Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.05 Billion |

| Market Size (2026) | USD 4.25 Billion |

| Market Size (2031) | USD 5.41 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

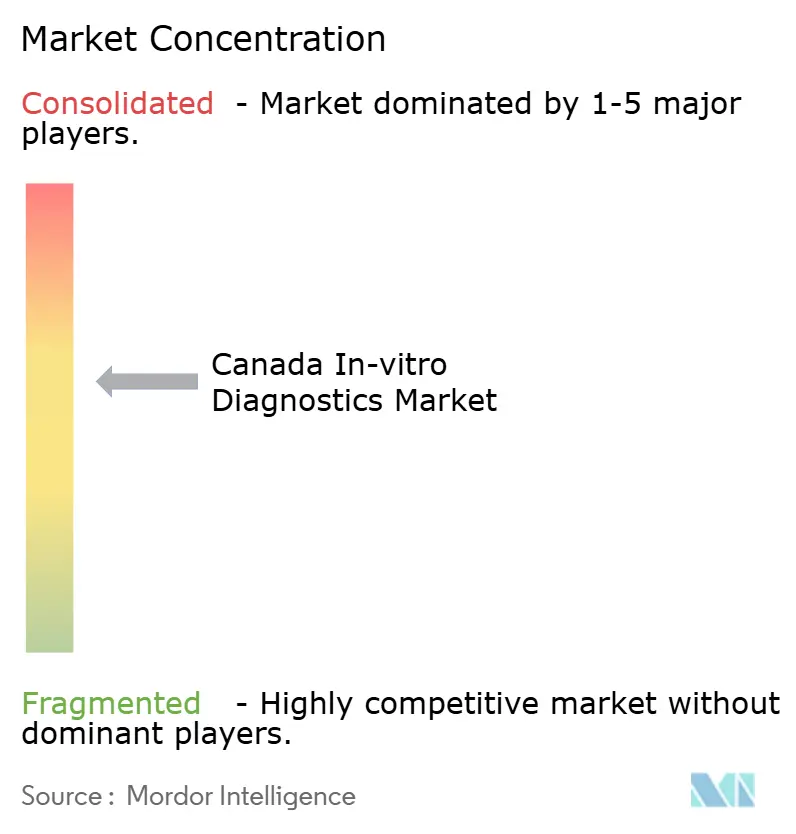

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada In-vitro Diagnostics Market Analysis by Mordor Intelligence

The Canada in-vitro diagnostics market size in 2026 is estimated at USD 4.25 billion, growing from 2025 value of USD 4.05 billion with 2031 projections showing USD 5.41 billion, growing at 4.93% CAGR over 2026-2031. Rising healthcare spending that hit USD 372 billion in 2024, equivalent to 12.4% of national GDP, is creating headroom for test adoption. Demand is further amplified by a growing chronic-disease burden, government commitments exceeding USD 200 billion to modernize the system, and rapid uptake of molecular and digital platforms. Consolidation among large laboratories, the pivot toward decentralized testing, and provincial push for preventive screening programs are reinforcing steady volume growth. Competitive intensity is increasing as global majors introduce precision-oriented solutions and capitalize on Health Canada’s comparatively flexible stance toward laboratory-developed tests.

Key Report Takeaways

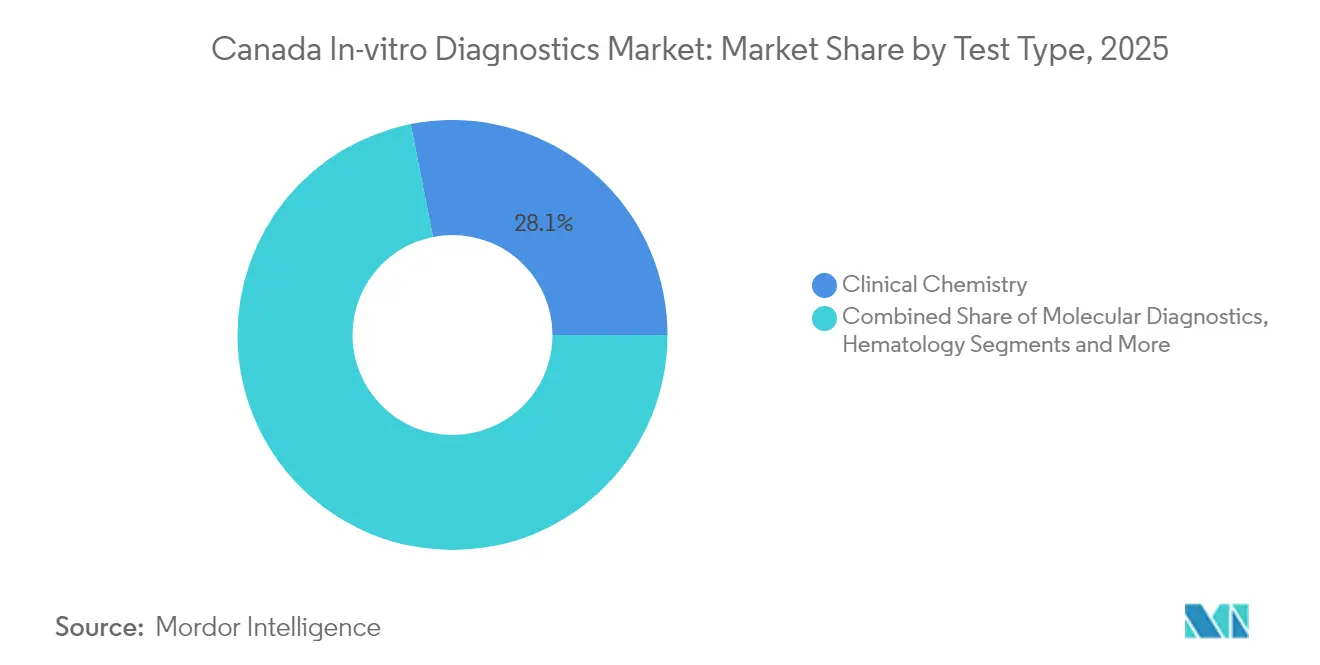

- By test type, Clinical Chemistry led with 28.12% share in 2025, whereas Molecular Diagnostics is projected to advance at a 10.42% CAGR from 2026 to 2031.

- By product, Reagents & Kits captured 62.14% of the Canada in-vitro diagnostics market share in 2025; Software & Services are forecast to grow at a 9.55% CAGR to 2031.

- By usability, Disposable IVD Devices accounted for 70.63% of the Canada in-vitro diagnostics market size in 2025, while Reusable IVD Devices are set to expand at a 9.05% CAGR through 2031.

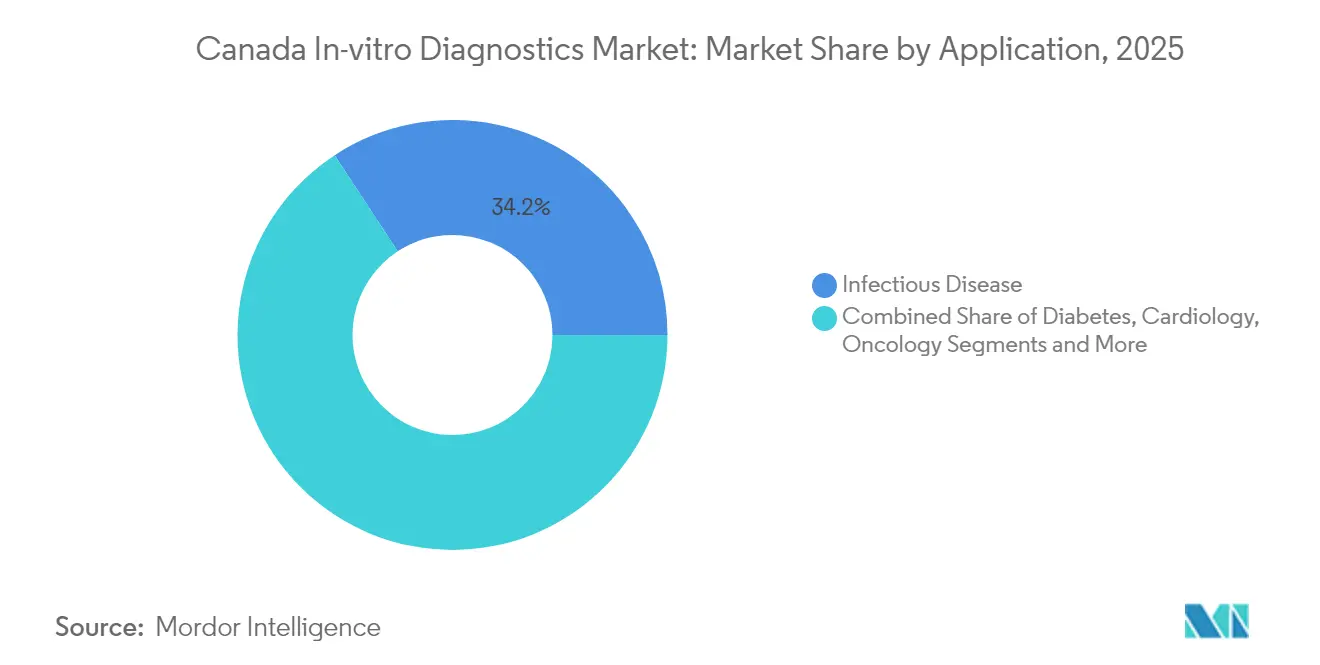

- By application, Infectious Disease testing held 34.23% revenue share in 2025, but Cancer/Oncology diagnostics will rise fastest at a 10.55% CAGR to 2031.

- By end user, Diagnostic Laboratories secured 45.74% share in 2025, whereas Home Care Settings are projected to grow quickest at an 8.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada In-vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of Chronic & Infectious Diseases | +1.2% | National, with higher impact in provinces with aging populations (Ontario, Quebec, British Columbia) | Long term (≥ 4 years) |

| Government-Led Healthcare Capacity Expansion & Modernization | +0.9% | National, with emphasis on underserved provinces and territories | Medium term (2-4 years) |

| Rising Adoption of Advanced Diagnostic Technologies | +0.7% | Urban centers initially, with gradual expansion to rural areas | Medium term (2-4 years) |

| Favorable National Screening & Preventive Health Programs | +0.5% | National, with provincial variations in implementation | Medium term (2-4 years) |

| Expanding Health-Insurance Coverage Including Mandatory Expat Benefits | +0.4% | National, with emphasis on provinces with higher immigrant populations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic & Infectious Diseases

Nineteen percent of Canadians were aged 65 or older in 2024, a ratio expected to climb to 22.5% in coming years, intensifying demand for early diagnostic services. Long-COVID adds complexity, with 1 in 5 adults reporting persistent symptoms and 100,000 unable to work as of December 2023[1]Office of the Chief Science Advisor, “Post-COVID Condition and its Continued Impact,” Science.gc.ca. These overlapping pressures are funneling public and private investment toward molecular and point-of-care assays capable of detecting chronic and infectious conditions earlier. As molecular diagnostics penetrate routine workflows, demand is shifting from static chemistry panels to high-value genomic and proteomic tests. This structural change underpins long-run volume and value growth for the Canada in-vitro diagnostics market.

Government-Led Healthcare Capacity Expansion & Modernization

Federal and provincial authorities have pledged more than USD 200 billion over ten years to widen family health services, clear backlogs, fortify mental-health supports, and digitize systems. Laboratory upgrades and cloud-enabled data platforms form a core element of this strategy, opening opportunities for integrated testing ecosystems. New policy guidance for machine-learning medical devices signals Health Canada’s intent to nurture innovation while maintaining safety standards. Collectively, these initiatives expand addressable budgets and accelerate procurement cycles for advanced testing instruments and software across the Canada in-vitro diagnostics market.

Rising Adoption of Advanced Diagnostic Technologies

Molecular assays are growing at twice the overall market pace, reflecting their central role in precision-therapy decisions. A 2024 survey of oncologists highlighted gaps in biomarker testing access linked to limited standardization and financial hurdles. Manufacturers are responding with platforms such as Roche’s Digital LightCycler and self-collection HPV assays that combine automation, high sensitivity, and seamless data flow. Broader availability of next-generation sequencing is expected to embed genomic profiling into routine cancer care, supporting sustained expansion of the Canada in-vitro diagnostics market.

Favorable National Screening & Preventive Health Programs

Pan-Canadian newborn-screening recommendations released in March 2025 standardized testing for 25 conditions, with scope to add 29 more[2]Canada’s Drug Agency, “Newborn Screening Recommendations,” cda-amc.ca. Digital pathology pilots in British Columbia, funded at USD 2.65 million, illustrate the push to leverage AI for earlier detection, especially in rural communities. Preventive initiatives create predictable demand for assay kits, reagents, and analytics platforms, bolstering the medium-term outlook for the Canada in-vitro diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technical Complexity and Need for Skilled Personnel | -0.7% | National, with greater impact in rural and remote areas | Medium term (2-4 years) |

| High Cost of Diagnostic Equipment and Tests | -0.4% | National, with greater impact in smaller provinces with limited healthcare budgets | Short term (≤ 2 years) |

| Stringent Regulatory and Approval Processes | -0.3% | National, with particular impact on innovative diagnostic technologies and smaller companies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technical Complexity and Need for Skilled Personnel

Advanced molecular and digital platforms require specialized operators, yet expertise is unevenly distributed. A 2025 systematic review flagged infrastructure gaps and staffing shortages as key barriers to community-based molecular testing. Certification frameworks advocated by the Canadian Society of Clinical Chemists underscore the training burden for widespread point-of-care deployment. These manpower constraints slow test adoption in underserved areas, tempering growth potential for the Canada in-vitro diagnostics industry.

High Cost of Diagnostic Equipment and Tests

New MRI and CT scanners cost roughly USD 2 million, surpassing the USD 1.5 million tax-depreciation cap under the Immediate Expensing Incentive program. Two-thirds of imaging equipment is already over five years old, driving wait times and prompting calls for USD 1 billion in capital upgrades. Termination of federal funding for HIV self-testing kits after spending USD 17 million in two years highlights vulnerability of access programs to fiscal pressures. These cost headwinds could dampen near-term expansion of the Canada in-vitro diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Redefining Clinical Practice

Clinical Chemistry retained 28.12% of Canada in-vitro diagnostics market share in 2025, reflecting its entrenched role in chronic-disease management. Molecular Diagnostics, projected to grow at a 10.42% CAGR, is gradually reshaping care pathways by enabling rapid pathogen identification and comprehensive genomic profiling. Investments such as the USD 18.9 million PREPARED initiative will deploy molecular testing across 50 sites, embedding PCR and sequencing workflows into frontline practice. Hematology, Microbiology, Immuno-Diagnostics, Coagulation, and Urinalysis remain critical for specific clinical decisions, yet none match the velocity of molecular uptake. As assay menus widen and reimbursement stabilizes, Molecular platforms are expected to claim a larger slice of the Canada in-vitro diagnostics market size by 2030.

Hematology analyzers underpin efficient blood-disorder work-ups, while Microbiology laboratories diversify into multiplex PCR to tackle antimicrobial resistance. Immuno-Diagnostics supports autoimmune monitoring and therapeutic-drug management, whereas Coagulation testing gains relevance in an aging population with cardiovascular risk. Affordable dipstick Urinalysis persists in primary care due to simplicity. However, the precision and speed of sequencing and digital PCR offer clear clinical advantages, positioning Molecular Diagnostics as the signature growth engine of the Canada in-vitro diagnostics market.

By Product: Digital Integration Transforming Test Ecosystems

Reagents & Kits generated 62.14% of revenue in 2025, underlining their consumable nature and resilient demand curve. Instruments face slower turnover because capital budgets remain constrained; many facilities operate legacy analyzers older than five years. Software & Services, though smaller, will register the fastest 9.55% CAGR as laboratories integrate cloud analytics, artificial intelligence, and workflow automation. Roche’s navify suite exemplifies the shift toward data-driven diagnostics that connect disparate sites and improve clinical decisions.

Ongoing supply-chain reinforcement since the pandemic has prompted multi-vendor sourcing strategies for reagents, while proposed tax changes to raise the expensing limit to USD 5 million could accelerate instrument upgrades. Altogether, digitization is expanding the value pool beyond wet chemistry, enlarging long-term potential for the Canada in-vitro diagnostics market.

By Usability: Disposable Devices Dominate Despite Sustainability Concerns

Disposable IVD Devices captured 70.63% of the segment in 2025 thanks to infection-control benefits and minimal maintenance requirements. Large-scale distribution of rapid antigen tests during COVID-19 embedded disposables into public health routines. Yet Reusable Devices are forecast to climb at a 9.05% CAGR as hospitals weigh environmental and cost implications. Advances in material science facilitate rigorous decontamination, reducing contamination risk and extending device lifespans.

Health Canada regulates both categories under the Medical Devices Regulations (SOR/98-282), with risk-based classification dictating evidence thresholds. Sustainability-oriented procurement guidelines may nudge laboratories toward reusable analyzers where feasible, gradually balancing the usability mix within the Canada in-vitro diagnostics market.

By Application: Precision Oncology Driving Diagnostic Innovation

Infectious Disease assays led with 34.23% revenue share in 2025, anchored by expanded respiratory-virus testing capacity. Cancer/Oncology testing is set to outpace all other applications at a 10.55% CAGR, propelled by biomarker-guided therapy protocols and funding such as Pfizer Canada’s USD 1.1 million grant program. Diabetes, Cardiology, Autoimmune, Nephrology, Blood Screening, and Prenatal segments continue to address population-specific needs, yet oncology’s escalation in test volume and complexity will increasingly influence revenue mix.

The proposed USD 25 million national molecular profiling network aims to standardize oncology diagnostics, potentially broadening patient access and reducing geographic disparities. These initiatives solidify oncology’s role as a primary catalyst for the Canada in-vitro diagnostics market size expansion.

By End User: Home Care Settings Disrupting Traditional Models

Diagnostic Laboratories accounted for 45.74% of test volume in 2025, fortified by Quest Diagnostics’ planned CAD 1.35 billion acquisition of LifeLabs. Hospitals and Clinics maintain substantial demand for acute-care assays, while Point-of-Care Centers bridge access gaps with rapid turnaround. Home Care Settings, projected to grow at an 8.25% CAGR, represent the vanguard of decentralized healthcare. Wearable sensors, mail-in genetic panels, and digitally guided rapid tests foster patient autonomy and reduce system load.

Quality-assurance frameworks such as MDSAP audit requirements are being adapted to cover decentralized platforms. As reimbursement catches up, home-based testing is expected to command a larger proportion of the Canada in-vitro diagnostics market.

Geography Analysis

Ontario, Quebec, and British Columbia collectively account for more than half of Canada in-vitro diagnostics market revenue, reflecting dense populations, teaching hospitals, and research centers. Alberta and Saskatchewan contribute meaningful volume via centralized laboratory networks that serve widely dispersed communities. Atlantic provinces and the territories trail in absolute terms but are experiencing above-average uptake of point-of-care devices due to infrastructure constraints. Government programs targeting underserved regions are funneling funds toward mobile clinics and cloud-linked laboratories, gradually narrowing service gaps. Urban centers lead early adoption of molecular assays, whereas rural areas initially rely on traditional chemistry panels due to staffing limitations. Investments in broadband and provincial cloud services are expected to redistribute digital testing capacity over the forecast horizon. The PREPARED pathogen-surveillance network, operating at 50 sites across the country, exemplifies nationwide initiatives designed to harmonize diagnostic standards and real-time data sharing. Altogether, geographical expansion of advanced testing will underpin steady growth in Canada in-vitro diagnostics market penetration across every province.

Regulatory Landscape

Health Canada regulates in vitro diagnostic devices (IVDDs) under the Medical Devices Regulations (SOR/98-282) using a four-class, risk-based classification system (Class I to Class IV). Higher-risk Class III and IV IVDs face more extensive premarket evidence requirements. Market access generally requires a Medical Device Licence (MDL) before sale, and Class III/IV submissions increasingly align to International Medical Device Regulators Forum (IMDRF) expectations for application structure and supporting performance evidence.

Quality-system compliance is anchored by Medical Device Single Audit Program (MDSAP) certification issued by recognized auditing organizations, which is widely used by manufacturers to support licensing and ongoing compliance in Canada. On the trade and procurement side, CUSMA remains a key framework for duty-free access for qualifying medical devices. Industry bodies such as Medtech Canada have also pointed to how provincial procurement practices, including Ontario procurement restriction policies, can act as practical barriers for supplier participation and tender competitiveness even when federal trade conditions are met.

Competitive Landscape

The top manufacturers— Becton, Dickinson and Company, Abbott, Siemens Healthineers, and Danaher —hold a sizeable slice of the Canada in-vitro diagnostics market, enabling scale advantages in R&D, distribution, and regulatory affairs. Competitive pressures escalated after Quest Diagnostics moved to acquire LifeLabs, bringing 382 collection centers and 16 laboratories under its umbrella and signaling aggressive expansion by U.S. majors into Canadian territory. Emerging players are expected to pursue niche segments such as liquid biopsy or AI-enabled image analysis to differentiate.

Innovation remains the primary weapon: Roche’s cobas HPV self-collection and Digital LightCycler platforms target high-growth niches in women’s health and rare-mutation detection. Siemens is integrating Atellica CI analyzers for mid-volume labs, while Abbott expands point-of-care portfolios to home settings. Health Canada’s lighter oversight of laboratory-developed tests, relative to imminent FDA regulations, offers domestic labs flexibility to partner with diagnostic firms on bespoke assays, potentially lowering entry barriers for innovative SMEs.

Pricing competition remains moderate due to the importance of bundled reagent-service contracts and the technical switching costs associated with analyzer platforms. However, purchasing coalitions among provincial health authorities are negotiating volume discounts, nudging vendors toward value-based pricing models and integrated service agreements. Over the forecast period, digital connectivity, automation, and sample-to-answer molecular platforms will define competitive advantage within the Canada in-vitro diagnostics market.

Canada In-vitro Diagnostics Industry Leaders

Bio-Rad Laboratories Inc.

Danaher Corporation

Siemens Healthineers

Abbott Laboratories

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Point-of-care and self-testing are creating visible whitespace in infectious disease and community screening, supported by multiple 2026 Health Canada licensing actions. BioLytical Laboratories received Health Canada authorization in May 2026 for its iStatis Hepatitis B Surface Antigen rapid test (manufactured in Richmond, British Columbia). OraSure received a Health Canada license in February 2026 for OraQuick HIV Self-Test, described as the first oral HIV self-test in Canada through an exclusive distribution arrangement with St. Michael's Hospital (Unity Health Toronto). These launches expand test formats and access channels that align with decentralized testing and public health screening needs.

Specialized molecular and precision diagnostics also have near-term adoption pathways through provincial and laboratory capability build-out. Rapid Novor received a provisional license from the Ontario Ministry of Health in March 2026 for its EasyM blood-based MRD assay for multiple myeloma. Dynacare inaugurated a new diagnostic and precision medicine laboratory in Laval's Biotech City in March 2026, with the $5+ million investment supporting demand for instruments, reagents, and software for advanced workflows. Supply resilience and local production are also being used as procurement differentiators, including SEKISUI Diagnostics and the Government of Prince Edward Island announcing a CAD 16 million investment to expand reagent contract manufacturing capabilities at Charlottetown facilities. This is intended to support reagent availability and contract manufacturing options for IVD vendors serving Canadian laboratories.

Recent Industry Developments

- July 2026: Bio-Rad Laboratories launched Vericheck ddPCR Kits compatible with the QX700 platform, targeting biopharma quality control and cell and gene therapy workflows. The release expands menu pull-through for digital PCR consumables and strengthens Bio-Rad's position in higher-value molecular applications relevant to Canadian labs and advanced therapy manufacturing ecosystems.

- May 2026: bioLytical Laboratories received Health Canada authorization for its iStatis Hepatitis B Surface Antigen (HBsAg) Test, described as the first point-of-care rapid test for hepatitis B in North America. Manufacturing in Richmond, British Columbia supports domestic supply and adds a new rapid-testing option for community screening and decentralized care settings.

- March 2025: Canada's Drug Agency issued pan-Canadian newborn-screening recommendations covering 25 conditions, with a pathway to add additional conditions in future updates. The harmonized recommendations provide a clearer national reference point for provinces, supporting more standardized demand for rare-disease assays, confirmatory testing, and associated laboratory informatics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Canada in vitro diagnostics market is counted as the value of tests done outside the body using patient samples, including the related instruments and reagents used in clinical and near patient settings.

Scope exclusions: We exclude in vivo diagnostic procedures and general hospital equipment that is not directly used to run in vitro tests.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immuno-Diagnostics

- Molecular Diagnostics

- Hematology

- Microbiology

- Coagulation

- Urinalysis

- Other Tests

- By Product

- Instruments

- Reagents & Kits

- Software & Services

- By Usability

- Disposable IVD Devices

- Reusable IVD Devices

- By Application

- Infectious Disease

- Diabetes

- Cancer / Oncology

- Cardiology

- Autoimmune Disorders

- Nephrology

- Blood Screening

- Prenatal / NIPT

- Other Applications

- By End User

- Diagnostic Laboratories

- Hospitals & Clinics

- Point-of-Care Centers

- Home Care Settings

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the guardrails for the model, especially around testing volumes, public health priorities, and how labs and hospitals buy and use diagnostics. We leaned on public sources such as Statistics Canada for health and demographic indicators, Health Canada for regulatory and device context, and the Public Health Agency of Canada for infectious disease and screening signals that affect test mix.

To translate those signals into market value, we also reviewed sources such as CIHI for system level utilization context, peer reviewed clinical literature for adoption trends by test type, and trade and customs summaries where relevant to cross-check supply availability. Company annual reports, investor presentations, and reputable press were used to confirm product launches, pricing direction, and any capacity expansion mentioned for Canada, supported by a paid subscription for company financials and a patent database view when pipeline activity needed clarification. These sources are illustrative only, and many other public and paid references were also used during data collection and validation.

Primary Interviews and Surveys

Primary work focused on confirming what drives demand and pricing in Canada. We spoke with a mix of diagnostic lab leaders, hospital stakeholders, distributors, and technical specialists who track test adoption and replacement cycles. Inputs from these discussions were used to validate desk assumptions on test menu shifts (for example, molecular share changes), instrument utilization, reagent pull-through, and the timing of procurement decisions across major provinces.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | |

| Mid tier: 59% | Functional/Unit leaders: 37% | |

| Smaller Players: 14% | Managers: 50% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction of the Canada demand pool, where healthcare utilization signals and disease testing needs are translated into expected test volumes by major IVD areas, and then valued using typical price bands seen across settings. After that total is built, selective bottom-up approximations are used to pressure-test the result, such as sampled instrument placements, reagent consumption per run, and channel feedback on annual purchasing patterns.

Key inputs used in the model include the share shift toward molecular diagnostics, public screening intensity for priority diseases, hospital and lab procurement cycles, installed base replacement timing for analyzers, and average reagent and consumable pricing movement over the period. When a variable is not visible for a smaller test category, we fill the gap with proxy ratios from adjacent test types and then re-check the implied spend with interview feedback so the totals do not drift.

For forecasting, scenario analysis was applied because policy funding, testing mix, and decentralization can move faster than population growth alone. Assumptions on test menu changes and pricing were aligned to what practitioners expect over the next few years, and then applied consistently across the time series so year-to-year steps remain explainable.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals. We compare implied spend per test, instrument utilization ranges, and growth patterns against what was heard in interviews and what is visible in public indicators. Outliers are flagged early, and the model is adjusted only after the driver can be explained. That rationale is reviewed again in an internal analyst check before sign-off.

The report is refreshed annually, and interim updates are made when a material event changes demand or pricing assumptions. (For example, a major reimbursement shift or a step change in testing volumes.) Before delivery, we do a final pass to ensure the latest public releases and interview insights are reflected in the view clients receive.

Mordor Intelligence's Vitro Diagnostics Canada Market Size Measured Against Other Published Estimates

Market size numbers for Canada IVD can look different across publications, even when the topic name is the same, because the scope boundaries and pricing logic are not always aligned. Differences also come from which year is treated as the base, how currency timing is handled, and whether assumptions were rechecked with people active in labs and hospital procurement.

The table shows a narrow spread around the mid-USD 4 B range for 2025 to 2026, and the remaining gaps usually trace back to what gets counted as IVD value and how test mix is projected to shift. Some estimates may add broader lab services, include adjacent medical device revenue, or apply aggressive price growth, while others use conservative utilization ramps that do not match the installed base and reagent pull-through seen in practice.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.05 B (2025) | |

| Industry Publisher A | USD 4.15 B (2025) | Uses a wider segmentation lens that can implicitly blend some lab service revenue into the total, and it applies a longer-horizon growth curve that smooths near-term mix shifts. |

| Industry Publisher B | USD 4.27 B (2026) | Anchors the starting point a year later and may assume faster price progression for reagents and consumables, which lifts the value even if volumes move gradually. |

The table points to a modest gap that largely comes from what is being counted and when, and in Mordor Intelligence's model the total is limited to IVD instruments and reagents tied to in vitro testing activity in Canada rather than broader lab service billings. Because the same demand signals are cross-checked through utilization, installed base, and interview feedback, the final view stays traceable to clear drivers and can be repeated when new public data becomes available.

Key Questions Answered in the Report

What is the value of Canada's in-vitro diagnostics sector in 2026?

It is worth USD 4.25 billion, reflecting sustained investment in clinical testing infrastructure.

What compound annual growth rate is projected for Canada's in-vitro diagnostics through 2031?

The sector is forecast to grow at a 4.93% CAGR, reaching USD 5.41 billion by the end of the period.

Which test type is expanding quickest within Canada's IVD landscape?

Molecular diagnostics leads, advancing at a 10.42% CAGR on the back of precision-medicine demand.

How dominant are disposable IVD devices compared with reusable alternatives across Canada?

Disposable formats hold 70.63% of current use, although reusable devices are rising at a 9.05% CAGR.

What factors are driving the rapid uptake of diagnostic services in home care settings across Canada?

Patient preference for convenience, telehealth expansion, and reliable point-of-care technologies are propelling an 8.25% CAGR in home testing.

How is federal funding influencing adoption of advanced diagnostics across Canadian provinces?

More than USD 200 billion committed to healthcare modernization is accelerating procurement of molecular platforms, digital tools, and cloud-linked laboratory systems.

Page last updated on: