Humanoid Robot GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

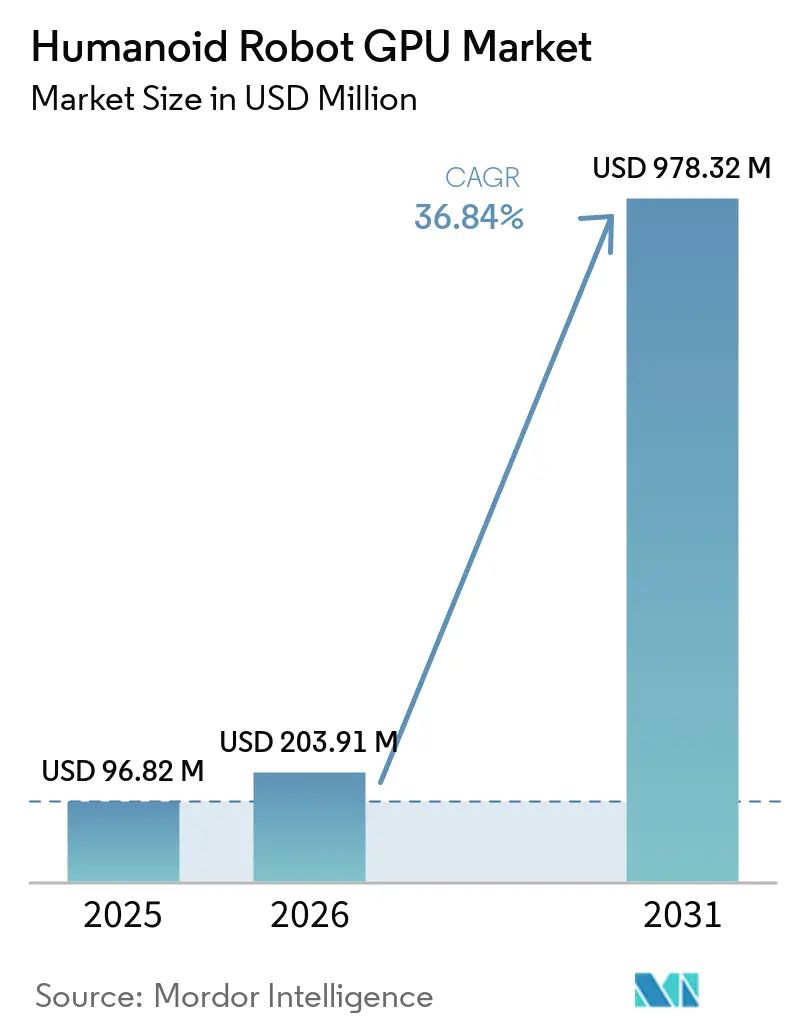

| Market Size (2026) | USD 203.91 Million |

| Market Size (2031) | USD 978.32 Million |

| Growth Rate (2026 - 2031) | 36.84% CAGR |

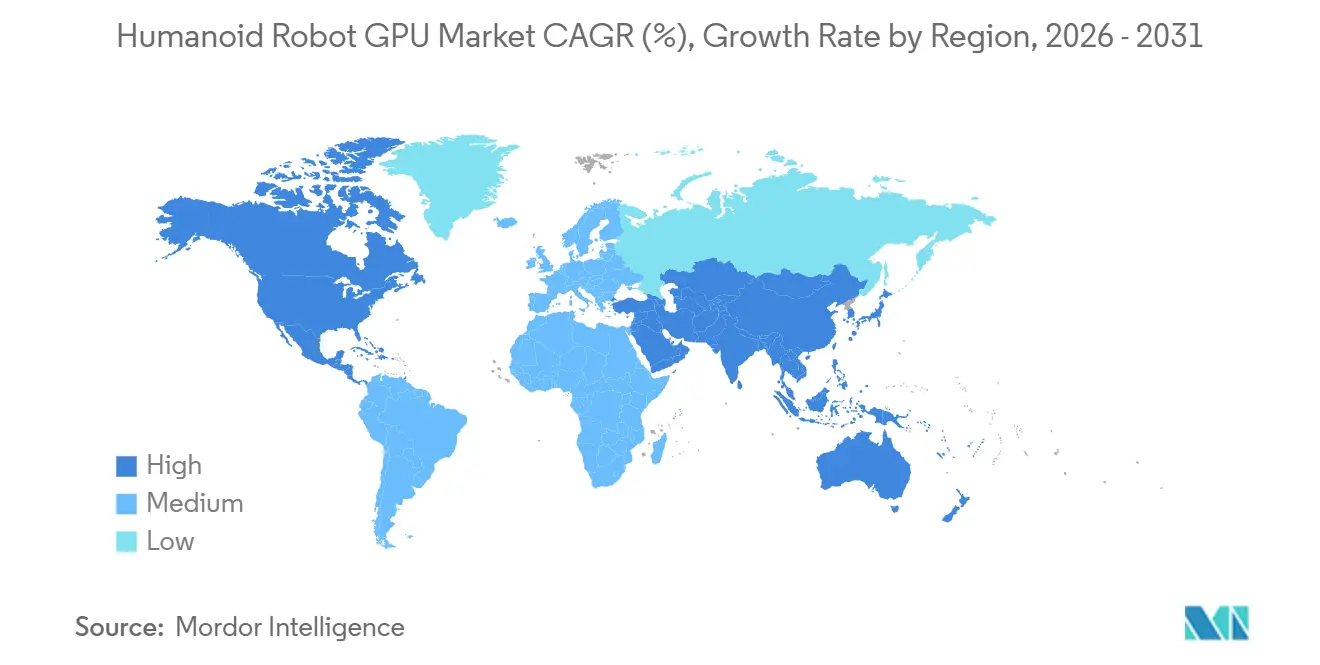

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Humanoid Robot GPU Market Analysis by Mordor Intelligence

The humanoid robot GPU market size is expected to increase from USD 96.82 million in 2025 to USD 203.91 million in 2026 and reach USD 978.32 million by 2031, growing at a CAGR of 36.84% over 2026-2031. The sharp increase in 2026 reflects the shift from prototype procurement to early commercial deployments, as robot programs move from testing environments into live production settings. Demand is rising because humanoid systems now need to run perception, motion planning, and language-driven reasoning simultaneously, making high-bandwidth, low-latency GPU compute a core part of the bill of materials. Public support for physical AI programs in China, Japan, and Europe is also shortening adoption timelines and encouraging broader investment in local compute stacks. Vendor competition is being shaped less by standalone chips and more by complete hardware and software ecosystems, which raises switching costs once a robotics developer commits to a training and inference stack. At the same time, battery limits and thermal design constraints keep commercial adoption tied to compute efficiency, which gives an advantage to suppliers that can balance performance, power draw, and integration.

Key Report Takeaways

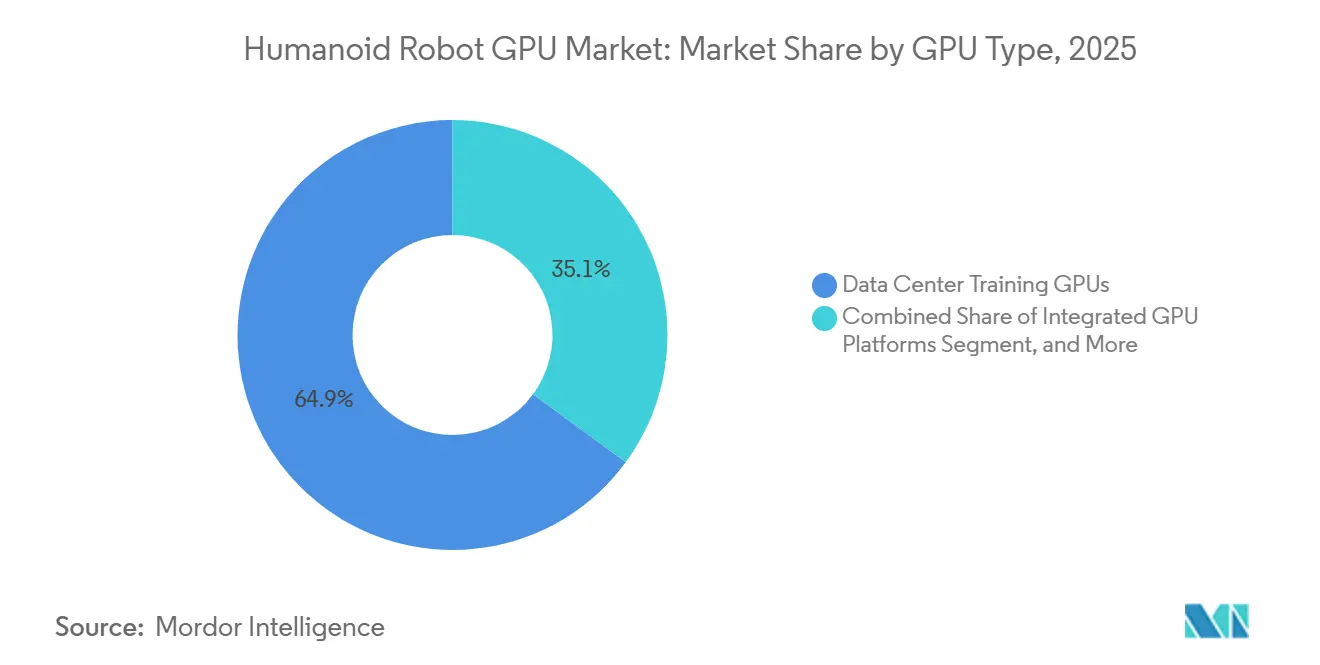

- By GPU type, Data Center Training GPUs held 64.92% of the humanoid robot GPU market share in 2025, while Integrated GPU Platforms are projected to expand at a 37.61% CAGR through 2031.

- By deployment type, Offboard Training and Simulation commanded 65.38% share in 2025, while Onboard Compute is expected to grow at a CAGR of 38.14% through 2031.

- By GPU function, Training and Simulation accounted for 48.87% of the humanoid robot GPU market size in 2025, while Digital Twin and Synthetic Data Generation are projected to grow at a 38.26% CAGR through 2031.

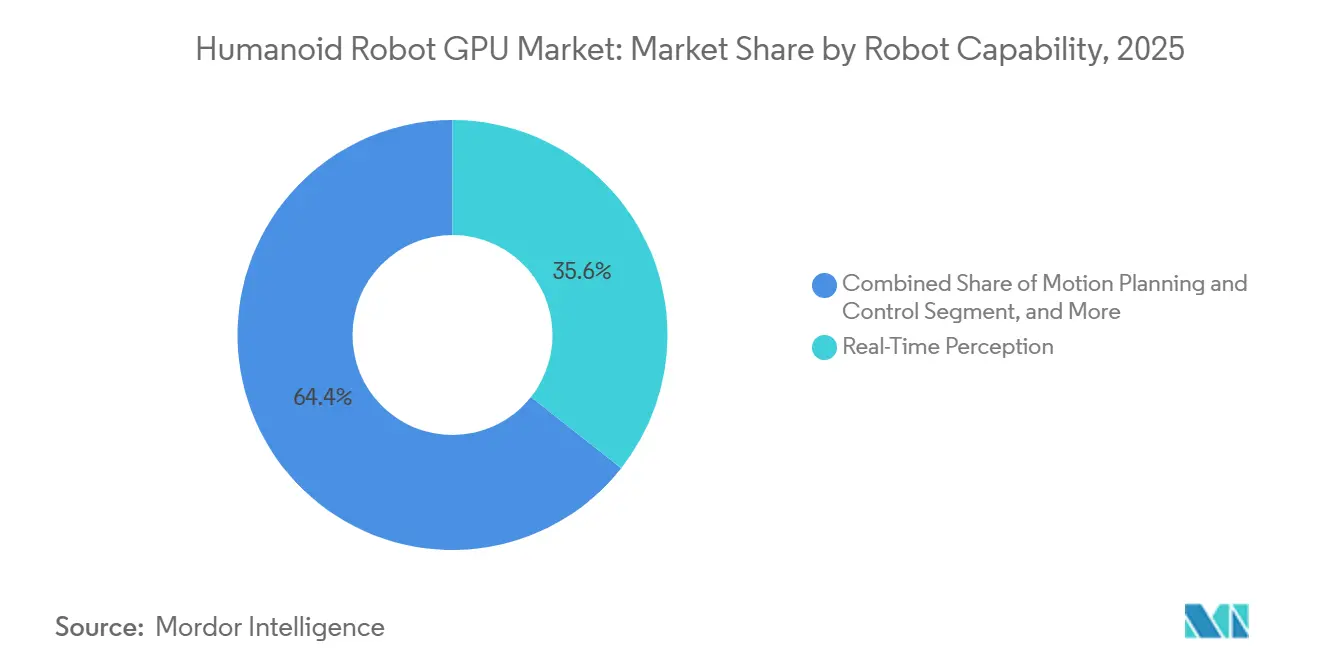

- By robot capability, Real-Time Perception held the largest share at 35.63% in 2025, while Multi-Modal Reasoning is expected to expand at a 37.92% CAGR through 2031.

- By end use industry, Automotive led with a 32.51% share in 2025, while Manufacturing and Assembly is projected to advance at a 38.49% CAGR through 2031.

- By geography, Asia-Pacific held 47.62% of the humanoid robot GPU market in 2025, while North America is projected to grow a 38.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Humanoid Robot GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Physical AI Compute Intensity in Humanoid Robots | +6.8% | Global, with intensity peaks in North America and China | Short term (≤ 2 years) |

| Growing Demand for Onboard Real-Time Inference | +5.2% | Global, particularly North America and the Asia-Pacific | Short term (≤ 2 years) |

| Increasing Use of Synthetic Data and Simulation Pipelines | +4.1% | North America and China are leading, spill-over to Europe and Japan | Medium term (2-4 years) |

| Expanding Pilot Deployments in Automotive Manufacturing | +3.2% | North America, Germany, South Korea, Japan | Short term (≤ 2 years) |

| Rising Preference for Edge Processing to Reduce Latency and Cloud Dependency | +2.4% | Global, with early adoption in North America and the Asia-Pacific | Medium term (2-4 years) |

| Strategic Platform Lock-In by Leading Robotics Compute Vendors | +1.8% | Global, concentration in North America and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Physical AI Compute Intensity in Humanoid Robots

The humanoid robot GPU market is expanding because physical AI workloads now run multiple model layers simultaneously rather than relying on a single vision or control task. NVIDIA positioned the Jetson AGX Thor T5000 to address this need with 2,070 FP4 teraflops, a significant leap from the Jetson AGX Orin platform and a clear indication of how quickly compute requirements are rising. The same GPU market for humanoid robots is also being shaped by memory requirements, as NVIDIA listed 24GB and higher VRAM for training systems and 128GB unified memory for edge inference in its GR00T hardware guidance. That matters because a developer moving from narrow imitation tasks to broader generalist behavior has to scale training hardware and onboard inference hardware simultaneously. NVIDIA also framed cloud-to-robot computing for physical AI as a foundational layer for humanoid development, which supports continued demand across both data center and embedded GPU products.

Growing Demand for Onboard Real-Time Inference

The humanoid robot GPU market is shifting toward onboard inference because latency and data-handling limitations make continuous cloud dependence less practical in live operating environments. 1X Technologies stated in 2026 that Jetson Thor was the only product available at the time that met the NEO robot's onboard compute requirement for real-time sensor processing, underscoring how narrow the field still is at the high end of embedded performance. Boston Dynamics also expanded its collaboration with NVIDIA to integrate Jetson Thor into Atlas, bringing server-class reasoning capability onto the robot itself rather than keeping the heavy workload offboard. In the humanoid robot GPU market, that architecture change matters because every additional robot deployed becomes a direct hardware sale rather than depending solely on centralized training clusters. As more deployments move into production lines and warehouse workflows, local inference is becoming a standard design requirement rather than an optional premium feature.

Increasing Use of Synthetic Data and Simulation Pipelines

The humanoid robot GPU market is gaining another demand layer from synthetic data generation, as real-world demonstration data remains limited and expensive to scale. NVIDIA reported that its Isaac GR00T blueprint generated 780,000 synthetic trajectories in 11 hours, which it equated to 6,500 hours of human demonstration data, and the company said the mixed dataset improved GR00T N1 policy performance by 40%.[1]NVIDIA Developer, “Isaac GR00T Hardware Requirements,” NVIDIA Developer, nvidia-isaac-gr00t.mintlify.app This means the humanoid robot GPU market is no longer driven solely by robot inference, since training teams also need dense simulation clusters capable of running digital twins and world models at high volume. NVIDIA linked that expansion directly to its Blackwell systems and broader physical AI stack, reinforcing the split between data center GPUs for development and edge modules for deployment. Peer-reviewed robotics work also showed 64 NVIDIA L40 GPUs training across 1,024 simulated environments per GPU, which confirms that large-scale simulation is becoming a standard workload rather than a niche experiment.

Expanding Pilot Deployments in Automotive Manufacturing

The humanoid robot GPU market is being pushed forward by automotive programs, as that sector is now producing the clearest evidence that humanoids can add value within structured industrial workflows. BMW stated that its Figure AI pilot in Spartanburg supported the production of more than 30,000 BMW X3 vehicles over 10 months, with the robots accumulating 1,250 operating hours and handling more than 90,000 sheet-metal parts. Agility Robotics also announced a commercial Robots-as-a-Service agreement with Toyota Motor Manufacturing Canada in February 2026, which moved humanoid deployment from trial mode toward contracted production use. In the humanoid robot GPU market, these programs matter because they create repeat demand for both onboard inference hardware and the training infrastructure required for fleet updates. They also give other manufacturers a clearer benchmark for how quickly GPU-backed robot programs can move from pilot lines to broader plant operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Power Draw and Thermal Design Complexity | -3.8% | Global, most acute in battery-operated humanoid deployments | Short term (≤ 2 years) |

| Elevated Bill of Materials and Total Cost of Ownership | -3.1% | Global, amplified in cost-sensitive markets outside North America | Medium term (2-4 years) |

| Software Portability and Developer Ecosystem Fragmentation | -2.2% | Global, with higher friction in markets outside NVIDIA's Isaac ecosystem | Long term (≥ 4 years) |

| Limited Real-World Training Data for Edge Cases | -1.6% | Global, most constraining in unstructured environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Power Draw and Thermal Design Complexity

The humanoid robot GPU market still faces a direct operating constraint because onboard compute has to share limited battery capacity with locomotion, sensing, and actuation. NVIDIA developer discussions about Jetson Thor showed that even the SoC-level power breakdown is a practical challenge for thermal design teams, especially when developers try to model sustained performance within the module's configurable TDP range. NVIDIA also described its Isaac GR00T reference robot with a 15Ah and 0.972kWh battery and around 3 hours of operating life, which remains well below a full industrial shift and forces workarounds such as battery swaps or fixed power support. In the humanoid-robot GPU market, that power ceiling slows adoption because peak inference and actuator loads hit the same system simultaneously. It also favors larger vendors that can invest in integrated thermal management, power governors, and full-system optimization.

Elevated Bill of Materials and Total Cost Of Ownership

The humanoid robot GPU market remains expensive to scale because compute hardware is one of the most difficult costs to compress without reducing capability. Robots-as-a-Service can spread spending over time, but that does not remove the underlying hardware cost, since the GPU still sits inside the monthly or usage-based fee charged to the customer. The humanoid robot GPU market is, therefore, more accessible today to developers and buyers who can absorb higher upfront engineering costs while waiting for volume efficiencies to emerge. Qualcomm's CES 2026 robotics platform launch showed why integrated CPU, GPU, and AI acceleration designs are being closely watched, as they offer a path to lower board complexity and better power efficiency in a single package. Until integrated platforms scale more broadly, the cost base is likely to keep commercial deployment concentrated among well-funded robot makers and early industrial adopters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Data Center Training Spending Anchors the Market While Integrated Platforms Gain Pace

Data Center Training GPUs held 64.92% of the humanoid robot GPU market share in 2025, indicating that most spending still sat upstream in model development rather than in fielded robots. The humanoid robot GPU market relied on that training layer because generalist robot policies need large-scale simulation, synthetic data generation, and continuous model refinement before commercial fleets can expand. NVIDIA's cloud-to-robot positioning for physical AI reflected this demand pattern by tying data center systems directly to robot training, simulation, and deployment workflows. The same humanoid robot GPU market also showed why embedded systems matter, as Jetson Orin had supported earlier deployments, and Jetson Thor moved into the role of reference onboard compute for more advanced commercial humanoids.

NVIDIA's ecosystem traction was reinforced by public commitments from Boston Dynamics and 1X, both of which tied their robot roadmaps to Jetson Thor for onboard reasoning and sensor processing.[2]1X Technologies, “Inside 1X's Humanoid Robot Stack: Simulation, AI Training, and Onboard Compute with NVIDIA,” 1X Technologies, 1x.tech Integrated GPU Platforms are projected to grow at a 37.61% CAGR from 2026 to 2031, making them the fastest-growing segment of this market. The humanoid robot GPU market is moving in that direction because integrated platforms reduce board complexity and can better balance power, thermal load, and compute than purely discrete approaches in mobile robots. Qualcomm's robotics platform launch at CES 2026 reflected this shift with a design built around CPU, GPU, and AI acceleration in one architecture for humanoid and mobile robotics use. For the humanoid robot GPU industry, that means the next phase of competition is likely to center on full-stack efficiency rather than peak standalone compute alone.

By Deployment Type: Offboard Training Leads While Onboard Revenue Builds Faster

Offboard Training and Simulation accounted for 65.38% of revenue in 2025, indicating that the humanoid robot GPU market remained focused on development infrastructure at that time. Vendors and robot developers still spent heavily on simulation clusters because digital environments let them test policies at a much larger scale than real-world trials can support. NVIDIA linked its humanoid development stack to Omniverse, Isaac, and Blackwell systems, which reflects how central offboard training remains in this market. The humanoid robot GPU market also continued to support hybrid models in which robots execute local inference while receiving heavier model updates from the cloud or data centers during downtime. That hybrid approach fits the current commercial stage because it lets operators use centralized training gains without forcing every compute step onto the robot.

Onboard Compute is forecast to expand at a 38.14% CAGR through 2031, which makes it the fastest-growing deployment mode in the humanoid robot GPU market. That acceleration follows from production settings in which latency, privacy, and operational continuity make constant offboard dependence hard to justify. 1X and Boston Dynamics both pointed to onboard Jetson Thor integration as the path to real-time reasoning and sensor processing on deployed robots, which gives this segment tangible commercial backing. As deployments widen, the humanoid robot GPU market is likely to move toward a more balanced split between centralized development compute and distributed embedded inference hardware.

By GPU Function: Training Workloads Dominate While Synthetic Data Systems Rise Quickly

Training and Simulation accounted for 48.87% of revenue in 2025, confirming that the humanoid robot GPU market continues to allocate the largest share of spend to model creation and refinement. That position is supported by the broad need to train vision, control, and reasoning models before fleets can handle changing tasks in live settings. NVIDIA reinforced this function by launching open humanoid model frameworks and cloud-to-robot infrastructure intended to keep training, fine-tuning, and simulation on its stack. The same humanoid robot GPU market also depends on inference and perception functions that process visual input, depth data, mapping, and task-state awareness once robots are deployed. Motion planning and control remain a separate compute requirement because stable actuation needs high-frequency execution with less tolerance for delay than many other AI tasks.

Digital Twin and Synthetic Data Generation is projected to grow at a 38.26% CAGR through 2031, which makes it the fastest-growing GPU function. The humanoid robot GPU market is moving in this direction because real-world data collection cannot cover enough edge cases or task variety at commercial speeds. NVIDIA's synthetic motion pipeline result of 780,000 trajectories in 11 hours, along with peer-reviewed work using 64 NVIDIA L40 GPUs across 1,024 simulated environments per GPU, shows how simulation has become an operating necessity rather than an experimental add-on. In the humanoid robot GPU industry, that shift creates demand for both larger training clusters and faster iteration between simulated and real robot behavior.

By Robot Capability: Perception Holds the Base While Multi-Modal Reasoning Raises Compute Needs

Real-Time Perception held the largest share at 35.63% in 2025, reflecting that the humanoid robot GPU market is still grounded in workloads such as object recognition, scene awareness, and obstacle handling. Industrial deployments remain perception-heavy because those tasks are the first to reach a practical level of reliability in structured environments. BMW's Leipzig deployment of Hexagon Robotics' AEON included a 21-sensor stack with cameras, radar, and force-torque sensing, which shows the continuous perception burden that live industrial humanoids place on embedded compute. The humanoid robot GPU market, therefore, continues to treat perception as the baseline capability that every commercial system must support before higher-order autonomy can scale. Motion planning and dexterous manipulation also remain closely linked to this segment because richer sensing enables a robot to perform more fine-motor tasks in real time.

Multi-Modal Reasoning is forecast to grow at a 37.92% CAGR through 2031, making it the fastest-growing capability area. The humanoid robot GPU market is moving in this direction because buyers want robots that can interpret natural language, adapt to new environments, and complete multi-step tasks without repeated manual reprogramming. NVIDIA's early access GR00T N1.7 update added finger-level dexterous control for contact-rich tasks, which signals a move toward more capable policies that combine perception, reasoning, and manipulation in the same system. As those capabilities mature, the humanoid robot GPU market will need stronger onboard modules with enough memory and bandwidth to support larger real-time models.

By End Use Industry: Automotive Leads Commercial Adoption While Broader Manufacturing Speeds Up

Automotive held the largest end-use share at 32.51% in 2025, which made it the clearest commercial anchor for the humanoid robot GPU market. BMW gave the most detailed production example in the draft, showing how Figure AI robots supported output over a 10-month period while accumulating meaningful operating hours and part-handling volume inside a real plant. The humanoid robot GPU market also benefited from the automotive sector, as the sector can justify higher initial system costs when labor gaps, workflow repetition, and production continuity create a clear path to value. Logistics and warehousing formed the next visible demand layer, supported by Agility Robotics deployments and the December 2025 Mercado Libre agreement that extended commercial humanoid use into fulfillment operations in South America. That mix of factory and logistics use cases matters because it broadens the set of tasks that justify the use of onboard inference hardware.

Manufacturing and Assembly is projected to grow at a 38.49% CAGR through 2031, which makes it the fastest-growing end-use segment in the humanoid robot GPU market. The expected acceleration comes from the transfer of lessons learned in automotive into electronics, semiconductor, and general industrial assembly settings where repetitive handling and inspection work can also benefit from embodied AI. The humanoid robot GPU market should therefore see demand widen from a few flagship automotive programs toward a larger set of industrial buyers that want flexible automation without redesigning every station around a fixed robot cell. Research, healthcare, and defense still represent longer-cycle opportunities, but they are likely to remain secondary until capability, safety, and cost improve further.

Geography Analysis

Asia-Pacific accounted for 47.62% of revenue in 2025, making it the largest region in the humanoid robot GPU market. That lead came from the concentration of humanoid OEM activity in China, the semiconductor base in Japan and South Korea, and broader public support for physical AI programs described in the draft. The humanoid robot GPU market in Asia-Pacific also benefits from a supply chain that can support sensors, packaging, memory, and compute integration at scale. Domestic compute platforms are beginning to supplement NVIDIA-based deployments in the region, which matters because localization goals are becoming a stronger factor in purchasing decisions. Even with that shift, the humanoid robot GPU market in Asia-Pacific remains closely tied to how quickly regional OEMs can move from pilot output toward repeatable commercial deployment.

North America is projected to expand at a 38.57% CAGR through 2031, making it the fastest-growing regional segment in the humanoid robot GPU market. The region combines a large installed base of AI infrastructure with several of the most commercially visible humanoid developers, which gives it a strong position in both training and deployment. NVIDIA's Jetson Thor roadmap and ecosystem messaging were directed heavily toward this development base, while Boston Dynamics and 1X both linked their robot stacks to NVIDIA's onboard compute path.[3]NVIDIA Developer, “NVIDIA Jetson Thor, Advanced AI for Physical Robotics,” NVIDIA, nvidia.com The humanoid robot GPU market in North America is also supported by the Robots-as-a-Service model, which turns deployments into a recurring hardware and software demand stream instead of a one-time equipment sale. Agility Robotics' commercial agreement with Toyota Motor Manufacturing Canada shows how that model is moving into live industrial operations and supporting embedded GPU demand at the unit level.

Europe accounted for a significant share of 2025 revenue in the humanoid robot GPU market, led by Germany's automotive deployments and the region's broader industrial automation base. BMW's Leipzig program gave Europe a visible reference point for physical AI in automotive production and reinforced the region's role in early industrial adoption. South America and the Middle East and Africa remained smaller contributors, but the humanoid robot GPU market gained a clear South American entry point through Mercado Libre's agreement with Agility Robotics in late 2025. Across these regions, safety compliance and deterministic system behavior are likely to matter more as commercial deployments move closer to routine human-robot collaboration.

Competitive Landscape

The humanoid robot GPU market is highly concentrated at the compute platform level, with NVIDIA holding the strongest position through a stack that spans data center training systems, Jetson onboard modules, and the Isaac GR00T development environment. NVIDIA reinforced that role by presenting physical AI as a cloud-to-robot compute model rather than a collection of disconnected products, which helps keep training, simulation, and inference on the same platform family. The humanoid robot GPU market reflects that platform strength in public adoption signals from companies such as Boston Dynamics and 1X, both of which aligned advanced humanoid programs with Jetson Thor. Once developers build around a training and simulation stack, switching becomes harder because software tools, model workflows, and deployment hardware are all connected. That makes platform control as important as raw silicon performance in this market.

Qualcomm is the clearest challenger named in the draft, and its CES 2026 robotics platform launch showed a direct attempt to compete on integrated performance, power efficiency, and developer tooling in the humanoid robot GPU market.[4]Automate.org, “CES 2026, Qualcomm Targets NVIDIA Jetson With New Robotics Developer Platform,” Automate.org, automate.org Qualcomm framed the offer as a full robotics technology suite for systems ranging from household robots to full-size humanoids, which signaled a serious intent to challenge NVIDIA in embedded compute. NVIDIA answered from the opposite direction by introducing the Isaac GR00T Reference Humanoid Robot in June 2026, which pushed its ecosystem further downstream into a packaged research platform. Boston Dynamics expanded its collaboration with NVIDIA in March 2025, while Agility Robotics said it would adopt Jetson Thor for the sixth-generation Digit platform, showing how leading robot developers are locking compute choices into future product cycles. The humanoid robot GPU market also has pressure from Chinese compute vendors in onboard applications, especially where energy efficiency and localization are prioritized over maximum peak performance.

The next competitive battleground in the humanoid robot GPU market is likely to sit in functional safety, workload isolation, and fleet-scale orchestration rather than in headline compute numbers alone. No company in the draft had yet established a purpose-built safety-certified compute standard for broad humanoid deployment, which leaves room for differentiation as industrial rollouts mature. The humanoid robot GPU market also favors vendors that can capture recurring upgrade demand from Robots-as-a-Service fleets, because those operators replace, refresh, and optimize compute over time instead of making a single purchase. For that reason, vendors with strong software control, integrated reference designs, and deployment partnerships are better positioned than vendors that compete only on chip-level specifications.

Humanoid Robot GPU Industry Leaders

NVIDIA Corporation

Qualcomm Incorporated

Intel Corporation

Advanced Micro Devices, Inc.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA announced the Isaac GR00T Reference Humanoid Robot at GTC Taipei, the first open humanoid robot reference design integrating a Unitree H2 Plus chassis with NVIDIA Jetson AGX Thor T5000 onboard compute delivering 2,070 FP4 teraflops. The platform is designed for academic and commercial research teams and is expected to be available from Unitree in late 2026, lowering the barrier to GPU-accelerated humanoid development across universities and robotics startups globally.

- June 2026: NVIDIA released Isaac GR00T N1.7 in early access with commercial licensing included, enabling production deployments of GR00T-based humanoid robot policies. N1.7 added finger-level dexterous control support for contact-rich tasks such as small parts assembly.

- April 2026: BMW Group launched the full pilot phase of its Leipzig humanoid robot deployment using Hexagon Robotics' AEON, marking the first humanoid robot in active automotive production in Europe. The deployment follows a December 2025 initial test and builds on the 10-month Spartanburg pilot with Figure AI that contributed to the production of over 30,000 BMW X3 vehicles.

- February 2026: Agility Robotics announced a commercial Robots-as-a-Service agreement with Toyota Motor Manufacturing Canada for 7 Digit humanoid robots at the Woodstock, Ontario RAV4 production facility, establishing the first commercially contracted humanoid deployment in the Canadian automotive industry. Each Digit unit deploys NVIDIA Jetson Thor for onboard inference, directly contributing to the onboard GPU segment's revenue inflection.

Global Humanoid Robot GPU Market Report Scope

The Humanoid Robot GPU Market refers to the segment of the GPU industry dedicated to providing graphical processing units specifically designed or optimized for humanoid robots. This market encompasses the development, production, and application of GPUs that enable advanced functionalities such as real-time processing, machine learning, and enhanced visual capabilities in humanoid robots.

The Humanoid Robot GPU Market Report is Segmented by GPU Type (Data Center Training GPUs, Edge AI GPUs, Embedded GPUs, and Integrated GPU Platforms), Deployment Type (Onboard Compute, Offboard Training and Simulation, and Hybrid Compute), GPU Function (Training and Simulation, Inference and Perception, Motion Planning and Control, and Digital Twin and Synthetic Data Generation), Robot Capability (Real-Time Perception, Motion Planning and Control, Dexterous Manipulation, and Multi-Modal Reasoning), End Use Industry (Automotive, Logistics and Warehousing, Manufacturing and Assembly, Research and Education, Healthcare and Assisted Living, and Defense and Security), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Data Center Training GPUs |

| Edge AI GPUs |

| Embedded GPUs |

| Integrated GPU Platforms |

| Onboard Compute |

| Offboard Training And Simulation |

| Hybrid Compute |

| Training and Simulation |

| Inference and Perception |

| Motion Planning and Control |

| Digital Twin and Synthetic Data Generation |

| Real-Time Perception |

| Motion Planning and Control |

| Dexterous Manipulation |

| Multi-Modal Reasoning |

| Automotive |

| Logistics and Warehousing |

| Manufacturing and Assembly |

| Research and Education |

| Healthcare and Assisted Living |

| Defense and Security |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By GPU Type | Data Center Training GPUs | |

| Edge AI GPUs | ||

| Embedded GPUs | ||

| Integrated GPU Platforms | ||

| By Deployment Type | Onboard Compute | |

| Offboard Training And Simulation | ||

| Hybrid Compute | ||

| By GPU Function | Training and Simulation | |

| Inference and Perception | ||

| Motion Planning and Control | ||

| Digital Twin and Synthetic Data Generation | ||

| By Robot Capability | Real-Time Perception | |

| Motion Planning and Control | ||

| Dexterous Manipulation | ||

| Multi-Modal Reasoning | ||

| By End Use Industry | Automotive | |

| Logistics and Warehousing | ||

| Manufacturing and Assembly | ||

| Research and Education | ||

| Healthcare and Assisted Living | ||

| Defense and Security | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the humanoid robot GPU space?

The humanoid robot GPU market size is expected to rise from USD 96.82 million in 2025 to USD 203.91 million in 2026 and reach USD 978.32 million by 2031, at a 36.84% CAGR over 2026-2031.

Which deployment model is growing the fastest for humanoid robot GPUs?

Onboard Compute is projected to grow the fastest, at a 38.14% CAGR through 2031, as live deployments need low-latency inference directly on the robot.

Why are data center training GPUs still the largest segment?

Data Center Training GPUs held 64.92% share in 2025 because robot developers still spend heavily on simulation, synthetic data generation, and foundation model training before scaling fleets.

Which end use sector is leading commercial adoption?

Automotive led with a 32.51% share in 2025, supported by visible deployments at BMW and contracted programs tied to Agility Robotics and Toyota.

What is pushing the demand for multi-modal reasoning in humanoid systems?

Buyers are looking for robots that can understand language, adapt to new settings, and complete multi-step tasks, which is why Multi-Modal Reasoning is projected to grow at a 37.92% CAGR through 2031.

Which region is strongest today, and which one is growing fastest?

Asia-Pacific led with a 47.62% share in 2025, while North America is projected to grow the fastest at a 38.57% CAGR through 2031 because it combines strong AI infrastructure with active commercial humanoid developers.

Page last updated on: