ADAS GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.38 Billion |

| Market Size (2031) | USD 16.27 Billion |

| Growth Rate (2026 - 2031) | 24.77% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ADAS GPU Market Analysis by Mordor Intelligence

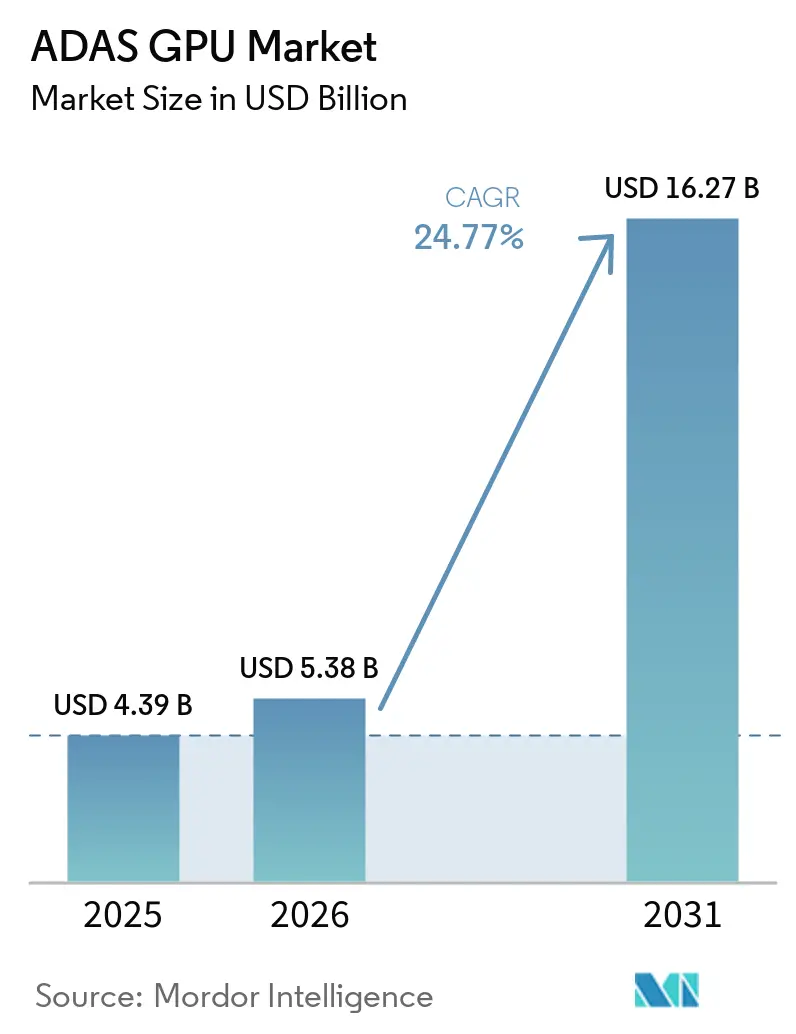

The ADAS GPU market size is expected to grow from USD 4.39 billion in 2025 to USD 5.38 billion in 2026 and is forecast to reach USD 16.27 billion by 2031 at 24.77% CAGR over 2026-2031. The move from optional driver assistance to always-on perception, planning, and in-cabin processing has made GPU-class computing a core part of new vehicle design. The ADAS GPU market is also gaining from the wider shift toward software-defined vehicles, where centralized compute replaces many smaller control units and raises the value of high-performance silicon in each platform. Safety rules are tightening at the same time, which is pushing automakers to adopt more capable computing stacks when they target advanced driver assistance functions and higher safety ratings. Memory bandwidth, thermal management, and functional safety qualification are shaping platform choices as strongly as raw compute performance, so suppliers that can combine hardware, software, and certification support are in a stronger position. This leaves the ADAS GPU market with clear room for growth in mainstream passenger vehicles, commercial fleets, and higher-autonomy programs, while competition increasingly centers on full-stack platform control rather than chip supply alone.

Key Report Takeaways

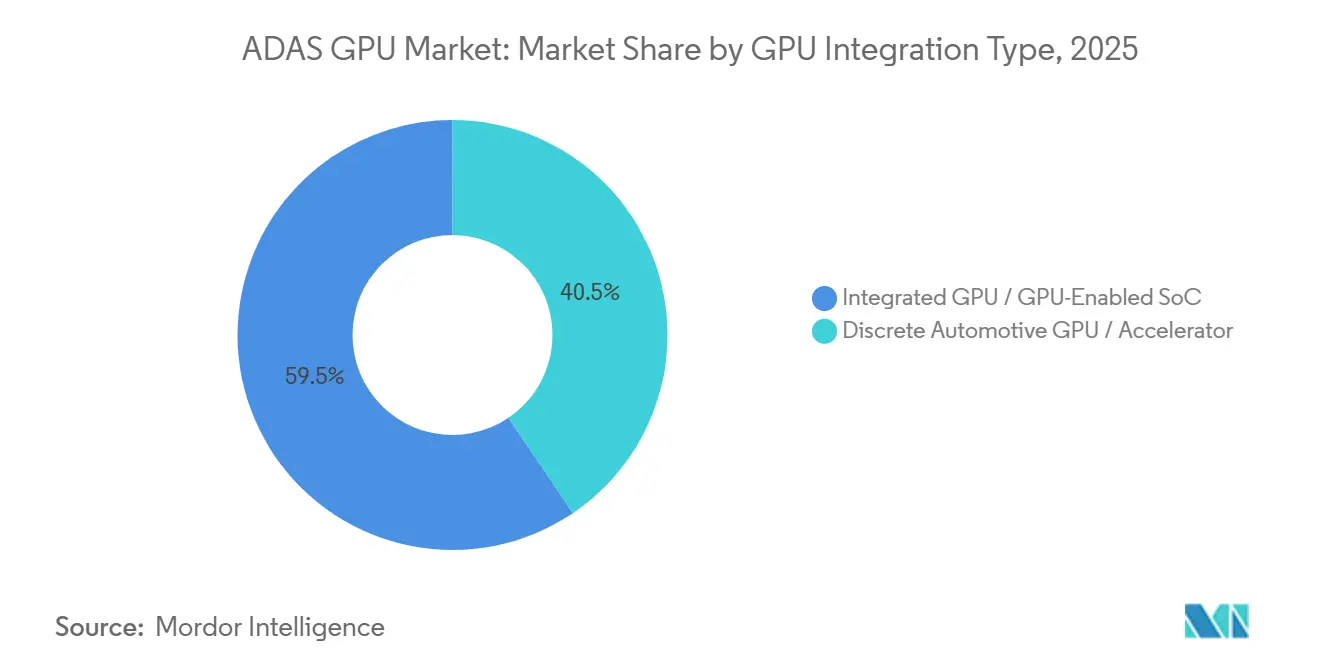

- By GPU integration type, integrated GPU and GPU-enabled SoC solutions led the ADAS GPU market with 59.46% of revenue in 2025, while discrete GPU and accelerator solutions are projected to expand at a 24.99% CAGR through 2031.

- By ADAS application, perception and sensor fusion accounted for 33.02% of revenue in 2025, while autonomous driving compute is projected to grow at a 25.03% CAGR through 2031.

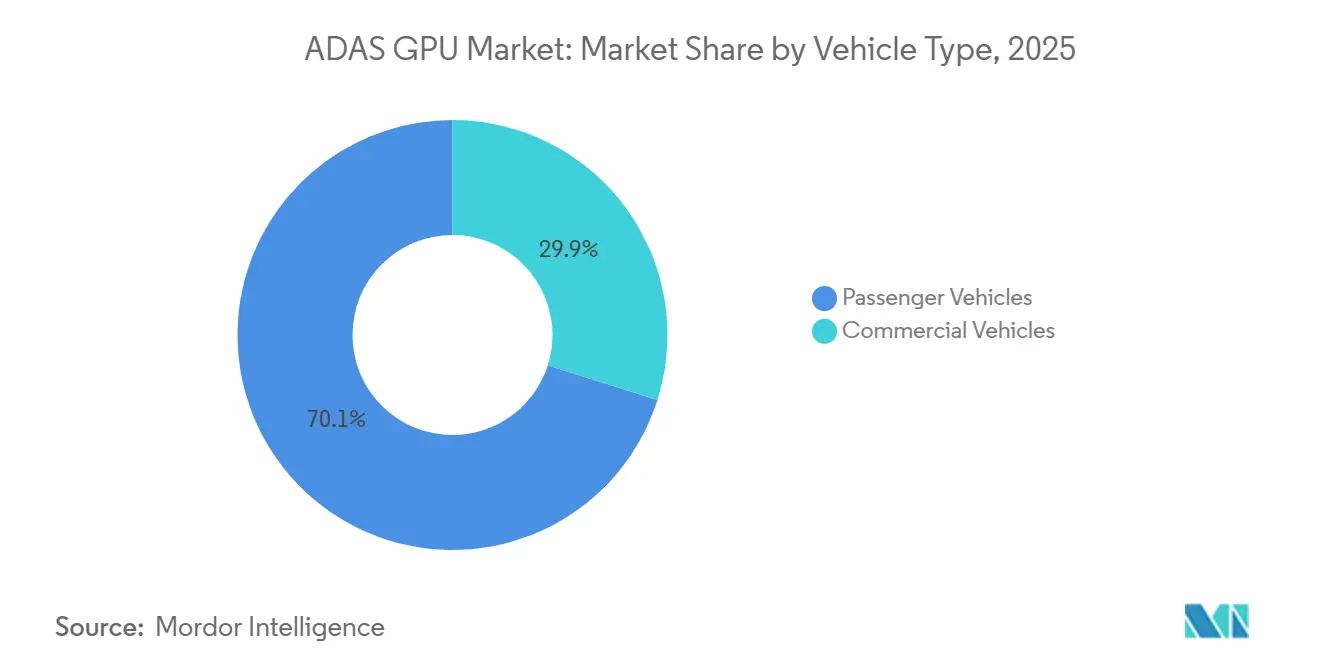

- By vehicle type, passenger vehicles accounted for 70.11% of revenue in the ADAS GPU market in 2025, while commercial vehicles are expected to record the highest CAGR of 25.33% through 2031.

- By level of autonomy, Level 2 systems accounted for 43.33% of revenue in 2025, while Level 4 systems are projected to grow at a 25.26% CAGR through 2031.

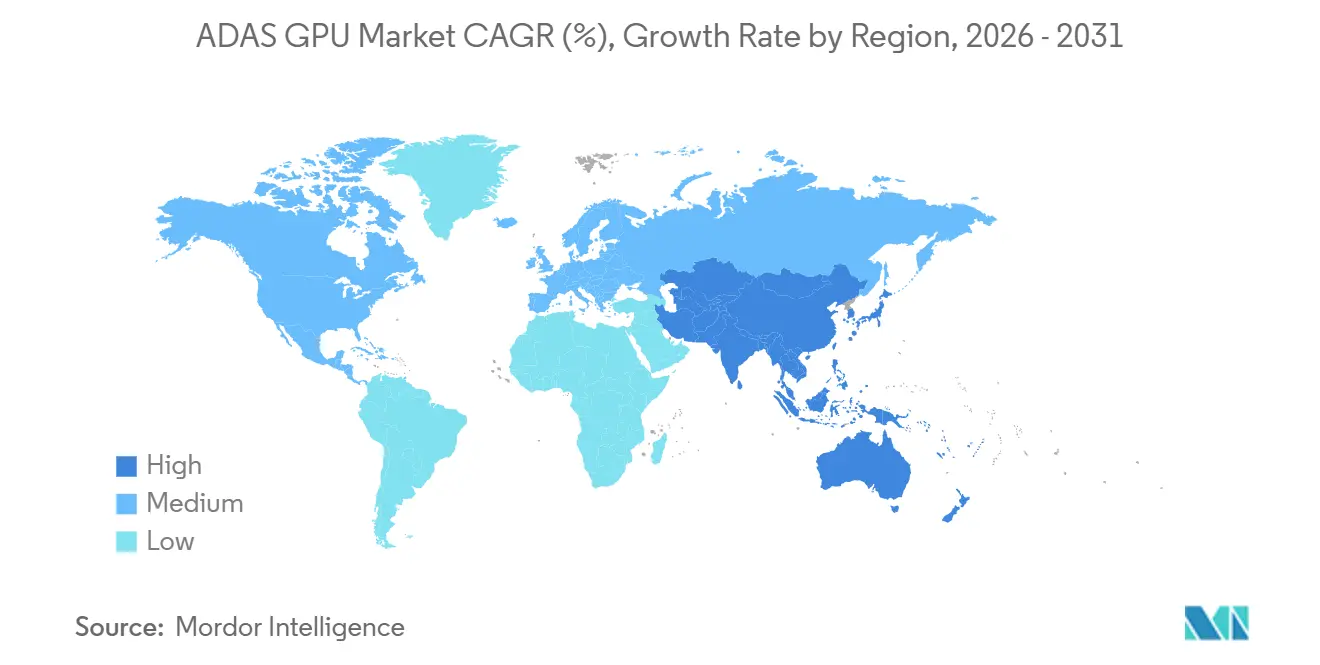

- By geography, Asia-Pacific led with 39.18% share of the ADAS GPU market revenue in 2025, while the Middle East and Africa are projected to expand at a 25.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ADAS GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ADAS Content Per Vehicle | +7.5% | Global | Short term (≤ 2 years) |

| Shift Toward Software-Defined Vehicles | +5.8% | Global | Medium term (2-4 years) |

| Growth of Centralized and Zonal Vehicle Architectures | +4.0% | Global, APAC core, spill-over to Europe and North America | Medium term (2-4 years) |

| Expansion of High-Resolution Digital Cockpits and Multi-Display Systems | +2.5% | Global, APAC and Europe leading | Short term (≤ 2 years) |

| Safety Regulation-Driven Compute Upgrades | +1.8% | North America and EU | Medium term (2-4 years) |

| Automotive AI and Sensor Fusion Workload Growth | +1.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising ADAS Content Per Vehicle

The ADAS GPU market is seeing its strongest near-term push from the steady increase in compute-heavy safety and convenience features per vehicle. Mid-range models now carry broader combinations of radar, surround-view cameras, driver monitoring, occupant monitoring, and highway or city assistance functions, which raises processing needs well beyond older control architectures. That change is no longer limited to premium vehicles, because mainstream launches now use feature bundles that require more parallel compute and faster data handling. As those features move into higher-volume production, suppliers are making GPU and SoC decisions earlier in the vehicle development cycle so they can lock software, memory, and validation plans together. This also raises the value of platforms that can support multiple workloads on the same silicon, since automakers want to avoid adding separate processors for each new function. The ADAS GPU market, therefore, benefits not only from more vehicles using assistance functions but also from each equipped vehicle carrying a higher compute load than the previous model cycle.

Shift Toward Software-Defined Vehicles

The shift toward software-defined vehicles is changing how automakers design electronic systems, and that directly supports the ADAS GPU market. Instead of spreading functions across dozens of dedicated control units, newer architectures move more sensing, decision-making, and user-interface tasks into fewer high-performance compute nodes. That model favors GPU-enabled SoCs because they are better suited to inference-heavy workloads that need fast parallel processing and shared memory access. Qualcomm and BMW introduced Snapdragon Ride Pilot in the all-new BMW iX3 as a jointly developed automated driving system, demonstrating how closely chip vendors now work with automakers on the software stack and hardware platform. The commercial effect is equally important because the software-defined model gives semiconductor platform suppliers a greater role in long-cycle vehicle programs and reduces the gap between the chip and vehicle roadmaps. For the ADAS GPU market, this means demand is increasingly tied to platform standardization across model families, not only to feature adoption in one vehicle line.

Growth Of Centralized And Zonal Vehicle Architectures

Centralized and zonal vehicle architectures are reinforcing the need for more capable automotive compute, which supports the ADAS GPU market over the medium term. In these designs, local zone controllers handle nearby actuation and input tasks, while a central compute domain manages perception, planning, connectivity, and other high-value functions. That arrangement increases the importance of GPU-capable silicon at the center of the vehicle because multiple workloads now need to run together with low latency and strong isolation. NVIDIA states that DRIVE Thor can isolate automated driving and in-vehicle infotainment on a single chip while linking functions with high-speed communication, which reflects the performance level that centralized designs are trying to reach.[1]NVIDIA Corporation, “NVIDIA DRIVE Thor, Platform Documentation,” NVIDIA, nvidianews.nvidia.com Microchip also notes that zonal deployments rely on Ethernet and PCIe links between zone controllers and a central compute module, which confirms that this architecture is becoming a practical foundation for software-defined vehicle programs.[2]Microchip Technology Inc., “Remote Control Protocol and the Concurrent Paradigm Shift to Zonal Architecture,” Microchip Technology, microchip.com As a result, the ADAS GPU market gains from every platform decision that shifts vehicle intelligence upward into fewer and more capable computing nodes.

Expansion Of High-Resolution Digital Cockpits And Multi-Display Systems

Digital cockpit expansion is adding another growth layer to the ADAS GPU market because display and assistance workloads increasingly share the same silicon. Newer vehicle interiors now combine instrument clusters, infotainment displays, head-up displays, and rear-seat screens, all of which need strong graphics processing and stable real-time response. When those functions are paired with ADAS processing on one platform, automakers can reduce the need for separate display chips and simplify system integration. NVIDIA presents DRIVE Thor as a platform that can run autonomous driving, infotainment, and dashboard functions at the same time, which captures this convergence clearly. Siemens also notes that software-defined vehicles depend on high-performance processors and advanced GPUs that can integrate sensor data, decision-making, and real-time response within a unified compute platform.[3]Siemens Digital Industries Software, “The Complete Guide to Software-Defined Vehicles,” Siemens Digital Industries Software, blogs.sw.siemens.com This means the ADAS GPU market can expand even in programs where autonomy remains limited, because cockpit graphics and assistance computing are moving onto the same hardware base.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Automotive Qualification and Functional Safety Burden | -1.2% | Global, stringent in Europe and North America | Long term (≥ 4 years) |

| Thermal and Power Envelope Constraints | -0.8% | Global | Medium term (2-4 years) |

| Semiconductor Supply Chain and Advanced Node Availability Risk | -0.6% | Global, Taiwan concentration risk | Short term (≤ 2 years) |

| Cost Pressure in Mass-Market Vehicle Platforms | -0.5% | Global, APAC mass-market, spill-over to South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Automotive Qualification And Functional Safety Burden

Functional safety remains one of the biggest constraints on the ADAS GPU market because automotive qualification requires more than strong compute performance. Suppliers need hardware safety mechanisms, redundancy, diagnostics, process controls, and documentation that meet the highest automotive safety standards over long development cycles. That adds time, cost, and engineering effort before a platform can enter production in safety-critical vehicle programs. NVIDIA said its DriveOS platform reached ASIL-D conformance, assessed by TÜV SÜD, and also achieved ISO 21434 cybersecurity process certification, which shows the scale of work needed to make a platform suitable for advanced autonomous applications. These requirements narrow the supplier base because consumer or data-center designs cannot be moved into vehicles without major redesign and validation. For the ADAS GPU market, the outcome is a smaller group of qualified platform vendors, premium pricing for compliant solutions, and slower capacity expansion than raw demand would otherwise support.

Thermal And Power Envelope Constraints

Thermal and power limits also restrain the ADAS GPU market, especially in higher-compute programs that push well beyond basic Level 2 assistance. Automotive environments expose compute hardware to enclosed spaces, high ambient temperatures, and sustained loads, making cooling a system-level problem rather than a chip-level one. Research on automotive GPU thermal behavior found that GPU junction temperatures can approach operating limits under city traffic conditions, where repeated stop-and-go cycles create heat accumulation over time. Thermal controls such as dynamic voltage and frequency scaling can reduce risk, but they can also introduce latency penalties that matter in real-time perception and response workloads. Active cooling helps at the high end, yet it raises packaging complexity and vehicle cost in programs that are already sensitive to bill-of-materials pressure. Because of that, the ADAS GPU market still depends on better packaging, tighter software management, and more efficient architecture choices to bring advanced compute into broader vehicle segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Integration Type: Integrated SoCs Hold The Revenue Base While Discrete Accelerators Gain In High-Compute Programs

Integrated GPU and GPU-enabled SoC solutions accounted for 59.46% of revenue in 2025, which kept this format at the center of the ADAS GPU market. Automakers continue to favor integrated designs because a single chip can simplify packaging, reduce power overhead, and streamline safety qualification across multiple functions. This advantage becomes stronger as centralized vehicle architectures spread, since one platform can cover perception, infotainment, gateway, and monitoring workloads in a shared compute domain. NVIDIA says DRIVE Thor is built to run automated driving and in-vehicle experiences on one architecture, which supports the value case for integrated solutions in multi-function vehicle platforms.

Discrete GPU and accelerator solutions are projected to grow at a 24.99% CAGR through 2031, which makes them the faster-rising integration format within the ADAS GPU market. Their growth comes from programs that need sustained compute far above what a single monolithic SoC can comfortably deliver in a mainstream thermal envelope. WeRide and Lenovo introduced an automotive-grade HPC 3.0 platform using dual NVIDIA DRIVE AGX Thor processors, and that example shows where discrete compute demand is emerging most clearly in autonomous mobility programs. At the same time, Imagination Technologies highlights safety-focused GPU IP that lowers power and die-area overhead, which supports the continued competitiveness of integrated formats in volume vehicle lines. This balance explains why integrated solutions still carry the larger ADAS GPU market size today, while discrete accelerators are building momentum where compute headroom matters more than packaging simplicity.

By ADAS Application: Perception And Sensor Fusion Lead Current Demand While Autonomous Driving Compute Advances Fastest

Perception and sensor fusion accounted for 33.02% of revenue in 2025, giving this category the largest application position in the ADAS GPU market. Every ADAS-equipped vehicle needs a perception pipeline, which keeps this workload relevant across Level 1, Level 2, and higher-autonomy configurations. The segment also benefits from the broad use of cameras, radar, and driver-monitoring functions that all rely on high-throughput parallel processing. That is why perception remains the revenue anchor even as other application categories gain speed within the ADAS GPU market.

Autonomous driving compute is projected to expand at a 25.03% CAGR through 2031, making it the fastest-growing application area in the ADAS GPU market. NVIDIA said BYD, Geely, Isuzu, and Nissan have adopted DRIVE Hyperion for Level 4 vehicle programs, pointing to rising demand for platforms that can handle surround sensing, path planning, and in-cabin AI together. Path planning, decision-making, surround view, parking assistance, and driver or occupant monitoring continue to expand as part of the same compute stack, rather than as isolated modules on separate hardware. As those workloads converge, platform vendors that can unify them on a single chip or compute domain gain a stronger value proposition with automakers. This is also where the ADAS GPU market share of advanced application stacks becomes more meaningful, because the fastest growth is coming from software-rich deployments rather than from simple feature additions alone.

By Vehicle Type: Passenger Vehicles Sustain Scale While Commercial Vehicles Set The Pace For Growth

Passenger vehicles accounted for 70.11% of revenue in 2025, making them the largest vehicle category in the ADAS GPU market. This leadership reflects the sheer volume of passenger car production and the broadening use of lane support, automatic emergency braking, parking functions, and driver monitoring in mid-range and premium trims. The segment also benefits from the way GPU-enabled SoCs can be reused across many models within an automaker's portfolio, which improves platform scale and cost control. As a result, passenger cars still define the largest part of the current ADAS GPU market size, even while newer autonomy programs attract more attention.

Commercial vehicles are projected to grow at a 25.33% CAGR through 2031, which makes them the fastest-rising vehicle type in the ADAS GPU market. Long-haul freight, transit, and controlled-route operations have strong incentives to use richer perception and planning stacks because uptime, safety, and labor economics are closely tied to automation performance. NVIDIA said Isuzu and TIER IV were developing Level 4 autonomous buses on DRIVE AGX Thor, which illustrates how higher-compute platforms are moving into commercial mobility use cases. The commercial segment still relies on passenger-vehicle scale for silicon cost learning, yet its own requirements are becoming distinct, as fleet operators often need sustained compute and broader sensing coverage. That relationship keeps passenger cars central to unit volume, while commercial vehicles raise the performance ceiling for the ADAS GPU market.

By Level Of Autonomy: Level 2 Provides The Revenue Foundation While Level 4 Drives The Next Growth Wave

Level 2 systems accounted for 43.33% of revenue in 2025, which made them the largest autonomy tier in the ADAS GPU market. Their position reflects global deployment across high-volume models where highway assist, lane centering, and automatic emergency braking are reaching a wider customer base. These features still require robust perception and inference capabilities, but they can be delivered in cost-controlled compute packages that suit mainstream production. That makes Level 2 the commercial foundation of the ADAS GPU market in the current cycle.

Level 4 is projected to grow at a 25.26% CAGR through 2031, making it the fastest-growing autonomy tier in the ADAS GPU market. NVIDIA and Uber announced plans to support a Level 4 mobility network targeting up to 100,000 autonomous vehicles, underscoring the procurement scale that fleet-based autonomy can achieve once deployments move beyond pilots. Qualcomm and BMW also launched a Level 2+ system validated for more than 60 countries, which shows how a single platform can scale globally before full autonomy reaches mass production. Level 3 remains limited to narrower operating domains, while Level 5 stays tied to research and long-range development rather than broad commercialization. The growth pattern therefore keeps current revenue centered on Level 2, while higher-autonomy programs define where the ADAS GPU market will add its most demanding compute opportunities.

Geography Analysis

Asia-Pacific held 39.18% of revenue in 2025, which gave it the leading regional position in the ADAS GPU market. The region benefits from large vehicle production volumes, fast feature rollout in China, and strong links between domestic vehicle programs and compute platform suppliers. China remains the main demand center because it combines broad passenger vehicle output with rapid adoption of centralized compute and advanced assistance functions. Japan supports the regional base through commercial vehicle and autonomous bus activity, while South Korea adds strength through advanced semiconductor and vehicle platform development. NVIDIA said BYD, Geely, Isuzu, and Nissan adopted DRIVE Hyperion for Level 4 programs, which underlines the depth of regional engagement across both passenger and commercial platforms.

North America and Europe form the next major cluster in the ADAS GPU market, supported by premium vehicle programs, strict safety expectations, and active autonomous mobility development. Euro NCAP announced a 2026 protocol overhaul with a four-pillar safety framework, and that increases the importance of tightly integrated compute for vehicles targeting top safety scores. North America remains important for robotaxi development, simulation infrastructure, and partnerships between compute platform vendors and mobility operators. Mercedes-Benz presented its next-generation S-Class on NVIDIA DRIVE AV with an L4-ready architecture, which shows how Europe continues to influence the high end of the ADAS GPU market through premium vehicle innovation.

The Middle East and Africa is projected to expand at a 25.11% CAGR through 2031, making it the fastest-growing regional segment in the ADAS GPU market. Growth there is supported by smart mobility investment, premium vehicle demand, and the early buildout of autonomous mobility ecosystems in Gulf markets. NVIDIA said its June 2026 DRIVE Hyperion ecosystem expansion included Middle East mobility collaborations, which signals active commercial interest rather than only exploratory positioning. South America remains smaller, but it is progressing through commercial fleet safety requirements and premium passenger vehicle adoption that gradually raise the compute content of locally relevant vehicle platforms.

Competitive Landscape

The ADAS GPU market has a concentrated platform layer and a more fragmented integration layer. A small group of suppliers holds the strongest position in high-value compute because automotive programs need certified software stacks, long validation histories, and deep engineering support. That combination creates barriers that are much harder to cross than standard chip design barriers alone. NVIDIA said its DRIVE Hyperion platform achieved key automotive safety and cybersecurity milestones for AV development, which shows why compliance depth is central to competitive standing in this market. In practical terms, the companies that control the hardware, operating system, and safety case together have the most durable advantage in the ADAS GPU market.

Competitive strategy is moving toward full-stack offerings that tie silicon, software, and vehicle deployment more tightly together. Stellantis expanded its partnership with Qualcomm in May 2026 to deploy Snapdragon Digital Chassis platforms across next-generation vehicle architectures, which shows how automakers are locking in broader compute relationships rather than sourcing isolated components. NVIDIA also deepened its position through DRIVE Hyperion adoption by BYD, Geely, Isuzu, and Nissan for Level 4 vehicles, which strengthened its visibility in future autonomous programs. These moves show that design wins now depend on ecosystem reach and software readiness as much as on raw TOPS performance.

There is still open space in lower-cost unified cockpit and ADAS nodes, in mid-range commercial vehicle platforms, and in software layers that can run across more than one chip architecture. Wayve and NVIDIA announced discussions around a proposed strategic investment in September 2025, which highlighted the value placed on scalable autonomous software approaches that can support future production programs. The market is also watching whether automakers deepen in-house compute efforts, because that could shift some value away from merchant silicon over time. For now, the ADAS GPU market remains shaped by platform vendors that can combine performance, safety certification, and automaker integration at production scale.

ADAS GPU Industry Leaders

NVIDIA Corporation

Qualcomm Technologies, Inc.

Intel Corporation

Advanced Micro Devices, Inc.

Mobileye Global Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA announced a major expansion of the DRIVE Hyperion robotaxi-ready platform ecosystem at GTC Taipei, adding Foxconn as a contract design and manufacturing partner for Level 4 electric vehicles with initial deployment in Taiwan and planned expansion into Asia and the Middle East. The announcement incorporated HUMAIN AI and mobility collaborations, with NVIDIA and Uber confirming expanded autonomous fleet deployment across eight cities on four continents by 2028.

- May 2026: Stellantis and Qualcomm Technologies expanded their multi-year collaboration to deploy Snapdragon Digital Chassis SoCs, including the Snapdragon Ride Pilot Level 2+ ADAS stack, across millions of next-generation Stellantis vehicles globally. The agreement also included a non-binding letter of intent for Stellantis' automated driving software subsidiary aiMotive to join Qualcomm Technologies, subject to various conditions and regulatory approvals.

- March 2026: NVIDIA announced that BYD, Geely, Isuzu, and Nissan adopted the DRIVE Hyperion platform for next-generation Level 4 autonomous vehicle programs, with Isuzu and TIER IV developing Level 4 autonomous buses on DRIVE AGX Thor SoCs. Hyundai Motor Company and Kia simultaneously expanded their strategic autonomous driving collaboration with NVIDIA, covering SDV development on DRIVE Hyperion and potential Motional Level 4 robotaxi integration.

- March 2026: Mercedes-Benz unveiled its next-generation S-Class built on NVIDIA DRIVE Hyperion and full-stack DRIVE AV software, with an L4-ready architecture combining end-to-end AI inference with a parallel classical driving stack. The vehicle's compute stack incorporated NVIDIA Halos for multi-layer AI safety oversight, including an NCAP five-star active safety module.

Global ADAS GPU Market Report Scope

The ADAS GPU Market refers to the market for graphics processing units used in advanced driver-assistance systems to process real-time data from cameras, radar, LiDAR, and other vehicle sensors. These GPUs enable functions such as lane departure warning, adaptive cruise control, object detection, and emergency braking by accelerating AI and sensor-fusion workloads.

The ADAS GPU Market Report is Segmented by GPU Integration Type (Integrated GPU/SoC, and Discrete GPU/Accelerator), ADAS Application (Perception and Sensor Fusion, Path Planning, Driver Monitoring, Surround View, and Autonomous Driving Compute), Vehicle Type (Passenger Vehicles, and Commercial Vehicles), Level of Autonomy (Level 1, Level 2, Level 3, Level 4, and Level 5), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPU / GPU-Enabled SoC |

| Discrete Automotive GPU / Accelerator |

| Perception and Sensor Fusion |

| Path Planning and Decision-Making |

| Driver Monitoring and Occupant Monitoring |

| Surround View and Parking Assistance |

| Autonomous Driving Compute |

| Passenger Vehicles |

| Commercial Vehicles |

| Level 1 |

| Level 2 |

| Level 3 |

| Level 4 |

| Level 5 |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By GPU Integration Type | Integrated GPU / GPU-Enabled SoC | |

| Discrete Automotive GPU / Accelerator | ||

| By ADAS Application | Perception and Sensor Fusion | |

| Path Planning and Decision-Making | ||

| Driver Monitoring and Occupant Monitoring | ||

| Surround View and Parking Assistance | ||

| Autonomous Driving Compute | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Level of Autonomy | Level 1 | |

| Level 2 | ||

| Level 3 | ||

| Level 4 | ||

| Level 5 | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the ADAS GPU space?

The ADAS GPU market was valued at USD 4.39 billion in 2025, reached USD 5.38 billion in 2026, and is forecast to reach USD 16.27 billion by 2031 at a 24.77% CAGR over 2026-2031.

Which region leads revenue generation for GPU-based ADAS solutions?

Asia-Pacific led with 39.18% of revenue in 2025, supported by strong vehicle production, rapid feature rollout, and active Level 4 platform adoption across key OEM programs.

Which vehicle category is growing fastest for advanced automotive GPU demand?

Commercial vehicles are projected to grow at a 25.33% CAGR through 2031, driven by fleet economics, safety requirements, and the compute needs of autonomous freight and transit applications.

Which ADAS application creates the largest revenue base today?

Perception and sensor fusion held 33.02% of revenue in 2025 because every ADAS-equipped vehicle needs a core perception pipeline regardless of its automation level.

Why are integrated automotive SoCs still dominant in this field?

Integrated GPU and GPU-enabled SoC solutions held 59.46% of revenue in 2025 because they simplify thermal management, system integration, and safety qualification across several functions.

What is the main challenge slowing wider deployment of higher-compute ADAS platforms?

Functional safety qualification and thermal management are the main hurdles, because suppliers must meet strict automotive standards while controlling sustained heat and power in enclosed vehicle environments.

Page last updated on: