GPU In Robotics and Smart Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.25 Billion |

| Market Size (2031) | USD 5.06 Billion |

| Growth Rate (2026 - 2031) | 22.42% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

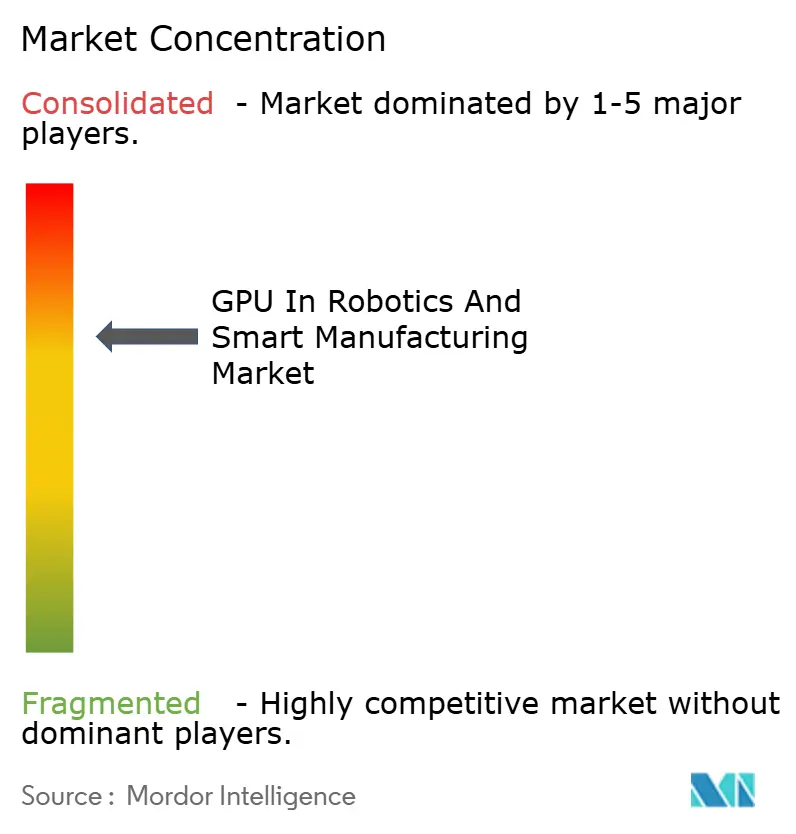

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU In Robotics and Smart Manufacturing Market Analysis by Mordor Intelligence

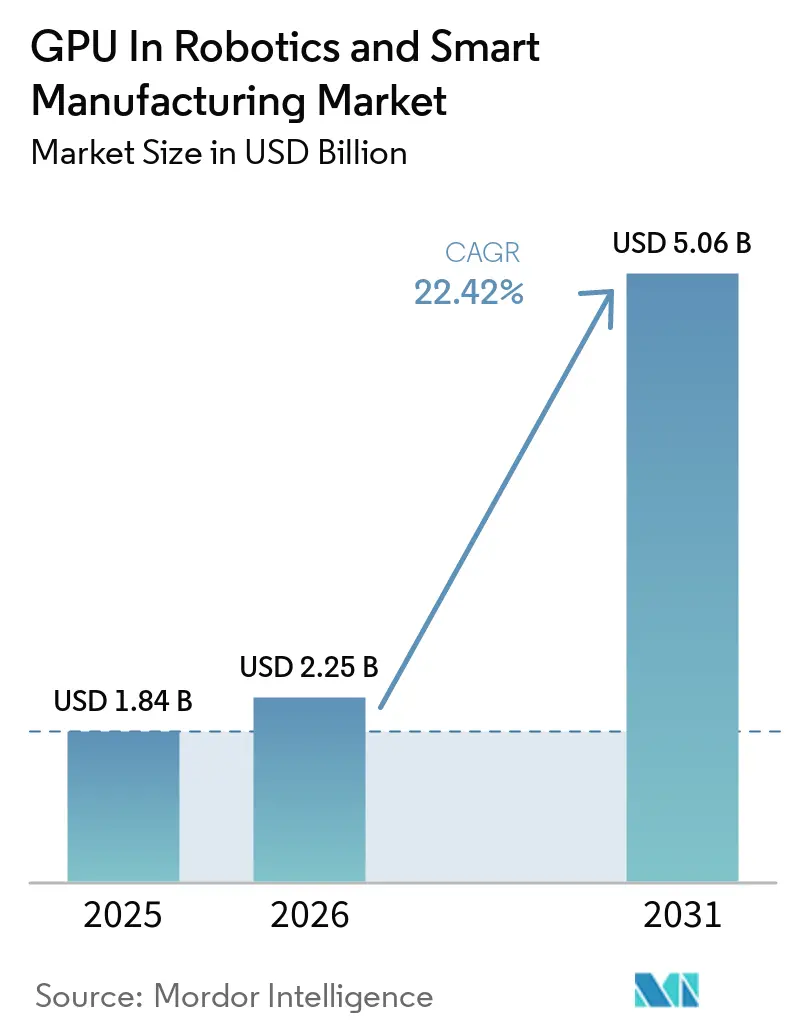

The GPU in robotics and smart manufacturing market size is expected to increase from USD 1.84 billion in 2025 to USD 2.25 billion in 2026 and reach USD 5.06 billion by 2031, growing at a CAGR of 22.42% over 2026-2031. Edge-deployed graphics processors are becoming the default engine for camera-heavy inspection, predictive maintenance and digital-twin workloads as manufacturers shift time-critical inference away from distant data centers. Demand is accelerating because modern transformer vision models require parallel architectures that outclass CPUs, while quantized visual-language-action networks now fit on single-slot consumer GPUs. Factories are also standardizing on hybrid topologies that train models centrally and push weights to line-side servers, lowering recurring data-science costs. Competitive intensity is rising as silicon vendors bundle purpose-built software stacks and partner directly with robot OEMs, compressing deployment timelines for brownfield plants.

Key Report Takeaways

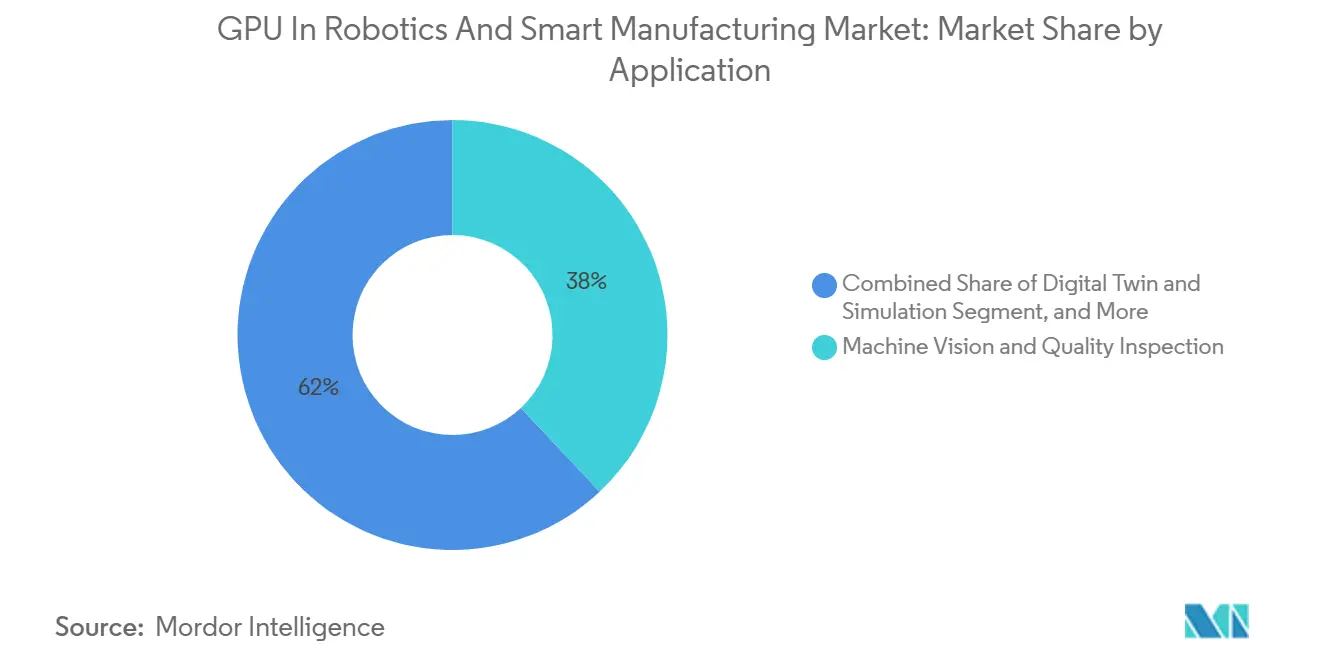

- By application, machine vision and quality inspection led with 38% of the GPU in robotics and smart manufacturing market share in 2025, whereas digital twin and simulation will experience the highest CAGR at 22.57% through 2031.

- By robot type, industrial robots captured 49% share of the GPU in robotics and smart manufacturing market size in 2025, while autonomous mobile robots are advancing at the fastest CAGR of 22.83% through 2031.

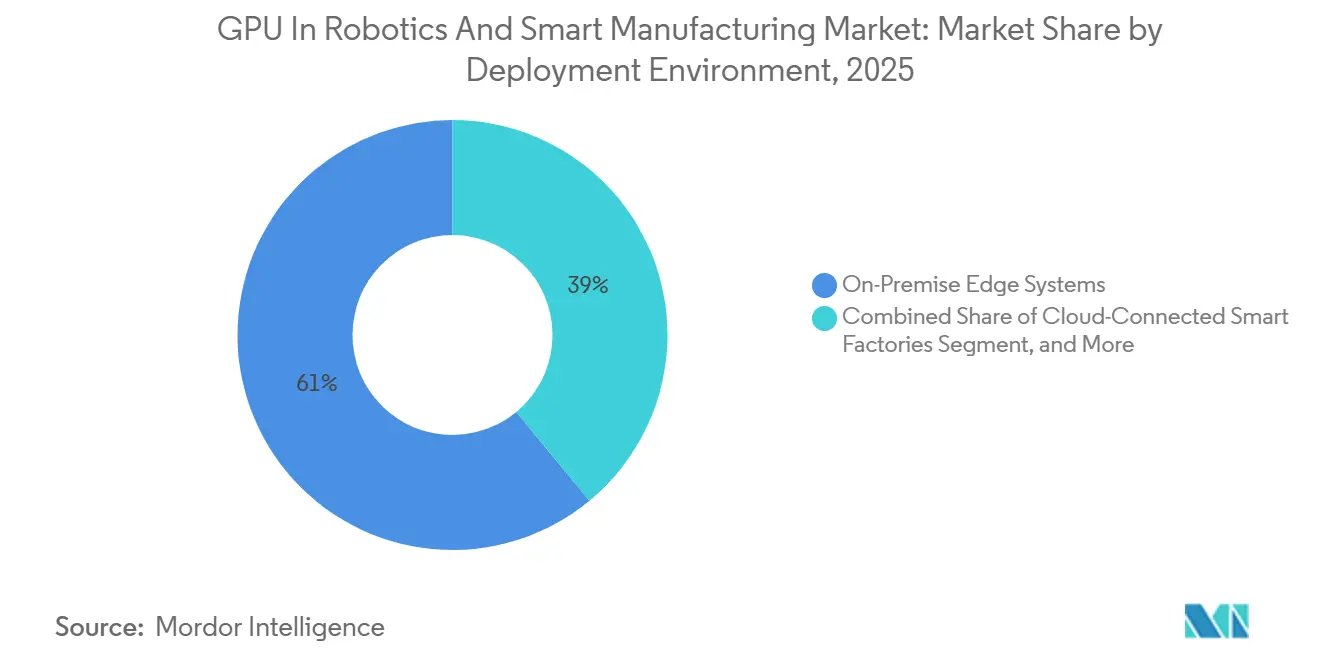

- By deployment environment, on-premise edge systems held 61% revenue share of the GPU in robotics and smart manufacturing market in 2025, but cloud-connected smart factories are projected to post the highest growth rate at 23.15%.

- By end-user industry, electronics and semiconductor accounted for 33% of the GPU in robotics and smart manufacturing market size in 2025, whereas logistics and warehousing is forecast to expand at the quickest pace at a CAGR of 22.65% over 2026-2031.

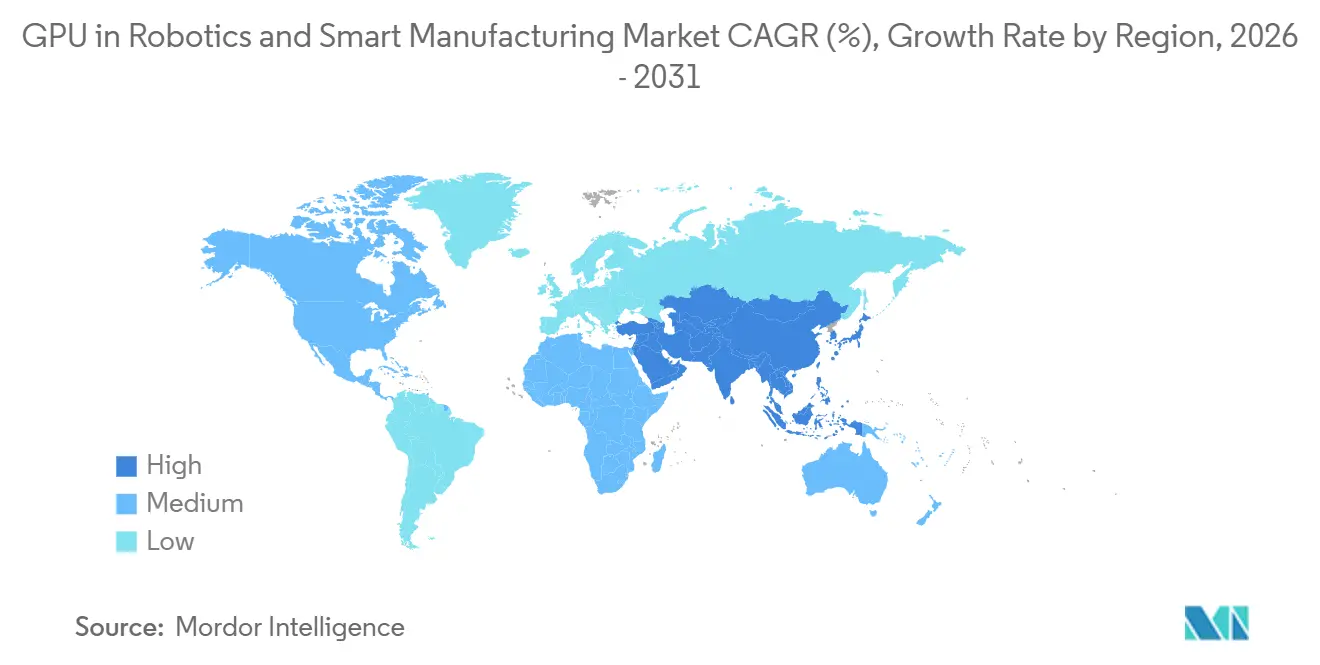

- By geography, Asia-Pacific commanded 64% revenue share of the GPU in robotics and smart manufacturing market in 2025, yet North America is poised for the most rapid CAGR of 22.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU In Robotics and Smart Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI‑Driven Machine Vision Quality Inspection | +5.2% | Global, with concentration in Asia‑Pacific electronics hubs and North America semiconductor corridors | Short term (≤ 2 years) |

| Expanding Adoption of Collaborative Robots in Automotive and Electronics Factories | +4.8% | North America and Europe automotive clusters, Asia‑Pacific electronics assembly lines | Medium term (2-4 years) |

| Demand for Real‑Time Predictive Maintenance Powered by Edge GPUs | +3.9% | Global, with early adoption in heavy machinery sectors | Medium term (2-4 years) |

| Rising Investment in Industry 4.0 Smart Factories Across Asia‑Pacific | +4.1% | Asia‑Pacific core, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Availability of Compact Liquid‑Cooled 4‑GPU Edge Servers Enabling In‑Cell Deployment | +2.7% | Global, with faster uptake in space‑constrained automotive and electronics plants | Short term (≤ 2 years) |

| Quantized Visual‑Language‑Action Models Enabling On‑Robot Inference on Consumer GPUs | +2.5% | Global, with accelerated adoption among small and medium enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in AI-Driven Machine Vision Quality Inspection

Modern electronics and semiconductor lines process gigapixel images at full conveyor speed, a data rate that overwhelms CPU pipelines. New inspection platforms pair 200-megapixel sensors with tensor-core GPUs, cutting escape rates below five parts per million and shrinking feedback loops from end-of-line to within a single lot. Automotive tier-1 suppliers report 25-40% fewer false positives, saving up to USD 5 million per plant each year. Transformer vision networks, which demand roughly ten times more compute than legacy convolutional models, cement GPUs as the only viable inference engine for next-generation quality control.

Expanding Adoption of Collaborative Robots in Automotive and Electronics Factories

Retrofit accelerator cards now slide into existing cobots, bringing real-time force-torque sensing and adaptive grasping without replacing mechanical arms. Automotive battery lines need sub-millimeter alignment that cannot tolerate 100-millisecond cloud roundtrips, so embedded GPUs handle vision, safety and motion planning locally. Eliminating perimeter cages reduces installation costs by up to 40% and frees floor space for additional tooling, a compelling return on investment for plants juggling frequent model changes.

Demand for Real-Time Predictive Maintenance Powered by Edge GPUs

Continuous vibration and acoustic monitoring at 1 kHz sampling rates lets algorithms warn of bearing or gear faults weeks before failure. Edge GPU servers analyze 10,000 sensor channels in milliseconds, whereas batch processing every four hours misses transient anomalies. Heavy-equipment operators in mining and steel avoid USD 50,000-200,000 per hour of unplanned downtime, achieving payback in roughly 18 months. These savings are driving multi-year procurement roadmaps for GPU-equipped controllers across discrete and process industries.

Rising Investment in Industry 4.0 Smart Factories Across Asia-Pacific

Policy incentives are fueling large-scale GPU deployment. South Korea plans 260,000 units by 2027 and China targets 30,000 smart factories, each mandated to embed AI inspection and predictive maintenance. Regional consortia standardize digital-twin frameworks so automotive, electronics and battery plants can simulate line changes virtually, trimming commissioning cycles by up to six months. Government subsidies accelerate purchases because plants that miss AI benchmarks risk losing export certifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Total Cost of Ownership of Industrial GPU Systems | −3.8% | Global, with acute impact on SMEs in emerging markets | Short term (≤ 2 years) |

| Integration Complexity with Legacy PLC and Control Architectures | −3.2% | North America and Europe brownfield industrial sites | Medium term (2–4 years) |

| Thermal Management Challenges in Enclosed Robot Bases | −1.9% | Global, with heightened risk in tropical climates | Medium term (2–4 years) |

| Supply‑Chain Risks for Advanced Packaging Substrates in HBM‑Based GPUs | −2.4% | Global, affecting pricing stability and lead times | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Total Cost of Ownership of Industrial GPU Systems

A rugged four-GPU edge box with liquid cooling can list above USD 100,000, quadruple the price of a CPU automation controller. Chilled-water loops, software licenses and IEC 62443 cybersecurity add another 20-30% over five years. Small and medium manufacturers in cost-sensitive economies postpone upgrades despite attractive payback windows, limiting near-term penetration outside tier-1 enterprises.

Integration Complexity with Legacy PLC and Control Architectures

Plants running 1990s-era PLCs must bridge Modbus or PROFIBUS to modern MQTT or OPC UA streams before inference servers can ingest data. Custom gateways and ladder-logic translation projects routinely last 6-12 months and cost up to USD 150,000 per line. Even automated toolchains support only the latest controller firmware, excluding millions of installed units and slowing GPU rollouts in brownfield facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Machine Vision Dominates While Digital Twins Accelerate

GPU in robotics and smart manufacturing market size allocation shows machine vision claimed 38% of 2025 revenue. Semiconductor fabs demand sub-micron defect detection, locking GPUs into every inspection bay. Digital twin and simulation workloads are the fastest climber because automotive OEMs now test dozens of line layouts in virtual environments, compressing ramp-up schedules by half. Predictive maintenance steadily scales as edge servers handle 1 kHz sensor fusion without overspending on compute. Autonomous material handling remains the smallest slice but is poised to surge as e-commerce hubs retrofit fleets of mobile robots that require sub-50-millisecond local inference.

Digital-twin users note energy savings up to 12% and cycle-time cuts near 8% after optimizing paint-shop robotics on high-end GPU clusters. Transformer vision models, ten times heavier than previous CNNs, guarantee continued silicon demand. Predictive maintenance users report downtime reductions of 25-40%, translating to millions of dollars annually. Autonomous material handling is gaining traction because an AMR fleet of 200-plus units creates larger cumulative GPU demand than incremental arm upgrades on fixed robots.

By Robot Type: Industrial Arms Lead as AMRs Grow Fastest

Industrial robots delivered 49% of 2025 revenue for the GPU in robotics and smart manufacturing market, driven by established automotive and electronics programs. AMRs and AGVs, though smaller today, are expanding quickest because warehouse paths change second-by-second and cannot wait for cloud decisions. Collaborative robots trail in share but show double-digit growth as bolt-on GPU cards modernize installed fleets. New cobot models integrate wrist cameras and embedded GPUs that moderate grip force, trimming scrap on fragile components by up to 50%.

North American warehouses added more than 1,000 new AMRs in early 2026, proving that edge GPUs erase the 100-200 ms latency that once capped robot speed. Industrial arms now rely on GPU-guided bin picking to achieve 120 picks per minute, aligning with just-in-sequence automotive delivery. Collaborative units benefit from GPU-accelerated safety perception that allows human-robot co-work without expensive cages.

By Deployment Environment: Edge Dominates as Hybrid Rises

On-premise edge servers captured 61% of 2025 revenue because safety loops require deterministic 10-50 ms response. Cloud-connected factories now grow fastest; hybrid topologies train models on centralized GPU farms then push weights to line-side devices. Hybrid adoption is rising after public clouds introduced rack-scale GPU appliances pre-certified for IEC 62443, reducing local IT overhead.

Fanless four-Jetson boxes rated for 70 °C enable edge inference in paint shops and foundries with punishing thermal profiles. Liquid-cooled 4U racks delivering 1.2 peta-int8 ops process 300 mm wafer images at 200 wafers per hour. Hybrid orchestrators update model versions across 50-plus plants without taking lines offline, a must for global automotive producers.

By End-User Industry: Electronics Dominates, Logistics Surges

Electronics and semiconductor lines consumed 33% of 2025 spending as wafer inspection moved entirely to GPU acceleration. Logistics and warehousing is the breakout segment through 2031 because each fulfillment center now orders hundreds of AMRs outfitted with Jetson-class modules. Automotive plants stay a strong second, embedding GPU inference into welding, assembly, and battery-pack stations. Heavy machinery firms increasingly embed GPUs in field equipment for condition-based maintenance, shaving 18-25% off unplanned downtime.

Advanced-node fabs in Arizona and Texas rely on GPU-equipped optical and electron-beam tools to hit sub-five-ppm yield targets. Logistics operators see 40-60% throughput gains from GPU-ready AMRs, unlocking 18-24-month payback windows even at high silicon prices. Automotive suppliers retrofitting 10,000 cobots avoid replacing mechanical arms, cutting capex by up to 40%.

Geography Analysis

Asia-Pacific contributed 64% of 2025 revenue to the GPU in robotics and smart manufacturing market due to massive policy-backed rollouts in South Korea, China and Japan. South Korea’s consortia plan 260,000 GPUs by 2027, while China mandates AI quality inspection in 30,000 smart factories. Japan subsidizes precision-machining SMEs that deploy GPU vision systems, and India includes GPUs in production-linked incentives for electronics clusters.[1]South Korea MOTIE, “M.AX Alliance Commits to Deploy 260,000 GPUs by 2027,” motie.go.kr

North America is the fastest-growing region over 2026-2031, buoyed by USD 202 billion of semiconductor and EV investments that specify GPU-accelerated defect detection. Arizona hosts multibillion-dollar fabs that embed GPU optics, and Tennessee’s new EV campus will run 1 200 cobots with on-board inference. Mexico upgrades nearshored automotive lines with GPU vision to match U.S. throughput, lifting Latin American adoption from a small base.

Europe ranks third but gains momentum from an industrial AI cloud launched in Germany with 10 000 latest-generation GPUs. The European Union’s AI Factories initiative allocates EUR 20 billion (USD 22 billion) for processors across Gigafactories, expanding demand for liquid-cooled server enclosures. The Middle East and Africa host early pilots in petrochemicals and logistics, while South America sees initial traction in automotive clusters.[2]European Commission, “EU AI Factories Initiative Allocates EUR 20 Billion,” ec.europa.eu

Competitive Landscape

Market concentration remains moderate, the top three suppliers dominate the GPU silicon scene, reaping about two-thirds of the accelerator revenue. This dominance highlights the significant influence these key players hold in shaping the market's trajectory. Meanwhile, a multitude of robot OEMs, system integrators, and edge server vendors compete for the remaining share, creating a fragmented landscape that fosters innovation and niche specialization. NVIDIA is streamlining deployment cycles to just six months by bundling synthetic-data generators with industrial AI operating systems, a strategy aimed at accelerating adoption and reducing time-to-market for end-users.[3]NVIDIA Corporation, “NVIDIA Announces Physical AI Data Factory Blueprint,” nvidia.com AMD is strategically positioning its cost-effective embedded GPUs, targeting niches like predictive maintenance and digital twins, which are gaining traction as industries increasingly adopt advanced analytics and simulation technologies. Intel is capitalizing on its established industrial PC presence, promoting cross-sales of its Arc graphics and Xeon CPUs, now with matrix extensions, to deliver enhanced computational capabilities tailored to industrial applications.

Turnkey solution integrators are setting themselves apart by pre-certifying their hardware and software to standards like IEC 62443 and ISO 13849, thereby lightening the compliance load for manufacturers and ensuring seamless integration into existing workflows. This approach not only reduces operational risks but also enhances the appeal of these solutions in highly regulated industries. An emerging aftermarket trend is evident with retrofit daughterboards designed to seamlessly integrate into existing cobots, showcasing efforts to prolong asset life and maximize return on investment for manufacturers.

There's a competitive engineering push, as seen in thermal-management patents for compact liquid-cooled enclosures, aiming to embed multi-GPU servers directly within production cells. These innovations are designed to withstand challenging conditions, including sweltering ambient temperatures exceeding 45 °C, ensuring reliable performance in demanding industrial environments.

GPU In Robotics and Smart Manufacturing Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Siemens deployed humanoid robots with embedded Jetson Thor at its Erlangen plant, demonstrating cage-free cooperative assembly.

- March 2026: Samsung confirmed HBM4 capacity is fully booked through mid-year, stretching GPU server lead times to more than 50 weeks.

- March 2026: NVIDIA introduced the Physical AI Data Factory Blueprint, slashing synthetic-data preparation from 12 months to two.

- February 2026: Germany’s Industrial AI Cloud came online with 10,000 Blackwell GPUs to centralize model training for regional manufacturers.

Global GPU In Robotics and Smart Manufacturing Market Report Scope

The GPU in Robotics and Smart Manufacturing Market pertains to the industry segment that leverages Graphics Processing Units (GPUs) to enhance computational efficiency, enable automation, and integrate intelligence into robotics and advanced manufacturing systems.

The Global GPU in Robotics and Smart Manufacturing Market Report is Segmented by Application (Machine Vision and Quality Inspection, Autonomous and Collaborative Robots, Industrial AI and Predictive Maintenance, Digital Twin and Simulation, Autonomous Material Handling), Robot Type (Industrial Robots, Collaborative Robots, Autonomous Mobile Robots), Deployment Environment (On-Premise Edge Systems, Cloud-Connected Smart Factories, Hybrid), End-User Industry (Automotive Manufacturing, Electronics and Semiconductor, Heavy Machinery and Industrial, Logistics and Warehousing), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Machine Vision and Quality Inspection |

| Autonomous and Collaborative Robots (Cobots) |

| Industrial AI and Predictive Maintenance |

| Digital Twin and Simulation |

| Autonomous Material Handling |

| Industrial Robots |

| Collaborative Robots (Cobots) |

| Autonomous Mobile Robots (AMRs/AGVs) |

| On-Premise Edge Systems |

| Cloud-Connected Smart Factories |

| Hybrid |

| Automotive Manufacturing |

| Electronics and Semiconductor |

| Heavy Machinery and Industrial |

| Logistics and Warehousing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Application | Machine Vision and Quality Inspection | |

| Autonomous and Collaborative Robots (Cobots) | ||

| Industrial AI and Predictive Maintenance | ||

| Digital Twin and Simulation | ||

| Autonomous Material Handling | ||

| By Robot Type | Industrial Robots | |

| Collaborative Robots (Cobots) | ||

| Autonomous Mobile Robots (AMRs/AGVs) | ||

| By Deployment Environment | On-Premise Edge Systems | |

| Cloud-Connected Smart Factories | ||

| Hybrid | ||

| By End-User Industry | Automotive Manufacturing | |

| Electronics and Semiconductor | ||

| Heavy Machinery and Industrial | ||

| Logistics and Warehousing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current GPU in robotics and smart manufacturing market size?

The GPU in robotics and smart manufacturing market is valued at USD 1.84 billion in 2025 and is projected to reach USD 5.06 billion by 2031.

Which application segment is the largest user of GPUs inside factories?

Machine vision and quality inspection is the largest segment, accounting for 38% of 2025 revenue, driven by the need for high parallel compute to enable sub-micron defect detection.

Why are autonomous mobile robots adopting GPUs faster than other robot types?

Autonomous mobile robots (AMRs) require sub-50 ms local inference for real-time dynamic path planning, a latency threshold that embedded GPUs consistently meet.

How are manufacturers mitigating the high upfront cost of industrial GPU systems?

Manufacturers are adopting leasing models and GPU-as-a-service contracts to spread capital expenditure, while retrofit accelerator cards help extend the life of existing robotic systems.

Which region is forecast to grow the fastest?

North America is forecast to register the highest CAGR through 2031, supported by the rollout of new semiconductor and electric vehicle manufacturing fabs specifying GPU-accelerated inspection and assembly lines.

What is driving the surge in predictive maintenance deployments?

Edge GPUs enable real-time processing of high-frequency vibration and acoustic sensor data, providing maintenance teams with a 2-4 week early warning window to prevent unplanned downtime.

Page last updated on: