Market Overview

| Study Period | 2020 - 2031 |

|---|---|

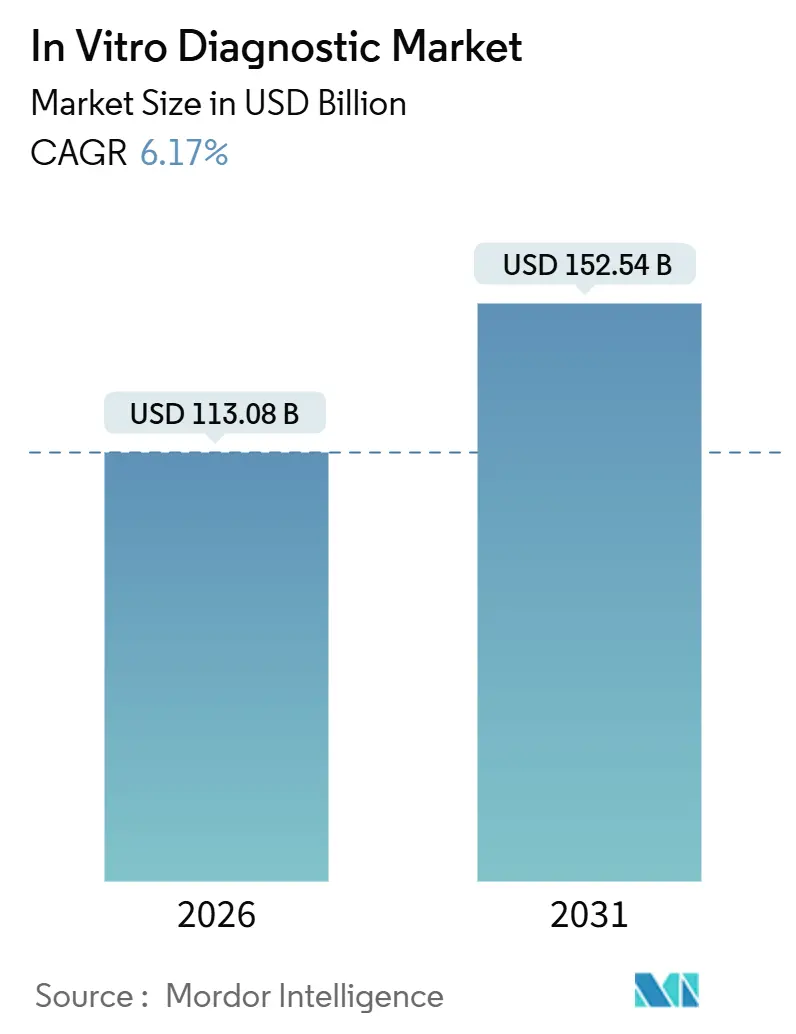

| Market Size (2026) | USD 113.08 Billion |

| Market Size (2031) | USD 152.54 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In Vitro Diagnostic Market Analysis by Mordor Intelligence

The In Vitro Diagnostic Market size is estimated at USD 113.08 billion in 2026, and is expected to reach USD 152.54 billion by 2031, at a CAGR of 6.17% during the forecast period (2026-2031).

Chronic disease prevalence, an aging global population, and artificial intelligence workflows now drive demand more sustainably than the pandemic surge. Laboratories are investing in cloud-based middleware, bundled reagent rental contracts, and integrated automation to contain labor costs and shorten turnaround times. Competitive pressure from ISO 13485-certified regional suppliers is compressing reagent margins, prompting multinationals to emphasize service bundles and decision-support software. Regulatory fragmentation, workforce shortages, and cybersecurity vulnerabilities remain structural headwinds; however, rising test volumes in the Asia-Pacific region and the increasing number of decentralized sites offset these constraints.

Key Report Takeaways

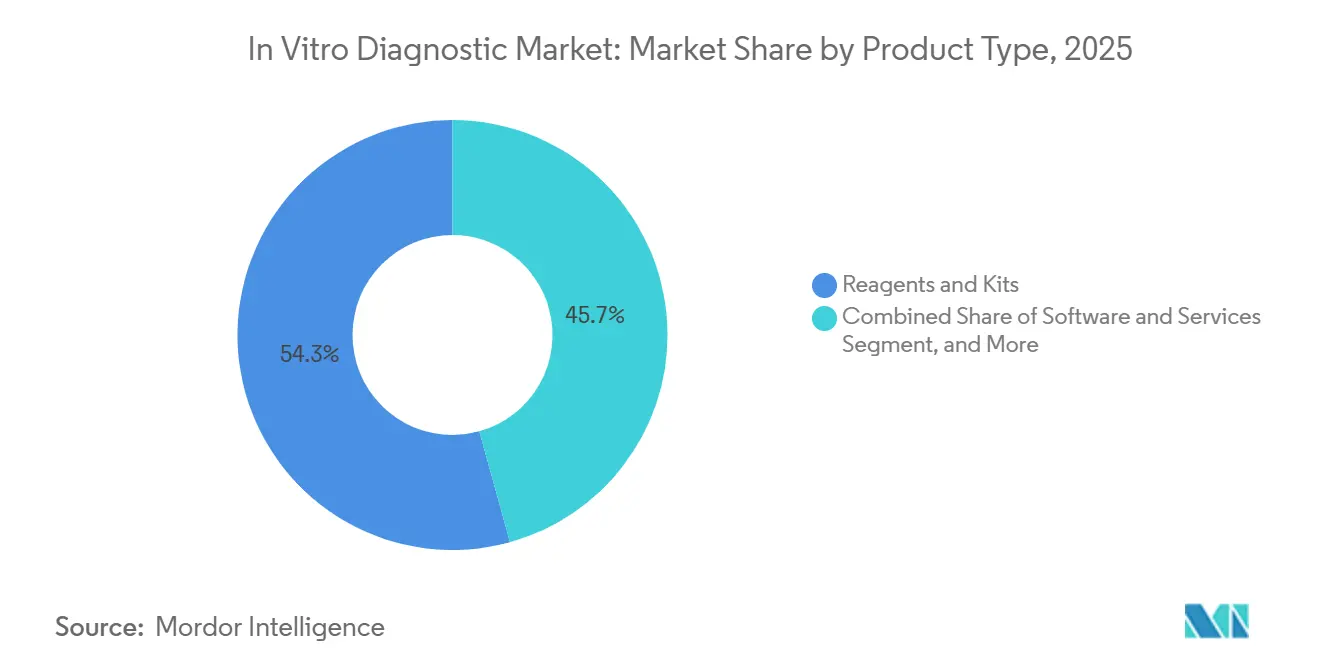

- By product type, reagents and kits accounted for 54.28% of revenue in 2025, while software and services are forecast to expand at a 10.29% CAGR through 2031.

- By technology, immunoassay led with 26.63% revenue share in 2025; molecular diagnostics are projected to advance at an 8.21% CAGR through 2031.

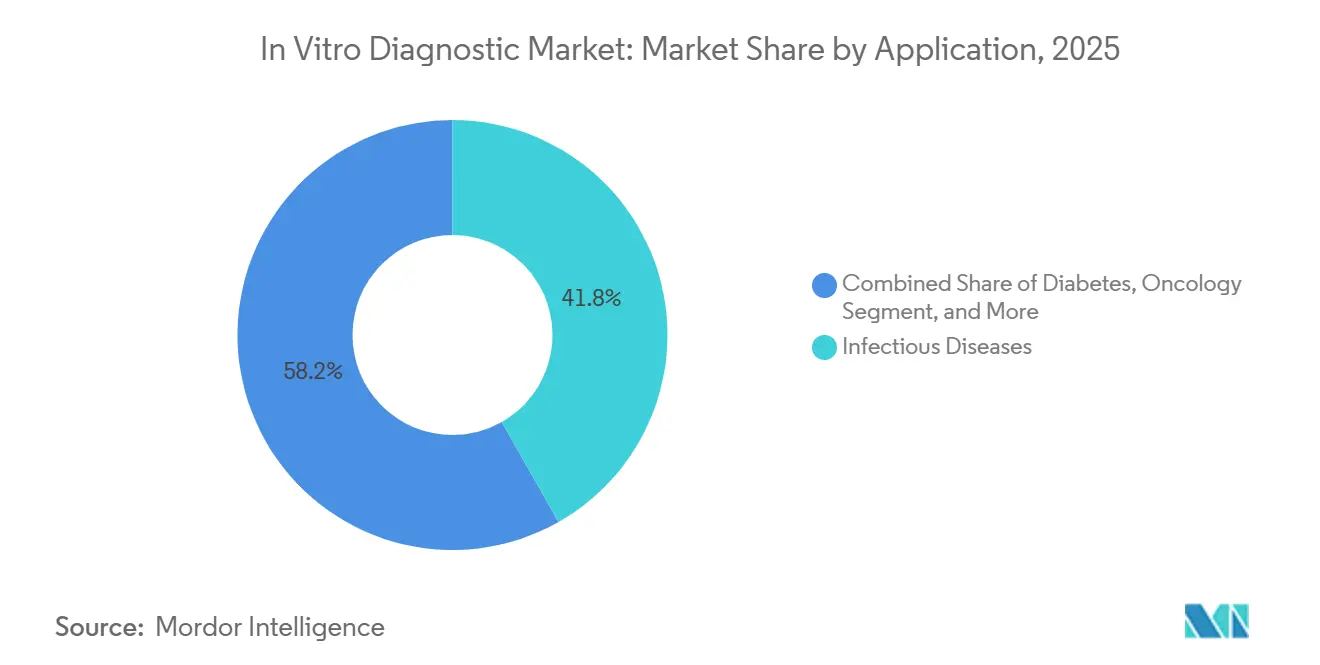

- By application, infectious diseases accounted for 41.76% of the in vitro diagnostic market share in 2025, whereas oncology is set to grow at a 9.94% CAGR to 2031.

- By end user, hospitals and academic laboratories held 48.28% share in 2025; point-of-care sites are poised for 7.94% CAGR through 2031.

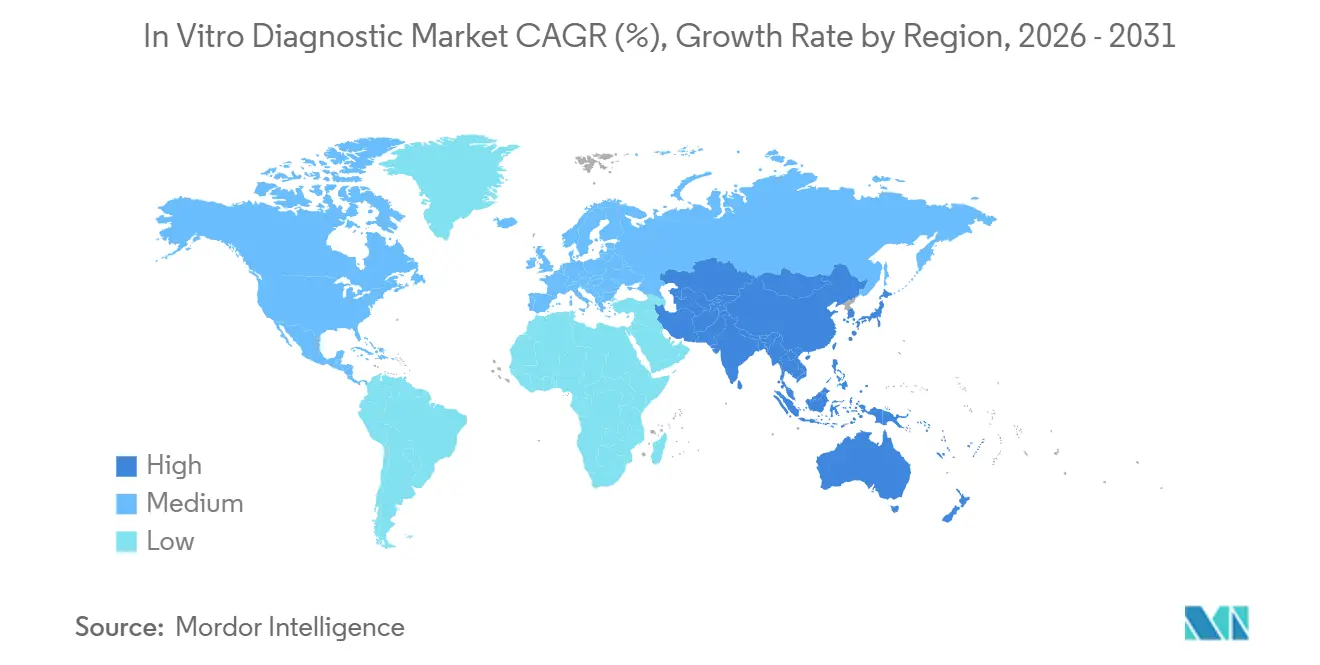

- By geography, North America captured 37.16% of 2025 revenue, yet Asia-Pacific is forecast to register a 7.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of In Vitro Diagnostic Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Adoption of Point-of-Care Diagnostics | +1.2% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| High Prevalence of Chronic Diseases | +1.5% | North America, Europe, Urban Asia-Pacific | Long term (≥ 4 years) |

| Aging Population Boosting Testing Volumes | +0.9% | Europe, Japan, South Korea, China | Long term (≥ 4 years) |

| Growing Infectious-Disease Burden | +0.8% | Sub-Saharan Africa, South Asia, Latin America | Short term (≤ 2 years) |

| Surge in Decentralized POC Testing | +1.0% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Lab Automation & Digital Pathology Convergence | +0.7% | North America, Europe, Developed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Adoption of Point-of-Care (POC) Diagnostics

Regulators expanded CLIA-waived categories in 2024 and 2025, allowing pharmacies and employer clinics to perform rapid strep, influenza, and lipid panels without requiring laboratory staff. Retail chains such as CVS Health and Walgreens now capture routine tests that once flowed to reference labs, forcing central facilities to specialize in esoteric sequencing and autoimmune panels.[1]“CVS Health Expands Access to Care with New MinuteClinic Services,” CVS Health, cvshealth.com FDA clearance of Dexcom’s over-the-counter continuous glucose monitor in 2024 demonstrated that consumer electronics firms can bypass legacy infrastructure entirely. Handheld immunoassay readers and smartphone-linked lateral-flow devices meet hospital-grade precision, narrowing the performance gap that protected central labs. This decentralization boosts test access but squeezes reagent volumes in high-margin hospital settings.

High Prevalence of Chronic Diseases

Diabetes, cardiovascular disease, and chronic kidney disease drove 1.3 billion diagnostic procedures in 2025, straining global laboratory capacity.[2]“Diabetes,” World Health Organization, who.int Diabetes prevalence climbed to 537 million adults in 2024, with the fastest growth in South Asia and the Middle East. Each chronic-care patient requires serial lipid, troponin, and kidney-function assays, raising consumable demand even as reimbursement remains flat. Wearable biosensors now continuously stream glucose and lactate data, shifting some monitoring from venipuncture to cloud analytics. Vendors, therefore, bundle laboratory reporting with longitudinal analytics subscriptions to preserve revenue even as traditional consumable sales plateau.

Aging Population Boosting Chronic Disease Testing Volumes

Citizens aged 65 plus generate a disproportionate share of chemistry panels. Japan’s over-75 cohort alone accounted for 47% of all clinical-chemistry tests in 2024.[3]“Ministry of Health, Labour and Welfare, Japan,” mhlw.go.jp Reimbursement cuts compelled laboratories to automate, integrating cartridge-based multiplex assays that combine hemoglobin A1c, creatinine, and lipid markers in a single run, thereby reducing labor time per specimen. China’s 2025 rural screening program for residents over 60 secured fixed-price contracts favoring high-volume reagent producers. Rising cancer incidence within aging populations likewise increases demand for tumor markers and liquid-biopsy monitoring, embedding advanced diagnostics deep into chronic-care pathways.

Growing Infectious-Disease Burden Fueling Rapid Diagnostics

Following the pandemic, hospitals adopted multiplex PCR panels that detect up to 30 pathogens in a single cartridge, maintaining high utilization even as COVID-19 testing subsided. WHO reported 10.8 million new tuberculosis cases in 2024, with 410,000 drug-resistant infections requiring two-hour molecular resistance profiling. Donor-funded programs distributed 120 million malaria rapid tests in 2024, reinforcing demand for low-infrastructure assays across Sub-Saharan Africa. Primary-care sites value a 15-minute turnaround, which improves antimicrobial stewardship and reduces hospital admissions, thereby sustaining growth in molecular diagnostics.

Restraints Impact Analysis of In Vitro Diagnostic Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Region Regulatory Timelines | -0.6% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Reimbursement Uncertainty for Emerging Tests | -0.5% | North America, Europe, Asia private payers | Medium term (2-4 years) |

| Cybersecurity & Data Interoperability Gaps | -0.3% | Connected infrastructures in North America, Europe | Short term (≤ 2 years) |

| Global Shortage of Skilled Lab Technologists | -0.4% | North America, Europe, Developed Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Regulatory Approval Timelines

The European Union’s IVD Regulation, fully enforced in May 2024, transitioned thousands of low-risk assays from self-certification to notified-body review, resulting in a median approval time of 22 months. Japan and China impose parallel data requirements, adding 18 to 24 months before multinational launches reach the Asia region. Small innovators lack the regulatory manpower to run simultaneous trials, so they prioritize the United States first, ceding early share abroad. Staggered launches delay global scale and allow fast-follower rivals to secure reimbursement ahead of pioneers, marginally shaving the in vitro diagnostic market CAGR.

Reimbursement Uncertainty Across Emerging Test Classes

CMS issued non-coverage decisions for several multi-cancer early-detection tests in 2024 due to the limited availability of mortality data. Private insurers echoed the stance, forcing laboratories to self-pay or negotiate risk-sharing contracts. FoundationOne CDx receives a Medicare reimbursement of USD 5,800, whereas comparable assays lacking FDA approval often face claim denials. Laboratories hesitate to deploy costly oncology panels until reimbursement is stabilized, slowing the adoption curve even after regulatory clearance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

In Vitro Diagnostic Market Segment Analysis

By Product Type:

Consumables Anchor Revenue, Software Captures GrowthReagents and kits accounted for 54.28% of 2025 revenue, underscoring the consumable-based economics that sustain most laboratories. Hospitals favor reagent-rental agreements that waive analyzer acquisition costs in exchange for multi-year consumable purchases, a model that smooths vendor revenue. Software and services are forecast to post a 10.29% CAGR through 2031, powered by AI decision-support, cloud-hosted middleware, and remote instrument diagnostics. Instruments remain vital as lock-in platforms; Siemens Healthineers’ Atellica Solution processes 440 tests per hour and auto-verifies 85% of results, saving labor minutes per report. The in vitro diagnostic market size for software is currently small, but its double-digit trajectory signals a shift by laboratories toward analytics and compliance outsourcing.

Software now decouples from hardware under the FDA’s Software-as-a-Medical-Device framework, enabling independent algorithm upgrades. Vendors differentiate by pairing cloud dashboards with quality-control materials, creating sticky ecosystems. As capital budgets tighten, revenue from reagent rental and subscription-based software will rise faster than hardware placements, reshaping vendor profit pools within the in vitro diagnostic market.

By Technology:

Molecular Diagnostics Outpace Legacy PlatformsImmunoassay retained a 26.63% revenue share in 2025, driven by thyroid, cardiac, and tumor markers. Yet, molecular diagnostics are projected to expand at an 8.21% CAGR, driven by liquid biopsy approvals, CRISPR assays, and syndromic infectious disease panels. Clinical chemistry automation has commoditized metabolic panels, so vendors now differentiate themselves through faster throughput and middleware integration rather than reagent chemistry. Hematology platforms incorporate AI-based cell classification, while microbiology shifts from culture to MALDI-TOF for rapid identification in 15 minutes.

Technology convergence is blurring legacy silos; next-generation platforms combine immunoassay, molecular techniques, and mass spectrometry on a single track. Laboratories welcome consolidated workflows that reduce sample handling, minimize error risk, and contain labor costs. As these hybrid systems scale, the in vitro diagnostic market will shift toward multi-modal analyzers that integrate AI-driven sample triage, increasing switching costs and solidifying vendor relationships.

By Application:

Oncology Accelerates, Infectious Disease StabilizesInfectious diseases accounted for 41.76% of 2025 revenue, buoyed by multiplex respiratory panels that remained in use after the pandemic peaks. Growth, however, is moderating as COVID-19 volumes return to normal. Oncology diagnostics, in contrast, are projected to increase by 9.94% per year to 2031, driven by companion diagnostics and minimal residual disease liquid biopsies, such as Guardant360. Diabetes testing remains a high-volume market but faces price pressure as continuous glucose monitors become available over the counter.

Cardiology markers are migrating to emergency department POC settings, while autoimmune and nephrology panels are gaining market share through multiplex formats that enhance diagnostic efficiency. Oncology’s higher reimbursement and clinical urgency drive capital investment in sequencing, flow cytometry, and mass spectrometry, positioning cancer testing as the fastest-growing slice of the in vitro diagnostic market.

By End User:

Point-of-Care Sites Gain Share, Hospitals Retain ComplexityHospitals and academic centers accounted for 48.28% of 2025 revenue, primarily driven by stat and high-complexity assays that require advanced infrastructure. Point-of-care sites, pharmacies, urgent care clinics, and employer health centers are forecasted to grow at a 7.94% CAGR, propelled by waived cartridges that deliver immediate results. Reference laboratories scale esoteric menus but endure payer pressure on routine panels. Home and over-the-counter channels remain small but exhibit steep growth as the FDA clears consumer diagnostics, such as continuous glucose monitors.

End-user fragmentation compels vendors to tailor offerings: compact analyzers for POC clinics, automation lines for hospitals, and cloud portals for at-home results. This segmentation increases touchpoints for the in vitro diagnostic market, expanding the total addressable volume but requiring versatile portfolios and adaptive go-to-market models.

Geography Analysis

North America In Vitro Diagnostic Market

North America accounted for 37.16% of the 2025 revenue, supported by early adoption of molecular diagnostics and robust reimbursement. CMS value-based-care models now tie laboratory utilization to bundled payments, pressuring providers to limit low-value testing. FDA cybersecurity mandates increase compliance costs but improve data integrity. Canada and Mexico consolidate testing into regional hubs to capture scale economies.

APAC In Vitro Diagnostic Market

The Asia-Pacific region is forecast to post a 7.19% CAGR from 2026 to 2031, the fastest regional pace. China’s volume-based procurement slashed reagent prices by up to 60%, yet soaring volumes protect vendor revenue. India’s National Health Mission funded 5,000 district labs in 2024-25, increasing per-capita test penetration from 0.08 to 0.15 tests per capita annually. Aging Japan and South Korea are automating aggressively to offset labor shortages, resulting in increased capital expenditure on total laboratory automation.

EMEA and South America In Vitro Diagnostic Market

Europe enforces the IVD Regulation, extending approval timelines and favoring multinationals with seasoned regulatory teams. GCC states channel oil revenue into laboratory infrastructure under Vision 2030. Sub-Saharan Africa remains under-penetrated but benefits from donor-funded HIV, tuberculosis, and malaria programs. South American laboratories struggle with currency fluctuations and import tariffs, sourcing reagents locally whenever possible to manage costs.

Regulatory Landscape

Regulatory requirements continue to diverge by region, with several 2024-2026 milestones shaping global launch sequencing and compliance costs. In the European Union, Regulation (EU) 2017/746 (IVDR) moved fully into force in May 2024, shifting many assays from self-certification to Notified Body review and extending time-to-market. The European Commission continued publishing updated information on Notified Body designation and application status in 2026 to support transition capacity planning.

In the United States, the FDA finalized a Laboratory Developed Test (LDT) framework in 2024, and Stage 1 of the phaseout policy began in May 2026. This brings medical device reporting, correction and removal reporting, and defined quality system complaint-file obligations into scope for affected laboratories. Quality management and reliance initiatives are also increasing the weight of harmonized standards in IVD quality systems and post-market processes. The FDA is implementing its Quality Management System Regulation (QMSR), aligning device quality system requirements more closely with ISO 13485 and updating inspection approaches during the transition period. At the multilateral level, WHO and the International Medical Device Regulators Forum (IMDRF) continue to promote reliance-based regulatory pathways via the WHO Global Model Regulatory Framework and the IMDRF Reliance Playbook (N89), providing a reference point for regulators and manufacturers seeking to reduce duplicative evidence generation across jurisdictions.

Competitive Landscape

The top five suppliers, Roche, Abbott, Siemens Healthineers, Danaher, and Thermo Fisher, indicate moderate consolidation. Each bundle of instruments, reagents, and AI middleware is locked into multi-year contracts that tie hospitals to exclusive reagent streams. Regional challengers in Asia and Latin America undercut pricing by up to 40% while meeting ISO 13485 standards, forcing incumbents to emphasize service, connectivity, and cybersecurity.

Technology innovation remains the battlefield. Roche’s cobas pro cuts turnaround time by 22%, justifying premium reagent pricing. Danaher’s Beckman Coulter filed 14 microfluidic-cartridge patents in 2024, while Siemens Healthineers secured nine predictive-maintenance AI patents. Consumer electronics giants are exploring non-invasive biosensors that could bypass venipuncture diagnostics, posing a long-term disruptive threat.

Regulatory and cybersecurity hurdles intensify competitive pressure. FDA’s 2024 guidance now requires encryption and patch management for connected devices, a standard that strains smaller firms. As decentralized testing gains ground, incumbents acquire niche innovators, such as Bio-Rad’s Stilla dPCR and bioMérieux’s SpinChip, to secure beachheads in faster-growing segments, thereby preserving relevance across diversified test settings.

In Vitro Diagnostic Industry Leaders

F. Hoffmann-La Roche Ltd

Thermo Fischer Scientific Inc

Siemens Healthineers AG

Abbott Laboratories

bioMerieux SA

- *Disclaimer: Major Players sorted in no particular order

In Vitro Diagnostic Market Companies Covered in this Report

- Abbott Laboratories

- Agilent Technologies

- Beckton Dickinson

- Bio-Rad Laboratories

- bioMérieux

- Danaher

- DiaSorin

- Roche

- GE Healthcare

- Grifols

- Hologic

- Illumina

- Meril Diagnostics Pvt Ltd

- Ortho Clinical Diagnostics / QuidelOrtho

- PerkinElmer

- QIAGEN

- QuidelOrtho

- Randox Laboratories

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

Market Opportunities and Future Outlook

Regulatory transition work in Europe and the scaling of compliance infrastructure are creating whitespace for consultative services, regulatory tooling, and portfolio rationalization that favors manufacturers able to sustain multi-year certification programs under IVDR. Concrete 2026 deadlines, such as the May 26, 2026 application lodging date for legacy Class C IVDs with an EU Notified Body and the May 28, 2026 EUDAMED use requirement for new IVDs, are pushing companies to refresh technical documentation, strengthen post-market surveillance processes, and prioritize assays with clearer reimbursement and clinical demand. In parallel, the European Commission published a simplification package in December 2025 (COM(2025) 1023 final) proposing amendments to MDR/IVDR to reduce administrative burden and address capacity constraints, giving manufacturers an active policy track to monitor when planning EU portfolios and submission timing.

On the supply and technology side, capacity localization and higher-throughput molecular manufacturing investments point to where vendors are committing capital to support faster menu expansion and resilience. In May 2026, bioMeriéux announced a EUR 250 million investment in a new PCR test manufacturing facility in La Balme-les-Grottes, France (planned to be operational in 2030), reinforcing regional manufacturing for molecular diagnostics. In May 2026, Natera disclosed an expansion in Austin, Texas, adding dedicated sequencing capacity, while India continued to attract manufacturing buildout, including a June 2026 opening of a new IVD-focused medical device facility by Lord's Mark Industries. Together, these steps support opportunities around scalable PCR and sequencing workflows, automation-ready consumables, and software and services that help laboratories integrate decentralized testing, cybersecurity controls, and cross-site quality management.

Recent Industry Developments in In Vitro Diagnostic Market

- July 2026: Roche announced the launch of the cobas Hepatitis D Virus (HDV) test as a fully automated solution on the cobas platform. The addition broadens menu depth in virology and supports consolidated, high-throughput workflows that laboratories use to improve turnaround time and standardization across sites.

- May 2026: Roche entered into a definitive merger agreement to acquire PathAI to strengthen digital pathology and AI-enabled diagnostic workflows. The combination aligns IVD vendors more tightly with software-driven interpretation and can increase platform stickiness through integrated algorithms and workflow tools.

- December 2024: Ortho Clinical Diagnostics received CE marking for the Ortho Vision Analyzer, a compact immunoassay system targeted at mid-sized European laboratories. The clearance supports continued competitive activity in EU immunoassay placements despite ongoing IVDR transition pressures and documentation requirements.

In Vitro Diagnostic Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the in vitro diagnostics market covers revenue earned from tests run on human samples outside the body to support screening, diagnosis, disease monitoring, and therapy guidance, across routine lab and near-patient settings.

Scope exclusions: Research-use-only and investigational-use-only assays are excluded, and hospital procedure costs are not counted unless they are part of a priced IVD product or service.

Segments Covered in This Report

- By Product Type

- Instruments

- Reagents & Kits

- Software & Services

- By Technology

- Immunoassay

- Clinical Chemistry

- Molecular Diagnostics

- Hematology

- Microbiology

- Coagulation

- Urinalysis

- Others

- By Application

- Infectious Diseases

- Oncology

- Diabetes

- Cardiology

- Autoimmune Diseases

- Nephrology

- Others

- By End User

- Hospitals & Academic Labs

- Reference Laboratories

- Point-of-Care Testing Sites

- Homecare/OTC Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model on observable demand signals and policy context before assumptions were built. We reviewed public health statistics and testing guidance from sources such as the World Health Organization, the US CDC, and the US FDA, then supplemented these with OECD health indicators and selected national health ministry dashboards to add context on lab activity and disease burden.

On the market side, company annual reports, investor presentations, and reputable press were reviewed to understand product mix shifts, for example reagent-heavy categories versus instrument placements, and how this played out by region. To avoid overstating volumes, trade and procurement signals were also checked using sources such as UN Comtrade and public tenders, then cross-checked with patent filings for technology direction. Where needed, paid subscriptions for company financials, news and financials, patent searches, and shipment-level trade tracking were used to standardize and reconcile inputs. The desk research sources listed here are illustrative only, and many other public references were used for validation and clarification.

Primary Interviews and Surveys

Primary interviews and surveys focused on what drives IVD spending in practice, and how price and mix move across both mature and emerging testing systems. We spoke with diagnostic laboratories, hospital lab stakeholders, distributors, and industry experts across APAC, EMEA, and the Americas, which helped pressure-test secondary signals and close gaps in instrument placement, reagent pull-through, and how service revenue should be treated in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 42% | EMEA: 33% |

| Smaller Players: 15% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing started with a top-down build where, for each country, testing demand and healthcare delivery signals were translated into IVD spending pools, then rolled up to regional and global totals. In practice, the model uses indicators such as the aging share of population, chronic disease testing intensity, infectious disease testing normalization after outbreak periods, lab automation adoption, and the shift of testing toward point-of-care and self-testing, which then feeds into mix and price behavior.

Those totals were then corroborated with selective bottom-up approximations. This included checking whether sampled supplier revenues and channel feedback on reagent pull-through, as well as indicative ASP x volume math for major test categories, sit within the modeled range. Where bottom-up evidence was incomplete in smaller countries, we filled the gap using proxy utilization and penetration assumptions tied to comparable health system metrics, and then rechecked with interview feedback.

For forecasting, scenario analysis was used so changes in reimbursement pressure, testing frequency, and mix (molecular versus immunoassay versus routine chemistry) could be reflected without forcing one straight-line outcome. ASP movement was treated as a combination of inflation, tender-driven price resets, and product mix, with assumptions adjusted only after they matched what respondents reported seeing in procurement cycles and lab budgets.

Data Validation & Update Cycle

Validation was performed in layers so the final numbers stayed consistent with demand side signals and supply side realities. We compared the modeled market totals against independent checks, including regional healthcare spend direction, reported diagnostics revenue trends in filings, and visible shifts in testing settings. Outliers were then reviewed and corrected before sign-off.

A second analyst review is completed to catch currency conversion timing issues, sudden mix changes, and one-off demand spikes that can distort a base year. Reports are refreshed annually, and if a material event occurs, for example a major reimbursement change or a sharp tender price reset, assumptions are revisited and the model is rebalanced. Before delivery, the latest public updates are rechecked so clients receive a current view.

Mordor Intelligence's In Vitro Diagnostics Market Size Compared Against Other Published Estimates

Published IVD market values often differ because update timing and the currency conversion window are not the same, and because some models treat ASP erosion and mix shifts as a single blended assumption. Differences also show up when one estimate counts only instruments and reagents, while another folds in software, services, and broader lab workflows.

Key gap drivers in this market typically come down to how fast pandemic-era testing is normalized, how reagent pull-through is linked to instrument placements, and whether tender resets are applied immediately or smoothed over multiple years. When the refresh cadence is tighter and FX timing is aligned to the stated base year, the estimate tends to track real procurement and lab utilization signals more closely, which is the approach used in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 113.08 B (2026) | |

| Global Consultancy A | USD 106.29 B (2025) | Uses a different base year and typically applies a smoother growth path, which can understate near-term mix changes from molecular and point-of-care shifts and can land on a lower starting value. |

| Industry Publisher B | USD 77.73 B (2025) | Likely applies a narrower revenue boundary or different inclusions for services and software, and the lower base year value can also reflect different FX timing and more aggressive ASP compression assumptions. |

The table shows that year selection and what gets counted inside IVD revenues are the main reasons the numbers do not line up. By keeping the steps traceable to testing demand signals, mix, and price logic, the estimate stays explainable and can be recreated when assumptions need to be updated.

Key Questions Answered in the Report

How fast is the in vitro diagnostic market expected to grow through 2031?

It is projected to expand from USD 113.08 billion in 2026 to USD 152.54 billion by 2031, translating to a 6.17% CAGR.

Which technology segment shows the highest growth potential?

Molecular diagnostics are forecast to grow at an 8.21% CAGR, outpacing immunoassay and clinical chemistry.

Why are point-of-care sites gaining importance?

CLIA-waived cartridge analyzers let pharmacies and urgent-care clinics perform routine panels, driving a 7.94% CAGR among point-of-care users.

What is the key driver behind Asia-Pacific growth?

Volume-based procurement in China and public-lab expansion in India are pushing Asia-Pacific toward a 7.19% CAGR through 2031.

How are vendors responding to skilled-labor shortages?

Laboratories invest in total automation and AI middleware that reduce manual review time, while vendors offer reagent-rental and remote-service models.

Page last updated on: