Supercomputers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

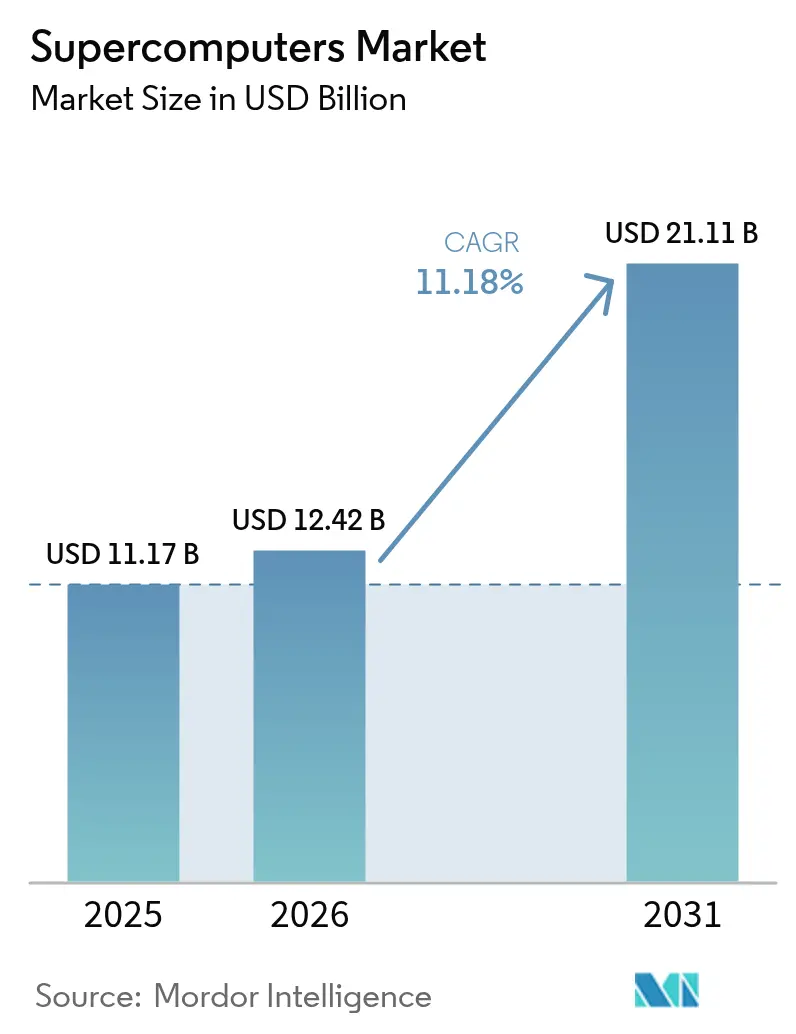

| Market Size (2026) | USD 12.42 Billion |

| Market Size (2031) | USD 21.11 Billion |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Supercomputers Market Analysis by Mordor Intelligence

The supercomputer market size in 2026 is estimated at USD 12.42 billion, growing from 2025 value of USD 11.17 billion with 2031 projections showing USD 21.11 billion, growing at 11.18% CAGR over 2026-2031. This rapid climb rests on the convergence of exascale breakthroughs, soaring artificial-intelligence workloads, and rising public-sector investment in digital sovereignty programs. National laboratories, cloud operators, and private research consortia are expanding procurement budgets, driving keen competition across processors, accelerators, and liquid-cooling technologies. At the same time, semiconductor supply-chain fragility and escalating energy costs shape purchasing decisions, pushing vendors to integrate energy-efficient architectures and advanced thermal solutions. Government export-control policies further fragment the supercomputer market, channeling demand toward domestically aligned suppliers and intensifying design-win battles in every major economy.

Key Report Takeaways

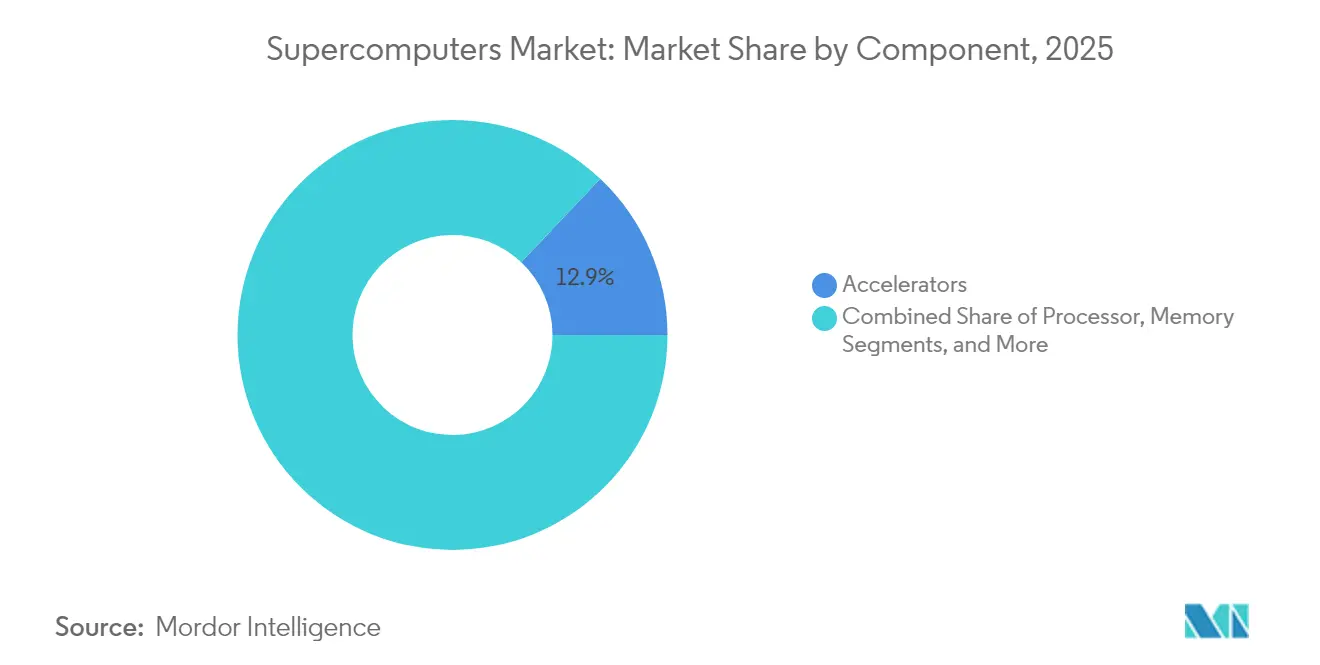

- By component, processors held 38.67% of the supercomputer market share in 2025.

- By system type, accelerators, driven by AI workloads, are forecast to expand at a 15.05% CAGR through 2031.

- By deployment mode, cloud-based HPC-as-a-Service recorded the highest projected CAGR of 19.98% to 2031.

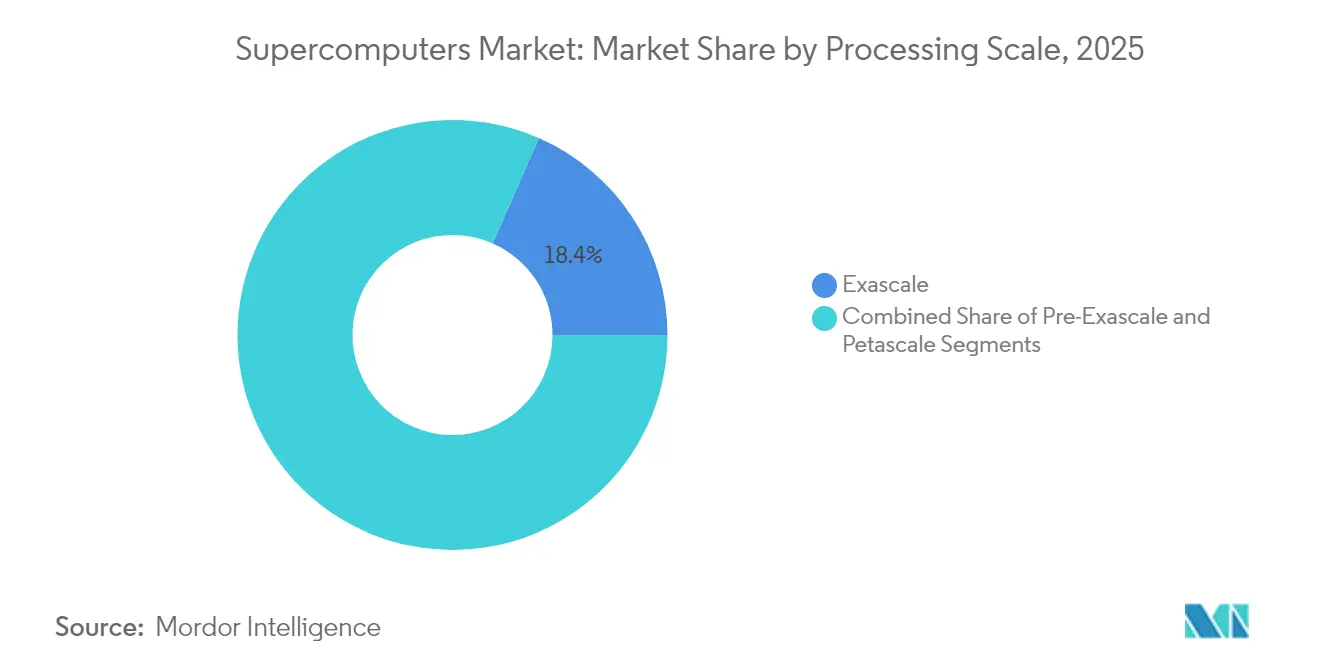

- By processing scale, Exascale installations major share of the supercomputer market size in 2025 and will accelerate at a 26.18% CAGR through 2031.

- By end-user, Healthcare and life sciences accounted for 15.44% CAGR, the quickest growth among end users.

- By geography, Asia-Pacific is projected to grow at a 12.55% CAGR, the fastest regional trajectory through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Supercomputers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Race-to-Exascale public funding surge | +2.8% | Global; high intensity in US, China, EU, Japan | Medium term (2-4 years) |

| Proliferation of AI/ML workloads on HPC systems | +3.2% | Global; North America, APAC lead | Short term (≤2 years) |

| Demand for climate and biomedical simulations post-COVID | +1.9% | Global; focus on developed economies | Medium term (2-4 years) |

| Rising availability of cloud-based HPC-as-a-Service | +2.1% | Global; early North America, Europe uptake | Short term (≤2 years) |

| Open-source HPC software-stack maturity | +1.4% | Global | Long term (≥4 years) |

| National digital-sovereignty programs | +1.8% | APAC, Europe, select emerging states | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Race-to-Exascale Public Funding Surge

Large-scale programs in the United States, Europe, China, and Japan fund next-generation systems that outpace today’s petascale machines by factors of 10 or more. The U.S. Department of Energy’s Discovery system targets 3-5 times Frontier’s throughput, while Europe’s EuroHPC Joint Undertaking funds a distributed exascale network that underpins regional research autonomy[1]Department of Energy, “Discovery supercomputer plan,” hpcwire.com. Vendors able to bundle hardware, software, and professional services capture longer contracts, assuring revenue visibility beyond initial installations. Academic bidding has intensified as universities seek leadership-class machines, creating a second tier of demand that sweeps smaller suppliers into national programs.

Proliferation of AI/ML Workloads on HPC Systems

AI inference and training now permeate traditional HPC centers, compelling architects to integrate high-bandwidth memory and heterogeneous compute subsystems. NVIDIA’s H100 and AMD’s MI300X accelerators have become standard line-items in new procurements, reflecting how AI layers drive peak-flops requirements[2]NVIDIA, “Fiscal 2024 data center revenue highlights,” nvidia.com. Financial institutions deploy ultra-low-latency clusters for risk analytics, while life-science firms exploit multi-node GPU racks for drug-discovery pipelines. The shift reshapes software ecosystems; compilers, schedulers, and libraries must optimize for tensor cores and sparsity-aware operations. System integrators that deliver turnkey AI-HPC solutions consistently win higher-margin service deals.

Demand for Climate and Biomedical Simulations Post-COVID

Researchers require ever-longer forecasting horizons for extreme-weather events and pandemic trajectories. Fugaku’s real-time tornado model cut prediction times to 80 minutes, signaling how computational power directly influences public-safety planning[3]Fujitsu Limited, “Real-time tornado prediction on Fugaku,” fujitsu.com. Oil-and-gas majors use exascale systems to evaluate carbon-capture scenarios and seismic data in a single workflow. Biomedical labs leverage genomic models to advance personalized medicine initiatives accelerated by pandemic-era funding. The broadening of application domains underpins resilient demand even amid cyclical IT spending slowdowns.

Rising Availability of Cloud-based “HPC-as-a-Service”

Public-cloud providers now offer elastic clusters capable of hundreds of petaflops, eliminating capital-expense barriers for smaller firms. Oracle’s zettascale roadmap shows how platform competition centers on raw compute per dollar rather than differentiated service layers[4]Oracle, “Oracle announces zettascale computing clusters,” oracle.com. Hybrid patterns dominate; sensitive workloads remain on-premises but burst to the cloud for development and seasonal peaks. Middleware must deliver seamless data mobility and scheduler awareness, opening fresh niches for software startups. European data-residency rules elevate regional providers, further fragmenting the landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ballooning datacenter power and cooling costs | −2.4% | Global; acute where electricity prices soar | Short term (≤2 years) |

| Persistent talent gap in parallel-programming skills | −1.8% | Global; pronounced in emerging markets | Long term (≥4 years) |

| Advanced-node chip supply-chain fragility | −2.1% | Global; focused on leading-edge fabs | Medium term (2-4 years) |

| Lengthy public-sector procurement cycles | −1.2% | Government-heavy regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ballooning Datacenter Power and Cooling Costs

Exascale machines regularly draw 20-40 MW, dwarfing budgets allocated only five years ago. Liquid and immersion cooling migrate from pilot to mainstream as air-cooling plateaus. Energy frequently surpasses amortized hardware costs over system lifetimes, forcing operators to negotiate long-term power-purchase contracts. Vendors differentiate on performance per watt metrics, spurring R&D into chiplets and optical interconnects that curb thermal footprints. Policy incentives for green datacenters influence site-selection, pushing new builds toward regions with renewable-energy surpluses.

Advanced-Node Chip Supply-Chain Fragility

A handful of advanced fabs manufacture high-bandwidth memory and cutting-edge accelerators. When packaging lines choke, lead times stretch past 12 months, derailing deployment schedules and inflating component prices. Export-control measures tighten supply further, especially for organizations flagged under national-security restrictions. Contingency designs using older-node silicon or alternative vendors often compromise performance, compelling buyers to weigh throughput penalties against schedule risk. These shocks complicate multi-year procurement roadmaps and depress near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Accelerators Propel AI–HPC Convergence

Accelerators commanded USD 1.45 billion of the supercomputer market size in 2025, upholding 15.05% CAGR projections through 2031. GPUs and custom ASICs shoulder AI inferencing alongside traditional floating-point simulations, lifting average rack-level heat from 40 kW to 80 kW. Memory vendors struggle to meet HBM3E demand, constraining many 2025 builds. Storage transitions to NVMe over Fabrics, shrinking I/O bottlenecks in data-rich workloads.

Processors retained 38.67% supercomputer market share in 2025, yet face slowing unit revenues as customers allocate larger budgets to accelerators. Vendors pivot to chiplet-based designs that attach coherently to GPUs, calling for unified memory semantics. Software and Services remains the highest-margin slice, where optimization contracts outlive hardware cycles. Interconnect revenue grows in lockstep with node counts, with 800 Gbps Ethernet lanes and 400 Gbps InfiniBand forming the backbone of next-generation topologies.

By System Type: Heterogeneous Clusters Advance

Cluster-based architectures represented USD 4.44 billion of the supercomputer market size in 2025, sustaining their 39.74% share as standardization eases procurement. Meanwhile, heterogeneous systems post 15.56% CAGR, bundling CPUs, GPUs, and purpose-built accelerators under a single scheduler to flex across AI and simulation workloads. Massively parallel processing remains essential for lattice-QCD and weather models that crave extreme node counts.

Software frameworks such as SYCL and OpenMP offload directives pave smoother development paths across diverse chips, raising utilization rates. Vendors that package high-density GPUs with CPU-rich head nodes ride demand from research facilities seeking dual-purpose clusters. Vector systems, though niche, find renewed relevance in genomic alignment and real-time risk-calculation tasks.

By Deployment Mode: Cloud Momentum Builds

Cloud offerings generated a USD 4.59 billion of supercomputer market size in 2025 and are forecast to grow at a 19.98% CAGR. Flexible pay-as-you-go pricing democratizes access for startups and mid-sized labs previously priced out of on-premises ownership. Early adopter sectors include autonomous-vehicle simulation and cinematic rendering, both needing sporadic yet massive bursts of compute power.

On-premises deployments, still 58.94% of the supercomputer market share in 2025, rely on sunk-cost facilities and strict data-sovereignty mandates. Hybrid strategies dominate among financial-services firms that keep trading models local while training algorithms in cloud sandboxes. Providers now bundle colocation racks inside sovereign data regions, marrying regulatory compliance with elastic capacity.

By Processing Scale: Exascale Era Dawns

Exascale installations booked USD 2.06 billion of the supercomputer market size in 2025 and will accelerate at a 26.18% CAGR as national labs move systems from pilot to production. Pre-exascale clusters fill the gap for institutions not ready for the power and space requirements of full exascale, while petascale systems remain cost-effective staples with 62.88% share in 2025.

Software ecosystems adapt; new memory models, checkpointing schemes, and asynchronous programming patterns emerge to exploit billion-way concurrency. Training pipelines for trillion-parameter AI models increasingly share runtime environments with climate and physics codes, spurring cross-disciplinary collaboration.

By End User: Healthcare Research Surges

Healthcare and life sciences absorbed USD 1.96 billion of spending in 2025, registering the supercomputer industry’s fastest 15.44% CAGR. Drug-discovery firms like Recursion shorten lead-times via in-silico screening, while genomics centers crunch pangenome datasets. Government and defense, at 31.62% share in 2025, remain cornerstone buyers funding classified AI and advanced-materials research.

Manufacturing exploits digital twins for real-time shop-floor optimization, while utilities simulate grid dynamics amid renewable variability. Academic consortia broker shared access for smaller departments, widening the user base. Financial-services clusters perform Monte-Carlo risk runs overnight, highlighting HPC’s role beyond pure science.

Geography Analysis

North America commanded 41.08% of 2025 revenue as the United States continued to bankroll multi-billion-dollar exascale projects, including the Discovery companion to El Capitan. Canada’s adoption of cloud-based research grants broadened access for university-affiliated startups. Hyper-scale providers upgraded regional availability zones with AI-intensive instance types, heightening competition among system integrators for managed-services contracts.

Asia-Pacific, advancing at 12.55% CAGR, benefits from China’s domestically sourced petascale rollouts and Japan’s Fugaku NEXT roadmap targeting 5-10 times current performance by 2030. India expands digital public-infrastructure missions, earmarking funds for genomics and climate applications that require localized compute-sovereignty. Australia and Singapore co-finance regional Earth-systems hubs, bolstering demand for mid-range clusters.

Europe maintains steady growth through EuroHPC Joint Undertaking grants that distribute capacity across Germany, Finland, and Italy. Sovereignty clauses push buyers toward open-architecture hardware combined with EU-developed software stacks. Energy-price volatility spurs Nordic data-center builds, leveraging low-carbon hydroelectricity to host dual-purpose commercial and public-research nodes. The Middle East funds AI factories, such as Saudi Arabia’s HUMAIN, to diversify economies beyond hydrocarbons. South America’s USD 4 billion Brazilian initiative elevates regional rank on TOP500 lists and opens collaboration with academic partners worldwide.

Regulatory Landscape

Export controls and end-use restrictions remain a primary compliance driver for the global supercomputers market, shaping component availability, system configuration, and supplier selection. In the United States, BIS rules under 15 CFR 744.23 govern items destined for supercomputer end uses and facilities involved in advanced-node IC development or production, which increases screening around end users, end uses, and data center operator ownership structures.

Value Chain Analysis

The supercomputer value chain starts upstream with advanced semiconductor design and manufacturing, then moves through packaging, board and module build-out, system integration, and finally deployment and lifecycle services. Leading-edge compute depends on a narrow set of foundries and advanced-packaging providers. After that, ODM/EMS firms assemble boards and racks, while OEMs and integrators deliver complete systems that include interconnect, storage, and software stacks.

Downstream, end users procure systems via long-cycle tenders, while software and services providers monetize porting, optimization, and ongoing operations. In May 2026, NVIDIA highlighted the scale-up of its MGX partner ecosystem, adding chassis and PCB contributors to support volume production of next-generation platforms. Manufacturing localization initiatives, including US-based assembly capacity cited by major AI system suppliers, complement national digital-sovereignty programs and help buyers mitigate geopolitical and export-control risk, while increasing the importance of qualified regional supply chains for racks, cooling, and power delivery.

Competitive Landscape

Moderate consolidation defines the supplier field. Hewlett Packard Enterprise leverages its Cray lineage to dominate national-lab awards, bundling Slingshot interconnects with optimized software toolchains. Dell Technologies and Lenovo chase breadth, competing hard on total cost of ownership for mid-range clusters. NVIDIA’s GPU roadmap anchors many procurements; shortages in 2024 exposed buyer dependence yet reinforced its lock-in via CUDA libraries. AMD’s EPYC processors close integer-performance gaps and, following the ZT Systems acquisition, offer vertically integrated racks that appeal to AI-first data centers.

Cloud vendors now vie for workloads previously reserved for on-premises behemoths. Amazon Web Services markets Trainium and Inferentia silicon, sidestepping GPU scarcity by owning supply chains. Oracle’s zettascale cluster announcement pivots the conversation to exascale-class–as-a-service offerings, intensifying price wars. Start-ups such as Cerebras Systems supply wafer-scale engines tailored to language-model training, compelling incumbent OEMs to explore domain-specific accelerators.

Cooling-technology specialist firms gain strategic weight; sub-10 °C liquid-immersion prototypes achieve >1.5 PFLOPS per rack, helping operators rein in power bills. Middleware vendors that orchestrate hybrid AI and simulation workloads fetch higher valuations as buyers seek abstraction layers blotting hardware complexity.

Supercomputers Industry Leaders

Atos SE

Intel Corporation

Hewlett Packard Enterprise Co.

Dell EMC (Dell Technologies Inc.)

Fujitsu Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Energy efficiency and facility constraints are pushing demand toward turnkey, power-aware designs, including liquid cooling and integration of servers, interconnect, storage, and advanced thermal management for exascale-class deployments. Large-scale liquid-cooled AI data center campuses coming online in 2026 illustrate specific procurement opportunities for OEMs and subsystem suppliers, and for colocation and cloud providers offering HPC-as-a-Service within sovereign or regulated regions.

Public-sector digital sovereignty and national compute programs are also grounding new build activity across regions. In Europe, EuroHPC JU activity around AI-optimized supercomputers and the AI factory model requires suppliers that can meet procurement, residency, and compliance expectations under evolving EU rules, including the EU AI Act that reaches full application on August 2, 2026. The June 2026 TOP500 debut of a new number-one system at Shenzhen Supercomputer Center using a CPU-only approach shows that architectures beyond GPUs can deliver leadership-class results, which raises the value of portable software stacks and vendor-neutral programming models across heterogeneous fleets.

Recent Industry Developments

- July 2026: The French State completed its acquisition of Bull, the Atos unit focused on HPC, AI, and quantum technologies, moving to establish it as an independent company. The transaction tightened national control over strategic compute capabilities and strengthened Bull's positioning for sovereignty-driven procurements across Europe. It also reshaped competitive dynamics for large public tenders where supplier nationality and strategic autonomy are evaluation factors.

- June 2026: Atos delivered the 8.8 petaflops Topaze supercomputer to the French Alternative Energies and Atomic Energy Commission (CEA). The deployment reinforced demand for leadership-class systems that couple simulation and AI workloads under tight security and performance constraints. It also signaled continued investment in domestic and European supply chains for sensitive research infrastructure.

- May 2026: NVIDIA highlighted the scale-up of its MGX partner ecosystem, adding chassis and PCB contributors to support volume production of next-generation platforms. The move supports broader adoption of AI-ready infrastructure for HPC deployments and strengthens ecosystem alignment across suppliers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the supercomputer market covers high-performance computing systems sold as integrated platforms to deliver very large compute workloads. It includes the core compute, interconnect, and storage building blocks that are delivered together so end customers can run at supercomputer-class scale.

Scope exclusions: this sizing excludes general-purpose enterprise servers and standard cloud compute instances that are not delivered or contracted as supercomputer or HPC-class capacity.

Segmentation Overview

- By Component

- Processor (CPU)

- Accelerators (GPU/ASIC)

- Memory

- Storage

- Interconnect

- Software and Services

- By System Type

- Cluster-Based

- Massively Parallel Processing (MPP)

- Accelerated / Heterogeneous

- Vector

- By Deployment Mode

- On-Premises

- Cloud-based (HPC-aaS)

- Hybrid

- By Processing Scale

- Petascale

- Pre-Exascale

- Exascale

- By End-user

- Government and Defense

- Academic and Research Institutes

- Financial Services

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Energy and Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the model and to keep assumptions tied to real-world compute demand signals. We reviewed public sources such as the TOP500 list releases, government and national lab procurement releases, select US DOE and NSF materials, and statistical references like the World Bank and OECD for R&D and macro indicators that influence advanced computing spend.

We also used company annual reports, earnings call transcripts, and investor presentations to understand system backlog language, customer mix patterns, and timing of major deployments. Patent databases were used to confirm architecture and accelerator trends that affect system value over time, and press coverage from established tech publications was used to cross-check announced installations. These examples are not exhaustive, and other public sources were also used for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focused on validating what gets purchased as a supercomputer system, how budgets are planned, and how pricing shifts when accelerators, networking, and energy constraints change system configurations. We spoke with a mix of system suppliers, component ecosystem participants, and end users such as research institutions, government and defense bodies, and commercial compute-intensive organizations across APAC, EMEA, and the Americas to close gaps that desk sources do not fully explain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 45% |

| Mid tier: 61% | Functional/Unit leaders: 38% | EMEA: 32% |

| Smaller Players: 14% | Managers: 50% | Americas: 23% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where demand pools are reconstructed from HPC procurement intensity across major end-user groups, and then translated into system value using realistic configuration and pricing logic. In practice, we mapped the installed and planned supercomputing capacity cycle using indicators such as large system award announcements, national program funding direction, accelerator attachment trends, and typical refresh timing at labs and research centers.

To keep totals grounded, results were corroborated with selective bottom-up checks, including sampled system price ranges by performance tier, channel and integrator feedback on shipment timing, and roll-ups of a limited set of publicly visible contract values. Key levers included accelerator share in new builds, interconnect and storage content per system, power and cooling constraints that influence configuration choices, and the split between on-premises and cloud-based supercomputing deployments. Forecasting relied on scenario analysis supported by expert views on budget cycles and deployment slippage, and then the growth path was smoothed where needed so year-to-year swings matched procurement realities. When bottom-up visibility was partial, gaps were handled by using conservative ranges, then re-testing them against the top-down demand signals before finalizing totals.

Data Validation & Update Cycle

Validation is done through step-by-step checks so unusual jumps are not carried into the final outputs without explanation. We compare modeled values against independent signals such as public installation pipelines, major contract disclosures, and the observed pace of capacity upgrades, and then investigate variances by region and end-user type before sign-off.

A second analyst review is used to challenge assumptions that have an outsized impact, such as accelerator pricing direction or unusually fast refresh cycles. If interview feedback conflicts with desk signals, respondents are re-contacted to confirm whether the difference is timing or scope related. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Supercomputer Market Size Compared Against Other Published Estimates

Published numbers for the supercomputer market do not always match because inclusion rules and timing assumptions vary from one publisher to another, even when the topic sounds identical. Differences are usually driven by what gets counted as a supercomputer system, which year is treated as the base, and how large project timing is handled in the forecast.

General-purpose HPC software and services revenue sits outside Mordor Intelligence's scope here, which helps keep the value focused on system-level supercomputing spend rather than broader HPC ecosystems that can inflate totals. Other gaps often come from using older exchange rates, counting cloud HPC consumption as if it were hardware sales, or applying aggressive ASP increases for accelerators without checking them against procurement budgets and the announced installation pipeline.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.42 B (2026) | |

| Global Consultancy A | USD 9.81 B (2024) | Uses a different base year and a type-led view that appears more hardware-only, with limited visibility on how large government and lab deployments are timed and converted into annual market value. |

| Industry Publisher B | USD 9.40 B (2024) | Starts from a 2024 estimate and extends a longer forecast horizon, which can widen outcomes if accelerator pricing, refresh cycles, and currency treatment are not revalidated against near-term procurement signals. |

The spread in the table is mainly explained by base-year differences and what adjacent revenue pools get mixed into the definition. By tying the model to observable procurement activity, installation timing, and configuration-level value drivers, the estimate stays more repeatable and easier to audit when assumptions are updated.

Key Questions Answered in the Report

How fast is spending on high-performance computing growing worldwide?

Global revenue in the supercomputer market is rising at 11.18% CAGR between 2026 and 2031, driven by exascale funding and AI workloads.

Which region shows the quickest growth in large-scale computing adoption?

Asia-Pacific posts 12.55% CAGR through 2031, propelled by Chinese, Japanese, and Indian national programs.

Why are accelerators becoming more important than traditional CPUs?

AI and machine-learning tasks dominate new workloads, and accelerators like GPUs deliver higher tensor throughput than general-purpose processors.

What challenges limit immediate expansion of exascale systems?

High power consumption, advanced-node chip shortages, and the scarcity of parallel-programming talent constrain near-term deployments.

Will cloud offerings replace all on-premises supercomputers?

No; on-premises clusters remain vital for security and data-sovereignty needs, though cloud HPC grows faster at 19.98% CAGR.

Page last updated on: