HR Transformation Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.12 Billion |

| Market Size (2031) | USD 36.29 Billion |

| Growth Rate (2026 - 2031) | 9.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

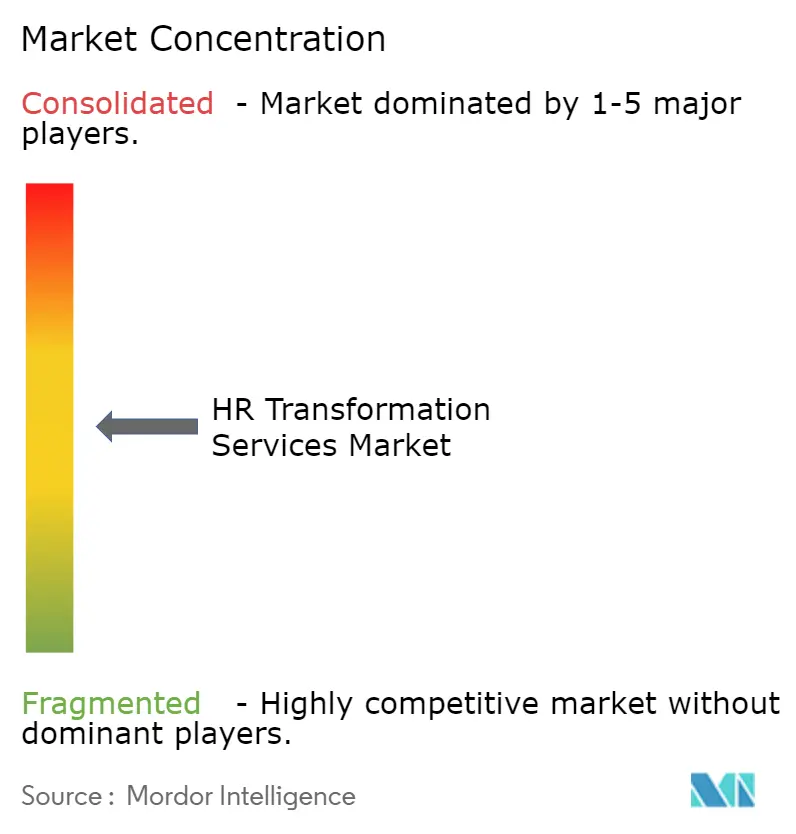

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Transformation Services Market Analysis by Mordor Intelligence

The HR transformation services market size is expected to increase from USD 21.37 billion in 2025 to USD 23.12 billion in 2026 and reach USD 36.29 billion by 2031, growing at a CAGR of 9.44% over 2026-2031. Growth is being sustained by a clear shift in how enterprises view HR, with the function moving away from an administrative support role and toward an AI-connected operating layer that shapes productivity, compliance, and workforce decisions. This is increasing demand for advisory, implementation, and change support because many organizations are now redesigning workflows, roles, and governance at the same time that they upgrade platforms. The spread of distributed workforces across countries is also making policy standardization, payroll coordination, and employee data governance more difficult for in-house teams to manage alone. A second wave of spending is also taking shape as companies that completed early cloud HCM deployments return to service providers to rebuild older configurations around newer delivery models. Even with that momentum, long change cycles inside legacy HR structures and the difficulty of proving near-term returns continue to slow buying decisions in part of the market.

Key Report Takeaways

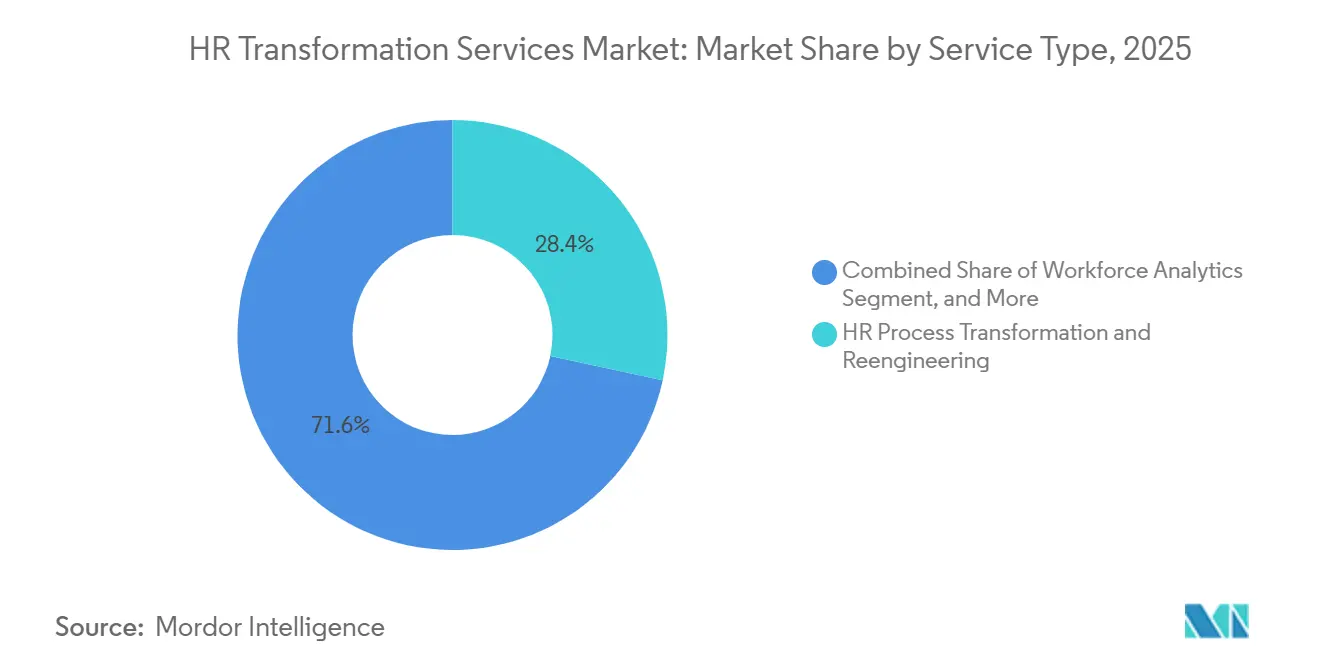

- By service type, HR Process Transformation and Reengineering held 28.37% of the HR transformation services market share in 2025, while Workforce Analytics and HR Data Transformation are projected to expand at an 11.62% CAGR through 2031.

- By enterprise size, large enterprises held 62.41% share in 2025, while Small and Medium Enterprises are expected to expand at a 12.84% CAGR through 2031.

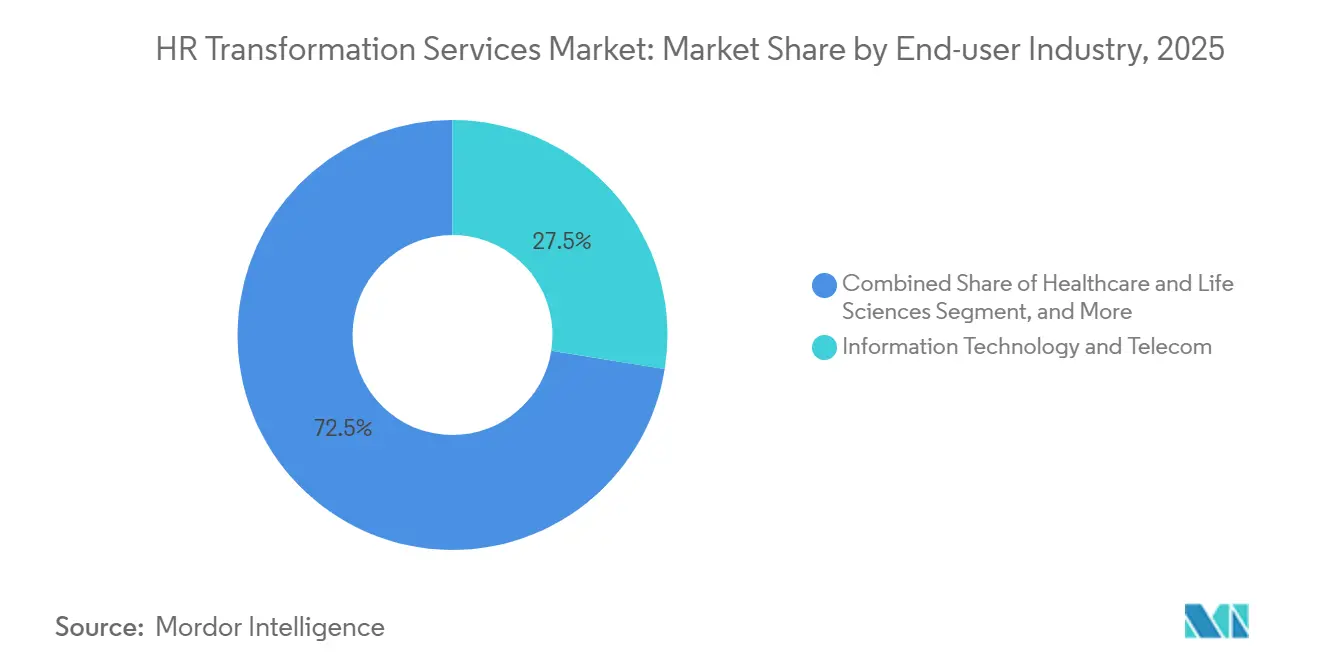

- By end-user industry, Information Technology and Telecom accounted for 27.53% share in 2025, while Healthcare and Life Sciences are projected to grow at a 13.47% CAGR through 2031.

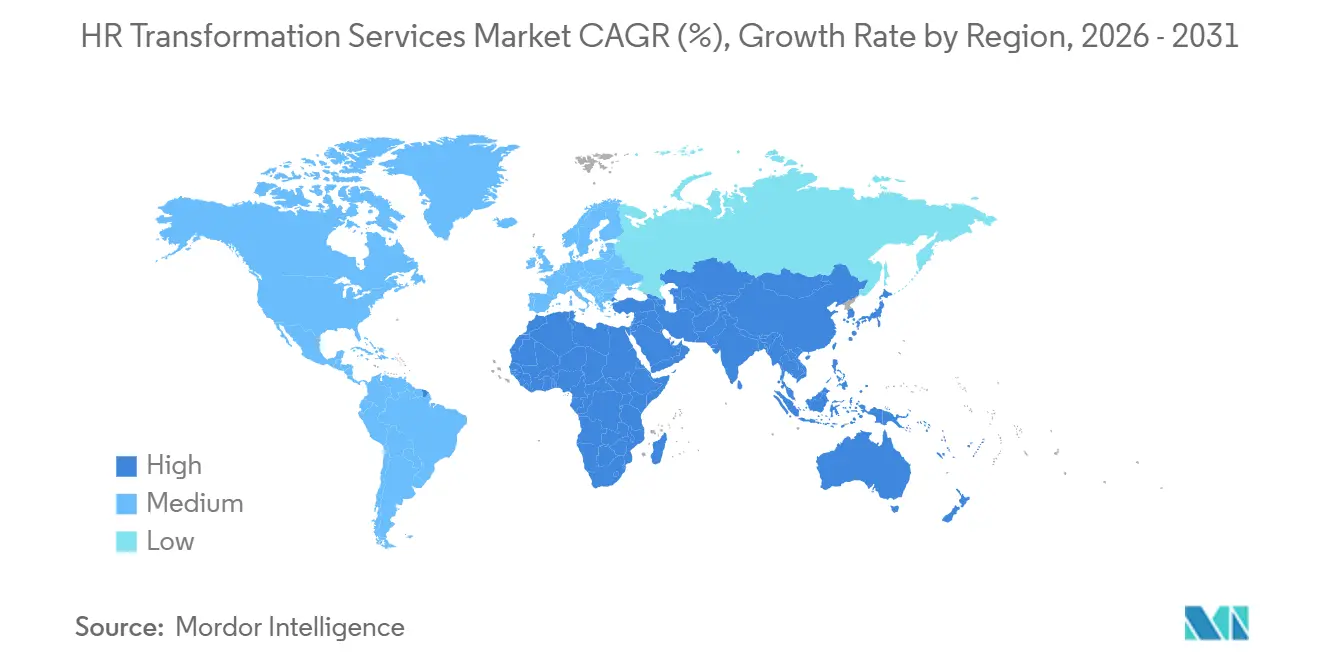

- By geography, North America held 38.29% share of the HR transformation services market in 2025, while Asia-Pacific is projected to advance at a 14.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Transformation Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Enterprise Demand for End-To-End HR Operating Model Redesign | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Cloud-Based HR Transformation Roadmaps | +2.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Data-Driven Workforce Planning and HR Analytics | +1.5% | Global, early gains in North America, Singapore, and Australia | Medium term (2-4 years) |

| Increased Pressure to Improve Employee Experience and Workforce Agility | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Need to Standardize Global HR Policies Across Distributed Workforces | +1.0% | Global, spill-over to Middle East and South America | Long term (≥ 4 years) |

| Accelerating Compliance Needs for Multi-Country Labor and Privacy Regulations | +0.9% | Europe, Asia-Pacific, emerging in South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Enterprise Demand for End-To-End HR Operating Model Redesign

End-to-end redesign has moved to the front of spending plans in the HR transformation services market because enterprises now see that new tools alone do not change outcomes. Many organizations still maintain HR structures built for control, approvals, and administrative consistency rather than for speed, analytics, and AI-supported decision-making. That is pushing clients toward programs that cover process ownership, service delivery layers, workflow automation, decision rights, and manager self-service within a single scope rather than in isolated projects. Recent product developments show that AI capabilities are being embedded across the HR stack, making redesign work more urgent because value depends on how workflows are configured and governed within the organization.[1]SAP SE, “SAP SuccessFactors 1H 2026 Release, Strengthening Connection Across HR and the Business,” SAP News Center, news.sap.com A similar direction emerged in 2026 with the introduction of specialized AI agents into HR workflows, which further raises the need for enterprises to rethink approval logic, escalation rules, and role definitions before automation can work reliably at scale. As a result, the HR transformation services market is seeing stronger demand for full architecture redesign than for isolated technology refresh work.

Rising Adoption of Cloud-Based HR Transformation Roadmaps

Cloud adoption continues to support the HR transformation services market, as many organizations now treat cloud HCM as the foundation for payroll, talent, onboarding, scheduling, and workforce planning. The first wave of deployments often relied on standard configurations that mirrored older HR processes, so a growing number of clients are returning to providers for optimization, integration, and governance work. More than 140 million users across 13,000 customers were served by a major cloud HCM platform, with 825 new go-lives completed in the first half of 2026, indicating a large installed base that still requires ongoing redesign and adoption services. Recent platform releases also strengthened suite-wide AI integration, unified workflows, and skills governance, extending the service tail well beyond initial platform deployment.[2]SAP SE, “SAP SuccessFactors Innovations, New Era of Autonomous HCM,” SAP News Center, news.sap.com A broader move toward autonomous enterprise capabilities further connected HR workflows such as payroll, recruiting, onboarding, and workforce planning with embedded assistants that still require configuration and change support. This cloud-then-optimize cycle is creating a durable pipeline for the HR transformation services market in both mature and high-growth regions.

Expansion of Data-Driven Workforce Planning And HR Analytics

Data-led workforce planning is expanding the HR transformation services market because executive teams want people decisions to connect more directly with business and financial outcomes. In 2026, 62% of C-suite executives reported dissatisfaction with how well people data connected to business performance, indicating that platform investment alone has not closed the insight gap. In many organizations, employee data still sits across disconnected payroll, talent, scheduling, learning, and finance systems, which limits the quality of planning and makes analytics programs hard to scale. That creates demand for services that combine data model redesign, integration work, governance design, dashboard creation, and manager adoption support in a single roadmap. Recent product developments have have also linked workforce planning more closely to HR, business, and financial needs, reinforcing that analytics is moving into the core HCM architecture rather than remaining a reporting layer at the edge. This is one reason the HR transformation services market is seeing strong momentum in workforce analytics and HR data transformation work.

Increased Pressure to Improve Employee Experience and Workforce Agility

Pressure to improve the employee experience now supports the HR transformation services market, as enterprises seek to streamline workforce processes without adding large administrative teams. Experience design is no longer limited to branding or engagement surveys, and it now affects onboarding speed, internal mobility, workforce scheduling, learning access, and manager decision quality. Recent product roadmaps have placed greater emphasis on unified workflow experiences and AI-assisted interactions, showing that employee and manager touchpoints are becoming a core part of transformation design rather than a side feature. In healthcare, organizations have been expanding upskilling efforts, using technology to reduce administrative burden, and redesigning care delivery models, which reflects the direct link between workforce agility and service delivery needs.[3]American Hospital Association, “2026 Health Care Workforce Scan,” American Hospital Association, aha.org The introduction of AI-powered HR agents in 2026 also points to a model in which routine decisions and coordination tasks move faster across recruiting, onboarding, and workforce actions, but only when the underlying experience is redesigned with clear rules and handoffs. These pressures are widening the role of the HR transformation services market across workflow design, adoption, and operating model execution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Change-Management Burden Across Legacy HR Organizations | -0.7% | Global, most acute in large-enterprise-heavy North America and Europe | Medium term (2-4 years) |

| Difficulty Quantifying Near-Term ROI From Transformation Programs | -0.5% | Global, affecting mid-size enterprises across all regions | Short term (≤ 2 years) |

| Talent Shortage In HR Process Redesign And Change Advisory Skills | -0.4% | Global, most severe in emerging Asia-Pacific and South American markets | Long term (≥ 4 years) |

| Fragmented Legacy HR Systems And Data Migration Complexity | -0.4% | Global, most pronounced in legacy-heavy industrial sectors in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Change-Management Burden Across Legacy HR Organizations

The HR transformation services market still faces resistance from legacy HR teams because many programs change roles, approval paths, service boundaries, and accountability models simultaneously. That makes transformation difficult even when leadership agrees with the need for digital tools and AI-enabled workflows. A 2026 digitalization survey found that time constraints and implementation complexity remained major barriers for enterprises, which aligns closely with the execution burden that slows HR redesign programs. The issue is often greater in multinational organizations because policy harmonization, payroll alignment, and employee data governance must move in step across jurisdictions. A 2026 engagement that modernized an HR landscape across Europe and the United States using multiple cloud HCM modules illustrates how broad the operating and adoption burden can become. Because of this, the HR transformation services market can see long sales cycles and extended delivery timelines even when the strategic need is already clear.[4]Zalaris, “Global Energy Leader Accelerates HR Transformation with Zalaris and SAP SuccessFactors,” Zalaris, zalaris.com

Difficulty Quantifying Near-Term ROI from Transformation Programs

Difficulty proving near-term returns remains a practical restraint on the HR transformation services market, as many benefits unfold over several stages rather than in a single immediate savings figure. Value often comes through lower administrative effort, faster staffing decisions, better workforce planning, stronger compliance, and more usable employee data, and those gains are harder to isolate than direct procurement or infrastructure savings. Client teams also need baseline metrics before they can tie transformation work to outcomes such as time-to-hire, retention, payroll accuracy, or manager productivity, and many organizations do not have those baselines in place at the start. Early AI deployment prototypes reported in 2025 showed the potential for more than 90% improvement in employee productivity, but the same example also illustrates why buyers want stronger proof before broad rollout, since pilot outcomes still need to be translated into enterprise-wide business cases. Mid-sized companies feel this challenge more sharply because they often have fewer data science, finance, and program management resources to track benefits over time. This keeps part of the HR transformation services market in a slower approval cycle, especially when projects are framed as capability building rather than near-term cost reduction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Process Redesign Commands The Market And Analytics Services Scale Fastest

HR Process Transformation and Reengineering accounted for 28.37% of the HR transformation services market in 2025, underscoring that workflow redesign remains central to enterprise buying decisions. This leadership reflects a clear spending sequence, as many clients want to fix process logic, service layers, and handoffs before investing more deeply in automation and advanced analytics. Organizations that move cloud HCM onto older workflows often see only limited gains, so redesign work continues to attract the largest budgets inside the HR transformation services market. HR Technology Transformation Services also plays a major role, as many enterprises are now consolidating platforms, improving integrations, and refining configurations following earlier migration programs.

Workforce Analytics and HR Data Transformation is projected to expand at an 11.62% CAGR through 2031, making it the fastest-growing service category in the HR transformation services market. Growth here is building in phases because clients first need to unify data sources, then improve governance, then create usable planning models, and then embed those insights into manager workflows. Recent product developments support this pattern by linking workforce planning more closely with business and financial needs, which increases the need for providers that can bridge technology, data, and operating design. HR Shared Services and Outsourcing Transformation continues to serve large organizations that are standardizing delivery through shared services centers, often after an initial redesign program. HR Operating Model and Organizational Design remains smaller by current spend, but it is gaining weight as enterprise buyers look for a stronger blueprint before they scale AI-enabled HR workflows. The HR transformation services industry is therefore shifting toward a mix of foundational redesign and data-centered modernization rather than relying solely on one-time platform implementation.

By Enterprise Size: Large Enterprises Anchor Revenue While SMEs Gain Momentum

Large enterprises held 62.41% of the HR transformation services market share in 2025, reflecting the scale and complexity of global HR environments. These organizations often run multi-country payroll structures, layered approval systems, and multiple core platforms simultaneously, which create longer, more complex contracts for strategy, integration, compliance design, and change execution. Their buying behavior continues to anchor the HR transformation services market, as transformation work in this segment is rarely limited to a single process or geography. Enterprise mandates also tend to continue after initial deployment because new AI features, governance requirements, and integration needs keep arriving across each release cycle.

Small and Medium Enterprises are projected to grow at a 12.84% CAGR through 2031, making them the fastest-growing buyer group in the HR transformation services market. Growth in this segment is being supported by more modular delivery models, pre-configured cloud solutions, and shorter implementation paths than were available earlier. A pre-packaged payroll solution launched in 2026 for small and mid-sized organizations in the United Kingdom was built around a faster deployment approach rather than a large bespoke program. That type of packaging lowers the resource threshold for clients who want formal HR transformation but cannot afford or sustain the cost or duration of enterprise-style engagements. As service providers standardize templates and delivery playbooks, the HR transformation services market is becoming more accessible to growth-stage firms. This should gradually narrow the spending gap between large companies and smaller buyers over the forecast period.

By End-User Industry: IT And Telecom Leads While Healthcare And Life Sciences Accelerates

Information Technology and Telecom accounted for 27.53% of the 2025 HR transformation services market, giving it the largest vertical position. The sector's weight stems from early adoption of HR technology, large pools of hybrid and digital labor, and the need to reshape roles as AI reshapes work patterns across product, service, and support functions. These companies also tend to have stronger internal data foundations, which can shorten the early phase of analytics-related transformation programs. As a result, the HR transformation services market has continued to draw strong demand from technology employers seeking faster internal mobility, greater skills visibility, and stronger workforce planning discipline.

Healthcare and Life Sciences is projected to grow at a 13.47% CAGR through 2031, making it the fastest-growing vertical in the HR transformation services market. Hospitals and health systems have been expanding upskilling programs, using technology to reduce administrative burden, and redesigning care delivery models, which directly support demand for HR operating changes and workforce process redesign. This vertical also faces persistent integration work after acquisitions and ongoing pressure to align workforce capabilities with new care delivery models. Those needs raise demand for advisory and implementation services that can standardize job architecture, learning pathways, governance, and workforce deployment rules. Other verticals, such as BFSI, retail, manufacturing, and government, remain important contributors to the HR transformation services market because each faces a mix of compliance, service redesign, and digital workforce pressures. The healthcare and life sciences segment is moving faster because workforce availability, skills alignment, and operational redesign have become tightly linked.

Geography Analysis

North America held 38.29% of the HR transformation services market share in 2025, making it the largest regional contributor. The region benefits from a high concentration of large enterprise buyers, mature consulting and IT services capacity, and wide adoption of cloud HCM across corporate HR functions. The United States remains the core demand engine because large employers are trying to align AI ambitions with practical redesign of HR workflows, data models, and governance. Canada adds volume through regional alignment with multinational programs, while Mexico is gaining relevance as nearshore delivery and policy coordination across North American operating zones become more common. These factors keep the HR transformation services market active in North America across both initial redesign mandates and follow-on optimization work.

Europe continues to generate steady demand for HR transformation services as compliance obligations and process standardization needs remain high across multinational employers. The region also carries a significant burden from older HR structures and complex implementation environments, and Germany's 2026 DIHK survey showed that time constraints and implementation complexity were still major barriers to business digitalization. That friction supports demand for providers that can combine redesign, governance, and change management rather than technology deployment alone. South America is still smaller in scale, but Brazil and other multinational operating hubs are starting to generate incremental work tied to enterprise digitalization and local labor compliance requirements.

Asia-Pacific is projected to expand at a 14.26% CAGR through 2031, making it the fastest-growing region in the HR transformation services market. India is a major driver because workforce formalization, digital public infrastructure, and growth in global capability centers are creating demand for shared services redesign, payroll standardization, and analytics support. The Conference Board reported in 2026 that CEOs across Asia-Pacific were reassessing growth, risk, and operating models, which elevated HR transformation from an operational issue to a broader business agenda. Japan, China, South Korea, and ASEAN markets are also building multi-year pipelines as companies modernize workforce models and seek better cross-border coordination. The Middle East is growing through national workforce development programs in Saudi Arabia and the UAE, while Africa remains an earlier-stage opportunity, led by formalization and technology-sector growth in markets such as South Africa and Nigeria.

Competitive Landscape

The HR transformation services market shows moderate concentration at the top and a broader, fragmented field below. Large advisory firms still hold strong positions in operating model design, organization structure, and change programs, while tier-one IT services companies compete more directly on integration scale, platform depth, and managed delivery. This creates a layered competitive structure rather than a winner-takes-all pattern across the whole HR transformation services market. Premium global accounts tend to favor firms with cross-border delivery capacity and deep certifications in SAP, Oracle, and Workday environments. Mid-market and specialist opportunities remain more open because many buyers still need focused help in payroll redesign, workforce analytics, or multi-country shared services transformation.

A major competitive trend in the HR transformation services market is the convergence of advisory and engineering capability. Service providers that used to focus mainly on strategy are building depth in implementation, while technology-led firms are moving up into operating design and transformation governance. A global payroll modernization program completed in 2026 by migrating operations to a cloud-based enterprise platform illustrates how large providers are using platform and delivery scale as a differentiator. The introduction of agentic HR applications in 2026 also shows how platform vendors are moving further into transformation-grade functionality by embedding reasoning-based AI agents directly into enterprise HCM workflows. That increases pressure on service firms to prove value beyond configuration, especially in governance, workflow redesign, and adoption.

Strategic moves in 2026 also show how firms are trying to widen their relevance inside the HR transformation services market. The expansion of a compensation benchmarking database with AI-specific job family classifications helps clients connect workforce strategy with changing skills demand. A global capability center innovation program was launched in 2026 to support innovation creation for multinational organizations and to strengthen the advisory presence in high-growth regions. Expanded AI collaborations for employee benefits administration also demonstrate how outsourcing specialists are using AI partnerships to strengthen operating leverage and service experience. Overall, the HR transformation services market remains active and competitive, with no sign that any provider model will dominate every segment.

HR Transformation Services Industry Leaders

Deloitte Touche Tohmatsu Limited

PricewaterhouseCoopers International Limited

Mercer LLC

Aon plc

Willis Towers Watson Public Limited Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP SE announced that Tata Consultancy Services successfully modernized its global payroll operations by transitioning to SAP S/4HANA Cloud on AWS, consolidating multi-country payroll operations into a unified cloud-based environment. The program aimed to reduce architectural fragmentation, improve cross-country operational visibility, and build a scalable digital foundation for AI-driven workforce management.

- May 2026: At SAP Sapphire in Orlando, SAP unveiled its Autonomous Enterprise vision, introducing new Joule Assistants within SAP SuccessFactors designed to automate and coordinate end-to-end HR workflows including payroll, recruiting, onboarding, and workforce planning. SAP announced plans for 15 new HR-focused Joule Assistants to be released through the remainder of 2026.

- April 2026: Oracle introduced Fusion Agentic Applications for HR, embedding 8 outcome-driven, reasoning-based AI agents directly into Oracle Fusion Cloud HCM. The applications are designed to execute decisions autonomously within business processes by accessing unified enterprise data, workflow policies, approval hierarchies, and transactional context.

- April 2026: SAP released the SAP SuccessFactors 1H 2026 product update, focusing on suite-wide AI integration, unified workflow experiences, compliance-grade process architecture, and a centralized talent intelligence hub providing enhanced skills governance across all HR modules.

Global HR Transformation Services Market Report Scope

The HR Transformation Services market comprises consulting and managed services that enable organizations to redesign, modernize, and optimize their human resource functions. These services encompass operating model and organizational design, process transformation and reengineering, HR technology transformation, shared services and outsourcing transformation, and workforce analytics with HR data transformation. Delivered to both large enterprises and SMEs, these services are adopted across industries such as BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The primary objective of this market is to help organizations improve HR efficiency, enhance employee experience, ensure compliance, leverage advanced technologies, and align workforce strategies with overall business goals

The HR Transformation Services market report is segmented by Service Type (HR Operating Model and Organizational Design, HR Process Transformation and Reengineering, HR Technology Transformation Services, HR Shared Services and Outsourcing Transformation, Workforce Analytics and HR Data Transformation), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa), The Market Forecasts are Provided in Terms of Value (USD).

| HR Operating Model and Organizational Design |

| HR Process Transformation and Reengineering |

| HR Technology Transformation Services |

| HR Shared Services and Outsourcing Transformation |

| Workforce Analytics and HR Data Transformation |

| Large Enterprises |

| Small And Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Service Type | HR Operating Model and Organizational Design | |

| HR Process Transformation and Reengineering | ||

| HR Technology Transformation Services | ||

| HR Shared Services and Outsourcing Transformation | ||

| Workforce Analytics and HR Data Transformation | ||

| By Enterprise Size | Large Enterprises | |

| Small And Medium Enterprises | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the managed HR services market?

The managed HR services market stood at USD 51.82 billion in 2025 and is projected to reach USD 88.60 billion by 2031, growing at a 9.88% CAGR during 2026-2031.

Which service category leads revenue in managed HR services?

Payroll and benefits administration led the market with a 32.47% revenue share in 2025, supported by the non-discretionary nature of payroll execution and high compliance risk.

Which deployment model is growing the fastest in HR managed services?

Hybrid delivery is the fastest-growing deployment model, with a projected CAGR of 11.72% through 2031, as enterprises balance cloud scale with tighter governance over sensitive employee data.

Why are SMEs becoming important buyers of outsourced HR services?

SMEs are projected to grow at a 13.41% CAGR through 2031 because providers now offer modular and usage-based services that lower contract barriers for smaller organizations.

Which end-user sector is expanding the fastest?

Healthcare and life sciences is forecast to grow at a 14.28% CAGR through 2031, driven by workforce expansion and stricter needs around credentialing, compliance, and workforce recordkeeping.

Which region shows the strongest growth outlook?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 15.36% through 2031, supported by outsourcing adoption in India, China, and Southeast Asia.

Page last updated on: