HR Compliance Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

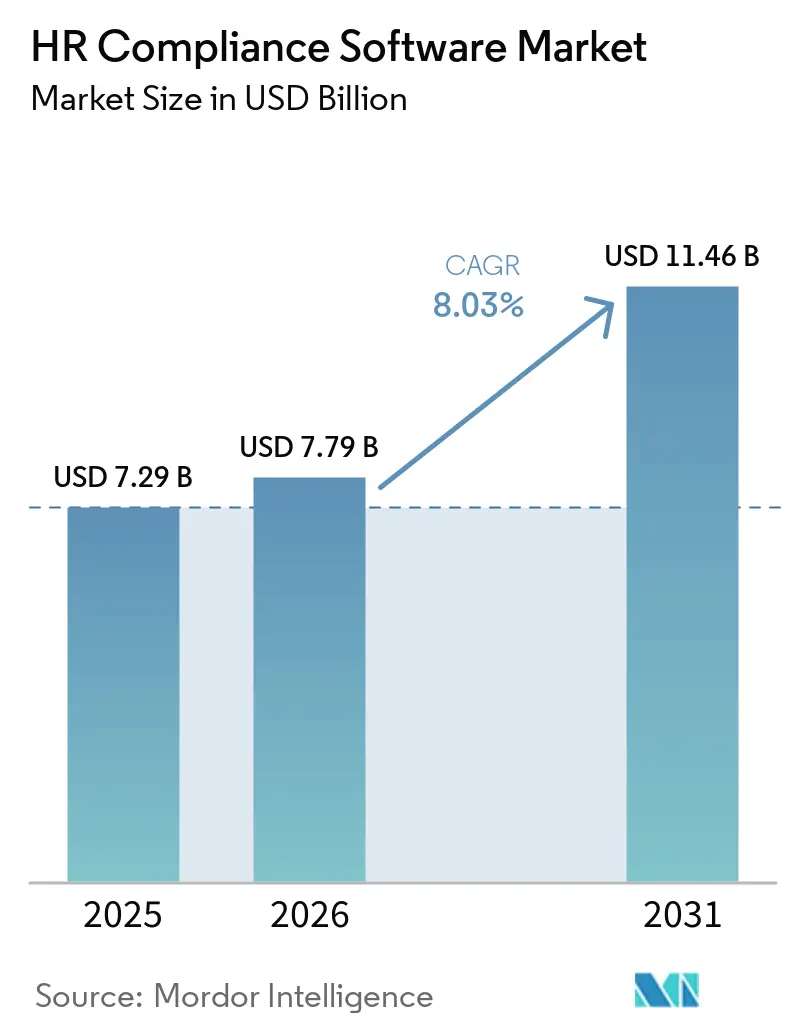

| Market Size (2026) | USD 7.79 Billion |

| Market Size (2031) | USD 11.46 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

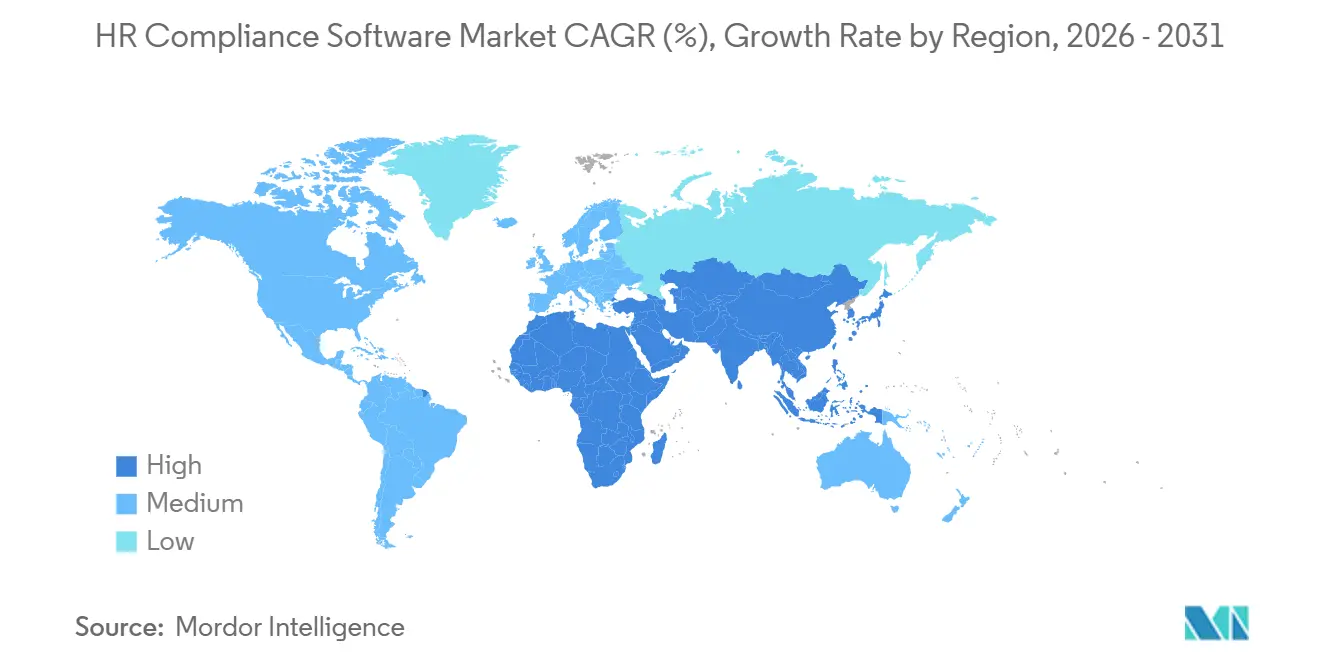

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Compliance Software Market Analysis by Mordor Intelligence

The HR compliance software market size is expected to increase from USD 7.29 billion in 2025 to USD 7.79 billion in 2026 and reach USD 11.46 billion by 2031, growing at a CAGR of 8.03% over 2026-2031. Growth is supported by the steady spread of labor rules across countries, states, and sectors, making manual monitoring less feasible for employers with distributed teams. Procurement demand is also rising because pay reporting, AI governance, and employee documentation rules are now being implemented on tighter timelines. Vendors are responding by adding continuous rule monitoring, payroll anomaly detection, and more configurable reporting layers into broader HR platforms. Regulated sectors continue to shape product priorities, as employers in healthcare, finance, and public administration face greater audit exposure and stricter recordkeeping requirements. The strongest near-term opening remains in the mid-market, where many firms still lack dedicated compliance systems even as legal complexity rises faster than internal HR capacity.

Key Report Takeaways

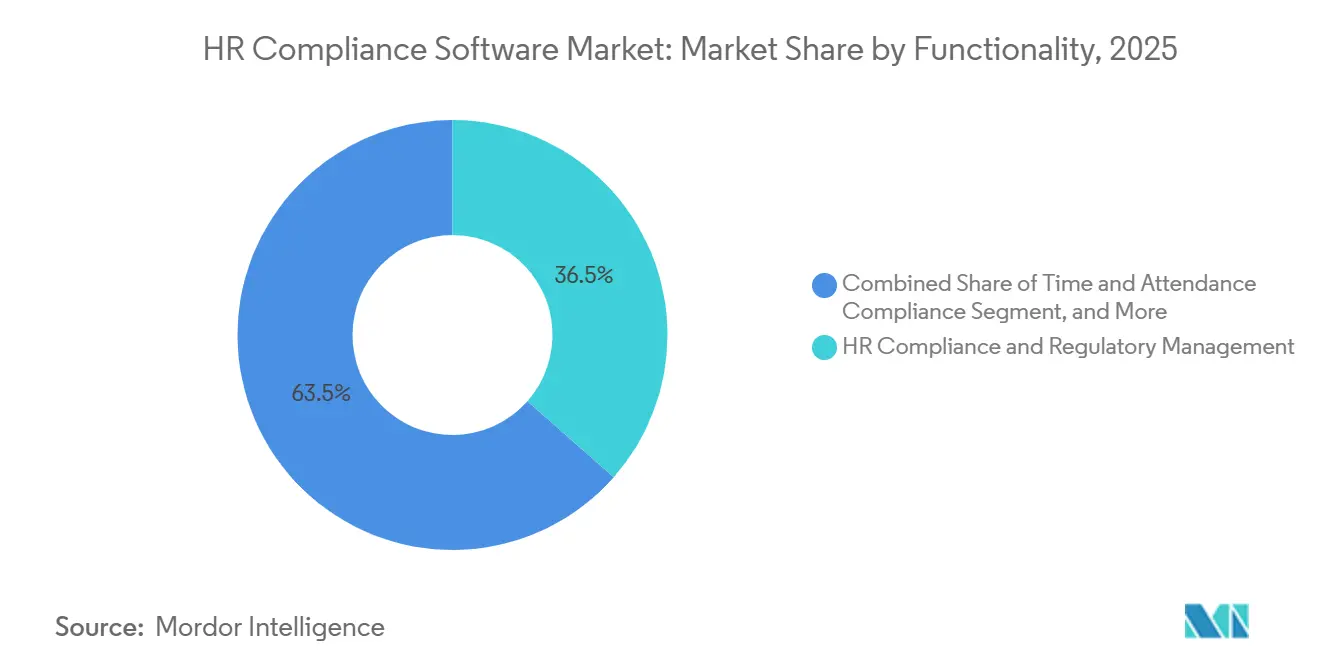

- By functionality, HR Compliance and Regulatory Management held 36.51% of the HR compliance software market share in 2025, while Benefits Administration and Document Compliance is projected to expand at an 8.69% CAGR through 2031.

- By deployment mode, on-premises accounted for 57.29% of revenue in 2025, while cloud-based deployment is projected to grow at a 9.41% CAGR through 2031.

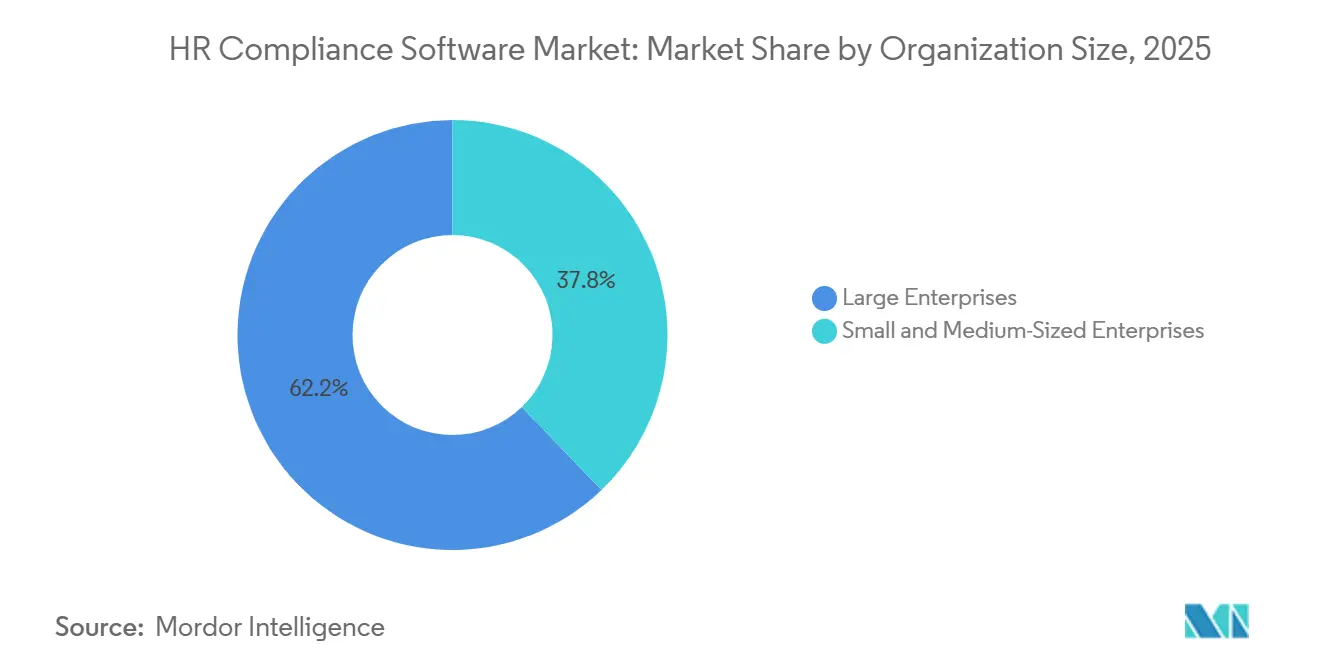

- By organization size, Large Enterprises held 62.18% of revenue in 2025, while SMEs are projected to expand at a 9.72% CAGR through 2031.

- By end-user industry, Information Technology and Telecommunications accounted for 28.49% of revenue in 2025, while Healthcare and Life Sciences are projected to advance at an 8.36% CAGR through 2031.

- By geography, North America held 34.22% of the HR compliance software market share in 2025, while Asia-Pacific is projected to expand at a 9.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Compliance Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Multi-Jurisdiction Labor and Tax Complexity | +2.5% | Global, concentrated impact in North America, EU, and APAC core markets | Short term (≤ 2 years) |

| Accelerating SME Cloud Adoption | +2.0% | Global, APAC and Europe showing highest acceleration | Medium term (2-4 years) |

| AI-Driven Payroll Error Detection | +1.5% | Global, North America and EU at the forefront, with early adoption in APAC | Short term (≤ 2 years) |

| Regulated-Industry HR Digitization | +1.0% | North America and EU core, spill-over to APAC and MEA | Medium term (2-4 years) |

| EU Pay Transparency Readiness Spending | +0.8% | Europe primarily, spill-over to global multinationals with EU operations | Short term (≤ 2 years) |

| AI-In-Employment Governance Requirements | +0.6% | EU and North America, early signals in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Multi-Jurisdiction Labor and Tax Complexity

More than 30 countries raised statutory minimum wage floors in 2026, and the United States had 30 states plus territories with minimums above the federal floor, each with separate effective dates and calculation rules. In the HR compliance software market, the spread of overlapping obligations has made jurisdiction tracking a daily operational task rather than an occasional legal review. Strada Global reported record payroll complexity across major economies in 2025, driven by real-time reporting mandates, changes in worker classification, and revised wage thresholds. As rule sets multiply, the cost of spreadsheets, reminders, and consultant-led monitoring rises faster than the cost of automation. That shift matters because buyers in the HR compliance software market are now treating regulatory management as core operating infrastructure rather than a back-office add-on. Remote found that 51% of HR leaders were actively looking for a new integrated compliance platform in 2025, with multi-country regulatory management cited as the main reason.

Accelerating SME Cloud Adoption

The UK Government found in 2024 that 69% of SME employers were using technology or web-based software to manage business operations.[1]UK Government, “Longitudinal Small Business Survey 2024, SME Employers,” UK Government, gov.uk In the HR compliance software market, broader software comfort shortens the sales cycle for cloud compliance tools because the operational change required is lower than it was a few years ago. Mosey found in 2025 that only 37% of organizations had a dedicated compliance platform, while 55% still used spreadsheets for at least some compliance tracking. That mismatch leaves the HR compliance software market with a large conversion pool among firms that have digitized general operations but not regulatory control. Mosey also reported average annual spending of USD 25,000 on external compliance consultants, legal advisors, and accountants in 2025, a level that often exceeds the cost of a SaaS subscription. ISG found in 2025 that fully integrated HR ecosystems delivered nearly twice the return on investment of siloed systems, which supports platform consolidation among growing employers.

AI-Driven Payroll Error Detection

A 2025 survey reported by KPMG and UKG showed that 69% of payroll leaders expected AI to improve accuracy and compliance outcomes, while 89% already used automated payroll comparison tools to benchmark payroll cycles. In the HR compliance software market, that shift is moving AI from experimental use into a standard control layer within payroll operations. UKG introduced Pro Pay with Workforce AI in May 2026, including anomaly detection that compares current payroll data with up to 5 years of historical records before pay is issued to employees. SAP SuccessFactors also introduced 4 payroll agents in its H1 2026 release to automate alert resolution, rule creation, and payroll data integration. In the HR compliance software market, these tools matter less as labor-saving features and more as documented controls that create cleaner audit trails during investigations. ISG said the average enterprise HR-AI budget reached USD 1.6 million in 2026, which signals that compliance-centered AI investment has moved into production environments.

Regulated-Industry HR Digitization

In the HR compliance software market, healthcare shows most clearly how sector-specific rules directly drive software demand. Virtru reported USD 9.9 million in HIPAA fines in 2024, with average resolution penalties of USD 579,000 per action. HHS published a broad HIPAA Security Rule proposal in January 2025, with a targeted finalization in 2026 and a 180-day compliance window after publication. OCR then imposed a USD 245,000 settlement on an employer-sponsored health plan in May 2026, placing direct pressure on HR and benefits teams rather than only traditional covered entities. New accreditation expectations on staffing, documentation, and competency validation added another recordkeeping layer that manual workflows struggle to support. The same pattern is evident in finance and manufacturing, where sector rules are pushing employers toward systems that connect workforce data, documentation, and audit-readiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border Data Privacy and Sovereignty Complexity | -1.2% | Europe, GDPR and national variants, APAC, data localization laws in Vietnam, China, India | Long term (≥ 4 years) |

| High Switching Costs From Legacy ERP-Linked Payroll | -1.0% | North America and EU, concentrated in large enterprise segment | Medium term (2-4 years) |

| AI Decision Explainability and Record-Retention Burden | -0.7% | EU and North America, spill-over to APAC | Medium term (2-4 years) |

| Rule Change Velocity Outpacing Vendor Release Cycles | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cross-Border Data Privacy and Sovereignty Complexity

The HR compliance software market faces a durable friction point in cross-border data privacy because GDPR interacts with national rules rather than replacing them with a uniform standard. That structure makes multinational deployment more difficult, since vendors must tailor storage, transfer, and retention logic by country. Germany's Federal Labor Court clarified that employers who transfer employee data through cloud-based HR systems without an adequate legal basis may face liability for damages. Vietnam's first AI law took effect in March 2026 and added governance duties for foreign technology vendors alongside existing data localization rules. In the HR compliance software market, these sovereignty requirements increase infrastructure and legal costs, weakening the scale advantage that cloud vendors typically rely on. Employers still need software, but they often need legal advisory support as well because reporting methods, retention windows, and consultation duties continue to vary across jurisdictions.

High Switching Costs From Legacy ERP-Linked Payroll

High switching costs remain a real brake on the HR compliance software market because payroll is often the most deeply embedded system inside large enterprise ERP environments. Strada Global found in mid-2025 that nearly 40% of global businesses still depended on aging on-premises HR systems, including 20% on Microsoft Dynamics and 19% on SAP. Tier2 Systems said replacement costs can run 1.5 to 3 times the annual cost of the new system before productivity loss is considered. ISG reported in November 2025 that 42% of enterprises cited budget limits and 42% cited integration complexity as the leading barriers to HR technology transformation. In the HR compliance software market, risk aversion is intensified by the fact that payroll mistakes create immediate employee, legal, and reputational consequences. The result is a delayed migration pattern, in which employers modernize the reporting and monitoring layers first and defer full core-system replacement until regulatory conditions are more stable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: Core Regulatory Modules Anchor Revenue, Benefits Compliance Accelerates

HR Compliance and Regulatory Management accounted for 36.51% of revenue in 2025, giving this module the largest share of the HR compliance software market among functionality groups. Its lead came from its role as the base layer for employers entering new jurisdictions, since rule libraries, filing logic, and update monitoring are usually in place before adjacent modules add value. The HR compliance software market also saw steady demand for Time and Attendance Compliance as governments pushed for tamper-resistant and more accessible working-time records. Spain advanced a digital working-time registration decree in 2026 that required interoperable records for labor inspectors. Germany will require fully electronic wage documentation under the Beitragsverfahrensverordnung by January 2027, which keeps attendance records and payroll evidence closely linked.

Worker Classification and Employment Eligibility gained urgency in the HR compliance software industry during 2026 after the U.S. Department of Labor proposed rescinding the prior independent contractor rule and replacing it with a revised economic reality test. That change pushed organizations with large contractor pools to review status, documentation, and audit exposure across multiple business units. Compliance Training and Policy Management also benefited from faster policy generation and attorney-reviewed template models that lowered update friction without removing legal oversight. Benefits Administration and Document Compliance is projected to grow at an 8.69% CAGR through 2031, and this segment of the HR compliance software market is being driven by the need to report pay components and benefits in more disaggregated forms. KPMG noted that the EU Pay Transparency Directive requires employers to separate base pay, variable pay, and benefits in reporting, while member states may still apply stricter national rules that favor configurable systems over fixed templates.

By Deployment Mode: On-Premises Leads in Value as Cloud Accelerates in Pace

On-premises deployment accounted for 57.29% of revenue in 2025, indicating that the HR compliance software market still has a large installed base tied to legacy payroll and ERP systems. This position reflects data residency demands, audit-trail continuity needs, and integration constraints rather than a lack of interest in cloud models. Strada Global said in 2025 that nearly 40% of global businesses remained on legacy on-premises platforms, with integration difficulty and budget pressure slowing migration. In practice, many employers are using hybrid models that keep sensitive payroll records in-house while shifting rule monitoring and reporting workflows into vendor-managed environments. That middle path lets buyers modernize the HR compliance software market architecture they depend on without taking full cutover risk during active regulatory change.

Cloud-based deployment is projected to grow at a 9.41% CAGR through 2031, making it the fastest-moving deployment model in the HR compliance software market. ISG found in 2025 that SaaS or hybrid cloud architectures formed the HR technology core for 69% of organizations globally. That matters because compliance software depends on frequent content and rules updates, which are easier to deliver through centralized release cycles than through enterprise-managed patching. SMEs are pushing much of this growth because they often lack sunk infrastructure costs and increasingly expect compliance automation as part of bundled HR software rather than as a separate purchase. Regional privacy rules and AI documentation duties still raise the bar for cloud vendors, but providers that can localize data handling are turning compliance design into a competitive advantage.

By Organization Size: Large Enterprises Anchor Spend, SMEs Define Growth Trajectory

Large Enterprises accounted for 62.18% of revenue in 2025, giving them the largest share of the HR compliance software market by organization size. Their spending weight comes from multi-country payroll complexity, broader audit exposure, and the budget authority needed for enterprise-wide platform rollouts. The EU Pay Transparency Directive adds more immediate pressure on larger employers, as firms with 250 or more employees must report annually from 2027, while those with 150 to 249 employees will report every 3 years from the same year. That staging accelerated procurement across large European employers in 2025 and kept implementation work active through 2026. In the HR compliance software industry, large employers also favor integrated platforms that connect regulatory management, workforce documents, and audit logs in a single workflow.

SMEs are projected to expand at a 9.72% CAGR through 2031, which makes them the fastest-growing buyer group in the HR compliance software market. Mosey found in 2025 that only 37% of organizations had a dedicated compliance platform, while 33% had incurred compliance penalties averaging USD 16,000 in the prior year. That mix of low current penetration and visible cost pain creates a strong case for cloud-native vendors that can offer simpler onboarding and lower upfront commitment. Employment Hero passed AUD 300 million in annual recurring revenue, USD 192 million, in October 2025 and served more than 300,000 SMEs globally, showing the scale that specialized SME-focused platforms can reach. Personio also reported profitability in Q1 2026 while serving 16,000 organizations across Europe, which supports the view that the mid-market HR compliance software market can scale without relying only on very large enterprise deals.

By End-User Industry: IT and Telecom Lead by Share, Healthcare Drives Fastest Expansion

Information Technology and Telecommunications held 28.49% of revenue in 2025, leading the HR compliance software market across end-user industries. The sector comprises a dense mix of contractors, remote workers, and cross-border employees, increasing the number of classification and location-specific rules employers must track. The EU Platform Work Directive must be transposed by December 2026 and adds transparency requirements for algorithmic management and employment presumption rules that directly affect tech employers with platform-based labor models. Banking, Financial Services, and Insurance also maintained strong demand because employee monitoring, record retention, and internal control needs overlap with broader financial compliance obligations. This helps explain why the HR compliance software market continues to see strong purchase activity from both digital-first and highly regulated employers.

Healthcare and Life Sciences is projected to grow at an 8.36% CAGR through 2031, and this segment is playing an increasingly important role in the HR compliance software market due to greater documentation pressure. HHS proposed a HIPAA Security Rule overhaul in January 2025 that would require encryption of electronic protected health information, multi-factor authentication for all ePHI access, and annual internal HIPAA compliance audits.[2]United States Department of Health and Human Services, “HIPAA Security Rule 2025 Notice of Proposed Rulemaking,” HHS, hhs.gov OCR also reached a USD 245,000 settlement with an employer-sponsored health plan in May 2026, demonstrating that HR and benefits teams fall within the compliance perimeter when sensitive employee health data is involved. Manufacturing, Retail and E-commerce, and Government and Public Sector remain meaningful installed-base markets because they face steady demands around workforce documentation, scheduling, and public reporting. Government procurement rules are especially important because they can make digital recordkeeping and pay equity reporting formal purchasing requirements rather than voluntary improvements.

Geography Analysis

North America accounted for 34.22% of revenue in 2025, making it the largest geography in the HR compliance software market. The United States remains the central driver because employment law changes more than 600 times each year at the state level, making manual monitoring unsustainable for employers with multi-state workforces. California, New York, Colorado, and Connecticut have enacted some of the most stringent rules on wages, leave, and AI use in employment, which keeps the compliance scope wide even within a single country. Paychex strengthened its regional position when it acquired SixFifty in July 2025 and combined employment law automation with its payroll and HR services stack. The U.S. Department of Labor then proposed a new independent contractor rule in February 2026, prompting many employers to review classification controls and sparking renewed interest in HR compliance software.

Europe remained the second-largest regional market for HR compliance software, with the United Kingdom, Germany, and France as major revenue drivers. Employers with 150 or more workers must submit their first gender pay gap reports by June 7, 2027, using 2026 workforce data under the EU Pay Transparency Directive, which has created one of the clearest spending deadlines in the current cycle. National layers matter as much as the EU baseline because Germany's labor court tightened rules on HR data transfers and Spain advanced digital working-time registration requirements. SD Worx responded in April 2026 by launching Legal Watch across several European countries, turning regulatory monitoring into a commercial product inside the regional HR compliance software market.

Asia-Pacific is projected to expand at a 9.02% CAGR through 2031, making it the fastest-growing regional segment in the HR compliance software market. Singapore moved workplace fairness from guidance to enforceable law in 2025, South Korea opened a tripartite process on AI use in workplaces in March 2026, and Vietnam enacted its first AI law, effective from March 2026. ADP extended Lyric HCM into Australia and New Zealand in December 2025 with design features tied to Fair Work, Single Touch Payroll, and Inland Revenue requirements, showing how vendors are localizing product fit for the region.[3]ADP, “ADP Unveils Lyric HCM in Australia and New Zealand,” ADP Media Center, mediacenter.adp.com South America, the Middle East, and Africa remain smaller parts of the HR compliance software market, but labor digitization in Brazil, wage protection in the UAE, and Saudization in Saudi Arabia continue to create targeted demand.

Competitive Landscape

The HR compliance software market remained moderately fragmented in 2026, with no single vendor controlling breadth of functionality, geographic reach, or regulatory depth. Competition is split between global unified platforms, regional payroll and HR specialists, and focused compliance automation providers that sell deeper jurisdictional intelligence. In March 2026, Deel unified hiring, compensation, global payroll, and workforce planning into a single product structure, underscoring the growing importance of full-suite positioning in the HR compliance software market. Mitratech expanded its AI Governance Suite in November 2025 to align with the EU AI Act, ISO 42001, and the NIST AI Risk Management Framework, thereby widening its relevance beyond classic legal workflow tools. Paychex's July 2025 acquisition of SixFifty and KKR's February 2025 investment in Employment Hero show that capital continues to flow toward vendors that combine compliance depth with scalable distribution.

AI-based regulatory monitoring is becoming the clearest technology differentiator in the HR compliance software market, as buyers want current rules, explainable workflows, and evidence trails within the same system. SD Worx launched Legal Watch in April 2026 to track legal changes across European jurisdictions and translate them into HR and payroll guidance. SAP SuccessFactors added autonomous payroll agents in its H1 2026 release, while Neeyamo launched ARIA in September 2025 for global payroll monitoring, anomaly detection, and compliance alerts.[4]SAP, “1H2026 Release, A Journey to Autonomous Payroll with SAP SuccessFactors,” SAP Community, community.sap.com These moves show that vendors are competing less on basic record storage and more on how quickly they can turn regulatory changes into usable actions in the HR compliance software market.

The strongest open space remains the mid-market, especially firms with 100 to 500 employees that operate across several countries but lack the budget or implementation capacity for large enterprise suites. In this buyer group, ERP-based tools often lack the depth of legal intelligence that specialists offer, while premium enterprise platforms can be too expensive or too complex to justify. That leaves room in the HR compliance software market for vendors that can offer jurisdiction-specific automation, faster deployment, and continuous updates at accessible subscription levels. As a result, competitive advantage is increasingly tied to 3 things: credible legal content, adaptable workflows, and a delivery model that does not require major internal IT projects.

HR Compliance Software Industry Leaders

Deel Inc.

Remote Technology Services, Inc.

Papaya Global Ltd.

Atlas Technology Solutions, Inc.

Oyster HR, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UKG unveiled agentic-powered UKG Pro Pay with Workforce AI at Payroll Congress 2026, featuring Payroll Anomaly Detection AI that compares current payroll data against up to 5 years of historical records and a Payroll Auditing AI for natural-language compliance queries. The launch positions UKG to reduce payroll processing timelines from days to hours while mitigating multi-jurisdiction compliance risk for frontline and hourly-heavy workforces.

- May 2026: Deel launched Akai, an agentic workflow platform designed to automate government filings, bank payout submissions, compliance reports, and cross-border payment workflows without requiring API development or IT integration projects. Akai is deployed internally across Deel's Finance, Tax, Treasury, Benefits, and HR operations and is now available externally to enterprise customers.

- April 2026: Papaya Global announced a strategic alliance with Tech Mahindra to modernize global workforce operations and enable compliant, scalable payments across employee and contingent workforce models across more than 180 countries.

- April 2026: SD Worx launched Legal Watch, an AI-powered regulatory monitoring platform built with AI specialist Faktion, that continuously tracks legal changes across multiple European jurisdictions and converts updates into actionable HR and payroll compliance guidance. Initial deployment covered Germany, Luxembourg, Spain, Sweden, and the Netherlands.

Global HR Compliance Software Market Report Scope

The HR Compliance Software Market comprises digital solutions that enable organizations to manage and ensure compliance with labor laws, employment regulations, workplace policies, and corporate governance requirements. These platforms provide capabilities such as compliance tracking, policy management, audit workflows, and regulatory reporting. They support organizations in minimizing legal risks and maintaining compliance across diverse workforce environments. The market focuses on automating and standardizing HR compliance processes.

The HR Compliance Software Market Report is Segmented by Functionality (HR Compliance and Regulatory Management, Time and Attendance Compliance, Benefits Administration and Document Compliance, Worker Classification and Employment Eligibility, Compliance Training and Policy Management, and Other Functionalities), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), End-User Industry (Banking, Financial Services and Insurance, Healthcare and Life Sciences, Information Technology and Telecommunications, Manufacturing, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HR Compliance and Regulatory Management |

| Time and Attendance Compliance |

| Benefits Administration and Document Compliance |

| Worker Classification and Employment Eligibility |

| Compliance Training and Policy Management |

| Other Functionalities |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| Information Technology and Telecommunications |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Functionality | HR Compliance and Regulatory Management | |

| Time and Attendance Compliance | ||

| Benefits Administration and Document Compliance | ||

| Worker Classification and Employment Eligibility | ||

| Compliance Training and Policy Management | ||

| Other Functionalities | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Small and Medium-Sized Enterprises | |

| Large Enterprises | ||

| By End-User Industry | Banking, Financial Services and Insurance | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecommunications | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the HR compliance software market?

The HR compliance software market generated USD 7.79 billion in 2026 and is projected to reach USD 11.46 billion by 2031, growing at an 8.03% CAGR over 2026-2031.

Which functionality segment holds the largest revenue base?

HR Compliance and Regulatory Management led functionality revenue with a 36.51% share in 2025 because it acts as the base layer for jurisdiction tracking, filing logic, and rule updates.

Which deployment model is growing the fastest?

Cloud-based deployment is projected to grow at a 9.41% CAGR through 2031 as employers prefer vendor-managed updates for fast-changing compliance rules.

Why are SMEs becoming a major growth area?

SMEs are projected to grow at a 9.72% CAGR through 2031 because many still lack dedicated compliance systems, while penalties and external advisory costs are creating a stronger software business case.

What is driving the fastest regional expansion in Asia-Pacific?

Asia-Pacific is projected to grow at a 9.02% CAGR through 2031 as governments across the region increase digital payroll reporting, workplace fairness requirements, and AI-related workplace governance rules.

Why is healthcare becoming a stronger buyer group?

Healthcare and Life Sciences is projected to grow at an 8.36% CAGR through 2031 because HIPAA-related controls, employer-sponsored health plan scrutiny, and tighter documentation requirements are increasing pressure on HR and benefits teams.

Page last updated on: