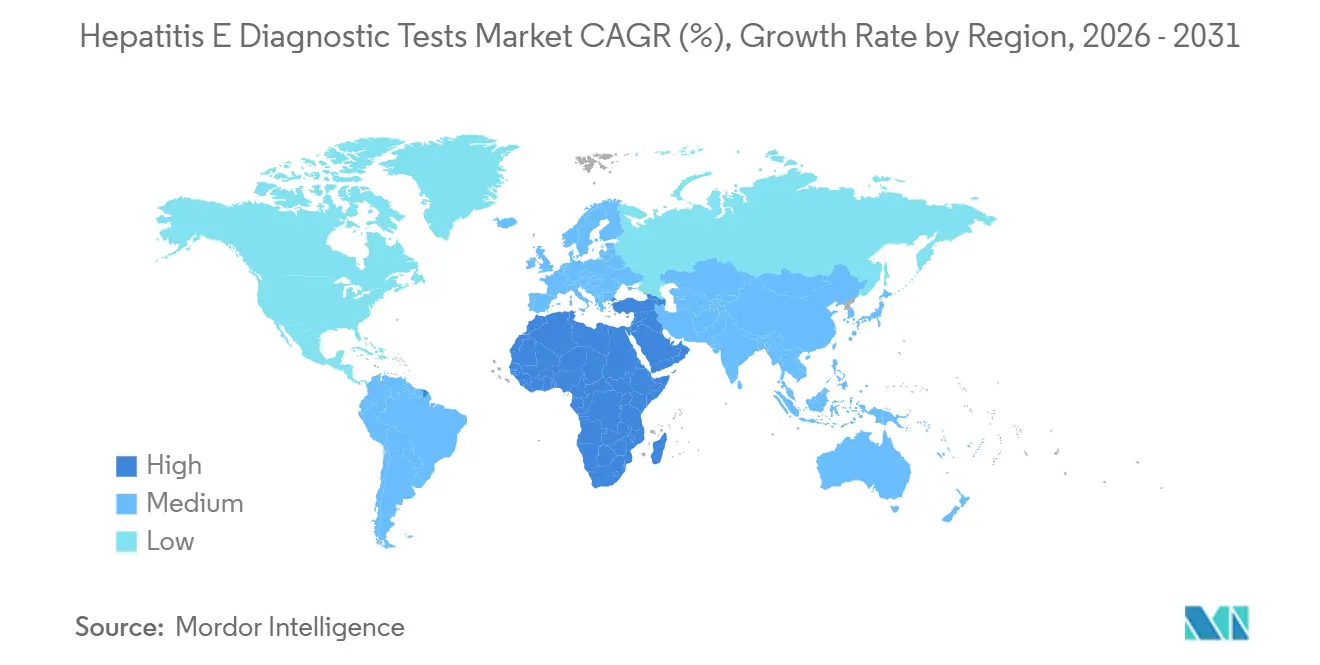

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

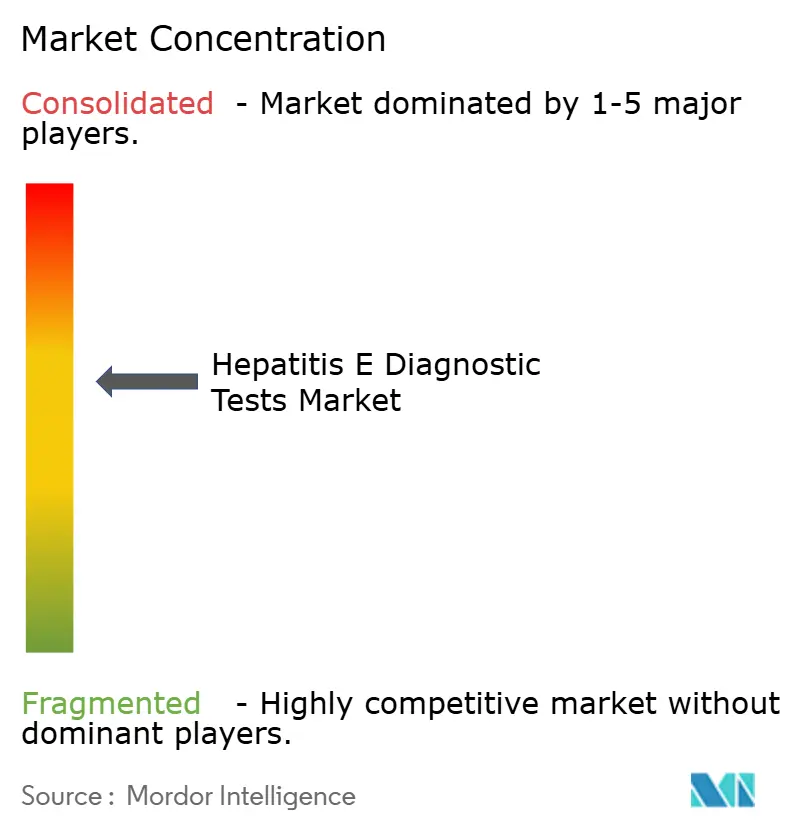

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hepatitis E Diagnostic Tests Market Analysis by Mordor Intelligence

The Hepatitis E Diagnostic Tests Market size is estimated at USD 70.71 million in 2026, and is expected to reach USD 92.67 million by 2031, at a CAGR of 5.56% during the forecast period (2026-2031).

Rising blood-safety mandates in high-income regions, recurrent waterborne outbreaks in humanitarian settings, and incremental gains in molecular-assay automation are steering demand away from single-step antibody screening toward high-throughput nucleic-acid platforms. ELISA remains the dominant surveillance workhorse in Asia-Pacific hospitals, but its share is edging downward as blood banks adopt multiplex NAT cartridges that simultaneously detect HEV, HIV, HBV, and HCV, trimming per-donation costs. Price-sensitive outbreak markets continue to favor IgM lateral-flow strips that do not require cold-chain logistics. Meanwhile, environmental surveillance programs are adding stool PCR to wastewater and food-safety workstreams, expanding testing beyond clinical laboratories. Consolidation is accelerating: Bruker’s 2024 acquisition of ELITechGroup illustrates the capital scale now required to meet new European validation rules for blood-bank assays[1]Bruker Corporation, “Acquisition of ELITechGroup,” BRUKER.COM .

Key Report Takeaways

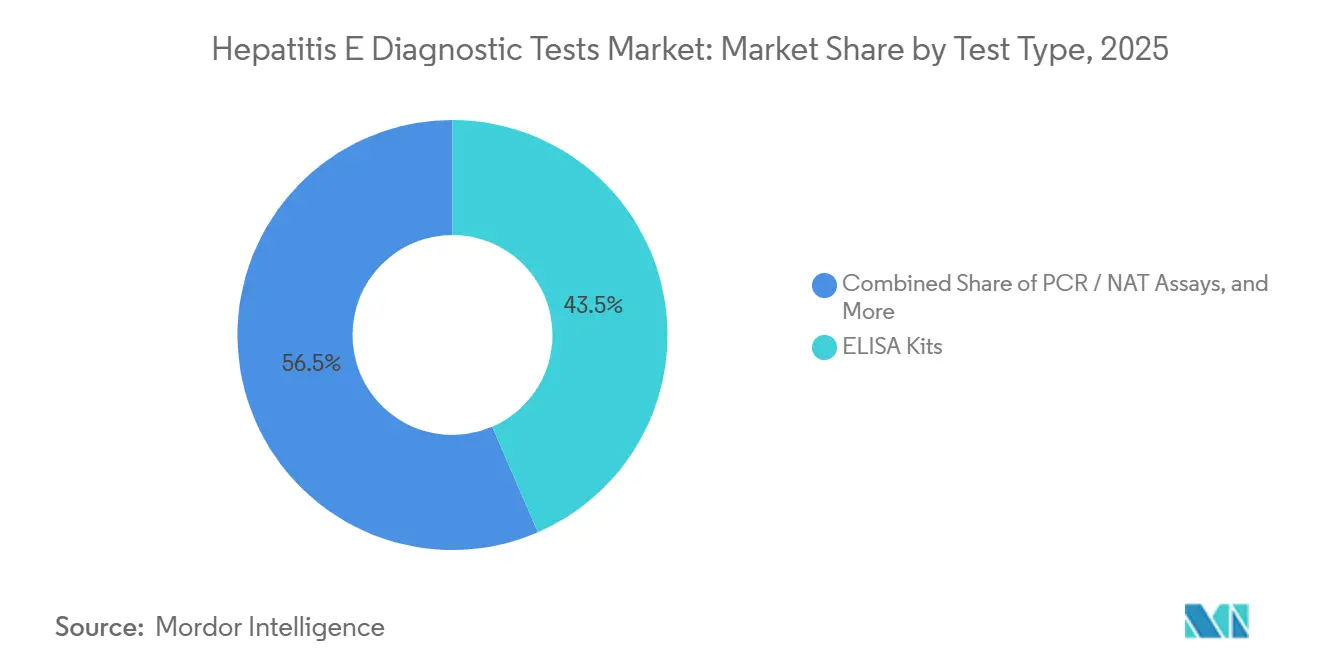

- By test type, ELISA kits held 43.55% of the Hepatitis E Diagnostic Tests market share in 2025, while PCR/NAT assays are forecast to advance at an 8.25% CAGR through 2031.

- By sample type, serum and plasma accounted for 70.53% of the Hepatitis E Diagnostic Tests market in 2025; stool testing is set to expand at a 9.85% CAGR through 2031.

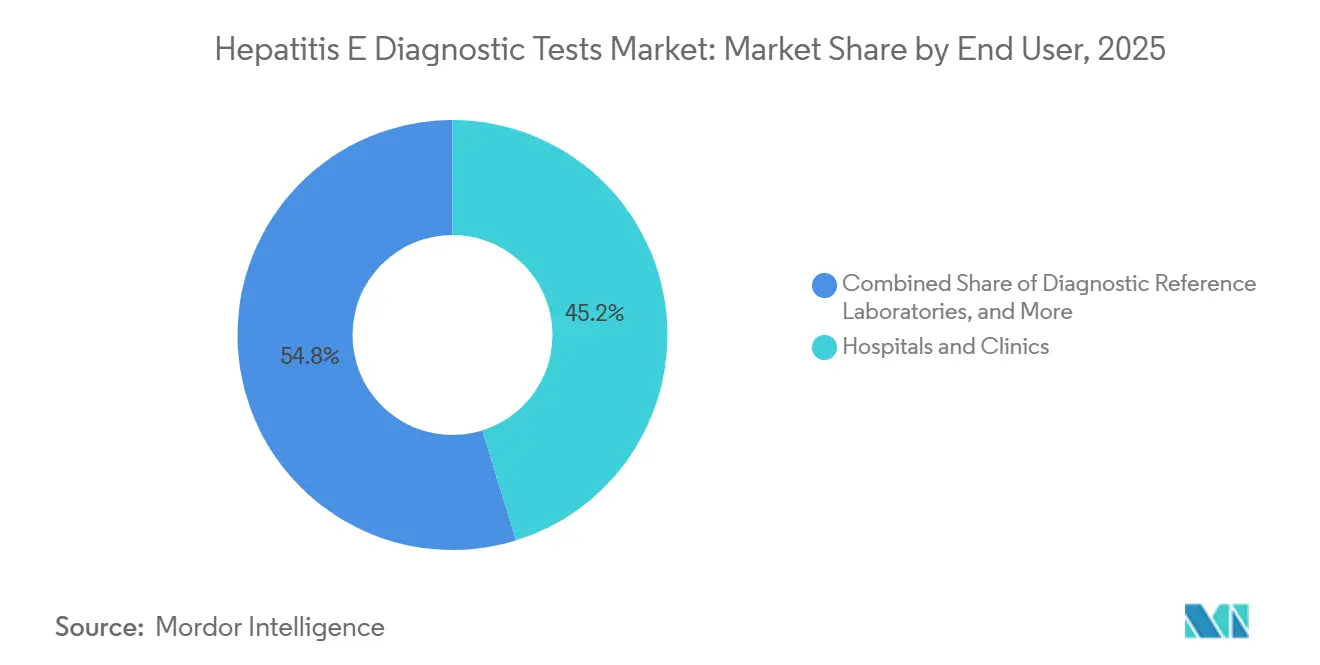

- By end user, hospitals and clinics led with 45.23% revenue share in 2025, whereas blood banks and transfusion centers are projected to grow at an 8.55% CAGR over the same period.

- By geography, Asia-Pacific contributed 38.13% of global revenue in 2025; the Middle East and Africa segment is poised for a 10.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hepatitis E Diagnostic Tests Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of HEV Outbreaks in Endemic Regions | +1.2% | Sub-Saharan Africa, South Asia, with spillover to Middle East refugee corridors | Short term (≤ 2 years) |

| Growing Blood-Safety Screening Mandates in Europe | +1.5% | Western Europe (UK, Ireland, Spain), expanding to Central and Eastern Europe | Medium term (2-4 years) |

| Technological Advances in Molecular Diagnostics | +1.0% | Global, with early adoption in North America, Western Europe, and Japan | Medium term (2-4 years) |

| Adoption of HEV Testing in Xenotransplantation Research | +0.3% | North America, select EU research hubs (Germany, Netherlands) | Long term (≥ 4 years) |

| Multiplex Travel-Medicine Panels Incorporating HEV | +0.4% | North America, Western Europe, Australia (high outbound travel markets) | Medium term (2-4 years) |

| Prenatal Screening Protocols in High-Risk Countries | +0.6% | South Asia (India, Bangladesh), Sub-Saharan Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of HEV Outbreaks in Endemic Regions

Waterborne outbreaks in refugee camps across Chad and Namibia shifted sporadic testing to year-round procurement of rapid IgM strips, with more than 5,000 confirmed cases reported between 2024 and 2025 alone[2]World Health Organization, “WHO Essential Diagnostics List 2023,” WHO.INT. Monsoon flooding in India’s Bihar and Odisha states produced localized surges that overwhelmed municipal laboratories, prompting emergency tenders for shelf-stable diagnostics that do not require electricity or refrigeration. The World Health Organization’s 2023 Essential Diagnostics List now prequalifies rapid HEV assays from Wantai and MP Diagnostics, validating field performance above 82% sensitivity and near-perfect specificity. Manufacturers capable of delivering single-use cartridges in fewer than 15 minutes have captured most outbreak-response budgets, narrowing opportunities for batch-processed ELISA kits in low-resource settings. The trend is expected to keep first-line testing focused on lateral-flow strips, while confirmatory workloads shift to regional hubs equipped with NAT instruments.

Growing Blood-Safety Screening Mandates in Europe

The European Union’s Regulation 2024/1938 now obliges blood establishments to validate assays against WHO International Standards covering HEV genotypes 1-4[3]European Commission, “Regulation (EU) 2024/1938 on Substances of Human Origin,” EUR-LEX.EUROPA.EU. The United Kingdom, France, and Spain already run universal donor screening; Germany and Poland are piloting selective protocols for high-risk recipients. Roche’s Elecsys and Grifols’ Procleix systems dominate these high-throughput environments by delivering multiplex results in 18 minutes or less and reducing false-positive callbacks[4]Roche Diagnostics, “Elecsys Anti-HEV IgM and IgG Assays,” ROCHE.COM. Compliance costs are likely to push smaller regional blood banks toward outsourcing NAT or joining consortia that share analyzer capacity. Consequently, the Hepatitis E Diagnostic Tests market is expected to see sustained instrument placements through 2028, even as per-test margins tighten under bulk-purchase contracts.

Technological Advances in Molecular Diagnostics

Pocket-sized analyzers are shrinking the infrastructure gap between ELISA and PCR. Northwestern University’s DASH prototype delivered a 15-minute HEV PCR using microfluidics and smartphone readout in December 2025. The FDA’s June 2024 clearance of Cepheid’s Xpert HCV set a predicate for point-of-care viral-load approvals, encouraging similar submissions for HEV. Digital droplet PCR and RT-LAMP are being adopted for wastewater monitoring, enabling municipalities to forecast spikes days before clinical presentation. Vendors that integrate extraction, amplification, and detection into sealed cartridges can sidestep the skilled-technician bottleneck that constrains NAT penetration in district hospitals.

Adoption of HEV Testing in Xenotransplantation Research

Vertical transmission studies in swine herds showed persistent HEV RNA in newborn piglets, forcing academic transplant programs to schedule serial NAT screens across breeding colonies. The FDA’s draft xenotransplantation guidance and similar European frameworks require validated, genotype-specific assays for donor animals, leading niche laboratories to pay premium list prices. Although test volumes are modest, per-sample revenues are 5 to 8 times higher than in routine clinical diagnostics, creating a profitable niche for assay makers with R&D bandwidth to customize panels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Awareness and Under-Reporting in Endemic Areas | -0.7% | South Asia (India, Bangladesh, Nepal), Sub-Saharan Africa, parts of Southeast Asia and Latin America | Short term (≤ 2 years) |

| Price Sensitivity and Limited Reimbursement | -0.5% | Global, most acute in low- and middle-income countries (Sub-Saharan Africa, South Asia) and U.S. commercial insurance markets | Medium term (2-4 years) |

| Cross-Reactivity Causing False-Positive Concerns | -0.4% | Global, particularly in low-prevalence populations (North America, Western Europe, Australia) | Medium term (2-4 years) |

| Porcine Supply-Chain Shocks Constraining Reagent Supply | -0.3% | Global manufacturing hubs (Europe, North America, China), with downstream impact on procurement in all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Awareness and Under-Reporting in Endemic Areas

In many endemic nations, clinicians still default to hepatitis A presumptions when confronted with acute jaundice, leading to test rates that capture fewer than 20% of suspected HEV cases during outbreaks. The absence of compulsory HEV case reporting disrupts data feedback loops that might otherwise justify budget lines for diagnostics. Until national medical curricula differentiate HEV genotypes and transmission routes, test-volume growth will trail true disease incidence, trimming roughly 0.7 percentage points off the forecast CAGR.

Price Sensitivity and Limited Reimbursement

Aetna’s 2024 bulletin limits HEV PCR reimbursement to antibody-positive patients, excludes routine prenatal or transplant screening, and forces U.S. labs to bill under generic viral-load codes, which are often denied. In LMICs, a USD 10 ELISA outprices the daily earnings of many at-risk households, and public budgets prioritize HIV, malaria, and tuberculosis diagnostics. Manufacturers face tightening margins as they juggle high-price, low-volume molecular sales in high-income markets against commodity-priced rapid-test tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Assays Gain Ground Despite ELISA Dominance

ELISA continued to account for 43.55% of the Hepatitis E Diagnostic Tests market revenue in 2025, supported by hospital laboratories that batch-process high sample volumes at low variable costs. Roche’s Elecsys Anti-HEV IgM delivers 18-minute results on an installed base of more than 8,000 cobas analyzers worldwide, giving incumbent suppliers substantial channel reach. Grifols’ Procleix NAT assay is expanding its presence in blood centers, and its ability to detect HEV RNA alongside HIV, HBV, and HCV is accelerating multiplex uptake at an 8.25% CAGR. Rapid lateral-flow kits remain indispensable for outbreak response: Wantai’s WHO-listed strip produces a visual readout in 15 minutes and retails near USD 1.50 for bulk orders.

Pressure is mounting for ELISA manufacturers to innovate. Digital ELISA platforms that amplify signals via nanoparticle conjugates promise a four-fold increase in sensitivity, enabling earlier detection after exposure; however, capital costs near USD 200,000 per analyzer limit uptake to tertiary centers. The Hepatitis E Diagnostic Tests industry is therefore bifurcating: molecular vendors chase high-margin transfusion accounts, while lateral-flow specialists compete on cost and shelf life for humanitarian tenders. The “Others” category—Western blot confirmation and RUO genotyping kits—retains relevance in reference virology laboratories but commands less than 5% of the value pool

By Sample Type: Stool Testing Emerges as Fastest-Growing Segment

Serum and plasma accounted for 70.53% of the Hepatitis E Diagnostic Tests market in 2025, aligning with standard acute hepatitis workflows. ELISA and chemiluminescence assays integrate seamlessly into existing serum analyzers, keeping variable cost per test below USD 5 in high-volume settings. Stool testing is the fastest-growing segment, expanding at 9.85% CAGR as municipalities add HEV RNA to wastewater dashboards that already track poliovirus and norovirus. Food-safety laboratories are also embracing fecal-matrix PCR to certify pork and shellfish batches under tightened EU and USDA guidelines.

Advances in nucleic-acid stabilization media now allow stool samples to remain analyzable for up to 72 hours at ambient temperature, a game-changer for rural clinics without cold-chain infrastructure. The Hepatitis E Diagnostic Tests market, therefore, stands to benefit from cross-sector demand, as environmental programs procure the same extraction cartridges used in clinical virology. Saliva and urine remain investigational matrices, but early data suggest sensitivity comparable to serum within the first week of symptom onset, hinting at future self-collection kits for telehealth workflows.

By End User: Blood Banks Accelerate Adoption Amid Transfusion-Safety Mandates

Hospitals and clinics remained the top revenue generators, with a 45.23% share in 2025, leaning heavily on batch ELISA formats that exploit existing immunochemistry automation. However, blood banks and transfusion centers exhibited the fastest trajectory, marching at an 8.55% CAGR as jurisdictions from Japan to Ireland enforce universal NAT screening. The shift obliges centers to install high-throughput analyzers and secure stable reagent pipelines, favoring multinational vendors that can bundle service contracts and integrate LIMS remotely.

Diagnostic reference laboratories occupy a resilient mid-tier, capturing send-out testing that smaller hospitals cannot perform in-house. ARUP and Mayo Clinic Laboratories manage complex genotyping and viral-load quantification, tapping into transplant-recipient and chronic-infection niches. Environmental and food-testing labs form the “Other End Users” bucket, a small but growing cohort spurred by European Food Safety Authority mandates to certify pork supply chains against HEV contamination.

Geography Analysis

Asia-Pacific retained leadership with 38.13% of global revenues in 2025, propelled by China’s extensive ELISA base and Japan’s universal donor NAT screening. Wantai’s WHO-prequalified kits dominate governmental procurements, while BGI Genomics leverages NGS panels to win contracts at provincial CDCs. India’s endemic burden is high but underdiagnosed; fewer than 20% of suspected acute hepatitis cases received HEV serology in 2025, signaling latent demand once awareness programs mature.

Europe ranked second, underpinned by the United Kingdom's blood services that detect approximately 1 HEV-positive unit per 10,000 donations. The new Regulation 2024/1938 raises assay-validation costs, but harmonizes NAT quality across member states, fostering a predictable reimbursement climate. Germany and France apply selective donor screening, focusing on immunocompromised recipients, while Spain and Ireland run universal programs.

The Middle East and Africa segment is the growth engine, forecasting a 10.81% CAGR through 2031 as refugee-camp outbreaks compel Ministries of Health to stockpile rapid strips. South Africa’s National Health Laboratory Service is upgrading provincial PCR capacity in response to urban clusters linked to informal settlements. Gulf Cooperation Council states report imported genotype-1 cases among expatriate workers, leading private hospitals to adopt multiplex travel panels.

North America remains smaller, as the United States lacks universal donor screening and HEV incidence stays low outside genotype-3 zoonotic exposures in pork consumers. Canada is reviewing cost-benefit scenarios for selective screening of immunosuppressed patients, but no mandates exist yet. Latin America sees episodic activity; Brazil’s health authorities deploy HEV IgM strips during flood-related outbreaks, while Argentina integrates HEV PCR into sentinel surveillance at abattoirs.

Competitive Landscape

The Hepatitis E Diagnostic Tests market shows moderate fragmentation: no firm exceeds a significant percentage of global revenue, yet scale advantages are tilting leadership toward a handful of multinationals. Bruker’s EUR 870 million takeover of ELITechGroup in May 2024 signaled escalating capital thresholds for assay development under stricter EU validation rules. Wantai Biological Pharmacy leverages cost leadership and WHO prequalification to dominate public tenders in LMICs, often bundling rapid strips and ELISA reagents at tiered pricing.

Roche and bioMérieux defend premium hospital segments through analyzer integration and LIS connectivity, offering 30-minute IgM/IgG chemiluminescence protocols that mesh with existing cobas and VIDAS fleets. Grifols wins blood-bank share with its Procleix multiplex NAT, and the company recently announced remote-troubleshooting software that cuts downtime by 25%, further entrenching its installed base.

Emerging disruptors cluster in two camps. Chinese NGS houses such as BGI Genomics undercut Western list prices by up to 30% while bundling HEV genotyping with broader pathogen panels, appealing to provincial public health labs. Rapid-test specialists like Biopanda and Healgen upgraded cassette designs in 2025, shortening read time to 10-15 minutes and improving sensitivity above 99%. Point-of-care NAT remains under-served; Northwestern University’s DASH prototype highlights untapped potential for instrument-free molecular cartridges capable of delivering PCR-grade accuracy at the bedside.

Regulatory compliance is emerging as a moat. The EU’s genotype-validation requirement and WHO traceability standards favor firms with deep clinical-trial budgets and global quality-management systems, creating acquisition targets among smaller serology manufacturers that lack resources to navigate multilayered approvals.

Hepatitis E Diagnostic Tests Industry Leaders

Abbott Laboratories

Bio-Rad Laboratories Inc.

QIAGEN N.V.

Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Bioars S.A. introduced single-test ELISA kits for the Alegria and Alegria 2 systems, covering hepatitis E IgG and IgM antibodies.

- May 2024: Bruker finalized the EUR 870 million acquisition of ELITechGroup, adding molecular-diagnostic production capacity and broadening its infectious-disease assay catalogue

Global Hepatitis E Diagnostic Tests Market Report Scope

As per the report's scope, hepatitis E diagnostics refers to laboratory methods used to detect infection caused by the hepatitis E virus (HEV), which primarily affects the liver and is commonly transmitted through contaminated water or food. Diagnosis is mainly based on serological tests that identify anti-HEV IgM and IgG antibodies in blood, indicating recent or past infection. Molecular tests, such as RT-PCR, are also used to detect HEV RNA for early and confirmatory diagnosis. These tests help clinicians confirm infection, monitor outbreaks, and guide appropriate patient management.

The hepatitis E diagnostic tests market segmentation includes test type, sample type, end user, and geography. By test type, the market is segmented into ELISA kits, PCR / NAT assays, rapid lateral-flow tests, and others. By sample type, the market is segmented into serum/plasma, stool, and other. By end user, the market is segmented into hospitals & clinics, diagnostic reference laboratories, blood banks & transfusion centers, and other end users. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| ELISA Kits |

| PCR / NAT Assays |

| Rapid Lateral-Flow Tests |

| Others |

| Serum / Plasma |

| Stool |

| Other Sample Types |

| Hospitals & Clinics |

| Diagnostic Reference Laboratories |

| Blood Banks & Transfusion Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | ELISA Kits | |

| PCR / NAT Assays | ||

| Rapid Lateral-Flow Tests | ||

| Others | ||

| By Sample Type | Serum / Plasma | |

| Stool | ||

| Other Sample Types | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Reference Laboratories | ||

| Blood Banks & Transfusion Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What drives new product launches in the Hepatitis E Diagnostic Tests market?

Blood-safety mandates and rising outbreak frequency reward assays that shorten turnaround times and multiplex HEV with other pathogens.

Which test format is growing fastest?

PCR/NAT assays are expanding at an 8.25% CAGR as blood banks migrate to genotype-specific RNA detection.

Why is stool PCR gaining attention?

Wastewater and food-safety programs use stool-matrix PCR to forecast community transmission, pushing this sample type toward a 9.85% CAGR.

How are European regulations affecting suppliers?

Regulation 2024/1938 imposes genotype validation and WHO standard traceability, raising compliance costs and spurring consolidation.

What limits adoption in endemic countries?

Low clinical awareness and patient price sensitivity curb routine testing despite high disease burden.

Page last updated on: