Neglected Tropical Diseases Diagnosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

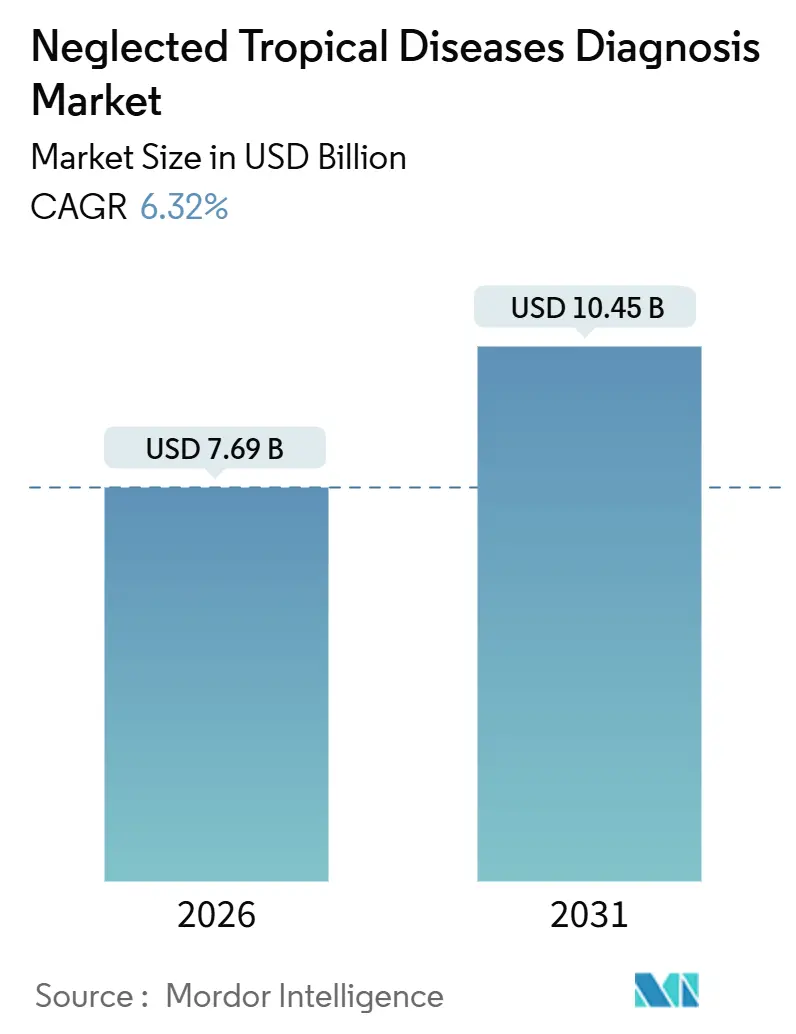

| Market Size (2026) | USD 7.69 Billion |

| Market Size (2031) | USD 10.45 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

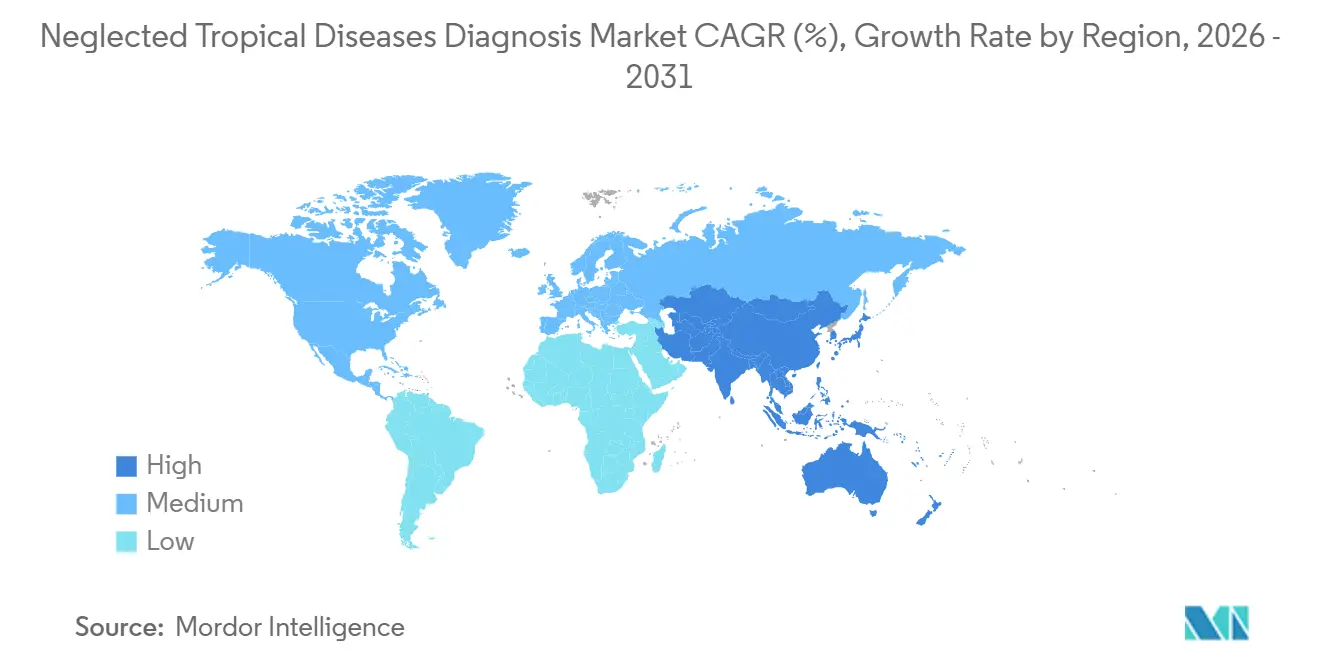

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neglected Tropical Diseases Diagnosis Market Analysis by Mordor Intelligence

The Neglected Tropical Diseases Diagnosis Market size is estimated at USD 7.69 billion in 2026, and is expected to reach USD 10.45 billion by 2031, at a CAGR of 6.32% during the forecast period (2026-2031).

Persistent case growth in dengue, Chagas disease, and lymphatic filariasis is widening the diagnostic addressable pool, while milestone-driven funding from multilateral agencies and the maturation of CRISPR and isothermal platforms are shortening development cycles. Commercial competition is shifting toward multiplex cartridges that bundle several arboviruses into one assay, compressing per-pathogen costs and simplifying procurement decisions for ministries of health. Reference laboratories in urban hubs still dominate complex workflows, yet portable PCR and lateral-flow cassettes are reducing result turnaround from days to hours in remote settings, creating new revenue corridors for suppliers that meet WHO prequalification thresholds. Regionally, North America captures premium innovation spend despite low endemicity, whereas Asia-Pacific is growing fastest as India and Indonesia expand district-level hubs and harmonize vector-surveillance protocols.

Key Report Takeaways

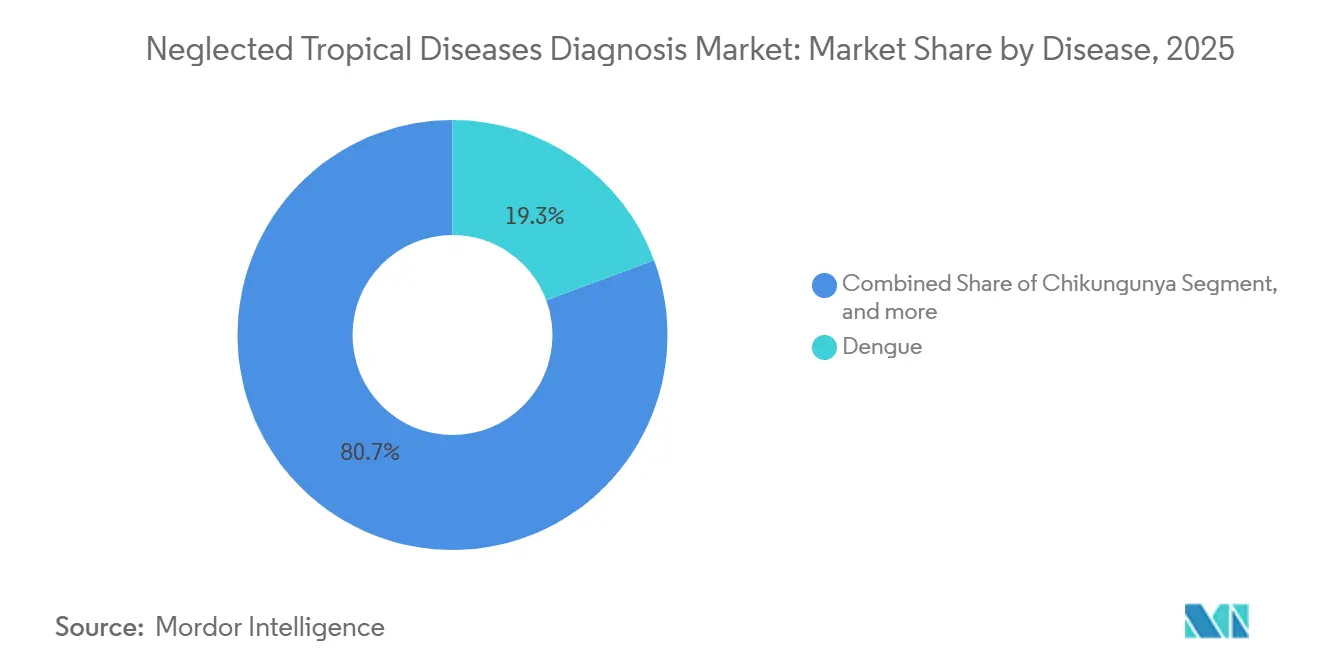

- By disease, dengue led with 19.34% revenue share in 2025; lymphatic filariasis diagnostics are advancing at an 8.54% CAGR through 2031.

- By diagnostic method, conventional techniques captured 54.43% share of the neglected tropical diseases diagnosis market in 2025, while molecular and modern methods are climbing at an 8.65% CAGR to 2031.

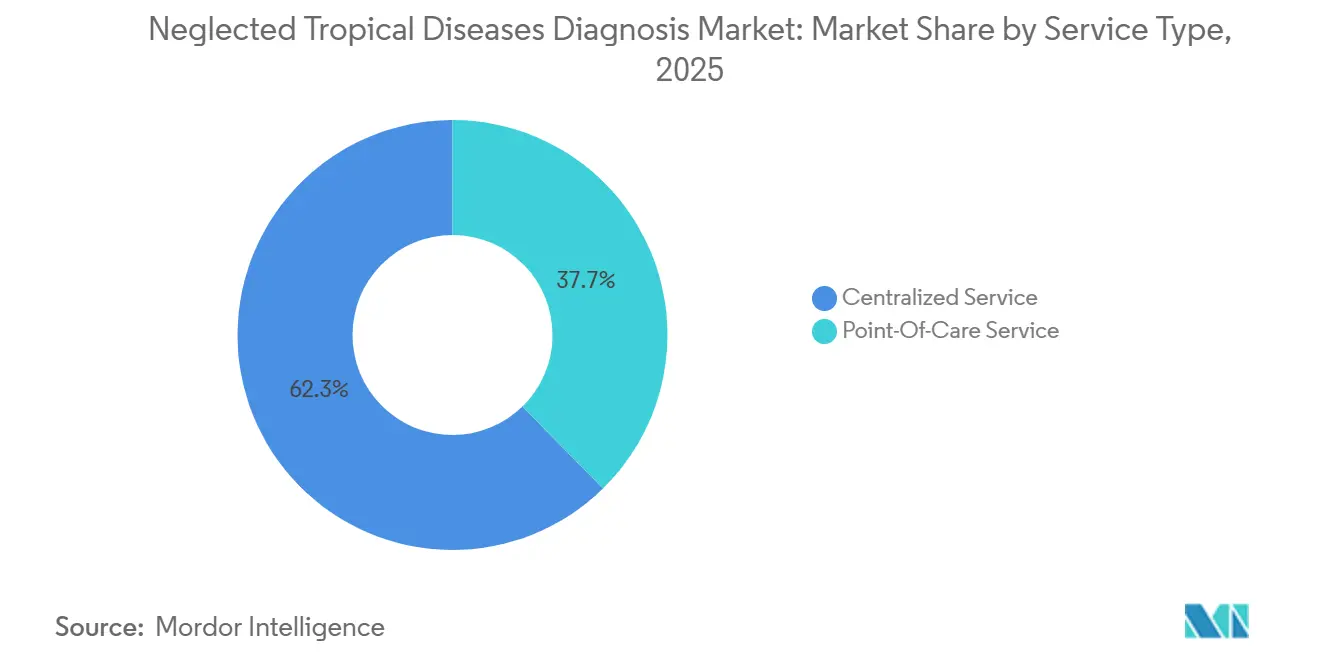

- By service type, centralized laboratories held 62.34% of 2025 volume, whereas point-of-care services are expanding at a 9.65% CAGR through 2031.

- By end user, clinical laboratories accounted for 48.43% demand in 2025; hospitals and clinics are posting a 9.86% CAGR to 2031.

- By geography, North America commanded 41.43% neglected tropical diseases diagnosis market share in 2025; Asia-Pacific is registering the highest 7.54% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neglected Tropical Diseases Diagnosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing burden of neglected tropical diseases | +1.2% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Strengthening global health initiatives and funding | +1.0% | WHO African and South-East Asia regions | Long term (≥ 4 years) |

| Technological advancements in diagnostic platforms | +1.1% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Expansion of healthcare infrastructure in endemic regions | +0.9% | Asia-Pacific, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Growing adoption of point-of-care testing solutions | +1.0% | India, Brazil, Nigeria | Medium term (2-4 years) |

| Emergence of integrated digital disease-surveillance systems | +0.8% | Asia-Pacific, East Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Neglected Tropical Diseases

Dengue infections surpassed 6.5 million cases in the Americas during 2024, tripling the prior-year count as El Niño rainfall expanded Aedes aegypti habitat. Lymphatic filariasis still affects 51 million people worldwide, and elimination efforts have stalled in 13 conflict-affected countries where standard field tests miss low-density infections. Chagas disease prevalence is rising in Spain and the United States, leaving an estimated 300,000 undiagnosed carriers in North America. African trypanosomiasis dropped below 1,000 recorded cases in 2024, but sustaining near-zero transmission now depends on ultra-sensitive LAMP assays that can detect asymptomatic reservoirs. This multifaceted burden is driving ministries to ring-fence diagnostic budgets as a non-negotiable prerequisite for drug-administration campaigns.

Strengthening Global Health Initiatives and Funding

The World Bank approved a USD 500 million facility in 2025 that dedicates 18% to NTD diagnostic capacity, embedding laboratory upgrades within broader pandemic-preparedness plans. The Bill & Melinda Gates Foundation earmarked USD 1.2 billion over five years in 2024, with nearly one-quarter supporting diagnostic innovations for helminth control[1]Bill & Melinda Gates Foundation, “NTD Elimination Strategy 2024-2029,” gatesfoundation.org. USAID expanded its NTD Program to 27 countries in 2025, integrating diagnostic quality assurance into mass-drug campaigns. Unitaid’s 2024 pooled procurement of 15 million dengue NS1 tests demonstrated how volume guarantees can compress prices, though a single manufacturing delay underscored supply-chain fragility. These multi-year commitments stabilize demand and increase supplier willingness to pursue WHO prequalification.

Technological Advancements in Diagnostic Platforms

Cepheid’s GeneXpert received WHO prequalification in 2024 for a 4-plex cartridge that delivers dengue, chikungunya, Zika, and yellow-fever results in 90 minutes, leveraging an existing tuberculosis footprint of more than 10,000 global sites. Abbott’s CRISPR-based lymphatic-filariasis assay showed 96% sensitivity in a 2025 Tanzanian field trial at 40% lower cost than ELISA. Smartphone-linked AI microscopy platforms are reducing parasite-count time by 70%, enabling task-shifting to community health workers[2]London School of Hygiene & Tropical Medicine, “AI-Enabled Parasite Microscopy,” lshtm.ac.uk. RPA chemistry kits from TwistDx received CE-IVD clearance for Chagas diagnosis in 2025, enabling molecular testing in electricity-scarce clinics. Collectively, these technologies uncouple diagnostic sophistication from infrastructure constraints.

Expansion of Healthcare Infrastructure in Endemic Regions

India budgeted INR 12 billion (USD 144 million) in fiscal 2025 to build 1,200 Health and Wellness Centers equipped with rapid tests for kala-azar and filariasis. Brazil increased its municipal laboratory network by 18% between 2024 and 2025, plugging dengue and Chagas screening into primary-care workflows. Nigeria retrofitted 300 rural clinics with solar-powered cold storage in 2024, tackling electricity gaps that once hampered molecular adoption. However, Ethiopia’s 2025 stockout of dengue rapid tests exposed supply-chain fragility when central warehouses failed to replenish district stores. Infrastructure gains thus remain only as strong as the consumable pipeline that sustains them.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited healthcare access in remote areas | -0.7% | Sub-Saharan Africa, Amazon Basin, Pacific Islands | Long term (≥ 4 years) |

| High cost of advanced diagnostic technologies | -0.6% | Low-middle-income endemic countries | Medium term (2-4 years) |

| Insufficient awareness among healthcare providers | -0.4% | Rural South Asia, Sub-Saharan Africa, Central America | Medium term (2-4 years) |

| Regulatory and quality-assurance challenges | -0.5% | Global, acute where WHO pathways absent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Healthcare Access in Remote Areas

Roughly 1.2 billion people live more than 2 hours from a laboratory, leaving them excluded from conventional diagnostics. Papua New Guinea’s 2024 survey found 63% of positive filariasis cases in villages reachable only by foot or boat, rendering antigen testing impractical when transport takes a week. A 2025 audit in Chad revealed 41% of health posts lacked functional refrigeration, constraining molecular uptake[3]Médecins Sans Frontières, “Cold-Chain Audit in Chad,” msf.org. Nigeria has one lab technician for every 18,000 rural residents, a six-fold shortfall compared to urban areas. Tele-microscopy pilots are promising but bandwidth costs impede wide rollout.

High Cost of Advanced Diagnostic Technologies

Molecular NTD tests priced at USD 15-40 consume up to 60% of annual per-capita health budgets in Malawi and Haiti, limiting routine use. Roche’s cobas Liat dengue assay costs USD 28 per test, confining adoption to private hospitals, while public facilities rely on USD 2 rapid tests with lower sensitivity. GeneXpert modules cost USD 17,000, which is equivalent to three years of a district hospital’s diagnostic budget. Although Abbott committed to supply dengue NS1 at USD 0.85 for Gavi-eligible countries in 2024, ancillary training and QC added USD 1.20, limiting uptake. Domestic manufacturing could lower costs, but mutual recognition of approvals remains scarce.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: Dengue Dominates, Filariasis Drives Future Upside

Dengue diagnostics captured 19.34% of 2025 revenue, reflecting both the virus’s 400 million annual infections and the ubiquity of NS1 antigen platforms in primary care. The neglected tropical diseases diagnosis market for lymphatic filariasis testing is projected to grow fastest, advancing at an 8.54% CAGR to 2031, as elimination programs mandate antigen screening before mass drug administration. Rising non-endemic Chagas surveillance, including a 22% jump in U.S. blood-bank tests during 2025, is enlarging the commercial footprint for chronic-infection assays.

African trypanosomiasis is approaching elimination thresholds, yet ultra-sensitive molecular tests are being priced at premium levels to detect asymptomatic carriers. Rabies diagnostics remain underpenetrated, though the WHO’s 2025 urging for laboratory confirmation is nudging hospitals toward lateral-flow antigen kits. Lesser-known conditions like yaws and Buruli ulcer together account for less than 5% of the neglected tropical diseases diagnosis market, reflecting limited awareness and few WHO-prequalified assays. Even so, Peru’s 2024 shift to ultrasound-guided PCR for cysticercosis shows how advanced imaging-molecular hybrids are unlocking precision therapies.

By Diagnostic Method: Molecular Platforms Ascend

Conventional microscopy, serology, and culture retained 54.43% share in 2025 because low consumable costs suit resource-constrained clinics. Yet molecular and modern approaches are rising at an 8.65% CAGR, with CRISPR and isothermal chemistries narrowing cost gaps. Multiplex cartridges, such as Abbott’s Alinity m Resp-4-Plex, reduce per-pathogen pricing and simplify procurement, incentivizing laboratories to convert from single-plex workflows.

Microscopy still anchors helminth detection, but WHO’s 2025 preference for antigen tests in elimination protocols is eroding its dominance. Digital PCR and next-generation sequencing remain research-centric, given >USD 200 per-sample prices, yet droplet digital PCR is already informing vector-control programs in Brazil. As economies of scale build, the molecular methods market share for neglected tropical disease diagnosis is expected to eclipse serology in high-volume, time-critical settings before 2031.

By Service Type: Point-of-Care Racing Ahead

Centralized laboratories generated 62.34% of 2025 volumes, benefiting from automated batch capacity and external proficiency oversight. However, point-of-care services are advancing at a 9.65% CAGR, propelled by donor procurement criteria that favor rapid tests deployable at the primary-care level. Thermo Fisher’s 2025 roll-out of portable PCR under a Global Fund grant confirms donors’ willingness to fund molecular decentralization.

Hybrid tiering is emerging: district labs manage serology while state references handle genotyping, optimizing both cost and speed. Home healthcare accounts for only 3% of the neglected tropical diseases diagnosis market, yet self-administered dengue kits tested in Brazil achieved 89% user accuracy, signaling latent demand once reimbursement paths are clarified. Mobile truck labs blur the boundary, delivering near-point-of-care turnaround with centralized-lab quality for hard-to-reach populations.

By End User: Hospitals Narrow the Gap

Clinical laboratories held 48.43% of demand in 2025, supported by high-throughput instruments from Roche and Siemens that anchor national surveillance. Hospitals and clinics are projected to expand at a 9.86% CAGR as integrated care models prioritize on-site diagnostics for time-sensitive diseases like dengue, where platelet trends guide fluid management.

Quest Diagnostics’ 2024 partnership with the African Society for Laboratory Medicine exemplifies centralized-lab consolidation, yet Thailand’s 2025 installation of PCR analyzers in 76 provincial hospitals cut dengue confirmation times from 72 to four hours, underscoring hospital appetite for autonomy. Home healthcare is inching forward, shaped by post-COVID familiarity with self-testing, although linkage-to-care remains unresolved.

Geography Analysis

North America accounted for 41.43% of 2025 revenue despite low endemicity, driven by NIH funding of USD 287 million in NTD research, 34% of which targeted diagnostics, and the FDA granting seven fast-track designations during 2024-2025. Blood-bank screening compliance for Chagas rose to 94% in 2025 following new FDA enforcement letters, which stimulated serological demand. Canada approved pharmacy-based dengue testing for travelers, broadening non-endemic retail channels, while Mexico equipped 23 border clinics with rapid tests following cross-border outbreaks.

Asia-Pacific is the growth engine, advancing at a 7.54% CAGR through 2031, as India procured 18 million dengue rapid tests in fiscal 2025 and Indonesia opened 500 district hubs, cutting the average access distance to 12 kilometers. China exported 300,000 dengue kits to Pakistan under Belt-and-Road health aid, and Japan licensed domestic dengue tests as Aedes albopictus moved northward. Australia invested AUD 42 million (USD 28 million) to extend Pacific Island diagnostic networks, cementing regional diplomacy via health infrastructure.

Europe, the Middle East & Africa, and South America comprise the remaining share. Five African CDC regional labs opened in 2025 to curb external referrals, and the UAE re-exported 40% of East African dengue tests by leveraging free-zone logistics. South America’s 6 million-case Chagas burden spurred Argentina’s USD 3 rapid-test launch, offering a cost-disruptive local alternative. Brazil’s domestic manufacturers supplied 52% of national dengue demand in 2025, while Europe’s CE-IVD process remained a critical regulatory gateway for many Middle Eastern and African tenders.

Competitive Landscape

Market concentration is moderate: the top five firms accounted for 48% of 2025 revenue, leaving room for regional specialists. Abbott’s 2024 push to prequalify four assays illustrates how breadth efficiencies amortize regulatory costs, whereas Roche leverages universal sample-prep on its cobas platform to embed NTD testing within routine clinical panels. SD Biosensor accelerates time-to-market by securing Korean FDA clearance first, then leveraging WHO reliance to compress prequalification cycles. Thermo Fisher’s 23 active isothermal patents create licensing leverage, while bioMérieux’s acquisition of a Senegalese transport network exemplifies vertical integration to control pre-analytical variables.

White-space lies in ultra-low-resource zones where solar-powered, instrument-free assays can unlock untapped demand below 15% current penetration. Sherlock Biosciences partners with FIND to develop sub-USD 5 CRISPR kits for soil-transmitted helminths, targeting price pain points unmet by incumbents. Post-market audits show that 31% of field-used assays fail quality checks, spotlighting enforcement gaps that threaten established brands' reputations while opening niches for quality-centric entrants. Business models are shifting from unit sales toward bundled solutions—Siemens Healthineers’ 10-year Tanzanian service contract demonstrates how turnkey laboratory operations can secure long-term annuities over transactional kit revenue.

Neglected Tropical Diseases Diagnosis Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche Ltd

Thermo Fisher Scientific Inc.

bioMérieux SA

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The World Health Organization (WHO) and the German pharmaceutical company, Bayer AG, have renewed a longstanding collaboration to support endemic countries in scaling up free-of-charge treatment against three deadly neglected tropical diseases (NTDs).

- October 2025: The Global Health Innovative Technology (GHIT) Fund invested JPY 1.73 billion (USD 11.6 million) in four R&D projects for the development of diagnostics and a vaccine for tuberculosis (TB), neglected tropical diseases (NTDs), and malaria.

Global Neglected Tropical Diseases Diagnosis Market Report Scope

As per the scope of the report, neglected tropical diseases (NTDs) Diagnosis refers to the identification and detection of infectious diseases primarily affecting impoverished populations in tropical and subtropical regions. It involves utilizing various diagnostic tools and tests to confirm the presence of specific NTDs. Accurate diagnosis is essential for effective treatment, control, and eventual elimination of these diseases.

The Neglected Tropical Diseases Diagnosis Market is Segmented by Disease (Dengue, Chikungunya, Rabies, Leprosy, Buruli Ulcer, Yaws, Lymphatic Filariasis, Taeniasis/Cysticercosis, Food-Borne Trematodiases, Echinococcosis, Chagas Disease, Dracunculiasis, African Trypanosomiasis, and Other Diseases), Diagnostic Method (Conventional and Molecular/Modern), Service Type (Centralized and Point-Of-Care), End-User (Clinical Laboratories, Hospitals/Clinics, and Home Healthcare), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Dengue |

| Chikungunya |

| Rabies |

| Leprosy |

| Buruli Ulcer |

| Yaws |

| Lymphatic Filariasis |

| Taeniasis / Cysticercosis |

| Food-Borne Trematodiases |

| Echinococcosis |

| Chagas Disease |

| Dracunculiasis |

| African Trypanosomiasis |

| Other Diseases |

| Conventional Method |

| Molecular / Modern Method |

| Centralized Service |

| Point-Of-Care Service |

| Clinical Laboratories |

| Hospitals / Clinics |

| Home Healthcare |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Disease | Dengue | |

| Chikungunya | ||

| Rabies | ||

| Leprosy | ||

| Buruli Ulcer | ||

| Yaws | ||

| Lymphatic Filariasis | ||

| Taeniasis / Cysticercosis | ||

| Food-Borne Trematodiases | ||

| Echinococcosis | ||

| Chagas Disease | ||

| Dracunculiasis | ||

| African Trypanosomiasis | ||

| Other Diseases | ||

| By Diagnostic Method | Conventional Method | |

| Molecular / Modern Method | ||

| By Service Type | Centralized Service | |

| Point-Of-Care Service | ||

| By End-User | Clinical Laboratories | |

| Hospitals / Clinics | ||

| Home Healthcare | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the neglected tropical diseases diagnosis market in 2026?

The market is valued at USD 7.69 billion in 2026 and is forecast to reach USD 10.45 billion by 2031.

Which disease segment grows fastest through 2031?

Lymphatic filariasis diagnostics are projected to grow at an 8.54% CAGR thanks to elimination-program screening mandates.

What share do molecular methods currently hold?

Conventional techniques still dominate, but molecular and modern methods are rising at an 8.65% CAGR and are on track to overtake serology in high-volume settings before 2031.

Which region leads growth?

Asia-Pacific posts the highest regional CAGR at 7.54%, supported by Indian and Indonesian infrastructure expansions.

Who are the leading suppliers?

Abbott, Roche, Thermo Fisher, bioMérieux, and Bio-Rad collectively hold 48% of 2025 revenue, indicating moderate concentration.

How are turnkey lab contracts changing competition?

Long-term service agreements, like Siemens Healthineers’ 10-year Tanzanian deal, shift revenue from one-off kit sales to bundled operational models, deepening customer lock-in.

Page last updated on: