Infectious Disease Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 48.38 Billion |

| Market Size (2031) | USD 57.05 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

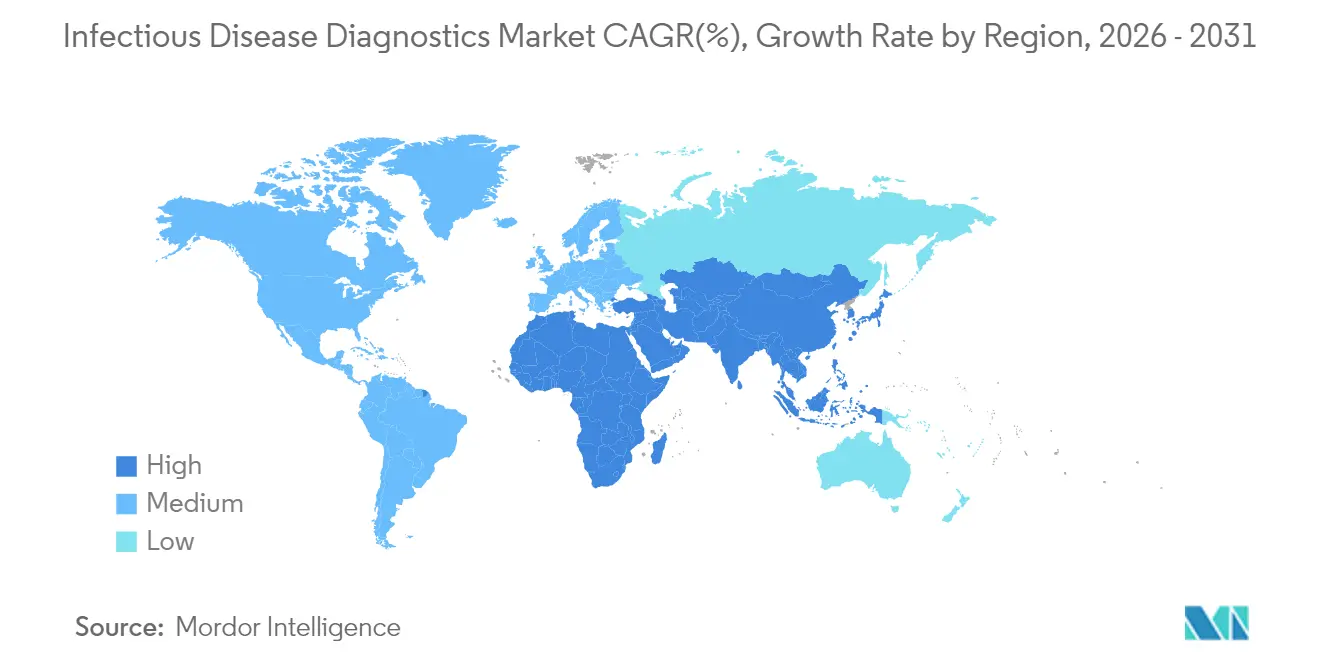

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infectious Disease Diagnostics Market Analysis by Mordor Intelligence

The infectious disease diagnostics market size was valued at USD 46.81 billion in 2025 and estimated to grow from USD 48.38 billion in 2026 to reach USD 57.05 billion by 2031, at a CAGR of 3.35% during the forecast period (2026-2031). This steady trajectory shows how the infectious disease diagnostics market is moving from pandemic-driven demand toward long-term growth anchored in endemic disease management, climate-linked outbreaks, and ongoing technology upgrades. Spending is broadening beyond respiratory tests to include vector-borne, antimicrobial-resistant, and emerging pathogens, helping laboratories offset lower COVID-19 volumes. Reagent sales remain the revenue backbone, yet software-enabled workflow tools are scaling fast as labs seek automation efficiencies. Competitive intensity is rising because new entrants armed with CRISPR, isothermal, and AI capabilities are challenging incumbents for share in the infectious disease diagnostics market.

Key Report Takeaways

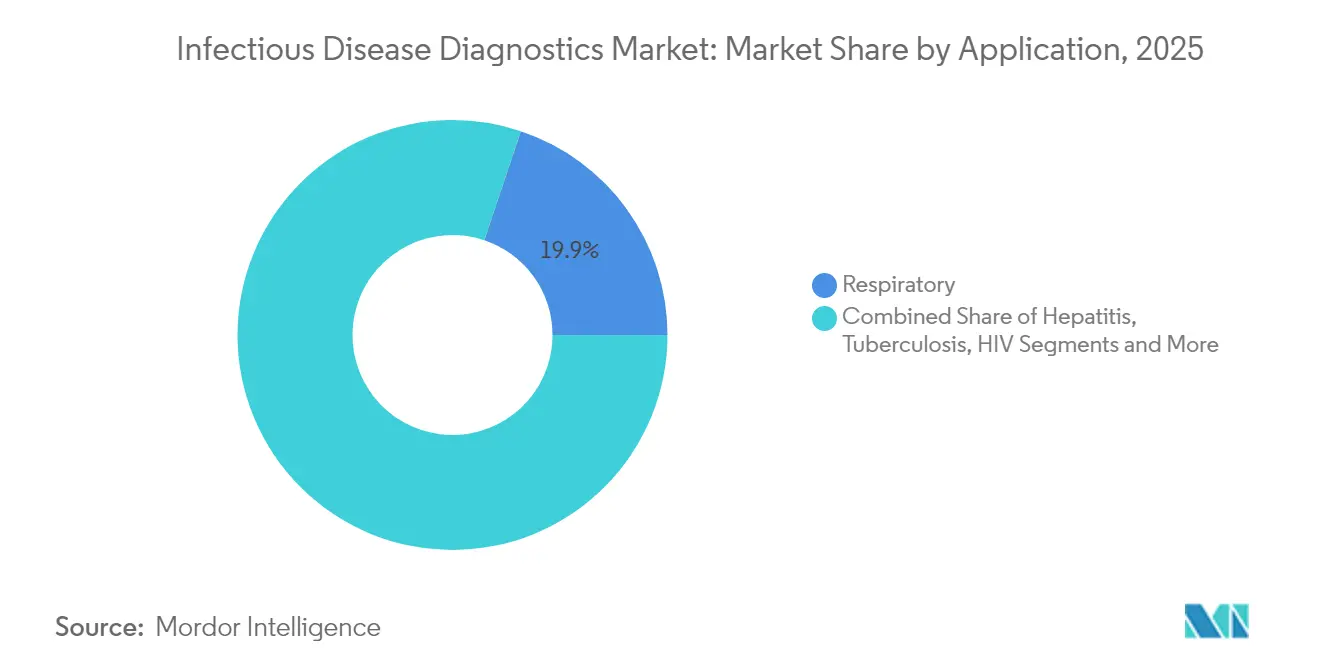

- By application, respiratory infections led with 19.85% of infectious disease diagnostics market share in 2025, while vector-borne and emerging pathogen tests are projected to expand at a 5.52% CAGR to 2031.

- By product and service category, assays, kits, and reagents commanded 52.90% of the infectious disease diagnostics market size in 2025; software and informatics are set to grow the fastest at a 5.48% CAGR.

- By technology, PCR and qPCR platforms held 34.20% of infectious disease diagnostics market size in 2025, whereas CRISPR-based diagnostics are expected to record the highest 5.18% CAGR.

- By end user, hospital and clinical laboratories accounted for 46.00% of infectious disease diagnostics market share in 2025; the home-care and OTC channel is advancing at a 6.62% CAGR.

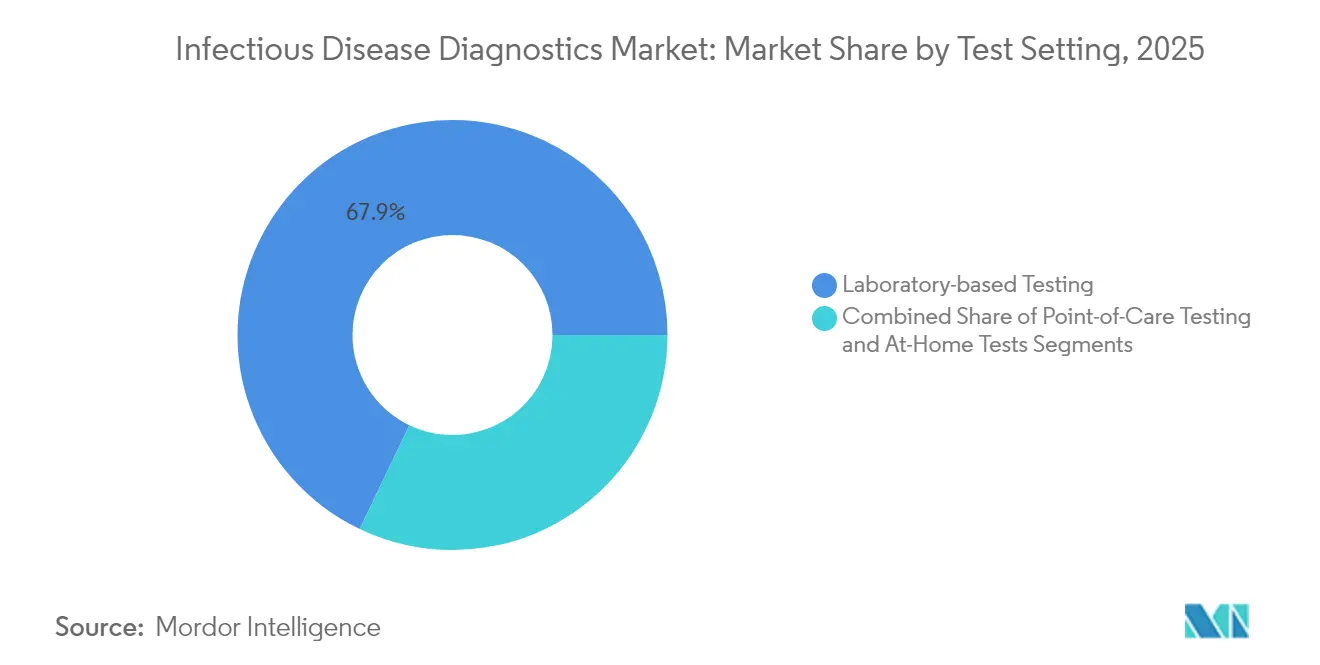

- By test setting, laboratory-based testing dominated with 67.90% share in 2025, but over-the-counter and at-home formats are forecast to grow at a 6.74% CAGR.

- By sample type, blood, plasma, and serum tests made up 42.95% of 2025 revenue, while swab-based assays are rising fastest at a 4.12% CAGR.

- By region, North America led with a 44.85% revenue share in 2025, whereas Asia-Pacific is projected to expand at a 5.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infectious Disease Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prevalence and resurgence of infectious diseases | +0.8% | Global, higher in Asia-Pacific and Africa | Medium term (2-4 years) |

| Growing demand for point-of-care and at-home testing | +0.6% | North America, Europe expanding to Asia-Pacific | Short term (≤ 2 years) |

| Continuous innovation in PCR/NGS platforms and chemistries | +0.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Government initiatives for prevention, diagnosis, and awareness | +0.4% | Global, policy-driven | Medium term (2-4 years) |

| Expansion of molecular and rapid antigen testing | +0.3% | Global, faster in emerging markets | Short term (≤ 2 years) |

| AI-driven laboratory workflows | +0.2% | North America and Europe first, Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence and Resurgence of Infectious Diseases

Vector-borne illnesses are climbing, with dengue cases running 15% above the five-year average in early 2025.[1]Centers for Disease Control and Prevention, “Ongoing Risk of Dengue Virus Infections and Updated Testing Recommendations in the United States,” cdc.govClimate change is widening mosquito habitats, so providers now test for pathogens once restricted to the tropics. The World Health Organization classified mpox as a grade 3 emergency in August 2024, prompting a 160% jump in test demand over the prior year. Antimicrobial resistance adds pressure: the WHO’s 2024 priority list highlights 15 resistant bacterial families that need rapid diagnostics. As new threats surface, laboratories must refresh menus frequently, creating recurring revenue for firms across the infectious disease diagnostics market.

Growing Demand for Point-of-Care and At-Home Testing

Regulators are green-lighting consumer tests at pace. In August 2024 the FDA cleared the first OTC syphilis assay, ushering retail diagnostics into mainstream practice.[2]U.S. Food and Drug Administration, “FDA Marketing Authorization Enables Increased Access to First Step of Syphilis Diagnosis,” fda.gov Syphilis incidence rose 80% from 2018 to 2022, so community pharmacies and e-commerce portals now stock rapid kits. Cepheid’s finger-stick hepatitis C test adds same-visit viral confirmation, closing care gaps in primary clinics. Payers value earlier therapy starts that reduce downstream costs, so reimbursement processes are catching up, even as coding complexity persists.

Continuous Innovation in PCR/NGS Platforms and Chemistries

CRISPR systems are approaching PCR-level sensitivity yet dispense with lengthy thermocycling steps. Portable devices such as the Dragonfly deliver 96.1% sensitivity for mpox without cold chain, fitting remote clinics. Isothermal nucleic-acid amplification bridges the gap between lab-based accuracy and field expediency. Metagenomic sequencing enables pathogen-agnostic detection, letting physicians identify unknown agents swiftly. Early adopters gain speed and menu breadth that cement competitive positioning in the infectious disease diagnostics market.

AI-Driven Laboratory Workflows for Testing

Machine-learning tools now auto-classify blood cultures and flag antimicrobial resistance patterns in minutes.[3]Phys.org, “CRISPR-Cascade Test Detects Bloodstream Infections in Minutes Without Amplification,” phys.orgAutomated quality-control algorithms catch analytic drift and improve consistency. Fully robotic “dark” labs use AI to maintain throughput despite staffing gaps. Vendors who embed analytics directly into instruments or LIS platforms see faster adoption, because laboratories value productivity gains that offset shrinking reimbursement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and inadequate reimbursement frameworks | -0.7% | Global, acute in emerging markets | Medium term (2-4 years) |

| Budget squeeze after COVID-19 testing wind-down | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Over-capacity of swab and PCR kit manufacturing assets | -0.3% | Global production hubs | Short term (≤ 2 years) |

| Regulatory grey zones for multiplex CRISPR assays | -0.2% | Global, varies by regulator maturity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented and Inadequate Reimbursement Frameworks

Payers insist on stringent coding before honoring claims, and the added paperwork stretches cash cycles for smaller labs. Government fee schedules, especially in low- and middle-income countries, rarely cover the full cost of advanced molecular platforms, limiting uptake. Laboratories in such settings rely on donor programs, slowing commercial momentum despite clear clinical need. Harmonized payment models would unlock wider adoption across the infectious disease diagnostics market.

Budget Squeeze After COVID-19 Testing Wind-Down

COVID-19 volumes collapsed in 2024, cutting 17.6% off Abbott’s diagnostics sales. Public-health budgets likewise fell after USD 76 billion in emergency funds expired, slowing capital purchases. Many regional labs merged into larger networks to survive lower volumes, raising concentration but trimming near-term equipment orders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Vector-Borne Diseases Drive Growth Beyond Respiratory Dominance

Respiratory panels held 19.85% of infectious disease diagnostics market share in 2025, yet vector-borne and emerging pathogens are set to climb at a 5.52% CAGR to 2031. A record 13 million dengue cases in 2024-2025 forced hospitals to expand test menus. Mpox, hepatitis, HIV self-tests, and AI-assisted tuberculosis assays broaden the clinical mix. The infectious disease diagnostics market size attached to vector-borne testing will keep rising as global mobility and climate change alter transmission zones.

Growth relies on rapid antimicrobial susceptibility tools for hospital-acquired infections and FDA OTC clearances for STI home kits. Laboratories value platforms that update quickly when the WHO adds bacteria to its resistance list; such flexibility strengthens vendor stickiness inside the infectious disease diagnostics market.

By Product & Service: Software Integration Accelerates Amid Hardware Maturity

Assays, kits, and reagents contributed 52.90% of infectious disease diagnostics market size in 2025 because consumables drive recurring revenue. Software and informatics, though smaller, will post the quickest 5.48% CAGR as labs digitize workflows. Instruments now compete on automation depth, sample-to-answer speed, and AI tie-ins rather than raw throughput alone.

Contract-testing services grow when hospitals outsource complex sequencing or drug-resistance panels. Cloud-based analytics link raw data to actionable reports, enhancing value per test. Vendors bundling reagents with informatics maintain share even as hardware margins tighten across the infectious disease diagnostics market.

By Technology: CRISPR Emergence Challenges PCR Dominance

PCR and qPCR kept 34.20% of infectious disease diagnostics market size in 2025, anchored by entrenched protocols and broad regulatory clearance. CRISPR assays will record a 5.18% CAGR because they reach PCR-grade sensitivity without full thermocycling steps. Isothermal NAAT devices and multiplex microarrays add flexibility for field teams.

Sequencing is pushing into routine care, aided by AI pipelines that shorten interpretation time. Pathogen-agnostic metagenomics is particularly useful for unexplained sepsis. The infectious disease diagnostics market benefits when multiple modalities converge in single instruments that cover screening, confirmation, and resistance profiling.

By End User: Home-Care Expansion Reshapes Market Dynamics

Hospitals and clinical labs retained 46.00% infectious disease diagnostics market share in 2025, yet OTC demand is rising fastest at 6.62% CAGR after FDA policies favor home testing. Reference labs absorb overflow and specialized NGS workloads, often contracting with regional facilities to standardize quality.

Telemedicine pairs with self-collection kits to widen access. Academic centers continue to pilot emerging tech and hand proven workflows to industry. As consumers take more control, vendors must design intuitive packaging and remote support to sustain adoption within the infectious disease diagnostics market.

By Test Setting: Over-the-Counter Testing Transforms Healthcare Access

Central laboratories still handle 67.90% of tests in 2025 because complex panels need stringent oversight. Yet OTC and at-home formats show a 6.74% CAGR, helped by CLIA-waived respiratory and STI minisystems. Regulators now demand embedded digital reporting to protect surveillance data as tests move outside labs.

Point-of-care molecular analyzers fit urgent-care clinics and ambulances, giving clinicians results in under 20 minutes. These shifts stretch supply chains but also introduce fresh channels for growth in the infectious disease diagnostics market.

By Sample Type: Swab Innovation Drives Non-Invasive Testing

Blood, plasma, and serum accounted for 42.95% of testing revenue in 2025, yet saliva and anterior-nares swabs are growing at 4.12% CAGR as collection becomes more comfortable. Multiplex saliva panels show sensitivity comparable to nasopharyngeal sticks. Urine NAATs expand STI screening, while AI-supported stool reviews improve parasite detection.

Improved buffers and extraction chemistries raise pathogen yield from low-volume samples. Portable devices now accept multiple matrices, boosting versatility and advancing decentralized adoption across the infectious disease diagnostics market.

Geography Analysis

North America generated 44.85% of global revenue in 2025, supported by established reimbursement rules, fast FDA clearances, and high routine screening volume. However, the region is now confronting budget compression as COVID-19 testing revenues fade, prompting labs to broaden menus and accelerate automation.

Asia-Pacific is projected to grow at a 5.20% CAGR to 2031 owing to infrastructure investment and rising infectious-disease burdens. Government programs in China, India, and Japan subsidize rapid dengue, mpox, and antimicrobial-resistance panels, which shortens adoption cycles. Digital health pilots link remote kits to teleconsults, increasing reach in rural regions.

Europe maintains steady demand and leads syndromic multiplex adoption. Fragmented reimbursement and data-privacy legislation slow cross-border digital-health scaling, yet antimicrobial-stewardship initiatives keep pressure on hospitals to deploy rapid diagnostics. Middle East and Africa markets remain smaller but are receiving donor-funded upgrades that create footholds for suppliers seeking geographic diversification within the infectious disease diagnostics market.

Competitive Landscape

M&A is accelerating as incumbents snap up niche innovators to access new chemistries and channels. Roche paid USD 295 million for LumiraDx’s point-of-care assets, bolstering its decentralized reach. Danaher’s USD 5.5 billion Abcam deal expanded its specialty reagent portfolio. bioMérieux acquired SpinChip to gain a 10-minute immunoassay for acute settings.

Disruptors such as BugSeq partner with BARDA to pair agnostic sequencing with AI analytics. QIAGEN is launching three prep instruments by 2026 to reinforce automation depth. Supply-chain lessons from COVID-19 are driving reshoring and dual-sourcing strategies, which could rebalance cost structures while enhancing resilience across the infectious disease diagnostics market.

Regulatory filings for multiplex panels, AI decision-support tools, and home kits hit record numbers in 2025. Early FDA clearances confer first-mover advantages and translate to shelf-space wins in retail channels. Consolidation among regional labs is concentrating buying power, so vendors with broad menus and integrated informatics tend to secure multi-year service bundles.

Infectious Disease Diagnostics Industry Leaders

BioMérieux SA

F. Hoffmann-La Roche Ltd

Abbott Laboratories

Becton, Dickinson and Company

Danaher

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Linear Diagnostics secures GBP 1 million (USD 1.3 million) for 5-minute EXPAR-based STI tests, aiming for rapid bacterial and viral detection.

- January 2025: bioMérieux buys SpinChip Diagnostics, adding a 10-minute immunoassay platform for acute infections

- June 2024: FDA grants CLIA waiver to BIOFIRE SPOTFIRE Respiratory/Sore Throat Panel Mini, enabling 15-minute multiplex PCR in outpatient settings

- January 2024: Roche acquires LumiraDx’s point-of-care technology for USD 295 million, expanding decentralized testing reach

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the infectious disease diagnostics market as all revenues from assays, kits, reagents, analyzers, software, and service contracts used to detect, identify, or quantify human pathogens in laboratory, point-of-care, and at-home settings worldwide. The definition covers molecular, immunological, microbiological, and emerging CRISPR-based platforms relied on by hospitals, stand-alone labs, clinics, public-health agencies, and OTC consumers.

Scope exclusion: veterinary tests and blood-donor screening panels are not included.

Segmentation Overview

- By Application

- Hepatitis (A, B, C, D, E)

- HIV / AIDS

- CT/NG & Other STIs

- Tuberculosis

- Respiratory (Influenza, RSV, COVID-19, Others)

- Vector-borne & Emerging Pathogens (Dengue, Zika, Mpox)

- Hospital-Acquired Infections (MRSA, C. diff, etc.)

- Others (Malaria, Lyme, Toxoplasmosis)

- By Product & Service

- Assays, Kits & Reagents

- Instruments & Analyzers

- Software & Informatics

- Services & Contract Testing

- By Technology

- PCR & qPCR

- Isothermal NAAT (LAMP, INAAT, TMA)

- Immunodiagnostics (ELISA, CLIA, LFIA)

- DNA/RNA Sequencing & NGS

- Microarray & Multiplex Panels

- CRISPR-based Diagnostics

- Metagenomic & Shotgun Sequencing

- By End User

- Hospital & Clinical Laboratories

- Reference / Central Laboratories

- Point-of-Care / Decentralised Settings

- Home-care & OTC Consumers

- Academic & Research Institutes

- By Test Setting

- Laboratory-based Testing

- Point-of-Care Testing

- Over-the-Counter / At-Home Testing

- By Sample Type

- Blood / Plasma / Serum

- Swab (NP/OP, Saliva)

- Urine

- Stool

- Other Fluids (CSF, Sputum, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Subsequently, we spoke with lab directors, infectious-disease clinicians, kit distributors, and procurement officers across North America, Europe, Asia-Pacific, and selected African nations. Their insights validated PCR cartridge adoption curves, average selling prices, and the rebound of hospital-acquired infection screening after the pandemic.

Desk Research

We began by reviewing tier-1 public sources such as WHO outbreak dashboards, CDC NNDSS releases, ECDC surveillance bulletins, national procurement notices, UN Comtrade cartridge codes, and peer-reviewed journals that benchmark assay sensitivity. Company 10-Ks, investor decks, and patent filings helped our team gauge pricing corridors and installed-base growth.

To verify financial splits, Mordor analysts pulled line items from D&B Hoovers and shipment-linked news via Dow Jones Factiva. These references framed the serviceable market; however, many additional reputable sources were consulted, and the list above is not exhaustive.

Market-Sizing & Forecasting

Our model starts with a top-down incidence-to-testing build that converts notifiable disease caseloads into potential test volumes, which are then reconciled with selective bottom-up supplier roll-ups and sampled ASP × volume checks. Key variables include vaccination-adjusted influenza prevalence, antimicrobial-resistance surveillance mandates, PCR platform installed base, respiratory-panel reimbursement shifts, and syndromic panel penetration. Forecasts use multivariate regression blended with scenario analysis so we can reflect funding shocks or outbreak cycles, while country gaps are bridged with region-level prevalence multipliers.

Data Validation & Update Cycle

Outputs pass multi-step variance checks against hospital billing databases, import records, and prior edition baselines before senior analyst sign-off.

Mordor refreshes the model every year and issues interim updates when material regulatory or epidemiologic events occur.

Why Mordor's Infectious Disease Diagnostics Baseline Earns Trust

Published estimates often diverge because definitions, data windows, and test-type granularity rarely align, a reality our clients recognize.

We find the largest gaps stem from narrower product scopes, unverified ASP assumptions, sporadic refresh cadences, and differing currency conversions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 46.81 B (2025) | Mordor Intelligence | - |

| USD 26.58 B (2025) | Global Consultancy A | excludes software and OTC tests; relies on vendor press releases for ASPs |

| USD 24.30 B (2024) | Trade Journal B | focuses on reagents only; limited geography weighting |

| USD 32.99 B (2024) | Industry Association C | mixes pandemic windfall with core segments; infrequent updates |

These comparisons show that Mordor's disciplined scoping, transparent variable selection, and annual refresh deliver a balanced, reproducible baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current value of the infectious disease diagnostics market?

The market is valued at USD 48.38 billion in 2026 and is forecast to reach USD 57.05 billion by 2031.

Which application segment is expanding the fastest?

Vector-borne and emerging pathogen testing is projected to grow at a 5.52% CAGR through 2031.

How quickly are CRISPR-based diagnostic technologies growing?

CRISPR assays are expected to post a 5.18% CAGR, challenging traditional PCR platforms.

Why is Asia-Pacific considered a high-growth region?

Rising healthcare investment, increasing disease burden, and supportive regulatory reforms drive a 5.20% CAGR in the region.

What factors are propelling at-home testing adoption?

Recent FDA approvals, consumer preference for convenience, and telemedicine integration are accelerating OTC diagnostics.

How will AI influence future infectious disease testing?

AI streamlines data analysis, improves quality control, and enables fully automated labs, thereby boosting productivity and accuracy.

Page last updated on: