Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

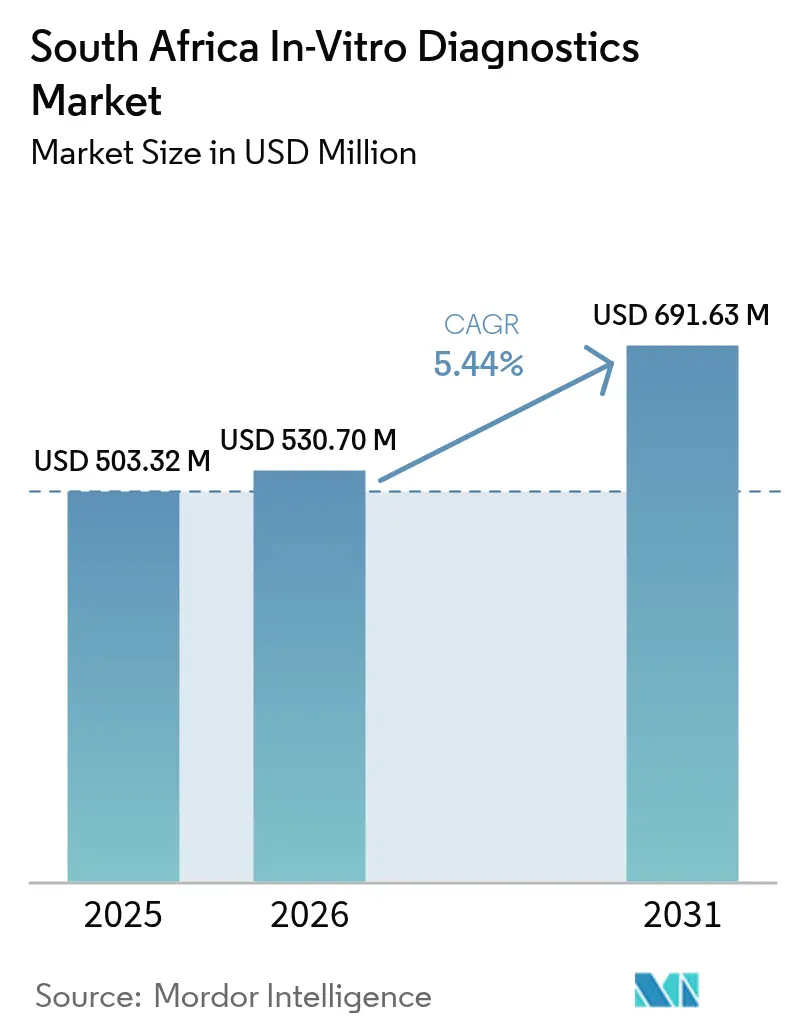

| Base Year Market Size (2025) | USD 503.32 Million |

| Market Size (2026) | USD 530.70 Million |

| Market Size (2031) | USD 691.63 Million |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The South Africa In-Vitro Diagnostics Market size was valued at USD 503.32 million in 2025 and is estimated to grow from USD 530.70 million in 2026 to reach USD 691.63 million by 2031, at a CAGR of 5.44% during the forecast period (2026-2031).

South Africa’s dual healthcare structure, where 85% of citizens depend on public facilities and 16% of insured residents are served by a well-funded private sector, drives strong demand for molecular and immuno-diagnostic platforms. However, rising operating costs from load shedding, currency-driven import inflation affecting 90% of devices, and stricter SAHPRA documentation guidelines (effective 2025) are increasing capital requirements. These challenges favor suppliers offering power-tolerant automation and compliant documentation. The National Health Insurance (NHI) Bill, passed in December 2023, is set to centralize procurement, potentially consolidating provincial tenders into national megacontracts, increasing volumes but pressuring reagent pricing in the South Africa in-vitro diagnostics market.

Private hospital groups are mitigating tariff pressures by implementing track-based laboratory automation to reduce labor costs. The public sector is focusing donor and Treasury funds on high-burden HIV and tuberculosis assays to maintain baseline test volumes. On the consumer side, pharmacy-led self-testing for HIV and glucose is normalizing home diagnostics, expanding the market beyond hospital laboratories. Local reagent production, supported by preferential procurement policies, is expected to enhance supply-chain resilience, though significant import reliance will likely persist until 2028.

Key Report Takeaways

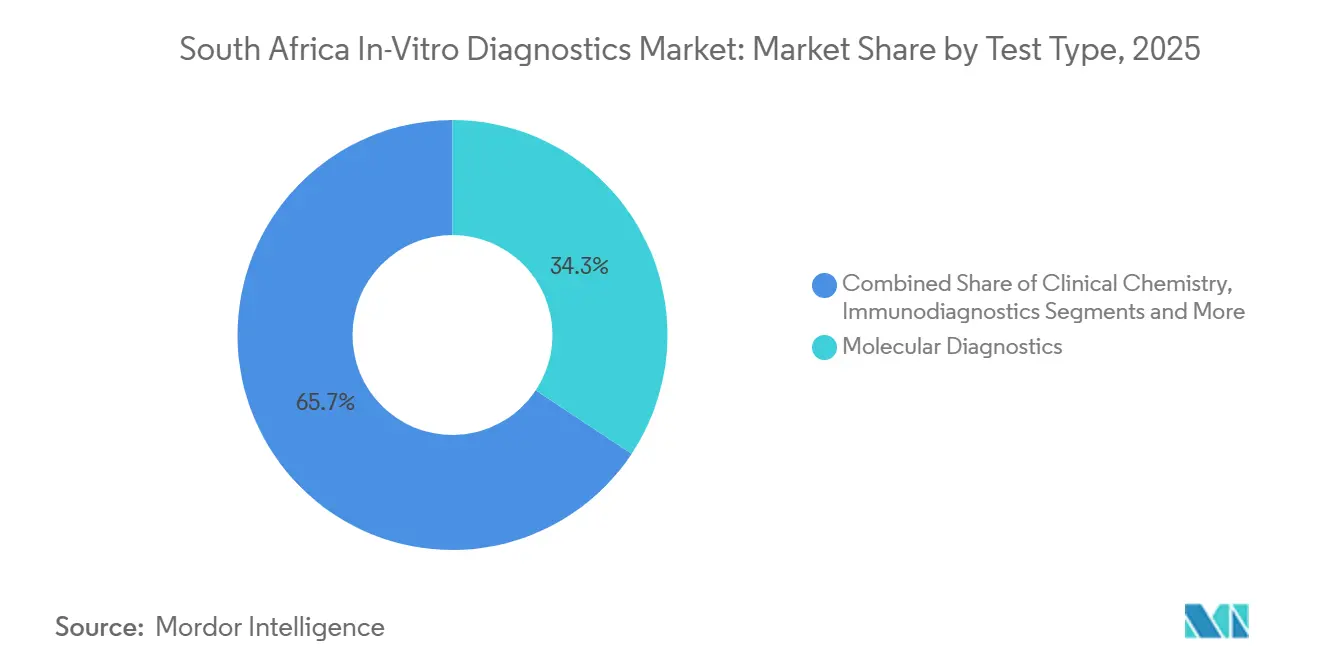

- By test type, molecular diagnostics led with 34.32% of South Africa in-vitro diagnostics market share in 2025, while immuno-diagnostics is projected to grow at a 7.54% CAGR through 2031.

- By product, reagents and kits accounted for 62.65% share of the South Africa in-vitro diagnostics market size in 2025, and software and services is expected to register the highest 8.21% CAGR over 2026-2031.

- By usability, disposable IVD devices captured 72.33% share of the South Africa in-vitro diagnostics market size in 2025; re-usable equipment is forecast to advance at a 7.87% CAGR to 2031.

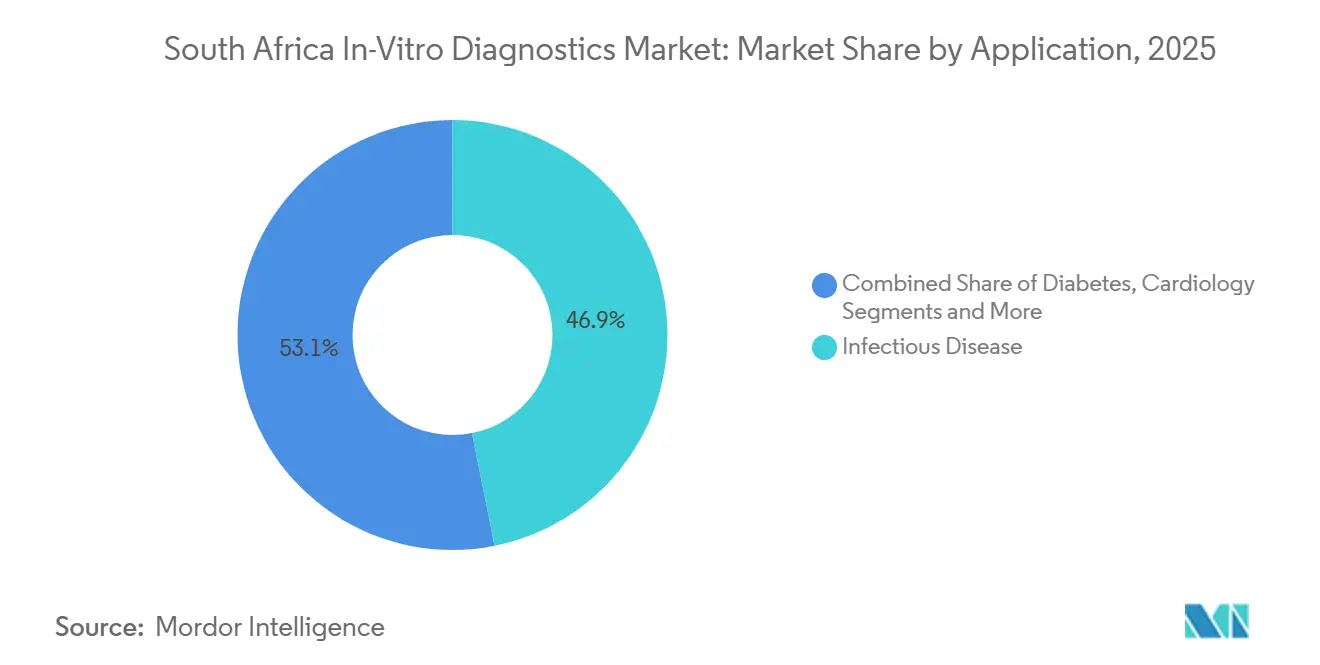

- By application, infectious diseases generated 46.87% of the South Africa in-vitro diagnostics market share in 2025, whereas oncology testing is poised for an 8.43% CAGR through 2031.

- By end user, hospital-based laboratories held 52.43% of the South Africa in-vitro diagnostics market share in 2025, and home-care and self-testing users are set to expand at a 6.54% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying HIV and tuberculosis disease burden | +1.2% | KwaZulu-Natal, Eastern Cape, Gauteng | Long term (≥ 4 years) |

| National Health Insurance rollout accelerating diagnostic spend | +0.9% | Pilot districts in Gauteng, Western Cape | Medium term (2-4 years) |

| Rapid uptake of point-of-care and self-testing platforms | +0.8% | National, peri-urban spill-over | Short term (≤ 2 years) |

| Laboratory automation and digital pathology adoption | +0.7% | Gauteng & Western Cape private hubs | Medium term (2-4 years) |

| Localization initiatives for reagent manufacturing | +0.5% | National, SADC export potential | Long term (≥ 4 years) |

| Growing investment in private hospital and clinic networks | +0.6% | Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying HIV and Tuberculosis Disease Burden

Roughly 7.9 million South Africans live with HIV, sustaining recurring demand for viral-load, CD4, and resistance assays that stabilize reagent pull-through for molecular and immuno platforms[1]National Department of Health, “HIV & TB Programme Report 2025,” health.gov.za. Tuberculosis remains a top mortality driver, anchoring thousands of Cepheid GeneXpert instruments, whose cartridge consumption accounts for 34.32% of 2025 test-type revenue. The emergence of extensively drug-resistant strains is accelerating whole-genome sequencing requests at tertiary centers, pressuring budgets but heightening clinical urgency. PEPFAR taper risk has triggered domestic financing conversations, including ring-fenced sin tax proceeds, to shield essential testing volumes. Winter respiratory surges push provincial labs near capacity, strengthening the case for point-of-care PCR units in primary clinics that circumvent courier delays and protect the South Africa in-vitro diagnostics market continuity.

National Health Insurance Rollout Accelerating Diagnostic Spend

The NHI Act positions a single public purchaser to negotiate national-scale IVD contracts, potentially boosting aggregate reagent volumes while tightening price ceilings. Early pilot districts bought basic chemistry and hematology panels first, signaling an incremental approach focused on high-volume, low-complexity assays. Private schemes, uncertain of their post-NHI mandate, are piloting value-based bundles that weave diagnostics into chronic-disease capitation models to justify parallel funding streams. During the 2026-2027 transition, provincial health departments are deferring analyzer upgrades, whereas private hospital groups are front-loading automation investments to lock in efficiency before state tariff realignment. The policy therefore injects medium-term procurement volatility yet lifts long-run test penetration across uninsured populations, ultimately enlarging the South Africa in-vitro diagnostics market.

Rapid Uptake of Point-Of-Care and Self-Testing Platforms

COVID-19 normalized at-home swabbing and teleconsultations, priming consumers to purchase HIV self-tests and glucose meters directly from pharmacies. SAHPRA over-the-counter approval expanded retail availability, though unit sales remain urban-skewed given ZAR 80-150 price points. Portable PCR and isothermal systems are reaching nurse-run clinics, trimming TB result turnaround from days to under two hours, albeit at higher per-test costs that still require donor co-funding. Diabetes prevalence, forecast by the International Diabetes Federation to climb from 4.2 million adults in 2021 to 7.5 million by 2045, underpins rising uptake of continuous glucose monitors in employer wellness programs. Reimbursement inconsistency by medical schemes continues to cap penetration, yet momentum remains net positive for the South Africa in-vitro diagnostics market.

Laboratory Automation and Digital Pathology Adoption

Netcare, Life Healthcare, and Mediclinic—controlling nearly 70% of private beds—are installing track-based automation that chains pre-analytics, core testing, and post-analytics under one roof, slicing turnaround times by up to 40% and partially insulating operations from load-shedding disruptions through battery-backed robotics. Life Healthcare’s 2024 purchase of 45 Fresenius dialysis centers includes integrated diagnostic IT, strengthening vertical control over nephrology testing. Digital pathology, propelled by AI-equipped whole-slide scanners, addresses national histopathologist shortages and enables remote reads from rural hospitals. SAHPRA’s 2025 software-as-medical-device guidance compels suppliers to document cyber-secure code and quality management alignment with IEC 62304, elevating entry barriers yet ensuring data integrity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency and import tariff volatility raising test costs | -0.6% | National, import-dependent labs | Short term (≤ 2 years) |

| Regulatory approval & reimbursement delays for novel assays | -0.4% | National | Medium term (2-4 years) |

| Infrastructure gaps including power outages and cold-chain breaks | -0.5% | Gauteng, Western Cape, KwaZulu-Natal | Short term (≤ 2 years) |

| Proliferation of sub-standard or grey-market test kits | -0.3% | Informal trade channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Inflating Imported Reagent Prices

South Africa imported ZAR 44 billion (USD 2.45 billion) worth of pharmaceuticals in 2023 versus ZAR 8 billion (USD 0.45 billion) in exports, highlighting deep reliance on external supply chains. With reagents representing 66.29% of the South Africa in vitro diagnostics market size, even single-digit rand depreciation raises per-test costs and squeezes laboratory margins. Collection materials already account for 21.4% of total lab spend while staff costs consume 59.9%, leaving little headroom for price shocks[3]. Smaller district facilities often lack hedging capacity and face reagent stock-outs that interrupt service continuity. Consequently, procurement agencies are exploring multi-year framework contracts and local reagent formulation partnerships to mitigate currency risk.

Infrastructure Gaps Including Power Outages and Cold-Chain Breaks

Eskom’s stage-6 load shedding interrupts analyzer cycles mid-run, causes reagent spoilage, and prolongs result turnaround, particularly in clinics lacking diesel generators. Medium-sized labs spend up to ZAR 2 million on backup systems and annual maintenance, a burden difficult to recoup under flat tariff schedules. Temperature excursions invalidate sensitive immuno- and molecular-kits, compelling emergency air-freight reorders at premiums exceeding 30%. Rural clinics, already technology-sparse, often shut down point-of-care PCR entirely during outages, shifting specimen flow back to over-stretched urban hubs. High data-link costs and patchy broadband slow laboratory information system adoption, hindering the digital traceability essential for NHI interoperability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Platforms Anchor Share, Immuno-Diagnostics Accelerate

Molecular diagnostics captured 34.32% of 2025 revenue, reflecting entrenched GeneXpert MTB/RIF capacity and pandemic-era PCR scale-up. The South Africa in-vitro diagnostics market size for molecular assays is expected to rise 5.1% annually as drug-resistance surveillance expands. Yet immuno-diagnostics will outpace all peers with a 7.54% CAGR, fueled by chemiluminescent analyzers that bundle tumor markers and cardiac panels for private hospitals demanding quick, high-margin assays.

Clinical chemistry retains the daily-volume crown but endures price deflation that nudges suppliers toward cross-selling integrated immuno-analyzer packages. Hematology is mid-refresh, shifting to five-part differentials that enhance sepsis detection and reduce manual smears, while microbiology growth moderates as syndromic molecular panels cannibalize culture work. High-sensitivity coagulation tests and point-of-care INR meters gradually redistribute volume from central labs to nurse-run outpatient clinics, diversifying the South Africa in-vitro diagnostics market revenue base without materially altering test-type rankings.

By Product: Reagents Dominate, Software and Services Surge

Reagents and kits delivered 62.65% of 2025 turnover, an illustration of the razor-and-blade model underpinning South Africa in-vitro diagnostics market share economics. Annual volume contracts with medical schemes drive bulk discounts, yet suppliers defend margins through bundled calibrators and mandatory QC consumables.

Instruments constitute a cyclical capex stream but are increasingly placed under reagent-rental pacts that swap upfront cash for multi-year volume guarantees. Software and services, currently just 8% of revenue, are projected to climb fastest at 8.21% CAGR as LIS upgrades and remote uptime monitoring become indispensable for multi-site hospital groups. Post-market surveillance stipulations in the 2025 SAHPRA guideline further entrench recurring service fees, expanding the South Africa in-vitro diagnostics industry digital layer.

By Usability: Disposables Lead, Re-Usable Equipment Gains Traction

Single-use cartridges, strips, and rapid tests accounted for 72.33% of 2025 dollars, underpinned by infection-control culture and pharmacy retail channels. This disposable preference protects operator safety and maintains tight process flow in facilities dealing with multidrug-resistant TB.

Re-usable analyzers, though just 27.7% of current spend, will grow 7.87% annually as private hubs install high-throughput systems that amortize capital over soaring specimen volumes. Load-shedding-tolerant battery kits on re-usable platforms are gaining marketing traction, particularly where cold-chain disruptions degrade cartridge shelf-life. Combined, these trends balance consumable and capital segments, broadening total South Africa in-vitro diagnostics market opportunity.

By Application: Infectious Diseases Dominate, Oncology Surges

Infectious disease testing generated 46.87% of 2025 application revenue, a direct outcome of HIV/TB dual epidemics. The South Africa in-vitro diagnostics market for infectious panels is projected to grow 4.8% annually, driven by reflex resistance genotyping mandates in updated national guidelines.

Oncology is the standout growth story at 8.43% CAGR as private labs adopt next-generation sequencing and ctDNA liquid biopsies to enable precision therapy reimbursement. Diabetes, cardiac, and renal panels track population aging curves, while autoimmune and therapeutic drug monitoring expand from low bases, together enriching the diagnostic mix and diversifying risk across the South Africa in-vitro diagnostics market.

By End User: Hospitals Lead, Home-Care Expands

Hospital laboratories contributed 52.43% of 2025 value, reflecting complex assay concentration and medical-scheme reimbursement alignment. Stand-alone reference labs capture overflow and GP-office referrals but keep pricing keen to defend share against in-house hospital automation.

Home-care and self-testing will log a 6.54% CAGR, supported by SAHPRA-approved OTC HIV kits, rising CGM reimbursement, and lingering telehealth habits post-pandemic. Pharmacy clinics and corporate wellness centers act as intermediate hubs, accelerating decentralization and embedding diagnostics into everyday consumer routines, thereby stretching the South Africa in-vitro diagnostics industry beyond institutional walls.

Competitive Landscape

Multinationals—Abbott, Roche, Siemens Healthineers, Danaher’s Beckman Coulter and Cepheid, and BD—command roughly 65% of total revenue through installed-base lock-in and nationwide service teams. Local assemblers such as CapeBio, Davies Diagnostics, and Medical Diagnostech pursue niche reagent and point-of-care markets, leveraging preferential procurement credits to secure public tenders. Switching costs for large analyzers can reach ZAR 5 million, fostering sticky reagent contracts.

Life Healthcare’s 2024 purchase of Fresenius’s dialysis assets, cleared with behavioral remedies by the Competition Tribunal, signals intensified vertical integration as hospital chains seek pathology revenue streams[2]. Asian challengers Mindray and Sysmex undercut capital pricing yet face skepticism over reagent logistics and long-term uptime guarantees.

Technology differentiation now rests on middleware and automation. Siemens’ Atellica and Beckman’s DxA 5000 lines tout track-based robotics and AI QC dashboards, while Abbott’s Alinity promises compact footprints for space-pressed city labs. SAHPRA’s 2025 clinical-evaluation rulebook increases regulatory overhead, fortifying the moat around incumbents who already hold ISO-aligned quality files and reinforcing moderate concentration in the South Africa in-vitro diagnostics market.

South Africa In-Vitro Diagnostics Industry Leaders

Siemens Healthineers

Abbott Laboratories

F. Hoffmann-La Roche Ltd

Danaher Corp.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cytespace Africa Laboratories (Cytespace), an MLM Medical Labs company and the only fully CAP-accredited central laboratory in South Africa, has significantly expanded its molecular testing capabilities to meet rising demand across Sub-Saharan Africa.

- September 2025: SAHPRA released final clinical-evaluation guidelines aligned with ISO 14155:2020, tightening evidence standards for IVD registration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines South Africa's in-vitro diagnostics (IVD) market as all reagent kits, analyzers, software, and related services used to test human blood, urine, and tissue outside the body for screening, diagnosis, or therapeutic monitoring inside formal laboratories, hospitals, and approved point-of-care (POC) settings.

Scope exclusion: Veterinary, research-only, and purely export-oriented test systems fall outside the frame of this assessment.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immuno-Diagnostics

- Molecular Diagnostics

- Hematology

- Coagulation

- Microbiology

- Other Test Types

- By Product

- Instruments

- Reagents & Kits

- Software & Services

- By Usability

- Disposable IVD Devices

- Re-Usable Equipment

- By Application

- Infectious Diseases

- Diabetes

- Oncology

- Cardiology

- Auto-Immune Disorders

- Nephrology

- Other Applications

- By End User

- Stand-Alone Laboratories

- Hospital-Based Laboratories

- Point-Of-Care Settings

- Home-Care & Self-Testing Users

Detailed Research Methodology and Data Validation

Primary Research

Our analysts conducted structured interviews with laboratory directors across Gauteng and Western Cape, purchasing managers at three private hospital groups, and distributors of POC devices in peri-urban clinics. Follow-up surveys with clinical pathologists and epidemiologists helped verify test-volume growth, reagent wastage rates, and forecast assumptions for emerging oncology panels.

Desk Research

We gathered foundational figures from public sources such as the National Health Laboratory Service annual reports, the South African National Department of Health tender database, Statistics SA trade codes, UNAIDS HIV surveillance, and the WHO Global Health Observatory. Company filings and investor decks helped flag average selling prices, while D&B Hoovers and Dow Jones Factiva provided cross-checks on supplier revenue exposure. Academic journals and the Southern African Society for Clinical Pathology proceedings supplied granular utilization ratios for key test panels. The sources cited above illustrate, not exhaust, the reference set consulted during desk work.

A second sweep focused on macro variables that steer demand, including medical-scheme enrollment, National Health Insurance budget releases, and quarterly import volumes for HS codes 3822, 3002, and 9018. These datasets, combined with patent search hits from Questel on molecular assays, shaped early trend vectors before we moved to field validation.

Market-Sizing & Forecasting

The core model starts with a top-down reconstruction of national test expenditures drawn from NHLS spend plus private-sector claims, which are then split by segment using prevalence-to-test and instrument install-base ratios. Select bottom-up roll-ups, for instance, sampled reagent ASP multiplied by unit shipments from customs, serve as guardrails for each segment. Key variables include HIV viral-load monitoring volumes, diabetic population growth, reagent import price inflation, POC penetration in primary-care clinics, and oncology test adoption curves. A multivariate ARIMA framework forecasts each driver; scenario analysis on currency swings and NHI funding adjusts the outer range. Data gaps on fragmented physician-office testing are bridged with calibrated penetration coefficients derived from primary calls.

Data Validation & Update Cycle

Before sign-off, model outputs pass variance checks against historical trade data and insurer claim totals. An additional analyst, not involved in modeling, reviews anomalies. Reports refresh yearly, and interim updates trigger when policy or reimbursement shifts move the baseline by more than five percent.

Why Mordor's South Africa In-Vitro Diagnostics Baseline Is Dependable

Published figures often differ because firms adopt distinct product scopes, price assumptions, and refresh cadences. Our disciplined alignment to nationally reported spend, coupled with targeted bottom-up checks, narrows those gaps for decision-makers.

Key differences arise when other publishers blend veterinary kits, bundle packaging revenues, or apply flat price escalators without testing volume elasticity. Some rely on three-year-old input data; Mordor Intelligence revisits inputs annually and layers currency normalization at transaction-level depth.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 503.32 mn (2025) | Mordor Intelligence | - |

| USD 739.3 mn (2024) | Global Consultancy A | Includes research reagents and multi-country OEM sales booked in South Africa |

| USD 600 mn (2024) | Trade Journal B | Applies uniform reagent ASPs and omits public-sector price caps |

Overall, the comparison shows that our stepwise scope definition, annual data refresh, and dual-path modeling deliver a balanced, transparent baseline clients can retrace with confidence.

Key Questions Answered in the Report

What CAGR is projected for the South Africa in-vitro diagnostics market between 2026 and 2031?

The market is forecast to grow at a 5.44% CAGR over 2026-2031.

Which test type currently holds the largest revenue share?

Molecular diagnostics led with 34.32% of 2025 revenue.

Which application segment is expanding fastest through 2031?

Oncology testing is projected to accelerate at an 8.43% CAGR.

How will National Health Insurance affect IVD procurement?

NHI will centralize buying power, boosting volumes but likely tightening reagent price ceilings.

What infrastructure issue most disrupts laboratory operations?

Eskom load shedding causes analyzer downtime and cold-chain breaches, increasing operational costs.

Which provinces generate the highest diagnostic spend?

Gauteng, Western Cape, and KwaZulu-Natal together account for about three-quarters of national revenue.

How large is the South Africa in-vitro diagnostics market in 2026?

The South Africa in-vitro diagnostics market is estimated to grow from USD 530.70 million in 2026 to reach USD 691.63 million by 2031.

Page last updated on: